Asia Pacific Frozen Food Market Segmentation by Product (Frozen Ready Meals, Meat & Poultry, Seafood, Vegetables & Fruits, Potatoes, and Soup), User (Retail and Foodservice Industry), And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Market Size, 2025

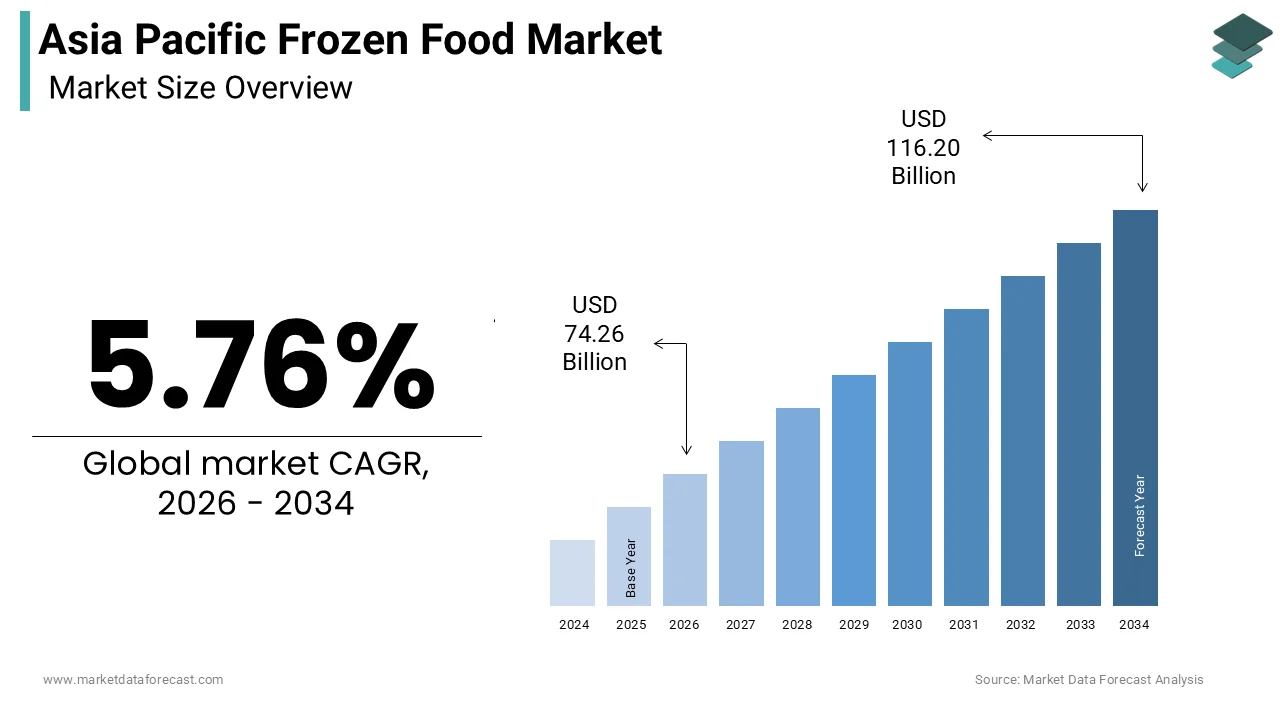

$70.20 BnMarket Estimate, 2026

$74.24 BnMarket Forecast, 2034

$116.20 BnCAGR, 2026–2034

5.76%Asia Pacific Frozen Food Market Size

The Size of the Asia Pacific Frozen Food Market was calculated to be USD 70.20 billion in 2025 and is anticipated to be worth USD 116.20 billion by 2034, from USD 74.24 billion in 2026, growing at a CAGR of 5.76% during the forecast period.

Frozen food is a wide array of pre-processed, temperature-controlled food products that are preserved at sub-zero temperatures for extended shelf life. This includes frozen fruits and vegetables, ready-to-eat meals, seafood, meat products, bakery items, and dairy-based frozen goods. The sector has evolved significantly over the past decade, driven by rapid urbanization, shifting consumer preferences, and advancements in cold chain logistics. Unlike traditional markets in North America and Europe, where frozen foods have long been staples, the Asia Pacific region is witnessing accelerated adoption due to lifestyle changes and increasing health awareness.

