Asia Pacific Home Healthcare Software Market Research Report – Segmented By Type of Software (Agency Management, Clinical Management, Hospice Software Solutions, Other Software), Service, Mode of Delivery and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) – Industry Analysis From 2026 to 2034

Asia Pacific Home Healthcare Software Market Size

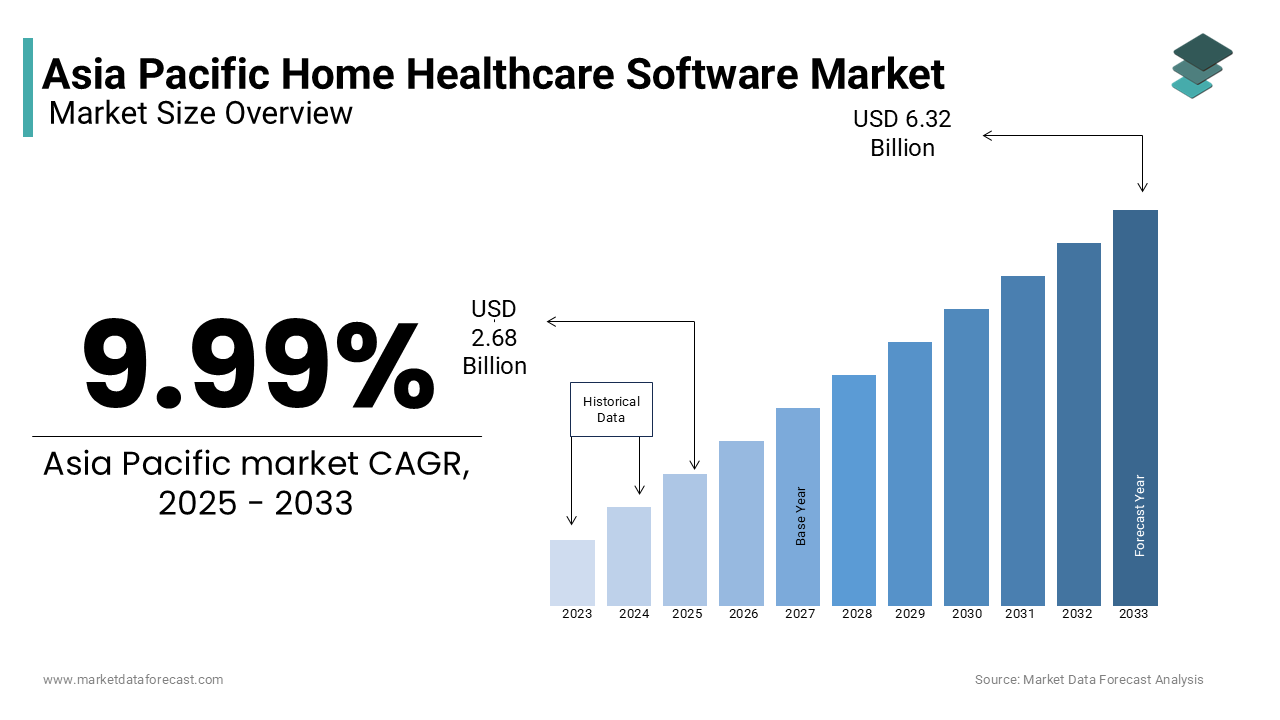

In 2024, the Asia Pacific home healthcare software market was valued at USD 2.68 billion and is forecasted to grow to USD 6.32 billion by 2033, at a CAGR of 9.99%.

