Global Acetone Market Size, Share, Trends & Growth Forecast Report – Segmented By Application (Methyl Methacrylate, Bisphenol A, Solvents, and other Applications), End User, and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) – Industry Analysis (2026 to 2034)

Global Acetone Market Report Summary

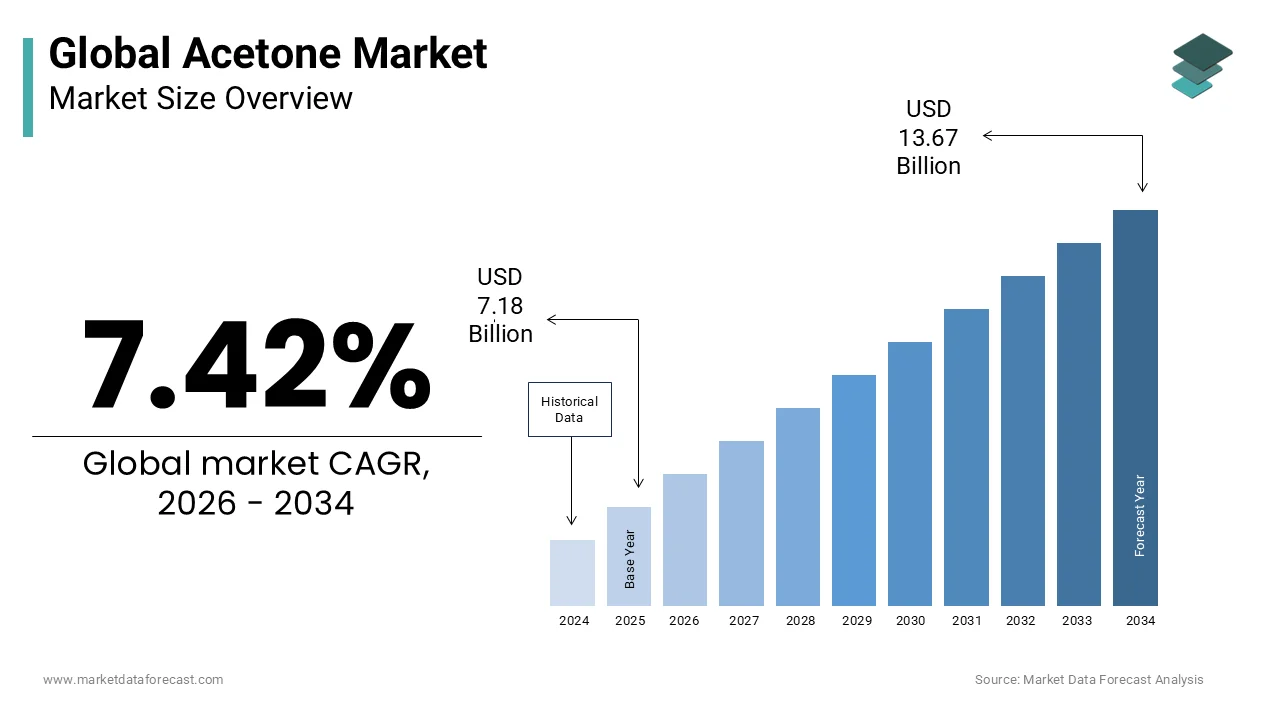

The global acetone market was valued at USD 7.18 billion in 2025, is estimated to reach USD 7.71 billion in 2026, and is projected to reach USD 13.67 billion by 2034, growing at a CAGR of 7.42% during the forecast period. Market growth is driven by increasing demand for solvents, rising applications in plastics and chemical manufacturing, and expanding use in pharmaceuticals and personal care products. Acetone is widely used as a key intermediate in the production of various chemicals and materials due to its high solvency and versatility. The growth of industrial manufacturing and construction sectors is further supporting strong market expansion globally.

Key Market Trends

- Rising demand for solvents in industrial and chemical applications is driving market growth.

- Increasing use in plastics and polymer production is boosting demand.

- Growing applications in pharmaceuticals and personal care products are supporting market expansion.

- Expansion of construction and manufacturing industries is enhancing demand.

- Technological advancements in chemical processing are improving production efficiency.

Segmental Insights

- Based on application, the bisphenol A segment was the largest and dominated the global acetone market in 2025. This dominance is attributed to its extensive use in the production of polycarbonate plastics and epoxy resins.

- Based on end user, the plastics segment led the global acetone market in 2025, driven by high demand for acetone as a precursor in manufacturing polycarbonate and acrylic plastics.

Regional Insights

- The global acetone market is experiencing strong growth across regions, supported by industrial demand and manufacturing expansion.

- Asia Pacific was the largest contributor, accounting for 45.3% of the global acetone market share in 2025, driven by rapid industrialization, strong chemical manufacturing base, and increasing demand for plastics and solvents.