Urban populations across countries like China, India, Japan, South Korea, and Australia are increasingly relying on convenience foods that offer both nutritional value and time-saving preparation. According to data from the United Nations Department of Economic and Social Affairs (UN DESA), a significant portion of the population in the Asia Pacific region now resides in urban areas, with this share expected to rise notably by 2040. This demographic shift has led to higher disposable incomes and changing dietary habits, fueling demand for processed yet nutritious frozen alternatives.

Besides, governments across the region are investing in infrastructure development, particularly in cold storage facilities and refrigerated transport systems. These efforts are improving product availability and reducing spoilage rates. There is a rise in concerns about food safety and traceability, which has led frozen foods to gain traction as they offer better control over contamination risks compared to fresh produce in certain markets.

MARKET DRIVERS

Rapid Urbanization and Changing Lifestyles

The rapid pace of urbanization and the corresponding shift in consumer lifestyles are driving the Asia Pacific frozen food market. As more people migrate to cities in search of employment and better living standards, traditional home-cooked meal routines are being replaced by fast-paced, convenience-driven eating habits. This urban expansion has led to increased participation of women in the workforce, longer working hours, and reduced time for meal preparation. Like, in India, there is a steady increase in white-collar job opportunities in metropolitan cities, further boosting demand for time-saving food solutions such as frozen meals. Moreover, the influence of Western dietary patterns, especially among younger demographics, has contributed to the popularity of frozen snacks, pizzas, and desserts. In Japan and South Korea, frozen food is not only seen as convenient but also as a way to preserve seasonal ingredients without compromising quality. This socio-economic transformation across the region is significantly driving the growth of the frozen food market in the Asia Pacific.

Advancements in Cold Chain Infrastructure

The substantial progress in cold chain infrastructure, which ensures the safe transportation and storage of perishable food products, is also propelling the growth of the Asia Pacific frozen food market. A robust cold chain network reduces spoilage, maintains product quality, and extends shelf life, which enhances consumer confidence in frozen food products. According to the Asian Development Bank (ADB), investments in cold storage and refrigerated transport in the Asia Pacific region are rising, supporting the expansion of frozen food supply chains.

In India, the Ministry of Food Processing Industries launched the Pradhan Mantri Kisan Sampada Yojana (PMKSY) to modernize food processing infrastructure, including cold storage facilities. This expansion has enabled manufacturers to distribute frozen foods more efficiently, even to remote regions. China has also made significant strides in cold chain development, with the country’s cold storage capacity expanded in recent years. Also, e-commerce platforms like Alibaba and JD.com have integrated frozen food delivery into their services, leveraging advanced cold chain logistics to ensure product integrity. These infrastructural improvements are playing a pivotal role in expanding the reach and acceptance of frozen food across the Asia Pacific region.

MARKET RESTRAINTS

Consumer Preference for Fresh Food Products

The deeply ingrained consumer preference for fresh food products, particularly in traditional culinary cultures, is one of the key restraints affecting the growth of the Asia Pacific frozen food market. Across many countries in the region, including India, Vietnam, and parts of China, there is a strong cultural emphasis on consuming freshly prepared meals using locally sourced ingredients. Also, households in rural Asia still rely heavily on daily visits to local markets for fresh produce rather than purchasing frozen or packaged alternatives. This preference is reinforced by perceptions that frozen foods are less nutritious, lack authentic taste, and may contain preservatives or artificial additives. Moreover, misinformation and a lack of awareness regarding freezing technology hinder market expansion. Many consumers associate frozen food with lower-quality offerings, especially in lower-income segments where affordability often drives purchasing decisions. In response, industry players are launching educational campaigns and introducing premium frozen lines that emphasize natural ingredients and minimal processing.

