Asia Pacific Regenerative Medicine Market Research Report – Segmented By Product (Cell-Based Products, Acellular Products ), Therapy, Application & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) – Industry Analysis From 2024 to 2033

Asia Pacific Regenerative Medicine Market Summary

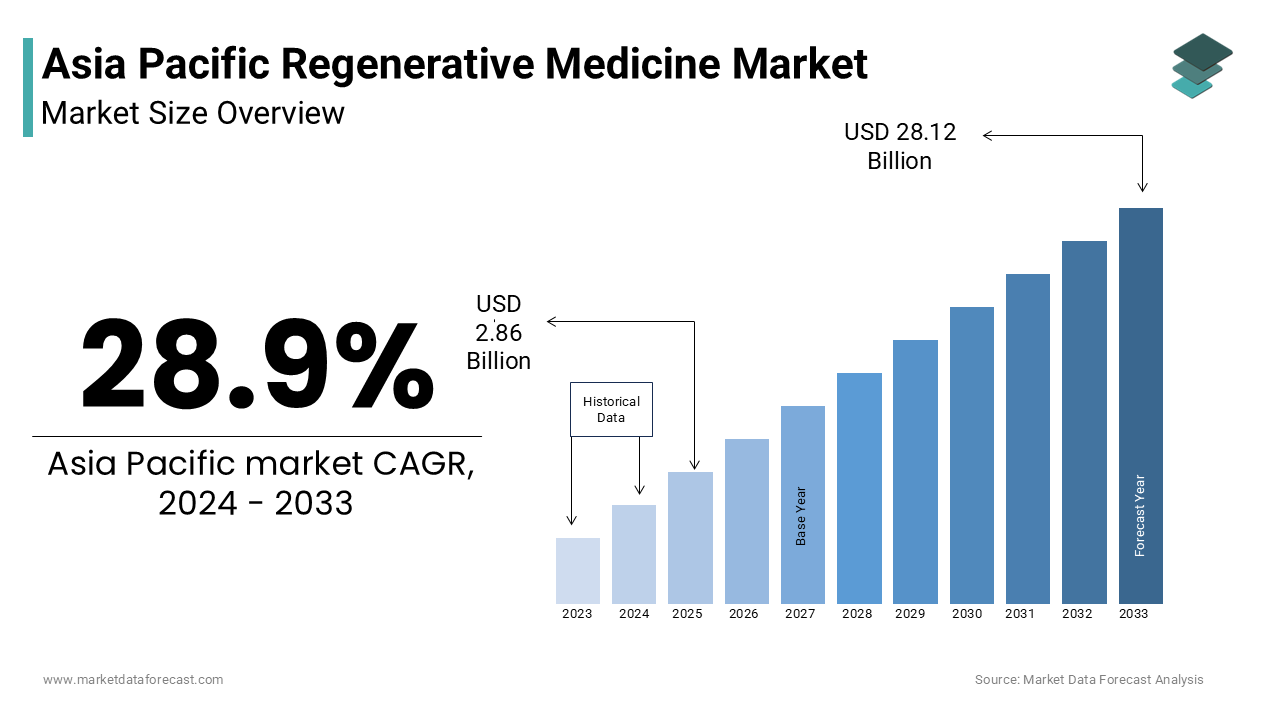

The Asia Pacific Regenerative Medicine Market is projected to grow from USD 2.86 billion in 2024 to USD 28.12 billion by 2033, registering a CAGR of 28.9%. The surge is driven by an aging population, increasing chronic disease burden, government support, and advancements in stem cell and gene therapies.

Key Market Trends & Insights

-

China led the market with a 35.4% share in 2024.

-

Japan and South Korea are driving innovation through iPSC and stem cell technologies.

-

Cell-based products held the largest product share (58.3%) in 2024.

-

Cell therapy dominated the therapy segment with 46.1% share.

-

Orthopedic & musculoskeletal applications accounted for 36.2% of the market.

