Asia Pacific Smart Irrigation Market Size, Share, Growth, Trends, And Forecasts Research Report, Segmented By Irrigation Controller, Hardware And Network Component, Application, and Region (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2026 to 2034

Market Size, 2025

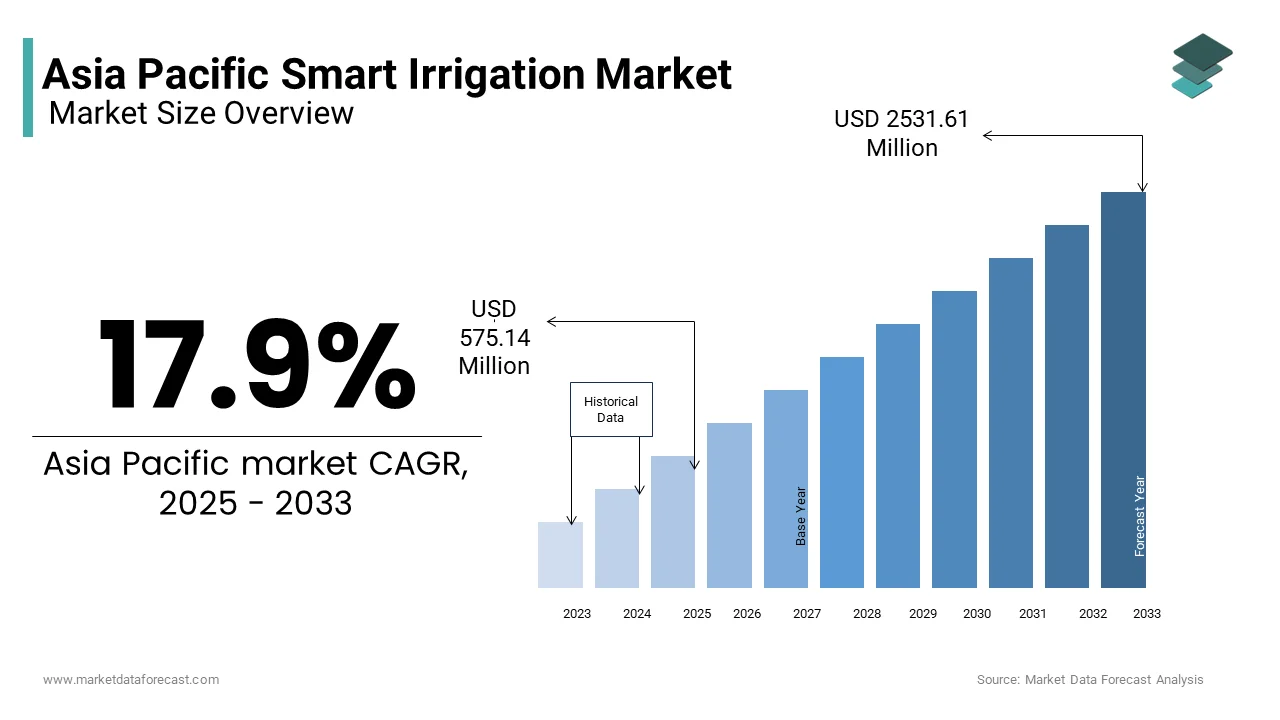

$678.09 MnMarket Estimate, 2026

$799.47 MnMarket Forecast, 2034

$2984 MnCAGR, 2026–2034

17.9%Asia Pacific Smart Irrigation Market Size

The Asia Pacific smart irrigation system market size was valued at USD 678.09 million in 2025 and is anticipated to reach USD 799.47 million in 2026 to reach USD 2984.77 million by 2034, growing at a CAGR of 17.9% during the forecast period from 2026 to 2034.

Smart Irrigation is are technologically advanced irrigation systems that optimize water usage through automation, real-time data monitoring, and sensor-based decision-making in agricultural practices. These systems integrate components such as soil moisture sensors, weather stations, cloud computing platforms, and automated control valves to deliver precise water quantities based on crop needs and environmental conditions. The market has gained momentum due to increasing water scarcity, rapid urbanization, and the need for sustainable farming practices across the region.

Moreover, in 2024, Asia Pacific accounted for over 60% of the global population, with agriculture remaining a dominant sector in countries like India, China, and Indonesia. According to the Food and Agriculture Organization (FAO), agriculture in the region consumes nearly 80% of freshwater resources, emphasizing the urgency for efficient water management solutions. As per the World Bank, approximately 35% of cultivated land in South Asia is irrigated, yet inefficiencies in traditional methods lead to significant water waste. So, governments are promoting digital agriculture and smart technologies, due to which the adoption of smart irrigation systems is accelerating, particularly in developed economies such as Australia, Japan, and South Korea, where precision farming is already well established.

