Asia Pacific Residential Water Heater Market Size, Share, Trends & Growth Forecast Report By Product (Instant, Storage), Capacity (30L, 30–100L, 100–250L), Fuel (Natural Gas, LPG), and Country (India, China, Japan, South Korea, Australia) – Industry Analysis From 2025 to 2033.

Asia Pacific Residential Water Heater Market Size

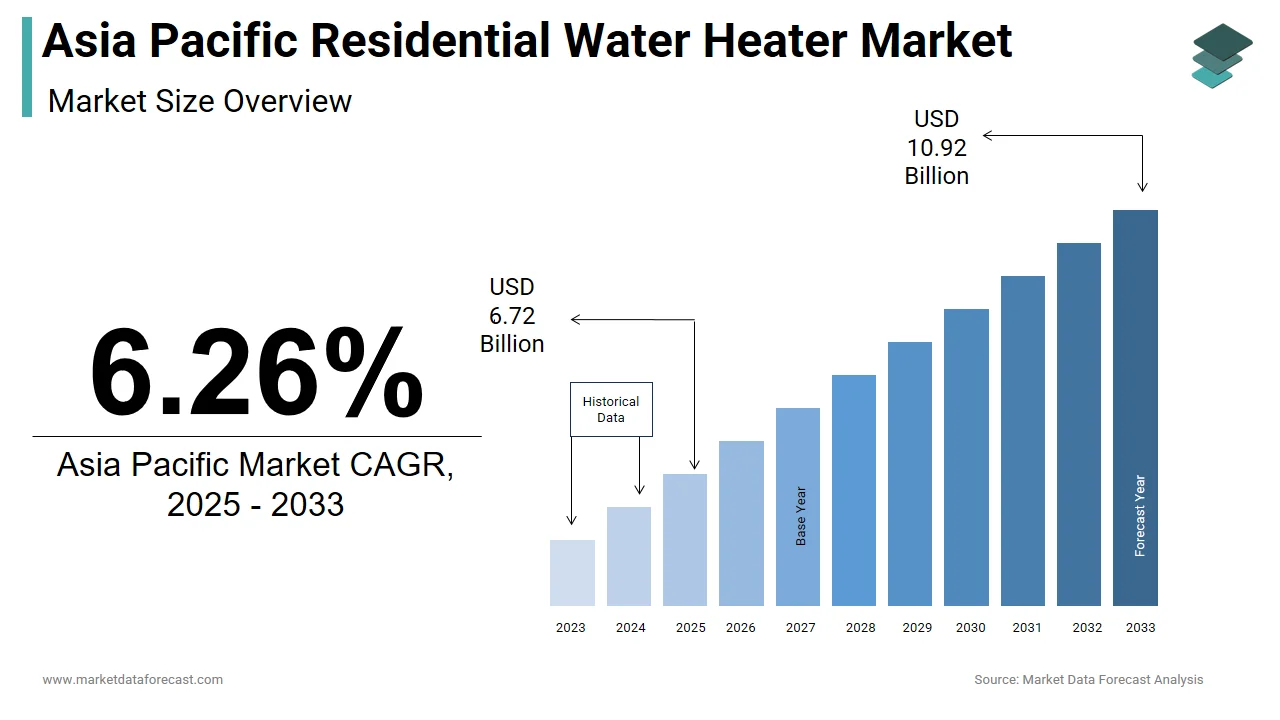

The size of the Asia Pacific residential water heater market was worth USD 6.32 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 6.26% from 2025 to 2033 and be worth USD 10.92 billion by 2033 from USD 6.72 billion in 2025.

Residential water heaters are essential appliances that provide hot water for daily household needs, including bathing, cooking, and cleaning. The market is characterized by a diverse range of products, including storage tank heaters, tankless (instantaneous) heaters, heat pump systems, and solar-powered heaters. These systems cater to varying consumer preferences, climate conditions, and energy availability across the region.

Urbanization trends further amplify this need, with cities like Mumbai, Shanghai, and Jakarta witnessing rapid growth in middle-class households. In addition, government initiatives promoting energy efficiency and renewable energy adoption have spurred innovations in water heating technologies, aligning with sustainability goals. Climate variability also plays a pivotal role.

