Global Cloud-Based Contact Center Market Size, Share, Trends & Growth Forecast Report By Solution (ACD, APO, Dialers, IVR, CTI, Reporting and Analytics, and Security), Service (Professional and Managed), Application, Deployment Model, Organization Size, Vertical & Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Industry Analysis 2025 to 2033

Global Cloud-Based Contact Center Market Summary

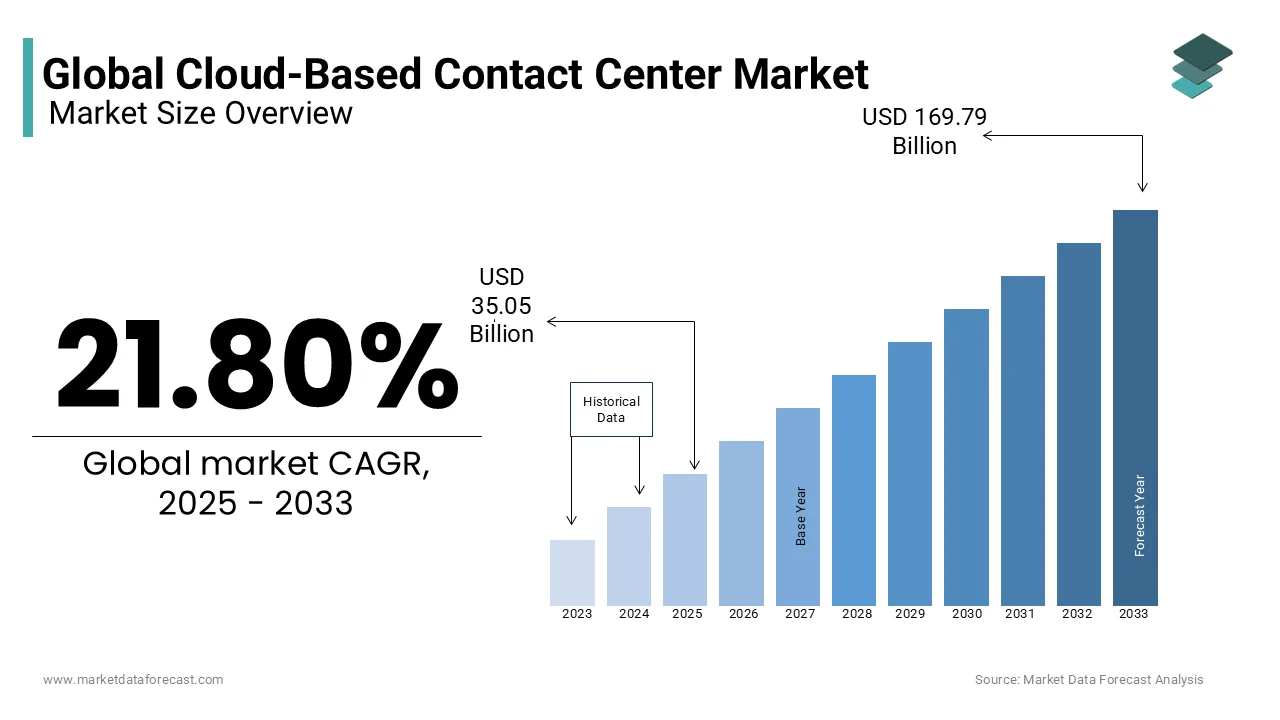

The global cloud-based contact center market was valued at USD 28.78 billion in 2024, is projected to reach USD 35.05 billion in 2025, and is expected to expand to USD 169.79 billion by 2033, growing at a CAGR of 21.8% from 2025 to 2033. The growth of the global cloud-based contact center market is driven by rising demand for scalable and flexible customer service solutions, increasing adoption of AI-powered analytics, and the shift toward remote and hybrid work models. The need for cost-efficient, omnichannel communication platforms and advancements in workforce optimization technologies further accelerate market expansion.

Key Market Trends

- Rising adoption of AI, chatbots, and automation to enhance customer experience.

- Increasing demand for real-time reporting and analytics to improve decision-making.

- Expansion of public cloud deployment due to cost-effectiveness and scalability.

- Growing use of workforce optimization (WFO) tools for agent performance management.

- Strong adoption of professional services to support implementation and integration.

Segmental Insights

- Based on solution, the reporting and analytics segment dominated the global cloud-based contact center market in 2024, reflecting the growing importance of data-driven insights.