MARKET DRIVERS

Increasing Water Scarcity and Regulatory Push for Sustainable Practices

The growing concern over water scarcity and the regulatory push toward sustainable water use in agriculture is one of the primary drivers of the Asia Pacific Smart Irrigation Market. Countries across the region are experiencing acute water stress due to over-extraction, climate change, and inefficient irrigation practices. According to the Asian Development Bank, by 2050, a significant number of people in Asia will live under water-stressed conditions, significantly impacting agricultural productivity. This has prompted governments to implement policies encouraging water-efficient technologies.

In Australia, where agriculture accounts for about 70% of total water use, the National Water Initiative promotes efficient irrigation technologies. As per the Australian Bureau of Meteorology, water use efficiency improved between 2015 and 2022 due to such measures. These developments are driving the adoption of smart irrigation systems across the Asia Pacific region.

Technological Advancements and Integration of IoT in Agriculture

The rapid advancement in Internet of Things (IoT) technology and its integration into agricultural practices is another key driver of the Asia Pacific Smart Irrigation Market. IoT-enabled smart irrigation systems offer real-time monitoring of soil moisture levels, weather patterns, and crop health, allowing farmers to make data-driven decisions.

China made significant strides in agricultural IoT adoption, with more than 200,000 smart greenhouses equipped with sensors and automated irrigation systems as of 2023, according to the Chinese Academy of Agricultural Sciences. Apart from these, Japan’s Ministry of Agriculture, Forestry, and Fisheries has been supporting pilot projects that combine robotics and IoT in farming, with a focus on reducing labor dependency and enhancing resource efficiency.

Moreover, in Australia, the Commonwealth Scientific and Industrial Research Organisation (CSIRO) has launched precision agriculture initiatives that utilize satellite data and machine learning algorithms to manage irrigation. These technological innovations are further propelling the growth of the smart irrigation market in the Asia Pacific region.

MARKET RESTRAINTS

High Initial Investment and Limited Farmer Awareness

The high initial investment required for smart irrigation systems, coupled with limited awareness among smallholder farmers, is a major restraint affecting the growth of the Asia Pacific Smart Irrigation Market. While these systems promise long-term benefits in terms of water conservation and yield improvement, their upfront costs remain prohibitive for many farmers, especially in rural and less-developed regions.

According to the International Fund for Agricultural Development (IFAD), nearly 80% of farms in Asia are smallholdings of less than two hectares, and most operate on tight financial margins. In India, despite government schemes like PMKSY offering partial subsidies, the adoption rate remains low in states such as Bihar and Odisha due to poor outreach and lack of technical support.

Besides, as per a survey conducted by the Food and Agriculture Organization (FAO) in Southeast Asia, less than 25% of farmers were aware of the benefits of smart irrigation technologies. Many continue to rely on traditional flood irrigation methods, which are not only inefficient but also contribute to water wastage.

Inadequate Infrastructure and Connectivity Challenges

The inadequate infrastructure and connectivity challenges, particularly in rural areas where internet penetration and electricity supply remain inconsistent another critical restraint in the Asia Pacific Smart Irrigation Market. Smart irrigation systems heavily rely on stable internet connectivity to transmit real-time data from sensors and control units, but in many parts of the region, such infrastructure is either lacking or unreliable.

As per the International Telecommunication Union (ITU), internet penetration in rural areas of countries like India and Indonesia was below 40% in 2023, compared to over 80% in urban centers. This disparity limits the feasibility of deploying IoT-based irrigation solutions in remote agricultural zones. Moreover, power outages are common in regions such as Papua New Guinea and parts of the Philippines, making it difficult to maintain in continuous operation of smart irrigation equipment.

In Bangladesh, where agriculture contributes nearly 12% to GDP, only 65% of rural households had access to electricity as of 2022, according to the World Bank. Even when farmers are willing to adopt smart systems, inconsistent power supply hampers their effectiveness. In addition, the absence of trained personnel to install and maintain these systems further exacerbates the problem.

MARKET OPPORTUNITY

Expansion of Precision Agriculture and Digital Farming Initiatives

The expanding scope of precision agriculture and digital farming initiatives being adopted across the region presents a significant opportunity for the Asia Pacific Smart Irrigation Market. Governments and private enterprises are increasingly investing in digitizing agriculture to improve productivity, reduce input costs, and ensure food security. According to the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), digital agriculture has the potential to increase farm incomes across the region.

In China, the Ministry of Agriculture and Rural Affairs has launched the "Digital Agriculture and Rural Areas Development Plan”. As part of this plan, smart irrigation is being integrated with drone-based crop monitoring and AI analytics to optimize resource use. In Thailand, the Department of Agricultural Extension has partnered with local tech firms to roll out smart farming hubs that provide training and access to precision irrigation tools for smallholders.