Market Size & Forecast

-

2024 Market Size: USD 2.86 Billion

-

2033 Projected Market Size: USD 28.12 Billion

-

CAGR (2025–2033): 28.9%

-

Top Market: China (35.4% share in 2024)

-

Other Key Markets: Japan, India, South Korea, Australia

Asia Pacific Regenerative Medicine Market Size

The Asia Pacific Regenerative Medicine Market is projected to grow from USD 2.86 billion in 2024 to USD 28.12 billion by 2033, at a CAGR of 28.9%.

The Asia Pacific regenerative medicine is a broad spectrum of therapies and technologies aimed at repairing, replacing, or regenerating human cells, tissues, and organs to restore normal function. This includes stem cell therapy, tissue engineering, gene therapy, and biomaterials-based approaches that offer long-term solutions for chronic diseases, degenerative conditions, and traumatic injuries. The region has emerged as a focal point for innovation and investment in regenerative medicine due to its rapidly aging population, increasing burden of non-communicable diseases, and growing healthcare expenditure. According to the World Health Organization (WHO), the prevalence of age-related diseases such as osteoarthritis, cardiovascular disorders, and neurodegenerative ailments is rising sharply across the Asia Pacific. As per the United Nations Department of Economic and Social Affairs (UN DESA), the proportion of people aged 60 years or older in the region is expected to double by 2050, significantly increasing demand for curative and restorative treatments beyond traditional pharmacological interventions.

MARKET DRIVERS

Aging Population and Rise in Chronic Diseases

The rapid aging of the population, which has led to an increased incidence of chronic and degenerative diseases that conventional treatment methods struggle to manage effectively is solely propelling the growth of the Asia Pacific regenerative medicine market. According to the United Nations Department of Economic and Social Affairs (UN DESA), the number of people aged 60 years or older in the Asia Pacific region reached over 700 million in 2023, accounting for nearly one-third of the global elderly population. As per the National Health Commission in China, surge in demand for stem cell therapies to treat heart failure, spinal cord injuries, and liver diseases.

Government Support and Regulatory Advancements

The strong government support and progressive regulatory environment that encourages innovation, clinical research, and commercialization of regenerative therapies is also propelling the growth of the Asia Pacific regenerative medicine market. Several governments have introduced favorable policies, financial incentives, and streamlined approval processes to accelerate the development and adoption of cutting-edge treatments. According to the Japanese Ministry of Health, Labour and Welfare, Japan has implemented one of the most advanced regulatory frameworks for regenerative medicine under the Act on the Safety of Regenerative Medicine and the Pharmaceuticals and Medical Devices Act. In South Korea, the Ministry of Food and Drug Safety (MFDS) has actively supported clinical trials involving mesenchymal stem cells and induced pluripotent stem cells (iPSCs). China has also prioritized regenerative medicine through its 14th Five-Year Plan, allocating substantial resources to stem cell research and tissue engineering. The Chinese Academy of Medical Sciences noted that over 150 clinical trials related to regenerative therapies were underway in 2023.

MARKET RESTRAINTS

High Cost and Limited Reimbursement Coverage

The high cost of regenerative therapies combined with limited reimbursement coverage, which restricts patient access and slows down market expansion. Unlike conventional treatments, regenerative medicine involves complex biological processing, customized manufacturing, and rigorous quality control, all of which contribute to elevated treatment costs.

According to the International Society for Cellular Therapy (ISCT), the average cost of a single dose of autologous stem cell therapy in countries like India and Thailand exceeds $10,000, making it unaffordable for most patients without insurance coverage. In Australia, the Medicare Benefits Schedule (MBS) covers only a few regenerative procedures, which is leaving many innovative treatments out-of-pocket expenses for patients. Moreover, lack of standardized pricing models and inconsistent regulatory pathways further complicate affordability assessments.