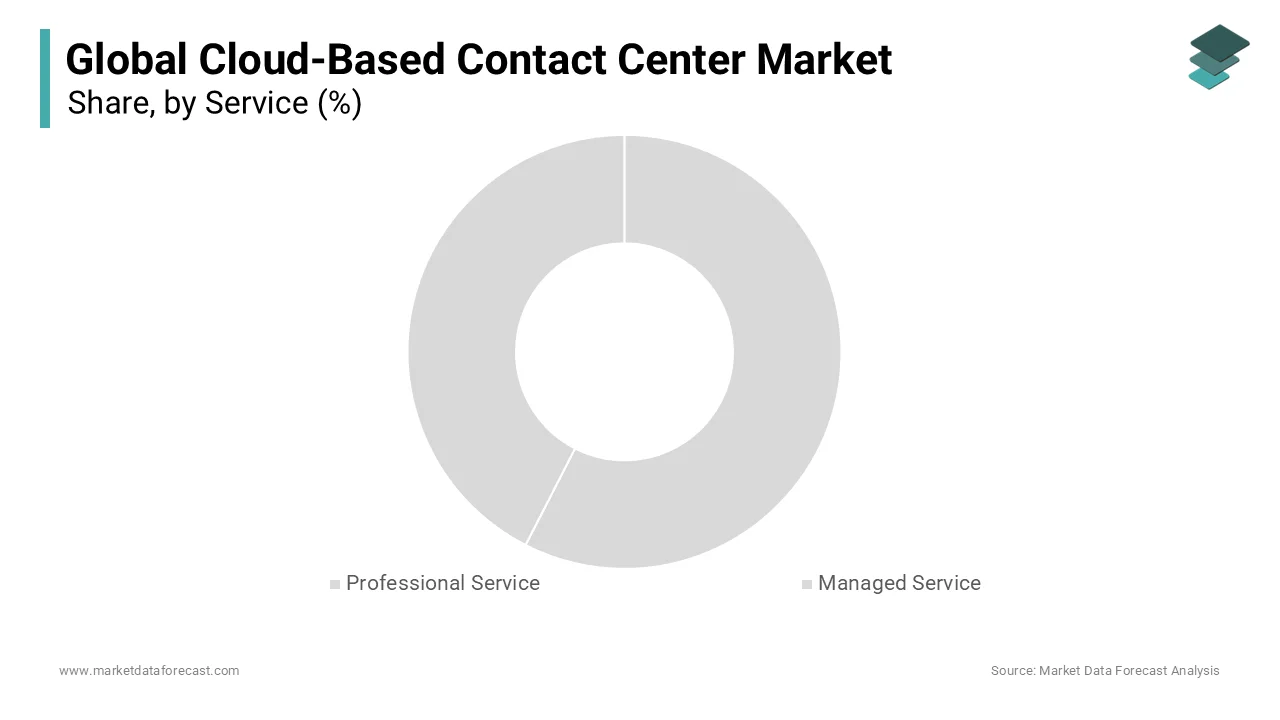

- Based on services, the professional services segment held the largest share at 58.3% in 2024, supported by demand for consulting, integration, and training services.

- Based on application, the workforce optimization (WFO) segment accounted for 31.2% share in 2024, highlighting its role in improving agent productivity and customer satisfaction.

- Based on deployment mode, the public cloud segment dominated in 2024, driven by flexibility, lower upfront costs, and faster implementation.

