Global Feed Enzymes Market Size, Share, Trends & Growth Forecast Report, Segmented By Type (Phytase, Carbohydrase, Protease And Others), Livestock (Poultry, Swine, Ruminants, Aquatic Animals And Others), Source (Microorganism, Plant, Animal), Form (Dry and Liquid), and Region (North America, Europe, Aisa-Pacific, Latin America, Middle East And Africa), Industry Analysis From (2026 to 2034)

Global Feed Enzymes Market Size

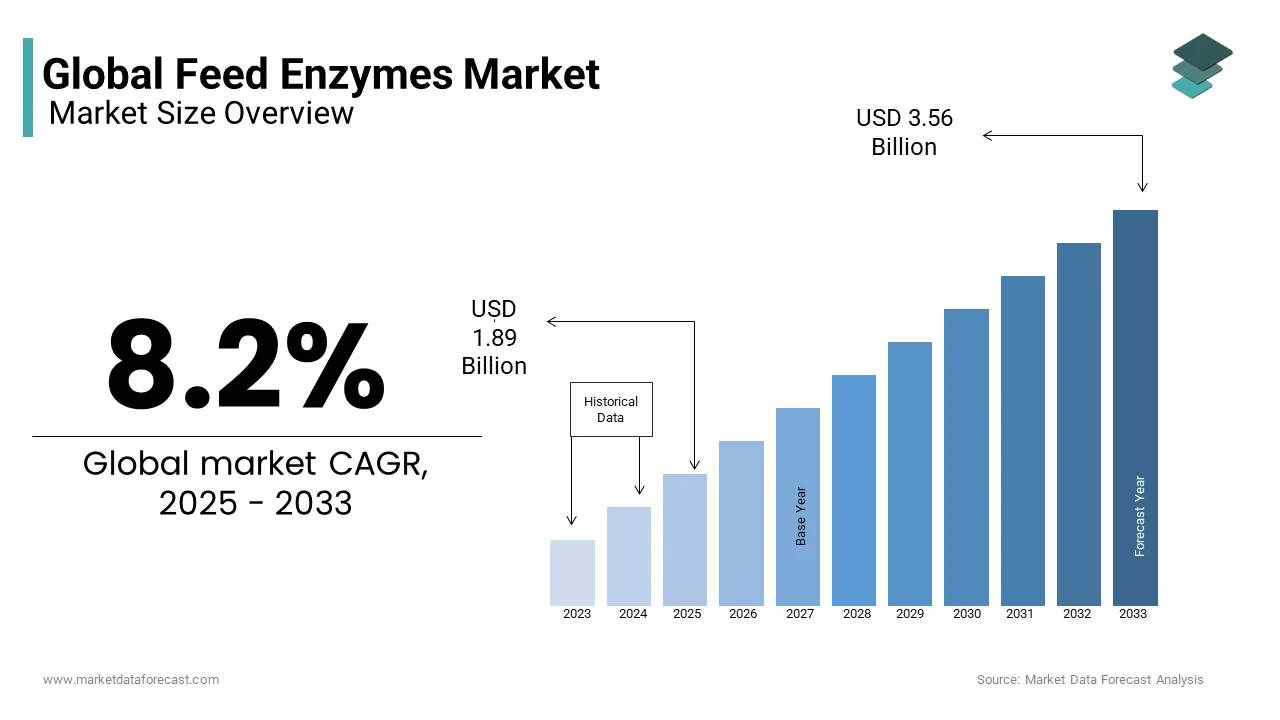

The global feed enzyme market size was valued at USD 1.89 billion in 2025 and is anticipated to reach USD 2.04 billion in 2026 from USD 3.84 billion by 2034, growing at a CAGR of 8.2% during the forecast period from 2026 to 2034.

