Asia Pacific Customized Premix Market By Nutrient (Vitamins, Minerals, Amino Acids, Nutraceuticals And Nucleotides), Form (Powder And Liquid), By Application (Beverages, Dairy Products, Cereals, Bakery & Confectionery, Nutritional Products And Dietary Supplements), Functionality (Bone Health, Skin Health, Energy, Immunity And Digestion), And By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Market Size, 2025

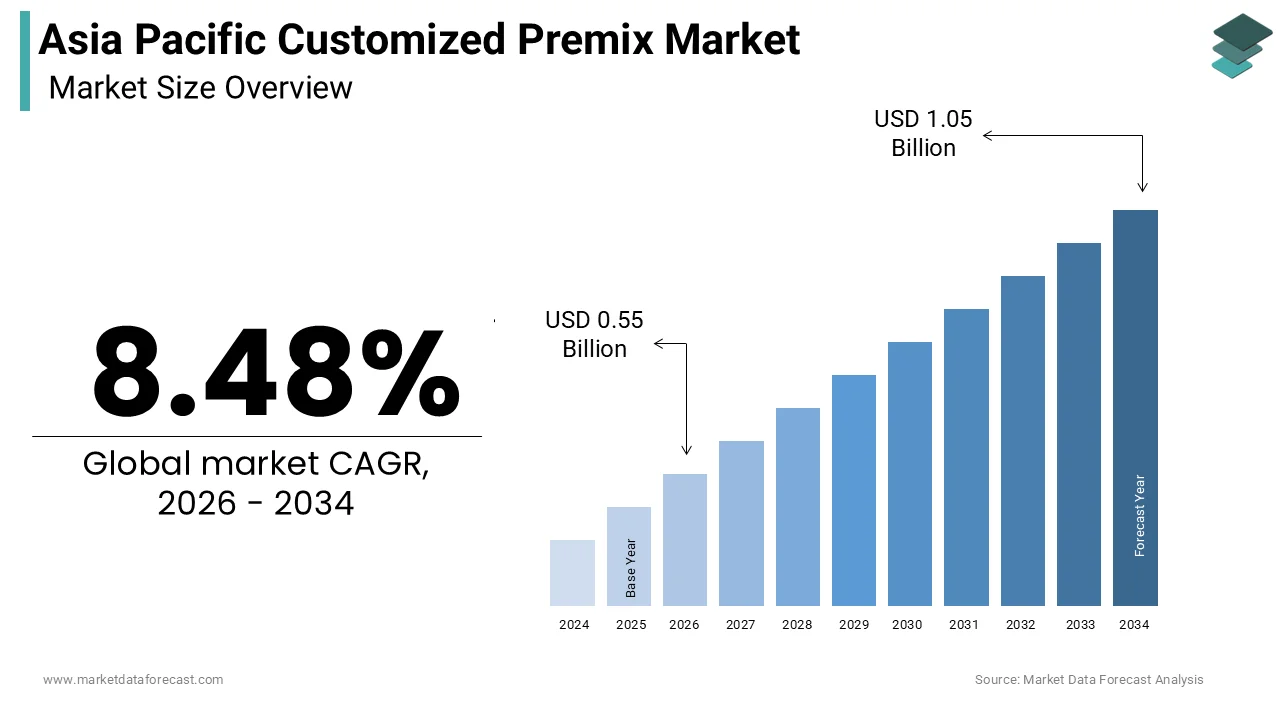

$0.51 BnMarket Estimate, 2026

$0.55 BnMarket Forecast, 2034

$1.05 BnCAGR, 2026–2034

8.48%Asia Pacific Customized Premixes Market Size

The Asia Pacific Customized Premixes Market size was calculated to be USD 0.51 billion in 2025 and is anticipated to be worth USD 1.05 billion by 2034, from USD 0.55 billion in 2026, growing at a CAGR of 8.48% during the forecast period.

Market Drivers and Restraints

Significant factors which have helped drive the Asia Pacific Customized Premix Market forward are Addition of necessary ingredients such as minerals, amino acids, vitamins, and nucleotides.

Demand for advanced premix products from the food industry is projected to rise as several companies involved in the production of customized blends of vitamin and mineral premixes, which are used in many food applications, such as dietary supplements, nutritional products for infants and athletes, and clinical nutrition

The operational efficiency in the manufacture of these premixes such as decreased inventory of products, reduced cost of quality control, less complexity of the supply chain and shorter lead time leads to cost reductions result in a fall in the price of customized premixes

The factors holding the Asia Pacific Customized Premix Market back include

The false claims made by the few producers about the components of the item and its applications may distract customers, which may restrict the development of the Asia Pacific market for customized premixes.

