Asia Pacific Oil-Free Air Compressor Market Size, Share, Trends & Growth Forecast Report By Product (Stationary, Portable), Technology (Reciprocating, Rotary/Screw, Centrifugal), Power Rating, Application, and Country (India, China, Japan, South Korea, Australia) – Industry Analysis From 2025 to 2033.

Asia Pacific Oil-Free Air Compressor Market Size

The size of the Asia Pacific oil-free air compressor market was worth USD 3.27 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 5.76% from 2025 to 2033 and be worth USD 5.41 billion by 2033 from USD 3.46 billion in 2025.

Oil-free air compressors are engineered to eliminate the use of lubricants, ensuring zero oil carryover in the output air, which is essential for sensitive applications.

MARKET DRIVERS

Stringent Regulatory Standards

Stringent regulatory standards governing air quality and product safety have emerged as a primary driver for the oil-free air compressor market in Asia Pacific. According to the International Organization for Standardization (ISO), industries such as pharmaceuticals and food & beverage must comply with ISO 8573-1 Class 0 certification, which mandates zero oil contamination in compressed air. This regulation has compelled manufacturers to adopt oil-free compressors to ensure compliance. Also, the growing emphasis on environmental protection has led governments in the region to enforce stricter emission norms. As per the United Nations Environment Programme, carbon emissions from industrial activities in Asia Pacific are expected to decline by 2030, thanks to the adoption of cleaner technologies like oil-free compressors.

Rising Demand in the Pharmaceutical Sector

The pharmaceutical sector’s rapid expansion in Asia Pacific serves as a significant driver for the oil-free air compressor market. According to the Also, the region’s pharmaceutical market is projected to grow significantly, driven by increasing healthcare investments and a growing aging population. Oil-free compressors play a crucial role in processes such as drug formulation, packaging, and sterilization, where purity is paramount. For example, Biocon Malaysia adopted advanced oil-free compressors in its bioprocessing facilities, achieving an improvement in production efficiency in 2023. Besides, the rise of personalized medicine and biologics has increased the demand for precision tools that ensure contamination-free operations. The biopharmaceutical sector in Asia Pacific is expected to double its production capacity by 2030, further amplifying the need for reliable oil-free air solutions.

MARKET RESTRAINTS

High Initial Costs and Maintenance Expenses

One of the key restraints affecting the oil-free air compressor market in Asia Pacific is the high initial cost of procurement and ongoing maintenance expenses. According to Deloitte Global, the capital expenditure required for installing oil-free compressors can be prohibitive for small and medium-sized enterprises (SMEs), particularly in emerging economies like Vietnam and Indonesia. These costs include not only the purchase price but also expenses related to calibration, software integration, and training personnel. In addition, the complexity of oil-free compressors often necessitates specialized maintenance, which can strain operational budgets.

Limited Awareness and Technical Expertise

Another significant restraint is the lack of awareness and technical expertise regarding the optimal use of oil-free air compressors. As per the United Nations Industrial Development Organization, many industrial facilities in rural areas of Asia Pacific lack access to training programs and technical resources needed to operate advanced oil-free compressors effectively. This knowledge gap often leads to suboptimal performance or premature equipment failure, discouraging further investment. Besides, the absence of standardized guidelines for oil-free compressor usage across industries exacerbates the problem, making it challenging for manufacturers to adopt best practices.

MARKET OPPORTUNITIES

Integration with Industry 4.0 Technologies

The integration of oil-free air compressors with Industry 4.0 technologies presents a transformative opportunity for the Asia Pacific market. Moreover, the adoption of smart manufacturing solutions in the region is expected to rise notably, driven by advancements in IoT, artificial intelligence, and data analytics. Oil-free compressors equipped with real-time monitoring and predictive maintenance capabilities can significantly enhance operational efficiency and reduce downtime. Furthermore, the ability to integrate these compressors with cloud-based platforms enables remote monitoring and control, making them ideal for decentralized industrial operations.

