Asia Pacific Computational Fluid Dynamics Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Deployment, End-User, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From (2026 to 2034)

Market Size, 2025

$870.65 MnMarket Estimate, 2026

$964.24 MnMarket Forecast, 2034

$2182.42 MnCAGR, 2026–2034

10.75%Asia Pacific Computational Fluid Dynamics Market Size

The Asia Pacific computational fluid dynamics market was valued at USD 870.65 million in 2025 and is anticipated to reach a valuation USD 964.24 million in 2026 and 2182.41 million by 2034, growing at a CAGR of 10.75%, from 2026 to 2034.

Computational Fluid Dynamics (CFD) is a branch of fluid mechanics that utilizes numerical algorithms and computational models to simulate, analyze, and predict fluid flow behavior. In the Asia Pacific region, CFD has become an indispensable tool across a wide range of industries, including aerospace, automotive, energy, marine, and environmental engineering. The technology enables engineers to optimize designs, improve efficiency, and reduce development costs by simulating real-world conditions without the need for extensive physical prototyping.

The Asia Pacific computational fluid dynamics market has gained significant traction due to rapid industrialization, increasing R&D investments, and growing demand for advanced simulation tools in manufacturing and infrastructure sectors. Countries such as China, Japan, South Korea, and India are leading the adoption curve, supported by government-backed initiatives promoting digital transformation in engineering and design processes.

Apart from these, the rise of smart cities and sustainable infrastructure projects has further reinforced the application of CFD in optimizing ventilation systems, managing urban heat islands, and improving building aerodynamics.

MARKET DRIVERS

Expansion of the Automotive Industry and Demand for Fuel-Efficient Vehicles

The rapid expansion of the automotive industry, particularly in countries like China, India, and South Korea is a major driver of the primary drivers of the Asia Pacific computational fluid dynamics market. These nations collectively account for a substantial share of global vehicle production, with rising consumer demand for fuel-efficient and environmentally friendly automobiles.

Automotive manufacturers increasingly rely on CFD simulations to enhance aerodynamic performance, reduce drag coefficients, and improve thermal management within engines and cooling systems. Furthermore, the emergence of autonomous and electric vehicles has intensified the need for precise thermal modeling to ensure optimal performance under diverse climatic conditions.

Growth of Renewable Energy Projects and Infrastructure Modernization

The surge in renewable energy installations across the Asia Pacific region has significantly boosted the demand for computational fluid dynamics solutions, particularly in wind and solar energy applications. Governments in countries like Australia, Japan, and Vietnam are aggressively investing in clean energy infrastructure to meet climate commitments and reduce dependence on fossil fuels.

In wind energy, CFD plays a crucial role in optimizing turbine blade design, predicting wind farm layout efficiency, and analyzing site-specific atmospheric conditions. Chinese energy firms, such as Goldwind and Envision Energy, have deployed advanced CFD simulations to maximize energy capture and reduce maintenance costs. Similarly, in Japan, where land constraints necessitate offshore wind developments, CFD is used extensively to model oceanic turbulence and structural resilience against typhoons.

Further, the modernization of urban infrastructure, including the construction of high-rise buildings and large-scale ventilation systems, has increased the use of CFD in architectural and civil engineering domains. This widespread application is expanding its role in the Asia Pacific’s technological landscape.

MARKET RESTRAINTS

High Cost of Advanced Simulation Software and Skilled Labor Shortage

The high cost associated with advanced simulation software and the scarcity of skilled professionals trained in CFD analysis are major restraints limiting the broader adoption of computational fluid dynamics in the Asia Pacific. Leading CFD platforms, such as ANSYS Fluent, Siemens STAR-CCM+, and COMSOL Multiphysics, require significant capital investment for licensing, hardware compatibility, and ongoing maintenance.

