Global Airborne Telemetry Market Size, Share, Trends & Growth Forecast Report Segmented By Technology (Radio Frequency Telemetry, Infrared Telemetry, Optical Telemetry, Satellite Telemetry), Application, Component, Platform, End User, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2026 to 2034

Global Airborne Telemetry Market Report Summary

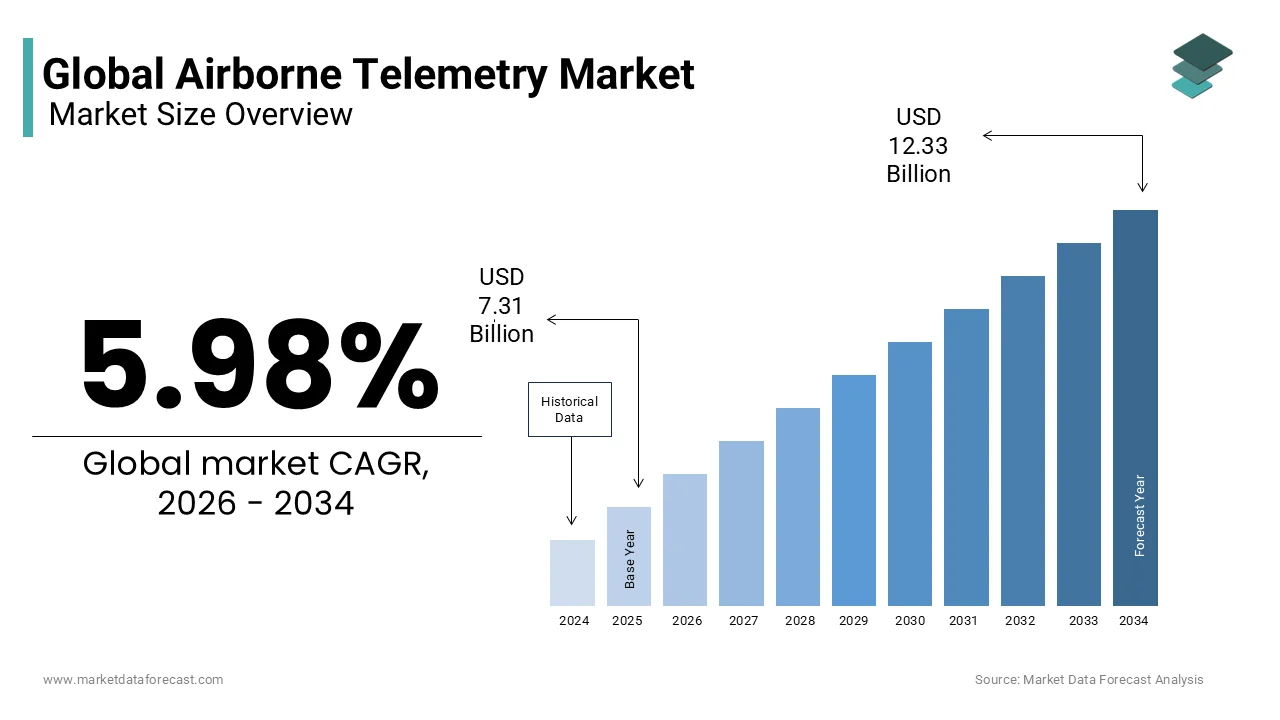

The global airborne telemetry market was valued at USD 7.31 billion in 2025, is estimated to reach USD 7.75 billion in 2026, and is projected to reach USD 12.33 billion by 2034, growing at a CAGR of 5.98% during the forecast period from 2026 to 2034. The growth of the global airborne telemetry market is driven by increasing investments in aerospace and defense modernization, rising demand for real-time flight data transmission, and growing adoption of advanced testing and monitoring systems in military and commercial aircraft. Airborne telemetry systems play a vital role in flight testing, mission monitoring, and performance evaluation by enabling secure, high-speed data communication. Additionally, advancements in wireless communication technologies, unmanned aerial systems, and avionics are further supporting market expansion.

Key Market Trends

-

Rising investments in aerospace and defense modernization programs are driving demand for advanced airborne telemetry systems.

-

Increasing adoption of real-time flight testing and mission monitoring solutions is enhancing operational efficiency and safety.

-

Growing deployment of unmanned aerial vehicles (UAVs) and autonomous aircraft is expanding telemetry applications.

-

Advancements in wireless communication, satellite connectivity, and secure data transmission technologies are improving telemetry capabilities.

-

Increasing focus on high-speed, low-latency telemetry solutions is supporting next-generation aerospace and defense programs.

Segmental Insights

-

Based on technology, the radio frequency telemetry segment dominated the global airborne telemetry market in 2025. The segment's leadership is attributed to its reliable long-range communication capabilities, high-speed data transmission, and widespread use in aircraft flight testing and defense applications.

