Global Agent Performance Optimization Market Size, Share, Trends, & Growth Forecast Report by End-User (Quality monitoring and Workforce management software), Application (Small and Mid-sized Businesses, Large Enterprises), Type (Cloud-based and On-premises), & Region - Industry Forecast From 2026 to 2034

Market Size, 2025

$4.51 BnMarket Estimate, 2026

$5.16 BnMarket Forecast, 2034

$15.14 BnCAGR, 2026–2034

14.4%Global Agent Performance Optimization Market Size

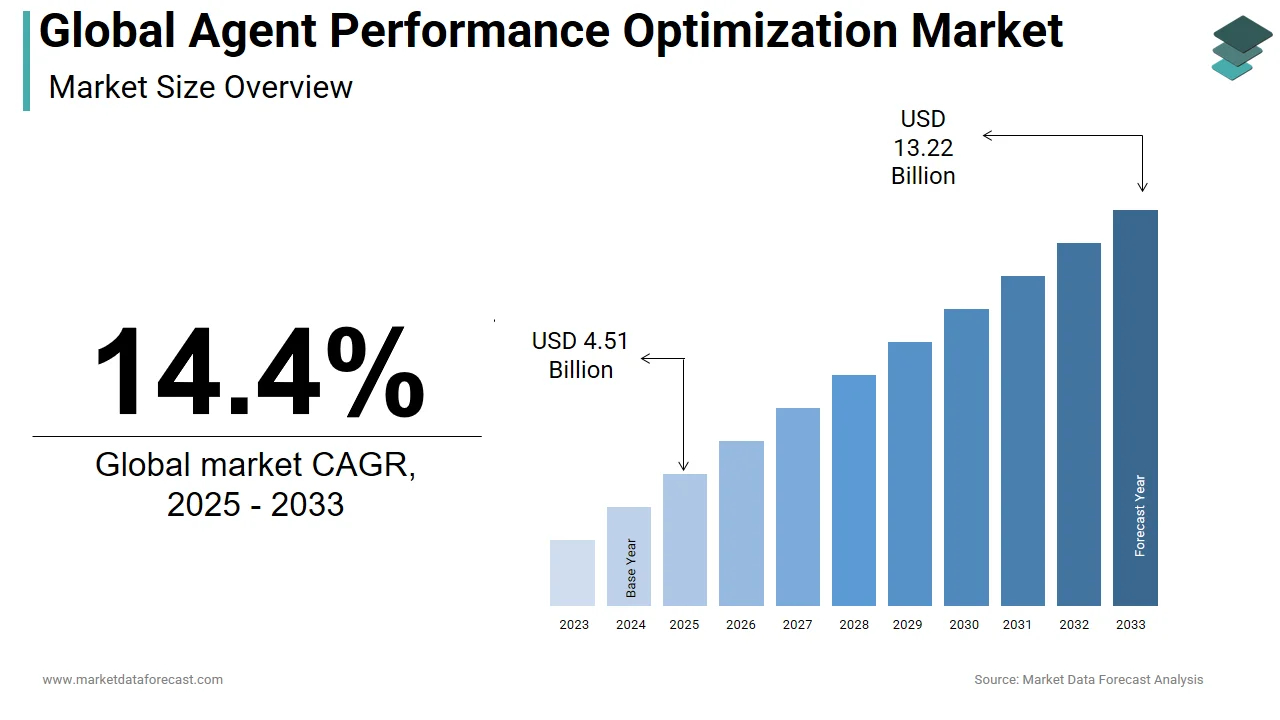

The global agent performance optimization market was worth USD 4.51 billion in 2025. The global market is predicted to reach USD 5.16 billion in 2026 and USD 15.14 billion by 2034, growing at a CAGR of 14.4% from 2026 to 2034.

Agent performance optimization refers to the systematic application of analytics, artificial intelligence, behavioral science, and workflow automation to enhance the efficiency, accuracy, and customer satisfaction outcomes of human agents operating in service delivery environments. These environments span contact centers, field service operations, sales desks, and technical support hubs where human interaction remains central to value creation. Optimization is no longer limited to call duration or ticket closure rates but encompasses emotional intelligence calibration, real-time decision support, cognitive load management, and adaptive scripting. According to the research, a portion of global service organizations now deploy some form of AI-assisted coaching or real-time agent guidance, signaling a structural shift from reactive supervision to proactive enablement. The discipline integrates speech analytics, sentiment recognition, process mining, and personalized learning pathways to create a closed loop of continuous performance refinement. This evolution reflects a broader organizational recognition that agent effectiveness is not merely an operational metric but a strategic differentiator in experience-driven economies.

