Asia Pacific Feed Enzymes Market Size, Share, Trends And Growth Forecast Research Report, Segmented By Type Of Ingredient, Type Of Animals, And By Region (India, China, Japan, South Korea, Australia, New Zealand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC), Industry Analysis From 2025 to 2033.

Asia Pacific Feed Enzymes Market Size

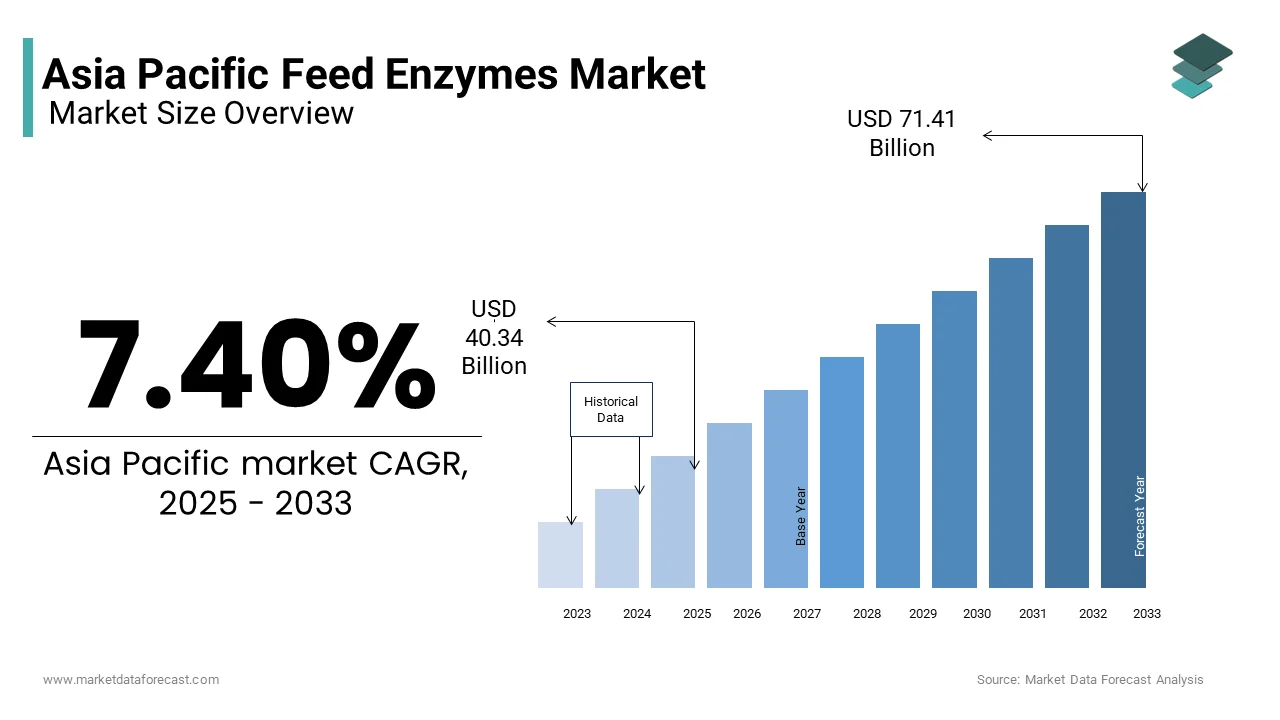

The Asia-Pacific feed enzymes market was valued at USD 37.56 billion in 2024 and is anticipated to reach USD 40.34 billion in 2025 from USD 71.41 billion by 2033, growing at a CAGR of 7.40% during the forecast period from 2025 to 2033.

Feed enzyme refers to specialized proteins, primarily phytase, protease, xylanase, and amylase, added to animal feed to enhance nutrient digestibility, improve feed conversion ratios, and reduce environmental impact. These enzymes are critical in monogastric diets, particularly for poultry and swine, where they break down anti-nutritional factors in plant-based feedstuffs such as corn, soybean meal, and wheat. The region accounts for over 60% of global poultry production and nearly 55% of swine output, driving substantial demand for efficient, cost-effective feeding strategies. With rising pressure to reduce reliance on imported feed ingredients and minimize phosphorus runoff from livestock waste, enzyme use has become integral to sustainable animal production across the region.