-

Based on application, the aerospace and defense segment held the largest share of the global airborne telemetry market in 2025. The segment's dominance is driven by increasing defense spending, expanding aircraft testing programs, and growing demand for secure mission-critical communication systems.

-

Based on platform, the fixed-wing aircraft segment accounted for the largest share of the global airborne telemetry market in 2025. The segment's growth is supported by the extensive use of fixed-wing platforms in military operations, commercial aviation, and aerospace testing activities.

-

Based on end user, the OEM segment dominated the global airborne telemetry market in 2025. The segment's leadership is attributed to increasing integration of advanced telemetry systems during aircraft manufacturing and growing demand for factory-installed monitoring and communication solutions.

Regional Insights

-

The global airborne telemetry market is witnessing steady growth due to increasing aircraft production, defense modernization initiatives, and technological advancements in aerospace communication systems.

-

North America dominated the global airborne telemetry market by accounting for 40.9% of the market share in 2025. The region's leadership is supported by substantial defense expenditures, the presence of leading aerospace manufacturers, extensive aircraft testing programs, and continuous investments in advanced avionics and telemetry technologies.

-

Europe remains a significant market due to strong aerospace manufacturing capabilities, growing defense modernization programs, and increasing investments in military aviation technologies.

Competitive Landscape

The global airborne telemetry market is highly competitive, with companies focusing on advanced wireless communication technologies, secure data transmission systems, and next-generation avionics to strengthen their market position. Manufacturers are investing in research and development, strategic collaborations, and integrated telemetry solutions to improve flight testing, mission monitoring, and operational efficiency across aerospace and defense applications. Key players operating in the global airborne telemetry market include BAE Systems, Rockwell Collins Inc., Honeywell International Inc., L3Harris Technologies Inc., Cobham PLC, TransDigm Group Inc., ORBIT Communication Systems Ltd., Safran, Curtiss-Wright Corporation, Dassault Aviation, Finmeccanica, Datasel S.r.l., Kongsberg, Airtech, Inc., and Leonardo S.p.A.

Global Airborne Telemetry Market Size

The global airborne telemetry market size was valued at USD 7.31 billion in 2025, and is expected to be worth USD 12.33 billion by 2034 from USD 7.75 billion by 2026. The market is growing at a CAGR of 5.98% during the forecast period.

Airborne telemetry is the specialized systems and technologies designed to measure, collect, and transmit data from aircraft and unmanned aerial vehicles to ground stations or other airborne platforms in real time. This critical infrastructure supports flight test engineering, mission operations, and structural health monitoring by converting physical parameters such as pressure, temperature, vibration, and acceleration into electrical signals for remote analysis. The sector is integral to the development of next generation aerospace platforms, ensuring safety compliance and performance optimization. According to the Federal Aviation Administration, thousands of commercial flights operate daily in the United States, each generating significant operational data that require robust telemetry frameworks for efficient management. Furthermore, as per the National Aeronautics and Space Administration, modern flight test programs require high bandwidth and low latency transmission capabilities to support real time decision making. The International Civil Aviation Organization mandates rigorous data recording and transmission standards for accident investigation and continuous airworthiness monitoring, driving the adoption of advanced telemetry solutions. With the proliferation of unmanned aerial systems for civilian and military applications, the demand for secure and reliable data links has intensified. The convergence of internet of things technologies with aerospace engineering has transformed telemetry from a niche testing tool into a fundamental component of connected aviation ecosystems, enabling predictive maintenance and enhanced situational awareness across global airspace.

MARKET DRIVERS

Proliferation of Unmanned Aerial Systems and Autonomous Flight Operations

The exponential growth in the deployment of unmanned aerial systems for commercial, military and industrial applications is primarily fuelling the expansion of the airborne telemetry market. These autonomous platforms rely entirely on real time data transmission for navigation, command and control, and payload management, making robust telemetry links indispensable. According to the Federal Aviation Administration, there are over 850,000 drones registered for use in the United States, with projections indicating continued double digit growth annually. Military agencies globally are increasing their investment in unmanned combat aerial vehicles, which require secure, high bandwidth telemetry to transmit video feeds and sensor data over long distances. The Department of Defense indicates that unmanned systems now represent a substantial share of total flight hours in certain operational theaters, creating sustained demand for advanced telemetry hardware. Commercial sectors such as agriculture, logistics, and infrastructure inspection are also adopting drone fleets that depend on telemetry for beyond visual line of sight operations. The European Union Aviation Safety Agency has established regulatory frameworks for unmanned traffic management, which mandate reliable data links for safe integration into shared airspace. As autonomy levels increase, the volume and complexity of data transmitted from these platforms surge, requiring telemetry systems with higher throughput and lower latency. This structural shift toward autonomous aviation ensures a consistent and expanding revenue stream for telemetry solution providers who can meet the stringent reliability requirements of diverse unmanned applications.

