Global Aircraft Engines Market Size, Share, Trends & Growth Forecast Report, Segmented By Engine Type (Turbofan, Turboprop), Aircraft Type, Component, End User, And Country (North America, Europe, Asia Pacific, Middle East and Africa, Latin America) - Industry Analysis From (2026 To 2034)

Global Aircraft Engines Market Size

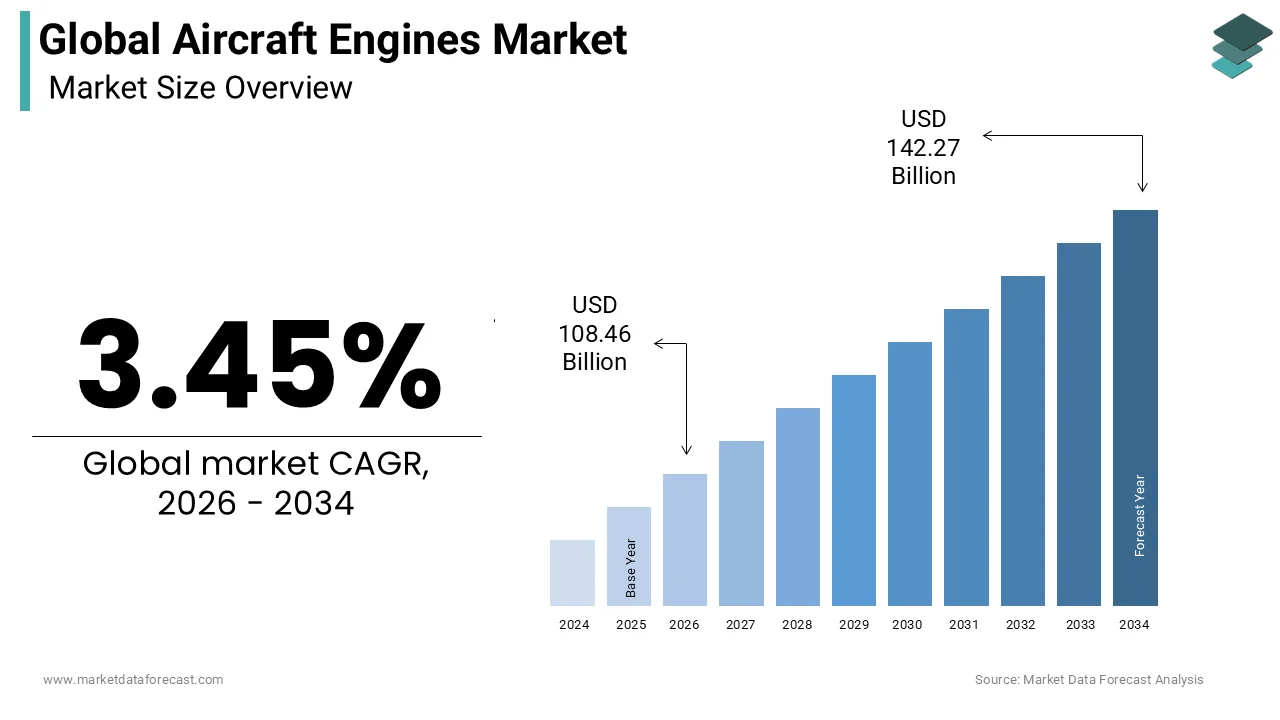

The global aircraft engines market size was calculated at USD 104.84 billion in 2025 and is anticipated to reach USD 142.27 billion by 2034, from USD 108.46 billion in 2026, growing at a CAGR of 3.45% during the forecast period.

Aircraft engines are propulsion systems that power commercial, military, and general aviation aircraft. These complex mechanical assemblies convert fuel into thrust through intricate thermodynamic processes involving compressors, combustors, and turbines. According to the International Civil Aviation Organization, global air traffic is projected to double by 2040, necessitating a significant expansion in propulsion capacity to support increased flight frequencies. The Federal Aviation Administration mandates strict certification standards for engine durability and emissions, which drive continuous engineering innovation. According to Boeing, the global fleet will require over 41,000 new aircraft between 2023 and 2042, each requiring advanced propulsion units to meet efficiency targets. Modern turbofan engines achieve bypass ratios exceeding 12:1, which significantly reduces fuel consumption compared to previous generations. According to the European Union Aviation Safety Agency, rigorous noise regulations compel manufacturers to develop quieter acoustic liners and optimized fan blade geometries. According to the Intergovernmental Panel on Climate Change, engine manufacturers must balance performance with environmental compliance as aviation accounts for approximately 2.5% of global carbon dioxide emissions. This regulatory landscape drives investment in sustainable technologies while maintaining the reliability required for safe commercial operations. The market is defined by a delicate equilibrium between technological advancement, regulatory adherence, and operational efficiency in an increasingly congested global airspace.