High Energy Costs and Regulatory Compliance in Cold Storage

The high energy costs associated with maintaining cold storage facilities and complying with stringent regulatory standards are another significant constraint on the Asia Pacific frozen food market. Freezing and preserving food requires continuous refrigeration, which leads to substantial electricity consumption and operational expenses. In countries like Thailand and Malaysia, where ambient temperatures are consistently high, maintaining optimal freezer conditions increases power demand and operational complexity. Regulatory compliance adds another layer of difficulty, particularly in emerging markets where enforcement mechanisms are evolving. In India, the Food Safety and Standards Authority of India (FSSAI) introduced updated hygiene and labeling norms in 2023, requiring frozen food manufacturers to meet enhanced quality benchmarks. While these measures ensure product safety, they also raise entry barriers for small-scale producers who struggle to invest in compliant infrastructure. These economic and regulatory challenges pose ongoing difficulties for market expansion in the Asia Pacific frozen food industry.

MARKET OPPORTUNITIES

Rising Demand for Health-Conscious and Organic Frozen Products

The growing demand for health-conscious and organic frozen products presents a significant opportunity within the Asia Pacific frozen food market. As consumers become more aware of nutrition and wellness, there is a shift toward frozen foods that offer clean labels, minimal processing, and organic ingredients. In countries like Japan and South Korea, where food safety and quality are paramount, organic frozen vegetables and plant-based meals have gained considerable traction. Also, Japan is experiencing an increase in certified organic frozen food sales, which is driven by consumer demand for chemical-free and sustainable products. India is also witnessing a surge in demand for nutrient-rich frozen meals, particularly among millennials and fitness enthusiasts. Companies like Nestlé and ITC have responded by launching fortified frozen lines targeting health-conscious consumers. Awareness continues to grow, and the health-oriented segment presents a lucrative avenue for expansion in the Asia Pacific frozen food market.

Expansion of E-Commerce and Online Grocery Platforms

The rapid expansion of e-commerce and online grocery platforms is another transformative opportunity for the Asia Pacific frozen food market. Digital retail channels have revolutionized the way consumers purchase groceries, offering convenience, doorstep delivery, and a wider variety of frozen food options. In China, e-commerce giants such as Alibaba, JD.com, and Pinduoduo have invested heavily in cold chain logistics to support the distribution of frozen products. Similarly, in India, digital marketplaces like BigBasket, Amazon Fresh, and Blinkit have expanded their frozen food sections, leveraging last-mile delivery networks to maintain product integrity. South Korea has also embraced digital frozen food retail, with leading platforms like Market Kurly and Coupang Fresh enhancing their frozen product portfolios.

MARKET CHALLENGES

Perishability and Quality Concerns During Transportation

The risk of product degradation during transportation due to logistical inefficiencies and fluctuating temperatures is a major challenge facing the Asia Pacific frozen food market. Maintaining a consistent cold chain is crucial for preserving the quality, texture, and nutritional content of frozen foods. However, in many parts of the region, especially in rural and island nations, inadequate refrigerated transport infrastructure leads to frequent disruptions. According to the World Bank Logistics Performance Index (LPI) 2023, several Southeast Asian countries scored below the global average in cold chain reliability, impacting the timely delivery of frozen goods. In Indonesia, for instance, where the archipelago consists of thousands of islands, transporting frozen products to remote locations poses significant hurdles. Moreover, power outages in developing economies further exacerbate the problem. These logistical constraints not only affect product quality but also erode consumer confidence in frozen food brands.

Price Sensitivity and Affordability in Lower-Income Segments

Price sensitivity and affordability present a significant challenge for the Asia Pacific frozen food market, particularly in lower-income segments where consumers prioritize cost-effective alternatives over convenience. Despite the growing trend of urbanization and lifestyle changes, many households in developing economies continue to rely on fresh, locally sourced ingredients due to budgetary constraints. In countries like Bangladesh, Nepal, and parts of rural India, frozen food remains a luxury rather than a necessity. Furthermore, price fluctuations in raw materials, packaging, and logistics add to the final retail cost of frozen products.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.76% |

| Segments Covered | By Product, User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, And the Rest Of Asia-Pacific |

| Market Leaders Profiled | Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg’s Company, Nestle S.A., and Flower Foods |