MARKET DRIVERS

Expansion of Industrialized Livestock Production in Emerging Economies

The rapid growth of large-scale, intensive poultry and swine farming in countries like Vietnam, India, and Indonesia is a primary catalyst for feed enzyme adoption. As urbanization and rising incomes increase demand for animal protein, commercial producers are prioritizing feed efficiency to maximize output and profitability. These operations rely heavily on enzyme supplementation to extract maximum energy from locally sourced cereals and by-products. Similarly, India’s poultry sector, which produces over 5 million metric tons of broiler meat annually, has seen a year-on-year increase in enzyme use since 2020. The shift from backyard to commercial farming models necessitates standardized, high-performance feed formulations, where enzymes play a critical role in improving digestibility and reducing feed waste, directly supporting productivity gains.

Regulatory Pressure to Reduce Phosphorus Discharge from Livestock Operations

Stringent environmental regulations targeting nutrient pollution from animal agriculture are accelerating the adoption of phytase, the most widely used feed enzyme in the region. In China, the Ministry of Ecology and Environment has imposed limits on phosphorus discharge from livestock farms, mandating reductions in manure runoff to combat eutrophication in waterways such as the Yangtze and Pearl River basins. As per the Chinese Academy of Agricultural Sciences, unutilized phosphorus in conventional swine diets can exceed 60%, contributing significantly to soil and water contamination. Phytase supplementation increases phosphorus availability by up to 50%, reducing the need for inorganic phosphate additives and lowering excretion. In Thailand, the Department of Livestock Development requires large poultry farms to implement nutrient management plans, incentivizing enzyme use. These regulatory frameworks are transforming phytase from a performance additive into an environmental compliance tool.

MARKET RESTRAINTS

High Cost and Price Volatility of Specialty Enzymes in Smallholder Systems

The relatively high cost of advanced feed enzymes, particularly protease and multi-enzyme complexes, limits their adoption among small-scale and independent livestock producers across the Asia Pacific. For many farmers in Cambodia, Myanmar, and eastern India, feed represents over 70% of total production costs, leaving little room for premium additives. While phytase is increasingly common, more specialized enzymes can increase feed formulation costs. Additionally, global supply chain disruptions and fluctuations in fermentation feedstock prices, such as corn steep liquor and molasses, have led to enzyme price volatility, discouraging long-term procurement commitments. This economic barrier hinders widespread penetration, particularly in fragmented, price-sensitive markets.

Limited Awareness and Technical Expertise Among Regional Feed Mill Operators

A significant barrier to market expansion is the lack of technical knowledge regarding enzyme selection, dosage, and feed matrix interactions among regional feed manufacturers and farm advisors. In many parts of Southeast Asia, feed formulations are still based on traditional practices rather than precision nutrition, leading to suboptimal enzyme utilization. Misapplication, such as using xylanase in corn-soy diets with low arabinoxylan content, reduces efficacy and undermines confidence in enzyme technology. Furthermore, inconsistent quality control in local enzyme products exacerbates skepticism. Without standardized training and access to technical support from enzyme suppliers, many producers remain hesitant to integrate enzymes into their feeding programs, constraining market growth despite proven benefits.

MARKET OPPORTUNITY

Rising Demand for Alternative Protein Sources and By-Product Utilization

The increasing use of non-conventional and locally available feed ingredients, such as rice bran, cassava, and distillers’ dried grains with solubles (DDGS), is creating strong demand for tailored enzyme solutions. Moreover, over 25 million tons of rice bran are produced annually in the region, much of which remains underutilized due to poor digestibility. Also, India’s expanding ethanol industry is generating large volumes of DDGS, which require protease and phytase for optimal inclusion in poultry diets. By enabling the efficient use of low-cost, region-specific feedstuffs, enzymes support feed independence, reduce import reliance, and enhance sustainability, opening a strategic growth avenue for enzyme manufacturers.

