Asia-Pacific Pet Insurance Market Size, Share, Trends & Growth Forecast Report By Coverage (Accident & Illness, Accident Only, Others), Animal (Dogs, Cats, Others), Sales Channel (Agency, Broker, Direct, Bancassurance, Others), and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC) – Industry Analysis From 2024 to 2033.

Asia-Pacific Pet Insurance Market Summary

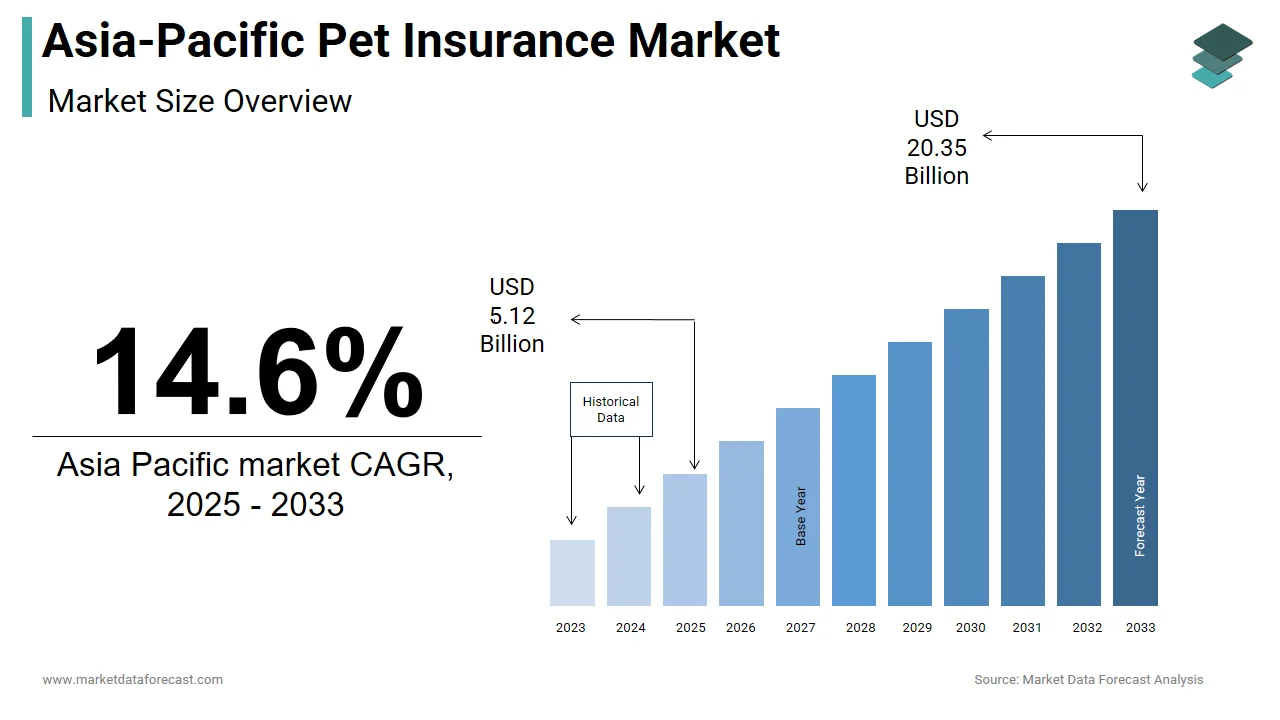

The Asia-Pacific pet insurance market size was valued at USD 4.31 billion in 2024 and is projected to reach USD 20.35 billion by 2033, growing at a CAGR of 14.6% from 2024 to 2033. The market is witnessing rapid growth driven by rising veterinary costs, increased awareness of pet wellness, and the adoption of digital insurance platforms.

Key Market Trends & Insights

- Japan accounted for the largest share of the Asia Pacific market in 2024, with a 30.4% share.

- Based on animal, the dogs segment held the leading share of 55.4% in 2024.