SEGMENTAL ANALYSIS

By Product Insights

The frozen seafood segment prevailed in the Asia Pacific frozen food market by accounting for 28.3% of total market revenue in 2025. The APAC's rich maritime resources, high seafood consumption rates, and extensive export-import trade dynamics are mainly driving the growth of the frozen seafood segment. Countries such as China, Japan, India, and Indonesia are among the world’s top producers and consumers of seafood, with freezing being a critical preservation method due to the perishable nature of aquatic products. Also, Asia contributes over 70% of global fish production, with a notable share of it being exported or processed into frozen formats. Moreover, seafood plays a central role in traditional diets across the region, especially in coastal communities where fresh catch may not always be available. The expansion of cold chain infrastructure has further enabled year-round availability of premium frozen fish, shrimp, and shellfish. In addition, rising health consciousness has increased demand for protein-rich seafood alternatives to red meat.

The frozen ready meals segment is projected to grow at the fastest rate and is likely to rise at a CAGR of 9.6% in the coming years. This rapid growth of the frozen ready meals segment is primarily fueled by shifting consumer lifestyles, increasing urbanization, and the rising preference for convenient meal solutions. In countries like South Korea, Japan, and Australia, where dual-income households and fast-paced work schedules are common, frozen ready meals have become an essential part of daily life. According to the Asian Development Bank (ADB), disposable incomes in the Asia Pacific region grew steadily over the past decade, enabling more consumers to spend on time-saving food options. Moreover, manufacturers have expanded their offerings to include healthier and culturally adapted variants such as paneer tikka, teriyaki chicken, and plant-based dumplings, catering to regional tastes while maintaining convenience. E-commerce platforms like Alibaba, BigBasket, and Coupang have further boosted accessibility through efficient frozen food delivery systems.

By User Insights

The retail sector commanded the Asia Pacific frozen food market by capturing 63.1% of total consumption in 2025. This expansion of the retail sector is largely driven by the growing penetration of modern grocery retail formats, including supermarkets, hypermarkets, and convenience stores, which offer a wide variety of frozen products to end consumers. Urbanization and rising household incomes have significantly influenced consumer purchasing behavior, particularly in emerging economies such as China, India, and Vietnam. Moreover, the rise of private-label frozen brands and promotional campaigns by retailers has made these products more accessible and affordable to a broader consumer base. Also, e-commerce platforms such as Amazon Fresh, BigBasket, and JD.com have played a crucial role in expanding retail distribution by offering home delivery of frozen items. These developments show the continued prowess of the retail segment in the Asia Pacific frozen food market.

The foodservice industry is expected to grow at the fastest pace, registering a CAGR of 9.1%. This growth of the foodservice industry is driven by the rapid expansion of quick-service restaurants (QSRs), cloud kitchens, and institutional catering services across the Asia Pacific region. As the hospitality sector rebounds post-pandemic, there is a growing reliance on frozen ingredients to ensure consistency, reduce preparation time, and maintain cost efficiency. Like, QSR chains in Southeast Asia expanded in recent years, with major players such as McDonald’s, KFC, and Domino’s increasingly sourcing frozen patties, nuggets, pizzas, and sauces to streamline operations. Furthermore, hotels, airlines, and hospitals are adopting frozen meal solutions to manage large-scale food preparation without compromising quality.

REGIONAL ANALYSIS

China Frozen Food Market Insights

China spearheaded the Asia Pacific frozen food market by contributing 32.3% of regional revenue in 2025. The country's dominant position is supported by its massive population, well-developed food processing industry, and growing consumer preference for convenience foods amid rapid urbanization. The Chinese frozen food market has also benefited from strong government support for cold chain infrastructure development. Moreover, the rise of e-commerce giants like Alibaba and Meituan has revolutionized frozen food logistics, ensuring last-mile delivery even in remote areas. In addition, the country remains a major exporter of frozen seafood and vegetables, particularly to Southeast Asia and Europe.