Home Healthcare Software involves digital platforms and systems designed to support remote patient monitoring, care coordination, electronic health records (EHR), medication management, and telehealth services delivered outside traditional clinical settings. This market is increasingly pivotal in addressing the growing demand for cost-effective, patient-centric healthcare solutions, especially in the wake of the global shift toward decentralized care models. Countries such as Japan, Australia, and South Korea have demonstrated early adoption due to their advanced healthcare infrastructures and aging populations. As per the United Nations, by 2030, the number of people aged 65 and above in the Asia Pacific region is projected to reach 650 million, significantly driving the need for home-based healthcare interventions. The integration of AI, IoT, and cloud-based systems into home healthcare software has further enhanced service delivery, enabling real-time monitoring and data-driven decision-making. Additionally, the World Health Organization has pointed out a steady rise in chronic disease prevalence across the region, particularly in countries like India and China, reinforcing the urgency for scalable digital health solutions. These evolving healthcare dynamics are shaping the trajectory of the Home Healthcare Software Market across the Asia Pacific.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases

The escalating burden of chronic diseases such as diabetes, cardiovascular disorders, and respiratory illnesses is one of the primary drivers of the Asia Pacific Home Healthcare Software Market. According to the World Health Organization, non-communicable diseases (NCDs) account for over 60% of all deaths in the Asia Pacific region, with countries like India and China witnessing a sharp increase in chronic disease incidence. This trend has intensified the demand for continuous, real-time health monitoring solutions that can be deployed in home settings. For instance, in China, the National Center for Chronic and Non-communicable Disease Control and Prevention reports that cardiovascular diseases cause more than 40% of all deaths, further amplifying the necessity for home-based digital health interventions. These software platforms facilitate early detection, personalized treatment, and seamless communication between patients and healthcare providers, reducing hospital readmissions and improving patient outcomes.

Increasing Geriatric Population and Demand for In-Home Care

The growing elderly population in the Asia Pacific region is another significant driver of the Home Healthcare Software Market. As per the United Nations, the proportion of the population aged 65 and above is increasing rapidly, with Japan leading the trend where over 29% of the population falls into this category. By 2050, this demographic is expected to account for a notable share of the total population across the Asia Pacific. Older adults often require long-term care and suffer from multiple comorbidities, making home-based healthcare an attractive alternative to institutionalized care. In response, governments and healthcare providers are increasingly investing in digital platforms that enable caregivers to monitor patients remotely. For example, in Australia, as per the Department of Health, in 2023, over 1.5 million Australians received some form of home or community-based care, with a large proportion supported by digital health tools. Similarly, South Korea has introduced national telehealth initiatives under its Ministry of Health and Welfare to support aging in place, significantly boosting the adoption of home healthcare software.

MARKET RESTRAINTS

Regulatory and Data Privacy Challenges

The complex regulatory environment and concerns around data privacy is a major restraints impeding the growth of the Asia Pacific Home Healthcare Software Market. Each country in the region has its own set of healthcare data protection laws, making it difficult for software providers to develop standardized solutions. For instance, in Australia, the Office of the Australian Information Commissioner enforces the Privacy Act 1988, which mandates strict handling of personal health information. Similarly, in Japan, the Act on the Protection of Personal Information (APPI) imposes stringent compliance requirements on digital health platforms. These regulations, while essential for patient safety, often result in increased development costs and delayed market entry for software providers. This has led to hesitancy among both providers and consumers to fully adopt digital health solutions due to fears of data misuse. The lack of harmonized data governance frameworks across the region further complicates interoperability and integration of home healthcare software with national health systems.

Limited Digital Literacy and Infrastructure Gaps

The limited digital literacy and uneven technological infrastructure across the region is another key restraint for the Asia Pacific Home Healthcare Software Market. While countries like Singapore, Japan, and South Korea have robust digital ecosystems, many emerging economies such as Indonesia, the Philippines, and parts of India still struggle with low internet penetration and inadequate healthcare IT infrastructure. This disparity hampers the widespread adoption of home healthcare software, especially among elderly and rural populations who are the primary beneficiaries. Additionally, as per a 2022 survey by the Asian Development Bank, only 40% of healthcare workers in Southeast Asia were proficient in using digital health tools, indicating a significant skills gap. In countries like Vietnam and Thailand, the lack of trained personnel to operate and maintain digital health systems further delays implementation. Moreover, the affordability of smart devices and reliable internet access remains a challenge for lower-income groups.