Research Methodology

The research done takes place in two phases namely-

Secondary Research: The first phase of the research process is an extensive secondary research and identification of the related intelligence. Secondary data is compiled from various sources. An extensive secondary research helps in generating hypothesis and identifying critical areas of interest that are investigated through primary research.

Primary Research: This entails conducting hundreds of primary interviews with industry participants and commentators in order to validate the data points obtained from secondary research and to fill the data gaps. A primary interview provides first-hand information on the market size, market trends, growth trends, competitive landscape, future outlook etc. It also helps in deciding the scope and deliverables of the study in terms of the requirement of the market. Primary research involves E-mail interactions, telephonic interviews as well as face-to-face interviews for each market, category, segment and sub-segment across geographies.

Asia Pacific Customized Premix Market Segmentation Analysis

By Nutrient

- Vitamins

- Minerals

- Amino Acids

- Nutraceuticals

- Nucleotides

By Form

- Powder

- Liquid

By Application

- Beverages

- Dairy Products

- Cereals

- Bakery & Confectionery

- Nutritional Products

- Dietary Supplements

By Functionality

- Bone Health

- Skin Health

- Energy

- Immunity

- Digestion

By Region

- China

- India

- Japan

- South Korea

- Australia

The vitamins category has the highest market value and is expected to continue to have a significantly higher CAGR over the forecast period. The Food & Beverages segment is projected to continue to dominate the market in terms of usage.

The tailored premixed beverage segment is the biggest and fastest-growing segment on this market, followed by bakery & pastry and nutritional items. The dominance of this implementation can be ascribed to the growing demand for drinks such as sports drinks, power drinks, fruit juices, vitamin water, herbal drinks, isotonic drinks and other non-carbonated drinks

APAC Customized Premix Market Geographical Analysis

Geographically the market is segmented into China, India, Japan, South Korea, and Australia. China and Japan are the dominant markets in this region and estimated to witness high growth in the forecast period.

Key Players in the Market

Major Key Players in the Asia Pacific Customized Premix Industry are

- Prinova Group LLC

- SternVitamin GmbH & Co. KG

- Koninklijke DSM N.V

- Jubilant Life Sciences

- Archer Daniels Midland Company

- Fenchem

- Glanbia plc

- B&H Biotechnology Co. Ltd

- Barentz,

- Farbest Brands

- Lycored

- Hexagon Nutrition

- Archer Daniels Midland Company

- WATSON-INC

Research Report Key Highlights

- Current and future market perspectives for Asia Pacific Customized Premixes Market in developed and emerging markets.

- Analyse different market perspectives using the analysis of five Porter forces

- The segment that is expected to dominate the market.

- Regions that are expected to grow faster during the forecast period.

- Identify the latest developments, market shares, and strategies of key market participants.

Frequently Asked Questions

1. What factors are driving the growth of the APAC customized premix market?

The market is driven by increasing demand for fortified foods and beverages, rising health awareness, growing dietary supplement consumption, expanding infant nutrition, and the trend toward personalized nutrition.

2. What ingredients are commonly used in customized premixes?

Common ingredients include vitamins, minerals, amino acids, probiotics, prebiotics, fibers, botanical extracts, nucleotides, enzymes, and specialty functional ingredients.

3. Which end-use industry holds the largest market share?

The food and beverage industry holds the largest market share due to the growing demand for fortified, functional, and convenience food products.

4. Why is demand for customized premixes increasing in Asia-Pacific?

Growing health consciousness, rising disposable incomes, expanding food processing industries, increasing consumption of dietary supplements, and demand for personalized nutrition are fueling market growth.

5. What applications commonly use customized premixes?

Customized premixes are widely used in dairy products, beverages, bakery products, cereals, infant formula, sports nutrition, meal replacements, dietary supplements, and functional foods.

6. What are the major challenges facing the APAC customized premix market?

Challenges include fluctuating raw material prices, regulatory compliance, ingredient stability, quality assurance, and supply chain disruptions.

7. How is technology influencing the customized premix market?

Technological advancements in precision nutrition, automated blending, microencapsulation, and quality control are improving product performance, consistency, and shelf life.

8. What opportunities exist in the APAC customized premix market?

Growth opportunities include functional foods, personalized nutrition, sports nutrition, healthy aging products, immune-support formulations, and plant-based food and beverage applications.

9. Who are the major customers in the customized premix market?

Major customers include food manufacturers, beverage companies, dietary supplement brands, pharmaceutical companies, infant nutrition manufacturers, contract manufacturers, and animal feed producers.

10. What is the future outlook for the APAC customized premix market?

The APAC customized premix market is expected to witness strong growth during the forecast period, driven by rising demand for personalized nutrition, expanding functional food and beverage industries, technological innovations, and increasing consumer focus on health and wellness.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com