Competitive Landscape

The global acetone market is highly competitive, with key players focusing on production capacity expansion, technological innovation, and supply chain optimization to strengthen their market position. Companies are investing in advanced chemical processing technologies, strategic partnerships, and global distribution networks. Prominent players in the global acetone market include Honeywell International Inc, Dow, Ineos, Formosa Chemicals and Fibre Corp, BASF SE, Mitsui Chemicals Inc, Shell Chemical Co, LG Chem Ltd, Reliance Chemicals Pvt Ltd, and Kumho P and B Chemicals.

Global Acetone Market Size

The global acetone market size was valued at USD 7.18 billion in 2025 and is projected to reach USD 13.67 billion by 2034 from USD 7.71 billion in 2026, growing at a CAGR of 7.42%.

Acetone is a clear, colorless liquid organic compound that is best known for its role as a powerful solvent. Chemically, it is the simplest and smallest member of the ketone family, often referred to by its systematic name, propan-2-one. Primarily produced via the cumene process acetone is integral to the synthesis of methyl methacrylate bisphenol A and various other industrial chemicals. Its applications extend across diverse sectors including pharmaceuticals cosmetics plastics and coatings due to its exceptional solvency and miscibility with water. According to the United States Environmental Protection Agency, acetone is classified as a VOC-exempt solvent because it does not contribute significantly to ground-level ozone formation, and its relatively low toxicity compared to other solvents facilitates its widespread use in consumer products. The market dynamics are heavily influenced by the downstream demand for polycarbonates and acrylics which are essential for construction automotive and electronics industries. As per the American Chemistry Council, the chemical industry in the United States supports more than half a million skilled jobs and contributes significantly to economic output, highlighting the strategic importance of basic chemical intermediates like acetone. Recent trends indicate a shift towards sustainable production methods and bio based alternatives driven by environmental regulations. The International Energy Agency reports that the chemical sector accounts for approximately 10 percent of global energy demand underscoring the need for energy efficient manufacturing processes. Regulatory frameworks such as the European Union’s REACH regulation strictly monitor the handling and emission of chemical substances ensuring safety and environmental protection. This regulatory landscape shapes production standards and drives innovation in green chemistry. The market operates within a complex supply chain where crude oil prices and propylene availability directly impact production costs and profitability.

MARKET DRIVERS

Surging Demand for Polycarbonates in Automotive and Electronics

The surging demand for polycarbonates in the automotive and electronics sectors is a primary driver for the acetone market. This is because acetone is a critical precursor for bisphenol A, which is essential for manufacturing polycarbonate resins. Polycarbonates are valued for their high impact resistance optical clarity and thermal stability making them indispensable in modern vehicle components and electronic devices. According to the International Organization of Motor Vehicle Manufacturers, global vehicle production reached approximately 93 million units in 2024, reflecting a steady recovery and growth in the automotive sector. This increase in production drives the consumption of lightweight materials such as polycarbonates to improve fuel efficiency and meet emission standards. Data from the International Data Corporation (IDC) indicates that shipments of smartphones reached approximately 1.24 billion units globally in 2024, marking a recovery after years of decline. These devices rely heavily on polycarbonate housings and components due to their durability and aesthetic appeal. As per the Plastics Industry Association, the demand for plastic products has grown at an annual rate of approximately 4 percent, driven by urbanization and industrial application. The transition towards electric vehicles further amplifies this trend as manufacturers seek materials that reduce weight while maintaining safety standards. Acetone producers benefit from this downstream growth as the integrated production chains ensure consistent demand. The versatility of polycarbonates in applications ranging from headlamp lenses to bullet proof glass ensures a broad market base. This structural demand from high growth industries sustains the robust consumption of acetone globally.

Expansion of the Pharmaceutical and Personal Care Industries

The expansion of the pharmaceutical and personal care industries is greatly accelerating the growth of the acetone market. This growth is driven by acetone’s wide use as a solvent and cleaning agent in manufacturing drugs, cosmetics, and nail care products. Its ability to dissolve a wide range of organic compounds makes it ideal for synthesizing active pharmaceutical ingredients and formulating topical treatments. According to research, the global pharmaceutical landscape is expected to reach approximately 1.6 trillion dollars by 2025, driven by an aging population and increased healthcare spending. This growth necessitates higher volumes of solvents for drug production and purification processes. Data from the Personal Care Products Council indicates that the beauty and personal care industry in the United States generates over 100 billion dollars in annual revenue, with skin care and hair care products being the most significant contributors. Acetone is the primary ingredient in most nail polish removers due to its effectiveness in breaking down nitrocellulose and other film forming agents. As per the European Cosmetic Toiletry and Perfumery Association the cosmetic industry in Europe employs hundreds of thousands of people and continues to innovate with new formulations that require high purity solvents. The rise of e commerce has made personal care products more accessible globally further boosting demand. Regulatory approvals for acetone in pharmaceutical grades ensure its safety and efficacy in medical applications. The consistent growth in health and wellness sectors provides a stable and recurring demand stream for acetone manufacturers. This diversification beyond industrial applications reduces dependency on single sectors.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