MARKET OPPORTUNITIES

Expansion of Telehealth Services and Remote Monitoring

The rapid expansion of telehealth services and remote patient monitoring (RPM) is one of the most promising opportunities for the Asia Pacific Home Healthcare Software Market. Governments and private healthcare providers across the region are increasingly recognizing the benefits of virtual consultations and continuous health tracking, especially in light of the post-pandemic healthcare landscape. The integration of RPM tools within home healthcare software allows for real-time data collection on vital signs, medication adherence, and activity levels, enabling timely interventions and reducing hospitalization rates. In India, the Ministry of Health and Family Welfare has launched the Ayushman Bharat Digital Mission, aiming to create a national digital health ecosystem that supports home-based care through software integration. Additionally, in China, the National Health Commission has encouraged the use of telehealth platforms to manage chronic diseases in rural areas, where access to traditional healthcare facilities is limited. These developments show a growing ecosystem conducive to the adoption of home healthcare software, offering immense potential for market players to innovate and scale their offerings across the Asia Pacific.

Integration of Artificial Intelligence and Predictive Analytics

The integration of artificial intelligence (AI) and predictive analytics into home healthcare software is emerging as a transformative opportunity for the Asia Pacific market. AI-driven tools are enabling more accurate diagnostics, personalized treatment plans, and proactive health management by analyzing vast amounts of patient data in real time. The use of predictive analytics is also gaining traction in China, where platforms such as Ping An Good Doctor are leveraging machine learning to provide remote health assessments and disease risk predictions. These technologies not only improve patient outcomes but also reduce the burden on healthcare systems by enabling early interventions.

MARKET CHALLENGES

Interoperability Issues Across Digital Health Platforms

The lack of interoperability among digital health platforms is one of the major challenges facing the Asia Pacific Home Healthcare Software Market. The region's healthcare ecosystem is highly fragmented, with diverse electronic health record (EHR) systems, telehealth platforms, and medical devices that often operate on incompatible data formats and communication protocols. According to a 2023 report by the Asia eHealth Information Network (AeHIN), only 30% of healthcare institutions in Southeast Asia have fully integrated digital systems, limiting the seamless exchange of patient data across providers. In countries like India and Indonesia, where multiple home healthcare software vendors operate with proprietary systems, the absence of standardized data exchange frameworks hampers care coordination and continuity. The World Health Organization has emphasized the need for universal health interoperability standards, such as HL7 and FHIR, but their adoption remains inconsistent across the region. Additionally, in Australia, the Australian Digital Health Agency has reported that interoperability issues contribute to nearly 25% of avoidable medical errors in home-based care settings. These technical barriers not only reduce the efficiency of home healthcare delivery but also discourage investment in digital health solutions.

High Implementation and Maintenance Costs

The high cost associated with the implementation and ongoing maintenance of digital health systems is a significant challenge for the Asia Pacific Home Healthcare Software Market. While the long-term benefits of home healthcare software are well-documented, initial setup costs, including software licensing, hardware procurement, staff training, and system integration, pose a major barrier, particularly for small healthcare providers and home care agencies. In developing economies such as Vietnam and the Philippines, where healthcare budgets are limited, these expenses can be prohibitive. Additionally, ongoing maintenance, cybersecurity upgrades, and software updates further add to the financial burden. As per the Ministry of Health in Thailand, nearly 40% of local home healthcare providers cited financial constraints as the primary reason for delaying digital transformation. Moreover, in rural areas, the lack of skilled IT personnel to manage these systems increases dependency on external consultants, escalating operational costs.

SEGMENTAL ANALYSIS

By Type of Software Insights

The Clinical Management Software segment held the largest share of the Asia Pacific Home Healthcare Software Market of 35.1% of total revenue in 2024. This dominance is primarily attributed to its critical role in managing patient records, treatment plans, medication schedules, and real-time health monitoring. As per the Asia Pacific Telehealth Federation, the increasing integration of electronic health records (EHRs) and clinical decision support systems (CDSS) within home healthcare settings has significantly boosted the demand for clinical management software. In Japan, for instance, as per the Ministry of Health, Labour and Welfare, over 60% of home healthcare agencies have adopted clinical management systems to streamline patient care and reduce medical errors. The software’s ability to support interoperability with wearable health devices and telehealth platforms has further strengthened its position as the most widely adopted solution.