The feed enzymes are specialized category of biological catalysts integrated into animal nutrition formulations to optimize digestive efficiency and enhance nutrient bioavailability. These enzymatic additives function by deconstructing complex dietary matrices, such as phytate bound phosphorus, non-starch polysaccharides, and resistant proteins into absorbable micromolecules. The strategic incorporation of these biocatalysts directly influences metabolic performance and reduces the environmental footprint of intensive farming operations. As per the Food and Agriculture Organization of the United Nations, global livestock populations exceeded 1.5 billion cattle and 1 billion poultry birds in 2024, generating unprecedented volumes of agricultural waste and nutrient runoff. The European Commission documented that nitrogen emissions from intensive animal husbandry surpassed 3 million metric tons annually across member states, underscoring the urgent need for dietary interventions that minimize excretory load. The progressive integration of enzyme technology into compound feed matrices represents a paradigm shift from conventional supplementation toward precision nutrition. Regulatory frameworks across multiple jurisdictions now mandate stricter phosphorus discharge limits by compelling feed manufacturers to adopt enzymatic hydrolysis as a standard formulation practice.

MARKET DRIVERS

Escalating Global Poultry and Swine Production Intensifies Demand for Digestive Enhancers

The exponential expansion of monogastric livestock operations with the integration of enzymatic additives into commercial feed formulations is propelling the growth of the feed enzymes market. Poultry and swine possess inherently limited endogenous enzyme synthesis by rendering them heavily dependent on exogenous biocatalysts to unlock bound nutrients within cereal derived diets. As per the International Meat Secretariat, global poultry meat production reached 142 million metric tons in 2024, while commercial pork output expanded to 128 million metric tons during the same period. This structural shift toward high volume protein generation compels integrators to maximize feed conversion ratios while maintaining stringent growth performance benchmarks. According to the United States Department of Agriculture, compound feed consumption for broiler operations alone consumed over 450 million metric tons annually, creating a massive substrate for enzymatic modification. Producers increasingly deploy carbohydrase and protease blends to degrade complex carbohydrate structures that typically impair intestinal viscosity and nutrient absorption. The continuous optimization of genetic lines for rapid weight gain has simultaneously elevated metabolic stress by making dietary enzyme supplementation indispensable for sustaining gut integrity and mitigating subclinical inflammation. Consequently, feed manufacturers prioritize multiple enzyme formulations that synchronize with accelerated digestive transit times and modern pelleting protocols.

Regulatory Mandates for Environmental Compliance Accelerate Enzyme Adoption Stringent governmental frameworks targeting agricultural nutrient runoff compel feed manufacturers to integrate specialized biocatalysts that minimize excretory pollution, which is also propelling the growth of the feed enzymes market. The regulatory mandates for environmental compliance Intensive livestock operations historically generated substantial phosphorus and nitrogen discharge, which directly degrades aquatic ecosystems and compromises groundwater quality. The European Union mandates maximum phosphorus inclusion thresholds in animal diets, forcing nutritionists to replace inorganic phosphate supplements with phytase driven nutritional strategies. According to the Environmental Protection Agency, phosphorus excretion from confined swine facilities decreased by 35% when commercial feed rations incorporated elevated dose phytase variants at concentrations exceeding 1500 units per kilogram. These regulatory interventions directly stimulate demand for advanced enzyme systems that enhance mineral retention and reduce dietary crude protein requirements. Compliance with tightening discharge standards transforms enzyme procurement from an optional nutritional strategy into a mandatory operational requirement. This regulatory alignment guarantees sustained market expansion as agricultural sectors globally transition toward ecologically responsible feeding paradigms that satisfy both environmental legislation and commercial productivity targets.

MARKET RESTRAINTS

Escalating Manufacturing Costs and Raw Material Volatility Constrain Market Expansion The commercial production of specialized feed enzymes demands substantial capital investment in fermentation infrastructure, precision purification systems, and cold chain logistics, which is hindering the growth of the feed enzymes market. Microbial strain development and large scale bioreactor maintenance require highly skilled personnel and continuous quality assurance protocols that strain manufacturer profit margins. Feed integrators operating in price sensitive emerging countries frequently hesitate to adopt premium enzymatic additives when conventional mineral and synthetic amino acid alternatives remain economically accessible. Consequently, procurement decisions heavily weigh the cost benefit ratio, compelling many commercial operations to limit enzyme inclusion to baseline nutritional thresholds rather than pursuing comprehensive multiple component formulations. This financial friction consistently moderates market velocity despite proven technical efficacy.