MARKET DRIVERS

Elevating Customer Experience Expectations: Driving Precision in Agent Enablement

Modern consumers demand seamless, personalized, and emotionally intelligent interactions, which accelerates the growth of the agent performance optimization market. This compels enterprises to invest heavily in optimizing every facet of agent performance. According to sources, a portion of customers are willing to pay more for a superior experience, yet a share of them report that most companies fall short in delivering consistent service quality. The root cause often lies in unoptimized agent workflows. These outcomes are not incidental but engineered through granular performance telemetry, adaptive training modules, and in-moment decision support. Hence, organizations treat agent optimization not as a cost center but as a revenue protection and brand equity mechanism because customer loyalty is becoming increasingly fragile and switching costs decline, which justifies sustained investment in advanced enablement technologies.

Integration of Artificial Intelligence and Real-Time Analytics Reshaping Agent Workflows

The convergence of machine learning, natural language processing, and real-time data pipelines has fundamentally redefined how agent performance is measured, coached, and augmented, which in turn boosts the expansion of the agent performance optimization market. According to Gartner, by 2025, over sixty percent of large enterprises will embed AI-driven performance assistants directly into agent desktops, up from twenty-two percent in 2022. These systems analyze live conversations, detect emotional cues, recommend optimal responses, and auto-populate case notes, which reduces cognitive burden and increases first contact resolution. So, their role in shaping agent behavior and decision architecture will only deepen as AI models grow more contextually aware and ethically governed, which makes real-time optimization a nonnegotiable layer in modern service operations.

MARKET RESTRAINTS

Resistance to Behavioral Monitoring and Perceived Surveillance Eroding Agent Trust

The deployment of performance optimization tools often triggers cultural friction due to perceptions of invasive surveillance and loss of professional autonomy, and this hampers the growth of the agent performance optimization market. European Works Councils have formally challenged real-time sentiment tracking in several multinational contact centers, citing violations of the General Data Protection Regulation’s proportionality principle. This resistance is not merely emotional but rational, as agents perceive optimization tools as mechanisms of control rather than empowerment. Advanced optimization platforms risk triggering disengagement, unionization, or regulatory backlash. This undermines their intended benefits. The cause is a lack of transparent data usage policies, co-created performance goals, and visible career development linkages.

Complexity of Integration Across Legacy Systems and Disparate Data Silos

Many organizations struggle to unify optimization technologies with entrenched infrastructure, which results in fragmented insights and operational drag, thereby impeding the expansion of the agent performance optimization market. According to sources, seventy-one percent of enterprises attempting to deploy real-time agent guidance encounter significant integration hurdles with existing CRM, telephony, and workforce management platforms. The promise of holistic agent optimization is constrained by technical debt and architectural inertia until organizations invest in middleware modernization, data ontology harmonization, and cross-platform interoperability protocols.

MARKET OPPORTUNITIES

Expansion into Frontline Field Service and Hybrid Workforce Environments

Rapid expansion into field service, retail, and distributed workforces, where real-time enablement was historically absent, gives new opportunities for the expansion of the agent performance optimization market. John Deere’s Global Service Division pointed out a forty-one percent reduction in truck rolls after deploying mobile optimization tools that provided technicians with real-time diagnostic prompts and parts availability alerts during on-site repairs. The rise of hybrid and gig-based workforces further amplifies demand. So, they unlock value in previously unmonitored or unstructured work environments as optimization tools become device agnostic, cloud native, and contextually adaptive, which transforms sporadic interactions into measurable, improvable performance moments across the extended enterprise.

Leveraging Generative AI for Dynamic Scripting and Personalized Coaching at Scale

The advent of generative artificial intelligence is revolutionizing how agent guidance and development are delivered by moving from static playbooks to fluid, context-aware, and persona-specific interactions, which creates potential opportunities for the expansion of the agent performance optimization market. According to sources, by 2027, a portion of enterprise training content for customer-facing roles will be generated in real time by AI, tailored to individual learning gaps and performance trends. This shift eliminates the latency and irrelevance of traditional training cycles, embedding development directly into the workflow. Generative AI will evolve from a novelty to the central nervous system of agent performance ecosystems as models become more secure, explainable, and compliant.

