Global Aircraft Nacelle and Thrust Reverser Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Nacelle, Thrust Reverser), Material, Platform, Engine Type, Application, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2026 to 2034

Global Aircraft Nacelle and Thrust Reverser Market Report Summary

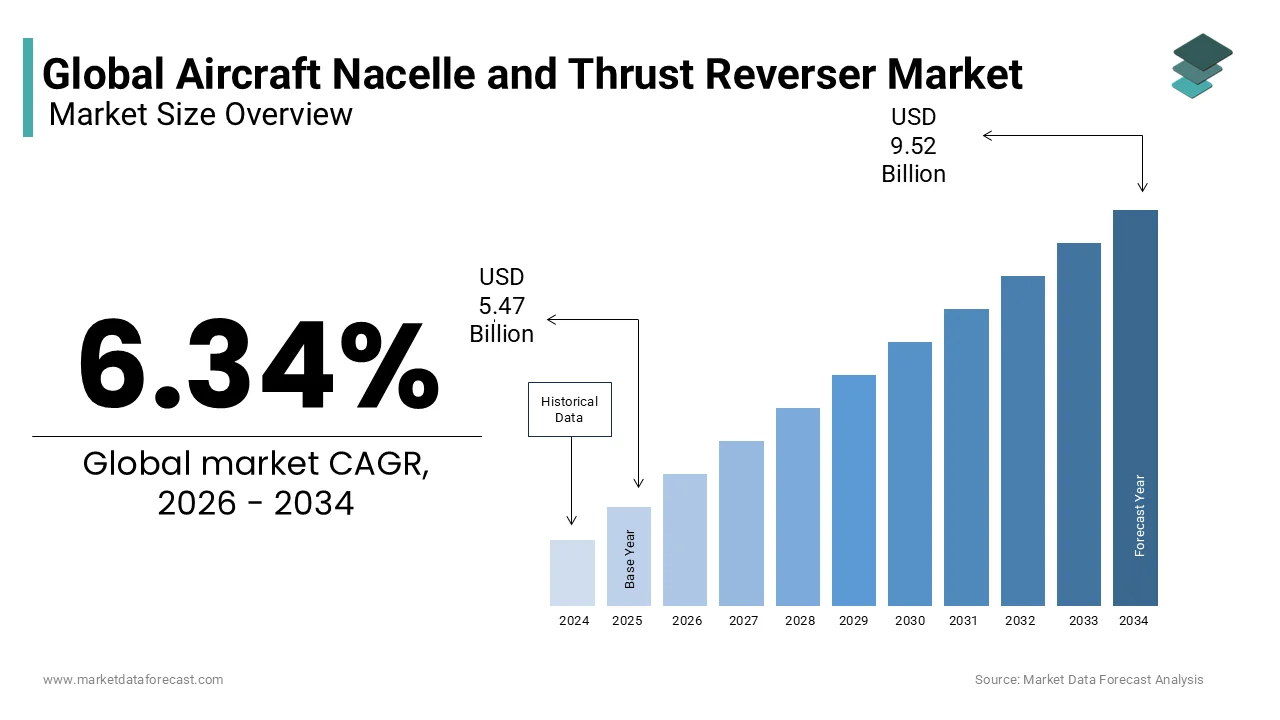

The global aircraft nacelle and thrust reverser market was valued at USD 5.47 billion in 2025, is estimated to reach USD 5.82 billion in 2026, and is projected to reach USD 9.52 billion by 2034, growing at a CAGR of 6.34% during the forecast period from 2026 to 2034. The growth of the global aircraft nacelle and thrust reverser market is driven by increasing commercial aircraft deliveries, rising air passenger traffic, and growing investments in fuel-efficient aircraft technologies. Aircraft manufacturers are increasingly adopting lightweight composite materials and advanced aerodynamic designs to improve fuel efficiency, reduce emissions, and enhance engine performance. Additionally, expanding aircraft fleet modernization programs, increasing maintenance, repair, and overhaul (MRO) activities, and growing demand for next-generation aircraft are further supporting market expansion.

Key Market Trends

-

Rising commercial aircraft production is driving demand for advanced nacelle and thrust reverser systems.

-

Increasing adoption of lightweight composite materials is improving fuel efficiency and reducing aircraft operating costs.

-

Growing investments in next-generation aircraft and engine technologies are accelerating product innovation.

-

Expansion of global maintenance, repair, and overhaul (MRO) activities is supporting aftermarket demand for nacelle components.

