Asia Pacific Cloud-Based Contact Center Market Size, Share, Trends, & Growth Forecast Report By Solution (ACD, APO, Diallers, IVR, CTI, Reporting and Analytics, and Security), Service (Professional and Managed), Application, Deployment Model, Organization Size, Vertical and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2024 to 2033

Asia Pacific Cloud-Based Contact Center Market Size

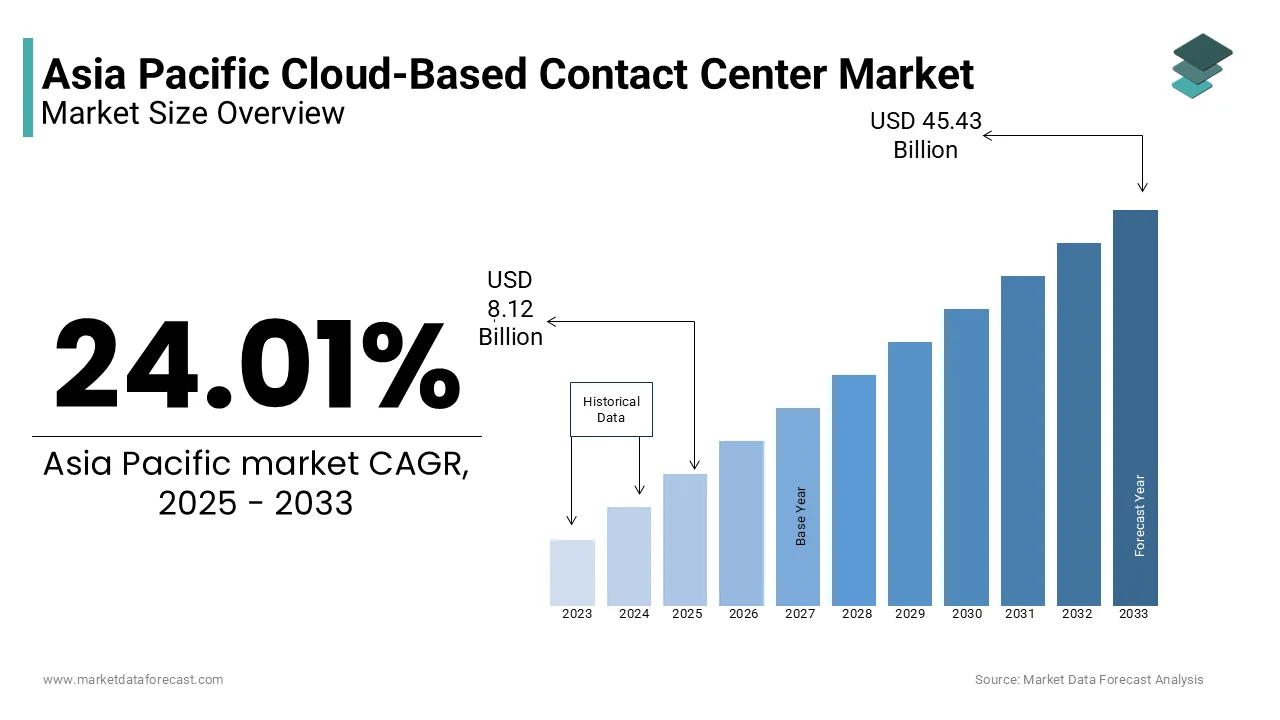

The Asia Pacific cloud-based contact center market was worth USD 6.55 billion in 2024. The Asia Pacific market is expected to register a CAGR of 24.01% from 2025 to 2033, and the Asia Pacific market is predicted to be worth USD 45.43 billion by 2033 from USD 8.12 billion in 2025.

Cloud-based contact center market refers to the deployment of customer engagement platforms through cloud computing infrastructure across countries in the region. These systems enable businesses to manage customer interactions via multiple channels such as voice, chat, email, and social media without relying on traditional on-premise infrastructure. This model offers scalability, cost-efficiency, and integration with AI-driven analytics, making it a preferred solution for enterprises aiming to enhance customer experience while optimizing operational costs.