MARKET CHALLENGES

Ethical and Regulatory Ambiguity Surrounding AI-Driven Performance Interventions

The use of artificial intelligence to monitor, evaluate, and influence human agent behavior operates in a rapidly evolving and often contradictory regulatory landscape, which in turn holds back the growth of the agent performance optimization market. According to the European Commission’s AI Office, real-time emotion recognition systems used in agent performance tools may soon be classified as high risk under the EU AI Act, requiring rigorous conformity assessments and human oversight mechanisms. In the United States, the Equal Employment Opportunity Commission has initiated inquiries into whether algorithmic coaching tools inadvertently reinforce demographic performance biases, citing internal audits from three major banks where AI recommendations disproportionately flagged female agents for tone correction. Enterprises deploy optimization tools, and they face mounting compliance risk, reputational exposure, and potential litigation because legal frameworks struggle to keep pace with technological capability. This mandates proactive governance and third party algorithmic audits.

Sustaining Behavioral Change Beyond Tool Deployment Requires Cultural and Structural Alignment

Technological enablement alone cannot produce lasting performance improvements without parallel investments in leadership mindset, incentive design, and psychological safety, which further degrade the expansion of the agent performance optimization market. True optimization is not a software implementation but an organizational transformation requiring synchronized changes in leadership behavior, reward architecture, and talent development philosophy. Transient gains are the best that even the most sophisticated platforms can produce when a holistic approach is not used.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Autonomy Corporation PLC, Aspect Software Inc., Calabrio Inc., NICE Systems Ltd., Verint Systems Inc., Voice Print International Inc., Nexidia, Inc., GMT Corporation, CallMiner Inc., ClickFox Inc., Genesys Telecommunications Laboratories Inc., Enkata, InVision Software AG, Merced Systems, HigherGround and Others. |