-

Increasing focus on reducing aircraft noise and carbon emissions is encouraging the development of advanced aerodynamic nacelle designs.

Segmental Insights

-

Based on type, the nacelle segment dominated the global aircraft nacelle and thrust reverser market in 2025. The segment's leadership is attributed to its critical role in improving engine aerodynamics, reducing drag, enhancing fuel efficiency, and protecting aircraft engines during operation.

-

Based on material, the composites segment held the largest share of the global aircraft nacelle and thrust reverser market in 2025. The segment's dominance is driven by the superior strength-to-weight ratio, corrosion resistance, and fuel-saving benefits offered by advanced composite materials.

-

Based on platform, the commercial aircraft segment accounted for the largest share of the global aircraft nacelle and thrust reverser market in 2025. The segment's growth is supported by increasing global passenger traffic, expanding airline fleets, and rising demand for fuel-efficient narrow-body and wide-body aircraft.

Regional Insights

-

The global aircraft nacelle and thrust reverser market is witnessing steady growth due to increasing aircraft production, expanding airline fleets, and continuous advancements in aerospace engineering.

-

North America dominated the global aircraft nacelle and thrust reverser market in 2025. The region's leadership is supported by the presence of major aircraft manufacturers, advanced aerospace manufacturing capabilities, significant defense spending, and a well-established aviation supply chain. The United States is expected to maintain its dominant position over the forecast period.

Competitive Landscape

The global aircraft nacelle and thrust reverser market is highly competitive, with leading aerospace companies focusing on lightweight materials, aerodynamic innovations, advanced manufacturing technologies, and strategic collaborations to strengthen their market positions. Manufacturers are investing in research and development, next-generation engine integration, and sustainable aerospace solutions to improve aircraft performance, reduce emissions, and enhance operational efficiency. Key players operating in the global aircraft nacelle and thrust reverser market include RTX Corporation, Safran Nacelles, Spirit AeroSystems, Inc., GKN Aerospace, Leonardo S.p.A., Airbus SE, Boeing, Collins Aerospace, Barnes Group Inc., Triumph Group, Inc., Middle River Aerostructure Systems, FACC AG, Nexcelle, ST Engineering, Ducommun Incorporated, and Aernnova Aerospace.

Global Aircraft Nacelle and Thrust Reverser Market Size

The global aircraft nacelle and thrust reverser market size was valued at USD 5.47 billion in 2025, and is expected to be worth USD 9.52 billion by 2034 from USD 5.82 billion by 2026. The market is growing at a CAGR of 6.34% during the forecast period.

Aircraft nacelle and thrust reversers are specialized aerodynamic structures and mechanical systems that house jet engines and facilitate deceleration during landing operations. Nacelles serve as the primary interface between the engine and the airframe, providing structural support, thermal insulation, and acoustic damping, while optimizing airflow into the fan section. Thrust reversers are critical safety components, integrated within the nacelle, that redirect engine exhaust forward to generate reverse thrust, significantly reducing landing distances and wear on wheel brakes. According to the International Air Transport Association, global air passenger traffic rose by 10.4% in 2024, reflecting a robust recovery that has intensified the operational tempo of commercial fleets worldwide. This surge in flight cycles directly accelerates the wear and tear on nacelle components and thrust reversal mechanisms and this requires frequent maintenance and eventual replacement. The European Union Aviation Safety Agency mandates rigorous certification standards for these systems, ensuring they meet strict requirements for structural integrity, deployment reliability, and noise reduction. Furthermore, the industry is increasingly focusing on lightweight composite materials to reduce overall aircraft weight, thereby improving fuel efficiency and lowering carbon emissions. As airlines prioritize operational efficiency and environmental compliance, the demand for advanced nacelle designs, featuring integrated acoustic liners and efficient thrust reversal technologies, continues to shape the strategic direction of this specialized aerospace sector.