Growth in Renewable Energy Applications

The renewable energy sector offers immense potential for the oil-free air compressor market, particularly in hydrogen fuel production and solar panel manufacturing. According to the International Renewable Energy Agency, hydrogen production capacity in Asia Pacific is projected to increase fivefold by 2030, driven by government initiatives to transition to clean energy sources. Oil-free compressors are critical in hydrogen electrolysis processes, where precise air flow control ensures optimal efficiency and safety. Similarly, in solar panel manufacturing, oil-free compressors are used to regulate air flows during thin-film deposition, enhancing product quality. For example, First Solar, a leading solar panel manufacturer, attributes a 15% improvement in production efficiency to the use of advanced oil-free compressors.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages have emerged as critical challenges impacting the oil-free air compressor market. Like, the global semiconductor shortage in 2023 adversely affected the production of electronic components used in oil-free compressors, leading to delays in delivery and increased costs. For instance, manufacturers in South Korea faced an increase in lead times for key components such as sensors and microcontrollers. Furthermore, geopolitical tensions and trade restrictions have exacerbated supply chain vulnerabilities, particularly for imported components. Companies like Ingersoll Rand have reported a decline in production capacity due to unreliable supply chains.

Intense Competition and Price Wars

The Asia Pacific oil-free air compressor market is highly competitive, with numerous players vying for market share. For instance, Sullair disrupted the market in 2022 by launching budget-friendly oil-free compressors priced lower than competitors. While this strategy attracts cost-sensitive consumers, it exerts downward pressure on profit margins for premium brands. In addition, the entry of Chinese manufacturers into Southeast Asia has further fragmented the market, making it challenging for incumbents to differentiate their offerings.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Technology, Power Rating, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Atlas Copco AB; FS Elliot Co., LLC; Hanwha Power Systems CO., LTD.; Ingersoll Rand; Doosan Portable Power; Sullivan-Palatek Inc.; ELGi; Zen Air Tech Private Limited; Frank Technologies Pvt Ltd.; Hitachi Industrial Equipment Systems Co., Ltd.; CIASONS Industrial Inc.; Aerzen; ANEST IWATA Corporation, and others. |