Volatility in raw material prices and supply chain disruptions limit the expansion of the Acetone Market. This creates uncertainty in production costs and availability. Acetone is primarily produced as a co product of phenol in the cumene process which relies on benzene and propylene derived from crude oil and natural gas. According to market data from ICE Brent, crude oil prices fluctuated significantly in 2024, reaching a high near 90 dollars in April before plunging to approximately 70 dollars per barrel by September due to geopolitical tensions and weakening global demand forecasts, particularly from China. These fluctuations directly impact the cost of feedstocks affecting the profitability of acetone producers. Studies indicate that propylene prices have experienced volatility due to maintenance shutdowns and unexpected plant outages in key producing regions like the US Gulf Coast. As per the Federal Reserve Bank of St Louis supply chain bottlenecks continue to affect the chemical industry leading to delays in raw material delivery and increased logistics costs. The interdependence of phenol and acetone markets means that imbalances in demand for one can lead to oversupply or shortage of the other complicating inventory management. Manufacturers face challenges in passing on cost increases to customers due to competitive pressures. Small and medium sized enterprises are particularly vulnerable to these price swings as they lack the hedging capabilities of larger corporations. The unpredictability of input costs makes long term planning difficult and can lead to reduced investment in capacity expansion. This economic instability tests the resilience of market participants and requires agile risk management strategies.

Stringent Environmental Regulations and Safety Standards

Stringent environmental regulations and safety standards further inhibit the expansion of the Acetone Market. This imposes compliance costs and operational restrictions on manufacturers and users. Although acetone is considered less toxic than many other solvents it is still classified as a volatile organic compound and a hazardous air pollutant in many jurisdictions. According to the European Chemicals Agency strict guidelines under the REACH regulation require comprehensive risk assessments and reporting for the handling and disposal of acetone. Data from the United States Environmental Protection Agency indicates that facilities emitting volatile organic compounds must adhere to rigorous monitoring and control measures to minimize atmospheric pollution. As per the Occupational Safety and Health Administration workplace exposure limits for acetone are strictly enforced to protect worker health requiring investments in ventilation systems and protective equipment. Compliance with these regulations increases operational expenses for chemical plants and downstream users. The push for greener alternatives encourages industries to explore bio based or less volatile solvents potentially reducing acetone consumption. Public perception of chemical safety influences regulatory decisions and corporate sustainability goals. Companies must invest in advanced emission control technologies and waste management systems to meet legal requirements. The complexity of navigating varying regulations across different regions adds to the administrative burden. These regulatory pressures can limit market growth and drive up costs for end users. The industry faces the challenge of balancing compliance with competitiveness.

MARKET OPPORTUNITIES

Development of Bio Based Acetone Production Technologies

The development of bio-based acetone production technologies offers a significant opportunity for the Acetone Market. This aligns with the global shift towards sustainability and circular economy principles. Traditional acetone production relies on fossil fuels but emerging biotechnological methods utilize renewable biomass such as corn sugarcane and agricultural waste. According to the Department of Energy and supporting research, bio-based chemicals represent a growing segment of the chemical industry with the potential to reduce greenhouse gas emissions by up to 88 percent or more compared to petroleum-based routes. As per the Journal of Industrial Microbiology and Biotechnology advances in fermentation processes using engineered bacteria such as Clostridium acetobutylicum have improved the yield and efficiency of bio acetone production. These innovations enable the creation of carbon neutral or negative products appealing to environmentally conscious consumers and regulators. Major chemical companies are partnering with biotech firms to scale up pilot plants and commercialize bio acetone. The availability of government grants and incentives for green chemistry further supports this transition. Bio based acetone can serve niche markets in pharmaceuticals and cosmetics where sustainability is a key purchasing criterion. The differentiation provided by eco friendly credentials allows producers to command premium prices. This technological advancement opens new revenue streams and reduces dependence on volatile fossil fuel markets. It positions early adopters as leaders in sustainable chemical manufacturing.