Moreover, the technical complexity of CFD modeling demands specialized expertise in mathematics, physics, and computer science—skills that are currently in short supply across many APAC countries. In markets like Indonesia and the Philippines, where engineering education programs lag behind international standards, the shortage of qualified personnel further hampers the effective deployment of CFD technologies.

In addition, smaller firms often lack the resources to build in-house CFD capabilities. This disparity creates an uneven playing field and restricts the penetration of CFD solutions beyond large-scale industrial applications.

Complexity in Integration with Existing Engineering Workflows

The difficulty in integrating CFD tools with existing engineering workflows and legacy systems is another significant challenge impeding the growth of the Asia Pacific computational fluid dynamics market. Many traditional manufacturing and design firms still rely on conventional methods such as physical testing and manual calculations, which do not seamlessly align with data-intensive simulation processes.

Integration issues are particularly pronounced in older industrial sectors such as shipbuilding and heavy machinery, where legacy CAD and PLM systems may not support modern CFD interfaces. As a result, companies face delays in data transfer, inconsistent results between simulation and real-world testing, and increased time-to-market for new products.

Moreover, resistance to change among engineering teams accustomed to traditional methodologies poses another barrier.

MARKET OPPORTUNITY

Increasing Adoption of AI and Machine Learning in CFD Simulations

The convergence of CFD with artificial intelligence (AI) and machine learning (ML) technologies presents a promising opportunity for the Asia Pacific computational fluid dynamics market. These advancements enable faster, more accurate simulations by leveraging predictive analytics and adaptive modeling techniques, reducing computational costs and accelerating decision-making in complex engineering environments.

Japanese and South Korean tech firms have been at the forefront of integrating AI with CFD, particularly in aerospace and automotive applications. Companies like Mitsubishi Heavy Industries and Hyundai have begun using deep learning algorithms to refine aerodynamic models and optimize real-time performance parameters. Similarly, in China, Baidu and Huawei are developing AI-powered cloud-based CFD platforms that allow engineers to run high-fidelity simulations remotely without requiring expensive local hardware.

Universities and research institutions across the region are also contributing to this trend. The National University of Singapore launched a joint initiative with NVIDIA to explore neural network-based turbulence modeling, which could drastically reduce the time required for complex fluid flow predictions.

Government Support for Digital Twin Technologies in Smart Manufacturing

The push toward digital twin technologies in smart manufacturing presents a major growth avenue for the Asia Pacific computational fluid dynamics market. Digital twins—virtual replicas of physical assets—are increasingly being used to monitor, simulate, and optimize industrial processes in real time. Given that CFD forms a core component of fluid-related digital twin models, its adoption is gaining momentum in sectors such as energy, aerospace, and semiconductor fabrication.

Governments in countries like India, Malaysia, and Thailand have launched national initiatives to promote Industry 4.0 adoption, offering subsidies and tax incentives for companies investing in simulation-based digital twins.

In South Korea, the Ministry of Trade, Industry, and Energy has mandated the inclusion of digital twin capabilities in new industrial parks, encouraging firms to adopt CFD-integrated virtual models for equipment performance monitoring and failure prediction. Besides, Japanese conglomerates such as Hitachi and Toshiba are deploying CFD-enabled digital twins in nuclear power plants and HVAC systems to enhance safety and efficiency.

MARKET CHALLENGES

Data Management and Storage Complexity in Large-Scale CFD Simulations

The increasing complexity of data management and storage associated with large-scale simulations is one of the foremost challenges facing the Asia Pacific computational fluid dynamics market. As CFD models become more detailed and realistic, they generate vast datasets that require high-performance computing (HPC) resources, efficient data handling protocols, and scalable storage solutions.

In emerging markets such as Vietnam and the Philippines, many engineering firms struggle with inadequate data center infrastructure and limited access to cloud-based HPC services, hindering their ability to conduct complex simulations efficiently. Even in developed economies like Japan and Australia, the exponential growth in simulation data has led to concerns about long-term data retention, version control, and interoperability across different software platforms.