SEGMENTAL ANALYSIS

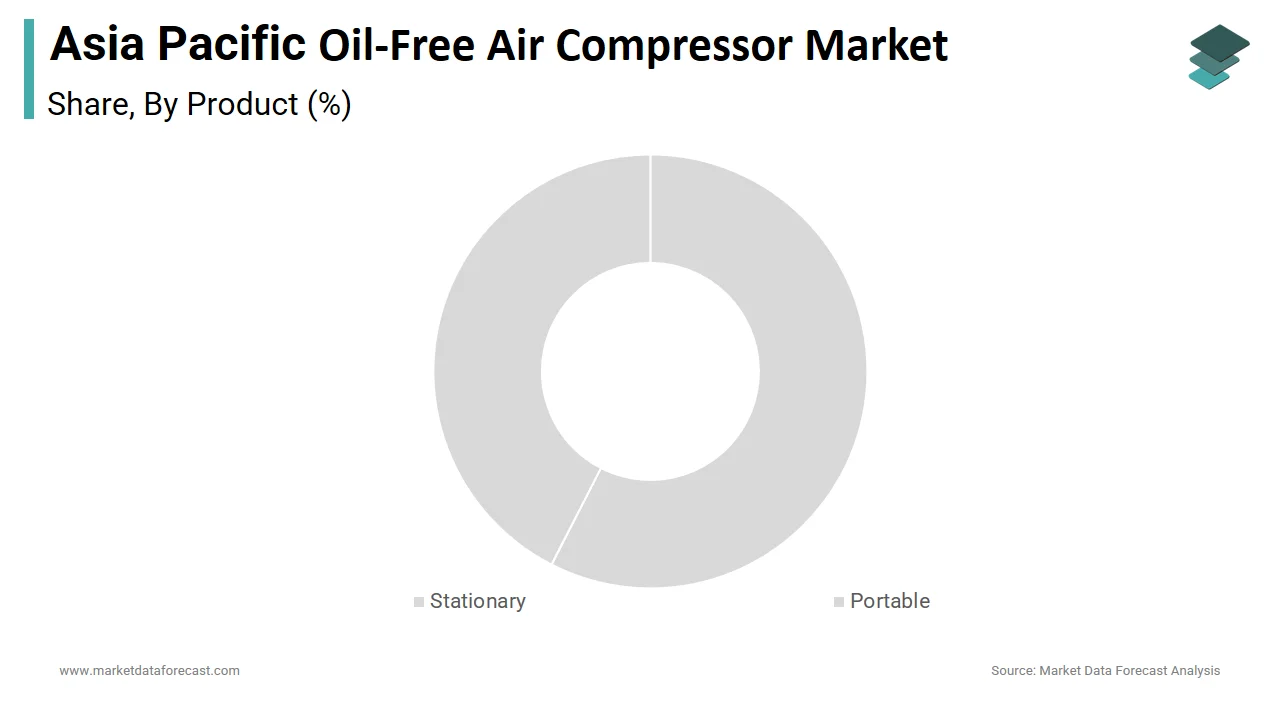

By Product Insights

The segment of stationary oil-free air compressors dominated the Asia Pacific market by holding a market share of a 60.8% in 2024. This leading position is driven by their widespread adoption in industries such as pharmaceuticals, food & beverage, and electronics manufacturing, where high-capacity, reliable air compression is essential. Also, a key factor behind this dominance is the increasing demand for contamination-free operations in large-scale industrial facilities. Moreover, the pharmaceutical sector in Asia Pacific accounts for considerable share of global production, necessitating stationary compressors for processes like drug formulation and packaging. Besides, the growing complexity of industrial processes has amplified the need for precision tools that ensure consistent performance. Another driving factor is the rising emphasis on energy efficiency, as stationary compressors are designed to minimize energy consumption while maintaining high output levels.

The segment of portable oil-free air compressors are the fastest-growing in the Asia Pacific market, with a projected CAGR of 8.5% through 2033. This rapid surge is caused by their versatility and suitability for applications in sectors such as construction, automotive repair, and field-based medical services. Additionally, the expansion of mobile healthcare services has increased the adoption of portable compressors. A further aspect is the growing trend toward decentralization in industrial operations, which necessitates flexible and mobile air compression solutions.

By Technology Insights

The rotary/screw oil-free air compressors segment accounted for the largest share of the Asia Pacific market, with a market share of 45.1% in 2024. This dominance is attributed to their efficiency, reliability, and ability to deliver continuous airflow, making them ideal for high-demand industrial applications. A significant point is the exponential growth of the semiconductor industry, which relies heavily on rotary/screw compressors for processes like wafer fabrication and cleanroom operations. Moreover, the increasing adoption of automation in manufacturing has bolstered demand for rotary/screw compressors. For instance, Toyota Motor Corporation integrated advanced rotary/screw compressors into its assembly lines, reducing energy consumption in 2023. One more aspect is the stringent environmental regulations governing emissions, which necessitate energy-efficient solutions.

The centrifugal oil-free air compressor segment is the swiftly advancing, with a CAGR of 9.2%. This expansion is propelled by their ability to deliver high airflow rates at low operational costs, making them suitable for large-scale applications in industries such as chemical processing, power generation, and water treatment. Also, investments in renewable energy projects in Asia Pacific are projected to grow annually, creating opportunities for centrifugal compressors in hydrogen production and biofuel refining. For example, Mitsubishi Heavy Industries installed centrifugal compressors in its hydrogen electrolysis plants, achieving an improvement in operational efficiency in 2023. Apart from these, the expansion of wastewater treatment facilities has increased the adoption of centrifugal compressors.

By Power Rating Insights

The oil-free air compressors with a power rating below 15kW held the biggest market share of a 50.4% in 2024. This top performace is propelled by their widespread use in small and medium-sized enterprises (SMEs) across industries such as food & beverage, pharmaceuticals, and electronics manufacturing. A main factor is the growing emphasis on process optimization in SMEs, which require cost-effective yet efficient air compression solutions. According to the Food and Agriculture Organization, the food processing sector in Asia Pacific is expanding at a rate of 8.8% annually, creating significant demand for low-power compressors in packaging and preservation. Additionally, the increasing focus on sustainability has led to the adoption of energy-efficient compressors, particularly in urban areas.

The segment of oil-free air compressors with a power rating between 55kW and 160kW is quickly emerging, with a CAGR of 10.5%. This advancement is credited to their suitability for medium to large-scale industrial applications, including chemical processing, oil & gas, and power generation. For example, Reliance Industries adopted 55-160kW compressors in its petrochemical plants, achieving a reduction in operational costs in 2023. Also, the expansion of renewable energy projects, such as biofuel production, has increased the adoption of these compressors. The International Renewable Energy Agency notes that biofuel production capacity in the region is expected to double by 2030, further accelerating demand for advanced flow control solutions.