Growth in Emerging Markets and Infrastructure Development

The growth in emerging markets and infrastructure development unlocks potential for the Acetone Market. Rapid urbanization and industrialization are driving demand for construction materials and consumer goods. Countries in Asia Pacific Latin America and Africa are investing heavily in infrastructure projects including roads buildings and transportation networks which require large quantities of plastics and coatings. According to the World Bank, infrastructure investment in developing countries is projected to require approximately $1.5 trillion dollars annually (or 4.5 percent of GDP) by 2030 to support sustainable economic growth. This construction boom increases the consumption of polycarbonates and acrylics derived from acetone. Data from the Asian Development Bank indicates that the middle class in Asia is expanding rapidly leading to higher disposable incomes and increased spending on automobiles electronics and personal care products. As per the United Nations Conference on Trade and Development, while foreign direct investment is a key driver for technology transfer, recent global flows to developing economies have actually declined, posing challenges for capacity building in sectors like chemicals. Local production of acetone and its derivatives is increasing to meet domestic demand and reduce import dependency. Governments are implementing policies to promote local manufacturing and value addition. The untapped potential in these regions offers significant volume growth opportunities for established players. By expanding distribution networks and establishing local partnerships companies can capture market share in these high growth areas. The demographic dividend in emerging markets ensures long term demand stability. This geographic expansion diversifies revenue sources and mitigates risks associated with mature markets.

MARKET CHALLENGES

Fluctuating Demand Dynamics Between Phenol and Acetone

Fluctuating demand dynamics between phenol and acetone constitute a major challenge for the Acetone Market. This is due to their coupled production in the cumene process. Since acetone is produced as a co-product with phenol in a fixed ratio of approximately 0.61 tons of acetone for every ton of phenol, manufacturers cannot adjust acetone output independently based on its specific market demand. According to the American Chemistry Council the demand for phenol is primarily driven by the production of bisphenol A and phenolic resins which may grow at different rates than acetone applications. Data from the Independent Chemical Information Service indicates that periods of high phenol demand can lead to acetone oversupply if the downstream markets for acetone do not absorb the additional volume. Conversely strong acetone demand may be constrained if phenol production is limited. As per multiple sources, this imbalance creates price volatility and margin pressure for producers who must manage inventory and sales strategies for both products simultaneously.The inability to decouple production means that acetone prices are often influenced by phenol market conditions rather than its own supply demand fundamentals. This structural constraint complicates pricing strategies and financial planning. Manufacturers may need to export excess acetone or store it during periods of low demand incurring additional costs. The market must constantly adapt to these inherent production linkages. This challenge requires sophisticated market intelligence and flexible logistics to optimize profitability.

Competition from Alternative Solvents and Recycling Initiatives

Competition from alternative solvents and recycling initiatives holds back the growth of the Acetone Market. This occurs as industries seek to reduce environmental impact and operational costs. Various green solvents such as ethyl lactate dimethyl carbonate and supercritical carbon dioxide are gaining traction as substitutes for traditional volatile organic compounds in cleaning and extraction processes. According to the Green Chemistry Institute these alternatives offer lower toxicity and better biodegradability appealing to companies with strict sustainability mandates. As per the Ellen MacArthur Foundation the push towards a circular economy encourages the recycling and recovery of solvents including acetone reducing the need for virgin material. Advanced distillation and purification technologies enable facilities to reuse acetone multiple times extending its lifecycle and lowering procurement costs. Regulatory pressures to minimize waste and emissions further drive the adoption of closed loop systems. The development of water based coatings and adhesives also reduces the reliance on organic solvents like acetone. Manufacturers face the challenge of demonstrating the superior performance and cost effectiveness of acetone against these emerging alternatives. The shift towards solvent free technologies in certain applications further threatens market volume. This competitive landscape requires continuous innovation and value proposition refinement. The industry must adapt to changing preferences and regulatory landscapes to maintain relevance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.42% |

| Segments Covered | By Application, End User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Honeywell International Inc. (US), Dow (US), Ineos (UK), Formosa Chemicals & Fibre Corp (Taiwan), BASF SE (Germany), Mitsui Chemicals Inc (Japan), Shell Chemical Co (US), LG Chem Ltd (South Korea), Reliance Chemicals Pvt Ltd (India), Kumho P&B Chemicals (Korea). |