MARKET DRIVERS

Rising Urbanization and Middle-Class Growth

Urbanization and the expansion of the middle class are significant drivers of the residential water heater market in the Asia Pacific. According to the World Bank, the urban population in the region is expected to grow by 50% by 2050, creating a surge in housing development and appliance demand. As urban households increasingly adopt modern lifestyles, the need for reliable and efficient water heating solutions becomes paramount. For example, in India, the Ministry of Housing and Urban Affairs reports that over 100 smart cities are under development, with residential complexes incorporating energy-efficient appliances like heat pump water heaters. Similarly, China’s rapid urbanization has led to a boom in high-rise apartments, where compact and instant water heaters are gaining popularity due to space constraints. Besides, rising disposable incomes enable households to invest in premium products, such as solar-powered heaters, which align with environmental consciousness.

Government Initiatives for Energy Efficiency

Government policies promoting energy conservation and sustainable living are another key driver of the residential water heater market. According to the Australian Energy Market Operator, over 2 million households have installed solar-powered systems, reducing reliance on conventional electricity grids. Similarly, Japan’s Top Runner Program incentivizes manufacturers to develop energy-efficient water heaters, ensuring compliance with stringent emission standards. The program has resulted in a reduction in energy consumption for residential appliances. These initiatives not only reduce household utility bills but also contribute to national sustainability goals, driving widespread acceptance of innovative water heating technologies.

MARKET RESTRAINTS

High Initial Costs of Advanced Systems

One of the primary restraints affecting the residential water heater market in the Asia Pacific is the high initial cost of advanced systems, particularly solar-powered and heat pump models. These technologies, while energy-efficient, often require significant upfront investment, deterring price-sensitive consumers. For instance, according to the Confederation of Indian Industry, over 60% of rural households in India cannot afford premium water heaters, limiting their adoption to urban areas. In emerging economies like Indonesia and the Philippines, where disposable incomes remain low, affordability remains a critical barrier. Even in developed markets like South Korea, where the government subsidizes green technologies, the payback period for solar water heaters can exceed five years, discouraging potential buyers. Apart from these, installation costs for heat pump systems, which require specialized expertise, further inflate expenses.

Lack of Awareness and Technical Knowledge

Another significant restraint is the limited awareness and technical understanding of advanced water heating technologies among end-users. Many consumers in the region are unfamiliar with the benefits of energy-efficient models, opting instead for traditional electric or gas heaters due to their perceived reliability. Like, limited number of households in Southeast Asia are aware of the long-term cost savings associated with solar-powered water heaters. This knowledge gap is exacerbated by inadequate marketing efforts and insufficient training programs for installers and retailers. For example, in Thailand, a study by the Federation of Thai Industries revealed that over 50% of consumers incorrectly believe that solar water heaters are unsuitable for urban environments. Furthermore, counterfeit or substandard products flooding the market in countries like Malaysia and Vietnam undermine trust in new technologies, discouraging adoption.

MARKET OPPORTUNITIES

Expansion of Smart Home Ecosystems

Smart water heaters, equipped with features like remote control, energy monitoring, and adaptive temperature settings, are becoming integral components of these ecosystems. Governments are also supporting this trend through incentives for smart appliance adoption.

Growing Demand for Sustainable Solutions

The increasing emphasis on sustainability offers another lucrative opportunity for the residential water heater market. According to the International Energy Agency, renewable energy adoption in the Asia Pacific surged notably between 2020 and 2022, with solar-powered water heaters playing a vital role in this transition. Countries like India and Australia are investing heavily in renewable energy infrastructure, driving demand for eco-friendly water heating solutions.

Australia’s Small-scale Renewable Energy Scheme provides financial incentives for households installing solar-powered systems, reducing carbon footprints while lowering utility bills. In addition, the rise of net-zero buildings in urban areas, as promoted by organizations like the Green Building Council of Australia, amplifies the need for energy-efficient water heaters.