MARKET DRIVERS

Expansion of High Bypass Ratio Engine Fleet Drives Demand for Advanced Nacelles

The widespread adoption of high bypass ratio turbofan engines in modern commercial aviation is majorly driving the aircraft nacelle and thrust reverser market growth, due to the unique structural and aerodynamic requirements of these powerplants. According to the Boeing 2025 Commercial Market Outlook, the global passenger widebody fleet is projected to increase to approximately 8,320 airplanes by the next two decades as long-haul international travel recovers. These engines feature larger fan diameters to improve propulsive efficiency, requiring correspondingly larger and more complex nacelles to manage airflow and minimize drag. The increased size and weight of these nacelles necessitate the use of advanced composite materials, such as carbon fiber reinforced polymers, to maintain structural integrity without compromising fuel economy. Furthermore, high bypass engines generate significant noise levels during operation, prompting manufacturers to integrate sophisticated acoustic treatment systems within the nacelle structure. These acoustic liners are essential for meeting stringent international noise regulations imposed by airports and regulatory bodies. The complexity of integrating thrust reversers into these larger nacelles also drives innovation in mechanical design, ensuring reliable deployment and stowage. As airlines continue to replace older, less efficient aircraft with new-generation models equipped with high bypass engines, the demand for specialized nacelle and thrust reverser systems will remain robust, sustaining market growth.

Stringent Noise Regulations Mandate Integration of Advanced Acoustic Liners

Strict environmental regulations governing aircraft noise emissions are compelling airlines and manufacturers to invest heavily in nacelles equipped with advanced acoustic suppression technologies, which is further fuelling the global market expansion. According to International Civil Aviation Organization standards, Chapter 14 noise regulations require new aircraft types to demonstrate significantly lower noise footprints compared to previous generations to mitigate environmental impact. Nacelles play a crucial role in noise reduction by housing acoustic liners made from honeycomb structures and perforated facesheets that absorb sound waves generated by the fan and jet exhaust. The integration of these liners requires precise engineering and manufacturing processes to ensure optimal acoustic performance without adding excessive weight or aerodynamic drag. Furthermore, airports in densely populated urban areas often impose curfews or operational restrictions on noisy aircraft, creating a strong financial incentive for airlines to operate quieter fleets. This regulatory pressure drives the continuous development of novel acoustic materials and nacelle designs that offer superior noise attenuation. Manufacturers are also exploring active noise control technologies that can be integrated into the nacelle structure to further reduce community noise impact. The uncompromising requirement to comply with evolving noise standards ensures that acoustic optimization remains a key focus area for nacelle developers, thereby driving sustained demand for advanced nacelle and thrust reverser systems.

MARKET RESTRAINTS

High Manufacturing Costs of Composite Materials Restrict Market Accessibility

The exorbitant costs associated with manufacturing and processing advanced composite materials that are essential for modern lightweight designs is impeding the aircraft nacelle and thrust reverser market growth. According to the Aerospace Industries Association, the production of carbon fiber reinforced polymer components involves complex layup processes, autoclave curing, and precision machining that require substantial capital investment and specialized labor. These high manufacturing costs are passed on to airlines and original equipment manufacturers, increasing the overall procurement price of nacelle systems. Furthermore, the supply chain for high-quality carbon fiber and resin systems is concentrated among a few global suppliers, leading to price volatility and potential supply bottlenecks. The lengthy certification process for new composite materials also adds to the development timeline and cost burden, delaying time-to-market for innovative designs. Small and medium-sized enterprises often struggle to compete with large, established players who can absorb these high upfront costs, limiting competition and innovation in the sector. Additionally, the repair and maintenance of composite nacelles require specialized tools and trained technicians, further increasing lifecycle costs for operators. This financial barrier restricts the widespread adoption of next-generation materials and slows the pace of technological advancement in the nacelle and thrust reverser market.

Complexity of Integrating Thrust Reversers with Compact Engine Designs

Integrating thrust reverser mechanisms into increasingly compact and efficient engine designs is further hampering the global market growth. Modern high bypass ratio engines have larger fan diameters but shorter nacelle lengths to reduce weight and drag, leaving limited space for the complex mechanical linkages and actuators required for thrust reversal. As per industry engineering standards, designers must utilize innovative folding door or cascade vane designs that can stow efficiently within the tight confines of the nacelle while maintaining structural rigidity during deployment. The complexity is further compounded by the need to ensure seamless aerodynamic continuity between the nacelle and the engine core to prevent flow separation and performance losses. Additionally, the thermal management of thrust reverser components exposed to hot exhaust gases requires advanced materials and cooling strategies that add weight and cost. Ensuring reliable operation under extreme environmental conditions, including ice ingestion and bird strikes, necessitates rigorous testing and validation, which extends development timelines. These intricate engineering challenges increase the risk of project delays and cost overruns, thereby restraining the speed at which new nacelle and thrust reverser technologies can be fielded. Manufacturers must balance performance, weight, and reliability constraints, which is making the integration process a critical bottleneck in product development.