Integration of Enzymes into Antibiotic-Free and Clean-Label Production Systems

The growing shift toward antibiotic-free (ABF) animal production in response to antimicrobial resistance (AMR) concerns is increasing reliance on feed enzymes as a gut health management tool. In Japan and South Korea, where regulatory restrictions on growth-promoting antibiotics are stringent, producers use enzyme-supplemented diets to maintain growth performance and reduce intestinal disorders. AMR-related deaths in Asia could reach 4.7 million annually by 2050 if current practices continue, prompting policy action. Enzymes such as protease and xylanase reduce undigested protein and fermentable carbohydrates in the hindgut, minimizing substrates for pathogenic bacteria like Clostridium and E. coli. Similarly, major retailers in China and Singapore are demanding clean-label meat, driving integrators to adopt enzyme-based feeding strategies that support health without antibiotics.

MARKET CHALLENGES

Variability in Raw Material Composition and Enzyme Efficacy

One of the most persistent technical challenges in the Asia Pacific feed enzyme market is the inconsistency in feedstock composition, which affects enzyme performance and dosing accuracy. Regional feed ingredients such as palm kernel meal, rice bran, and cassava exhibit high variability in fiber, protein, and moisture content depending on origin, season, and processing method. This variability complicates formulation standardization, especially for small feed mills lacking analytical capabilities. Inconsistent enzyme response undermines producer confidence and leads to under- or over-dosing, reducing cost-effectiveness. Unlike in Western markets with standardized ingredient databases, the Asia Pacific lacks comprehensive nutritional profiling systems, making it difficult to optimize enzyme use. This variability demands region-specific enzyme blends and on-site technical support, increasing complexity for suppliers.

Counterfeit and Substandard Enzyme Products in Unregulated Markets

The proliferation of low-quality and counterfeit enzyme products in unregulated or loosely monitored markets poses a significant challenge to legitimate manufacturers and end-user trust. In countries, unlicensed producers sell diluted or inactive enzyme formulations at lower prices, often without proper stability testing or activity guarantees. These substandard products deliver no nutritional benefit, leading farmers to perceive all enzymes as ineffective. The absence of mandatory enzyme labeling and third-party certification in many jurisdictions enables this informal market to thrive. Reputable companies face reputational damage and reduced adoption rates due to these imitations. Combating this issue requires stronger regulatory enforcement, traceability systems, and farmer education initiatives that are progressing slowly across the region, hindering market integrity and long-term growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.40% |

| Segments Covered | By Sub-Additive, Animal, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | DuPont, DSM, ASF Corporation, Alltech, Novozymes, Adisseo France, AB Enzymes GmbH, Advanced Enzymes Technologies Limited, Amano Enzyme Inc., Bio-Vet JSC, Biocatalysts Ltd, Chr. HansenInc.c, EnmeSAB de CVCv, Lesaffre Group, PURATOS GROUP, Rossari Biotech Limited, Shenzhen Leveking Bio-Engineering, Co., Ltd, Sunson Industry Group Company Limited |

SEGMENTAL ANALYSIS

By Sub-Additive Insights

The phytases segment commanded the largest market share, 45.3% in 2024. This dominance is due to the widespread reliance on plant-based feed ingredients such as soybean meal and corn, which are rich in phytic acid, a compound that binds phosphorus and renders it indigestible for monogastric animals like poultry and swine. Phytases break down phytic acid, releasing bioavailable phosphorus and reducing the need for inorganic phosphate supplements. This not only lowers feed costs but also curbs environmental phosphorus pollution. Like, over 70% of swine and poultry diets in Southeast Asia are based on cereal grains, amplifying the necessity for phytase supplementation. Additionally, regulatory tightening on phosphorus discharge in countries like China and Thailand has pushed feed manufacturers to adopt phytase-enriched formulations. Mandatory nutrient efficiency standards in China’s feed regulations have increased enzyme usage by 18% since 2020, further cementing phytase’s lead.

The carbohydrases segment is emerging as the fastest-growing segment and is projected to expand at a CAGR of 8.7% from 2025 to 2033. This accelerated growth is driven by the increasing inclusion of non-conventional, fibrous feedstuffs such as rice bran, wheat by-products, and cassava in animal diets across India, Vietnam, and Indonesia. These ingredients contain high levels of non-starch polysaccharides (NSPs), which impair nutrient absorption and increase digesta viscosity. Carbohydrases degrade these NSPs, enhancing feed efficiency and energy utilization. Moreover, the shift toward antibiotic-free poultry production, particularly in Japan and South Korea, has elevated the role of carbohydrases in maintaining gut health. With increasing investments in enzyme R&D by firms like Novozymes and Adisseo in APAC, innovation in thermostable and broad-spectrum carbohydrases is further accelerating adoption.