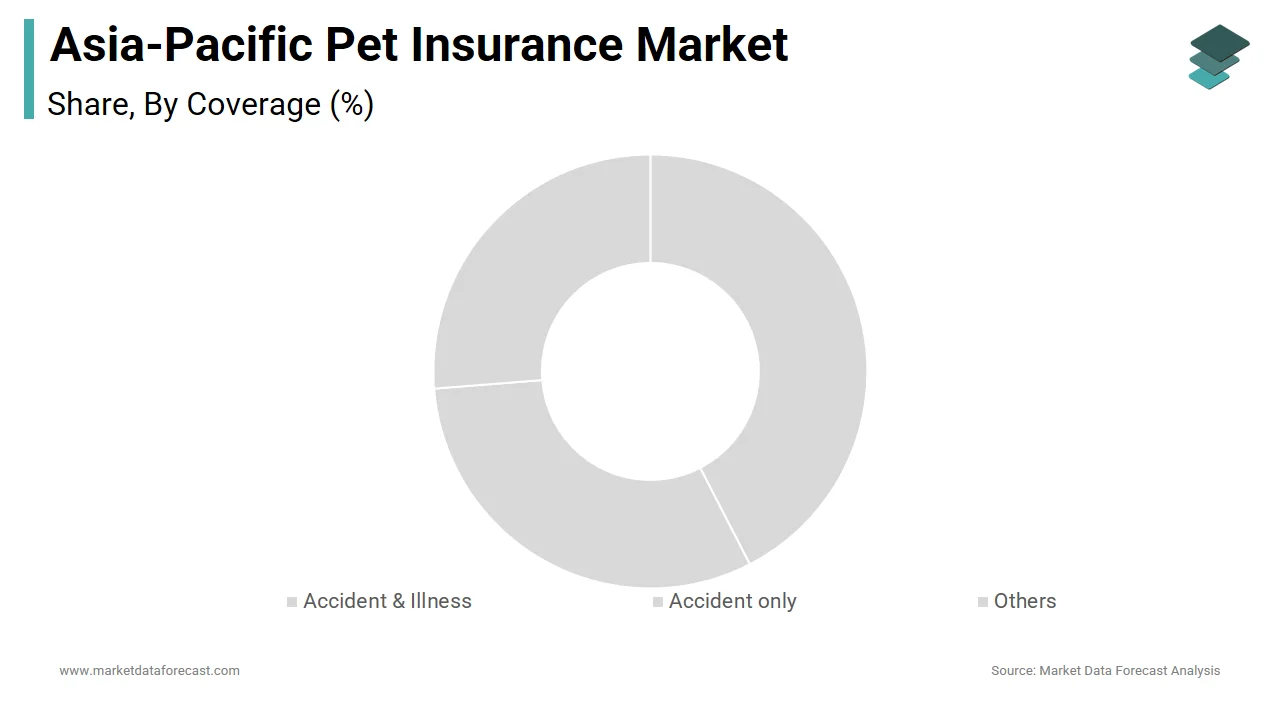

- Based on coverage, the accident and illness coverage segment dominated the market in 2024.

- Based on sales channel, the direct sales channel captured 45.3% of the market in 2024.

- India and China are emerging as high-growth markets due to increasing insurance awareness.

Market Size & Forecast

- 2024 Market Size: USD 4.31 Billion

- 2033 Projected Market Size: USD 20.35 Billion

- CAGR (2024–2033): 14.6%

- Japan: Largest market in 2024

- India & China: Fastest-growing markets

Asia-Pacific Pet Insurance Market Size

The Asia-Pacific pet insurance market is projected to grow from USD 4.31 billion in 2024 to USD 20.35 billion by 2033, at a CAGR of 14.6% from 2024 to 2033.

MARKET DRIVERS

Rising Veterinary Costs and Advanced Treatments

The escalating cost of veterinary care is a significant driver of the Asia Pacific pet insurance market.. For instance, in Australia, the average cost of treating a dog with cancer exceeds $5,000, as reported by the Australian Veterinary Association. These rising costs have prompted pet owners to seek financial protection by boosting demand for insurance plans. Additionally, the integration of telemedicine platforms has revolutionized pet healthcare by enabling remote consultations and reducing costs. Over 40% of urban pet owners in the region prefer subscription-based insurance models that include telehealth services.

Growing Awareness of Pet Health and Wellness

Increasing awareness of pet health and wellness is another key driver of the Asia Pacific pet insurance market. In Japan, campaigns promoting pet wellness have resulted in a 30% increase in insurance adoption rates since 2020, as per the Japan Pet Insurance Association. Furthermore, the rise of social media influencers and educational platforms has amplified awareness about the benefits of pet insurance. For example, collaborations between insurers and veterinarians on platforms like Instagram have attracted tech-savvy millennials.

MARKET RESTRAINTS

Low Awareness in Rural Areas

Low awareness of pet insurance remains a significant restraint in rural and underdeveloped regions. This mindset is deeply rooted in cultural practices, where pets are often considered working animals rather than companions. For instance, in Indonesia and Vietnam, traditional methods such as herbal remedies are still preferred over commercial healthcare solutions. Additionally, the absence of targeted awareness campaigns exacerbates the issue by leaving many unaware of the benefits of pet insurance. Overcoming this barrier requires localized marketing strategies and partnerships with local veterinarians, which is posing operational challenges for industry players.