Japan Frozen Food Market Insights

Japan contributes significantly to the Asia Pacific frozen food market. The country’s mature food industry, coupled with a culture of convenience and high-quality food standards, has fostered widespread adoption of frozen products across households and commercial sectors. This reflects a long-standing consumer trust in frozen food safety and nutritional value, particularly for seafood, vegetables, and ready-to-eat meals. In addition, Japan’s aging population and shrinking household sizes have led to increased demand for portion-controlled, easy-to-prepare frozen dishes. The country's advanced cold chain infrastructure ensures minimal product degradation during transportation and storage. Moreover, major food companies such as Ajinomoto, Nichirei, and Maruha Nichiro continue to innovate with premium frozen lines, including organic and functional food options. These factors sustain Japan’s strong presence in the Asia Pacific frozen food market.

India Frozen Food Market Insights

India is emerging as a key growth engine in the Asia Pacific frozen food market due to rising disposable incomes, changing dietary habits, and expanding retail infrastructure. Though traditionally reliant on fresh produce, the country is transforming food consumption patterns, particularly in urban centers. Urbanization has played a pivotal role, with over 30% of the population now residing in cities, where time constraints and dual-income households encourage the use of convenience foods. Also, the Indian government has been investing in cold chain infrastructure under initiatives like the Pradhan Mantri Kisan Sampada Yojana (PMKSY). Furthermore, multinational brands like Nestlé and local players such as ITC and Godrej have launched frozen meal lines tailored to Indian palates. These developments position India as a rapidly evolving hub within the Asia Pacific frozen food market.

Australia Frozen Food Market Insights

Australia adds notably to the Asia Pacific frozen food market, which is driven by high consumer awareness, a well-established food processing industry, and a growing preference for healthy frozen options. The country's market is characterized by premium product offerings, strong regulatory oversight, and a mature cold chain network. The shift toward clean eating and fitness-conscious lifestyles has spurred demand for organic and low-calorie frozen meals. In addition, Australia's foodservice industry, including cafes, restaurants, and airline catering, relies heavily on frozen ingredients for operational efficiency. Moreover, e-commerce platforms such as Woolworths Online and Coles Express have integrated frozen food delivery into their services, improving accessibility.

South Korea Frozen Food Market Insights

South Korea is distinguished by its high-tech food industry, strong brand loyalty, and innovative product development. The country’s frozen food sector benefits from a highly urbanized population, well-developed logistics networks, and a culture that embraces convenience-driven consumption. The rise of single-person households and busy work schedules has further accelerated demand for portion-controlled, easy-to-prepare frozen meals. Moreover, South Korean brands such as CJ CheilJedang and Ottogi have introduced premium frozen lines with extended shelf life and enhanced flavor profiles. The country’s e-commerce sector, led by platforms like Coupang and Market Kurly, has also boosted frozen food accessibility.

LEADING PLAYERS IN THE ASIA PACIFIC FROZEN FOOD MARKET

One of the leading players in the Asia Pacific frozen food market is Nestlé S.A., a Swiss multinational corporation with a strong regional presence. Nestlé offers a diverse portfolio of frozen meals, vegetables, and seafood, tailored to local tastes across Asian markets. The company's emphasis on product innovation, brand trust, and sustainability has enabled it to capture a wide consumer base, particularly in India, China, and Southeast Asia.

Another key player is CJ CheilJedang, a South Korean conglomerate known for its high-quality frozen convenience foods. CJ has built a reputation for blending traditional Korean flavors with modern frozen food technology. Its expansion into neighboring markets and strategic partnerships with retail and foodservice chains have solidified its influence in the region’s frozen food landscape.

Ajinomoto Co., Inc., a Japanese food and biotechnology company, also holds a prominent position. Ajinomoto focuses on health-conscious frozen meals and ingredients, leveraging its expertise in amino acid science to enhance flavor and nutrition. With a strong distribution network and commitment to quality, the company plays a vital role in shaping frozen food consumption trends across Asia.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Asia Pacific frozen food market employ several strategic approaches to reinforce their competitive edge. One major strategy is product diversification and localization, where companies develop region-specific frozen offerings that align with local culinary preferences while maintaining nutritional value and convenience.