Advancement in-Flight Test Engineering and Aircraft Certification Processes

The rigorous requirements for aircraft certification and the increasing complexity of modern aerospace platforms are further contributing to the airborne telemetry market growth. Flight test campaigns generate massive volumes of data that must be captured and analyzed in real time to validate aerodynamic performance, structural integrity, and system functionality. According to the European Union Aviation Safety Agency, the certification process for new commercial aircraft involves thousands of flight hours and millions of data points that must be accurately recorded and transmitted for regulatory approval. Modern aircraft feature highly integrated digital architectures that produce complex data streams requiring high speed telemetry links for efficient ground based analysis. The National Aeronautics and Space Administration emphasizes that real time telemetry allows engineers to monitor critical parameters during high risk test maneuvers, enabling immediate abort decisions if safety thresholds are breached. This capability reduces the need for post flight data extraction and accelerates the overall development cycle. Furthermore, the rise of electric vertical takeoff and landing vehicles introduces new testing paradigms that rely heavily on continuous telemetry for battery management and flight control validation. As aerospace manufacturers strive to reduce time to market while maintaining strict safety standards, the adoption of advanced telemetry systems with wireless capabilities and high channel counts becomes essential. This technological necessity underpins the steady growth of the market as developers seek to optimize their testing workflows.

MARKET RESTRAINTS

Stringent Spectrum Allocation and Regulatory Compliance Burdens

The limited availability of radio frequency spectrum and the complex regulatory landscape governing its use present significant restraints to the airborne telemetry market. Telemetry systems operate within specific frequency bands that are strictly managed by national and international bodies to prevent interference with critical communication and navigation services. According to the International Telecommunication Union, the allocation of spectrum for aeronautical mobile satellite services is highly contested, leading to congestion and potential signal degradation in crowded airspace. Obtaining licenses for specific frequency bands often involves lengthy administrative processes and substantial fees, which can delay project timelines and increase operational costs. The Federal Communications Commission enforces strict power limits and emission masks for telemetry transmitters, requiring manufacturers to invest heavily in compliance testing and certification. In multinational operations, companies must navigate disparate regulatory frameworks across different jurisdictions, creating logistical challenges and legal uncertainties. The European Conference of Postal and Telecommunications Administrations notes that harmonization of spectrum policies remains incomplete, leading to fragmentation in equipment standards. Furthermore, the emergence of 5G networks has raised concerns about potential interference with existing telemetry bands, prompting additional scrutiny and mitigation requirements. These regulatory hurdles limit the flexibility of system designers and constrain the deployment of new telemetry technologies, particularly in regions with rigid spectrum management policies. The cost and complexity of ensuring compliance act as a barrier to entry for smaller innovators and slow the adoption of advanced wireless telemetry solutions.

High Implementation Costs and Technical Complexity

The substantial financial investment required for developing, deploying, and maintaining advanced airborne telemetry systems are further impeding the airborne telemetry market expansion, particularly for smaller operators. High performance telemetry equipment, including sensors, transmitters, antennas, and ground station receivers, involves sophisticated engineering and precision manufacturing, which drives up unit costs. According to the Aerospace Industries Association, the cost of outfitting a single prototype aircraft with a comprehensive telemetry suite can exceed several million dollars depending on the number of channels and data rates required. Additionally, the integration of these systems into existing aircraft architectures often requires extensive modification and validation efforts, further escalating expenses. The technical complexity of managing high volume data streams necessitates specialized personnel with expertise in signal processing, network architecture, and cybersecurity. The Society of Flight Test Engineers highlights that there is a global shortage of qualified telemetry engineers, leading to higher labor costs and project delays. Maintenance and calibration of sensitive telemetry instruments also incur recurring expenses that strain operational budgets. For small and medium sized enterprises engaged in drone development or niche aerospace projects, these costs can be prohibitive, limiting their ability to adopt state of the art telemetry solutions. Consequently, many operators opt for lower cost, less capable systems, which may compromise data quality and reliability. This economic barrier restricts the widespread adoption of advanced telemetry technologies and slows the overall growth of the market, particularly in price sensitive segments.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Edge Computing Capabilities

The integration of artificial intelligence and edge computing into airborne telemetry systems presents a promising opportunity for the airborne telemetry market growth. Traditional telemetry architectures transmit raw data to ground stations for analysis, which can introduce latency and bandwidth bottlenecks. By embedding AI algorithms directly into telemetry hardware, systems can process and filter data at the source, transmitting only relevant insights or anomalies. According to the National Institute of Standards and Technology, edge computing can reduce data transmission volumes by up to 90%, significantly alleviating spectrum congestion and lowering communication costs. This capability is particularly valuable for autonomous drones and military aircraft operating in contested environments where bandwidth is limited or jammed. The Department of Defense is actively exploring AI enabled telemetry for real time threat detection and mission adaptation, demonstrating strong government interest in this technology. Commercial aviation companies are also leveraging edge analytics for predictive maintenance, using telemetry data to identify component failures before they occur. The International Air Transport Association estimates that predictive maintenance powered by real time data analysis can reduce unscheduled maintenance events by 20%. As processing power becomes more compact and energy efficient, the feasibility of onboard AI integration increases. This technological evolution enables new applications such as autonomous swarm coordination and adaptive flight control, creating lucrative opportunities for telemetry providers who can deliver intelligent embedded solutions.