Ethical Concerns and Regulatory Heterogeneity

Another significant constraint on the Asia Pacific regenerative medicine market is the presence of ethical concerns and varying regulatory landscapes across different countries, which create uncertainty and slow down product approvals. While some nations have adopted progressive frameworks to foster innovation, others maintain strict restrictions based on ethical considerations surrounding stem cell sources and gene-editing techniques. According to the World Medical Association (WMA), there is considerable divergence in how Asian countries regulate the use of embryonic stem cells and gene modification technologies. Japan and South Korea have taken a more permissive approach by allowing clinical applications of induced pluripotent stem cells (iPSCs) and allogeneic cell therapies. However, even in these countries, regulatory hurdles persist, particularly regarding scalability and commercialization.

MARKET OPPORTUNITIES

Expansion of iPSC-Based Therapies and Personalized Medicine

A significant opportunity within the Asia Pacific regenerative medicine market lies in the expansion of induced pluripotent stem cell (iPSC)-based therapies and personalized medicine approaches. iPSC technology allows scientists to reprogram adult cells into pluripotent stem cells by eliminating ethical concerns associated with embryonic sources and enabling patient-specific treatments. According to the Center for iPS Cell Research and Application (CiRA) at Kyoto University, Japan has been at the forefront of iPSC research, with multiple clinical trials already underway for treating Parkinson’s disease, macular degeneration, and heart failure. South Korea has also made significant strides in this area, with the Korean Ministry of Health and Welfare supporting clinical programs focused on iPSC-derived neural and cardiac cells.

Growth of Bioengineering and Tissue Engineering Solutions

Another transformative opportunity for the Asia Pacific regenerative medicine market is the rapid advancement of bioengineering and tissue engineering solutions that enable the creation of functional human tissues for transplantation and drug testing. These innovations hold immense potential for addressing organ shortages and revolutionizing regenerative treatments. According to the International Society for Biofabrication (ISBF), Asia Pacific accounts for over 40% of global research publications in 3D bioprinting and scaffold-based tissue regeneration. India is leveraging collaborations between IITs and medical research institutes to develop affordable tissue-engineered skin grafts for burn victims.

MARKET CHALLENGES

Complexity of Clinical Translation and Long Development Timelines

A major challenge facing the Asia Pacific regenerative medicine market is the complexity involved in translating laboratory discoveries into clinically viable and commercially scalable treatments. Unlike conventional pharmaceuticals, regenerative therapies often require intricate manufacturing processes, stringent quality controls, and prolonged clinical evaluation, which extend development timelines and increase investment risks. According to the International Society for Stem Cell Research (ISSCR), the transition from preclinical studies to Phase III clinical trials for regenerative medicine products takes an average of 8–10 years, significantly longer than for small molecule drugs. Japan, despite having a relatively progressive regulatory framework, still faces challenges in transitioning therapies from conditional approval to full commercialization. The Pharmaceuticals and Medical Devices Agency (PMDA) indicated that post-marketing surveillance requirements delay widespread adoption is posing a significant hurdle to market expansion across the Asia Pacific region.

Lack of Standardization and Quality Control Frameworks

Another critical challenge confronting the Asia Pacific regenerative medicine market is the lack of standardized protocols and robust quality control frameworks across the region. Regenerative therapies involve living cells and complex biological materials, requiring precise handling, storage, and administration factors that vary widely among countries. According to the World Health Organization (WHO), disparities in manufacturing practices and regulatory oversight have led to inconsistencies in product safety and efficacy. In China, the National Medical Products Administration (NMPA) has introduced updated guidelines, but enforcement varies between provinces. The Chinese Society for Regenerative Medicine noted that inconsistent quality assurance practices hinder international collaboration and commercial scalability.

SEGMENTAL ANALYSIS

By Product Insights

The cell-based products segment was the largest and held 58.3% of the Asia Pacific regenerative medicine market share in 2024. According to the International Society for Cellular Therapy (ISCT), Asia Pacific accounts for over 40% of global stem cell clinical trials, with countries like Japan, South Korea, and China leading in translational research. In South Korea, the Ministry of Food and Drug Safety (MFDS) noted a surge in mesenchymal stem cell applications for osteoarthritis, spinal cord injuries, and autoimmune disorders. China has also witnessed a rapid rise in clinical adoption, with the Chinese Academy of Medical Sciences indicating that over 300 MSC-based clinical trials were active in 2023.