MARKET DRIVERS

Surging Global Air Passenger Traffic Drives Propulsion Demand

YOY growth in the air passenger market is primarily propelling the growth of the global aircraft engines market. According to the International Air Transport Association, global passenger numbers are expected to reach 4.5 billion by 2026, reflecting a robust recovery and expansion beyond pre-pandemic levels. This surge necessitates the addition of thousands of new aircraft to existing fleets, each requiring powerful and efficient propulsion systems. For every new narrow-body aircraft added to service, two high-thrust turbofan engines are installed, creating a direct correlation between fleet expansion and engine production. According to Boeing, the Asia Pacific region alone will account for 40% of new aircraft deliveries over the next two decades, driving substantial orders for engine manufacturers. Airlines seek engines with lower specific fuel consumption to mitigate rising jet fuel prices, which can constitute up to 30% of operating costs. The introduction of more fuel-efficient models has accelerated the replacement of older, less efficient aircraft. This fleet renewal cycle generates sustained demand for next-generation engines that offer double-digit improvements in fuel burn. The economic imperative to reduce cost per seat mile ensures that carriers prioritize modern propulsion technology, thereby sustaining strong order books for major engine manufacturers globally.

Stringent Environmental Regulations Mandate Technological Innovation

The aviation sector is likely to see a continued increase in environmental regulation for the foreseeable future, which is further contributing to the aircraft engines market expansion. According to the International Civil Aviation Organization, the Carbon Offsetting and Reduction Scheme for International Aviation requires airlines to offset emissions growth above 2020 levels. As per the European Union Aviation Safety Agency, new engine certifications must meet increasingly stringent nitrogen oxide emission limits, which are 15% lower than previous standards. These regulatory pressures drive investment in advanced materials such as ceramic matrix composites that allow higher operating temperatures and improved thermal efficiency. Manufacturers are also integrating lean-burn combustor designs that reduce pollutant formation during the combustion process. According to the Intergovernmental Panel on Climate Change, aviation contributes approximately 2.5% of global carbon dioxide emissions, prompting urgent action from regulators. The push for net-zero emissions by 2050 has accelerated research into hybrid-electric and hydrogen-fueled propulsion systems. Engine makers must demonstrate compliance with noise regulations as well, with modern airports imposing curfews on louder aircraft. This regulatory framework creates a mandatory upgrade cycle where older engines become obsolete, not due to mechanical failure but due to non-compliance with environmental standards. Consequently, manufacturers are forced to innovate continuously to meet these evolving legal requirements while maintaining performance and reliability.

MARKET RESTRAINTS

Supply Chain Disruptions and Raw Material Scarcity Restrain Production

Supply chain and material constraints are significant restraints to the global aircraft engines market growth. The aerospace industry relies heavily on specialized alloys such as titanium and nickel-based superalloys, which are subject to volatile global markets. According to the US Geological Survey, global titanium production faced a 10% decline in 2023 due to geopolitical tensions affecting key exporting nations. These material shortages lead to extended lead times for engine components, with some parts experiencing delays of up to 18 months. As per Boeing, supply chain bottlenecks have reduced engine delivery rates by 20% compared to pre-pandemic levels, impacting airline fleet expansion plans. The complexity of engine manufacturing involves thousands of suppliers across multiple continents, making the system vulnerable to localized disruptions. Labor shortages in specialized machining and casting facilities further exacerbate production delays. According to the International Air Transport Association, 60% of airlines experienced delivery delays for new aircraft in 2024, primarily due to engine availability issues. These constraints force manufacturers to ration engine allocations, prioritizing high-value customers while delaying others. The inability to scale production rapidly in response to surging demand creates a backlog that may take years to clear. This structural limitation restricts market growth despite strong order books and high demand for new propulsion systems.

High Maintenance Costs and Aging Fleet Complexities Impose Financial Burdens

The costs associated with older engine fleets are further likely to impede the global market expansion. As global fleets age, the frequency of shop visits increases dramatically, with older engines requiring major overhauls every 3,000 to 5,000 flight cycles. According to Oliver Wyman, maintenance, repair, and overhaul costs for mature engines can be 40% higher than for new units due to component wear and tear. The scarcity of spare parts for discontinued engine models forces airlines to source components from secondary markets at premium prices. As per the Regional Airline Association, small carriers spend up to 25% of their operating budget on engine maintenance, limiting their ability to invest in new technology. The complexity of modern engines with integrated electronic controls requires specialized diagnostic equipment and highly trained technicians, which are in short supply. Labor agreements in major manufacturing hubs have led to wage increases of 15% over the past three years, further driving up service costs. Insurance premiums for older aircraft have also risen due to perceived higher risks of mechanical failure. These cumulative costs discourage airlines from retaining older aircraft longer than necessary but also delay new purchases due to capital constraints. The financial strain of maintaining legacy propulsion systems thus acts as a brake on market expansion and fleet modernization efforts.