Thermal Instability During Feed Processing Compromises Enzymatic Efficacy

The integration of biological catalysts into compound feed matrices frequently encounters severe degradation during high temperature pelleting and extrusion protocols, which fundamentally undermines their functional performance. The thermal instability during feed processing is also limiting the growth of the feed enzymes market. Modern feed manufacturing routinely subjects mash mixtures to steam conditioning at temperatures exceeding 85 degrees Celsius and sustained pressures above 40 bars, creating an inhospitable environment for delicate protein structures. According to the European Association of Animal Production, thermal denaturation rates vary substantially across enzyme classes with xylanase and beta glucanase exhibiting 45% activity loss when exposed to prolonged conditioning cycles without protective microencapsulation. Feed manufacturers face considerable technical challenges when balancing optimal starch gelatinization requirements with the preservation of heat sensitive biocatalysts. The necessity for specialized coating technologies and liquid application systems introduces additional complexity and capital expenditure for mill operators. These processing constraints frequently deter widespread adoption in facilities lacking advanced thermal management infrastructure. The inconsistent enzymatic performance across varying production batches erodes producer confidence and limits the seamless integration of these biological additives into standardized feed manufacturing workflows.

MARKET OPPORTUNITIES

Precision Enzyme Engineering Unlocks Next Generation Nutritional Optimization

The rapid advancement of synthetic biology and directed evolution methodologies enables the design of highly customized biocatalysts that exhibit unprecedented thermal resilience and substrate specificity. The precision enzyme engineering unlocks next generation nutritional optimization is majorly to enhance new opportunities for the growth of the feed enzymes market. Researchers now utilize computational protein modeling and high throughput screening to engineer enzyme variants capable of maintaining structural integrity under extreme pelleting conditions, while targeting complex anti nutritional factors. These scientific breakthroughs facilitate the development of broad spectrum enzyme cocktails that simultaneously degrade multiple indigestible matrices, thereby maximizing nutrient release across diverse dietary compositions. Commercial manufacturers increasingly leverage these tailored formulations to replace expensive synthetic amino acids and inorganic mineral premixes, generating substantial cost savings for integrated livestock operations. The transition from single function additives to multiple targeted biological complexes aligns perfectly with the industry demand for precision nutrition strategies. This technological evolution fundamentally transforms enzyme procurement from a commodity transaction into a value driven scientific partnership, opening lucrative revenue channels for innovators who can deliver measurable performance differentials.

Aquaculture Expansion and Alternative Feed Integration Drive Niche Enzyme Demand The accelerating transition toward sustainable aquatic protein production creates substantial demand for specialized enzymatic formulations designed to optimize digestibility in fish and crustacean diets. The aquaculture expansion nd alternative feed integration is also to drive new opportunities for the growth of the feed enzymes market. Aquaculture operations increasingly incorporate botanical derived ingredients such as soybean meal and rapeseed protein to offset marine fishmeal reliance, yet these substrates contain elevated concentrations of non starch polysaccharides and phytate that impair nutrient absorption. As per the Food and Agriculture Organization, global aquaculture production surpassed 130 million metric tons in 2024, with compound feed consumption for finfish and shrimp operations exceeding 55 million metric tons annually. The parallel emergence of insect meal and microalgae derived feed ingredients further amplifies the requirement for tailored enzymatic systems capable of degrading chitin and complex algal cell walls. Feed manufacturers actively explore multiple enzyme platforms that synchronize with novel protein sources to maintain optimal growth trajectories while minimizing aquatic waste discharge.

MARKET CHALLENGES

Fragmented Regulatory Approval Frameworks Hinder Global Market Harmonization

The commercial distribution of feed enzymes encounters substantial administrative friction due to divergent approval methodologies, varying safety thresholds, and inconsistent labeling requirements across international jurisdictions. The fragmented regulatory approval frameworks is likely to pose as a major challenge for the growth of the feed enzyme market. Manufacturers must navigate complex registration protocols that differ significantly between agricultural authorities, demanding extensive toxicological dossiers and prolonged evaluation periods before market entry. As per the European Food Safety Authority, the average approval timeline for novel feed additives spans 38 months, requiring comprehensive environmental impact assessments and multiple species safety trials before commercial authorization. This administrative fragmentation forces producers to maintain parallel development pipelines and duplicate clinical validation studies, substantially inflating commercialization expenses. Small and mid-scale manufacturers frequently lack the regulatory expertise and financial resources required to sustain multiple regional compliance initiatives, limiting their geographic reach and concentrating market power among established multinational corporations. The absence of harmonized international standards creates persistent trade barriers that delay product launches and restrict the seamless transfer of innovative enzymatic technologies to emerging agricultural economies requiring rapid nutritional modernization.

