Asia Pacific Orthopedic Biomaterial Market Size, Share, Trends & Growth Forecast Report By Material Type (Ceramics, Polymers, Metals, Others), Application (Joint Replacements, Spine Implants, Orthobiologics, Tissue Fixation, Others), and Country (India, China, Japan, South Korea, Rest of APAC) – Industry Analysis, 2026 to 2034

Market Size, 2025

$5,414 MnMarket Estimate, 2026

$5,928 MnMarket Forecast, 2034

$12,253 MnCAGR, 2026–2034

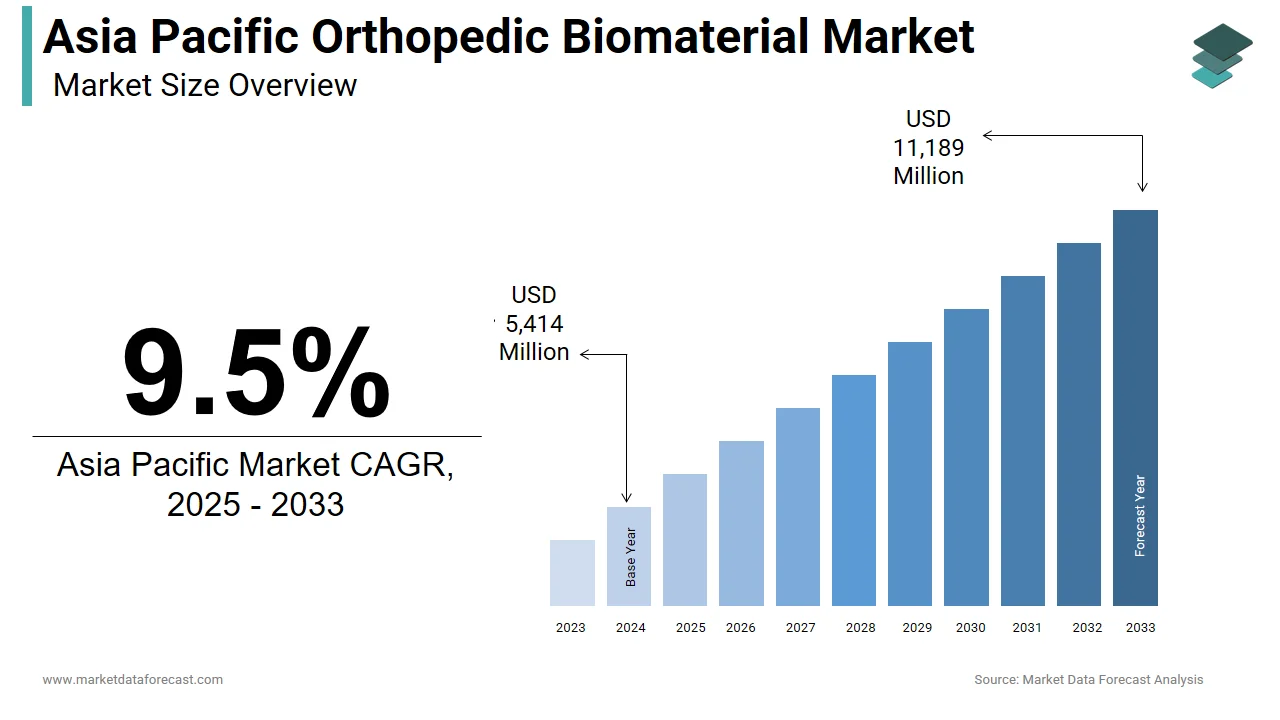

9.5%Asia Pacific Orthopedic Biomaterial Market Size

The size of the Asia Pacific orthopedic biomaterial market was worth USD 5,414 million in 2025. The regional market is anticipated to grow at a CAGR of 9.5% from 2026 to 2034 and be worth USD 12,253 million by 2034 from USD 5,928 million in 2026.