Regional Insights

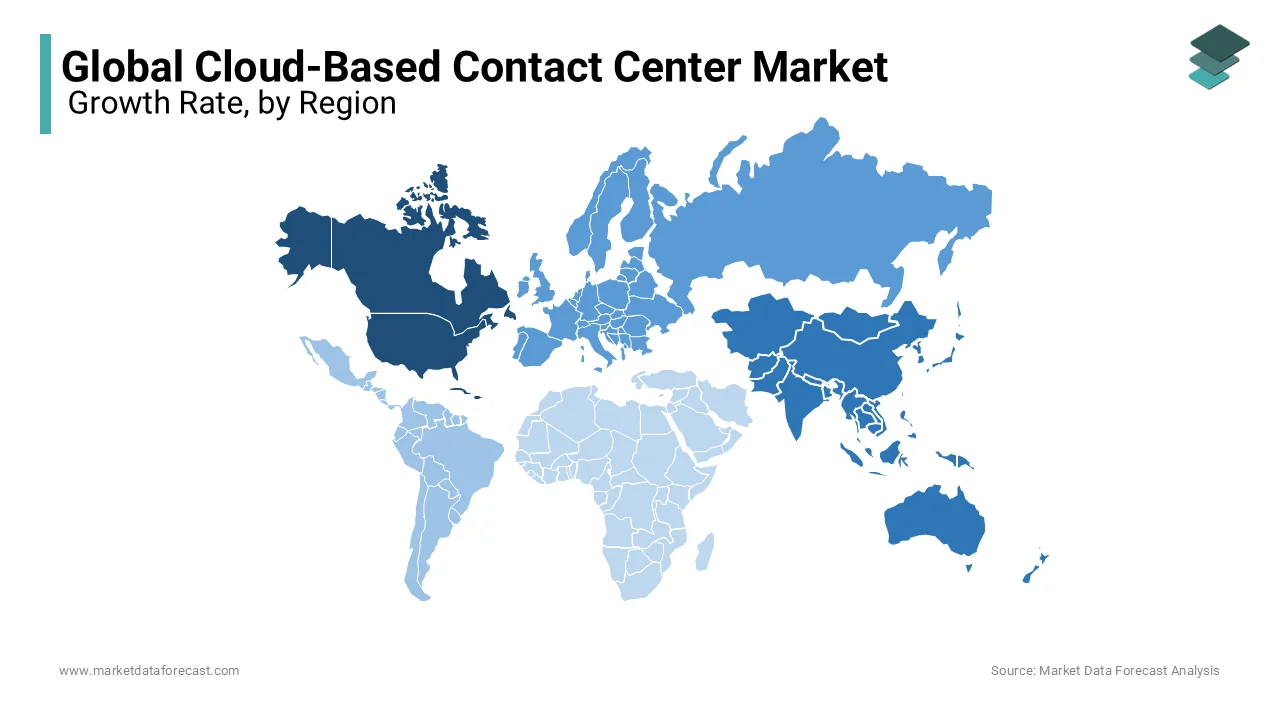

- North America was the leading region, capturing 38.3% of the global cloud-based contact center market in 2024, supported by strong enterprise adoption, advanced IT infrastructure, and the presence of leading solution providers.

- Europe is experiencing steady growth, driven by customer engagement, digitalization and strict compliance requirements.

- Asia-Pacific is projected to grow at the fastest pace, fueled by increasing cloud adoption, expanding BPO sector, and rapid digital transformation in countries like India and China.

- Latin America and the Middle East & Africa are emerging markets, supported by the adoption of cloud technologies to modernize customer service operations.

Competitive Landscape

Key players in the global cloud-based contact center market include Cisco Systems, Genesys, Five9, New Voice Media, Oracle, 3clogic, Aspect Software, Nice Ltd., Connect First, Avaya, Vonage, and Talkdesk. These companies are focusing on AI-driven platforms, omnichannel integrations, and strategic partnerships to strengthen their global presence.

Global Cloud-Based Contact Center Market Size

The global cloud-based contact center market size was valued at USD 28.78 billion in 2024. The global market is expected to grow at a CAGR of 21.8% from 2025 to 2033 and to be worth USD 169.79 billion by 2033 from USD 35.05 billion in 2025.

The Cloud-Based Contact Center architecture supports real-time analytics, artificial intelligence (AI)-driven routing, omnichannel engagement, and seamless integration with customer relationship management (CRM) systems. As enterprises increasingly prioritize digital transformation, the shift toward cloud-based models has accelerated, particularly in sectors such as telecommunications, banking, healthcare, and e-commerce. The proliferation of remote workforces has further amplified demand, with companies requiring resilient, decentralized communication frameworks. Additionally, advancements in AI and machine learning have enabled predictive customer behavior modeling and automated resolution pathways, enhancing operational efficiency.

MARKET DRIVERS

Accelerated Digital Transformation in Enterprise Customer Service

The widespread pursuit of digital transformation across enterprises has emerged as a pivotal factor in propelling the growth of the Cloud-Based Contact Center Market. Organizations are increasingly dismantling legacy infrastructure in favor of agile, software-defined communication platforms that align with broader IT modernization goals. The financial services sector, for instance, has witnessed a 42% increase in cloud contact center deployments between 2021 and 2023, with the need for real-time fraud detection, personalized service delivery, and compliance automation. The scalability of these systems allows enterprises to respond dynamically to fluctuating demand from retailers during peak seasons; for example, they can scale agent capacity by 200% within hours. As per IDC, 78% of global enterprises now consider cloud contact centers a core component of their customer experience (CX) strategy.