The acellular products segment is projected to grow with a CAGR of 13.7% in the next coming years driven by rising interest in extracellular vesicles, exosomes, and growth factor-based therapies as alternatives to live cell interventions. According to the International Journal of Molecular Sciences, acellular therapies have gained traction in wound healing, dermatology, and cardiovascular regeneration due to their ability to modulate inflammation and promote tissue repair without the risks associated with live cell transplantation. In India, academic institutions such as AIIMS and IIT-Delhi have launched research programs on exosomal delivery systems for diabetic wound healing, supported by grants from the Department of Biotechnology (DBT). South Korea has also seen a surge in acellular biologics development, with the Korea Advanced Institute of Science and Technology (KAIST) partnering with biotech firms to commercialize platelet lysate and amniotic fluid-derived regenerative products.

By Therapy Insights

The cell therapy was accounted in holding 46.1% of the Asia Pacific regenerative medicine market share in 2024 with the expanding application of stem cell-based treatments for musculoskeletal, neurological, and cardiovascular conditions. As per the Asian Regenerative Medicine Forum, over 500 clinical trials involving stem cells were actively underway in the Asia Pacific region in 2023, particularly in Japan, China, and South Korea. South Korea has been at the forefront, with companies like Medipost and GC Cell offering commercially available stem cell products for orthopedic indications.

The gene therapy segment is expected to grow with a CAGR of 14.9% during the forecast period with the advancements in gene editing technologies such as CRISPR-Cas9, lentiviral vectors, and mRNA-based modifications in regenerative medicine applications. According to the International Journal of Molecular Sciences, the Asia Pacific region accounted for over 30% of global gene therapy research in 2023, with Japan and Singapore emerging as key hubs for innovation. Australia has also expanded its gene therapy capabilities, with the Australian Regenerative Medicine Institute (ARMI) conducting trials on gene-assisted tissue regeneration for heart and nerve repair.

By Application Insights

The orthopedic and musculoskeletal spine segment was accounted in holding 36.2% of the Asia Pacific regenerative medicine market share in 2024. According to the Asia Pacific League of Associations for Rheumatology (APLAR), musculoskeletal disorders affected over 200 million people across the region in 2023, prompting increased adoption of stem cell injections and PRP (platelet-rich plasma) therapies. China has also experienced a surge in musculoskeletal applications, with the Chinese Medical Doctor Association noting that regenerative interventions are increasingly used in orthopedic departments.

The Central Nervous System (CNS) applications segment is expected to grow with a CAGR of 15.3% in the next coming years. According to the World Health Organization (WHO), neurological disorders account for over 15% of all health-related disability-adjusted life years (DALYs) lost in the Asia Pacific region. In China, the Chinese Medical Association reported that over 10 million people suffer from Parkinson’s disease, with regenerative medicine offering a promising avenue for dopaminergic neuron replacement therapy.

REGIONAL ANALYSIS

China Regenerative Medicine Market Insights

China was the top performer in the Asia Pacific regenerative medicine market with 35.4% of the share in 2024. According to the Chinese Academy of Medical Sciences, over 300 clinical trials involving stem cells and tissue engineering were active in 2023, covering indications ranging from liver cirrhosis to spinal cord injuries. In addition, China’s growing biopharma sector is accelerating the commercialization of regenerative products. The National Medical Products Administration (NMPA) has implemented expedited review pathways for regenerative therapies, encouraging local and multinational companies to enter the market.

Japan Regenerative Medicine Market Insights

Japan regenerative medicine market growth is driven by maintaining a strong presence due to its advanced healthcare system, supportive regulatory environment, and pioneering work in induced pluripotent stem cell (iPSC) technology. The country leads in translational research and clinical applications of regenerative medicine in neurological and cardiovascular indications.

According to the Pharmaceuticals and Medical Devices Agency (PMDA), Japan has one of the most progressive regulatory frameworks for regenerative medicine, allowing conditional approval based on early-phase data to speed up patient access. In 2023, the Japanese Ministry of Education, Culture, Sports, Science and Technology (MEXT) reported that over 40 regenerative medicine products had received conditional approval, with several entering commercial distribution.