MARKET CHALLENGES

Counterfeit and Substandard Products

A pressing challenge facing the residential water heater market in the Asia Pacific is the prevalence of counterfeit and substandard products, which compromise safety and erode consumer trust. According to the Federation of Indian Chambers of Commerce & Industry, counterfeit water heaters account for notable share of the market in some Southeast Asian countries, posing significant risks to users. These products often fail to meet international safety and performance standards, increasing the likelihood of malfunctions or accidents during operation.

The influx of counterfeit goods is fueled by weak enforcement mechanisms and inadequate quality control measures in certain regions. For instance, a 2021 investigation by the Malaysian Consumer Protection Association revealed that over 40% of imported water heaters tested did not comply with required safety benchmarks. This issue is further exacerbated by price-sensitive buyers who prioritize cost over quality, inadvertently supporting the proliferation of substandard products.

Limited Adoption in Rural Areas

The Asia Pacific population resides in rural regions, many of which lack access to reliable electricity or gas connections. Traditional methods, such as wood-fired heating, remain prevalent, leaving communities vulnerable to inefficiencies and health hazards.

Besides, the absence of government subsidies or incentives in rural areas further impedes the adoption of modern water heaters. For example, a study by the Asian Development Bank found that a very small portion of rural households in countries like Cambodia and Laos use electric or solar water heaters, showcasing the disparity in access to technology.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Capacity, Fuel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | A. O. Smith India Water Products Pvt. Ltd., Ariston Holding N.V., American Standard Water Heaters, Bosch Thermotechnology Corp., Bradford White Corporation, USA, Ferroli S.p.A, GE Appliances, Haier Inc., Havells India Ltd., Lennox International Inc., NORITZ Corporation, Racold, Rheem Manufacturing Company, Rinnai America Corporation, State Industries, Vaillant, Westinghouse Electric Corporation and others. |