In recent years, the adoption of cloud-based contact centers has surged across industries like BFSI, retail, healthcare, and telecom in the Asia Pacific region. The rise in digital transformation initiatives, increasing internet penetration, and growing demand for omnichannel communication are shaping the market dynamics significantly.

MARKET DRIVERS

Rising Digital Transformation Initiatives Across Enterprises

Digital transformation is a key catalyst driving the adoption of cloud-based contact center solutions in the Asia Pacific region. Businesses are increasingly investing in technologies such as artificial intelligence (AI), machine learning (ML), and robotic process automation (RPA) to modernize customer service operations. In Japan, where labor shortages are a persistent challenge, companies are leveraging cloud contact centers to automate routine tasks and reduce dependency on human agents.

Moreover, governments across the region are promoting digital infrastructure development. Like, in India, the government’s push toward digital payments and e-governance has led to an increased need for scalable customer engagement platforms. These trends show how digital transformation is not just a strategic goal but a necessity for maintaining competitive advantage in today’s fast-evolving business environment.

Growing Demand for Remote Work Solutions Post-Pandemic

The shift toward hybrid and remote work environments has significantly boosted the demand for cloud-based contact center solutions in the Asia Pacific region. Unlike traditional contact centers that require physical infrastructure and centralized operations, cloud-based systems allow agents to operate from any location with internet access. Like, in South Korea, the Ministry of Employment and Labor recorded a 40% increase in remote working arrangements between 2021 and 2023, which directly influenced the growth of cloud-based customer engagement systems. Furthermore, vendors have responded to this trend by enhancing features such as mobile agent apps, secure login protocols, and real-time performance dashboards tailored for distributed teams. This shift is not only enabling workforce flexibility but also helping enterprises reduce overhead costs associated with physical call centers, reinforcing the long-term viability of cloud-based solutions.

MARKET RESTRAINTS

Data Privacy and Regulatory Compliance Concerns

The complexity surrounding data privacy and regulatory compliance is one of the primary challenges impeding the rapid expansion of the cloud-based contact center market in the Asia Pacific region. Many countries in the region have introduced stringent data protection laws that govern the storage, processing, and transfer of customer information across borders. For example, China’s Personal Information Protection Law (PIPL), implemented in 2021, imposes strict requirements on cross-border data flows, affecting multinational companies operating in the country. According to a report by PwC, nearly 60% of foreign enterprises in China had to reconfigure their cloud strategies to comply with PIPL guidelines. Similarly, in India, the proposed Digital Personal Data Protection Bill mandates localized data storage, posing a challenge for global cloud providers accustomed to centralized data centers. Even in more developed markets like Australia, the Notifiable Data Breaches scheme under the Privacy Act has heightened scrutiny on how customer data is handled. These evolving regulations, while essential for consumer protection, create operational hurdles for vendors and enterprises alike. Ensuring compliance often requires additional investments in data encryption, regional server infrastructure, and legal consultations, thereby increasing total cost of ownership and slowing down adoption rates in certain segments.

Cybersecurity Threats and Infrastructure Vulnerabilities

Cybersecurity remains a significant concern for enterprises considering cloud-based contact center adoption in the Asia Pacific region. As contact centers handle sensitive customer data, including personal identification, financial details, and behavioral patterns, they are prime targets for cyberattacks. According to a report by IBM Security, the average cost of a data breach in the Asia Pacific region reached USD 2.28 million in 2023, higher than the global average, indicating the financial risks associated with security incidents. Meanwhile, in India, CERT-In reported over 1.4 million cybersecurity incidents in the same year, prompting stricter enforcement of incident reporting and response protocols. These threats have made businesses cautious about migrating critical customer interaction systems to the cloud without robust security frameworks in place. Additionally, disparities in digital infrastructure across the Asia Pacific region further complicate the security landscape. While countries like Singapore and South Korea boast advanced cybersecurity ecosystems, others face challenges related to outdated IT systems and limited threat detection capabilities. These factors contribute to hesitancy among potential adopters, acting as a drag on market growth despite the evident advantages of cloud-based contact centers.