Japanese institutions such as Kyoto University’s Center for iPS Cell Research and Application (CiRA) have been instrumental in advancing stem cell-based treatments for Parkinson’s disease, retinal disorders, and heart failure. The Japanese Society for Regenerative Medicine noted that over 10,000 patients received regenerative treatments in 2023, demonstrating real-world adoption.

India Regenerative Medicine Market Insights

India regenerative medicine market is emerging as a key growth hub due to rising disease burden, increasing research activity, and government initiatives aimed at promoting indigenous development of regenerative therapies. According to the Indian Council of Medical Research (ICMR), over 100 regenerative medicine research projects were underway in 2023, focusing on diabetes, cardiovascular diseases, and spinal cord injuries. The Ministry of Health and Family Welfare has encouraged academic-industry collaboration through initiatives like the Biotechnology Ignition Grant (BIG) and Make in India program, fostering the development of affordable regenerative treatments.

South Korea Regenerative Medicine Market Insights

South Korea regenerative medicine market growth is likely to grow with its strong biotech ecosystem, progressive regulatory policies, and early adoption of stem cell therapies. According to the Korea Biomedical Review, South Korea has one of the most advanced regulatory environments for regenerative medicine, with the Ministry of Food and Drug Safety (MFDS) allowing conditional marketing authorizations for stem cell products based on preliminary evidence. Leading biotech firms such as Medipost, Anterogen, and GC Cell have commercialized regenerative treatments for osteoarthritis, Crohn’s disease, and myocardial infarction.

Australia Regenerative Medicine Market Insights

Australia regenerative medicine market growth is likely to grow with the high-quality research infrastructure, ethical governance, and a growing emphasis on translational medicine. According to the Australian Regenerative Medicine Institute (ARMI), Australia has been at the forefront of stem cell research, particularly in the fields of cardiac regeneration, bone repair, and autoimmune disease treatment. The Therapeutic Goods Administration (TGA) maintains strict regulatory oversight, ensuring high safety and efficacy standards.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Noteworthy companies operating in the APAC Regenerative Medicines Market profiled in this report are Vertex Pharmaceuticals Incorporated (U.S.), Acelity L.P. Inc. (U.S.), Celgene Corporation (U.S.), StemCells, Inc. (U.S.), Organogenesis Inc. (U.S.), NuVasive, Inc. (U.S.), Vericel Corporation (Genzyme) (U.S.), Japan Tissue Engineering Co., Ltd. (Japan), Cytori Therapeutics Inc. (U.S.), Advantagene, Inc. (U.S.) and Mesoblast Ltd. (Australia).

The competition in the Asia Pacific regenerative medicine market is marked by a blend of global pharmaceutical giants and dynamic local biotech innovators striving to capture a share of this high-growth sector. Multinational corporations bring technological expertise, regulatory experience, and substantial R&D budgets, while regional players leverage localized clinical insights, cost-effective manufacturing, and tailored patient access models.

Government policies play a defining role in market dynamics, with Japan and South Korea adopting forward-looking regulations that allow conditional approvals and accelerated pathways for regenerative therapies. In contrast, China and India are balancing innovation with cautious regulation, aiming to ensure safety while promoting domestic development. Australia and New Zealand emphasize ethical research and translational medicine, which is attracting global collaborations through high-quality clinical environments.

The rise of personalized and gene-editing-based therapies has intensified competition, compelling firms to differentiate through proprietary technologies, IP portfolios, and clinical validation. Companies are recalibrating strategies to enhance market penetration, streamline manufacturing, and build sustainable business models in this evolving therapeutic domain as the demand for regenerative treatments expands across musculoskeletal, neurological, and cardiovascular applications.

Top Players in the Asia Pacific Regenerative Medicine Market

One of the leading players in the Asia Pacific regenerative medicine market is Takeda Pharmaceutical Company Limited, a global pharmaceutical giant with deep expertise in cell and gene therapies. Takeda has been actively involved in advancing stem cell-based treatments for rare diseases and immune disorders. The company collaborates with academic institutions and biotech firms across Japan, South Korea, and China to accelerate clinical translation and commercialization.