SEGMENTAL ANALYSIS

By Product Insights

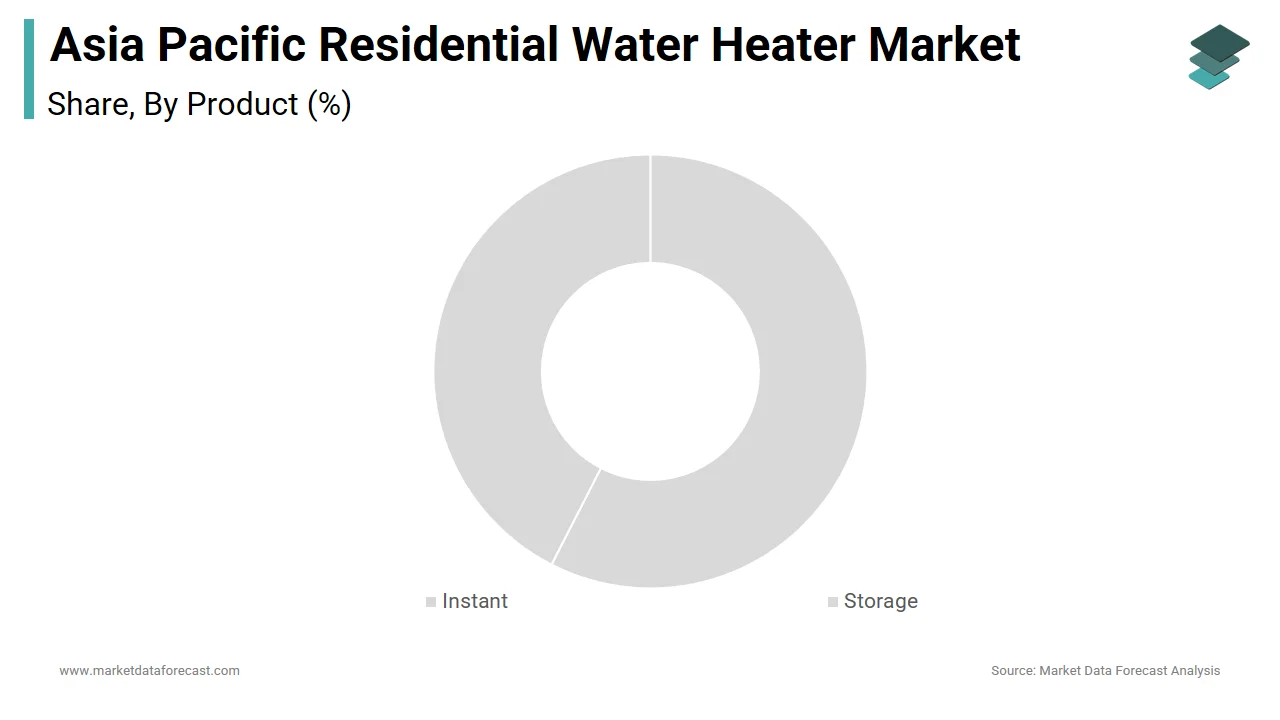

The segment of storage water heaters led the Asia Pacific residential water heater market by holding a market share of 55.6%in 2024. This leading position is credited to their widespread adoption in households due to their reliability, ease of use, and affordability. According to the Asian Development Bank, a large number of urban households in the region prefer storage heaters for their consistent hot water supply, especially in regions with colder climates like Japan and South Korea. A key driver of this segment's dominance is the growing demand for energy-efficient models. For instance, advancements in insulation technologies have reduced heat loss in storage heaters, making them more appealing to cost-conscious consumers. Apart from these, the rise of compact designs has made storage heaters suitable for small apartments, which are prevalent in densely populated cities like Mumbai and Manila. Another factor is the availability of affordable financing options. In India, schemes like the Pradhan Mantri Awas Yojana provide subsidies for home appliances, including storage water heaters, enabling lower-income households to access these products. This accessibility ensures sustained demand for storage heaters across diverse demographics.

The instant (tankless) water heaters segment is the fastest-growing in the Asia Pacific residential water heater market, with a CAGR of 12%. This is fueled by their space-saving design and energy efficiency, particularly in urban areas where real estate is at a premium. The surge in urbanization is a significant driver. Instant heaters are particularly popular in countries like Thailand and Vietnam, where small living spaces necessitate efficient solutions. Besides, technological advancements, such as digital thermostats and Wi-Fi connectivity, have enhanced user convenience, further boosting adoption. Government initiatives also play a pivotal role. For example, Australia’s Renewable Energy Target promotes the use of energy-efficient appliances, with instant heaters gaining traction due to their lower electricity consumption compared to traditional models.

By Capacity Insights

The 30-100 liters capacity segment held the largest share of the Asia Pacific residential water heater market i.e. 40.5% of total sales in 2024. This dominance is supported by its suitability for medium-sized households, which constitute the majority of family structures in the region. A key factor propelling this segment is the rising demand for energy-efficient solutions. This makes them an attractive choice for middle-class families seeking cost-effective yet reliable appliances. Also, the segment benefits from its versatility, catering to both urban apartments and suburban homes. Government policies also support this trend. Furthermore, manufacturers are introducing innovative features like smart controls and eco-friendly materials, enhancing the appeal of these products.

The <30 liters capacity segment is the swiftest expanding in the Asia Pacific residential water heater market, with a CAGR of 15%. This progress is backed by the increasing popularity of compact living spaces and single-person households, particularly in urban areas. Like, a significant share of new housing units in cities like Tokyo and Singapore are designed for single occupants or couples, amplifying demand for small-capacity heaters. Technological advancements have also played a crucial role. For example, South Korean manufacturers have introduced instant heaters with capacities under 30 liters, equipped with features like voice control and energy monitoring, aligning with the region’s smart home trend. Government initiatives further accelerate acceptance. In Australia, the Small-scale Renewable Energy Scheme incentivizes the installation of compact solar-powered heaters, reducing reliance on conventional energy sources.

By Fuel Insights

The LPG-powered water heaters commanded the Asia Pacific market by holding a share of 45.4% in 2024. This influence over the category is attributed to the widespread availability and affordability of LPG in rural and semi-urban areas. Also, a large share of households in Southeast Asia rely on LPG for cooking and heating, making it a natural choice for water heaters. A different aspect is the lack of reliable electricity infrastructure in many regions. For instance, in Indonesia and the Philippines, where power outages are common, LPG heaters provide a dependable alternative. Besides, the low initial cost of LPG systems compared to electric or solar models makes them accessible to lower-income households. In India, LPG heater sales grew notably in rural India between 2020 and 2022, reflecting their popularity.