Inconsistent Efficacy Validation Standards Generate Producer Skepticism

The feed additives sector struggles with substantial methodological variability when quantifying enzymatic performance, which frequently generates confusion among livestock producers regarding actual nutritional benefits and return on investment. The inconsistent efficacy validation standards is another factor to inhibit the growth of the feed enzyme market. Divergent laboratory testing protocols, varying substrate compositions, and non-standardized in vivo trial designs produce inconsistent bioavailability metrics that complicate purchasing decisions. The lack of standardized performance guarantees complicates formulation optimization and discourages widespread adoption among cost conscious operations that demand transparent efficacy documentation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.2% |

| Segments Covered | By Type, Livestock, Source, Form, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cargill, Incorporated (US), BASF SE (Germany), DuPont (US), Bluestar Adisseo Co., Ltd. (China), Koninklijke DSM NV (Netherlands), Kemin Industries, Inc., Novus International, BEC Feed Solutions, BioResource International, Inc., Bioproton Pty Ltd, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The phytase segment was the largest by holding 45.3% of the feed enzymes market share in 2025. The urgent regulatory and economic imperative to reduce inorganic phosphate supplementation in animal diets is elevating the growth of the segment. As per the International Fertilizer Association, global phosphate rock reserves are finite, with current extraction rates projected to deplete high quality deposits within 80 years, driving up costs for synthetic mineral additives. The mandatory reductions in dietary phosphorus levels across member states have compelled feed manufacturers to adopt high dose phytase variants that release bound phosphorus from plant-based ingredients. This enzymatic hydrolysis allows producers to lower total diet phosphorus content by up to 0.15%age points without compromising skeletal development or growth performance. These environmental compliance measures combined with significant cost savings on mineral premixes solidify phytase as the indispensable cornerstone of modern compound feed formulations globally.

The protease segment is likely to register a fastest CAGR of 7.8% throughout the forecast period owing to the shift toward reducing crude protein levels in animal rations to mitigate nitrogen pollution and lower feed costs. As per the United States Department of Agriculture, soybean meal prices fluctuated by 25% in 2024 by prompting nutritionists to seek alternative protein sources, such as rapeseed meal and sunflower meal, which contain higher levels of anti-nutritional factors. The ability to formulate low protein diets while maintaining lean tissue accretion rates drives substantial adoption among integrated poultry and swine producers. Furthermore, recent advancements in thermal stable protease variants allow for effective retention during high temperature pelleting processes by addressing previous efficacy concerns.

By Livestock Insights

The poultry segment was accounted in holding 42.3% of the feed enzymes market share in 2025 owing to the sheer scale of commercial broiler and layer operations, which rely heavily on cereal based diets rich in non-starch polysaccharides. As per the Food and Agriculture Organization, global poultry meat production reached 142 million metric tons in 2024, requiring over 450 million metric tons of compound feed annually. The short digestive tract of birds limits endogenous enzyme secretion, making exogenous supplementation essential for unlocking energy from wheat, barley, and corn substrates. According to the International Poultry Council, the inclusion of carbohydrase blends improves feed conversion ratios by 3 to 5 points, translating to significant economic gains in high volume production systems. The intense genetic selection for rapid growth rates further elevates metabolic demands by necessitating precise nutrient availability that only enzymatic enhancement can provide. Regulatory pressures to reduce antibiotic usage in poultry farming have also elevated the role of enzymes in maintaining gut health and preventing pathogenic bacterial proliferation, thereby reinforcing their strategic importance in modern avian nutrition protocols.