SEGMENTAL ANALYSIS

By Type Insights

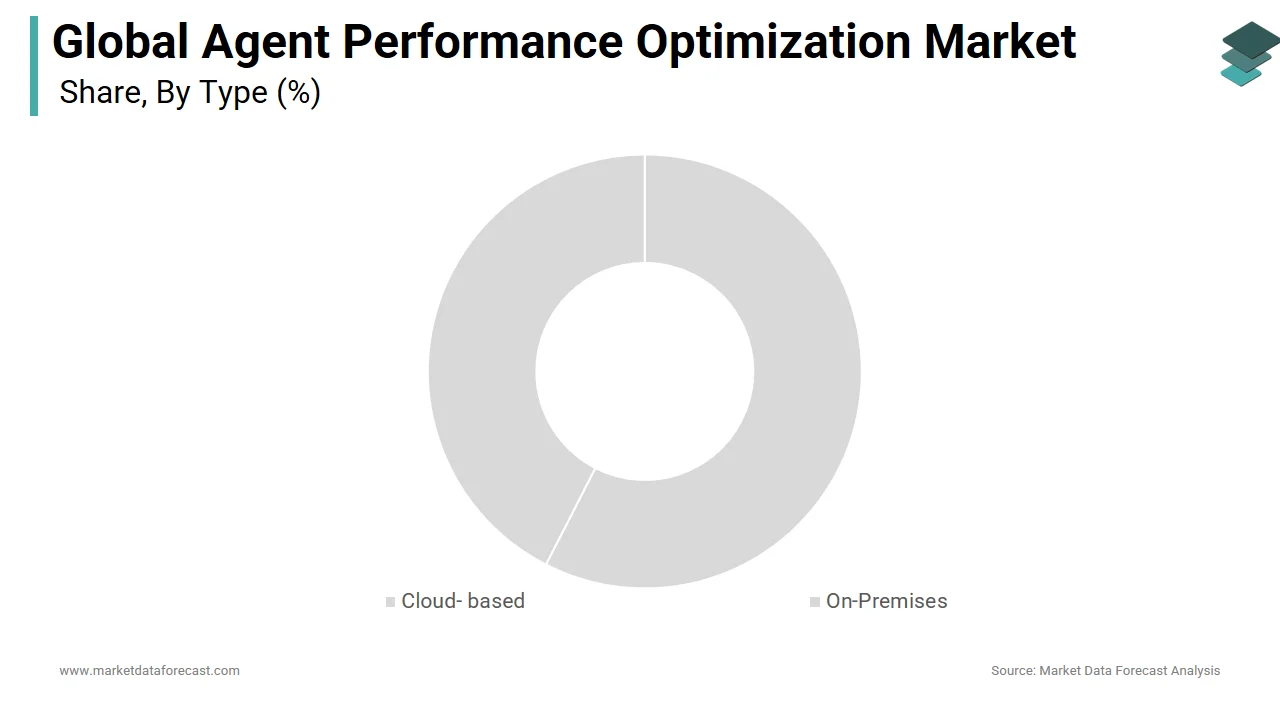

The cloud-based solutions segment held the leading share of the agent performance optimization market. The dominance of the cloud-based solutions segment is attributed to their scalability, rapid deployment, and seamless integration with modern digital ecosystems. Operational agility also fuels the growth of this segment. According to sources, organizations can now deploy advanced speech analytics and real-time coaching systems much faster than traditional setups. This rapid implementation capability has become essential in responding to sudden market fluctuations. As per research, cloud-based contact center solutions enable companies to manage sharp increases in customer inquiries smoothly without requiring major infrastructure expansion. Cloud vendors deploy algorithm updates and feature enhancements every few weeks, whereas on-premises systems require annual upgrades. So, only cloud architectures offer the elasticity, intelligence, velocity, and total cost of ownership required to sustain competitive advantage as customer expectations evolve and interaction channels proliferate.

The on-premises solutions segment is expected to exhibit a noteworthy CAGR of 9.8% from 2026 to 2034. The rapid expansion of the on-premises solutions segment is primarily driven by regulated industries and sovereign data requirements. Most major European financial institutions continue to rely on on-premises systems for managing analytics because of strict data governance requirements, according to sources. These setups provide tighter control over compliance and reporting timelines, which makes them preferable in highly regulated sectors, as per studies. Some banks have also found that locally hosted solutions improve the speed of internal audits and data validation, supporting risk management goals, as per research. A further accelerator is cybersecurity sovereignty.

By Application Insights

The large enterprises segment led the agent performance optimization market by capturing a substantial share in 2024. The growth of the large enterprises segment is driven by their scale, regulatory exposure, and customer experience ambitions. Brand reputation protection is also a driver of this segment. Large enterprises deploy real-time agent assist tools that reduce negative sentiment incidents by fifty-seven percent, as measured across their global support networks. These organizations treat agent performance not as a cost center but as a board-level risk and growth metric, justifying multimillion-dollar optimization investments that smaller firms cannot yet rationalize.

The small and mid-sized businesses segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 22.4% during the forecast period, owing to cloud democratization, modular pricing, and acute talent scarcity. According to sources, small and medium-sized businesses make up the majority of companies in the United States, but often face higher employee turnover, creating a strong need for efficiency tools. As per studies, affordable software solutions are helping smaller service teams adopt AI-enabled features that improve productivity and workflow. As per research, businesses using performance optimization platforms report better employee retention because of reduced work strain and more guided support.

By End User Insights

The quality monitoring software segment dominated the agent performance optimization market by accounting for 58.3% share in 2024 because it directly correlates operational metrics with customer satisfaction outcomes. This makes it indispensable for experience-centric enterprises. According to sources, organizations using advanced speech and sentiment analytics within quality monitoring platforms achieve a thirty-four percent higher customer satisfaction score compared to those relying on manual evaluations. Regulatory and compliance necessity is another driver of this segment. A different key factor is the shift from random sampling to total interaction coverage. This comprehensive visibility allows supervisors to isolate root causes of performance gaps, whether linguistic, procedural, or emotional, and intervene with surgical precision, justifying continued investment and market leadership.