MARKET OPPORTUNITIES

Adoption of Sustainable Aviation Fuels Creates New Engineering Opportunities

The global transition towards Sustainable Aviation Fuels (SAF) is a significant opportunity for the global aircraft engines market. Major engine makers are certifying their latest models to operate on 100% SAF blends, which reduce lifecycle carbon emissions by up to 80%. According to the International Air Transport Association, SAF production is expected to reach 10 million tons annually by 2030, creating a substantial market for compatible propulsion systems. Manufacturers are modifying fuel nozzles and combustor liners to handle the different chemical properties of biofuels and synthetic kerosene. As per Rolls-Royce, successful tests have demonstrated that existing turbofan engines can run on pure SAF without modification, opening new revenue streams for retrofit services. Governments in Europe and North America are offering subsidies for SAF adoption, which incentivize airlines to upgrade their fleets with compatible engines. According to the European Union, mandates require that 2% of aviation fuel must be sustainable by 2025, rising to 70% by 2050. This regulatory push ensures long-term demand for engines designed with SAF flexibility in mind. Companies that lead in SAF compatibility gain a competitive advantage in securing contracts with environmentally conscious carriers. This technological pivot allows manufacturers to align with global sustainability goals while capturing value from the emerging green aviation economy.

Development of Hybrid Electric and Hydrogen Propulsion Systems Opens New Markets

Innovation in zero-emission propulsion is another prominent opportunity for the global aircraft engines market. Engine manufacturers are investing billions in developing zero-emission powertrains that combine traditional gas turbines with electric motors or hydrogen fuel cells. According to Airbus, the first commercial hydrogen-powered aircraft could enter service by 2035, creating a new segment for specialized propulsion units. GE Aerospace and Safran have launched joint ventures to develop open-rotor engine architectures that promise 20% better fuel efficiency than current turbofans. As per the Hydrogen Council, global hydrogen demand in aviation could reach 5 million tons by 2050, driving the need for new engine designs. These novel propulsion systems require entirely new supply chains and manufacturing processes, offering first-mover advantages to early adopters. Government grants and research funding support these initiatives, with the European Clean Sky program allocating 1 billion euros for green aviation technologies. Airlines seeking to meet net-zero targets are eager to partner with manufacturers developing these breakthrough technologies. The potential to disrupt the traditional fossil fuel-dependent model attracts significant venture capital and strategic investments. This shift positions forward-thinking companies to dominate the next generation of aviation propulsion while addressing climate change concerns.

MARKET CHALLENGES

Integration of Artificial Intelligence in Engine Design and Monitoring Poses Technical Challenges

The integration of artificial intelligence is expected to face a complex regulatory and technical validation phase, which is a key challenge to the expansion of the aircraft engines market. While AI offers predictive capabilities, ensuring its accuracy in safety-critical applications requires extensive validation and regulatory approval. According to the Federal Aviation Administration, certifying AI-driven control systems involves demonstrating fail-safe mechanisms that traditional mechanical systems do not require. The sheer volume of data generated by modern engines exceeds current processing capabilities, leading to latency issues in real-time decision-making. As per SAE International, inconsistent sensor data quality can lead to false positives in fault detection, causing unnecessary maintenance actions and operational disruptions. Engineers struggle to create algorithms that generalize well across different operating conditions and aircraft types without extensive retraining. Cybersecurity vulnerabilities associated with connected AI systems pose additional risks, as malicious actors could potentially manipulate engine parameters. The lack of standardized data formats across different manufacturers hinders the development of universal AI models. Training machine learning models requires vast amounts of historical failure data, which is often proprietary and fragmented. These technical hurdles slow down the deployment of fully autonomous engine management systems and require significant investment in computational infrastructure and cybersecurity measures to ensure safe and reliable operation.

Workforce Shortages in Specialized Engineering Roles Hinder Innovation Capacity

Labor market challenges in the aerospace sector are further challenging the global market expansion. The complexity of modern engines requires expertise in thermodynamics, materials science, and digital analytics, which are in scarce supply globally. According to the National Association of Manufacturers, the aerospace industry faces a deficit of 200,000 skilled workers, including engineers and machinists, by 2025. This talent gap delays research and development projects as companies struggle to staff critical design and testing roles. As per Boeing, the average time to hire a specialized propulsion engineer has increased by 40% over the past five years due to intense competition from tech sectors. Universities are not producing enough graduates with the specific interdisciplinary skills required for next-generation engine development. Retention of senior experts is also challenging, as retirement rates accelerate among the baby boomer generation, who hold institutional knowledge. The loss of this expertise creates knowledge gaps that slow down problem-solving and innovation cycles. Training new employees takes several years before they become fully productive, further constraining output. This human capital crisis limits the ability of manufacturers to scale production and introduce new technologies rapidly. Without adequate staffing, companies face project delays and increased costs, which ultimately impact their competitiveness in the global market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.45% |

| Segments Covered | By Engine Type, Aircraft Type, Component, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, the Middle East and Africa, And Latin America |

| Market Leaders Profiled | GE Aerospace, RTX Corporation, Rolls-Royce Holdings plc, Safran Aircraft Engines, MTU Aero Engines AG, Honeywell Aerospace, CFM International, IAE International Aero Engines AG, Williams International, PBS Group, Textron Aviation, Aero Engine Corporation of China (AECC), Kawasaki Heavy Industries, Hanwha Aerospace, Kratos Defense & Security Solutions |