Expansion of Remote and Hybrid Work Models

The structural shift toward remote and hybrid workforce models is additionally to promote the growth of the Cloud-Based Contact Center Market. Before 2020, fewer than 15% of customer service agents worked remotely, as noted by Deloitte’s 2019 global service operations survey. By 2023, that figure surged to over 60%, with cloud contact centers enabling secure, decentralized access to communication tools and customer data. Cloud platforms facilitate this shift by providing encrypted voice-over-IP (VoIP), secure single sign-on (SSO), and real-time performance monitoring regardless of agent location. As per a PwC analysis, companies leveraging cloud contact centers reported a 28% improvement in first-call resolution rates among remote agents compared to those using legacy systems. Additionally, workforce flexibility has expanded talent pools beyond urban centers, allowing enterprises to recruit bilingual agents from tier-2 and tier-3 cities, enhancing multilingual support capabilities. The U.S. Bureau of Labor Statistics recorded a 33% increase in remote customer service employment between 2020 and 2022, which signals a permanent reconfiguration of service delivery geography.

MARKET RESTRAINTS

Data Security and Privacy Compliance Complexities

The stringent data protection regulations and persistent security are majorly restricting the growth of the Cloud-Based Contact Center Market. The European Union’s General Data Protection Regulation (GDPR) and similar frameworks in countries like Japan and Australia mandate that customer data be stored and processed within specific jurisdictions, complicating the deployment of globally hosted cloud solutions. As per a 2023 Cisco Cybersecurity Readiness Index, 56% of enterprises in the Asia-Pacific region delayed or scaled back cloud contact center implementations due to compliance risks. Financial institutions, for example, face heightened scrutiny under standards such as the Payment Card Industry Data Security Standard (PCI DSS), requiring end-to-end encryption and regular audits challenges which are more complex in multi-tenant cloud environments. A report by the Ponemon Institute revealed that the average cost of a data breach in customer service systems reached $4.45 million in 2023, with cloud misconfigurations accounting for 18% of incidents. In India, the Digital Personal Data Protection Act of 2023 imposes strict localization requirements, forcing multinational vendors to establish regional data centers, thereby increasing deployment costs and timelines. Additionally, third-party vendor risk assessments have become more rigorous, with 72% of enterprises conducting quarterly security audits of their cloud contact center providers, as noted by KPMG’s 2023 Global Risk Survey.

Integration Challenges with Legacy Enterprise Systems

The adoption of cloud-based contact centers lies in the technical and operational complexities associated with integrating these platforms with existing enterprise systems in organizations is limiting the growth of the Cloud-Based Contact Center Market. Many enterprises operate with legacy CRM, ERP, and workforce management systems that were not designed for cloud interoperability, leading to data silos and process inefficiencies. In the banking sector, for instance, 68% of institutions still rely on core banking systems developed before 2000, which lack standardized APIs for seamless data exchange with modern cloud platforms. Furthermore, inconsistent data formats and real-time synchronization issues often degrade customer experience; Gartner found that 40% of failed omnichannel implementations stemmed from poor backend integration.

MARKET OPPORTUNITIES

Artificial Intelligence and Conversational Automation Integration

The integration of artificial intelligence (AI) and cloud-based contact centers is exceptionally to enhance the growth of the Cloud-Based Contact Center Market. AI-powered virtual agents, natural language processing (NLP), and sentiment analysis tools are now being embedded into cloud platforms to automate routine inquiries and enable intelligent agent assistance. As per a 2023 MIT Technology Review survey, enterprises deploying AI in cloud contact centers observed a 45% reduction in average handling time and a 32% increase in customer satisfaction scores. Google Cloud’s Contact Center AI has been adopted by over 1,200 enterprises globally, including Singapore Airlines, which reported a 40% improvement in first-contact resolution after integrating AI-powered knowledge recommendations. Additionally, AI enables real-time coaching for agents by analyzing conversation patterns and suggesting optimal responses, a feature now used by 65% of large contact centers in Australia, as noted by Accenture.

Expansion into Emerging Markets with High Mobile Penetration

The rapid proliferation of mobile internet and smartphone adoption in emerging countries is expected to boost the growth of the Cloud-Based Contact Center Market. Gojek, Indonesia’s leading super-app, processes over 2 million customer inquiries monthly through its cloud-native support system, leveraging real-time analytics to manage service quality across 200+ cities. This has driven a surge in digital-first customer service models, with cloud contact centers enabling rapid scalability for startups and SMEs. The Philippines, a major BPO hub, has seen a 35% increase in cloud-based deployments among mid-tier service providers between 2021 and 2023, as documented by the International Data Corporation. These markets offer low infrastructure lock-in, allowing enterprises to bypass legacy systems entirely and adopt modern cloud platforms from inception.