Regulatory and Standardization Gaps in Simulation-Based Certification Processes

The lack of standardized regulatory frameworks for simulation-based certification in critical industries such as aviation, healthcare, and pharmaceuticals is a persistent challenge in the Asia Pacific computational fluid dynamics market. Unlike traditional physical testing, which follows well-established validation procedures, the acceptance of CFD-generated data for regulatory approval varies significantly across countries in the region.

For instance, while Japan and South Korea have started incorporating CFD into aircraft design certifications under guidelines issued by the Civil Aviation Bureau of Japan and the Korea Office of Aviation Safety, similar policies are either absent or inconsistently applied in countries like Indonesia and Thailand.

Similarly, in the pharmaceutical sector, regulatory authorities in India and China are still in the early stages of defining how CFD-derived insights can be used for drug formulation and bioreactor design validation. The absence of harmonized standards makes it difficult for companies to justify simulation-based decisions to regulators, limiting the adoption of CFD in regulated fields.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.75% |

| Segments Covered | By Deployment Model, End-User, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Ansys Inc., Siemens Digital Industries Software (Simcenter STAR-CCM+), Dassault Systèmes (SIMULIA/PowerFLOW), Hexagon AB (MSC Software), Altair Engineering (AcuSolve & ultraFluidX), Autodesk Inc., NUMECA International (now part of Cadence Design Systems), Toshiba Energy Systems & Solutions Corporation, Nihon Unisys Limited (Japan), CD-adapco (part of Siemens, but historically influential in APAC). |