Expansion Of Beyond Visual Line Of Sight Drone Operations

The regulatory approval and operational expansion of beyond visual line of sight drone operations create substantial opportunities for the airborne telemetry market. BVLOS flights require robust and redundant telemetry links to ensure continuous command and control over long distances and in complex environments. According to the Federal Aviation Administration, the implementation of remote identification rules and unmanned traffic management systems relies heavily on secure telemetry data for tracking and deconfliction. Logistics companies are piloting large scale drone delivery networks that depend on reliable telemetry for navigation and package monitoring. The European Union Aviation Safety Agency has introduced specific operational categories for BVLOS flights, mandating high integrity data links to ensure public safety. This regulatory shift drives demand for telemetry systems with extended range, encryption, and anti jamming features. Additionally, the use of drones in critical infrastructure inspection, such as power lines and pipelines, often occurs in remote areas where cellular coverage is sparse, necessitating satellite based telemetry solutions. The Global Satellite Operators Association reports growing demand for low earth orbit satellite connectivity for IoT and telemetry applications, enabling global coverage for BVLOS operations. As industries increasingly adopt drones for automated tasks, the requirement for sophisticated telemetry infrastructure will grow proportionally. Telemetry providers who can offer scalable, secure, and long range solutions are well positioned to capitalize on this emerging market segment driven by the automation of aerial services.

MARKET CHALLENGES

Cybersecurity Vulnerabilities and Data Integrity Risks

The increasing connectivity of airborne telemetry systems exposes them to significant cybersecurity threats, posing a major challenge to the airborne telemetry market expansion. Telemetry links are potential entry points for malicious actors seeking to intercept sensitive data, hijack control signals, or disrupt operations. According to the Cybersecurity and Infrastructure Security Agency, the aviation sector faces a rising number of cyber attacks targeting communication links, including telemetry systems used in flight testing and unmanned operations. The broadcast nature of many telemetry protocols makes them susceptible to eavesdropping and spoofing attacks, which can compromise mission integrity and safety. The Federal Aviation Administration has issued alerts regarding vulnerabilities in legacy telemetry systems that lack modern encryption standards, urging operators to upgrade their security measures. However, implementing robust encryption and authentication mechanisms adds complexity and latency to telemetry transmissions, which can be detrimental to real time applications. The International Civil Aviation Organization emphasizes the need for holistic cybersecurity frameworks but acknowledges the difficulty of securing diverse and distributed telemetry networks. Furthermore, the supply chain for telemetry components is global, increasing the risk of counterfeit or tampered hardware entering the market. Ensuring end to end security requires continuous monitoring, regular software updates, and rigorous penetration testing, which strains resources. As telemetry systems become more integrated with broader aviation networks, the attack surface expands, making cybersecurity a persistent and evolving challenge that demands constant vigilance and investment from all market participants.

Signal Interference and Environmental Propagation Issues

Physical environmental factors and electromagnetic interference present persistent challenges to the reliability and performance of airborne telemetry systems. Radio frequency signals are susceptible to attenuation, reflection, and multipath propagation caused by terrain, weather conditions, and urban structures. According to the National Oceanic and Atmospheric Administration, severe weather events such as heavy rain, thunderstorms, and ionospheric disturbances can significantly degrade signal quality, leading to data loss or connection drops. In mountainous or urban environments, signal blockage and reflection create blind spots that disrupt continuous telemetry coverage. The International Telecommunication Union notes that the increasing density of wireless devices in the electromagnetic spectrum exacerbates interference issues, causing packet errors and reduced throughput. Military operations in electronic warfare environments face intentional jamming, which requires expensive and complex countermeasures to maintain link integrity. Commercial operators also struggle with interference from nearby radar systems and communication towers, particularly in congested airspace. Mitigating these issues often requires sophisticated antenna designs, frequency hopping techniques, and error correction codes, which increase system cost and complexity. The Society of Flight Test Engineers highlights that signal reliability remains a critical metric in flight testing, with even brief interruptions potentially invalidating valuable data sets. Overcoming these physical limitations requires ongoing research into adaptive modulation and resilient network architectures. Until these challenges are fully addressed, they remain a significant hurdle for achieving seamless and uninterrupted telemetry performance in diverse operational scenarios.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.98% |

| Segments Covered | By Technology, Application, Component, Platform, End User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BAE Systems, Rockwell Collins Inc., Honeywell International Inc., L3Harris Technologies Inc., Cobham PLC, TransDigm Group Inc., ORBIT Communication Systems Ltd., Safran, Curtiss-Wright Corporation, Dassault Aviation, Finmeccanica, Datasel S.r.l., Kongsberg, Airtech, Inc., and Leonardo S.p.A. |