The Asia Pacific orthopedic biomaterial market encompasses a range of biocompatible materials used in the repair, replacement, or regeneration of musculoskeletal tissues such as bones, cartilage, and ligaments. These biomaterials include metals (e.g., titanium and stainless steel), polymers (e.g., ultra-high-molecular-weight polyethylene), ceramics (e.g., hydroxyapatite), and biologics (e.g., bone graft substitutes and growth factors). They are widely utilized in joint replacements, spinal implants, trauma fixation, and tissue engineering applications.

This market is being driven by the rising prevalence of musculoskeletal disorders, increasing geriatric population prone to osteoporotic fractures, and growing adoption of advanced implant technologies.

Additionally, improvements in healthcare infrastructure, coupled with rising medical tourism in countries like India, Thailand, and South Korea, have contributed to the demand for high-quality orthopedic biomaterials. Governments across the region are also promoting innovation in regenerative medicine and encouraging public-private partnerships to develop next-generation biomaterials tailored for local patient profiles. As per the Asia Pacific Orthopaedic Association, surgical interventions for orthopedic conditions have increased significantly, reinforcing the strategic importance of biomaterials in modern orthopedic care.

MARKET DRIVERS

Rising Prevalence of Musculoskeletal Disorders and Orthopedic Injuries

The increasing incidence of musculoskeletal disorders and orthopedic injuries, which necessitate surgical interventions involving implants and biomaterials, is one of the primary drivers of the Asia Pacific orthopedic biomaterial market. Conditions such as osteoarthritis, rheumatoid arthritis, osteoporosis, and sports-related injuries are becoming more prevalent due to sedentary lifestyles, obesity, and an aging population. With increasing awareness about minimally invasive procedures and better post-operative outcomes, the reliance on orthopedic biomaterials continues to grow, making this a key driver of market expansion across the Asia Pacific.

Technological Advancements in Biocompatible and Regenerative Materials

The rapid advancement in biocompatible and regenerative biomaterial technologies is a major factor driving the Asia Pacific orthopedic biomaterial market. Innovations such as bioactive ceramics, synthetic bone grafts, and 3D-printed implants are transforming orthopedic treatment approaches by offering enhanced integration with human tissue, reduced inflammation, and faster healing times.

Japan has been at the forefront of developing novel biomaterials, particularly in the field of bioactive glass and calcium phosphate-based scaffolds. Institutions like the Korea Advanced Institute of Science and Technology are actively involved in creating smart biomaterials that respond to mechanical stress and stimulate cellular regeneration.

India and China are also investing heavily in regenerative medicine, with startups and academic institutions exploring stem cell-integrated biomaterials for bone repair. These technological advancements are not only improving clinical outcomes but also expanding the application scope of orthopedic biomaterials across the Asia Pacific.

MARKET RESTRAINTS

High Cost of Advanced Orthopedic Biomaterials and Limited Reimbursement Coverage

The high cost associated with advanced biomaterials, including bioactive ceramics, titanium implants, and synthetic bone graft substitutes, is a significant restraint affecting the Asia Pacific orthopedic biomaterial market. These materials often come with premium pricing due to complex manufacturing processes, stringent regulatory requirements, and limited domestic production capabilities in several emerging economies. This financial burden discourages patients from opting for premium biomaterial-based implants, leading to continued reliance on lower-cost alternatives with potentially compromised performance.

Stringent Regulatory Requirements and Lengthy Approval Processes

The complexity and duration of regulatory approval processes across different countries is another critical challenge facing the Asia Pacific orthopedic biomaterial market. Unlike the United States or European Union, where regulatory frameworks are more standardized, the Asia Pacific consists of diverse jurisdictions with varying compliance standards, delaying product launches and market entry. In Southeast Asia, countries like Malaysia and Thailand have introduced stricter regulations aimed at ensuring product safety, but inconsistent enforcement and documentation requirements create additional hurdles for international manufacturers seeking regional expansion. Without greater harmonization of regulatory policies, these barriers will continue to impede market growth.