Government subsidies also play a critical role. In Thailand, the Ministry of Energy provides financial assistance for LPG appliances, ensuring affordability for rural communities.

The natural gas-powered water heaters segment is quickly moving ahead in the market, with a CAGR of 14%. This development is credited to the expansion of natural gas infrastructure and its reputation as a cleaner and more cost-effective fuel. Countries like China and Japan are leading this trend. For example, China’s National Development and Reform Commission promotes natural gas as part of its clean energy strategy, resulting in a considerable increase in gas heater installations. Similarly, Japan’s Top Runner Program incentivizes manufacturers to develop energy-efficient natural gas heaters, aligning with national sustainability goals. Urbanization further amplifies demand. In Australia, a significant portion of new residential developments are connected to natural gas networks.

COUNTRY LEVEL ANALYSIS

China led the Asia Pacific residential water heater market by commanding a market share of a 40.3% in 2024. This dominance is underpinned by the country’s massive population and rapid urbanization. According to the National Bureau of Statistics of China, over 60% of households now reside in urban areas, driving demand for modern water heating solutions. Moreover, a main factor is the government’s push for energy efficiency. The Ministry of Ecology and Environment mandates the use of eco-friendly appliances, spurring innovation in solar and heat pump heaters. Also, China’s manufacturing prowess enables cost-effective production, making water heaters accessible to a wide demographic.

India is another key player in the market. The country’s growing middle class and urbanization trends are driving demand for residential water heaters. Additionally, the rise of e-commerce platforms has expanded market reach, particularly in rural areas, ensuring steady growth for the segment.

Japan holds a significant position in the market. The advanced technology and emphasis on sustainability of the country drive adoption of energy-efficient water heaters. According to the Japan External Trade Organization, a large majority of households use eco-friendly models, aligning with national emission reduction goals. Cold winters in regions like Hokkaido amplify demand for advanced heating solutions. Also, the government’s Top Runner Program incentivizes manufacturers to innovate, ensuring Japan remains a leader in the global market.

South Korea is experiencing rise in the market which is driven by its focus on smart home integration and energy efficiency. Like, a notable shareof households use gas-powered water heaters, supported by extensive natural gas infrastructure. The nation’s emphasis on innovation is evident in its AI-enabled water heaters, which optimize energy usage. Government policies promoting renewable energy further enhance adoption, ensuring sustained growth for the segment.

Australia contributes notably to the market, with a strong emphasis on sustainability. Government schemes like the Small-scale Renewable Energy Scheme provide incentives for eco-friendly appliances, driving adoption. Besides, the rise of net-zero buildings amplifies demand for energy-efficient water heating solutions, positioning Australia as a key player in the regional market.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC residential water heater market profiled in this report are A. O. Smith India Water Products Pvt. Ltd., Ariston Holding N.V., American Standard Water Heaters, Bosch Thermotechnology Corp., Bradford White Corporation, USA, Ferroli S.p.A, GE Appliances, Haier Inc., Havells India Ltd., Lennox International Inc., NORITZ Corporation, Racold, Rheem Manufacturing Company, Rinnai America Corporation, State Industries, Vaillant, Westinghouse Electric Corporation and others.

TOP LEADING PLAYERS IN THE MARKET

AO Smith Corporation

AO Smith is a global leader in the residential water heater market, renowned for its innovative and energy-efficient solutions. The company’s expertise lies in developing advanced technologies such as tankless heaters, heat pumps, and solar-powered systems, which cater to diverse consumer needs across the Asia Pacific region. AO Smith’s commitment to sustainability is evident in its eco-friendly product range, aligning with regional green initiatives.

Rinnai Corporation

Rinnai Corporation is a dominant player in the Asia Pacific residential water heater market, specializing in gas-powered and instant water heaters. The company’s focus on reliability and energy efficiency has earned it a strong reputation among urban households. Rinnai’s emphasis on smart home integration has enabled it to offer cutting-edge products like AI-driven thermostats and voice-controlled systems. Additionally, its robust distribution network and localized manufacturing facilities ensure timely delivery and customer satisfaction, reinforcing its leadership in both regional and global markets.