The Hospice Software Solutions segment is the fastest-growing in the Asia Pacific Home Healthcare Software Market and is projected to expand at a CAGR of 12.5% from 2025 to 2033. The rapid growth of this segment is driven by the rising demand for end-of-life care services and the need for specialized digital tools to manage patient comfort, medication, and caregiver coordination. In India, as per the Indian Association of Palliative Care, home-based hospice services have grown by 45% since 2020, largely due to cultural preferences for end-of-life care at home. To support this shift, hospice software solutions are being equipped with features such as symptom tracking, pain management alerts, and family communication portals. In South Korea, as per the National Cancer Center, digital adoption in hospice care has improved care delivery efficiency by 35%, encouraging more agencies to invest in specialized software.

By Service Insights

The Skilled Nursing segment led the Asia Pacific Home Healthcare Software Market by capturing 30.4% of total revenue in 2024. This segment involves the delivery of professional medical care, including wound care, intravenous therapy, and post-surgical recovery, all of which require robust software support for scheduling, documentation, and compliance. In Japan, where over 29% of the population is aged 65 or above, as per the Ministry of Health, Labour and Welfare, home-based skilled nursing services increased by 25% between 2020 and 2023. The integration of real-time monitoring and mobile documentation tools into skilled nursing software platforms has further enhanced efficiency and care accuracy.

The Rehabilitation Services segment is the fastest-growing in the Asia Pacific Home Healthcare Software Market and is projected to grow at a CAGR of 13.2% through 2033. The growth of this segment is primarily fueled by the increasing incidence of musculoskeletal disorders, stroke recovery cases, and post-operative rehabilitation needs. According to the World Health Organization, stroke is a leading cause of disability in the Asia Pacific, with over 7 million cases reported annually, particularly in China and India. In response, home-based rehabilitation services supported by digital platforms are gaining traction. For instance, in India, the Indian Spinal Injuries Centre reported a 50% rise in home-based physiotherapy services between 2021 and 2023, largely enabled by mobile-enabled rehabilitation software. In South Korea, as per the Korean Society of Physical Medicine and Rehabilitation, the use of AI-assisted rehabilitation software increased patient adherence to therapy by 40% in 2023.

By Mode of Delivery Insights

The Cloud-Based Software segment dominated the Asia Pacific Home Healthcare Software Market by accounting for 55.6% of total revenue in 2024. The lead position of this segment is driven by the increasing preference for scalable, cost-effective, and interoperable digital solutions that support remote access, real-time data synchronization, and seamless integration with other healthcare platforms. In India, as per the Ministry of Electronics and Information Technology, the government’s push for digital health records under the Ayushman Bharat Digital Mission has accelerated cloud adoption among home care providers.

The On-Premises Software segment is the fastest-growing in the Asia Pacific Home Healthcare Software Market and is projected to expand at a CAGR of 11.8% from 2025 to 2033. The growth of this segment is attributed to the increasing demand for localized data control, compliance with stringent data protection laws, and the preference for customized software deployment among large healthcare providers. Similarly, in South Korea, as per the Korea Internet & Security Agency, 60% of large home healthcare organizations prefer on-premises systems to comply with the country’s stringent personal information protection laws.

REGIONAL ANALYSIS

Japan Home Healthcare Software Market Insights

Japan led the Asia Pacific Home Healthcare Software Market by accounting for 25.4% of total regional revenue in 2024. As a leader in healthcare digitization and aging population management, Japan has been at the forefront of adopting home healthcare software to support its rapidly expanding elderly demographic. According to the Statistics Bureau of Japan, over 29% of the population is aged 65 or above, driving the demand for home-based care solutions. The Japanese Ministry of Health, Labour and Welfare has actively promoted home healthcare through policy incentives and digital health initiatives such as the “New Orange Plan,” which supports home nursing and elderly care services. Additionally, the widespread adoption of electronic health records (EHRs) and remote monitoring systems has enabled seamless care delivery outside traditional hospital settings. Companies such as Fujitsu and NEC have played a pivotal role in developing AI-driven home healthcare software that enhances patient monitoring and caregiver coordination.