Affordability Concerns Among Low-Income Groups

Affordability concerns present another major restraint among low-income populations in emerging markets. Moreover, the high cost of comprehensive plans exacerbates the issue, with many unable to afford coverage for advanced treatments. For example, in rural India, only 10% of pet owners have access to affordable insurance options,. These financial constraints not only restrict market growth but also necessitate the development of budget-friendly plans by posing a challenge for companies aiming to balance profitability with accessibility.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Emerging markets such as India, Indonesia, and Vietnam present significant opportunities for the Asia Pacific pet insurance market. Population resides in rural areas, many of whom remain underserved by commercial pet healthcare solutions. The rise of affordable insurance plans tailored to local needs has begun to bridge this gap by enabling wider adoption. For instance, in 2022, HDFC Ergo launched a low-cost pet insurance plan in India by resulting in a 25% increase in policy sales within six months, as per Nielsen. Additionally, government initiatives promoting livestock health have indirectly benefited pet insurance by creating awareness about animal welfare. The veterinary outreach programs in Southeast Asia have improved healthcare standards by fostering trust among rural populations. The companies can unlock immense growth potential in these untapped markets by addressing infrastructural gaps and tailoring offerings to local preferences.

Integration of Technology and Personalized Plans

The integration of technology and personalized insurance plans offers transformative opportunities for the Asia Pacific pet insurance market. For example, Singapore-based PawfectCare introduced an app in 2022 that provides real-time health monitoring and personalized insurance recommendations, attracting over 100,000 users within a year. Another factor is the rise of subscription-based models, which offer convenience and recurring revenue streams. The urban pet owners in the region prefer bundled plans that include wellness benefits, such as annual check-ups and grooming services. These innovations not only cater to evolving consumer preferences but also position companies as pioneers in the digital transformation of pet insurance.

MARKET CHALLENGES

Fragmented Regulatory Frameworks

Fragmented regulatory frameworks pose a significant challenge to the Asia Pacific pet insurance market by creating operational inefficiencies for multinational companies. Each country imposes unique compliance requirements by complicating efforts to standardize policies and pricing. For instance, while Japan mandates stringent quality certifications for pet healthcare providers, countries like Thailand have minimal regulations, leading to inconsistencies in service standards. Furthermore, sudden policy changes disrupt operations, as seen in China’s ban on certain imported pet medications in 2021, which affected over $300 million in annual claims, according to the International Trade Administration. Such complexities necessitate significant investments in regulatory expertise, which is straining resources for smaller players and limiting market entry for new entrants.

Limited Veterinary Infrastructure in Rural Areas

Limited veterinary infrastructure remains a critical challenge in rural and underdeveloped regions. According to the World Organisation for Animal Health, over 50% of Asia Pacific countries lack adequate veterinary facilities, which results in untreated illnesses and higher mortality rates among pets. For example, in Cambodia and Myanmar, only 20% of pet owners have access to professional healthcare services, as per Veterinarians Without Borders.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Coverage, Animal, Sales Channel, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Trupanion, Inc., Deutsche Familienversicherung AG (DFV), Petplan (Allianz), Jab Holding Company, Direct Line, EQT Group, Lassie, Getsafe GmbH, Waggel Limited, Feather Insurance, Napo Limited, Tesco, Sainsbury Bank Plc, Fressnapf Holding SE, MetLife Services and Solutions, LLC, HDFC Ergo, Nationwide Mutual Insurance Company, Anicom Insurance, AliPay, and others. |

SEGMENTAL ANALYSIS

By Coverage Insights

The "Accident & Illness" segment dominated the Asia Pacific pet insurance market with a significant share in 2024, with the rising costs of veterinary care, particularly for chronic conditions and surgeries. A key factor fueling this growth is the increasing awareness of preventive healthcare among urban populations. Additionally, insurers have introduced bundled wellness benefits, such as annual check-ups and vaccination,s by enhancing the appeal of these policies. These factors ensure that "Accident & Illness" remains the largest and most lucrative segment in the market.

The "Accident Only" segment is Asia Pacific pet insurance market is likely to register a CAGR of 18.5% during the forecast period owing to the affordability concerns among price-sensitive consumers in emerging markets like India and Indonesia. Another driving factor is the rise of microinsurance products tailored to rural populations. For instance, in 2022, HDFC Ergo launched an accident-only plan in India priced at less than $5 monthly by resulting in a 40% increase in policy adoption within six months.