Another key player is Medipost Co., Ltd. is a South Korean biotechnology firm specializing in stem cell therapies. Medipost has developed innovative products targeting orthopedic conditions such as osteoarthritis. Its flagship therapy, Cartistem, has received regulatory approval and is being explored in international markets. The company plays a vital role in shaping regional regenerative medicine policies and clinical practices.

Stempeutics Research Private Limited, based in India, also holds a prominent position. It focuses on mesenchymal stem cell therapies for chronic conditions like diabetic foot ulcers and cardiovascular complications. Stempeutics is advancing its product pipeline and improving access to affordable regenerative treatments in emerging economies across Asia with support from national research councils.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific regenerative medicine market employ several strategic approaches to reinforce their competitive edge. One major strategy is strategic collaborations and academic-industry partnerships, where companies engage with universities, research hospitals, and government agencies to accelerate clinical translation and product development.

Another critical approach is expanding clinical applications through targeted R&D and regulatory engagement by allowing firms to navigate diverse approval pathways and secure conditional or full market authorization in countries with progressive policies, such as Japan and South Korea.

Scaling up manufacturing capabilities and biobanking infrastructure plays a pivotal role in strengthening market positioning. Companies are investing in GMP-certified production facilities and stem cell banking services to ensure consistency, scalability, and compliance with international standards.

RECENT MARKET DEVELOPMENTS

- In January 2023, Takeda Pharmaceutical entered into a research agreement with a leading South Korean university to co-develop iPSC-based treatments for rare neurological disorders. This partnership is anticipated to allow Takeda to access cutting-edge stem cell technology and strengthen its pipeline in the Asia Pacific region.

- In May 2023, Medipost Co., Ltd. expanded its clinical trial network to include Malaysia and Vietnam, aiming to validate its stem cell therapy platform in new markets. This move is expected to allow Medipost to enhance regional regulatory recognition and broaden its commercial reach.

- In September 2023, Stempeutics Research received conditional approval from the Indian Drug Controller General of India (DCGI) for its stem cell therapy targeting diabetic foot ulcers. This approval is expected to allow Stempeutics to commercialize its product in both public and private healthcare settings, which is boosting market visibility.

- In March 2024, GC Cell Corporation opened a state-of-the-art GMP-grade stem cell manufacturing facility in South Korea, designed to meet global regulatory standards and support large-scale clinical and commercial applications. This expansion is expected to allow GC Cell to improve production efficiency and supply chain resilience.

- In April 2024, Eisai Co., Ltd. acquired a Singapore-based regenerative medicine startup specializing in neural regeneration. This acquisition is anticipated to allow Eisai to integrate advanced stem cell platforms into its neuroscience division and strengthen its position in the Asia Pacific regenerative medicine market.

MARKET SEGMENTATION

This research report on the APAC regenerative medicine market has been segmented and sub-segmented into the following categories:

By Product

- Cell-Based Products

- Autologous Cell-Based Products

- Allogeneic Cell-Based Products

- Acellular Products

By Therapy

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Immunotherapy

By Application

- Orthopedic & Musculoskeletal Spine

- Dermatology

- Cardiovascular

- Central Nervous System

- Oncology

- Diabetes

- Other Applications

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is the size of the Asia Pacific Regenerative Medicine Market?

The regenerative medicine market size in the Asia-Pacific is estimated to be worth USD 28.12 billion by 2033.

What are the major drivers of growth in the Asia Pacific Regenerative Medicine Market?

Factor such as increasing prevalence of chronic diseases, growing aging population, advancements in regenerative medicine technology, and increasing healthcare expenditure are propelling the growth of the regenerative medicine market in the Asia Pacific reigon.

Which countries are holding major share of the regenerative medicine market in the APAC region?

China, Japan, and South Korea are expected to capture the major share of the APAC market in the coming years.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com