China Home Healthcare Software Market Insights

China is another key player in the Asia Pacific Home Healthcare Software Market by capturing 20.5% of total regional revenue in 2024. The country’s rapid urbanization, rising chronic disease burden, and aging population are key drivers of home healthcare software adoption. According to the National Bureau of Statistics of China, the proportion of the population aged 60 and above reached 19% in 2023, equating to over 280 million individuals. The Chinese National Health Commission has responded by promoting home-based medical services through policy frameworks such as the "Guidelines for Strengthening Home-Based Medical Services," which encourage the use of digital tools to support elderly and post-acute care. Additionally, the expansion of telemedicine platforms like Ping An Good Doctor and WeDoctor has accelerated the integration of home healthcare software into routine patient care. In 2023, as per the China Academy of Information and Communications Technology, over 45 million home healthcare consultations were conducted via digital platforms, a 30% increase from the previous year.

Australia Home Healthcare Software Market Insights

Australia held a significant portion in the Asia Pacific Home Healthcare Software Market. The country’s well-developed healthcare infrastructure, high digital literacy, and strong government support for home-based care have contributed to its prominent position. The Australian Digital Health Agency has played a crucial role in promoting digital health integration through initiatives such as My Health Record, a national electronic health record system that supports home healthcare coordination.

South Korea Home Healthcare Software Market Insights

South Korea is a major player in the Asia Pacific Home Healthcare Software Market. The country’s advanced healthcare IT infrastructure, coupled with a rapidly aging population, has created a conducive environment for digital home healthcare solutions. According to Statistics Korea, the elderly population (aged 65 and above) accounted for 18.4% of the total population in 2023, up from 16.7% in 2020. The South Korean Ministry of Health and Welfare has actively supported home healthcare through initiatives like the Smart Senior Healthcare Service, which integrates remote monitoring, AI diagnostics, and mobile nursing services. The country’s focus on smart aging, combined with robust digital health policies, positions South Korea as a key growth driver in the regional home healthcare software market.

India Home Healthcare Software Market Insights

India is emerging as a significant market in the Asia Pacific Home Healthcare Software Market. The country’s growing middle-class population, increasing prevalence of chronic diseases, and rising awareness of home-based care are key factors fueling market growth. According to the Indian Council of Medical Research, non-communicable diseases account for over 65% of total deaths in India, with diabetes, hypertension, and cardiovascular diseases being the most prevalent. To address this burden, the Ministry of Health and Family Welfare has launched the Ayushman Bharat Digital Mission, which promotes digital health records and home healthcare software integration.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a significant role in the APAC home healthcare software market profiled in this report are Allscripts Healthcare Solutions, Carestream Health, GE Healthcare, NextGen Healthcare Information System LLC, Siemens Healthcare, Novarad Corporation, MEDITECH, Cerner Corporation, Agfa Healthcare, WellSky, Medical Information Technology, Inc. (Meditech), and Continulink.

The Asia Pacific Home Healthcare Software Market is characterized by a dynamic and evolving competitive landscape, with a mix of global leaders and regional players striving to capture market share. The market is moderately fragmented, with several established software vendors offering specialized solutions tailored to the diverse healthcare needs of different countries. While multinational corporations bring in advanced technological capabilities and strong brand recognition, local players are leveraging their in-depth understanding of regional regulatory frameworks and patient care models to gain traction. Innovation remains a key battleground, with companies continuously enhancing their platforms through AI integration, cloud-based deployment, and interoperability features. Additionally, strategic acquisitions and partnerships are becoming increasingly common as firms seek to strengthen their product portfolios and expand into high-growth markets. The emphasis on user-friendly interfaces, compliance with healthcare standards, and seamless integration with existing health systems is shaping the competitive dynamics across the Asia Pacific region.