SEGMENTAL ANALYSIS

By Application Insights

The Bisphenol A (BPA) segment dominated the Acetone Market in 2025. This dominance of the segment is driven by the extensive use of BPA in the manufacturing of polycarbonate plastics and epoxy resins which are essential for various industrial applications. It serves as the primary derivative, consuming approximately 65 to 70 percent of global acetone production. The spearheading of the Bisphenol A segment is mainly supported by the robust demand for polycarbonate plastics in the construction, automotive, and electronics industries. Polycarbonates are valued for their high impact resistance transparency and thermal stability making them ideal for applications such as glazing materials automotive components and electronic housings. According to the International Organization of Motor Vehicle Manufacturers, global vehicle production exceeded 92.5 million units in 2024, creating substantial demand for lightweight and durable materials like polycarbonate. As per the American Chemistry Council, the construction sector accounts for a significant portion of polycarbonate consumption, particularly in energy-efficient building envelopes and safety glazing. The transition towards electric vehicles further amplifies this trend as manufacturers seek materials that reduce vehicle weight to enhance battery efficiency. Acetone producers benefit directly from this downstream growth since BPA production is inextricably linked to acetone availability. The integrated nature of these supply chains ensures consistent demand for acetone as long as polycarbonate production remains strong. This structural dependency cements the leading position of the BPA segment in the acetone market landscape. The expansion of epoxy resin applications significantly contributes to the market leadership of the Bisphenol A segment as epoxy resins are widely used in coatings adhesives composites and electrical insulation. BPA is a key raw material in the synthesis of epoxy resins which offer superior adhesion chemical resistance and mechanical strength. Data from the Global Wind Energy Council indicates that new wind turbine installations require large quantities of epoxy based composites for blade manufacturing due to their lightweight and high strength properties. As per the European Coatings Journal the protective coatings industry heavily relies on epoxy resins for corrosion protection in infrastructure and industrial facilities. The rise in offshore wind farms and infrastructure rehabilitation projects further boosts demand. Acetone consumption is sustained by this diverse application base which spans multiple high growth industries. The versatility of epoxy resins allows them to be used in everything from aerospace components to consumer electronics. This broad utility ensures that fluctuations in one sector can be offset by stability in another. The continuous innovation in epoxy formulations also drives the need for high purity BPA and consequently acetone. This multifaceted demand supports the sustained dominance of the BPA segment.

The Methyl Methacrylate (MMA) segment is estimated to register the fastest CAGR of 5.8% from 2026 to 2034 due to increasing demand for polymethyl methacrylate (PMMA) in automotive lighting signage and medical devices. MMA is a critical intermediate produced using acetone and hydrogen cyanide or other routes. This rapid growth of the segment is fueled by the growing adoption of polymethyl methacrylate in automotive lighting and glazing applications due to its excellent optical clarity and weather resistance. Automakers are increasingly using PMMA for headlamp lenses tail lights and interior components to achieve sleek designs and improve energy efficiency. According to S&P Global, global automotive production is projected to fall by 0.9% in 2026 to 14 million units, while OICA data shows that regional production, particularly in Europe, remains significantly below 2019 levels. As per the European Automobile Manufacturers Association (ACEA), regulatory focus is currently on the "Weights and Dimensions Directive," which seeks to grant additional weight allowances for zero-emission vehicles to facilitate the transition to climate neutrality by 2050. The rise of electric vehicles further accelerates this trend as designers seek innovative lighting solutions that integrate with aerodynamic shapes. Acetone is a key feedstock in certain MMA production processes linking its demand to this automotive shift. The durability of PMMA ensures long term performance reducing maintenance costs for consumers. This alignment with automotive innovation trends drives sustained growth for the MMA segment. The expanding middle class in emerging markets also increases car ownership rates further boosting demand. The expansion in medical device and healthcare applications significantly accelerates the growth of the Methyl Methacrylate segment as PMMA is widely used in bone cements intraocular lenses and dental prosthetics. The aging global population and increasing prevalence of chronic diseases drive the demand for advanced medical treatments and devices. According to the World Health Organization the number of people aged 60 years and older is expected to double by 2050 reaching 2.1 billion globally. This demographic shift increases the need for orthopedic surgeries and ophthalmic procedures where PMMA plays a crucial role. The biocompatibility and transparency of PMMA make it ideal for these sensitive applications. Acetone producers benefit from this specialized demand which is less susceptible to economic cycles than industrial applications. Regulatory approvals for medical grade PMMA ensure high standards and consistent quality. The continuous innovation in minimally invasive surgical techniques further expands the use of PMMA based devices. This healthcare driven growth provides a stable and expanding market for MMA and its precursor acetone.

By End User Insights

The Plastic end user segment led the Acetone Market in 2025 because acetone is a fundamental precursor for producing bisphenol A and methyl methacrylate, which are essential for manufacturing polycarbonate and acrylic plastics. These plastics are ubiquitous in modern life. The leading position of the Plastic segment is largely attributed to the ubiquity of polycarbonate in consumer goods ranging from water bottles and food containers to electronic casings and eyewear. Polycarbonate offers a unique combination of strength clarity and heat resistance that few other materials can match. According to the Plastics Industry Association the global production of engineering plastics continues to rise with polycarbonate being a major contributor. As per the Consumer Technology Association the shipment of billions of electronic devices annually requires durable and lightweight plastic housings often made from polycarbonate. The convenience and durability of plastic products drive consistent consumer demand. Acetone is integral to this supply chain as it is converted into BPA for polycarbonate production. The versatility of polycarbonate allows it to be used in diverse applications ensuring broad market reach. Recycling initiatives are improving the sustainability profile of plastics enhancing their acceptance. The cost effectiveness of plastic manufacturing compared to glass or metal further supports its dominance. This widespread usage across multiple consumer categories sustains the leading position of the plastic segment. The extensive industrial applications of acrylics significantly contribute to the market leadership of the Plastic segment as acrylic sheets and molds are used in construction signage and automotive parts. Acrylics derived from methyl methacrylate offer superior weatherability and optical properties. As per the Sign Industry Magazine the advertising and signage sector relies heavily on acrylics for illuminated signs and displays which require high light transmission. The automotive industry uses acrylics for instrument panels and exterior trim. Acetone is a key raw material in the production of MMA which is polymerized to form acrylics. The growth in urbanization and infrastructure development drives the consumption of these materials. The ability of acrylics to be molded into complex shapes adds to their appeal. Industrial users value the long service life and low maintenance requirements of acrylic products. This robust industrial demand ensures that the plastic segment remains the largest consumer of acetone.