SEGMENTAL ANALYSIS

By Deployment Model Insights

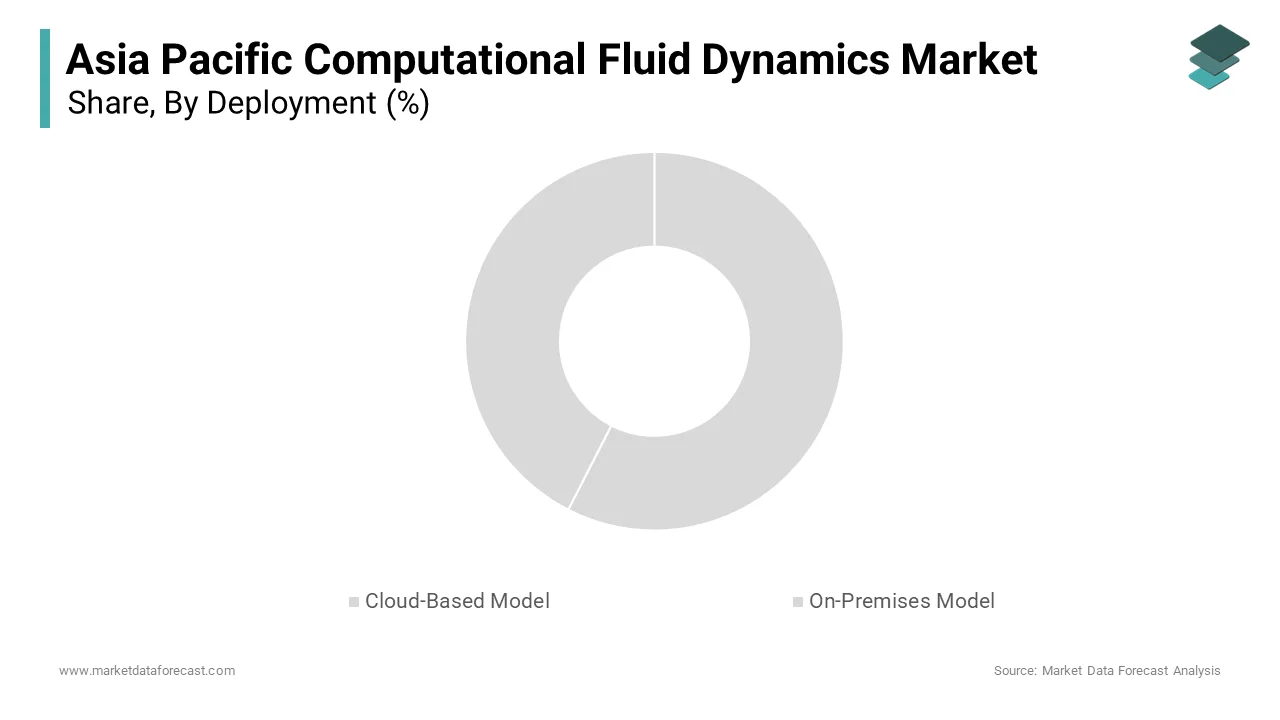

On-Premises Deployment

The on-premises deployment model segment dominated the Asia Pacific computational fluid dynamics market by capturing 57.3% of the total share in 2024. This segment’s dominance is primarily attributed to its widespread adoption among large-scale industrial enterprises and research institutions, which require high-performance computing capabilities and stringent data security controls is primarily attributed This dominance of the on-premises deployment model segment.

In countries like Japan and South Korea, where aerospace, automotive, and semiconductor manufacturing industries are highly advanced, organizations prefer on-premises CFD solutions due to their ability to handle complex simulations with minimal latency.

Similarly, in China, government-backed defense and energy projects mandate the use of localized infrastructure to safeguard sensitive design information.

Apart from these, legacy engineering firms across India and Australia continue to operate on traditional IT infrastructures, further reinforcing the preference for on-site CFD deployments despite the growing availability of cloud-based alternatives.

Cloud-Based Deployment

The cloud-based deployment model segment is emerging as the fastest-growing segment in the Asia Pacific computational fluid dynamics market and is projected to expand at a CAGR of 13.4% from 2025 to 2033. Increasing demand for scalable, cost-effective, and accessible simulation tools among small and medium-sized enterprises (SMEs), startups, and academic institutions is driving the rapid growth of the cloud-based deployment model segment.

In India, the proliferation of digital engineering platforms and government initiatives such as "Make in India" has encouraged SMEs to adopt cloud-based CFD solutions without significant upfront investment in hardware or software licenses.

South Korea has also witnessed strong momentum in this segment, particularly within the electric vehicle and renewable energy sectors.

Moreover, multinational software vendors such as ANSYS and Siemens have expanded their cloud offerings in the APAC region, providing pay-per-use models that lower entry barriers for budget-constrained users.

By End User Insights

Automotive Industry

The automotive sector commanded the Asia Pacific computational fluid dynamics market by accounting for 34.3% of total revenue in 2024. Extensive application of CFD in aerodynamic design optimization, engine cooling, fuel efficiency enhancement, and noise reduction across vehicle platforms is propelling the growth of the automotive sector. Countries like China, India, and Japan, which are global leaders in automotive production, have increasingly adopted CFD to accelerate product development cycles and meet evolving emission standards. Japanese automakers, including Toyota and Honda, have been pioneers in integrating CFD into virtual wind tunnel testing, reducing reliance on physical prototypes and shortening time-to-market. Furthermore, the shift toward autonomous and connected mobility has intensified the need for precise airflow modeling around sensors and onboard electronics.

Energy Sector

The energy end-user segment is experiencing the most rapid expansion in the Asia Pacific computational fluid dynamics market and is anticipated to grow at a CAGR of 14.1% between 2025 and 2033. Rising investments in renewable energy infrastructure, particularly in wind, solar, and hydrogen technologies, where fluid dynamics play a crucial role in performance optimization, are largely fuelling the surge of other energy end-user segments.

Chinese turbine manufacturers like Goldwind and Ming Yang Smart Energy extensively use CFD to simulate wind flow patterns, blade efficiency, and offshore turbulence conditions to maximize energy output and reduce maintenance costs.