SEGMENTAL ANALYSIS

By Technology Insights

The radio frequency telemetry segment held the largest share of the global market in 2025 and is expected to remain the dominant technology in the global market throughout the forecast period due to its deeply entrenched infrastructure and proven reliability across diverse operational environments. According to the Federal Communications Commission, the allocation of specific aeronautical mobile telemetry bands ensures dedicated spectrum availability for critical flight testing and military operations. This regulatory backing provides manufacturers and operators with the confidence that their systems will function without harmful interference from commercial telecommunications networks. The widespread availability of ground station receivers and compatible antennas globally further solidifies its leading position. The Institute of Electrical and Electronics Engineers notes that a vast majority of existing aerospace test ranges are fully equipped with radio frequency reception infrastructure. Upgrading these massive physical installations to entirely new technologies would require billions of dollars in capital expenditure. Consequently, organizations prefer to incrementally upgrade their existing radio frequency hardware rather than replace it completely. This massive installed base creates a continuous demand for replacement components, system expansions, and software upgrades, ensuring that radio frequency telemetry maintains its overwhelming market dominance in the foreseeable future.

On the other side, optical telemetry segment is estimated to register the fastest CAGR in the global market over the forecast period. The Optical telemetry is emerging as the fastest growing segment, driven by the exponential increase in data generation by modern airborne platforms. According to the National Aeronautics and Space Administration, next generation sensors, high definition video cameras, and advanced radar systems produce massive volumes of data that easily overwhelm traditional radio frequency bandwidth limitations. Optical communication links utilizing laser technology can transmit data at rates exceeding 10 gigabits per second, which is several orders of magnitude faster than conventional radio systems. This immense bandwidth capability is critical for real time transmission of ultra high definition video, synthetic aperture radar imagery, and complex telemetry data streams from high altitude and space platforms. The Defense Advanced Research Projects Agency emphasizes that the ability to download terabytes of mission data in minutes rather than hours drastically accelerates the intelligence analysis cycle and operational decision making. As airborne platforms become more sensor rich, the bottleneck shifts from data collection to data transmission. Optical telemetry solves this bottleneck by providing a virtually unlimited data pipe, enabling the full exploitation of advanced sensor payloads. This technological necessity is driving rapid investment and adoption of optical communication systems across both military and scientific aerospace programs globally.

By Application Insights

The aerospace and defense segment led the market by capturing the major share of the global market in 2025 and is expected to continue holding the dominating share of the global market during the forecast period primarily due to massive global military modernization budgets and the continuous development of advanced weapon systems. According to the Stockholm International Peace Research Institute, global military expenditure reached approximately 2.9 trillion dollars in 2025, with a significant portion allocated to aerospace research and flight testing. Modern fighter jets, stealth bombers, and next generation missiles require extensive flight test campaigns to validate aerodynamic performance, weapon integration, and survivability. Each of these test flights relies on high performance telemetry systems to transmit thousands of parameters back to ground stations in real time. The United States Department of Defense conducts thousands of flight test hours annually, requiring a vast array of telemetry transmitters, receivers, and ground infrastructure. Furthermore, the shift toward unmanned combat aerial vehicles and loyal wingman concepts necessitates secure, high bandwidth telemetry for command and control as well as payload data transmission. The continuous cycle of prototyping, testing, and fielding new defense platforms ensures a steady and substantial demand for advanced telemetry solutions. This sustained government investment and the critical nature of national security programs guarantee that aerospace and defense remains the largest and most lucrative application segment in the global market.

The R&D segment is predicted to register a promising CAGR in the global market during the forecast period owing to the explosive growth of the commercial space sector and advanced academic research. According to the Federal Aviation Administration Office of Commercial Space Transportation, the number of commercial orbital launch attempts has increased dramatically, with private companies launching hundreds of satellites and developing reusable rocket systems. These space vehicles rely heavily on advanced telemetry to monitor propulsion system health, trajectory, vehicle structural integrity, and payload conditions during the extreme environments of launch and re-entry. According to the National Aeronautics and Space Administration, the transition from government led space programs to a vibrant commercial space economy has multiplied the number of entities requiring specialized space telemetry solutions. Universities and private research institutions are also conducting high altitude balloon experiments and suborbital research flights that require robust data transmission capabilities. The democratization of space access means that smaller companies and academic teams are procuring telemetry systems that were previously only available to major government agencies. This broadening of the customer base and the rapid pace of innovation in the commercial space sector are driving unprecedented growth in the research and development application segment.