By Animal Insights

The dogs dominated the Asia Pacific pet insurance market with 55.4% of share in 2024 owing to the widespread perception of dogs as loyal companions and protectors in urban areas. A key factor is the high cost of veterinary treatments for dogs, which has increased by 20% annually between 2019 and 2022. Additionally, insurers have introduced specialized plans for breeds prone to genetic conditions, such as German Shepherds and Bulldogs by enhancing the appeal of dog insurance.

The cats segment is anticipated to exhibit a CAGR of 20.3% from 2025 to 2033. This rapid expansion is fueled by the growing popularity of cats as low-maintenance pets among urban professionals. Another factor is the rise of telemedicine platforms offering specialized care for feline health issues, such as urinary tract infections and obesity. These trends position cats as the segment with the highest growth potential, which is reflecting evolving lifestyle preferences.

By Sales Channel Insights

The direct sales channel segment was accounted in holding 45.3% of the Asia Pacific pet insurance market share in 2024 with proliferation of e-commerce platforms and mobile apps by enabling seamless policy purchases. A key factor is the integration of AI-driven tools that simplify the underwriting process by reducing turnaround times. Data from Gartner reveals that over 60% of urban millennials prefer purchasing insurance directly through digital channels due to convenience. Additionally, personalized marketing campaigns targeting tech-savvy consumers have enhanced adoption rates.

The agency sales channel segment is likely to grow with a CAGR of 17.8% from 2025 to 2033 with the increasing presence of trained agents in rural and semi-urban areas, bridging awareness gaps about pet insurance. Another factor is the collaboration between insurers and local veterinarians to educate communities about the benefits of pet insurance. For instance, in 2022, Royal Canin partnered with veterinary clinics in Thailand to train agents by resulting in a 30% increase in rural policy adoption.

REGIONAL ANALYSIS

Japan led the Asia Pacific pet insurance market with 30.4% of share in 2024. The country’s dominance is driven by its advanced veterinary infrastructure and high adoption of pet insurance, particularly among urban households. According to the Japan Pet Insurance Association, over 60% of dog owners in Tokyo and Osaka have insurance policies, reflecting a strong culture of preventive healthcare.

A key factor is the integration of telemedicine platforms, which have streamlined access to veterinary services. Data from Deloitte reveals that 40% of Japanese pet owners use online consultations by reducing costs and improving accessibility. Additionally, government initiatives promoting pet welfare have fostered trust in commercial insurance products, ensuring sustained growth.

Australia ranks second in the Asia Pacific pet insurance market with its robust regulatory framework and high pet ownership rates. A key factor is the emphasis on pet health and wellness, with comprehensive insurance plans gaining popularity.

Another factor is the rise of eco-friendly insurance providers, aligning with the country’s sustainability goals. Additionally, partnerships with global brands like Mars Petcare have expanded accessibility, enabling seamless cross-border transactions. These developments ensure Australia remains a hub for cutting-edge pet insurance solutions.-

China is an emerging powerhouse in the Asia Pacific pet insurance market, driven by its young, tech-savvy population and increasing urbanization. A key factor is the rise of affordable insurance plans tailored to local needs, such as microinsurance products for rural populations. Another factor is the proliferation of mobile apps offering real-time health monitoring and personalized recommendations. Additionally, collaborations with e-commerce giants like Alibaba have streamlined distribution, boosting sales. These efforts position China as a high-potential market with immense growth opportunities.

South Korea is a mature player in the Asia Pacific pet insurance market, characterized by its focus on innovation and premiumization. A key factor is the integration of AI-driven platforms that analyze pet health data by offering customized coverage options. Another factor is the rise of pet cafes and social spaces, which have amplified awareness about pet insurance trends. According to a data from Euromonitor, over 60% of urban millennials participate in pet-related activities, which is driving demand for innovative policies. Additionally, government initiatives promoting spaying and neutering have improved pet health standards by fostering trust in commercial solutions. These dynamics ensure South Korea remains a key contributor to the regional market.

India is an emerging market in the Asia Pacific pet insurance sector, driven by its large rural population and increasing awareness of pet healthcare. A key factor is the introduction of affordable microinsurance plans, which cater to price-sensitive consumers in rural areas. Another factor is the rise of mobile veterinary clinics, which have improved access to healthcare and created awareness about insurance benefits. Additionally, collaborations with e-commerce platforms like Flipkart have streamlined access to pet insurance, which is boosting sales. These efforts position India as a high-growth market with immense potential.