Ariston Thermo Group

Ariston Thermo Group is a key contributor to the residential water heater market, offering a wide range of products tailored to meet regional demands. The company’s portfolio includes storage heaters, heat pumps, and solar-powered systems, designed to address varying climate conditions and energy availability. Ariston’s dedication to innovation is reflected in its development of eco-friendly solutions that align with sustainability goals.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Customization

Leading companies in the Asia Pacific residential water heater market are heavily investing in product innovation to address specific regional challenges. For instance, manufacturers are developing compact, energy-efficient models tailored for urban apartments and rural households with limited access to electricity. By introducing eco-friendly solutions like solar-powered and heat pump systems, these firms cater to growing environmental consciousness.

Strategic Partnerships and Collaborations

To strengthen their market presence, key players are forming strategic partnerships with e-commerce platforms, local distributors, and technology firms. These collaborations enable companies to expand their reach in untapped markets and integrate advanced features like IoT connectivity into their products. For example, partnering with smart home ecosystem providers allows firms to offer integrated solutions that appeal to tech-savvy consumers.

Focus on Sustainability and Energy Efficiency

Promoting sustainability is another critical strategy adopted by market leaders. Companies are emphasizing the development of energy-efficient appliances that reduce carbon footprints and lower utility bills. By aligning with government incentives and certification programs, such as Australia’s Renewable Energy Target, firms enhance their credibility and attract environmentally conscious consumers.

COMPETITION OVERVIEW

The Asia Pacific residential water heater market is characterized by intense competition, driven by the presence of both multinational corporations and regional players striving to capture market share. Leading companies leverage their technological expertise and extensive distribution networks to maintain dominance, while smaller firms focus on niche applications to carve out a foothold. The market’s competitive landscape is shaped by the growing emphasis on energy efficiency, sustainability, and smart home integration, necessitating continuous innovation and compliance with international standards. Urbanization trends further amplify rivalry, as firms compete to meet the diverse needs of densely populated cities and rural areas.

RECENT MARKET DEVELOPMENTS

- In March 2023, AO Smith Corporation launched a new line of IoT-enabled water heaters designed for smart homes in Australia. This move aimed to capitalize on the growing trend of home automation and enhance user convenience through features like remote control and energy monitoring.

- In June 2023, Rinnai Corporation partnered with a leading e-commerce platform in India to expand its online sales channels. This collaboration was intended to increase accessibility for rural consumers and tap into the booming digital retail sector.

- In August 2023, Ariston Thermo Group established a training center in Thailand to educate installers and retailers on the latest advancements in solar-powered water heaters. This initiative underscored the company’s commitment to promoting renewable energy solutions in Southeast Asia.

- In November 2023, Vaillant Group acquired a local manufacturer in Vietnam to strengthen its supply chain and product portfolio in the region. This acquisition enabled Vaillant to address the rising demand for affordable gas-powered water heaters in emerging markets.

- In January 2024, Bajaj Electricals introduced a new range of compact instant water heaters specifically designed for urban apartments in Indonesia. This launch aimed to address space constraints and cater to the growing middle-class population in metropolitan areas.

MARKET SEGMENTATION

This Asia Pacific residential water heater market research report is segmented and sub-segmented into the following categories.

By Product

- Instant

- Storage

By Capacity

- 30 liters

- 30 – 100 liters

- 100 – 250 liters

- 250 – 400 liters

- >400 liters

By Fuel

- Natural Gas

- LPG

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What drives the Asia Pacific residential water heater market?

Urbanization, rising middle-class incomes, government energy efficiency policies, and growing demand for smart, energy-saving water heaters drive the Asia Pacific residential water heater market.

2. What challenges affect the Asia Pacific residential water heater market?

High upfront costs, limited awareness of advanced technologies, prevalence of counterfeit products, and lack of reliable infrastructure in rural areas challenge the Asia Pacific residential water heater market.

3. What opportunities exist in the Asia Pacific residential water heater market?

Opportunities in the Asia Pacific residential water heater market include adoption of solar and smart heaters, government incentives, and rising demand for eco-friendly, compact solutions in urban homes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com