MARKET OPPORTUNITIES

Expansion of Regenerative Medicine and Tissue Engineering Applications

The growing integration of regenerative medicine and tissue engineering techniques presents a major opportunity in the Asia Pacific orthopedic biomaterial market. With advancements in stem cell therapy, bioengineered scaffolds, and growth factor delivery systems, there is a shift toward developing biomaterials that facilitate natural tissue regeneration rather than merely acting as passive implants. Leading research institutions such as Seoul National University Hospital are conducting clinical trials to assess the efficacy of biomaterial-assisted cartilage regeneration. Japan’s regenerative medicine sector has seen rapid progress, with companies like Terumo and Olympus collaborating with academic institutions to develop injectable hydrogels and bioactive matrices designed to accelerate bone healing.

Increasing Adoption of Additive Manufacturing and Patient-Specific Implants

The growing adoption of additive manufacturing (AM), commonly known as 3D printing, to produce patient-specific implants and customized orthopedic devices is an emerging opportunity in the Asia Pacific orthopedic biomaterial market. AM allows for the creation of complex geometries, porous structures, and personalized implant designs that enhance osseointegration and biomechanical compatibility. China has emerged as a leader in 3D-printed orthopedic implants, with companies such as Stryker and local players partnering with hospitals to offer customized spinal and craniofacial implants. South Korea and Singapore are also investing in digital orthopedics, leveraging AI-driven imaging and CAD modeling to design implants that match patient-specific biomechanical needs.

MARKET CHALLENGES

Limited Availability of Skilled Professionals and Training Infrastructure

The shortage of skilled professionals trained in the latest biomaterial applications and surgical techniques is one of the key challenges confronting the Asia Pacific orthopedic biomaterial market. The successful implementation of advanced orthopedic implants requires surgeons, biomedical engineers, and rehabilitation specialists who are proficient in handling cutting-edge biomaterials and understanding their biological interactions. In countries like Indonesia, the Philippines, and Nepal, the lack of specialized training centers and continuing medical education programs limits the adoption of sophisticated biomaterial-based implants. Moreover, in India and Vietnam, the disparity between urban and rural healthcare settings exacerbates the skill gap. Rural hospitals often rely on conventional surgical methods due to a lack of expertise in newer biomaterial technologies, resulting in suboptimal patient outcomes.

Post-Implantation Complications and Long-Term Biocompatibility Concerns

Concerns regarding post-implantation complications such as infection, wear debris generation, and long-term biocompatibility continue to pose challenges to the Asia Pacific orthopedic biomaterial market. Issues related to material degradation, immune response, and mechanical failure can lead to implant revision surgeries, increasing healthcare costs and reducing patient confidence in biomaterial-based treatments. In Japan, as per the Japanese Orthopaedic Association, approximately 5% of total joint replacement cases required revision within five years due to complications linked to implant wear and loosening. Similarly, in Australia, the Australian Orthopaedic Association’s National Joint Replacement Registry indicated that adverse reactions to certain metal-on-metal implants persisted despite regulatory scrutiny. In emerging markets, the situation is compounded by limited access to post-operative monitoring and diagnostic tools necessary for early detection of implant-related complications. As per a study published in the Indian Journal of Orthopaedics, inadequate follow-up care and limited awareness among patients about implant longevity contribute to higher failure rates in low-resource settings.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Zimmer Biomet, Stryker, DePuy Synthes Companies, Medtronic, Arthrex, Inc., NuVasive, Inc., Globus Medical, Inc., and others.. |

SEGMENT ANALYSIS

By Material Type Insights

The metals segment held the largest share of 38.1% of the overall market in 2024. Their superior mechanical strength, biocompatibility, and durability, making them ideal for load-bearing implants such as hip and knee prostheses, spinal fixation devices, and trauma fixation systems is driving the dominance of metals. The increasing prevalence of musculoskeletal disorders and rising geriatric population across the region are key contributors to this segment's growth. Additionally, advancements in metal alloys, such as titanium and cobalt-chromium, have enhanced implant longevity and reduced failure rates. Moreover, the expansion of healthcare infrastructure in emerging economies like India and China has led to increased access to advanced orthopedic treatments, further boosting metal-based biomaterial usage. The growing number of orthopedic surgical procedures, particularly in countries such as Japan and South Korea, has also contributed to the sustained demand for metallic implants.