Top Players in the Asia Pacific Home Healthcare Software Market

One of the leading players in the Asia Pacific Home Healthcare Software Market is McKesson Corporation. The company has a strong global presence and has been instrumental in developing advanced home healthcare software solutions that streamline clinical workflows, enhance patient engagement, and improve care coordination. McKesson's software platforms are widely used across Asia Pacific for managing home nursing, telehealth, and chronic disease monitoring. Its focus on interoperability and integration with electronic health records has made it a preferred choice among healthcare providers.

Another key player is Allscripts Healthcare Solutions, known for its comprehensive home healthcare software offerings that support remote patient monitoring, medication management, and mobile documentation. The company has been actively expanding its footprint in the Asia Pacific by partnering with regional healthcare providers and leveraging cloud-based technologies to deliver scalable solutions. Allscripts has contributed significantly to improving the efficiency of home healthcare delivery through its intuitive and user-friendly platforms.

Cerner Corporation, now part of Oracle, is also a major contributor to the Asia Pacific Home Healthcare Software Market. The company offers robust software solutions tailored for home care settings, including clinical documentation, billing, and patient engagement tools. Cerner's integration of AI and analytics into home healthcare platforms has enabled providers to make data-driven decisions and deliver personalized care. Its global expertise and continuous innovation have made it a key player in shaping the digital transformation of home healthcare in the region.

Top Strategies Used by Key Market Participants

A major strategy employed by key players in the Asia Pacific Home Healthcare Software Market is strategic partnerships and collaborations. Companies are increasingly aligning with local healthcare providers, government agencies, and technology firms to enhance their service offerings and better understand regional healthcare needs. These collaborations help in customizing software solutions to meet specific regulatory and clinical requirements across different countries in the region.

Another key strategy is product innovation and feature enhancement. Market leaders are investing heavily in research and development to integrate advanced technologies such as artificial intelligence, machine learning, and predictive analytics into their software platforms. These enhancements improve patient monitoring, automate clinical workflows, and support decision-making, thereby increasing the adoption of home healthcare software.

Lastly, expansion into emerging markets is a crucial growth strategy. As countries like India, Indonesia, and Vietnam show increasing demand for home-based care, companies are expanding their presence through localized solutions, regional offices, and distribution networks. This approach allows them to tap into new customer bases and establish long-term market footholds in high-growth areas of the Asia Pacific.

RECENT MARKET DEVELOPMENTS

- In February 2024, McKesson Corporation launched a new cloud-based home healthcare management platform in Australia, designed to improve patient engagement and streamline caregiver workflows. The platform integrates with existing telehealth systems and supports real-time data exchange between patients and healthcare providers.

- In June 2024, Allscripts Healthcare Solutions partnered with a leading telemedicine provider in India to embed its home healthcare software into virtual care platforms, enhancing remote monitoring and medication adherence capabilities for chronic disease patients.

- In September 2024, Cerner Corporation, now under Oracle, expanded its regional headquarters in Singapore to better serve Southeast Asian markets, focusing on localized software development and customer support for home healthcare providers.

- In November 2024, Philips, a key player in connected health solutions, introduced an AI-powered home monitoring system in Japan that integrates with existing home healthcare software to support elderly patients with chronic conditions.

- In March 2025, Fujitsu collaborated with a South Korean home care agency to deploy an AI-driven patient analytics module that enhances clinical decision-making and enables proactive care planning for home-based patients.

MARKET SEGMENTATION

This research report on the APAC home healthcare software market has been segmented and sub-segmented into the following categories.

By Type of Software

- Agency Management

- Clinical Management

- Hospice Software Solutions

- Other Software

By Service

- Rehabilitation

- Infusion Therapy

- Respiratory Therapy

- Pregnancy Care

- Skilled Nursing

- Others

By Mode of Delivery

- Cloud-Based Software

- On-Premises Software

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com