MARKET OPPORTUNITIES

Integration of AI and Automation Technologies

The integration of artificial intelligence (AI) and automation into cloud-based contact centers presents a transformative opportunity for the Asia Pacific market. Enterprises are increasingly deploying AI-powered virtual agents, sentiment analysis tools, and predictive routing to enhance customer engagement and streamline operations. Moreover, the convergence of AI with natural language processing (NLP) and machine learning (ML) is enabling deeper personalization and faster issue resolution. In Australia, insurance companies are using AI-driven speech analytics to assess customer emotions during calls and route them to the most suitable agent.

Expansion of Omnichannel Customer Engagement Strategies

The growing emphasis on omnichannel customer engagement is opening new avenues for growth in the Asia Pacific cloud-based contact center market. Customers today expect seamless interactions across multiple touchpoints including voice, email, SMS, social media, and messaging apps. This shift is not confined to large enterprises; small and medium-sized businesses (SMBs) are also embracing omnichannel capabilities to compete effectively. Moreover, vendors are responding to this trend by offering modular solutions that allow businesses to add channels incrementally without overhauling existing systems.

MARKET CHALLENGES

Fragmented Regulatory Landscape Across Asia Pacific Countries

The fragmented regulatory landscape across the region is a significant challenge facing the growth of the Asia Pacific cloud-based contact center market. Each country has its own set of data governance policies, cybersecurity mandates, and telecommunications regulations, creating compliance complexities for multinational vendors and enterprises. For example, while Singapore follows a relatively open and transparent regulatory framework conducive to cloud adoption, countries like Vietnam and Thailand impose strict data localization requirements, mandating that customer data be stored within national borders.

According to a report by Ernst & Young (EY), over 50% of cloud service providers operating in the Asia Pacific region cited regulatory fragmentation as a key obstacle to scaling their offerings. In particular, the lack of harmonized standards makes it difficult for vendors to offer uniform services across multiple jurisdictions without significant customization. In India, the evolving nature of the Digital Personal Data Protection Bill has created uncertainty regarding cross-border data transfers, influencing investment decisions of global cloud providers. As per a study by PwC, 40% of enterprises in India delayed their cloud contact center rollouts due to concerns over unclear regulatory guidelines.

Moreover, in Japan, the revised Act on the Protection of Specially Designated Secrets and stricter interpretations of the Act on the Protection of Personal Information have added layers of compliance burden for foreign vendors. Similarly, in Australia, the introduction of the Consumer Data Right (CDR) regime has necessitated enhanced consent management and data portability mechanisms. These variations in legal frameworks increase both time-to-market and operational costs, hindering the seamless expansion of cloud-based contact center solutions across the Asia Pacific region.

Limited Awareness and Technical Expertise Among SMEs

Small and medium-sized enterprises (SMEs) in the Asia Pacific region continue to lag due to limited awareness, and technical expertise is also a major challenge for the market. Many SMEs remain reliant on conventional telephony systems, lacking knowledge about the benefits of transitioning to cloud-based models.

Even when awareness exists, implementation barriers persist. SMEs often lack in-house IT resources required to deploy and manage cloud solutions effectively. In Indonesia, where SMEs account for over 99% of all businesses, as per a report by McKinsey, only 12% had the necessary digital skills to integrate cloud-based customer engagement tools. To bridge this gap, some governments and private sector players have initiated training programs and subsidized cloud adoption schemes. However, progress remains uneven, particularly in rural areas where internet connectivity and digital literacy are still developing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Solution, Service, Application, Deployment Mode, Organization Size, Vertical, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia Pacific |

| Market Leaders Profiled | 8x8 Inc. (US), Five9 (US), Cisco Systems (US), Genesys (US), Oracle (US), NewVoiceMedia (UK), Connect First (US), Aspect Software (US), and 3CLogic (US). |