MARKET CHALLENGES

Ensuring Consistent Service Quality Across Distributed Networks

Maintaining uniform service quality in cloud-based contact centers is creating new challenges for the growth of the Cloud-Based Contact Center Market. In India, 48% of remote customer service agents reported intermittent connectivity issues affecting service delivery, as per a 2023 Telecom Regulatory Authority of India (TRAI) study. These technical limitations impact key performance indicators such as average speed of answer and customer satisfaction.

Managing Vendor Lock-In and Interoperability Limitations

The risk of vendor lock-in, where dependence on a single provider’s proprietary architecture limits flexibility, increases long-term costs, and hinders integration with other enterprise systems, also inhibiting the growth of the Cloud-Based Contact Center Market. According to a 2023 analysis by Omdia, 58% of enterprises using proprietary cloud contact center platforms faced significant obstacles when attempting to migrate data or integrate third-party analytics tools. Additionally, proprietary AI models and machine learning algorithms are often not transferable, forcing companies to retrain systems from scratch upon vendor change.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 21.8% |

| Segments Covered | By Solution, Service, Application, Deployment Mode, Organization Size, Vertical, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Cisco Systems, Genesys, Five9, New Voice Media, Oracle, 3clogic, Aspect Software, Nice Ltd, Connect First, Avaya, Vonage, Talkdesk, and Others. |

SEGMENTAL ANALYSIS

By Solution Insights

The reporting and analytics were accounted in holding a dominant share of the cloud-based contact center market in 202,4 with the increasing reliance on data-driven decision-making in customer service operations, where enterprises demand granular insights into agent performance, customer sentiment, and operational efficiency. The integration of real-time analytics into cloud platforms enables supervisors to monitor key metrics such as average handle time, first call resolution, and customer satisfaction (CSAT) with unprecedented precision. According to a 2023 study by MIT Sloan Management Review, organizations leveraging advanced analytics in customer service report a 38% improvement in service quality and a 29% reduction in operational costs. Additionally, the European Union’s emphasis on performance transparency under the Digital Services Act has compelled contact centers to adopt standardized reporting frameworks, further accelerating adoption.

The Security segment is projected to grow with a CAGR of 22.4% from 2025 to 2033, with the escalating cyber threats and stringent data protection mandates. Japan’s Personal Information Protection Commission (PIPC) fined a major telecom operator $3.2 million in 2022 for inadequate data safeguards in its outsourced contact center, signaling stricter enforcement. Furthermore, the Payment Card Industry Data Security Standard (PCI DSS) now mandates that all cloud contact centers handling cardholder data adopt point-to-point encryption (P2PE), a requirement that has spurred investments in secure voice and screen recording solutions.

By Service Insights

The professional services segment accounted in holding 58.3% of the cloud-based contact center services market share in 2024 due to the complexity involved in migrating from legacy systems to cloud-native platforms, which necessitates expert consultation, system customization, and change management. Enterprises often lack in-house expertise to configure advanced routing logic, integrate CRM systems, or ensure compliance with regional data laws, making external professional support indispensable. Similarly, in India, the National Association of Software and Services Companies (NASSCOM) found that 68% of BPO firms required professional services to retrain 150,000 agents on new cloud interfaces during digital transformation initiatives. The implementation phase is particularly resource-intensive; Cisco’s 2023 Global IT Survey indicated that enterprises spend an average of 42% of their total cloud contact center budget on professional services, including workflow design and API integration. Moreover, financial institutions in Singapore, such as DBS Bank, have mandated third-party audits and architectural reviews before go-live, further amplifying demand.

The managed services segment is likely to grow with an expected CAGR of 19.8% from 2025 to 2033. Enterprises are increasingly shifting from capital-intensive ownership models to operational expenditure (OpEx)-based managed service agreements, where providers assume responsibility for platform maintenance, updates, security monitoring, and performance optimization. This transition is particularly pronounced in small and medium enterprises (SMEs), which lack the scale to justify full-time IT teams. The U.S. Bureau of Labor Statistics notes that the number of full-time IT support roles in customer service departments declined by 24% between 2020 and 2023, replaced by outsourced managed service contracts.