The polymers segment is projected to grow at the fastest CAGR of around 7.2% during the forecast period. Advancements in biodegradable and bioresorbable polymer technologies, which are increasingly being used in applications such as orthobiologics and tissue fixation, are fuelling the rapid growth ofthe polymers segment. Unlike traditional materials, biodegradable polymers like polylactic acid (PLA) and polyglycolic acid (PGA) degrade naturally in the body after fulfilling their function, eliminating the need for secondary surgeries to remove implants. Additionally, the rising demand for minimally invasive surgeries (MIS) has further accelerated the adoption of polymer-based implants, especially in spinal and joint reconstruction procedures. The expansion of 3D printing technologies in medical device manufacturing has also enabled the production of customized polymer implants, enhancing patient outcomes. For example, in 2023, Japan-based companies such as Teijin Limited and Toray Industries invested heavily in R&D for advanced polymer composites used in orthopedic applications. Furthermore, increased healthcare spending and growing awareness about regenerative medicine in countries like India and South Korea are creating a favorable environment for polymer-based biomaterials.

By Application Insights

The joint replacements segment led the market by accounting for 35.5% of the Asia Pacific orthopedic biomaterial market in 2024. Rising incidence of osteoarthritis, rheumatoid arthritis, and osteoporosis, particularly in the aging population across the region, is largely attributed to the dominance of the joint replacements segment. Additionally, urbanization and sedentary lifestyles have contributed to an increase in obesity and related joint disorders, further driving demand for joint replacement surgeries. The expansion of private healthcare facilities and government initiatives to improve orthopedic care have also played a significant role in boosting this segment. For instance, India's National Health Mission (NHM) has been actively promoting affordable orthopedic treatments, including joint replacements, especially in rural areas. Moreover, technological advancements in implant materials, such as highly cross-linked polyethylene and ceramic-on-ceramic bearings, have improved implant longevity and reduced revision rates, further enhancing the adoption of joint replacement procedures. The presence of global orthopedic players like Zimmer Biomet, Stryker, and Johnson & Johnson in the region has also contributed to the availability of high-quality implants and surgical tools.

The orthobiologics segment is anticipated to grow at the fastest CAGR of around 8.1% between 2025 and 2033. Rising sports injuries and musculoskeletal trauma, especially in countries like India, China, and Australia, are propelling the surge ofthe orthobiologics segment. Orthobiologics, which include bone graft substitutes, growth factors, and platelet-rich plasma (PRP), are increasingly being used in spinal fusion, trauma repair, and sports injury recovery. Additionally, advancements in regenerative medicine, including stem cell therapy and tissue engineering, are opening new avenues for orthobiologic applications. For example, Japan has been at the forefront of regenerative medicine, with regulatory approvals for autologous cell therapies increasing significantly in recent years. The rising preference for minimally invasive procedures and shorter recovery times associated with orthobiologics has further boosted their adoption. In India, orthobiologic treatments have gained popularity in sports medicine clinics, with a 25% year-on-year increase in PRP therapy usage reported by the Indian Orthopaedic Association in 2023. Moreover, favorable reimbursement policies and government support for regenerative medicine research in countries like Australia and South Korea are accelerating market growth.

COUNTRY LEVEL ANALYSIS

China Orthopedic Biomaterial Market Insights

China led the Asia Pacific orthopedic biomaterial market by contributing 28.4% of the regional revenue in 2024. The country’s dominant position is driven by its aging population, rising prevalence of osteoarthritis and osteoporosis, and a surge in orthopedic surgeries. In China, over 100 million people in the country suffer from osteoporosis, with an estimated 7 million fractures annually, many of which require orthopedic implants. Additionally, urbanization and sedentary lifestyles have contributed to an increase in musculoskeletal disorders, further boosting demand for orthopedic biomaterials. The Chinese government has been actively investing in healthcare infrastructure, with over 40,000 orthopedic surgeries performed annually in Tier 1 cities like Beijing and Shanghai. Moreover, domestic players such as MicroPort and Vigon International have expanded their product portfolios to include advanced implants and biocompatible materials, reducing reliance on imported products. The growing presence of global orthopedic companies like Zimmer Biomet and Stryker has further enhanced the availability of high-quality biomaterials.