The Electrical & Electronics segment is anticipated to witness the fastest CAGR of 6.2% during the forecast period owing to the miniaturization of devices and the need for high performance insulating materials. Acetone is used in the production of components and as a cleaning solvent. The swift growth of the Electrical & Electronics segment is fueled by the proliferation of smart devices and the rollout of 5G infrastructure which require advanced materials for circuit boards and enclosures. Polycarbonates and other acetone derived plastics are essential for these applications due to their dielectric properties and heat resistance. According to sources, the number of mobile broadband subscriptions is expected to reach 9 billion by 2028, while ITU data emphasizes that nearly three-quarters of the global population is now connected. Data from the Semiconductor Industry Association shows that global semiconductor sales continue to grow supporting the production of electronic components. As per research, the deployment of 5G networks requires significant new infrastructure like base stations; separately, material science experts note these components increasingly utilize high-performance plastics for stable RF quality. Acetone is used in the manufacturing process of these components and as a solvent for cleaning precision parts. The miniaturization of electronics demands materials that can withstand higher densities and temperatures. The Internet of Things expansion further increases the number of connected devices. This technological evolution creates a sustained demand for specialized plastics and solvents. The high value added nature of electronic components supports investment in advanced materials. This sector's dynamic growth outpaces traditional industries. The demand for high performance insulating materials significantly accelerates the growth of the Electrical & Electronics segment as power distribution and renewable energy systems require reliable insulation. Epoxy resins derived from BPA an acetone derivative are widely used for encapsulating and insulating electrical components. According to the International Energy Agency investment in power grids is increasing to support the integration of renewable energy sources. Data from the National Electrical Manufacturers Association indicates that the demand for transformers and switchgear is rising driven by grid modernization efforts. Acetone based epoxies provide the necessary thermal and electrical stability. The expansion of electric vehicle charging infrastructure also drives demand for insulated cables and connectors. The reliability of these materials is critical for preventing failures and ensuring safety. Regulatory standards for electrical safety mandate the use of high quality insulating materials. This focus on reliability and performance drives the adoption of acetone derived products. The growth in renewable energy and electrification ensures long term demand. This sector represents a high growth opportunity for acetone producers.

REGIONAL ANALYSIS

Asia Pacific Snack Product Market Analysis

Asia Pacific outperformed other regions in the global Acetone Market and occupied a 45.3% share in 2025. This supremacy of the segment is credited to rapid industrialization and a massive manufacturing base for plastics and electronics. The region is the global hub for chemical production. Moreover, the Asia Pacific market is characterized by strong demand from China India and Southeast Asian countries where construction and automotive sectors are booming. According to the Asian Development Bank the region’s GDP growth remains robust supporting infrastructure development. Data from the Chinese Petroleum and Chemical Industry Federation indicates that China is the world’s largest producer and consumer of acetone and its derivatives. According to the Indian Ministry of Chemicals and Fertilizers, the Indian chemical industry is growing at a CAGR of approximately 9.3 percent, driven by government initiatives like Make in India and PLI schemes. The presence of major electronics manufacturers in South Korea Japan and Taiwan drives demand for high purity acetone. Urbanization rates are increasing leading to higher consumption of construction materials. The region benefits from favorable government policies and investment in chemical parks. Supply chain integration within the region enhances efficiency. The growing middle class drives demand for consumer goods made from plastics. Environmental regulations are becoming stricter prompting investments in cleaner technologies. These factors collectively sustain Asia Pacific’s leadership in the global acetone market.