Another crucial approach is expanding digital and e-commerce presence, as leading brands collaborate with online grocery platforms and invest in home delivery infrastructure to meet the growing demand for convenient frozen food access among urban consumers.

Lastly, strategic partnerships and supply chain optimization play a pivotal role in strengthening market positions. Companies are forming alliances with cold storage providers, logistics firms, and retail chains to ensure efficient product distribution and maintain quality throughout the cold chain.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Asia Pacific Frozen Food Market include Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg’s Company, Nestle S.A., and Flower Foods.

The competition in the Asia Pacific frozen food market is characterized by a mix of global giants and well-established regional players vying for dominance through innovation, branding, and supply chain efficiency. While international companies like Nestlé and Ajinomoto bring technological expertise and global experience, domestic manufacturers tailor products to local tastes and cultural preferences, creating a dynamic and fragmented marketplace. Consumer awareness regarding health, convenience, and food safety is reshaping purchasing behaviors, prompting brands to continuously evolve their product lines. The rise of organized retail and e-commerce has further intensified competition, as companies seek to expand their reach and improve last-mile delivery capabilities. Also, the growing emphasis on sustainability and clean labeling has pushed manufacturers to reformulate products and adopt eco-friendly packaging solutions.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Nestlé launched a new line of plant-based frozen meals across multiple Asia Pacific markets, targeting health-conscious consumers and expanding its sustainable food offerings in response to rising demand for alternative proteins.

- In May 2023, CJ CheilJedang entered into a strategic partnership with a leading Indonesian supermarket chain to increase shelf space for its frozen dumplings and ready-to-cook meals, aiming to strengthen its retail footprint in Southeast Asia.

- In September 2023, Ajinomoto introduced an upgraded frozen soup range in Japan featuring reduced sodium content and natural preservatives, reinforcing its commitment to health-focused product development and catering to aging demographics.

- In February 2025, Simplot Australia, a major frozen food processor, expanded its cold storage facilities in Queensland to enhance supply chain resilience and support growing export demand from neighboring Pacific nations.

- In March 2025, Godrej Foods launched a budget-friendly frozen meal series in India under a new sub-brand, targeting middle-income households and leveraging digital marketing to drive awareness and trial adoption.

MARKET SEGMENTATION

This research report on the Asia Pacific Frozen Food Market has been segmented and sub-segmented based on product, user, and region.

By Product

- Frozen Ready Meals

- Meat & Poultry

- Seafood

- Vegetables & Fruits

- Potatoes

- Soup

By User

- Retail

- Foodservice Industry

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

1. What factors are driving the growth of the APAC frozen food market?

Urbanization, busy lifestyles, rising disposable incomes, and growing demand for convenient food options are major growth drivers.

2. What are the major product categories in the frozen food market?

Major categories include frozen ready meals, frozen meat and seafood, frozen fruits and vegetables, frozen bakery products, and frozen snacks.

3. Why are frozen foods becoming popular in APAC?

Consumers prefer frozen foods because of their convenience, longer shelf life, easy storage, and reduced food wastage.

4. Which distribution channels are important in the market?

Supermarkets, hypermarkets, convenience stores, online grocery platforms, and specialty food stores are major distribution channels.

5. What role does cold chain infrastructure play in the market?

Efficient cold chain logistics help maintain product quality, freshness, and safety during transportation and storage.

6. What challenges does the frozen food market face?

High cold storage costs, supply chain disruptions, and consumer concerns regarding preservatives are key challenges.

7. What trends are shaping the APAC frozen food market?

Plant-based frozen foods, premium ready-to-eat meals, sustainable packaging, and clean-label products are major trends.

8. Which sector is a major consumer of frozen foods?

The retail and foodservice sectors, including restaurants and hotels, are major consumers of frozen food products.

9. How are manufacturers innovating in the frozen food market?

Manufacturers are introducing healthier recipes, regional flavors, advanced freezing technologies, and eco-friendly packaging solutions.

10. What is the future outlook for the APAC frozen food market?

The market is expected to witness strong growth due to increasing urbanization, expanding cold chain networks, and rising demand for convenient food products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com