The aquatic animals segment is likely to witness a fastest CAGR of 8.2% during the forecast period with the aquaculture transitions toward sustainable feed formulations. The rapid expansion of fish and shrimp farming necessitates innovative nutritional solutions to replace diminishing marine resources with plant-based alternatives. As per the World Aquaculture Society, global aquaculture production surpassed 130 million metric tons in 2024, with compound feed usage exceeding 55 million metric tons. Plant derived ingredients, such as soybean meal contain high levels of phytate and complex carbohydrates that impair digestibility in fish species with limited enzymatic capacity. The increasing consumer demand for environmentally responsible seafood drives producers to adopt enzyme technologies that minimize waste and optimize nutrient utilization. Additionally, the emergence of novel ingredients like insect meal and microalgae requires specialized enzymatic profiles to degrade chitin and cell walls, creating new avenues for targeted biocatalyst application in aquatic nutrition.

By Source Insights

The microorganism segment was accounted in holding a significant share of the feed enzymes market share in 2025. Industrial fermentation using bacteria and fungi allows for the consistent manufacturing of high purity enzymatic proteins at competitive costs. As per the Industrial Biotechnology Association, microbial fermentation yields are 10 times higher than plant extraction methods by enabling manufacturers to meet the massive volume demands of the global feed industry. The genetically modified microbial strains produce enzyme variants with enhanced thermal stability and pH tolerance by ensuring functionality during rigorous feed processing conditions. The ability to tailor microbial genetics for specific substrate targeting facilitates the development of customized enzyme cocktails that address diverse dietary challenges across livestock species. Regulatory approvals for microbial derived additives are well established in major markets, providing manufacturers with streamlined pathways for commercialization. The cost effectiveness of large-scale bioreactor operations combined with continuous innovation in strain improvement technologies cements microorganisms as the foundational source for commercial feed enzyme production worldwide.

The plant segment is likely to grow at a fastest CAGR of 6.5% during the forecast period with the consumer preference for natural and non-genetically modified ingredients. As per the Organic Trade Association, sales of organic animal products increased by 12% in 2024 by creating demand for processing aids that align with natural sourcing principles. The advances in extraction technologies have improved the yield and stability of plant based enzymes, such as bromelain from pineapple and papain from papaya by making them commercially viable for specialized feed applications. These enzymes offer unique functional properties, including anti-inflammatory benefits and improved protein digestibility without the perceived risks associated with microbial fermentation. The growing awareness toward industrial bioprocessing in certain consumer segments fuels investment in plant based alternatives.

By Form Insights

The dry form enzymes segment was the dominant by capturing a 59.1% of the feed enzymes market share in 2025. Powdered formulations integrate seamlessly into dry mash and pellet production lines, allowing for uniform distribution within compound feed matrices. As per the American Feed Industry Association, over 70% of global compound feed is produced in dry form, necessitating enzymatic additives that withstand mixing and pelleting without clumping or degradation. According to the International Feed Ingredients Federation, dry enzymes exhibit superior shelf life, retaining 90% of their activity after 12 months of storage under ambient conditions compared to liquid variants which require refrigeration. The logistical advantages of transporting concentrated powders reduce shipping costs and simplify inventory management for feed mills operating in remote locations. Recent innovations in microencapsulation technology have further enhanced the thermal protection of dry enzymes, ensuring high retention rates during high temperature conditioning. These operational efficiencies and robust stability profiles make dry forms the preferred choice for large scale commercial feed operations prioritizing consistency and cost effectiveness.

The liquid form enzymes segment is lucratively growing at a fastest CAGR of 7.2% from 2026 to 2034 due to advancements in post pelleting application technologies. The ability to apply liquid enzymes directly onto finished feed pellets avoids exposure to high heat and pressure, preserving maximum biological activity. According to the Feed Machinery Manufacturers Association, installation of liquid dosing systems in feed mills increased by 15% in 2024, reflecting industry adoption of precision application methods. Liquid formulations allow for flexible dosage adjustments and easy integration of multiple enzyme types without segregation issues common in dry mixes. The rise of specialized feed mills equipped with advanced coating drums facilitates accurate liquid distribution, ensuring uniform coverage on pellet surfaces. This technological shift enables producers to utilize lower enzyme inclusion rates while achieving equivalent or better results, optimizing cost efficiency and driving the rapid uptake of liquid enzymatic solutions in modern feed production facilities.