By Application Insights

The Workforce Optimization (WFO) segment was the largest by capturing 31.2% of the cloud-based contact center market share in 2024. WFO encompasses forecasting, scheduling, performance management, and quality monitoring, all essential for maintaining service level agreements (SLAs) in high-volume environments. The integration of real-time adherence tracking has also become a regulatory necessity in South Africa; the Independent Communications Authority mandates that telecom providers maintain a minimum 85% agent availability rate during peak hours, prompting widespread adoption of WFO analytics. Furthermore, the rise of hybrid work models has increased the complexity of workforce management, with agents dispersed across time zones and home offices. Cloud-based WFO platforms address this by offering centralized dashboards that monitor attendance, performance, and training compliance.

The Real-time decision-making segment is likely to witness a CAGR of 23.6% in the coming years, with the demand for dynamic customer engagement and AI-powered intervention. Similarly, in the UAE, Emirates NBD employs real-time fraud detection algorithms that analyze transaction patterns during customer calls, blocking suspicious activities within milliseconds. According to a 2023 McKinsey study, banks using real-time decision-making tools experienced a 37% reduction in financial fraud losses. Furthermore, real-time analytics are now integrated with agent assist tools, providing live recommendations during calls. A Salesforce survey found that agents using real-time guidance resolved 41% more inquiries without escalation.

By Deployment Mode Insights

The public cloud deployment segment held a dominant share of the cloud-based contact center market in 2024 with its cost efficiency, rapid scalability, and minimal infrastructure requirements, making it the preferred choice for enterprises seeking agile, pay-as-you-go models. Public cloud platforms eliminate the need for on-premise hardware, software licensing, and dedicated IT staff, reducing total cost of ownership by up to 45%, according to a 2023 Deloitte analysis of 300 global deployments. In India, 78% of fintech startups utilize public cloud contact centers to launch customer support operations within days, leveraging providers like AWS and Twilio. Moreover, public cloud vendors continuously update their security and compliance frameworks. Microsoft Teams Calling, for instance, now supports GDPR, HIPAA, and ISO 27001 certifications across 60 regions by enabling global enterprises to maintain compliance without additional investment. A 2023 report by the Cloud Security Alliance found that 83% of enterprises perceive public cloud security as equal to or better than on-premise systems due to automated patching and threat intelligence sharing.

The hybrid segment is deemed to grow with expected to grow with a CAGR of 21.3% from 2025 to 2033. Enterprises in highly regulated sectors such as banking, healthcare, and government are adopting hybrid models to host sensitive customer data on private clouds or on-premise servers while leveraging public cloud infrastructure for scalable customer engagement and AI processing. The hybrid model also supports legacy integration; a 2023 Everest Group study found that 52% of enterprises with hybrid deployments successfully connected cloud platforms to pre-2010 core banking systems without data migration. In Australia, the Commonwealth Bank reduced its cloud migration risk by 40% by adopting a phased hybrid approach, gradually shifting non-sensitive workloads to public cloud. Additionally, hybrid architectures enhance disaster recovery; according to a 2023 Uptime Institute survey, enterprises with hybrid setups experienced 55% faster service restoration during outages.

REGIONAL ANALYSIS

North America Cloud-Based Contact Center Market Insights

North America was the top performer of the global cloud-based contact center market with 38.3% of share in 2024, with the advanced digital infrastructure, high enterprise adoption of AI, and a mature regulatory framework for data protection. According to the U.S. Census Bureau, 87% of American businesses with over 500 employees have migrated to cloud-based customer service platforms with the need for remote workforce support and omnichannel integration. The Federal Communications Commission reports that VoIP adoption in U.S. contact centers reached 92% in 2023, enabling seamless cloud connectivity. Furthermore, the Securities and Exchange Commission’s emphasis on audit trails and call recording has accelerated investment in cloud-based compliance tools. A 2023 Brookings Institution study found that AI-enhanced cloud contact centers in the U.S. reduced average handling time by 31%, enhancing operational efficiency.

Europe Cloud-Based Contact Center Market Insights

Europe is a balanced blend of regulatory rigor and digital transformation across both Western and Eastern economies. The European Union’s Digital Decade initiative aims to ensure 90% of enterprises use cloud computing by 2030, a target accelerates contact center modernization. The UK, despite post-Brexit uncertainties, remains a hub for financial services contact centers, with 68% of banks using cloud platforms for fraud monitoring and customer onboarding, as per TechUK. France has seen a 40% increase in cloud adoption since 2021, fueled by government subsidies for digital SMEs. The General Data Protection Regulation (GDPR) has shaped deployment strategies, with 82% of EU enterprises opting for private or hybrid cloud models to ensure data sovereignty, as noted by the European Data Protection Board.