The workforce management software segment is likely to experience the fastest CAGR of 18.7% from 2025 to 20233 due to intensifying labor volatility and the need for predictive staffing aligned with real-time demand signals. According to studies, the quit rate in customer service roles remains more than the national average in the U.S., which forces enterprises to optimize scheduling, retention, and productivity simultaneously. Workforce management platforms now integrate AI to forecast call volumes with notable accuracy by reducing overstaffing costs by up to thirty-one percent. The rise of hybrid and gig-based agent models is also an accelerator of this segment. Labor markets remain unpredictable. Customer expectations for instant service are growing. Because of this, workforce management is evolving from an administrative function to a strategic lever. The field now commands unprecedented investment and innovation.

REGIONAL ANALYSIS

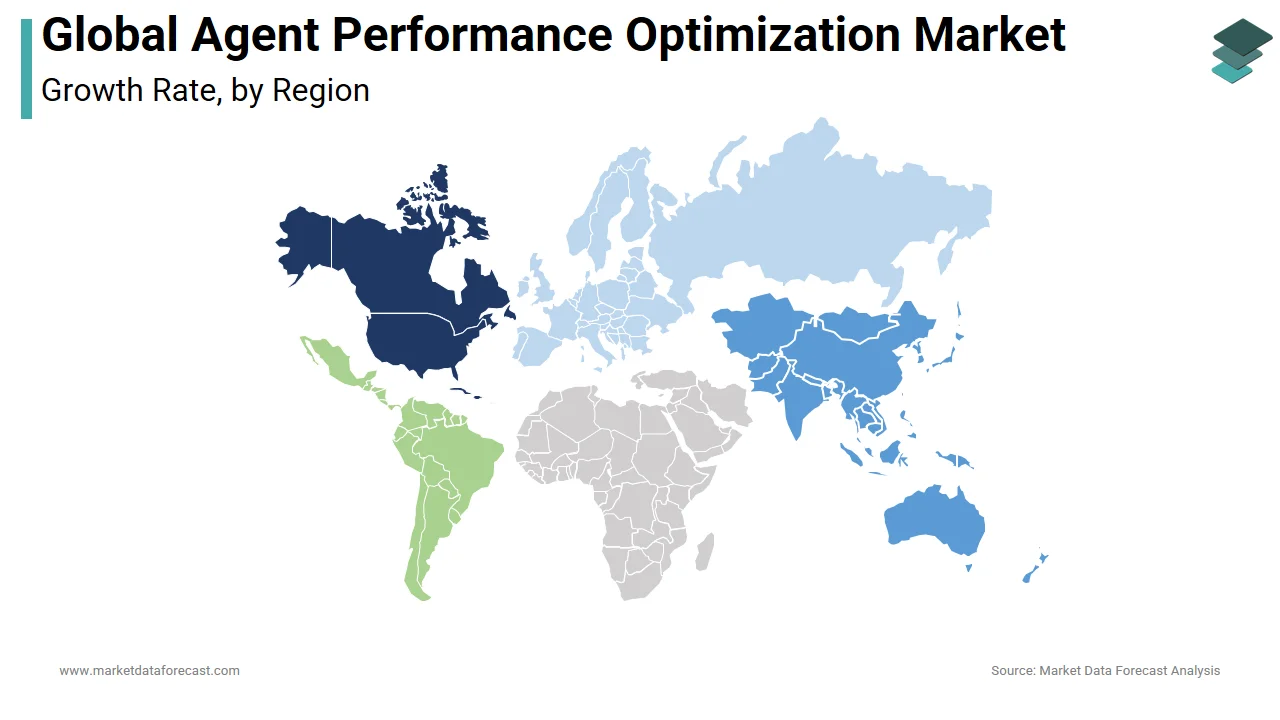

North America Agent Performance Optimization Market Analysis

North America outperformed other regions in the agent performance optimization market in 2024 by accounting for 38.5% of the global market share. The prominence of North America is mainly due to early technology adoption, a mature customer experience culture, and the concentration of global enterprise headquarters. The region benefits from robust venture funding and academic research. North America continues to lead in developing conversational AI technologies, according to sources. Regulatory requirements are encouraging financial institutions to adopt automated systems that ensure accurate record-keeping, as per studies. Companies implementing real-time agent assistance have improved compliance outcomes and operational efficiency, as per research. High employee turnover in the customer service sector is further prompting businesses to use predictive tools and personalized coaching programs to enhance retention, according to sources. This convergence of regulatory, economic, and innovation factors cements North America’s dominance.