Japan Orthopedic Biomaterial Market Insights

Japan is also a major player in the Asia Pacific orthopedic biomaterial market. The country's strong market position is primarily due to its aging population, high healthcare expenditure, and advanced medical infrastructure. According to the Ministry of Health, Labour and Welfare, over 30% of Japan's population is aged 65 or older, making it one of the most aging societies globally. This demographic trend has led to a high incidence of osteoarthritis, fractures, and spinal disorders, driving demand for orthopedic implants and biomaterials. The country’s regulatory environment is also conducive to innovation, with the Pharmaceuticals and Medical Devices Agency (PMDA) facilitating faster approvals for advanced biomaterials and regenerative therapies. Companies like Terumo Corporation and Olympus have been actively involved in developing next-generation orthopedic biomaterials, including bioactive ceramics and polymer composites. Additionally, Japan's strong R&D ecosystem and government funding for regenerative medicine have positioned it as a leader in orthobiologics and tissue engineering.

India Orthopedic Biomaterial Market Insights

India is emerging in the Asia Pacific orthopedic biomaterial market. The country’s market is rapidly expanding due to rising awareness about orthopedic treatments, increasing healthcare expenditure, and a growing middle-class population with improved access to medical services. Additionally, urbanization and changing lifestyles have led to a higher incidence of osteoarthritis and spinal disorders, especially in metropolitan cities like Mumbai, Delhi, and Bengaluru. The Indian government has been actively promoting medical tourism, with orthopedic procedures being one of the most sought-after treatments by international patients. According to the Confederation of Indian Industry (CII), medical tourism in India generated over USD 9 billion in 2023, with orthopedics contributing significantly to this revenue. Moreover, local manufacturers such as Siora Surgicals and Integra LifeSciences India have been scaling up production of cost-effective implants and biomaterials, making orthopedic care more accessible.

South Korea Orthopedic Biomaterial Market Insights

South Korea holds a significant share of the Asia Pacific orthopedic biomaterial market and is positioning it as a technologically advanced and rapidly growing market in the region. The country benefits from high healthcare expenditure, a rapidly aging population, and a strong focus on innovation in medical devices. According to the Korean Ministry of Health and Welfare, South Korea’s population aged 65 and above reached 18.4% in 2023, leading to a significant increase in musculoskeletal disorders and orthopedic interventions. South Korea is also known for its strong regulatory framework and support for medical technology innovation, with Korea’s Ministry of Food and Drug Safety (MFDS) facilitating faster approvals for advanced biomaterials and orthopedic devices. Companies like Corentec and Hanil Medtech have been instrumental in developing high-quality implants and bioceramics for domestic and international markets. Additionally, South Korea is a leader in regenerative medicine, with government-backed initiatives to develop stem cell-based orthobiologics.

Australia Orthopedic Biomaterial Market Insights

Australia is reflecting its mature healthcare system, high per capita healthcare spending, and well-established orthopedic infrastructure. The country’s market is characterized by high patient awareness, advanced surgical techniques, and a growing aging population, which has led to increased demand for orthopedic implants and biomaterials. According to the Australian Institute of Health and Welfare, over 300,000 orthopedic procedures were performed in Australia in 2023, with a significant proportion involving joint replacements and spinal implants. The Australian government has been investing in healthcare modernization, with a focus on improving access to orthopedic care in both urban and rural areas. Additionally, Australia has a strong regulatory environment, with Therapeutic Goods Administration (TGA) ensuring the safety and efficacy of orthopedic biomaterials. The presence of global orthopedic companies like Stryker, Zimmer Biomet, and Medtronic has further enhanced the availability of high-quality implants and surgical tools. Moreover, Australia’s focus on regenerative medicine and orthobiologics, supported by research institutions like the University of Melbourne and Monash University, is expected to further drive innovation in the orthopedic biomaterial space.