Asia-Pacific Cloud-Based Contact Center Market Insights

Asia-Pacific is emerging with prominent growth with the rapid digitalization, mobile-first populations, and booming e-commerce. The country’s Unified Payments Interface (UPI) processed 10.2 billion transactions in December 2023, necessitating scalable cloud support systems for fintech firms like Paytm and PhonePe. Japan’s aging workforce has spurred investment in AI agents; NTT’s cloud contact center handles 60% of routine inquiries without human intervention, as reported by the Ministry of Internal Affairs and Communications.

Latin America Cloud-Based Contact Center Market Insights

Latin America is driving adoption through digital banking and e-commerce expansion. Brazil’s Pix instant payment system, launched in 2020, now processes over 140 million transactions daily, compelling banks like Itaú and Bradesco to deploy cloud contact centers for real-time customer support. According to Brazil’s Central Bank, digital banking users surged to 120 million in 2023, a 55% increase from 2020, necessitating scalable cloud infrastructure. Mexico, with a 72% internet penetration rate (INEGI, 2023), has seen a 48% rise in cloud contact center deployments among retail and telecom firms. MercadoLibre, the region’s largest e-commerce platform, uses AWS-powered cloud contact centers to manage 8 million monthly inquiries across 18 countries.

Middle East and Africa Cloud-Based Contact Center Market Insights

The Middle East and Africa cloud-based contact center market is growing with the smart city initiatives and financial inclusion. The UAE leads the region, with Dubai’s Smart Government initiative mandating 100% digital service delivery by 2025, prompting entities like Dubai Electricity and Water Authority (DEWA) to adopt cloud contact centers. Saudi Arabia’s Vision 2030 includes a $10 billion investment in digital transformation, with STC Group deploying AI-powered cloud contact centers across healthcare and utilities.

COMPETITIVE LANDSCAPE

The competitive landscape of the cloud-based contact center market is characterized by rapid innovation, strategic differentiation, and a convergence of communication, analytics, and artificial intelligence. Market leaders are no longer competing solely on feature sets but on the depth of integration, intelligence, and ease of deployment. The lines between traditional contact center vendors, cloud infrastructure providers, and collaboration platforms are increasingly blurring, as companies like Amazon, Microsoft, and Google leverage their broader cloud ecosystems to offer comprehensive customer engagement solutions. Differentiation is achieved through AI-driven personalization, omnichannel fluency, and developer-friendly architectures that enable customization and scalability. Mid-tier players focus on niche capabilities such as workforce optimization, industry-specific compliance, or multilingual support to carve out specialized positions. Strategic partnerships, acquisitions, and platform integrations are common as vendors aim to expand their functionality and global reach. The market also sees growing pressure to balance innovation with security, data governance, and ethical AI use, particularly in regulated sectors. Customer expectations for seamless, instant, and context-aware service continue to drive product evolution, making agility and responsiveness success factors.

KEY MARKET PARTICIPANTS

Companies that play a key role in the cloud-based contact center market include

- Cisco Systems

- Genesys

- Five9

- New Voice Media

- Oracle

- 3clogic

- Aspect Software

- Nice Ltd

- AWS

- Connect First

- Avaya

- Vonage

- Talkdesk

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- Amazon Web Services has emerged as a dominant force in the cloud-based contact center landscape through its innovative Amazon Connect platform. Designed for scalability and integration, AWS leverages its vast global cloud infrastructure to deliver a serverless, omnichannel contact center solution that adapts to dynamic enterprise needs. The company’s strength lies in its seamless synergy with other AWS services, such as artificial intelligence, machine learning, and data analytics, enabling organizations to build intelligent, responsive customer engagement systems. AWS emphasizes flexibility, allowing businesses to customize workflows without heavy reliance on IT teams. Its pay-per-use model and rapid deployment capabilities have made it a preferred choice for enterprises undergoing digital transformation.

- Cisco has established a formidable presence in the cloud-based contact center market through its Webex Contact Center solution, which integrates voice, video, chat, and AI-driven insights into a unified collaboration environment. The company’s strategic advantage stems from its deep-rooted expertise in enterprise communications and networking, enabling secure, high-performance contact center deployments across hybrid and remote work models. Cisco emphasizes end-to-end encryption, compliance, and user experience, aligning its offerings with the evolving demands of regulated industries. Its focus on intelligent automation, real-time agent assistance, and workforce engagement tools differentiates its platform in a competitive landscape.