Europe Agent Performance Optimization Market Analysis

Europe is another key region in the agent performance optimization market by occupying 29.3% share in 2024. The growth of Europe is propelled by stringent data governance, multilingual service complexity, and public sector digitization. According to sources, most European citizens now expect government services to provide instant digital assistance, prompting agencies to modernize their support operations. As per studies, public healthcare systems have started integrating AI-based assistance tools to enhance service efficiency and improve overall response accuracy. GDPR compliance remains a critical driver. Europe’s optimization market thrives not despite regulation but because of it by turning compliance into a competitive advantage.

Asia Pacific Agent Performance Optimization Market Analysis

Asia Pacific is the fastest-growing region in the agent performance optimization market due to digital transformation, rising middle-class consumption, and government-led service modernization. According to sources, the rapid expansion of contact center employment across major Asian markets is driving strong demand for scalable performance enhancement tools. As per studies, government initiatives in India are supporting the use of AI-based optimization solutions to improve efficiency within the country’s outsourcing industry. A further driver of this segment is mobile first customer behavior. Asia Pacific’s diversity and velocity make it the laboratory for next-generation optimization models.

Latin America Agent Performance Optimization Market Analysis

Latin America agent performance optimization market is expanding steadily, owing to nearshore outsourcing growth, fintech disruption, and improving digital infrastructure. According to sources, contact center capacity in Latin America has expanded rapidly to meet service demand from international clients. As per studies, major financial institutions in the region have improved operational performance by adopting real-time analytics and customer sentiment monitoring tools. Regulatory modernization is a further driver. So, Latin America is transitioning from cost arbitrage to capability dominance as connectivity improves and regulatory frameworks mature.

Middle East and Africa Agent Performance Optimization Market Analysis

The Middle East and Africa region is likely to grow in the agent performance optimization market during the forecast period, which is driven by sovereign vision programs, financial inclusion mandates, and youth-driven digital adoption. According to sources, Saudi Arabia is investing heavily in modernizing its contact center infrastructure as part of national digital transformation efforts. As per studies, financial institutions in the region are adopting AI-driven coaching tools to enhance service quality while ensuring alignment with ethical and regulatory standards. Though nascent, this region’s convergence of policy, technology, and demographic energy positions it for exponential future growth.

COMPETITIVE LANDSCAPE

The Agent Performance Optimization Market is characterized by intense innovation rivalry among established technology vendors and agile AI startups, each vying to redefine how human performance is measured and enhanced. Incumbents leverage deep domain expertise and global client portfolios to embed optimization within broader customer experience suites, while challengers disrupt with vertical-specific, lightweight tools built on generative AI. Competition centers on the accuracy of real-time intervention, depth of regional and linguistic adaptation, and seamless integration with legacy infrastructure. Differentiation increasingly stems from ethical design, agent trust building, and demonstrable impact on retention and revenue rather than feature checklists. Vendors are consolidating capabilities through acquisition and API ecosystems as enterprises demand unified platforms that merge quality, workforce, and journey analytics. The race is no longer about monitoring agents but about augmenting them intelligently, sustainably, and scalably across global and hybrid work environments.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global agent performance optimization market include

- Autonomy Corporation PLC

- Aspect Software Inc.

- Calabrio Inc.

- NICE Systems Ltd.

- Verint Systems Inc.

- Voice Print International Inc.

- Nexidia, Inc.

- GMT Corporation

- CallMiner Inc.

- ClickFox Inc.

- Genesys Telecommunications Laboratories Inc.

- Enkata

- InVision Software AG

- Merced Systems

- HigherGround

Top Players in the Agent Performance Optimization Market

- NICE Ltd has deepened its footprint in the Asia Pacific by aligning its AI-driven performance optimization tools with regional linguistic and cultural nuances. NICE collaborates with major BPO providers to embed predictive coaching and compliance automation, reducing onboarding time by up to forty percent. Its regional data centers in Singapore and Mumbai ensure low latency and regulatory alignment, while partnerships with local universities help tailor training content to graduate skill levels, which strengthens workforce readiness in high-growth markets.