MARKET OPPORTUNITIES

Adoption of Additive Manufacturing for Complex Nacelle Components

The emergence of additive manufacturing technologies is a significant opportunity for the aircraft nacelle and thrust reverser market by enabling the production of complex, lightweight components with reduced material waste. According to General Electric, additive manufacturing allows for the creation of intricate geometric structures, such as lattice infills and optimized brackets, that are impossible to achieve through traditional subtractive methods. This technology significantly reduces the weight of nacelle components, contributing to overall fuel efficiency improvements and lower operating costs for airlines. Furthermore, additive manufacturing enables rapid prototyping and iteration, accelerating the design and testing phases for new nacelle configurations. Manufacturers can produce customized parts on-demand, reducing inventory holding costs and lead times for spare parts. The ability to consolidate multiple parts into single printed assemblies also simplifies assembly processes and reduces the number of fasteners required, enhancing structural integrity. As metal 3D printing technologies mature and become more cost-effective, they offer a viable alternative for producing high-strength, heat-resistant components for thrust reverser mechanisms. This technological leap creates a premium market segment for innovatively designed nacelle parts that deliver superior performance through advanced manufacturing techniques.

Development of Smart Nacelles with Integrated Health Monitoring Systems

The integration of Internet of Things sensors and health monitoring systems into aircraft nacelles offers a promising opportunity for the global aircraft nacelle and thrust reverser market. According to the SITA Air Transport IT Insights report, over 60% of airlines are investing in predictive maintenance technologies to reduce unscheduled downtime and optimize asset utilization. Smart nacelles, equipped with embedded sensors, can monitor parameters such as vibration, temperature, strain, and acoustic performance in real-time, transmitting data to ground stations for analysis. This capability allows maintenance crews to identify potential issues, such as loose panels or degraded acoustic liners, before they lead to failures, reducing the need for costly inspections and repairs. Furthermore, the data collected from smart nacelles provides valuable insights for designers to improve future iterations of nacelle structures and thrust reverser mechanisms. Manufacturers who develop open-architecture sensor platforms can partner with software providers to create comprehensive health management ecosystems. This shift from passive structural components to intelligent, connected systems opens new revenue streams through data services and subscription-based maintenance models, driving innovation and value creation in the market.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Specialized Composite Materials

The aircraft nacelle and thrust reverser market faces significant challenges due to supply chain vulnerabilities for specialized composite materials, such as carbon fiber and high-performance resins. According to the United States Geological Survey, the global supply of precursor materials for carbon fiber is concentrated in a few regions, making it susceptible to geopolitical tensions and trade restrictions. Disruptions in the supply of these critical inputs can lead to prolonged lead times and production delays for nacelle manufacturers who rely on just-in-time inventory models. Additionally, the stringent quality requirements for aerospace-grade composites mean that alternative sources cannot be easily qualified without extensive testing and validation. This dependency on a limited supplier base increases the risk of price spikes and availability shortages, impacting the profitability of nacelle programs. Furthermore, the energy-intensive nature of composite production makes it vulnerable to fluctuations in energy prices, adding another layer of uncertainty to manufacturing costs. Mitigating these supply chain risks requires diversifying sourcing strategies and investing in domestic production capabilities, but these measures take time and significant capital to implement effectively.

Regulatory Hurdles for Certification of Novel Materials and Designs

The rigorous certification process mandated by aviation authorities is another significant challenge to the aircraft nacelle and thrust reverser market growth. According to the Federal Aviation Administration, obtaining type certification for new composite structures or thrust reverser mechanisms can take several years, involving extensive laboratory tests, flight trials, and documentation reviews. This lengthy timeline delays the commercialization of new products and increases research and development costs for manufacturers who must maintain multiple prototype versions during the approval phase. Furthermore, any minor design change requires re-certification, which stifles innovation and discourages manufacturers from introducing incremental improvements to existing products. The high barrier to entry created by these regulatory requirements protects incumbent players but limits competition from smaller innovators who may lack the resources to navigate the complex approval process. Additionally, differences in certification standards between regions require manufacturers to undergo separate approval processes for each market, further complicating global product launches. This regulatory burden slows the pace of technological adoption in the nacelle market, as operators wait for certified solutions rather than adopting cutting-edge but unapproved technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.34% |

| Segments Covered | By Type, Material, Platform, Engine Type, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | RTX Corporation, Safran Nacelles, Spirit AeroSystems, Inc., GKN Aerospace, Leonardo S.p.A., Airbus SE, Boeing, Collins Aerospace, Barnes Group Inc., Triumph Group, Inc., Middle River Aerostructure Systems, FACC AG, Nexcelle, ST Engineering, Ducommun Incorporated, and Aernnova Aerospace |