By Animal Insights

The Poultry segment stands as the prime consumer of feed enzymes in the Asia Pacific by capturing an estimated 42.2% share in 2024. The sector’s position is anchored in the region’s explosive growth in broiler and egg production, particularly in countries like China, India, and Indonesia. The intensification of poultry farming has led to a heavy reliance on formulated feeds rich in cereals and plant proteins, which inherently contain anti-nutritional factors such as phytate and arabinoxylans. Enzymes like phytase and xylanase are now standard in commercial poultry diets to maximize nutrient uptake and reduce feed costs. Moreover, the push for sustainable production has intensified enzyme adoption; phytase use in poultry feed reduces phosphorus excretion by up to 50%, according to a 2021 study by the Journal of Applied Poultry Research. This environmental benefit aligns with tightening regulations in countries like Thailand and Vietnam, where water pollution from poultry farms is a growing concern. Additionally, the rise of integrated poultry players such as Charoen Pokphand Foods and Venky’s has standardized high-efficiency feeding protocols, embedding enzyme use into mainstream production.

The aquaculture segment is the fastest-growing in the APAC feed enzyme market and is projected to grow at a CAGR of 9.3% from 2025 to 2033. This surge is fueled by the region’s dominance in global fish and shrimp farming. Asia produces over 90% of the world’s farmed seafood, according to the FAO’s State of World Fisheries and Aquaculture 2022. Species like tilapia, catfish, and whiteleg shrimp are increasingly fed plant-based diets to reduce dependency on fishmeal, but these diets contain high levels of indigestible carbohydrates and anti-nutritional factors. Enzymes such as proteases, phytases, and carbohydrases are critical in improving protein and mineral availability in such formulations. In Vietnam, the world’s second-largest shrimp exporter, enzyme use in aqua feed has risen since 2020, driven by disease outbreaks linked to poor digestion and gut health. Similarly, in India, the government’s Pradhan Mantri Matsya Sampada Yojana (PMMSY) aims to double fish production to 70 lakh metric tons by 2025, necessitating higher feed efficiency. With rising investments from companies like BioMar and Skretting in enzyme-enhanced aqua feeds, the sector’s enzyme uptake is poised for sustained acceleration.

COUNTRY-LEVEL ANALYSIS

China stood at the forefront of the Asia Pacific feed enzyme market by commanding an estimated 32.5% share in 2024. As the region’s largest livestock and aquaculture producer, China’s industrialized animal farming sector drives massive demand for feed additives. The country’s annual compound feed output is 321.6 million metric tons, the highest in the world, as reported by the China Feed Industry Association in 2023. Regulatory shifts have played a pivotal role since the 2018 ban on antibiotic growth promoters; feed enzyme adoption has surged as a key alternative for maintaining animal health and performance. The Ministry of Agriculture and Rural Affairs mandates reduced phosphorus discharge, pushing integrators like New Hope Group and COFCO to adopt phytase-enriched formulations. With domestic enzyme production growing at 10% annually and firms like VTR Bio-Tech expanding capacity, China’s dominance is structural and self-reinforcing.

India is also a key player in the APAC feed enzyme market. The country’s position is underpinned by its rapidly expanding poultry and aquaculture sectors, supported by rising protein demand from a population exceeding 1.4 billion. The adoption of feed enzymes is accelerating due to the high cost of imported feed ingredients and the prevalence of locally sourced, fibrous materials like rice bran and sorghum, which require carbohydrase supplementation. Government initiatives like the National Livestock Mission and PMMSY are promoting scientific feeding practices, further boosting enzyme uptake. Additionally, India’s booming shrimp exports are driving demand for enzyme-enhanced aqua feeds to improve survival and growth rates. With domestic enzyme production still limited, multinational players like DSM and Novozymes are expanding distribution networks, signaling strong future growth.