By Application Insights

The pharmaceutical industry represented the prominent application segment in the Asia Pacific oil-free air compressor market by accounting for a 35.8% of total demand in 2024. This dominance is driven by the region’s position as a global leader in pharmaceutical manufacturing. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), Asia Pacific produced over 30% of the world’s pharmaceuticals in 2023, with oil-free compressors playing a critical role in ensuring process purity. A basic point is the increasing complexity of drug formulation, which requires advanced air compression solutions for processes like sterilization and packaging. Moreover, the proliferation of personalized medicine and biologics has heightened the need for precision tools that ensure contamination-free operations.

The semiconductor & electronics sector is the fastest-growing application segment in the Asia Pacific oil-free air compressor market, with a CAGR of 11.2%. This progress is fueled by the increasing demand for precision instruments in semiconductor fabrication, cleanroom operations, and electronics assembly. Additionally, the rise of 5G networks, IoT devices, and electric vehicles has spurred investments in semiconductor manufacturing facilities, further amplifying demand for oil-free compressors.

COUNTRY LEVEL ANALYSIS

China was at the forefront of the Asia Pacific oil-free air compressor market by accounting for a 30.5% of regional sales in 2024. The country’s dominance is caused by its robust manufacturing base, particularly in the semiconductor and chemical industries. In addition, the Chinese government’s push for technological self-reliance has spurred investments in domestic semiconductor manufacturing, further boosting the adoption of oil-free compressors. For instance, SMIC reported an increase in production capacity after integrating state-of-the-art oil-free compressors in 2023.

Japan marks significant progress in the market. The country’s position is attributed to its strong presence in high-tech industries such as semiconductors, automotive, and pharmaceuticals. Like, Japanese manufacturers invest heavily in automation and precision technologies, driving demand for oil-free compressors. For example, Toyota Motor Corporation adopted advanced oil-free compressors in its hydrogen fuel cell production lines, achieving an improvement in efficiency.

South Korea holds a notable market share which is supported by its world-class semiconductor and electronics industries. Also, the country is home to leading semiconductor giants like Samsung and SK Hynix, which rely heavily on oil-free compressors for fabrication processes. Additionally, the government’s focus on green energy has increased the adoption of oil-free compressors in hydrogen production and carbon capture projects.

India is exhibiting a descent rise in the market and is propelled by its rapidly expanding pharmaceutical and chemical industries. According to the Indian Pharmaceutical Alliance, the country is the largest producer of generic drugs globally, creating significant demand for precise air compression solutions. Also, government initiatives like “Make in India” have encouraged local manufacturing, further boosting the adoption of oil-free compressors.

Australia & New Zealand collectively hold a considerable market that is supported by their strong focus on renewable energy and water treatment. Additionally, the region’s strict environmental regulations have driven demand for precise flow control solutions.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC oil-free air compressor market profiled in this report are Atlas Copco AB; FS Elliot Co., LLC; Hanwha Power Systems CO., LTD.; Ingersoll Rand; Doosan Portable Power; Sullivan-Palatek Inc.; ELGi; Zen Air Tech Private Limited; Frank Technologies Pvt Ltd.; Hitachi Industrial Equipment Systems Co., Ltd.; CIASONS Industrial Inc.; Aerzen; ANEST IWATA Corporation, and others.

TOP LEADING PLAYERS IN THE MARKET

Atlas Copco

Atlas Copco is a global leader in the oil-free air compressor market, renowned for its innovative solutions tailored to industries such as pharmaceuticals, food & beverage, and electronics. The company’s contribution to the global market lies in its ability to deliver cutting-edge, energy-efficient compressors that meet stringent air quality standards. Atlas Copco has consistently focused on integrating smart technologies like IoT and predictive maintenance into its products, enabling real-time monitoring and enhanced operational efficiency.

Ingersoll Rand

Ingersoll Rand is a key player in the oil-free air compressor market, offering a diverse portfolio of products designed for applications in gas and liquid flow control. The company’s global influence stems from its commitment to sustainability and reliability, particularly in industries like semiconductor manufacturing, healthcare, and renewable energy. Ingersoll Rand has played a pivotal role in advancing oil-free compressor technology, addressing the growing demand for zero-contamination solutions.