SEGMENTAL ANALYSIS

By Solution Insights

The Reporting and Analytics segment holds the largest share of 23.5% of the Asia Pacific cloud-based contact center market in 2024. Increasing demand for real-time insights into customer behavior, agent performance, and operational efficiency across industries such as banking, retail, and telecommunications is primarily credited to the dominance of the Reporting and Analytics segment. The rising integration of artificial intelligence (AI) and machine learning (ML) into reporting modules is another key driver behind this growth. Additionally, the proliferation of omnichannel communication platforms has increased the volume of data generated from voice, chat, email, and social media interactions. Moreover, regulatory mandates requiring detailed audit trails and compliance reporting are pushing organizations to invest heavily in robust analytics capabilities. In Japan, where labor shortages are acute, companies are leveraging predictive analytics to forecast call volumes and allocate resources more efficiently. These factors strengthen the lead position of the Reporting and Analytics segment in the Asia Pacific cloud-based contact center market.

The Interactive Voice Response (IVR) solution segment is projected to grow at the fastest rate, with a CAGR of 19.7% between 2025 and 2033. The increasing need for automated, self-service customer support solutions that reduce reliance on human agents while maintaining high service levels is driving the rapid expansion of Interactive Voice Response (IVR) solution segment. The widespread adoption of AI-driven IVR systems that offer natural language processing (NLP) and conversational interfaces is also a major factor contributing to this growth. Similarly, in India, telecom operators have reported a 40% reduction in agent workload after deploying intelligent IVR systems integrated with cloud platforms, according to EY. Additionally, the shift toward remote and hybrid work models post-pandemic has further amplified the need for scalable, cloud-hosted IVR solutions. In South Korea, government agencies and large corporations have adopted multilingual IVR systems to serve diverse populations across regions. These trends underline why the IVR segment continues to outpace other solutions in terms of growth within the Asia Pacific cloud-based contact center market.

By Service Insights

The Managed Services segment led the Asia Pacific cloud-based contact center market by capturing 56.3% of total service revenue in 2024. The growing preference among enterprises, especially mid-sized businesses, for outsourcing day-to-day operations to third-party providers who can ensure system uptime, scalability, and technical support without the need for in-house expertise is propelling the position of Managed Services segment. The increasing complexity of cloud contact center deployments, particularly when integrating AI, automation, and omnichannel capabilities, is another key driver of this trend ofthe Managed Services segment. Rise in demand for pay-per-use and subscription-based pricing models, which allow businesses to align expenses with actual usage, is a further contributing factor. These patterns strengthen the sustained leadership of the Managed Services segment in the Asia Pacific cloud-based contact center market.

The Professional Services segment is expected to register the highest growth in the Asia Pacific cloud-based contact center market, with a CAGR of 18.4% during the forecast period of 2025–2033. The increasing need for customized deployment strategies, system integration, and consulting services tailored to evolving business requirements is largely fuelling the surge of the Professional Services segment. The rising demand for digital transformation initiatives across industries is among the key drivers behind this growth Professional Services segment. Enterprises are seeking expert guidance to migrate legacy systems to cloud-based architectures while ensuring seamless integration with CRM, ERP, and AI-driven analytics tools. Similarly, in South Korea, the government’s push for smart city projects has led to increased investments in professional services for integrating cloud contact centers with public service portals, as per a report by Samsung SDS. The growing complexity of compliance and cybersecurity frameworks in the region is another critical factor. Businesses are increasingly relying on professional service providers to conduct risk assessments, implement encryption protocols, and ensure adherence to local data protection laws. These developments show the expanding role of professional services in shaping the future of the Asia Pacific cloud-based contact center landscape.

By Application Insights

The Workforce Optimization (WFO) application segment commanded the prominent share of the Asia Pacific cloud-based contact center market by accounting for 27.4% of total application-based revenue in 2024. Growing emphasis on enhancing agent productivity, improving quality assurance, and streamlining training processes across contact centers in the region is one of the reasons behind the dominance of Workforce Optimization (WFO) application segment. The increasing integration of real-time monitoring and performance analytics tools that help supervisors provide actionable feedback to frontline agents is also a primary driver of WFO adoption. Similarly, in India, leading telecom operators have deployed WFO modules to evaluate agent-customer interactions and identify areas for improvement. Additionally, the shift toward remote and hybrid work environments has heightened the need for centralized workforce management tools that enable seamless scheduling, training, and performance tracking. These trends collectively highlight why Workforce Optimization remains the most dominant application segment in the Asia Pacific cloud-based contact center market.