- Genesys stands as a pioneer in the cloud-based contact center domain, renowned for its PureCloud-powered Genesys Cloud CX platform that delivers a fully unified, AI-enhanced customer experience ecosystem. The company’s philosophy centers on hyper-personalization, predictive engagement, and omnichannel consistency, enabling businesses to anticipate customer needs and deliver seamless interactions across touchpoints. Genesys distinguishes itself through its open architecture, which supports rapid integration with CRM, workforce optimization, and data analytics tools, fostering agility in complex enterprise environments. Its commitment to innovation is evident in its continuous advancements in natural language processing, sentiment analysis, and automated routing. With a strong global footprint and a focus on customer-centric design, Genesys empowers organizations to transform service operations into strategic growth engines. Its developer-friendly environment and robust API framework encourage ecosystem expansion by making it a preferred partner for enterprises seeking intelligent, scalable, and future-ready contact center solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- One major strategy employed by leading players is deep integration with artificial intelligence and machine learning to enhance customer engagement and operational efficiency. These intelligent systems enable personalized interactions, reduce handling times, and improve first-contact resolution, thereby elevating service quality. Vendors are increasingly incorporating generative AI to assist in script generation, knowledge retrieval, and self-service automation, allowing agents to focus on complex inquiries. This strategic emphasis on AI not only differentiates platforms but also aligns with enterprise demands for predictive insights and scalable automation.

- Another key approach is the development of open, API-first architectures that promote seamless interoperability with third-party applications and enterprise systems. Leading providers are prioritizing ecosystem expansion by enabling easy integration with CRM platforms, collaboration tools, data warehouses, and security frameworks. This openness allows businesses to avoid vendor lock-in, customize workflows, and leverage existing technology investments.

- A third strategy is the expansion of global cloud infrastructure and regional data centers to address data sovereignty, compliance, and latency concerns. As enterprises operate across multiple jurisdictions with varying privacy regulations, vendors are investing in localized cloud deployments to ensure adherence to regional laws such as GDPR, CCPA, and DPDP.

Global Cloud-Based Contact Center Market News

- In March 2024, Genesys launched its next-generation AI assistant, designed to provide real-time guidance to agents by analyzing customer sentiment and suggesting optimal responses, enhancing service quality and consistency across interactions.

- In January 2024, Cisco integrated advanced generative AI capabilities into Webex Contact Center, enabling automated summarization of customer calls, dynamic knowledge retrieval, and intelligent self-service options to improve agent productivity.

- In November 2023, Amazon Web Services introduced a new compliance framework within Amazon Connect, supporting regional data residency and encryption standards to meet stringent regulatory requirements across Europe and Asia-Pacific.

- In September 2023, Five9 expanded its partnership with Google Cloud to enhance AI-powered analytics and speech recognition within its contact center platform by enabling deeper customer insights and improved operational efficiency.

- In June 2023, NICE extended its cloud contact center suite with augmented reality-based agent training modules, which is leveraging immersive learning environments to accelerate onboarding and skill development.

MARKET SEGMENTATION

This research report on the global cloud-based contact center market has been segmented and sub-segmented based on solution, service, application, deployment mode, organization size, vertical and region.

By Solution

- Automatic Call Distribution (ACD)

- Agent Performance Optimization (APO)

- Dialers

- Interactive Voice Response (IVR)

- Computer Telephony Integration (CTI)

- Reporting and analytics

- Security

- Others (issue tracking, omnichannel, and mobile care solutions)

By Service

- Professional Service

- Managed Service

By Application

- Call Routing and Queuing

- Data Integration and Recording

- Chat Quality and Monitoring

- Real-Time Decision-Making

- Workforce Optimization (WFO)

By Deployment Mode

- Public cloud

- Private cloud

- Hybrid cloud

By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

By Vertical

- Banking, Financial Services, and Insurance (BFSI)

- Consumer goods and retail

- Government and public sector

- Healthcare and life sciences

- Manufacturing

- Media and entertainment

- Telecommunication and Information Technology-Enabled Services (ITES)

- Others (transportation and logistics, and education

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What factors are driving the growth of the cloud-based contact center market globally?

Factors driving growth include the need for flexibility, scalability, cost-effectiveness, and the demand for omnichannel customer engagement solutions, all of which are addressed by cloud-based contact center services.

Which regions are experiencing the highest growth in the adoption of cloud-based contact centers?

North America and Europe are leading in the adoption of cloud-based contact centers, with Asia-Pacific also witnessing rapid growth due to increasing digital transformation initiatives.

Who are the major companies in the global cloud-based contact center market?

Cisco Systems, Genesys, Five9, New Voice Media, Oracle, 3clogic, Aspect Software, Nice Ltd, Connect First, Avaya, Vonage and Talkdesk are some of the major players in the global cloud-based contact center market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com