Similarly, in Australia, the AgriFutures organization has funded several pilot projects that combine smart irrigation with blockchain traceability to enhance transparency in the supply chain. These initiatives indicate a strong shift towards digitally enabled farming ecosystems, where smart irrigation plays a central role.

Rising Government Support and Funding for Sustainable Agriculture

The increasing level of government support and funding aimed at promoting sustainable agriculture practices is another promising opportunity for the Asia Pacific Smart Irrigation Market. Several national and regional authorities are introducing policy incentives, subsidies, and research grants to encourage farmers to adopt water-efficient technologies. According to the Asian Development Bank (ADB), over USD 10 billion has been allocated across Asia for climate-resilient agriculture projects since 2020, with a significant portion directed toward smart irrigation development.

India's Ministry of Agriculture and Farmers' Welfare has extended subsidies covering up to 50–60% of the installation cost of micro-irrigation systems under the PMKSY scheme. In Vietnam, the Ministry of Agriculture and Rural Development has launched the "Smart Agriculture 2030" program, which includes provisions for funding smart irrigation trials in drought-prone provinces such as Ninh Thuan and Binh Thuan.

In South Korea, the Rural Development Administration (RDA) has been actively supporting R&D in smart farming technologies, including automated drip irrigation systems tailored for greenhouse cultivation. These government-led efforts are opening new avenues for market growth in the Asia Pacific region.

MARKET CHALLENGES

Complexity of Technology and Lack of Skilled Labor

The complexity of the technology involved and the lack of skilled labor required to operate and maintain these systems effectively are one of the major challenges facing the Asia Pacific Smart Irrigation Market. Unlike traditional irrigation methods, smart irrigation requires knowledge of software interfaces, sensor calibration, data interpretation, and troubleshooting. However, in many parts of the region, especially in rural areas, farmers lack formal training in digital agriculture tools.

In countries like Cambodia and Laos, where agriculture employs more than 30% of the workforce, digital literacy rates remain low, limiting the ability of farmers to fully utilize smart irrigation systems. A report by the International Labour Organization (ILO) highlighted that less than 15% of agricultural workers in the region have access to vocational training in agri-tech applications.

Furthermore, even when smart irrigation systems are installed, the lack of local technicians for maintenance results in downtime and reduced system efficiency. For example, in India, as per a study by the Indian Institute of Technology (IIT) Kanpur, nearly 40% of installed smart irrigation units remained non-operational after one year due to technical issues and unavailability of repair services.

Fragmented Supply Chain and Equipment Standardization Issues

The fragmented nature of the supply chain and the lack of standardized equipment specifications across different countries are other significant challenges confronting the Asia Pacific Smart Irrigation Market. Smart irrigation systems involve multiple components—sensors, controllers, valves, and software platforms—often sourced from various manufacturers. This fragmentation creates compatibility issues and complicates procurement, especially for small-scale farmers and local distributors.

For instance, in Southeast Asia, import regulations and varying certification requirements hinder the seamless movement of smart irrigation equipment across borders. According to the ASEAN Secretariat, differences in product compliance standards delay the availability of cutting-edge irrigation technologies in markets like Myanmar, Vietnam, and the Philippines. Moreover, the absence of universal calibration protocols for sensors and controllers affects the accuracy and interoperability of systems.

In India, despite domestic manufacturing growth, many high-end components still need to be imported, leading to price volatility and longer lead times. In Japan and Australia, while standardization is more advanced, integrating foreign-made components with local systems often requires additional engineering, raising costs and reducing adoption rates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.9% |

| Segments Covered | By irrigation Controller, Hardware and Network Component, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | Hunter Industries, Rain Bird Corporation, Netafim, HydroPoint Data Systems, Inc., Rachio Inc., The Toro Company, Calsense, Galcon, Blossom, and Green Electronics LLC (RainMachine). |

SEGMENTAL ANALYSIS

By Irrigation Controller Insights

The weather-based controllers segment led the Asia Pacific Smart Irrigation Market by accounting for 42.5% of the total business value in 2025. Mass adoption of weather-based systems in large-scale commercial farming and government-backed irrigation modernization projects across the region is primarily attributed to the dominance of the weather-based controllers segment. In addition, the availability of accurate climatic data and integration with cloud platforms, which enables automated decision-making without requiring physical sensors in the field, is another key driver behind the leading position of this segment. For instance, in China, the Ministry of Agriculture has collaborated with Huawei to integrate AI-powered weather analytics into irrigation scheduling, benefiting over 1.5 million hectares of farmland.