REGIONAL ANALYSIS

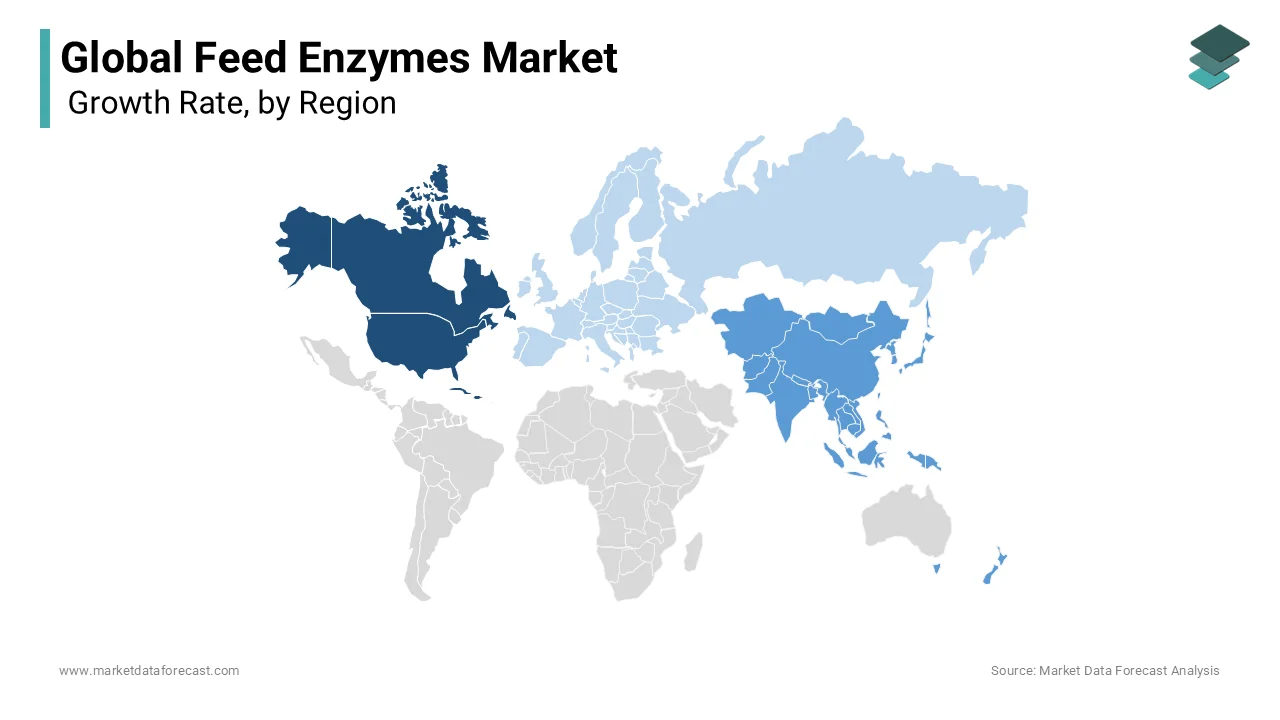

Asia Pacific Market Analysis

Asia Pacific was the largest contributor in the feed enzymes market by holding 38.3% of share in 2025 with the massive scale of livestock production in China, India, and Vietnam. The region serves as the global epicenter for poultry and swine farming, consuming vast quantities of compound feed enriched with enzymatic additives. According to the Chinese Ministry of Agriculture, national mandates restricting antibiotic use in animal feed since 2020 have accelerated the adoption of enzyme technologies as alternative gut health promoters. Rapid urbanization and rising disposable incomes have increased per capita meat consumption, compelling producers to intensify operations and optimize feed conversion ratios. The presence of numerous local enzyme manufacturers alongside multinational corporations fosters competitive pricing and widespread accessibility. Government initiatives promoting sustainable agriculture and waste reduction further support market expansion.