Australia has also seen a notable uptick in CFD adoption for hydrogen storage and pipeline transport modeling, as the country positions itself as a future clean energy exporter. The Australian Renewable Energy Agency supported multiple research initiatives in 2023 focused on optimizing hydrogen liquefaction using CFD simulations.

Further, in Southeast Asia, nations like Vietnam and Indonesia are leveraging CFD for hydroelectric dam design and geothermal heat extraction processes.

REGIONAL ANALYSIS

China Computational Fluid Dynamics Market Analysis

China spearheaded the Asia Pacific computational fluid dynamics market by contributing 30.5% of total revenue in 2024. As a global manufacturing powerhouse, China's aerospace, automotive, and renewable energy sectors heavily rely on CFD for design validation and performance optimization. The Chinese Ministry of Science and Technology has prioritized simulation-based engineering under its Made in China 2025 initiative, allocating substantial funding for domestic CFD software development and high-performance computing infrastructure.

The country's expanding defense and space programs have further driven demand for sophisticated fluid dynamics modeling, particularly in missile aerodynamics and hypersonic flight simulations. Moreover, the rapid growth of the electric vehicle industry, coupled with stringent emission regulations, has prompted automakers to invest heavily in CFD-based thermal management solutions.

Japan Computational Fluid Dynamics Market Analysis

Japan is maintaining a strong position due to its leadership in high-precision engineering and aerospace innovation. Japanese firms have long embraced simulation technologies to enhance product development cycles, particularly in automotive, robotics, and semiconductor manufacturing. The Japan Aerospace Exploration Agency has been a key proponent of CFD in aircraft design, utilizing advanced turbulence modeling to improve fuel efficiency and structural integrity.

Automotive giants like Nissan and Subaru leverage CFD extensively in virtual wind tunnel testing, allowing them to optimize vehicle aerodynamics without costly physical trials.

Beyond mobility, Japan’s nuclear and thermal power plants employ CFD for reactor cooling system analysis and emergency ventilation planning. The Ministry of Economy, Trade, and Industry has promoted the integration of AI-enhanced CFD tools to support predictive maintenance and safety assessments.

India Computational Fluid Dynamics Market Analysis

India is seeing rapid adoption of the Asia Pacific computational fluid dynamics market, which is driven by a growing ecosystem of engineering startups, academic research centers, and government-backed digital manufacturing initiatives. The country’s rapidly expanding automotive and renewable energy sectors have spurred demand for cost-effective simulation tools that can streamline design and prototyping.

The Indian government’s Make in India and Digital India campaigns have played a pivotal role in promoting simulation-based engineering education. Besides, the Department of Science and Technology funded several national-level CFD research labs focusing on urban air quality modeling and sustainable infrastructure development.

Indian startups specializing in drone technology, electric propulsion, and smart agriculture have increasingly adopted open-source and cloud-based CFD tools to prototype fluid-related applications. The Bangalore-based startup ecosystem, in particular, has emerged as a hub for simulation-driven innovation, attracting both domestic and international investors.

South Korea Computational Fluid Dynamics Market Analysis

South Korea contributes significantly to the Asia Pacific computational fluid dynamics market, with a strong focus on semiconductor fabrication, aerospace engineering, and smart manufacturing. The country’s heavy reliance on precision manufacturing has made CFD an essential tool for optimizing cleanroom airflow, thermal dissipation in microchips, and satellite re-entry aerodynamics.

Leading conglomerates such as Samsung Electronics and Hyundai Heavy Industries have integrated CFD into their design pipelines to enhance process efficiency and reduce failure risks.

The Korean government has also been proactive in supporting simulation-driven innovation through initiatives like the Smart Manufacturing Innovation Strategy, which encourages the use of digital twins and AI-integrated CFD platforms. Universities such as KAIST and POSTECH are actively involved in developing next-generation CFD algorithms tailored for semiconductor and aerospace applications.