North America Snack Product Market Analysis

North America was the second largest region in the global Acetone Market and captured a share of 20.7% share in 2025. This prominence of the North American market is credited to a mature chemical industry and strong demand from the automotive and healthcare sectors. The United States is a key producer. The North American market is distinguished by advanced technology and strict environmental regulations that drive innovation in sustainable production. According to the American Chemistry Council, the US chemical industry is a major global exporter of chemical products, particularly plastic resins and basic chemicals, though it remains a competitive player in the broader acetone derivatives market. Data from the US Department of Commerce indicates that trade agreements facilitate the export of chemical products to global markets. As per Federal Reserve Economic Data, industrial production in the manufacturing sector has shown fluctuating growth, with recent output remaining essentially flat amid shifting demand and economic uncertainty. The shale gas boom has provided cost competitive feedstocks for chemical production. The healthcare sector’s growth drives demand for pharmaceutical grade acetone. The automotive industry’s shift towards electric vehicles creates new opportunities for lightweight plastics. Regulatory frameworks like TSCA ensure safety and compliance. Investment in research and development leads to new applications. The region’s infrastructure supports efficient distribution. These structural advantages maintain North America’s strong position.

Europe Snack Product Market Analysis

Europe is another key player in the global Acetone Market owing to stringent environmental standards and a focus on high value applications. The region prioritizes sustainability and circular economy principles. In addition, the European market is influenced by the REACH regulation which mandates safe handling of chemicals promoting the adoption of greener processes. According to the European Chemical Industry Council the industry is investing in bio based alternatives. Data from Eurostat indicates that the manufacturing sector in Germany and France drives significant demand. As per the European Automobile Manufacturers Association the transition to electric vehicles supports demand for advanced plastics. The construction industry’s focus on energy efficiency boosts demand for insulation materials. The region is a leader in recycling technologies reducing waste. High labor costs drive automation and efficiency. Trade policies impact import and export dynamics. The focus on sustainability drives innovation in product formulations. These factors shape the European market landscape.

Middle East and Africa Snack Product Market Analysis

The Middle East and Africa region is moving ahead steadfastly in the global Acetone Market owing to abundant raw material resources and growing industrialization. The region is expanding its downstream capabilities. Besides these, the Middle East market benefits from low cost feedstocks derived from oil and gas production supporting competitive chemical manufacturing. According to the Gulf Petrochemicals and Chemicals Association capacity expansions are underway in Saudi Arabia and Qatar. Data from the African Development Bank indicates that infrastructure investment is driving demand in Africa. As per the Saudi Arabian Ministry of Industry and Mineral Resources the kingdom aims to localize chemical production. The growing population drives demand for consumer goods. Political stability in key countries supports investment. Logistics improvements enhance distribution. The region is becoming a net exporter of chemicals. These dynamics position the region for growth.

Latin America Snack Product Market Analysis

Latin America is anticipated to expand significantly in the global Acetone Market over the forecast period owing to economic recovery and increasing demand from the automotive and packaging industries. Brazil and Mexico are key markets. The Latin American market is influenced by economic fluctuations but shows resilience in key sectors. : According to the Economic Commission for Latin America and the Caribbean, the region is facing a "prolonged period of low growth" with structural challenges limiting industrial dynamism. Data from the Brazilian Chemical Industry Association (Abiquim) indicates a contraction in the chemical sector, with domestic demand for chemicals decreasing by 1.5% and capacity utilization hitting a historical low of 64%. As per the Mexican Ministry of Economy the automotive sector drives demand for plastics. Urbanization supports construction activity. Trade agreements with North America facilitate commerce. Investment in local production reduces import dependency. The region offers growth potential as economies stabilize. These factors contribute to market development.

COMPETITIVE LANDSCAPE

The competition in the Europe snack product market is intense and characterized by the presence of established multinational corporations alongside emerging artisanal brands. Major players leverage their extensive distribution networks and strong brand recognition to maintain dominance while smaller competitors focus on niche segments such as organic gluten free or vegan options. Innovation serves as a key differentiator with companies continuously launching new flavors and healthier formulations to attract health conscious consumers. Price competition remains significant particularly in the mass market segment where private label products from major retailers pose a substantial threat to branded items. Sustainability has become a critical competitive factor as consumers increasingly prefer brands with transparent and ethical supply chains. Regulatory pressures regarding sugar content and labeling further shape competitive dynamics forcing companies to reformulate products. Digital marketing and e commerce capabilities are essential for reaching broader audiences and enhancing customer engagement. The market sees frequent strategic alliances and acquisitions as firms seek to expand their portfolios and geographic reach. This dynamic environment requires constant adaptation and investment in technology and sustainability to sustain competitive advantage and meet evolving consumer demands effectively.

Key Market Players

The major key players in the global acetone market are

- Honeywell International Inc.