North America Market Analysis

North America feed enzymes market was ranked second by holding 22.1% of share in 2025 with the advanced technological adoption and stringent environmental regulations. The United States and Canada feature highly integrated livestock sectors that prioritize precision nutrition and operational efficiency. As per the United States Department of Agriculture, the US poultry industry alone consumes over 200 million metric tons of feed annually, with high penetration rates for phytase and carbohydrase supplements. The strict guidelines on nutrient runoff from concentrated animal feeding operations drive mandatory implementation of enzyme strategies to minimize phosphorus and nitrogen excretion. The region benefits from robust research infrastructure and early adoption of next generation enzymatic variants with enhanced thermal stability. Major feed manufacturers collaborate closely with biotechnology firms to develop customized solutions tailored to specific dietary formulations. High labor costs and capital-intensive farming models incentivize investments in productivity enhancing additives. The mature market structure focuses on value added innovations rather than volume growth, maintaining steady demand for premium enzyme products that deliver measurable performance improvements.

Europe Market Analysis

Europe feed enzymes market growth is deemed to grow at a fastest CAGR during the forecast period with the rigorous regulatory frameworks and strong emphasis on environmental sustainability. The European Union leads global policy development regarding agricultural emissions and animal welfare, directly influencing feed formulation practices. The Farm to Fork Strategy mandates significant reductions in nutrient losses from fertilizers and animal feed by compelling widespread adoption of phytase and protease technologies. The approval processes for novel feed additives prioritize environmental impact assessments by favoring enzymes that reduce ecological footprints. The region exhibits high awareness of antibiotic resistance, driving substitution of medicinal growth promoters with enzymatic gut health solutions. Dense livestock populations in countries like Germany, Spain, and France create concentrated demand for efficient waste management strategies. Premium pricing for sustainably produced meat encourages farmers to invest in advanced nutritional technologies. The mature regulatory environment ensures high product quality standards, fostering trust in enzymatic additives among producers and consumers alike.

Latin America Market Analysis

Latin America feed enzymes market growth is driven by the expanding export oriented livestock sectors in Brazil, Argentina, and Mexico. As per the Brazilian Animal Protein Association, Brazil exported over 4 million metric tons of chicken meat in 2024, necessitating efficient feed utilization to maintain profitability. According to the Inter American Institute for Cooperation on Agriculture, increasing adoption of modern farming techniques in the region drives demand for enzymatic additives that improve feed conversion ratios. Large scale integrated producers dominate the market, leveraging economies of scale to implement advanced nutritional strategies. Growing domestic meat consumption due to population growth and urbanization further stimulates feed demand. Regulatory harmonization efforts across Mercosur countries facilitate trade and standardize additive approvals.

Middle East and Africa Market Analysis

Middle East and Africa feed enzymes market growth is likely to grow with the emerging livestock industries and increasing investment in food security initiatives. Countries such as Saudi Arabia, Egypt, and South Africa are expanding domestic meat production to reduce reliance on imports. The agricultural development programs prioritize intensification of poultry and dairy sectors by creating new opportunities for feed efficiency technologies. According to the Gulf Cooperation Council Standardization Organization, evolving regulatory frameworks encourage the adoption of safe and effective feed additives to support growing animal populations. Water scarcity and limited arable land necessitate optimal resource utilization, driving interest in enzymes that enhance nutrient bioavailability from imported feed ingredients. Foreign direct investment in modern feed mills introduces advanced manufacturing capabilities and enzymatic solutions to the region. Rising middle class incomes increase demand for animal protein, stimulating local production expansions.

COMPETITIVE LANDSCAPE

The feed enzymes market features intense competition among established multinational corporations and emerging regional manufacturers. Leading companies differentiate themselves through scientific innovation, product efficacy, and technical support services. Competitive dynamics revolve around developing enzymes with enhanced stability and broader substrate specificity. Price sensitivity in emerging markets drives local production and cost optimization strategies. Regulatory compliance and sustainability credentials serve as key differentiators in premium segments. Mergers and acquisitions consolidate market power and expand technological capabilities. Collaboration with research institutions accelerates product development cycles. Customer relationships rely on demonstrated performance improvements and return on investment.