Australia Computational Fluid Dynamics Market Analysis

Australia is distinguished by its strong application in energy, environmental science, and marine engineering. The country’s abundant natural resources and commitment to climate resilience have led to increased reliance on CFD for modeling atmospheric flows, ocean currents, and carbon capture mechanisms.

Australian universities and research bodies, including the Commonwealth Scientific and Industrial Research Organisation (CSIRO), have pioneered the use of CFD in studying bushfire behavior and urban heat island effects.

In the energy sector, CFD plays a vital role in optimizing gas pipelines, LNG terminal designs, and hydrogen storage tanks. The Australian Renewable Energy Agency has funded several studies exploring wind farm layout optimization using advanced fluid dynamics simulations.

Government agencies and private firms alike recognize the strategic value of CFD in addressing environmental challenges, positioning Australia as a key player in niche CFD applications across the APAC region.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific computational fluid dynamics market is marked by a convergence of global software vendors and regional innovators striving to meet the evolving demands of engineering and scientific communities. Established players leverage their technological expertise and vast customer base to maintain dominance, while emerging firms focus on niche applications, affordability, and ease of use to carve out competitive positions. The market is witnessing intensified rivalry as companies race to integrate artificial intelligence, machine learning, and cloud computing into their CFD offerings, aiming to provide faster, more intuitive simulation experiences. Strategic collaborations with academic institutions, government agencies, and industry consortia have become essential for driving adoption and ensuring long-term relevance. Apart from these, vendors are increasingly emphasizing user-friendly interfaces, modular licensing models, and vertical-specific solutions to cater to the diverse needs of sectors ranging from automotive and aerospace to energy and environmental sciences. As demand for precision modeling expands across the region, only those firms that continuously innovate and adapt to local requirements will sustain leadership in this dynamic and rapidly growing market.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific computational fluid dynamics market.

- Ansys Inc.

- Siemens Digital Industries Software (Simcenter STAR-CCM+)

- Dassault Systèmes (SIMULIA/PowerFLOW)

- Hexagon AB (MSC Software)

- Altair Engineering (AcuSolve & ultraFluidX)

- Autodesk Inc.

- NUMECA International

- Toshiba Energy Systems & Solutions Corporation

- Nihon Unisys Limited (Japan)

- CD-adapco

Top Players In The Market

- One of the leading players in the Asia Pacific computational fluid dynamics market is ANSYS Inc. The company has a strong presence across major APAC countries, offering advanced simulation tools widely used in aerospace, automotive, and electronics sectors. ANSYS’s CFD solutions are known for their high accuracy and integration with AI-driven analytics, enabling engineers to optimize complex fluid flow problems efficiently. Its partnerships with academic institutions and industry leaders have helped drive innovation and expand adoption in emerging markets.

- Siemens Digital Industries Software is another key player shaping the regional CFD landscape. With its STAR-CCM+ platform, Siemens provides end-to-end simulation capabilities that support product design, energy optimization, and process engineering. In the Asia Pacific, Siemens collaborates closely with manufacturing hubs to enhance digital twin applications, fostering seamless integration of CFD into industrial workflows. Its commitment to smart manufacturing and Industry 4.0 initiatives further strengthens its foothold in the region.

- Dassault Systèmes, through its SIMULIA brand, plays a pivotal role in advancing CFD technologies across diverse industries in the Asia Pacific. Known for its robust simulation environment, Dassault offers scalable solutions tailored for both large enterprises and SMEs. The company actively engages with research organizations and government-backed projects to promote simulation literacy and support sustainable engineering practices across the region.

Top Strategies Used By Key Market Participants

- A primary strategy adopted by key players in the Asia Pacific computational fluid dynamics market is deepening integration with cloud-based platforms. Major vendors are shifting toward scalable, on-demand computing environments that allow users to run high-fidelity simulations without heavy upfront infrastructure investments. This approach supports broader accessibility, especially among startups and academic institutions.