KEY MARKET PLAYERS

Companies dominating the Asia-Pacific pet insurance market profiled in this report are Trupanion, Inc., Deutsche Familienversicherung AG (DFV), Petplan (Allianz), Jab Holding Company, Direct Line, EQT Group, Lassie, Getsafe GmbH, Waggel Limited, Feather Insurance, Napo Limited, Tesco, Sainsbury Bank Plc, Fressnapf Holding SE, MetLife Services and Solutions, LLC, HDFC Ergo, Nationwide Mutual Insurance Company, Anicom Insurance, AliPay, and others.

TOP LEADING PLAYERS IN THE MARKET

Allianz Care

Allianz Care is a leading player in the Asia Pacific pet insurance market, offering comprehensive coverage plans tailored to urban and rural consumers. In 2023, the company launched a mobile app enabling real-time claims processing, significantly enhancing user convenience. Additionally, Allianz partnered with local veterinary clinics in Australia and Japan to offer bundled wellness services, such as annual check-ups and vaccinations, boosting policy adoption. The company’s focus on affordability and accessibility has strengthened its reputation among price-sensitive consumers.

Royal Canin (Mars Group)

Royal Canin has emerged as a key innovator in the Asia Pacific pet insurance market by integrating health-focused solutions with its premium pet food offerings. In 2023, the company introduced a subscription-based model combining pet insurance with dietary management plans, targeting chronic health conditions. Furthermore, Royal Canin collaborated with telemedicine platforms in Thailand to provide remote consultations, improving healthcare accessibility. Royal Canin has positioned itself as a trusted provider of holistic pet care solutions by leveraging its expertise in pet nutrition and wellness.

PetSure

PetSure specializes in digital-first pet insurance solutions, making it a preferred choice for tech-savvy millennials. In 2023, the company partnered with e-commerce platforms like Lazada and Flipkart to streamline policy purchases, particularly in emerging markets like India and Indonesia. Additionally, PetSure introduced AI-driven tools to analyze pet health data, enabling personalized coverage recommendations. The company also launched educational campaigns promoting pet wellness, fostering trust among consumers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Asia Pacific pet insurance market employ diverse strategies to maintain their competitive edge. Partnerships with e-commerce platforms and veterinary clinics have streamlined distribution and enhanced accessibility. Additionally, investments in technology, such as AI-driven underwriting and telemedicine integrations, have improved user engagement. Companies also prioritize sustainability by adopting eco-friendly practices to align with consumer values. Finally, mergers and acquisitions allow firms to consolidate resources and expand into untapped markets, which is ensuring sustained growth and innovation.

COMPETITION OVERVIEW

The Asia Pacific pet insurance market is highly competitive, driven by the presence of global giants like Allianz Care and Mars Group, alongside regional players catering to local needs. Global firms leverage their technological expertise and extensive portfolios to attract urban consumers, while local operators capitalize on cultural insights and affordability. This rivalry has spurred significant innovations, such as AI-driven health monitoring and eco-friendly policies. However, challenges like fragmented regulations and limited awareness persist, creating barriers for new entrants.

RECENT MARKET DEVELOPMENTS

- In March 2023, Allianz Care launched a mobile app in Australia enabling real-time claims processing by significantly enhancing user convenience and boosting policy adoption rates.

- In June 2023, Royal Canin introduced a subscription-based model in Japan combining pet insurance with dietary management plans, which is targeting chronic health conditions among pets.

- In August 2023, PetSure partnered with Lazada to expand its presence in Southeast Asia, streamlining policy purchases through the e-commerce platform.

- In November 2023, Allianz Care collaborated with veterinary clinics in Thailand to offer bundled wellness services, such as annual check-ups and vaccinations, improving customer retention.

- In January 2024, Royal Canin integrated telemedicine platforms in India to provide remote consultations, which is addressing accessibility challenges in rural areas.

MARKET SEGMENTATION

This research report on the Asia Pacific pet insurance market has been segmented and sub-segmented based on coverage, animal, sales channel, and country.

By Coverage

- Accident & Illness

- Accident only

- Others

By Animal

- Dogs

- Cats

- Others

By Sales Channel

- Agency

- Broker

- Direct

- Bancassurance

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

In 2022, how much pet insurance market was valued in the Asia-Pacific?

The APAC pet insurance market was valued at USD 4.31 billion in 2024.

Which country is predicted to hold major share of the APAC pet insurance market in the coming years?

China is one of the potential regional markets in APAC.

What are the companies playing a leading role in the APAC pet insurance market?

The New India Assurance Company Limited, Oriental Insurance, Rakuten Inc., ipet Insurance, Anicom Insurance Inc., The People's Insurance Company of China, Guide Dogs Pet Insurance Australia, Medibank Private Limited, and Pet Insurance Australia are some of the notable companies in the APAC pet insurance market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com