SEGMENTAL ANALYSIS

By Type Insights

The nacelle segment dominated the market by capturing the highest share of the global market in 2025. The dominance of nacelle segment in the global market is majorly primarily driven by the fundamental requirement that every single aircraft engine must be enclosed within a comprehensive outer housing to manage aerodynamics and structural integration. According to the Airbus Global Market Forecast, the global commercial fleet is projected to reach approximately 49,210 aircraft by 2044, and every single one of these airframes necessitates at least two large structural nacelles to enclose the powerplant. The nacelle encompasses the inlet, fan cowl, core cowl, and exhaust systems, representing a significantly higher material and manufacturing value per unit than the internal reversal mechanism alone. This fundamental requirement ensures that the nacelle segment maintains absolute dominance in terms of volume and revenue within the broader market landscape. Furthermore, the nacelle serves as the primary structural interface between the engine and the aircraft wing, requiring complex load-bearing designs that elevate its engineering complexity and procurement cost.

On the other end, the thrust reverser segment is expanding at the fastest and is predicted to grow at a promising CAGR of 7.2% during the forecast period owing to the rapid transition toward ultra-high bypass ratio engines and geared turbofan architectures. As per technical specifications from engine manufacturers, the new generation geared turbofan engines often require lighter-weight thrust reverser systems that must handle higher airflow volumes. This technological shift forces manufacturers to develop novel cascade vane and translating cowl designs, driving a rapid cycle of research, development, and procurement. The larger fan diameters of modern engines alter the exhaust flow dynamics, necessitating completely redesigned reversal mechanisms to maintain optimal aerodynamic efficiency. As airlines aggressively retire older fleets in favor of these next-generation powerplants, the demand for advanced thrust reversers tailored to specific new engine models accelerates at an unprecedented pace, establishing it as the fastest-growing segment.

By Material Insights

The composites segment led the market by holding the leading share of the global market in 2025. The growth of the composites segment in the global market can be credited to the unparalleled strength-to-weight ratio these materials offer, which is absolutely crucial for reducing overall aircraft weight and significantly improving fuel efficiency. According to Boeing, the extensive use of carbon fiber reinforced polymers in modern nacelle fan cowls and inlet structures reduces component weight by up to 30% compared to traditional aluminum equivalents. This substantial weight reduction directly translates into lower fuel burn and reduced carbon emissions, aligning perfectly with the strict environmental mandates set by international aviation authorities. As airlines prioritize operational economics and sustainability, the procurement of composite nacelles has become the industry standard. The ability to mold complex aerodynamic shapes from composite materials also allows engineers to optimize airflow around the engine, further enhancing the overall propulsive efficiency of the aircraft.

However, the thermoplastics segment is experiencing the fastest growth and is predicted to record a CAGR of 9.2% during the forecast period owing to the unique advantage of being fully recyclable and capable of being rapidly thermoformed. According to industry analysis, thermoplastic composite manufacturing cycles are up to 50% faster than traditional thermoset composites, allowing manufacturers to scale production efficiently to meet surging aircraft delivery rates. This rapid formability enables complex geometries to be produced with minimal material waste, appealing to manufacturers seeking to optimize their supply chains and reduce production costs. Unlike thermoset materials, thermoplastics can be melted and reshaped, which significantly simplifies the repair process and reduces the amount of scrap generated during manufacturing. As the aviation industry pushes for faster production rates and sustainable manufacturing practices, the adoption of thermoplastics is accelerating rapidly.

By Platform Insights

The commercial aircraft segment held the highest share of the global market in 2025 and is likely to remain the dominant market for the next few years due to the sustained demand for new narrowbody and widebody jets. The commercial aircraft segment holds the leading position in the market due to the sheer volume of production and the massive scale of the global passenger fleet, which dwarfs all other aviation platforms combined. According to Airbus, the global commercial aviation fleet is projected to reach over 48,000 aircraft by 2042, requiring millions of commercial-grade nacelles and thrust reversers to equip these airframes. Every new narrow-body and wide-body jet delivered necessitates a complete set of highly engineered nacelle systems, generating massive baseline demand. This continuous and high-volume production cycle guarantees that the commercial aircraft platform will remain the undisputed leader in terms of revenue and unit shipments. Furthermore, the intense competition among commercial airlines drives continuous upgrades to cabin noise reduction and exterior aerodynamics, ensuring a steady stream of orders for advanced nacelle technologies.