- Another crucial strategy is collaborating with educational and research institutions. Companies are investing in training programs, simulation labs, and joint R&D initiatives to build a skilled workforce and foster early adoption of CFD tools among engineering students and researchers across the region.

- Lastly, expanding localized support and customization services has become a key differentiator. Vendors are tailoring their software interfaces, technical support, and application-specific modules to align with regional industry needs, regulatory standards, and language preferences, thereby enhancing user experience and market penetration.

RECENT MARKET NEWS

- In April 2024, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen its market presence.

- In March 2024, ANSYS launched a new regional innovation hub in Singapore focused on supporting CFD research and development for Southeast Asian industries. The initiative aimed at accelerating technology adoption among local manufacturers and academic institutions.

- In February 2024, Siemens expanded its partnership with a leading Japanese university to co-develop next-generation CFD algorithms tailored for semiconductor cooling applications, reinforcing its presence in high-tech manufacturing segments.

- In January 2024, Dassault Systèmes introduced an industry-specific CFD training program in India in collaboration with several technical universities, targeting enhanced skill development and wider software adoption in engineering education.

- In May 2024, a prominent South Korean simulation software firm partnered with a global cloud service provider to launch a dedicated CFD-as-a-Service platform, making high-performance fluid dynamics modeling more accessible to SMEs across the region.

MARKET SEGMENTATION

This research report on the Asia Pacific Computational fluid dynamics market is segmented and sub-segmented into the following categories.

By Deployment

- Cloud-Based Model

- On-Premises Model

By End User

- Automotive

- Aerospace and Defense

- Electrical and Electronics

- Industrial Machinery

- Energy

- Material and Chemical Processing

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is the Asia Pacific computational fluid dynamics market?

It refers to the use and demand for CFD software and services — tools that simulate fluid flow, heat transfer, and related physical phenomena — across industries in the Asia Pacific region.

What drives growth in the Asia Pacific computational fluid dynamics market?

Demand is rising due to increased engineering simulation needs, growth in automotive and aerospace sectors, renewable energy projects, and the push for digital design optimization in manufacturing.

Which industries commonly use computational fluid dynamics in Asia Pacific?

Automotive, aerospace & defense, energy & power generation, chemical processing, electronics cooling, and HVAC (heating, ventilation, and air-conditioning) sectors rely heavily on CFD.

Why is CFD important for automotive engineering?

CFD helps engineers optimize aerodynamics, improve fuel efficiency, study thermal management, and reduce drag — enabling better vehicle performance with fewer physical prototypes.

How does CFD support the aerospace industry in Asia Pacific?

CFD enables aircraft designers to simulate airflow, reduce structural weight, improve fuel efficiency, and ensure safety under different flight conditions without costly wind-tunnel testing at early stages.

What factors challenge the Asia Pacific computational fluid dynamics market?

High software costs, shortage of specialized simulation talent, complex integration with legacy systems, and varying digital maturity levels across regional industries.

How is digital transformation shaping the Asia Pacific computational fluid dynamics market?

Industry 4.0 adoption, cloud-based simulation platforms, high-performance computing (HPC), and AI-assisted model optimization are accelerating CFD uptake among mid-to-large enterprises.

Are small and medium enterprises (SMEs) adopting CFD tools in Asia Pacific?

Yes — as CFD tools become more accessible and cloud-enabled, SMEs in sectors like consumer electronics, building services, and smaller manufacturers are increasingly using simulations.

Which countries are leading the Asia Pacific CFD market?

China, Japan, South Korea, India, and Australia are among the front-runners due to strong industrial bases, rapid innovation cycles, and significant R&D investments.

What is the future outlook for the Asia Pacific computational fluid dynamics market?

The market is expected to grow steadily as adoption spreads across industries, high-performance computing becomes more affordable, and engineering teams increasingly rely on digital simulations to reduce product development time and cost.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com