SEGMENTAL ANALYSIS

By Engine Type Insights

The turbofan engine segment accounted for 61.6% of the global market share in 2025 and is expected to maintain its dominant position in the industry for the next few years. This segment's leadership position stems from its universal application across commercial aviation, where narrow-body and wide-body aircraft constitute the backbone of global air transport fleets. The turbofan configuration delivers optimal fuel efficiency for medium to long-haul operations, which represent the largest revenue-generating routes for airlines worldwide. Modern turbofan designs incorporate advanced materials such as ceramic matrix composites and next-generation thermal barrier coatings that enable higher operating temperatures and improved thrust-to-weight ratios. The proliferation of single-aisle aircraft has created sustained demand for high-bypass ratio turbofans that offer double-digit fuel burn improvements over previous generation engines. Airlines prioritize these engines because they directly impact operational economics through reduced fuel consumption, which typically accounts for 30% of airline operating costs. The regulatory environment further reinforces turbofan dominance, as new type certificates require compatibility with sustainable aviation fuels and stricter noise regulations that modern turbofan architectures can meet more effectively than alternative propulsion types. Military applications also contribute significantly, with fifth-generation fighter programs and transport aircraft relying exclusively on turbofan technology for their mission requirements.

However, the hybrid electric propulsion segment is predicted to expand at a CAGR of 8.2% during the forecast period, owing to the aviation industry's urgent transition toward decarbonization and electrification, driven by international climate commitments and regulatory mandates. According to the European Union, ReFuelEU regulations require all new type certificates issued after 2025 to demonstrate full compatibility with 100% sustainable aviation fuel, which accelerates the development of hybrid architectures that can integrate multiple energy sources. Advanced air mobility vehicles, particularly urban air taxis and regional electric vertical takeoff and landing platforms, serve as primary catalysts for hybrid electric adoption, with companies like Joby Aviation and Archer Aviation receiving regulatory approvals that validate the commercial viability of these technologies. Research and development expenditures focus on gearbox lubrication and thermal management as priority targets, supporting this segment's outperformance within the broader aircraft engines market landscape.

By Aircraft Type Insights

The commercial aviation engine segment dominated the market by holding 44.1% of the global market share in 2025 and is projected to maintain its substantial market presence for the next few years. This leadership position reflects the fundamental role of single-aisle aircraft in global air transportation networks, where carriers deploy these platforms on high-frequency domestic and short-haul international routes that generate the majority of passenger traffic volumes. The Boeing 737 MAX and Airbus A320neo families drive this segment with combined order backlogs exceeding several thousand units that ensure production stability through the end of the decade. Airlines favor narrow-body configurations because they offer optimal seat-mile costs for routes under 3,000 nautical miles, while providing flexibility to adjust capacity through frequency changes rather than aircraft size modifications. The recovery from pandemic-era disruptions accelerated fleet renewal cycles as carriers replaced older, less efficient aircraft with new-generation models featuring LEAP and geared turbofan engines that deliver 20% fuel burn improvements. Regional expansion in Asia-Pacific markets, particularly India and Southeast Asia, creates additional demand, with Air India and VietJet Aviation alone accounting for substantial portions of recent narrow-body orders totaling more than 1,200 units between 2024 and 2025. Lessors report double-digit leasing rate increases, signaling strong residual value expectations that support manufacturer production planning. The aftermarket ecosystem surrounding commercial narrow-bodies generates substantial recurring revenue streams through maintenance, repair, and overhaul activities, with independent service providers capturing increasing market share. Supply chain localization initiatives in manufacturing hubs across Japan and the United Kingdom diversify risk while hedging currency exposure for original equipment manufacturers serving this critical segment.

On the other hand, the advanced air mobility segment is poised to be the fastest-growing aviation category through the next few years and is predicted to grow at a CAGR of 9.4% during the forecast period. This remarkable growth rate reflects the emergence of entirely new transportation paradigms focused on urban and regional connectivity using electric and hybrid propulsion systems. Regulatory milestones achieved by companies like Joby Aviation and Archer Aviation in obtaining type certifications validate the technical and safety feasibility of these platforms, opening pathways for commercial operations in major metropolitan areas. Cargo operators focusing on time-critical logistics represent early adopters, recognizing that advanced air mobility vehicles can bypass ground congestion and deliver packages within hours rather than days for distances under 200 miles. The integration of advanced air mobility into existing aviation infrastructure requires the development of vertiports and charging networks, creating parallel investment opportunities beyond aircraft manufacturing itself. Urban route economics demonstrate viability when vehicle utilization exceeds certain thresholds, with battery swap or rapid charging enabling multiple daily rotations. Investment flows from venture capital and strategic corporate investors exceed billions of dollars annually, reflecting confidence in market potential despite current pre-revenue stages for most participants. The electrification of subsystems feeds demand for high-power density generators that couple with small gas turbines in hybrid configurations, extending range capabilities beyond pure battery-electric limitations. Municipal governments partner with operators to establish pilot programs that gather real-world performance data while addressing community concerns about noise and visual impact. Workforce development initiatives train maintenance technicians and pilots in electric propulsion systems, creating employment opportunities in emerging occupational categories. Insurance frameworks evolve to address unique risk profiles associated with autonomous or remotely piloted operations in dense urban environments.