COMPETITIVE LANDSCAPE

The Asia Pacific orthopedic biomaterial market is highly competitive, marked by the presence of both global leaders and emerging regional players striving to capture a larger market share. Established multinational corporations dominate due to their extensive product portfolios, advanced technologies, and strong distribution networks. However, increasing investments by domestic manufacturers in research and development are enabling them to produce cost-effective alternatives, thereby intensifying competition. Strategic moves such as product launches, collaborations, and geographic expansions are common tactics used to strengthen market positions. Additionally, the growing demand for customized implants and bioengineered materials is pushing companies to innovate rapidly. Regulatory support and rising healthcare expenditure in emerging economies further contribute to a dynamic and evolving competitive landscape in the region.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Asia Pacific orthopedic biomaterial market profiled in this report are

- Zimmer Biomet

- Stryker

- DePuy Synthes Companies

- Medtronic

- Arthrex, Inc.

- NuVasive, Inc.

- Globus Medical, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Zimmer Biomet is a leading global player in orthopedic biomaterials and holds a strong presence in the Asia Pacific region. The company offers a broad portfolio of products, including joint implants, spinal devices, trauma fixation systems, and orthobiologics. In the Asia Pacific market, Zimmer Biomet has been actively expanding its footprint through strategic partnerships, local manufacturing, and collaborations with healthcare providers. Its commitment to innovation is evident in its development of advanced biomaterials that enhance implant durability and patient recovery. With a focus on emerging markets such as India and China, the company plays a crucial role in shaping regional trends and advancing orthopedic care standards across the Asia Pacific.

- Stryker is a dominant force in the orthopedic biomaterial sector, known for its cutting-edge technologies and extensive product range tailored for joint replacement, spine surgery, and trauma management. In the Asia Pacific region, Stryker has strategically invested in research and development centers, distribution networks, and training programs for surgeons. The company’s emphasis on digital integration, such as robotic-assisted surgical platforms, has strengthened its market position. By aligning with local healthcare ecosystems and investing in sustainable medical solutions, Stryker continues to expand its influence in the Asia Pacific orthopedic biomaterial landscape. Its contributions are instrumental in improving surgical outcomes and driving technological advancements in the field.

- Johnson & Johnson, through its subsidiary DePuy Synthes, is a key player in the orthopedic biomaterial space globally and in the Asia Pacific region. The company provides a comprehensive range of orthopedic implants, biologics, and surgical tools designed to meet diverse clinical needs. In Asia Pacific, DePuy Synthes has focused on localized product development, strategic acquisitions, and strengthening its supply chain infrastructure. It has also prioritized educational initiatives for orthopedic professionals and collaborated with governments to improve access to advanced orthopedic care. With its strong brand reputation, robust R&D capabilities, and deep-rooted presence in major APAC markets, Johnson & Johnson remains a pivotal contributor to the growth and evolution of the orthopedic biomaterial industry in the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading players in the Asia Pacific orthopedic biomaterial market is product innovation and development. Companies continuously invest in research to introduce advanced biomaterials that offer better biocompatibility, durability, and integration with human tissue. These innovations cater to the growing demand for minimally invasive procedures and long-lasting implants, particularly in aging populations across the region. Another key approach is strategic partnerships and collaborations, where companies engage with hospitals, academic institutions, and regulatory bodies to accelerate product development and ensure compliance with regional standards. This enhances market penetration and fosters trust among medical professionals. Lastly, market expansion through mergers and acquisitions is a widely adopted strategy. Major players acquire regional firms or establish joint ventures to strengthen their distribution networks, gain local expertise, and expand their customer base in high-growth APAC countries like India, China, and South Korea.

RECENT MARKET DEVELOPMENTS

- In February 2024, Zimmer Biomet launched a new line of bioresorbable implants tailored specifically for orthopedic trauma applications in the Asia Pacific region. This product launch aimed to address the growing demand for implants that naturally dissolve after healing, eliminating the need for secondary surgeries and enhancing patient recovery times.