By Platform Insights

The fixed wing aircraft segment led the market by accounting for the major share of the global market in 2025. The growth of the fixed wing aircraft segment in the global market is attributed to their overwhelming dominance in both commercial aviation and long range military operations. According to the International Air Transport Association, the global commercial fleet consists of thousands of fixed wing jetliners that require regular maintenance, testing, and system upgrades. Every commercial aircraft undergoes rigorous flight testing during its manufacturing phase and periodic check flights throughout its operational life, necessitating the use of telemetry systems to validate avionics and structural health. In the military domain, fixed wing platforms such as fighter jets, bombers, and transport aircraft form the backbone of air power. The United States Department of Defense operates thousands of fixed wing aircraft that require continuous telemetry monitoring for mission systems integration and weapons testing. The sheer volume of fixed wing aircraft in operation globally creates a massive installed base for telemetry equipment. Furthermore, the physical size and payload capacity of fixed wing aircraft allow for the installation of comprehensive telemetry suites with multiple antennas and high power transmitters. This capability to carry extensive sensor packages makes fixed wing platforms the primary users of complex and high performance telemetry systems, solidifying their leading market position.

However, the unmanned aerial vehicles segment is the fastest growing platform segment and is expected to exhibit a promising CAGR in the global market during the forecast period owing to the rapid expansion of commercial and industrial drone applications. For instance, the commercial drone market is expanding into diverse sectors including agriculture, infrastructure inspection, and package delivery. These applications require reliable telemetry links to transmit high definition video, sensor data, and flight control commands beyond visual line of sight. As per the Federal Aviation Administration, the number of commercial drone registrations has grown exponentially, which is creating a massive new customer base for lightweight and cost effective telemetry systems. Unlike traditional manned aircraft, unmanned aerial vehicles rely entirely on telemetry for navigation and mission execution and this is making these systems absolutely critical for their operation. The integration of advanced sensors such as thermal cameras and multispectral imagers on drones generates significant data volumes that must be transmitted in real time to ground operators. The versatility and affordability of unmanned aerial vehicles have democratized access to airborne data collection, driving widespread adoption across industries. This rapid proliferation of commercial drones is fundamentally transforming the telemetry market and establishing unmanned aerial vehicles as the fastest growing platform segment.

By End User Insights

The OEM segment led the market by capturing the highest share of the global market in 2025. The growth of the OEM segment in the global market can be credited to the critical integration of telemetry systems during the initial assembly and manufacturing of aircraft. According to the Aerospace Industries Association, every new aircraft produced requires a comprehensive suite of telemetry equipment for flight testing and certification before it can be delivered to the customer. Airframers such as Boeing and Airbus install temporary or permanent telemetry transmitters, sensors, and antennas directly into the aircraft structure during the manufacturing process. This factory installed equipment ensures that the telemetry systems are perfectly integrated with the aircraft avionics and structural design. The Federal Aviation Administration mandates that all flight test data be collected using certified equipment, which is typically sourced directly by the original equipment manufacturers. The high volume of aircraft production globally translates to a massive and consistent demand for telemetry components from the manufacturing sector. Furthermore, original equipment manufacturers have long term contracts with telemetry suppliers, ensuring a stable and predictable revenue stream. The essential nature of telemetry for aircraft certification and the sheer scale of global aircraft production solidify the leading position of original equipment manufacturers in the market.

On the other side, the aftermarket segment is the fastest growing end user category and is predicted to grow at a healthy CAGR in the global market during the forecast period owing to the aging global commercial and military aircraft fleet requiring system upgrades and replacements. As of 2026, the average age of the global commercial aircraft fleet is approximately 18 years, with many aircraft exceeding 15 years of service. Older aircraft are often equipped with legacy telemetry systems that are heavy, power hungry, and lack the bandwidth required for modern data acquisition needs. Airlines and military operators are increasingly retrofitting these aging platforms with modern lightweight digital telemetry systems to improve performance and reduce maintenance costs. The International Air Transport Association notes that upgrading avionics and telemetry systems is a key strategy for extending the operational life and economic viability of older aircraft. Furthermore, regulatory mandates for enhanced flight data monitoring and safety reporting require older aircraft to be equipped with modern data recording and transmission capabilities. This massive retrofit market provides a lucrative and rapidly expanding revenue stream for telemetry suppliers who can offer drop in replacement solutions and upgrade kits for legacy platforms.