The Real-Time Decision-Making application segment is anticipated to grow at the fastest pace and is recording a CAGR of 21.3% between 2025 and 2033. The increasing reliance on instant data analysis to personalize customer interactions and improve response accuracy in real-time is driving the rapid expansion of Real-Time Decision-Making application segment. Integration of AI and machine learning algorithms that enable dynamic routing of customer queries based on behavioral patterns and historical data is also a key factor fueling this growth of Real-Time Decision-Making application segment. The growing use of real-time dashboards that allow supervisors to monitor agent performance and make immediate adjustments to workflows is another driving force. These advancements are accelerating the adoption of real-time decision-making capabilities across the Asia Pacific cloud-based contact center ecosystem.

By Vertical Insights

The Banking, Financial Services, and Insurance (BFSI) segment commanded the market by contributing 31.2% of total revenue in the Asia Pacific cloud-based contact center market in 2024. The sector’s high dependency on customer engagement, regulatory compliance, and the need for secure, scalable communication infrastructures is propelling the dominance of the BFSI segment. Increasing digitization of financial transactions and customer service channels is one key factor supporting this dominance of BFSI segment. In India, where digital payments have surged following initiatives like UPI, banks and fintech firms have migrated to cloud-based contact centers to handle rising inquiry volumes. Moreover, the need for enhanced security and compliance features, especially in light of stringent data protection regulations, is another contributing element.

The Healthcare and Life Sciences segment is projected to expand at the fastest rate, with a CAGR of 22.1% during the coming years. The increasing adoption of telehealth services, patient engagement platforms, and cloud-based appointment scheduling systems across the Asia Pacific region is driving the growth of the Healthcare and Life Sciences segment. The accelerated digital transformation in healthcare post-pandemic is also a key driver behind this surge of the Healthcare and Life Sciences segment. The growing integration of AI-powered virtual assistants and chatbots to handle routine inquiries and reduce the burden on frontline staff is another significant factor. These innovations are reshaping patient engagement and positioning the healthcare sector as the fastest-growing vertical in the Asia Pacific cloud-based contact center market.

COUNTRY-LEVEL ANALYSIS

India Cloud-Based Contact Center Market Insights

India remained among the major contributors to the Asia Pacific cloud-based contact center market. The country's strong presence in the global BPO industry, coupled with rapid digital transformation across BFSI, telecom, and retail sectors, has driven widespread adoption of cloud-based customer engagement solutions. This digital expansion has enabled businesses to scale omnichannel contact center operations seamlessly. Additionally, the government’s Digital India initiative has spurred investments in cloud infrastructure, with state-backed programs promoting cloud adoption among SMEs. Moreover, India’s cost-effective labor pool combined with rising English proficiency makes it a preferred destination for global enterprises setting up offshore contact centers. These factors contribute to India’s strong market position in the Asia Pacific cloud-based contact center landscape.

China Cloud-Based Contact Center Market Insights

China occupies a prominent position in the Asia Pacific cloud-based contact center market. As one of the world’s largest digital economies, China’s extensive e-commerce ecosystem and high adoption of mobile-first customer engagement strategies have significantly boosted demand for cloud-based contact center solutions. A major driver of this growth is the dominance of tech giants such as Alibaba, Tencent, and Baidu, which have developed sophisticated AI-powered customer service platforms. Additionally, the Chinese government’s push for digital infrastructure modernization, including 5G rollout and cloud computing incentives, has facilitated the expansion of cloud-based contact center ecosystems. These developments solidify China’s leadership role in the Asia Pacific cloud-based contact center market.