By Component Insights

The turbine assemblies segment had 35.9% of the global market share in 2025 and is expected to remain a critical and high-value component segment for the next few years. This dominant position reflects the extreme engineering complexity and material intensity of turbine modules, which operate at temperatures exceeding the melting points of conventional alloys, requiring sophisticated cooling architectures and exotic superalloy compositions. Each turbine stage experiences centrifugal forces measured in tens of thousands of Gs while exposed to combustion gases approaching 2,000 degrees Celsius, necessitating single-crystal blade manufacturing processes and thermal barrier coating applications that represent cutting-edge materials science achievements. The high replacement rates for turbine components stem from cumulative damage mechanisms, including creep, fatigue, oxidation, and foreign object damage, which progressively degrade performance margins over operational lifecycles. Airlines schedule shop visits based on flight-hour accumulation or calendar intervals, whichever occurs first, with turbine module inspections representing the most labor-intensive and costly aspects of engine overhauls. The strategic importance of turbine technology drives national security considerations, with export controls limiting technology transfers for military-grade applications. Research investments focus on ceramic matrix composites that promise weight reductions of 20% alongside temperature capability increases, enabling next-generation engine architectures with substantially improved specific fuel consumption metrics.

However, the gearbox systems segment is the fastest-growing component segment and is expected to record a CAGR of 6.3% during the forecast period, owing to the expanding penetration of geared turbofan architectures pioneered by Pratt and Whitney's PW1000G family and increasingly adopted across multiple aircraft programs. MTU Aero Engines invested 220 million US dollars in advanced machining capabilities at its Munich facility specifically to meet commitments for PW1000G gearbox output, illustrating the capital intensity required to support this growth segment. Geared turbofan designs decouple fan speed from low-pressure turbine rotation, allowing each component to operate at optimal rotational velocities, which delivers double-digit fuel burn improvements and significant noise reduction benefits valued by airports and communities near flight paths. Enhanced lubrication formulations and thermal management designs extend mean time between overhauls while maintaining propulsive efficiency advantages that justify the added mechanical complexity. The gearbox introduces additional failure modes compared to direct-drive architectures, requiring sophisticated health monitoring systems that track vibration signatures, oil particle counts, and temperature gradients to detect incipient faults before catastrophic failures occur. As geared turbofan installations accumulate flight hours, maintenance organizations gain experience with gearbox overhaul procedures, creating learning curves that reduce turnaround times and improve first-pass yield rates. The competitive landscape features limited qualified suppliers due to high barriers to entry, including extensive testing infrastructure requirements and long qualification timelines that protect incumbent manufacturers from new competition.

By End User Insights

The OEM factory-fit segment dominated the market by accounting for the 54.9% of the global market share in 2025 and is likely to remain the primary revenue engine for the market over the next few years. This leadership position reflects the fundamental business model where engine manufacturers sell new powerplants directly to aircraft manufacturers who integrate them during final assembly before delivering completed aircraft to airline customers. Production schedules for narrow-body aircraft, particularly the Boeing 737 MAX and Airbus A320neo families, drive the majority of factory-fit volume, with monthly output rates gradually recovering toward pre-pandemic peaks as supply chain constraints ease. Original equipment manufacturers negotiate long-term supply agreements with airframers that lock in pricing structures and delivery schedules spanning multiple years, providing revenue visibility and enabling capacity planning investments. The factory-fit segment benefits from economies of scale in manufacturing, where standardized production processes and automated assembly lines reduce unit costs compared to bespoke aftermarket solutions. Quality control procedures for factory-fit engines involve comprehensive testing protocols, including sea-level static tests, altitude chamber simulations, and endurance runs that verify performance against design specifications before release. New program launches create step-change opportunities for market share gains, as seen with CFM International's LEAP engine securing majority positions on both A320neo and 737 MAX platforms through aggressive pricing and performance commitments.

On the other hand, the replacement and aftermarket segment is expected to experience strong growth and is predicted to register a CAGR of 5.5% during the forecast period, owing to the expanding installed base of aircraft engines reaching mid-lifecycle stages where major overhauls, component replacements, and performance restorations become necessary to maintain airworthiness and operational efficiency. CFM International disclosed more than 1,000 LEAP performance restorations in 2025, underpinning 2 billion US dollars in service revenue, demonstrating the substantial economic value generated by aftermarket activities. Independent maintenance, repair, and overhaul organizations now command over 40% of CFM56 shop visits, representing a dramatic increase from 25% in 2020 as these third-party providers expand capacity and compete aggressively on price and turnaround time. Airlines leverage competitive quotes from multiple service providers to reduce cost per engine flight hour by up to 15%, creating powerful incentives to diversify maintenance sourcing strategies beyond original equipment manufacturer networks. Regulatory directives from aviation authorities compel original equipment manufacturers to share technical data and repair procedures with licensed third parties, limiting the exclusivity advantages that previously protected OEM service monopolies. Supply chain dynamics for aftermarket parts involve complex reverse logistics, remanufacturing processes, and inventory optimization challenges that require sophisticated enterprise resource planning systems to manage effectively across global networks.