Japan occupies a mature yet influential position in the APAC feed enzyme market. The country’s significance lies in its high-value, technology-driven animal production systems, particularly in poultry and swine, where feed efficiency and food safety are paramount. Japan imports a large share of its feed grains, making enzyme use critical for maximizing nutrient extraction from costly inputs. The country’s antibiotic-free (ABF) poultry movement, led by major retailers, has made enzyme supplementation a standard practice. Also, xylanase and protease blends improved broiler feed conversion ratios, directly supporting ABF production. Furthermore, Japan’s strict environmental regulations limit phosphorus runoff, incentivizing phytase use. The country also serves as a hub for enzyme innovation; firms operate advanced R&D centers in Japan, tailoring products for high-performance diets. While volume growth is moderate, Japan’s premium pricing and regulatory leadership amplify its market influence.

Vietnam has emerged as a dynamic force in the APAC feed enzyme market. Its rise is fueled by one of the fastest-expanding animal protein sectors in Southeast Asia, particularly in swine and aquaculture. The country’s feed industry produces millions of metric tons of compound feed per year, with enzyme penetration rising rapidly due to the use of locally available, high-fiber ingredients like rice bran and cassava. With foreign investments from Cargill and Charoen Pokphand, and local firms like Biogreen expanding enzyme production, Vietnam’s market is poised for continued expansion.

KEY MARKET PLAYERS

DuPont, DSM, ASF Corporation, Alltech, Novozymes, Adisseo France, AB Enzymes GmbH, Advanced Enzymes Technologies Limited, Amano Enzyme Inc., Bio-Vet JSC, Biocatalysts Ltd, Chr. Hansen Inc., EnmexSAB de CVv, Lesaffre Group, PURATOS GROUP, Rossari Biotech Limited, Shenzhen Leveking Bio-Engineering C,o. Ltd, Sunson Industry Group Company Limited. Some major key players are involved in the Asia Pacific feed enzymes market.

Top Players In the Market

Novozymes A/S has long been a pivotal force in the Asia Pacific feed enzyme landscape, leveraging its robust R&D capabilities and deep scientific expertise to deliver high-performance enzyme solutions tailored to regional feed formulations. The company has intensified its focus on Asia by expanding technical service teams in India, China, and Thailand, ensuring close collaboration with feed millers and integrators. The company also strengthened its regional footprint through partnerships with local distributors and participation in key agricultural expos such as VIV Asia. Its investment in digital tools like Enzyme Evaluator, which models enzyme performance in specific diets, has enhanced customer engagement and adoption. Novozymes continues to lead in innovation, particularly in carbohydrases for poultry and swine, reinforcing its reputation as a technology-driven market enabler in the region.

ADM (Archer Daniels Midland Company) has significantly expanded its presence in the Asia Pacific feed enzyme market through the strategic integration of its animal nutrition portfolio and localized production capabilities. Since then, ADM has invested in upgrading formulation labs in Singapore and Shanghai to develop region-specific enzyme blends that address challenges like high-fiber diets and heat stress. ADM has also deepened relationships with major poultry producers by offering holistic nutrition programs that combine enzymes with mycotoxin binders and probiotics. Its emphasis on sustainability, including carbon footprint reduction in feed production, aligns with regional regulatory trends, positioning ADM as a solutions-oriented player driving efficiency and environmental compliance across the APAC livestock sector.

Danisco Animal Nutrition (part of DuPont) holds a prominent position in the Asia Pacific feed enzyme market through its pioneering work in enzyme technology and strong technical support infrastructure. The company’s Axtra portfolio, including Axtra PHY and Axtra XB, has gained widespread acceptance in poultry and swine operations across India, Japan, and South Korea due to its thermostability and efficacy in complex diets. Danisco has invested heavily in field trials and application research, collaborating with universities and government agencies to validate enzyme performance under local conditions. In 2023, the company launched Axtra XAP, a protease-xylanase blend, in Vietnam and the Philippines, targeting improved protein digestibility in low-soy diets. DuPont also enhanced its regional technical service team and introduced digital advisory tools to support feed formulators. By combining scientific rigor with customer-centric innovation, Danisco has solidified its role as a trusted partner in advancing feed efficiency and sustainability across diverse APAC production systems.

Top Strategies Used By The Key Market Participant

Key players in the Asia Pacific feed enzyme market are prioritizing product innovation, regional customization, and strategic partnerships to strengthen their foothold. Companies are investing in R&D to develop thermostable and multi-enzyme complexes suited for tropical feed processing and plant-based diets. Collaborations with local feed mills and integrators enable tailored solutions and faster market penetration. Expanding technical service teams and digital tools enhances customer engagement and adoption. Mergers and acquisitions, such as ADM’s integration of Neovia, amplify distribution reach. Additionally, firms are aligning with sustainability trends by promoting enzyme use to reduce phosphorus excretion and lower carbon footprints, meeting regulatory and consumer demands across the region.