Japan Cloud-Based Contact Center Market Insights

Japan is among the key contributors to the Asia Pacific cloud-based contact center market. The country’s aging population, labor shortages, and high digital maturity have created a conducive environment for the adoption of cloud-based customer engagement solutions across sectors such as finance, healthcare, and manufacturing. One key growth factor is the increasing integration of robotic process automation (RPA) and AI into contact center operations. In the banking sector, major institutions such as Mitsubishi UFJ Financial Group and Sumitomo Mitsui Banking Corporation have migrated to cloud-based contact centers to improve service efficiency and support remote operations. Another contributing element is the government’s focus on smart city initiatives and digital transformation policies aimed at modernizing public and private sector services. These developments underscore Japan’s strategic importance in the Asia Pacific cloud-based contact center landscape.

Australia Cloud-Based Contact Center Market Insights

Australia holds a strong position in the Asia Pacific cloud-based contact center market. The country’s high internet penetration, mature digital infrastructure, and proactive regulatory framework have fostered widespread adoption of cloud-based customer engagement solutions across both public and private sectors. A major growth driver is the increasing implementation of hybrid and remote work models post-pandemic. In the government sector, federal and state agencies have adopted cloud contact centers to streamline citizen service delivery. Another key factor is the country’s stringent data protection and privacy regulations, which have prompted enterprises to invest in secure, compliant cloud contact center solutions. These dynamics reinforce Australia’s competitive standing in the Asia Pacific cloud-based contact center market.

South Korea Cloud-Based Contact Center Market Insights

South Korea is another major player in the Asia Pacific cloud-based contact center market. The country’s advanced digital infrastructure, high smartphone penetration, and widespread use of mobile-first customer engagement platforms have propelled rapid adoption of cloud-based contact center solutions. One key growth factor is the increasing convergence of AI, big data analytics, and cloud technologies in customer service operations. Another contributing element is the government’s Smart Nation and digital innovation initiatives, which have encouraged cloud adoption across public and private sectors. These developments position South Korea as a pivotal player in the Asia Pacific cloud-based contact center market.

KEY MARKET PARTICIPANTS

The key players in the Asia-Pacific cloud-based contact center market include 8x8 Inc. (US), Five9 (US), Cisco Systems (US), Genesys (US), Oracle (US), NewVoiceMedia (UK), Connect First (US), Aspect Software (US), and 3CLogic (US)

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the Asia Pacific cloud-based contact center market is Genesys. The company has a strong global footprint and offers a comprehensive suite of cloud-based customer engagement solutions tailored to regional needs. Genesys has been instrumental in driving innovation through AI integration, omnichannel capabilities, and advanced analytics. Its focus on delivering seamless customer experiences across diverse industries has made it a preferred choice for enterprises in the region.

Another major player is Five9, known for its cloud contact center platform that supports scalable and flexible deployments. Five9 has been actively expanding its presence in the Asia Pacific by forming strategic partnerships and enhancing its service offerings to meet local compliance and operational requirements. The company emphasizes automation, workforce optimization, and real-time analytics to help businesses improve efficiency and customer satisfaction.

Avaya is also a key participant in the market, offering hybrid and cloud-based contact center solutions that cater to large enterprises and government organizations. Avaya’s strength lies in its ability to integrate legacy systems with modern cloud infrastructure, ensuring smooth digital transformation. The company continues to invest in AI-driven insights and collaboration tools, reinforcing its competitive edge in the Asia Pacific landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Asia Pacific cloud-based contact center market are leveraging strategic partnerships and collaborations to enhance their regional presence. By aligning with local telecom providers, system integrators, and technology partners, vendors can better address regulatory nuances and offer customized solutions. These alliances help expand distribution networks and accelerate product adoption across sectors.

Another prevalent strategy is product innovation and feature enhancement, where companies continuously refine their platforms with AI, automation, and omnichannel capabilities. This allows them to meet evolving customer expectations and differentiate themselves in a competitive environment. Vendors are focusing on intuitive interfaces, real-time analytics, and improved agent productivity tools to attract new clients and retain existing ones.

Lastly, market expansion through localized deployment models is gaining traction. Companies are adapting their cloud infrastructures to comply with data sovereignty laws while maintaining high performance. This includes establishing regional data centers and offering hybrid deployment options to ensure flexibility and security, which is critical for enterprise customers in highly regulated industries.