REGIONAL ANALYSIS

North America Aircraft Engines Market Analysis

North America had the major share of the global market in 2025 and is expected to remain a leader in the global aircraft engines market during the forecast period. The region benefits from robust domestic manufacturing capabilities, strong defense procurement budgets, and mature commercial aviation infrastructure. The region hosts headquarters and major production facilities for leading original equipment manufacturers, including GE Aerospace in Cincinnati, Ohio, and Pratt and Whitney divisions of RTX Corporation in Connecticut, creating concentrated expertise clusters that drive innovation and employment. Boeing's 737 MAX production ramp-up in Renton, Washington, generates substantial demand for CFM LEAP engines, with monthly output rates steadily increasing toward target levels as supply chain bottlenecks gradually resolve. According to a 2026 GE Aerospace announcement, the company is investing US$ 1 billion across its U.S. manufacturing sites to accelerate engine deliveries and strengthen defense production. The United States Air Force Next Generation Adaptive Propulsion program represents a transformative opportunity, with adaptive cycle demonstrators competing for contracts that could exceed 1,000 engine deliveries in the 2030s, creating counter-cyclical revenue streams insulated from commercial aviation volatility. NATO alliance commitments drive multinational procurement programs, including multi-role tanker transport aircraft equipped with dual Trent 700 or V2500 powerplants that sustain production lines and support allied interoperability objectives. Canada contributes specialized expertise in regional aircraft propulsion through Pratt and Whitney Canada's turboprop and turboshaft divisions, serving business aviation and helicopter markets globally. Mexico emerges as a manufacturing hub, leveraging lower labor costs and proximity to United States facilities for component production and subassembly operations that integrate into North American supply chains. Sustainability initiatives, including sustainable aviation fuel blending mandates and hydrogen combustion research, receive substantial government funding through Department of Energy programs that de-risk private sector investments in breakthrough technologies.

Europe Aircraft Engines Market Analysis

Europe is poised for steady expansion as it navigates a structural transformation toward operational efficiency and environmental compliance over the forecast period. The continent occupies a critical position in the aircraft engines market, characterized by established aerospace manufacturing traditions, strong regulatory frameworks, and collaborative international programs that shape global industry standards. The continent hosts major original equipment manufacturers, including Rolls-Royce in the United Kingdom, Safran in France, and MTU Aero Engines in Germany, each contributing specialized technologies ranging from widebody turbofans to geared turbofan components and military propulsion systems. Airbus production facilities in Toulouse, France, Hamburg, Germany, and Seville, Spain, drive demand for engine installations on A320neo, A350, and A220 programs, though output rates remain below pre-pandemic peaks as supply chain recovery continues through 2026 and beyond. According to the European Union, ReFuelEU regulations mandate 100% sustainable aviation fuel compatibility for all new type certificates issued after 2025, forcing combustor and fuel system redesigns across every thrust class and accelerating research into alternative fuel architectures. Geared turbofan groundings related to Pratt and Whitney PW1100G powder metallurgy defects created temporary disruptions affecting European carriers, particularly Wizz Air, which finalized negotiations to power incoming A320neo fleets with these engines, highlighting the interdependence between engine reliability and airline fleet planning. Brexit implications continue affecting supply chain logistics and regulatory alignment between the United Kingdom and European Union jurisdictions, creating administrative burdens for cross-border component flows. Research collaborations through Clean Sky initiatives pool resources from multiple countries to develop open-rotor contra-rotating propeller technologies and hydrogen combustion demonstrators that address long-term decarbonization goals.

Asia Pacific Aircraft Engines Market Analysis

Asia Pacific is expected to experience the fastest regional growth over the next few years. The region is the largest market for aircraft engines globally, driven by unprecedented fleet expansion, manufacturing localization, and rising middle-class travel demand. China leads regional growth with domestic airlines placing substantial orders for narrow-body and wide-body aircraft to serve expanding route networks connecting tier-one cities with secondary markets, while indigenous engine programs through AECC progress toward commercial viability, though remaining several years away from displacing imported powerplants at scale. India emerges as a manufacturing powerhouse, with Air India's historic order placement and government initiatives promoting aerospace cluster development in Bangalore and Hyderabad, attracting original equipment manufacturer investments in component production and maintenance facilities. Japan contributes advanced materials expertise and precision manufacturing capabilities through companies like IHI Corporation and Mitsubishi Heavy Industries, which participate as risk-sharing partners in international engine programs supplying critical components for GE and Pratt and Whitney products. South Korea develops indigenous capabilities while maintaining strong partnerships with Western manufacturers, particularly in business jet and military trainer applications, where Hanwha Corporation provides transmission systems and structural components. Southeast Asian carriers, including VietJet Aviation, placed significant narrow-body orders accounting for substantial portions of the more than 1,200 units ordered regionally between 2024 and 2025, reflecting confidence in post-pandemic traffic recovery and tourism-driven demand. According to GE Aerospace, the company expects LEAP deliveries to remain strong as a significant portion enters Asian fleets, underscoring the region's centrality to global production planning. Rising disposable incomes and urbanization trends sustain long-term passenger traffic growth projections that justify fleet expansion plans and support engine demand trajectories through the forecast period.