Sullair

Sullair has established itself as a trusted name in the oil-free air compressor market, leveraging its expertise in precision engineering and energy-efficient designs. The company’s global impact is evident in its ability to provide high-performance compressors for demanding applications in construction, automotive, and chemical processing. Sullair’s focus on innovation has led to advancements in portable and stationary oil-free compressors, catering to the region’s growing emphasis on green technologies.

TOP STRATEGIES USED BY KEY PLAYERS IN THE MARKET

Product Innovation and Customization

Key players in the Asia Pacific oil-free air compressor market are heavily investing in research and development to introduce innovative products tailored to specific industry needs. Companies like Atlas Copco and Ingersoll Rand have focused on enhancing the efficiency and versatility of their compressors, particularly for applications in semiconductor fabrication and renewable energy.

Strategic Partnerships and Collaborations

To strengthen their market presence, leading companies are forming strategic partnerships with regional manufacturers and technology firms. For instance, collaborations with semiconductor giants and renewable energy projects allow brands to integrate their compressors into larger ecosystems, enhancing value for end-users.

Expansion of Regional Footprint

Another major strategy involves expanding manufacturing and distribution networks across Asia Pacific. Players like Sullair and Gardner Denver have established local facilities and partnered with distributors to improve accessibility and reduce lead times.

COMPETITION OVERVIEW

The Asia Pacific oil-free air compressor market is characterized by intense competition, driven by the presence of global leaders like Atlas Copco, Ingersoll Rand, and Sullair, alongside emerging regional players. The market’s dynamics are shaped by the rapid industrialization and technological advancements in sectors such as semiconductors, chemicals, and renewable energy. Global players leverage their expertise in precision engineering and smart technologies to maintain dominance, while regional manufacturers focus on cost-effective solutions tailored to local needs. The growing emphasis on sustainability and process optimization has intensified rivalry, prompting companies to differentiate themselves through innovation and customization. Additionally, the rise of Industry 4.0 has created opportunities for integrating IoT-enabled compressors, further elevating competition.

RECENT MARKET DEVELOPMENTS

- In April 2024, Atlas Copco launched a next-generation AI-driven oil-free compressor system in Japan. This innovation aimed to enhance process efficiency in cleanroom operations and solidify Atlas Copco’s leadership in precision air compression solutions.

- In July 2023, Ingersoll Rand partnered with a renewable energy firm in Australia to develop advanced oil-free compressors for hydrogen fuel production. This collaboration positioned Ingersoll Rand as a key enabler of clean energy technologies in the region.

- In September 2023, Sullair expanded its manufacturing facility in India to meet the rising demand for low-power oil-free compressors in the pharmaceutical and chemical industries. This move strengthened Sullair’s supply chain and market presence in South Asia.

- In November 2022, Gardner Denver acquired a local distributor in South Korea to streamline its distribution network and improve customer accessibility. This acquisition enhanced Gardner Denver’s ability to serve the Korean industrial market effectively.

- In February 2024, Kaishan Group introduced a smart oil-free compressor system with IoT integration for water treatment applications in Southeast Asia. This launch addressed the region’s growing focus on sustainable infrastructure and process optimization.

MARKET SEGMENTATION

This Asia Pacific oil-free air compressor market research report is segmented and sub-segmented into the following categories.

By Product

- Stationary

- Portable

By Technology

-

- Reciprocating

- Rotary/Screw

- Centrifugal

By Power Rating

-

- Below 15kW

- 15-55kW

- 55-160kW

- Above 160 kW

By Application

-

- Food & Beverage

- Pharmaceutical

- Semiconductor & electronics

- Chemical

- Oil & Gas

- Automotive

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What drives the Asia Pacific oil-free air compressor market?

The Asia Pacific oil-free air compressor market is driven by strict air quality regulations, rapid growth in pharmaceuticals and electronics, and increasing demand for contamination-free and energy-efficient solutions.

2. What challenges affect the Asia Pacific oil-free air compressor market?

The Asia Pacific oil-free air compressor market faces high initial costs, complex maintenance needs, limited technical expertise in rural areas, and supply chain disruptions impacting timely product delivery.

3. What opportunities exist in the Asia Pacific oil-free air compressor market?

Major opportunities in the Asia Pacific oil-free air compressor market include Industry 4.0 integration, adoption in renewable energy and hydrogen production, and rising demand for smart, IoT-enabled compressor solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com