- In June 2024, Stryker Corporation announced a strategic collaboration with a leading Japanese research institute to develop next-generation orthobiologic solutions. This partnership was intended to accelerate the commercialization of regenerative therapies and enhance Stryker's offerings in the fast-growing orthobiologics segment across Asia.

- In September 2024, Johnson & Johnson expanded its manufacturing facility in Singapore to increase local production capacity for orthopedic implants and biomaterials. This move was part of the company’s broader strategy to strengthen its supply chain and respond more efficiently to the rising demand in Southeast Asia.

- In November 2024, a prominent Indian orthopedic biomaterial manufacturer entered into a distribution agreement with a global player to co-market advanced polymer-based implants across the Asia Pacific. This alliance was designed to combine local market knowledge with international product expertise.

- In January 2025, a South Korean medtech firm acquired a smaller Australian biomaterial startup specializing in 3D-printed orthopedic implants. This acquisition was aimed at expanding the company’s footprint in the APAC region while enhancing its capabilities in personalized orthopedic solutions.

MARKET SEGMENTATION

This Asia Pacific orthopedic biomaterial market research report is segmented and sub-segmented into the following categories.

By Material Type

- Ceramics

- Polymers

- Metals

- Others

By Application

- Joint Replacements

- Spine Implants

- Orthobiologics

- Tissue Fixation

- Others

By Country

- India

- China

- Japan

- South Korea

- Rest Of APAC

Frequently Asked Questions

1. Which countries lead the Asia Pacific Orthopedic Biomaterial Market?

China and India dominate the Asia Pacific Orthopedic Biomaterial Market, followed by Japan, South Korea, Australia, and Southeast Asian countries, driven by their aging populations and rising orthopedic procedures

2. What factors drive growth in the Asia Pacific Orthopedic Biomaterial Market?

Key growth drivers for the Asia Pacific Orthopedic Biomaterial Market include an aging demographic, increased prevalence of osteoarthritis and osteoporosis, expanding medical tourism, and investments in innovative biomaterial technologies

3. What are the main material types used in the Asia Pacific Orthopedic Biomaterial Market?

Major types include polymers, ceramics (including bioactive glass), metals, calcium phosphate cements, and composite materials used for implants, joint reconstructions, and bone grafts

4. How is nanotechnology influencing the Asia Pacific Orthopedic Biomaterial Market?

Nanotechnology is advancing the Asia Pacific Orthopedic Biomaterial Market by enabling biomaterials with better biocompatibility, longevity, and integration with living tissue for improved patient outcomes

5. What is the role of orthobiologics in the Asia Pacific Orthopedic Biomaterial Market?

Orthobiologics including platelet-rich plasma (PRP) and stem cell-based technologies—are increasingly used for joint and bone regeneration, reducing recovery times and improving success rates of orthopedic procedures in Asia Pacific

6. Which segments dominate the Asia Pacific Orthopedic Biomaterial Market?

The knee and hip biomaterial segments are the largest, driven by the high incidence of joint replacements and repair surgeries across the Asia Pacific Orthopedic Biomaterial Market

7. Who are the key players in the Asia Pacific Orthopedic Biomaterial Market?

Major companies include Zimmer Biomet Holdings, Johnson & Johnson (DePuy Synthes), Stryker Corporation, Medtronic, Smith & Nephew, DSM, and Evonik Industries, along with strong regional manufacturers

8. How does medical tourism impact the Asia Pacific Orthopedic Biomaterial Market?

Medical tourism, especially in countries like India, Thailand, and Singapore, expands the Asia Pacific Orthopedic Biomaterial Market by increasing demand for affordable, advanced orthopedic procedures and implants

9. What are the main challenges in the Asia Pacific Orthopedic Biomaterial Market?

Challenges include regulatory complexity, ensuring long-term implant safety, cost barriers for next-generation biomaterials, and managing biocompatibility and durability concerns

10.How is minimally invasive surgery affecting the Asia Pacific Orthopedic Biomaterial Market?

The trend toward minimally invasive orthopedic procedures is propelling demand for innovative, easy-to-use biomaterials that promote rapid patient recovery and reduce complications

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com