- Genesys has strategically customized its Cloud CX platform for the Asia Pacific’s diverse service environments, integrating generative AI that dynamically adjusts scripts based on customer sentiment and regional communication styles. The company established innovation labs in Bangalore and Manila to co-develop features with regional clients, focusing on multilingual quality scoring and hybrid workforce scheduling. Genesys also launched industry-specific workflows for banking and telecom sectors, ensuring compliance with local data sovereignty laws while improving agent productivity and customer satisfaction metrics.

- Verint Systems has fortified its Asia Pacific presence through strategic alliances and localized analytics deployments. Verint’s platform now includes region-specific dashboards that track agent wellness and attrition risk, addressing high turnover in markets like the Philippines and Malaysia. The company also introduced mobile-first coaching modules accessible via low-bandwidth networks by expanding reach to tier two and tier three cities. By embedding local regulatory templates and vernacular speech models, Verint ensures its solutions remain relevant and scalable across the region’s fragmented linguistic and infrastructural landscape.

Top Strategies Used by Key Market Participants

Leading participants prioritize embedding artificial intelligence into real-time workflows to deliver contextual agent guidance and reduce decision latency. They invest heavily in regional customization, adapting linguistic models, compliance frameworks, and interface designs to local markets. Strategic partnerships with system integrators and BPO providers accelerate deployment and ensure operational relevance. Vendors increasingly adopt modular pricing and usage-based licensing to attract small and mid-sized enterprises. Continuous innovation through dedicated regional R&D centers ensures solutions evolve with local regulatory and cultural dynamics. Companies also focus on agent experience, designing tools that reduce cognitive load and foster skill development rather than surveillance. Integration with existing CRM and telephony ecosystems remains a core technical priority to minimize implementation friction and maximize adoption velocity across diverse enterprise environments.

GLOBAL AGENT PERFORMANCE OPTIMIZATION MARKET NEWS

-

Observe.AI Unveils New AI-Powered Agent Performance & Coaching Suite to Fuel the Future of Remote Work

MARKET SEGMENTATION

This research report on the global agent performance optimization market has been segmented and sub-segmented based on the type, application, end-user, and region.

By Type

- Cloud- based

- On-Premises

By Application

- Quality Monitoring

- Workforce Management Software

By End-User

- Small and Mid-sized Businesses

- Large Enterprises

By Region

- North America

- Latin America

- Middle East & Africa

- Asia-Pacific

- Europe

Frequently Asked Questions

1. What is the Agent Performance Optimization Market and what drives its growth?

The Agent Performance Optimization Market includes technologies and solutions that enhance agent efficiency, productivity, and quality in contact centers, sales, and support teams, driven by the demand for superior customer experiences and digital-first service models

2. What is the current size and forecast for the Agent Performance Optimization Market?

The Agent Performance Optimization Market is valued at around USD 4.5 billion in 2025, projected to reach over USD 5.8 billion by 2033 at a CAGR of 9–14% depending on segment and region

3. How are AI and machine learning transforming the Agent Performance Optimization Market?

AI-driven analytics power real-time monitoring, predictive coaching, personalized feedback, and task automation, delivering higher agent productivity and customer satisfaction

4. Which deployment mode is leading in the Agent Performance Optimization Market?

Cloud-based APO solutions lead due to their scalability, flexibility, and ease of integration with remote or hybrid agent environments

5. What role does speech and text analytics play in the Agent Performance Optimization Market?

Speech and text analytics extract actionable insights from customer interactions, enabling real-time performance management and improved compliance

6. Which industries are major adopters in the Agent Performance Optimization Market?

BFSI, healthcare, retail, telecommunications, and BPO sectors are top users, prioritizing service quality and operational efficiency

7. What are the main types of solutions in the Agent Performance Optimization Market?

Key solutions include performance measurement dashboards, gamification, scheduling, quality monitoring, and real-time agent coaching

8. How does Agent Performance Optimization Market impact customer experience (CX)?

By enabling faster response times, consistent service, and automatic skill improvement, APO solutions directly enhance CX outcomes

9. Who are the leading vendors in the Agent Performance Optimization Market?

Key vendors include NICE Ltd., Verint Systems, Genesys, Cisco Systems, Avaya, Calabrio, Five9, Talkdesk, 8x8, and Oracle

10. How does gamification enhance the Agent Performance Optimization Market?

Gamification modules boost agent engagement, motivation, and retention by using performance-based rewards and recognition

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com