On the other side, the business jets segment is likely to see the fastest growth over the next few years as manufacturers focus on cabin quietness and range and grow at a CAGR of 8.1% during the forecast period due to the rapid expansion of the ultra-long-range market, which requires highly specialized and acoustically optimized nacelles. For instance, deliveries of business jets have remained strong, driving intense demand for bespoke composite nacelles that reduce cabin noise. Corporate travelers demand exceptionally quiet and smooth flight experiences, prompting manufacturers to integrate advanced acoustic treatments and aerodynamic refinements directly into the nacelle design. This premium focus on passenger experience and performance drives rapid innovation and procurement. The ability to offer a whisper-quiet cabin environment is a critical differentiator for business jet manufacturers, establishing this platform as the fastest-growing segment in the nacelle market.

REGIONAL ANALYSIS

North America Aircraft Nacelle and Thrust Reverser Market Analysis

North America held the largest share of the global market in 2025. The United States is expected to maintain its leadership in the North American market for the next few years due to its robust fleet renewal activity. The United States occupies a dominant position in the North American aircraft nacelle and thrust reverser market, accounting for approximately 35% of the global revenue share. The market status is characterized by massive domestic fleet operations and the presence of leading aerospace manufacturing conglomerates. According to the Federal Aviation Administration, the United States possesses the largest commercial aviation network in the world, handling over 900 million passengers annually. This immense volume necessitates the continuous procurement of durable and highly efficient nacelle systems for narrow-body and wide-body aircraft. The primary driving factor is the intense focus on fleet modernization and weight reduction, aligning with strict environmental mandates that accelerate the adoption of lightweight composite nacelles. Furthermore, the robust supply chain and advanced engineering capabilities within the country ensure that the United States remains the undisputed leader in the North American market, driving continuous innovation in thrust reverser technologies and acoustic suppression systems.

Europe Aircraft Nacelle and Thrust Reverser Market Analysis

Europe captured a prominent share of the global market in 2025. France is likely to continue its central role in the European market for the next few years as it continues to advance propulsion integration and aerodynamic design. France serves as the central powerhouse of the European aircraft nacelle and thrust reverser market, a region that holds roughly 28% of the global share. The market status is heavily influenced by the presence of major airframe manufacturers and a strong emphasis on premium aerodynamic innovation. According to industry reports, the European aerospace ecosystem is a global leader in developing advanced nacelle structures that integrate sophisticated acoustic liners and lightweight composite materials. The primary driving factor is the stringent regulatory environment regarding passenger safety and environmental sustainability, which compels manufacturers to integrate advanced materials and energy-efficient designs. Additionally, the high concentration of long-haul international flights originating from European hubs creates a strong demand for highly optimized thrust reversers. The collaborative research initiatives between European universities and aerospace firms foster continuous technological advancements, ensuring France remains a critical hub for high-value nacelle technologies and next-generation propulsion integration.

China Aircraft Nacelle and Thrust Reverser Market Analysis

China is poised to remain the fastest-growing market in the Asia-Pacific region for the next few years as it expands its infrastructure and fleet capacity. China stands as the fastest-growing and most influential market in the Asia-Pacific aircraft nacelle and thrust reverser sector, a region that commands approximately 22% of the global share. The market status is defined by unprecedented fleet expansion and a rapidly expanding middle class with a strong preference for air travel. According to the Civil Aviation Administration of China, the nation plans to hit 450 civil airports by 2035, requiring thousands of new aircraft equipped with modern nacelle systems. The primary driving factor is the aggressive modernization of domestic airline fleets and the push for technological self-reliance. The Chinese government is actively promoting the localization of aerospace supply chains, encouraging domestic manufacturers to develop indigenous composite nacelle technologies to reduce reliance on foreign imports. This massive scale of aircraft deliveries ensures that China will continue to drive the growth and technological innovation of the market in the Asia-Pacific region.