Latin America Aircraft Engines Market Analysis

Latin America is anticipated to show gradual progress in market development as it continues to modernize fleets and improve regional connectivity over the next few years. The region occupies a developing position in the aircraft engines market, characterized by fleet modernization through operating leases, regional connectivity improvements, and gradual infrastructure investments that support aviation growth despite economic volatility. Brazil serves as the regional anchor, with Embraer's commercial and business jet production creating demand for Pratt and Whitney Canada turboprops and Honeywell turbofans, while Gol and LATAM Airlines pursue fleet renewal strategies, replacing aging aircraft with fuel-efficient narrow-bodies powered by CFM LEAP or IAE V2500 engines. Operating lease structures dominate acquisition strategies, allowing carriers to spread capital risk while accessing the latest-generation technology without large upfront investments, which is particularly important given currency fluctuation exposures and financing cost variations across the region. Argentina, Chile, and Colombia expand domestic and intra-regional route networks, stimulating demand for regional jets and turboprops suited to shorter sectors with lower passenger volumes where larger narrow-bodies prove uneconomical. Maintenance capabilities concentrate in Sao Paulo, Panama City, and Bogota, where authorized service centers perform line maintenance and minor repairs, though heavy overhauls often require shipment to North American or European facilities due to limited local infrastructure. Indigenous manufacturing aspirations remain limited, with most countries focusing on maintenance training and component distribution rather than design and production capabilities, given the capital intensity and technical barriers inherent in engine manufacturing.

Middle East and Africa Aircraft Engines Market Analysis

The Middle East and Africa region is projected to maintain a strong growth trajectory for the next few years. The region reflects ambitious fleet expansion plans, strategic geographic positioning, and unique operational challenges. Gulf carriers, including Emirates, Qatar Airways, and Etihad Airways, placed orders exceeding 400 GE9X and GEnx engines, underpinning forthcoming deliveries of Boeing 777X and 787 aircraft that will serve long-haul routes connecting Europe, Asia, and Africa through hub-and-spoke networks optimized for transit traffic. Ambient temperatures exceeding 50°C in hubs such as Dubai shorten turbine blade life by approximately 15%, increasing shop visit frequency and necessitating larger spare engine pools to maintain schedule reliability during hot summer months. Saudi Arabia's Vision 2030 initiative drives aviation infrastructure investments, including new airport construction and flag carrier expansion, creating sustained demand for wide-body and narrow-body engines as the kingdom diversifies its economy beyond oil dependence. Egypt serves as an African aviation hub with Egyptair pursuing fleet modernization, while Nigeria, Kenya, and Ethiopia develop regional connectivity through leased aircraft that spread capital requirements across multiple operators and lessors. Sustainable aviation fuel adoption faces infrastructure limitations, though Gulf states leverage financial resources to invest in production facilities and research partnerships that position the region as a future SAF hub serving both domestic and international aviation needs.

COMPETITION OVERVIEW

Competition in the aircraft engines market is characterized by high barriers to entry due to immense capital requirements and complex certification processes. A few dominant players control the majority of the market through established technological leadership and long-term contracts with airframers. Intense rivalry focuses on fuel efficiency, noise reduction, and maintenance costs as airlines prioritize operational economics. Innovation in sustainable aviation fuels and hybrid electric propulsion creates new competitive dimensions beyond traditional gas turbine performance. Aftermarket services represent a critical battleground where independent providers challenge original equipment manufacturers through competitive pricing and faster turnaround times. Regulatory compliance and safety records significantly influence purchasing decisions, making reliability a key differentiator. Geopolitical factors and trade policies impact supply chains and market access, requiring companies to maintain flexible global operations. The shift toward service-based revenue models alters competitive dynamics by emphasizing lifecycle value over initial sale price. Emerging technologies in additive manufacturing and digital analytics offer opportunities for disruptors to gain footholds in niche segments. Overall, the market remains consolidated but faces increasing pressure from sustainability mandates and technological disruption.