- Dow

- Ineos

- Formosa Chemicals & Fibre Corp

- BASF SE

- Mitsui Chemicals Inc

- Shell Chemical Co

- LG Chem Ltd

- Reliance Chemicals Pvt Ltd

- Kumho P&B Chemicals

Top Players in the Market

- Ineos Phenol GmbH is a leading global producer of phenol and acetone with extensive manufacturing capabilities across Europe Asia and North America. The company leverages its integrated production sites to ensure cost efficiency and reliable supply chains for downstream customers. Ineos recently invested in upgrading its facilities to enhance energy efficiency and reduce carbon emissions aligning with sustainability goals. It focuses on long term contracts with key clients in the polycarbonate and epoxy resin sectors to secure stable demand. The corporation actively participates in industry initiatives promoting responsible care and safety standards. Ineos also explores innovations in catalyst technology to improve yield and product purity. These strategic actions strengthen its market position by ensuring operational excellence and meeting evolving regulatory requirements while maintaining competitive pricing structures for global clients.

- Sunoco LP is a major player in the global acetone market operating large scale cumene phenol and acetone production facilities primarily in the United States. The company benefits from access to low cost raw materials and strategic locations near key demand centers. Sunoco recently optimized its production processes to increase flexibility and responsiveness to market fluctuations. It focuses on providing high quality products to diverse industries including plastics pharmaceuticals and solvents. The corporation invests in maintenance and reliability programs to minimize unplanned downtime and ensure consistent supply. Sunoco also engages in strategic partnerships with logistics providers to enhance distribution efficiency. These efforts reinforce its reputation as a dependable supplier and help it capture opportunities in growing end use segments. The company continues to evaluate expansion options to meet future demand trends effectively.

- Mitsui Chemicals Inc. is a significant contributor to the global acetone market with a strong presence in Asia and expanding operations globally. The company produces acetone as part of its integrated phenol value chain serving various industrial applications. Mitsui Chemicals recently announced plans to expand its production capacity in Singapore to cater to growing demand in the Asia Pacific region. It emphasizes innovation and sustainability by developing advanced materials and eco friendly processes. The corporation collaborates with customers to create tailored solutions for specific application needs. Mitsui Chemicals also invests in research and development to improve process efficiency and reduce environmental impact. These initiatives enhance its competitive edge and support long term growth in key markets. The company remains committed to delivering value through high performance products and reliable service.

Top Strategies Used by the Key Market Participants

Key players in the Europe Snack Product Market primarily employ product innovation and premiumization strategies to differentiate their offerings. Companies invest heavily in research and development to create unique flavors and healthier formulations such as reduced sugar or organic variants. Sustainability initiatives form another core strategy with firms focusing on ethical sourcing of cocoa and eco friendly packaging solutions to meet regulatory standards and consumer expectations. Digital transformation is crucial as brands enhance their e commerce presence and utilize data analytics for personalized marketing. Strategic partnerships and collaborations with retailers ensure optimal shelf placement and visibility. Mergers and acquisitions allow companies to expand their portfolios and enter new niche segments. Brands also leverage influencer marketing and social media campaigns to engage younger demographics and build brand loyalty. These multifaceted approaches help participants navigate competitive pressures and adapt to evolving consumer preferences while maintaining profitability and market relevance in the dynamic European landscape.

MARKET SEGMENTATION

This research report on the global acetone market has been segmented and sub-segmented based on application, end-user, and region.

By Application

- Solvent

- Bisphenol A (BPA)

- Methyl Methacrylate (MMA)

- Others

By End User

- Paints & Coatings

- Plastic

- Automotive

- Adhesives

- Pharmaceuticals

- Cosmetics

- Electrical & Electronics

- Others

By Country

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1.What is the acetone market?

The acetone market comprises the production, distribution, and consumption of acetone, a volatile organic solvent widely used in chemical manufacturing and industrial applications.

2.What are the key growth drivers of the acetone market?

Growth is driven by increasing demand for methyl methacrylate and bisphenol A production, expansion of paints and coatings, and rising pharmaceutical and cosmetics consumption.

3.What are the primary applications of acetone?

Major applications include solvents in paints and coatings, adhesives, pharmaceuticals, cosmetics, and as a chemical intermediate in plastics production.

4.Which end use industry dominates the acetone market?

The chemical industry dominates due to acetone use in producing methyl methacrylate and bisphenol A for polycarbonate and epoxy resins.

5.How is acetone produced?

Acetone is primarily produced as a byproduct of phenol manufacturing through the cumene process.

6.What role does acetone play in the pharmaceutical industry?

It is used as a solvent in drug formulation and as a cleaning agent in pharmaceutical manufacturing processes.

7.How does the construction sector influence acetone demand?

The construction sector supports demand through increased use of paints, coatings, sealants, and adhesives.

8.What are the environmental concerns associated with acetone?

Acetone is highly volatile and flammable, and strict regulations govern its storage, transportation, and emissions control.

9.Which regions are major consumers of acetone?

Asia Pacific leads consumption due to strong chemical manufacturing, while North America and Europe maintain significant demand.

10.What challenges does the acetone market face?

Key challenges include raw material price volatility, environmental regulations, and fluctuating demand from downstream industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com