Brazil Aircraft Nacelle and Thrust Reverser Market Analysis

Brazil is expected to sustain steady growth in its regional market over the next few years as its regional connectivity continues to improve. Brazil maintains a commanding position in the Latin American aircraft nacelle and thrust reverser market, a region that accounts for roughly 8% of the global share. The market status is marked by gradual fleet modernization and the integration of advanced systems onto newly acquired regional platforms. According to Brazilian civil aviation authorities, the recent expansion of the regional jet fleet has necessitated the procurement of state-of-the-art nacelle and thrust reverser systems. The primary driving factor is the need to secure vast territorial borders and improve regional connectivity, which requires durable and reliable nacelle components capable of withstanding diverse operational environments. Additionally, local aerospace industries are developing specialized retrofit solutions to extend the service life of older aircraft, focusing on cost-effective composite upgrades. The combination of new platform acquisitions and regional connectivity demands ensures a steady market growth in Brazil and the broader Latin American region.

United Arab Emirates Aircraft Nacelle and Thrust Reverser Market Analysis

The United Arab Emirates is expected to lead the Middle East and Africa market for the next few years by continuing to invest in high-efficiency long-haul technology. The United Arab Emirates acts as the primary catalyst for the Middle East and Africa aircraft nacelle and thrust reverser market, a region that holds approximately 7% of the global share. The market status is renowned for its ultra-premium aviation hubs and the highest concentration of luxury wide-body configurations globally. According to the General Civil Aviation Authority, the United Arab Emirates is home to major international carriers that operate extensive fleets of wide-body aircraft featuring highly optimized nacelles for long-haul efficiency. The primary driving factor is the relentless pursuit of operational excellence and fuel efficiency on ultra-long routes, which requires the most advanced lightweight nacelle structures available in the market. Furthermore, the extreme ambient temperatures in the region necessitate the use of highly durable and heat-resistant thrust reverser components. The combination of massive traffic volumes and extreme operating conditions drives premium demand for advanced nacelle systems.

COMPETITIVE LANDSCAPE

Competition in the aircraft nacelle and thrust reverser market is characterized by a highly consolidated landscape dominated by a few major aerospace suppliers with extensive technical expertise and established relationships with engine manufacturers. High barriers to entry due to stringent safety certifications complex engineering requirements and significant capital investment protect incumbent players from new competitors. Leading companies differentiate themselves through superior material science innovations advanced acoustic suppression technologies and seamless integration capabilities with next generation engines. Price competition is moderate as airlines and original equipment manufacturers prioritize reliability weight savings and noise reduction over initial cost savings for these critical structural components. However vendors compete aggressively on lifecycle support services customization capabilities and speed of delivery for both linefit and retrofit projects. The shift toward sustainable materials and smart monitoring systems creates new battlegrounds for innovation where technological agility becomes a key differentiator. Strategic alliances with material suppliers and technology firms are frequently utilized to share development risks and access specialized expertise. Regional players focus on niche markets or specific component supplies while global leaders leverage their broad portfolios to secure large scale fleet contracts. Overall the market remains stable with continuous technological advancement and strong demand for fuel efficient solutions driving sustained competitive intensity among top tier manufacturers who continuously invest in automation and digitalization.

KEY MARKET PLAYERS

Some of the key players dominating the global aircraft nacelle and thrust reverser market are

- RTX Corporation

- Safran Nacelles

- Spirit AeroSystems, Inc.

- GKN Aerospace

- Leonardo S.p.A.

- Airbus SE

- Boeing

- Collins Aerospace

- Barnes Group Inc.

- Triumph Group, Inc.

- Middle River Aerostructure Systems

- FACC AG

- Nexcelle

- ST Engineering

- Ducommun Incorporated

- Aernnova Aerospace

Top Players in the Market

- Safran Nacelles stands as a global leader in the design and manufacturing of aircraft nacelle systems providing comprehensive solutions for commercial and military aviation. The company specializes in advanced composite structures and integrated thrust reverser mechanisms that optimize aerodynamic performance and reduce noise levels. Recent strategic initiatives include the expansion of production facilities to support next generation engine programs such as the CFM LEAP and Pratt and Whitney geared turbofan. Safran actively collaborates with engine manufacturers to develop lightweight acoustic liners and smart monitoring systems. Their commitment to sustainability is evident in the adoption of recyclable thermoplastic materials and energy efficient manufacturing processes. By focusing on innovation and operational excellence Safran continues to enhance its reputation for delivering high quality and reliable nacelle solutions worldwide.