COMPETITION OVERVIEW

The Asia Pacific feed enzyme market features intense competition driven by technological differentiation and regional adaptability. Global leaders like Novozymes, DuPont, and ADM compete with emerging regional players and local manufacturers by emphasizing innovation, technical support, and sustainability. While multinationals dominate in product quality and R&D, local firms offer cost-effective alternatives, particularly in price-sensitive markets like India and Indonesia. Competition is increasingly shaped by the ability to deliver customized enzyme blends for diverse feed matrices and animal species. Companies are also differentiating through digital tools, field trials, and regulatory compliance support. Strategic expansions, product launches, and partnerships are common tactics. With rising demand for sustainable and antibiotic-free animal production, the competitive landscape is evolving toward integrated nutrition solutions, where enzyme efficacy, reliability, and environmental impact determine market success.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Novozymes launched Hostazym X, a high-stability phytase, across Southeast Asia to enhance phosphorus availability and support antibiotic-free poultry production, strengthening its technical leadership in the region.

- In July 2022, ADM completed the acquisition of Neovia, integrating its animal nutrition expertise and distribution network to expand enzyme market access in China, Vietnam, and Indonesia.

- In January 2024, DuPont introduced Axtra® XAP, a protease-xylanase enzyme blend, in the Philippines and Vietnam to improve protein digestibility in low-soy aquaculture and swine diets.

- In September 2023, Adisseo inaugurated a new technical application center in Shanghai to develop customized enzyme solutions for Asian feed millers and livestock producers.

- In May 2023, Kemin Industries expanded its enzyme production capacity in Singapore to meet rising demand for phytase and carbohydrase products in the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia Pacific feed enzymes market is segmented and sub-segmented into the following categories.

By Ingredients

- Carbohydrase

- Phytase

- Others

By Animal Type

- Ruminant

- Swine

- Poultry

- Aquaculture

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

what is the current size of the Asia Pacific feed enzymes market?

The current size of the Asia-Pacific feed enzymes market has been estimated at USD 37.56 Billion in 2024.

what is the expected growth value in Asia Pacific feed enzymes market?

Asia-Pacific feed enzymes market is expected to grow at USD 43.33 Billion by 2028, growing at a CAGR of 7.40% during the forecast period from 2025 to 2033.

which segment highly dominating the Asia Pacific feed enzymes market?

Poultry and swine segments comprise the majority of feed enzymes market share, followed by ruminants. Carbohydrates are the most widely used enzyme.

which region accounted for the largest share in the Asia Pacific feed enzymes market?

China is the major manufacturer, which accounts for around half of the production of feed Enzymes in the Asia-Pacific region.

what are the key market players involved in the Asia Pacific feed enzymes market?

DuPont, DSM, ASF Corporation, Alltech, Novozymes, and Adisseo France, AB Enzymes GmbH, Advanced Enzymes Technologies Limited, Amano Enzyme Inc. Bio-Vet JSC, Biocatalysts ltd, Chr. Hansen Inc, Enmex Sa De Cv, Lesaffre Group, PURATOS GROUP, Rossari Biotech Limited, Shenzhen Leveking Bio-Engineering Co. Ltd, Sunson Industry Group Company Limited. Some major key players are involved in the Asia Pacific feed enzymes market.

What is driving demand in the Asia Pacific feed enzymes market?

Rising livestock production and the need for efficient feed utilization are pushing farmers to adopt enzymes like phytase and protease.

What types of enzymes are most commonly used?

Phytase tops the list, helping animals absorb phosphorus and reducing the need for inorganic supplements.

How do feed enzymes support cost-efficiency for farmers?

They improve nutrient digestion, allowing lower feed inputs while maintaining animal growth and health.

What role do regulations play in enzyme adoption?

Countries are setting standards for enzyme safety and labeling, building trust among feed manufacturers.

What challenges do suppliers face in the region?

Small farms often lack awareness about enzyme benefits, requiring education and technical support.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com