COMPETITION OVERVIEW

The competition in the Asia Pacific cloud-based contact center market is intensifying as global and regional vendors strive to capture a larger share of the growing demand. With digital transformation accelerating across industries, enterprises are increasingly prioritizing customer experience, prompting contact center solution providers to innovate rapidly. The market features a mix of established multinational corporations and emerging local players, each vying to deliver more agile, secure, and intelligent platforms. While global vendors bring advanced technologies and robust ecosystems, regional players often have an edge in understanding local regulations, language nuances, and industry-specific workflows.

Differentiation is primarily achieved through feature-rich platforms that incorporate artificial intelligence, automation, and omnichannel integration. Vendors are also emphasizing ease of deployment, scalability, and compliance with evolving data protection norms to appeal to both large enterprises and SMEs. Strategic acquisitions and partnerships are becoming common as companies seek to strengthen their service portfolios and geographic reach. Additionally, as customer expectations evolve, vendors are investing heavily in user experience design and support services to build long-term client relationships. This dynamic competitive environment fosters continuous innovation, making the Asia Pacific market one of the most vibrant and fast-moving globally.

RECENT MARKET DEVELOPMENTS

- In February 2024, Genesys expanded its cloud infrastructure in Singapore by launching a new regional data center. This move was aimed at improving service reliability and meeting stringent data residency requirements for enterprise clients across Southeast Asia.

- In May 2024, Five9 announced a strategic partnership with a leading telecommunications provider in Japan to co-develop integrated cloud contact center solutions tailored for the Japanese market, addressing localization and compliance challenges.

- In July 2024, Avaya introduced a new AI-powered customer engagement tool designed specifically for the BFSI sector in India, enhancing agent efficiency and personalization for banks and insurance firms.

- In October 2024, RingCentral, a key player in unified communications, entered the Australian market with a dedicated cloud contact center offering, targeting mid-sized enterprises looking for scalable and secure communication solutions.

- In December 2024, NICE inContact launched an enhanced workforce optimization module integrated with its cloud contact center platform, focusing on improving agent training and quality assurance for enterprises in South Korea.

MARKET SEGMENTATION

This research report on the Asia-Pacific cloud-based contact center market has been segmented and sub-segmented into the following categories.

By Solution

- ACD

- APO

- Dialers

- IVR

- CTI

- Reporting and Analytics

- Security

By Service

- Professional

- Managed

By Application

- Call Routing and Queuing

- Data Integration and Recording

- Chat Quality and Monitoring

- Real-Time Decision-Making

- Workforce Optimization (WFO)

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Organization Size

- Small and Medium-sized Enterprises

- Large Enterprises

By Vertical

- Banking, Financial Services, and Insurance

- Consumer goods and retail

- Government and public sector

- Healthcare and life sciences

- Manufacturing

- Media and entertainment

- Telecommunication and Information Technology Enabled Services

- Others

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia Pacific

Frequently Asked Questions

Which countries in the Asia-Pacific region are at the forefront of adopting cloud-based contact center solutions?

Countries like India, Australia, and Japan are at the forefront of adopting cloud-based contact center solutions in the Asia-Pacific region, driven by the need for scalable and flexible customer service solutions.

What factors are contributing to the growth of cloud-based contact centers in China?

In China, the growth of cloud-based contact centers is fueled by the increasing demand for omnichannel customer experiences, the rapid expansion of e-commerce, and a focus on enhancing customer engagement.

What is the market share of cloud-based contact centers in the rapidly growing tech hubs of Southeast Asia?

Cloud-based contact centers hold a substantial market share in the tech hubs of Southeast Asia, such as Kuala Lumpur and Bangkok, as companies prioritize digital transformation initiatives to stay competitive.

Who are the key players in the Asia-Pacific cloud-based contact center market?

8x8 Inc. (US), Five9 (US), Cisco Systems (US), Genesys (US), Oracle (US), NewVoiceMedia (UK), Connect First (US), Aspect Software (US), and 3CLogic (US) are playing the leading role in the regional market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com