KEY MARKET PLAYERS

A few major players in the aircraft engines market include

- GE Aerospace

- RTX Corporation

- Rolls-Royce Holdings plc

- Safran Aircraft Engines

- MTU Aero Engines AG

- Honeywell Aerospace

- CFM International

- IAE International Aero Engines AG

- Williams International

- PBS Group

- Textron Aviation

- Aero Engine Corporation of China (AECC)

- Kawasaki Heavy Industries

- Hanwha Aerospace

- Kratos Defense & Security Solutions

Top Strategies Used by the Key Market Participants

Key players in the aircraft engines market prioritize research and development to enhance fuel efficiency and reduce emissions through advanced materials and aerodynamic designs. Strategic partnerships and joint ventures enable companies to share technological risks and access new markets while leveraging complementary expertise. Expansion into sustainable aviation fuel compatibility and hybrid electric propulsion systems addresses regulatory pressures and environmental concerns effectively. Service-oriented business models, such as power by the hour agreements, provide stable recurring revenue streams and deepen customer relationships. Supply chain localization and vertical integration efforts mitigate geopolitical risks and reduce lead times for critical components. Digital transformation initiatives, including predictive maintenance and digital twins, optimize operational performance and reduce downtime for airline customers globally.

Leading Players in the Global Market

- GE Aerospace stands as a dominant force in global propulsion through its CFM International joint venture with Safran. The company supplies LEAP engines for leading narrowbody aircraft, including the Airbus A320neo and Boeing 737 MAX families. Recent strategic moves include significant investments in additive manufacturing facilities to produce complex fuel nozzles and turbine blades more efficiently. GE Aerospace also advances sustainable aviation by testing hydrogen combustion technologies and hybrid electric architectures. Their commitment to digital services enhances engine performance monitoring and predictive maintenance capabilities for airline customers worldwide. This comprehensive approach ensures they remain at the forefront of technological innovation and operational reliability in the commercial and military aviation sectors globally.

- Rolls-Royce maintains a strong presence in widebody aviation with its Trent engine family powering Airbus A350 and Boeing 787 aircraft. The company focuses heavily on sustainability initiatives, including successful tests of one hundred% sustainable aviation fuel in its UltraFan demonstrator program. Rolls-Roycee recently secured contracts for next-generation military propulsion systems while expanding its nuclear small modular reactor business. Their strategic pivot emphasizes service-based models through TotalCare agreements that align revenue with engine availability and performance. Investments in advanced materials like ceramic matrix composites help improve thermal efficiency and reduce weight. These efforts reinforce their reputation for engineering excellence and long-term customer partnerships in both civil and defense markets.

- Pratt and Whitney drives innovation through its geared turbofan technology, which offers superior fuel efficiency and noise reduction benefits. The PW1000G series powers the Airbus A220 and A320neo families, along with the Embraer E2 regional jets. Recent actions include resolving material quality issues in powder metal components to restore full production rates and rebuild customer confidence. The company actively participates in the US Air Force Next Generation Adaptive Propulsion program, developing adaptive cycle engines for future fighter aircraft. Pratt and Whitney also invests in digital twin technologies to optimize maintenance schedules and extend component life cycles. These strategic initiatives strengthen their competitive position in both commercial narrowbody and high-performance military propulsion segments globally.

MARKET SEGMENTATION

This research report on the Global Aircraft Engines market has been segmented and sub-segmented based on engine type, aircraft type, component, end user, and region.

By Engine Type

- Turbofan

- Turboprop

By Aircraft Type

- Commercial Aviation

- Others

By Component

- Compressor

- Turbine

By End User

- OEM Factory-Fit

- Others

By Region

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What are the major factors driving the aircraft engines market?

Growing air passenger traffic, increasing aircraft deliveries, fleet modernization, rising defense spending, and advancements in fuel-efficient engine technologies are driving market growth.

2. What are the main types of aircraft engines?

The primary types include turbofan, turboprop, turboshaft, turbojet, and piston engines.

3. Which engine type dominates the market?

Turbofan engines dominate the market due to their widespread use in commercial passenger and cargo aircraft.

4. Which aircraft segment accounts for the largest market share?

Commercial aviation holds the largest share because of the increasing demand for air travel and continuous fleet expansion.

5. Which region leads the Global Aircraft Engines Market?

North America leads the market owing to the presence of major engine manufacturers, advanced aerospace infrastructure, and significant defense investments.

6. What are the major challenges facing the aircraft engines market?

High development costs, stringent certification requirements, supply chain disruptions, and expensive maintenance are key challenges.

7. What technologies are shaping the future of aircraft engines?

Advanced materials, digital engine monitoring, predictive maintenance, additive manufacturing, and next-generation propulsion systems are transforming the market.

8. How are sustainability initiatives influencing engine development?

Manufacturers are developing engines compatible with sustainable aviation fuels (SAFs), hybrid-electric propulsion, and hydrogen technologies to reduce emissions.

9. Who are the major customers in the aircraft engines market?

Commercial airlines, aircraft OEMs, military organizations, business jet operators, leasing companies, and MRO service providers are the primary customers.

10. What is the future outlook for the Global Aircraft Engines Market?

The market is expected to grow steadily, supported by increasing aircraft production, technological innovation, rising global air travel, and the industry's focus on fuel efficiency and sustainable aviation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com