- Collins Aerospace contributes significantly to the market through its extensive portfolio of nacelle and thrust reverser systems serving a wide range of aircraft platforms. The company leverages deep engineering expertise to deliver robust and lightweight structures that meet stringent safety and performance standards. Recent actions to strengthen its position involve investing in advanced manufacturing technologies such as automated fiber placement and additive manufacturing to improve production efficiency. Collins Aerospace also expands its service network globally to provide rapid maintenance and repair support for airline customers. The company focuses on integrating digital health monitoring sensors into nacelle components to enable predictive maintenance. Through continuous technological advancement and customer centric service Collins Aerospace maintains a strong competitive edge in the global aerospace supply chain.

- Spirit AeroSystems plays a pivotal role in the aircraft nacelle market by supplying high volume structural components and thrust reverser systems for major airframers. The company specializes in large scale composite manufacturing and precision assembly services that ensure consistent quality and timely delivery. Recent efforts to bolster its market presence include securing long term contracts for new narrow body aircraft programs and expanding its global manufacturing footprint. Spirit AeroSystems actively partners with original equipment manufacturers to co develop innovative nacelle designs that reduce weight and improve fuel efficiency. The company emphasizes lean manufacturing principles and supply chain optimization to maintain cost competitiveness. By prioritizing operational reliability and strategic partnerships Spirit AeroSystems delivers critical propulsion integration solutions that support the growth of the global aviation industry.

Top Strategies Used by the Key Market Participants

Key players in the aircraft nacelle and thrust reverser market prioritize research and development to create lightweight composite structures that reduce overall aircraft weight and improve fuel efficiency. Strategic partnerships with engine manufacturers enable companies to integrate nacelle systems seamlessly into new propulsion architectures ensuring optimal aerodynamic performance. Expansion into sustainable manufacturing practices including the use of recyclable thermoplastics and additive manufacturing helps participants meet environmental regulations and reduce production waste. Investment in digital health monitoring technologies allows for predictive maintenance and enhanced operational reliability for airline customers. Focus on global supply chain resilience and localized production capabilities mitigates geopolitical risks and ensures timely delivery of critical components to meet surging aircraft production demands.

MARKET SEGMENTATION

This research report on the global aircraft nacelle and thrust reverser market is segmented and sub-segmented into the following categories.

By Type

- Nacelle

- Thrust Reverser

By Material

- Composites

- Metals

- Alloys

- Thermoplastics

By Platform

- Commercial Aircraft

- Military Aircraft

- Business Jets

- Helicopters

By Engine Type

- Turbofan

- Turboprop

- Turbojet

By Application

- Landing

- Takeoff

- In-flight

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the Aircraft Nacelle and Thrust Reverser Market?

The Aircraft Nacelle and Thrust Reverser Market includes the design, manufacturing, and maintenance of nacelles and thrust reverser systems that improve engine performance, aerodynamics, and aircraft braking efficiency.

What factors are driving the growth of the Aircraft Nacelle and Thrust Reverser Market?

Rising aircraft deliveries, increasing air passenger traffic, fleet modernization, and growing demand for fuel-efficient aircraft are the primary drivers of market growth.

What is the function of an aircraft nacelle?

An aircraft nacelle houses the engine, improves aerodynamic performance, reduces engine noise, and protects critical engine components from external environmental conditions.

What is a thrust reverser, and why is it important?

A thrust reverser redirects engine exhaust during landing to help slow the aircraft, reducing landing distance and minimizing wear on wheel brakes.

Which aircraft segment holds the largest share of the Aircraft Nacelle and Thrust Reverser Market?

Commercial aircraft account for the largest market share due to increasing global air travel, expanding airline fleets, and growing aircraft production.

What materials are commonly used in aircraft nacelles and thrust reversers?

Manufacturers commonly use composites, aluminum alloys, titanium alloys, thermoplastics, and other lightweight materials to improve fuel efficiency and durability.

Which engine types use nacelles and thrust reversers?

These systems are primarily used in turbofan engines, while certain applications also include turboprop and turbojet-powered aircraft.

Which region dominates the Aircraft Nacelle and Thrust Reverser Market?

North America holds a significant market share due to the presence of leading aircraft manufacturers and aerospace suppliers, while Asia-Pacific is expected to experience the fastest growth.

What challenges does the Aircraft Nacelle and Thrust Reverser Market face?

High manufacturing costs, stringent aviation safety regulations, complex certification processes, and supply chain disruptions are key market challenges.

What is the future outlook for the Aircraft Nacelle and Thrust Reverser Market?

The market is expected to grow steadily over the coming years, driven by rising aircraft production, technological advancements, growing airline investments, and increasing demand for lightweight and fuel-efficient aerospace components.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com