REGIONAL ANALYSIS

North America Airborne Telemetry Market Analysis

North America had 40.9% of the global market share in 2025 and is expected to maintain its dominant market position over the next several years. The dominance of North America in the global market is driven by a high concentration of aerospace R&D, sustained government defense investment, massive defense spending and a highly advanced aerospace manufacturing base. The primary driving factor is the substantial budget allocated by the United States government for military modernization and aerospace research. According to the Congressional Budget Office, the United States defense budget for 2026 was requested at approximately 961 billion dollars, with a significant portion dedicated to flight testing and the development of next generation aircraft and missiles. The presence of major aerospace original equipment manufacturers and specialized telemetry suppliers in the United States fosters a robust domestic supply chain. Furthermore, the Federal Aviation Administration and the National Aeronautics and Space Administration conduct extensive civil and space flight testing programs that require advanced telemetry infrastructure. The region benefits from a highly skilled workforce and cutting edge research institutions that drive continuous innovation in telemetry technologies. The strong emphasis on national security and the continuous development of advanced aerospace platforms ensure that North America remains the largest and most technologically advanced market for airborne telemetry systems globally.

Europe Airborne Telemetry Market Analysis

Europe is poised for consistent growth in the coming years as regional collaboration on defense programs, strict aviation safety standards continue to drive innovation, strong collaborative defense programs, a rigorous regulatory environment for civil aviation, the presence of major aerospace conglomerates and the coordinated defense initiatives of the European Union. According to the European Defence Agency, member states are increasingly collaborating on joint aerospace projects, such as the Future Combat Air System, which requires extensive flight testing and advanced telemetry integration. The European Union Aviation Safety Agency enforces strict certification standards for commercial aircraft, driving demand for high performance telemetry systems during the development and testing phases. The region is also a leader in the development of optical and satellite telemetry technologies driven by the European Space Agency and various national space programs. Furthermore, the growing focus on unmanned traffic management and the integration of drones into civilian airspace is creating new opportunities for telemetry solution providers. The combination of strong government support, collaborative research, and a mature aerospace industry ensures that Europe remains a critical and highly innovative market in the global airborne telemetry sector.

Asia Pacific Airborne Telemetry Market Analysis

The Asia Pacific region is anticipated to be the fastest growing market in the next few years due to accelerated military modernization and the rapid expansion of domestic commercial aviation industries. The market status in this region is characterized by rapid military expansion and a booming commercial aviation sector. The primary driving factor is the increasing defense budgets and aerospace modernization programs in major economies such as China and India. According to the International Institute for Strategic Studies, military expenditure in the Asia Pacific region has grown significantly as nations seek to modernize their air forces with advanced fighter jets and unmanned systems. This rapid expansion of military and civil aerospace capabilities necessitates advanced telemetry infrastructure, positioning the region for significant growth in the coming decade.

COMPETITIVE LANDSCAPE

The competition in the airborne telemetry market is characterized by intense rivalry among specialized aerospace technology firms and large defense contractors. Major players leverage their extensive experience in flight testing and strong government relationships to maintain dominance while innovators disrupt the landscape with wireless and optical technologies. The market features a mix of proprietary hardware systems and open architecture solutions creating a diverse competitive environment. Companies differentiate themselves through data throughput capabilities signal security and ruggedness rather than price alone. Strategic alliances between telemetry providers and satellite communication companies are becoming increasingly common as stakeholders seek to offer global coverage solutions. The entry of commercial drone manufacturers into the telemetry space has further intensified competition by driving demand for cost effective and lightweight components. Regulatory hurdles regarding spectrum allocation act as a barrier to entry for smaller firms but also ensure high standards of reliability. Intellectual property protection plays a crucial role in sustaining competitive advantages as companies patent unique modulation techniques and antenna designs. Overall the market remains dynamic with continuous innovation driving shifts in competitive positioning and customer preferences across the global aerospace sector.

KEY MARKET PLAYERS

Some of the key players dominating the global airborne telemetry market are

- BAE Systems (U.K.)

- Rockwell Collins Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- L-3 Harris Technologies Inc. (U.S.)

- Cobham PLC (U.K.)

- TransDigm Group Inc

- ORBIT Communication Systems Ltd. (Israel)

- Safran (France)

- Curtiss-Wright Corporation (U.S.)

- Dassault Aviation (France)

- Finmeccanica (Italy)

- Datasel S.r.l.

- Kongsberg (Norway)

- Airtech, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

Top Players in the Market

- Curtiss Wright Corporation maintains a leading position in the global airborne telemetry market through its specialized data acquisition and recording systems. The company provides robust solutions for flight test engineering and structural health monitoring across military and commercial aerospace sectors. Recently Curtiss Wright enhanced its product portfolio by integrating advanced wireless telemetry capabilities into its existing wired systems. This innovation allows for easier installation and reduced aircraft weight which is critical for modern flight testing. The company also expanded its support services to include real time data analytics helping engineers make faster decisions during critical test phases. These strategic improvements reinforce its reputation for reliability and technical excellence in demanding aerospace environments.