KEY MARKET PLAYERS

Some of the leading companies operating in the global feed enzyme market are

- Cargill

- Incorporated (US)

- DSM Firmenich AG

- Adisseo

- Novozymes

- BASF SE (Germany)

- DuPont (US)

- Bluestar Adisseo Co., Ltd. (China)

- Koninklijke DSM NV (Netherlands)

- Kemin Industries, Inc

- Novus International

- BEC Feed Solutions

- BioResource International, Inc.

- Bioproton Pty Ltd

Top Players In The Market

- DSM Firmenich AG operates as a global leader in nutritional sciences, delivering innovative enzyme solutions that enhance animal health and sustainability. The company leverages extensive research capabilities to develop next generation phytase and carbohydrase products that improve nutrient digestibility and reduce environmental impact. DSM Firmenich recently expanded its production facilities in Asia to meet rising demand for precision nutrition additives. Their strategic collaborations with feed manufacturers ensure seamless integration of enzymatic technologies into diverse dietary formulations. The company emphasizes digital tools for dosage optimization, helping producers maximize return on investment.

- Novozymes A S specializes in biological solutions, offering a comprehensive portfolio of feed enzymes designed to optimize animal performance and resource efficiency. The company utilizes advanced fermentation technologies to produce high potency enzymes with superior thermal stability. Novozymes actively invests in research and development to create customized enzyme cocktails targeting specific anti nutritional factors in plant-based ingredients. Recent initiatives, include partnerships with academic institutions to explore novel microbial strains for enhanced efficacy. The company provides technical support services to help feed mills implement best practices for enzyme application.

- Adisseo focuses on animal nutrition expertise, providing specialized enzyme products that improve gut health and feed efficiency. The company integrates enzymatic solutions with its broader portfolio of amino acids and vitamins to offer holistic nutritional strategies. Adisseo recently launched new protease variants designed for low protein diets, supporting industry efforts to reduce nitrogen emissions. The company expands its manufacturing footprint in emerging markets to enhance supply chain reliability and customer proximity. Adisseo collaborates with key stakeholders to conduct field trials demonstrating the economic benefits of enzyme supplementation.

Top Strategies Used by Key Market Participants

Key players prioritize research and development to create thermally stable and multi functional enzyme complexes. Strategic acquisitions enable companies to expand geographic reach and diversify product portfolios. Partnerships with feed manufacturers facilitate customized solutions and technical integration. Investment in production capacity ensures supply chain resilience and cost competitiveness. Digital platforms provide data driven insights for optimized enzyme usage and performance tracking.

MARKET SEGMENTATION

This market research report on the global feed enzymes market is segmented and sub-segmented into the following categories.

By Type

- Phytase

- Carbohydrase

- Protease

- Others (lipase, mannanase, and á-galactosidase)

By Livestock

- Poultry

- Swine

- Ruminants

- Aquatic animals

- Others (equine and pets)

By Source

- Microorganism

- Plant

- Animal

By Form

- Dry

- Liquid

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global feed enzymes market?

It refers to the market for enzyme additives used in animal feed to improve digestion, nutrient absorption, and overall animal performance.

What drives growth in the feed enzymes market?

Rising demand for animal protein, need for efficient feed utilization, and focus on reducing feed costs drive market growth.

What are common types of feed enzymes?

Phytase, protease, carbohydrase (e.g., xylanase, amylase), and multi-enzyme blends are common types.

How do feed enzymes benefit livestock?

They improve nutrient digestibility, enhance growth performance, and reduce waste and environmental pollution.

Which animals are major end users of feed enzymes?

Poultry, swine, ruminants (cattle, sheep), and aquaculture species are key end users.

Which regions lead the feed enzymes market?

Asia-Pacific, North America, and Europe are major markets due to expanding livestock production.

What challenges affect the market?

High R&D costs, variable enzyme efficacy across feeds, and formulation compatibility are key challenges.

How does sustainability influence the market?

Feed enzymes help reduce nutrient excretion and greenhouse gas emissions from livestock, supporting sustainable animal farming.

What opportunities exist in the feed enzymes market?

Growth in precision nutrition, enzyme innovation, and increasing use in aquafeed and specialty feeds present opportunities.

What is the future outlook for the global feed enzymes market?

The market is expected to grow steadily due to rising animal protein demand and technology-driven enzyme solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com