- TransDigm Group Inc contributes significantly to the market by offering high performance telemetry transmitters and receivers designed for extreme operational conditions. The company focuses on delivering secure and jam resistant communication links for unmanned aerial vehicles and combat aircraft. TransDigm recently invested in developing miniaturized telemetry modules that support higher data rates while consuming less power. This technological advancement addresses the growing need for compact and efficient systems in small drone platforms. The firm also strengthened its manufacturing facilities to ensure rapid delivery of customized solutions for defense contracts. By prioritizing innovation and operational efficiency TransDigm continues to meet the evolving demands of global military and aerospace customers.

- Datasel S.r.l. serves as a key provider of modular telemetry systems tailored for complex flight test applications. The company specializes in high channel count data acquisition units that can handle diverse sensor inputs simultaneously. Datasel recently launched a new series of ruggedized telemetry recorders with enhanced storage capacity and faster processing speeds. This product update enables more comprehensive data collection during long duration flights and high speed maneuvers. The company also expanded its international distribution network to better serve emerging markets in Asia and the Middle East. Through continuous product development and global outreach Datasel strengthens its position as a trusted partner for aerospace testing and validation projects worldwide.

Top Strategies Used by Key Market Participants

Key players in the airborne telemetry market primarily employ strategies focused on technological innovation and strategic partnerships to maintain competitive advantage. Companies invest heavily in research and development to create miniaturized and high bandwidth telemetry systems that meet the demands of modern aerospace platforms. Collaborations with aerospace original equipment manufacturers help integrate telemetry solutions directly into new aircraft designs during the production phase. Mergers and acquisitions are common tactics used to expand product portfolios and acquire specialized engineering talent. Additionally firms focus on enhancing cybersecurity features to protect sensitive data from interception and jamming threats. Compliance with international regulatory standards remains central to operational strategies ensuring trust and reliability among users. These multifaceted approaches enable market participants to address evolving security requirements and capture growing demand for advanced data transmission solutions.

MARKET SEGMENTATION

This research report on the global airborne telemetry market is segmented and sub-segmented into the following categories.

By Technology

- Radio Frequency Telemetry

- Infrared Telemetry

- Optical Telemetry

- Satellite Telemetry

By Application

- Aerospace & Defense

- Research & Development

- Automotive Testing

- Healthcare Monitoring

By Component

- Transmitters

- Receivers

- Sensors

- Data Acquisition Systems

By Platform

- Rotary Wing

- Fixed Wing

- Unmanned Aerial Vehicle

- Parachutes

By End User

- Government Agencies

- Commercial Enterprises

- Research Institutions

- Military Organizations

By Operating Environment

- Urban

- Rural

- Remote

- Adverse Weather Conditions

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Airborne Telemetry Market?

The Airborne Telemetry Market refers to the global industry focused on systems that collect, transmit, and analyze real-time data from aircraft, missiles, unmanned aerial vehicles (UAVs), and other airborne platforms for testing, monitoring, and operational purposes.

2. What is driving the growth of the Airborne Telemetry Market?

The market is driven by increasing defense modernization programs, growing aircraft testing activities, rising adoption of UAVs, advancements in wireless communication technologies, and the need for real-time flight data monitoring.

3. Which industries are the major users of airborne telemetry systems?

Major end users include aerospace and defense organizations, government agencies, research institutions, commercial aviation companies, automotive testing facilities, and military organizations.

4. Which technologies are commonly used in airborne telemetry?

Common technologies include radio frequency (RF) telemetry, satellite telemetry, infrared telemetry, and optical telemetry, each designed to meet different communication and operational requirements.

5. What are the key components of an airborne telemetry system?

An airborne telemetry system typically consists of transmitters, receivers, sensors, antennas, data acquisition systems, and telemetry processing software.

6. Which region holds the largest share of the Airborne Telemetry Market?

North America holds the largest market share due to significant defense spending, extensive aircraft testing activities, and the presence of leading aerospace and defense companies.

7. Which region is expected to witness the fastest growth in the Airborne Telemetry Market?

The Asia-Pacific region is expected to record the fastest growth owing to increasing military modernization, expanding aerospace manufacturing, and rising investments in UAV development.

8. What challenges does the Airborne Telemetry Market face?

Major challenges include high deployment costs, spectrum allocation limitations, cybersecurity concerns, complex system integration, and strict regulatory requirements.

9. How are UAVs influencing the Airborne Telemetry Market?

The increasing deployment of UAVs for defense, surveillance, environmental monitoring, and commercial applications is significantly boosting demand for reliable airborne telemetry systems.

10. What is the future outlook for the Airborne Telemetry Market?

The market is expected to experience steady growth over the coming years, supported by technological advancements in wireless telemetry, increasing aerospace R&D investments, next-generation military aircraft programs, and expanding demand for real-time data transmission solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com