Furthermore, an additional major factor contributing to this segment’s leadership is the lower maintenance costs compared to sensor-based systems. Weather-based controllers do not require frequent calibration or on-ground installation of soil moisture or humidity sensors, reducing operational complexity. This makes them particularly attractive in countries like India and Indonesia.

Sensor-based controllers

A notable shift is occurring within the irrigation controller segment, emerging as the fastest-growing category, projected to register a CAGR of 18.6% during the forecast period. The rapid expansion of this segment can be attributed to increasing demand for real-time, hyper-localized irrigation decisions based on actual field conditions rather than generalized weather forecasts. In addition, the integration of IoT-enabled sensors with farm automation platforms, allowing for precise water delivery tailored to specific crop needs, is also a growth driver of this segment. Further, rising investments in precision horticulture and greenhouse farming are accelerating the adoption of sensor-based controllers. For example, in South Korea, the Rural Development Administration (RDA) has been promoting smart greenhouses using wireless soil sensors that communicate directly with irrigation control units. These systems have enabled yield increases while cutting water usage by nearly half in pilot projects conducted in Jeju Island and Gyeonggi Province.

By Hardware and Network Components

The sensors segment led the Asia Pacific Smart Irrigation Market by holding a share of 35.3% in 2025. Their critical role in enabling real-time monitoring of soil moisture, temperature, humidity, and other environmental variables essential for optimizing irrigation schedules is fuelling the dominance of the other sensors segment. Further, the increasing deployment of IoT-enabled sensors in precision agriculture, especially in countries like India and China, is one major reason for the growth of this segment. In China, the Ministry of Science and Technology reported that more than 800,000 acres of farmland are now monitored using wireless soil sensors integrated with AI-based irrigation management platforms.

Moreover, the expansion of agritech startups offering sensor-as-a-service models has significantly boosted adoption among smallholder farmers who may otherwise lack the capital for full system installations. As per a study by NASSCOM, agritech funding in India reached USD 350 million in 2023, with over 40% directed toward sensor-based irrigation and monitoring technologies.

Smart detection systems

In contrast, the smart detection systems segment is witnessing the most rapid growth. The rising need for predictive maintenance in irrigation networks, particularly in urban and industrial settings where water loss due to leaks can be substantial, is one key driver behind the high growth rate of the market detection systems segment. This segment includes advanced leak detection, flow anomaly identification, and fault monitoring systems that enhance the reliability and efficiency of smart irrigation infrastructure. According to the Asian Development Bank (ADB), non-revenue water losses in Southeast Asia range between 30% and 50%, prompting utilities and agro-industrial complexes to adopt smart detection technologies. For instance, in Malaysia, the National Water Services Commission (SPAN) reported a 22% reduction in distribution losses after implementing smart detection systems in Selangor's irrigation zones in 2023. Apart from these, advancements in machine learning and edge computing are enhancing detection accuracy, enabling early identification of pipeline bursts and pressure irregularities.

By Application Insights

The agriculture application segment continued to dominate the Asia Pacific Smart Irrigation Market by capturing a substantial share in 2025. The region’s heavy reliance on agriculture for food security, employment, and rural livelihoods is largely driving the overwhelming dominance of the agriculture application segment. In addition, a primary factor fueling this segment’s growth is the widespread implementation of government-led micro-irrigation programs, especially in countries like India and China. According to the Ministry of Jal Shakti, India’s Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) has facilitated the installation of smart drip and sprinkler systems across 9.8 million hectares of farmland as of 2023. These initiatives have contributed to an estimated 30% reduction in water consumption in targeted regions, as reported by the National Water Mission.

Furthermore, the expansion of contract farming and agri-tech partnerships is accelerating the adoption of smart irrigation in commercial agriculture. In China, Alibaba Cloud has partnered with local cooperatives to develop AI-driven irrigation platforms that optimize water use in large-scale rice and wheat plantations. According to the Chinese Academy of Agricultural Sciences, these efforts have improved yield efficiency in select provinces.

The non-agriculture segment —comprising landscaping, golf courses, parks, and urban green spaces—is emerging as the fastest-growing application area. The growth of this segment is fueled by increasing urbanization and the rising emphasis on sustainable city planning across the region. Also, an additional key driver behind this rapid expansion is the integration of smart irrigation in smart city initiatives, particularly in countries such as Singapore, South Korea, and Australia. According to the Urban Land Institute, Singapore has incorporated intelligent irrigation systems in over 60% of its public parks and roadside greenery, helping reduce municipal water usage by 25% since 2020. Similarly, in South Korea, the Seoul Metropolitan Government has mandated the use of smart irrigation in all new residential developments under its Green City Action Plan.

Besides, the growing investment in commercial real estate and luxury resorts is further boosting demand for automated landscape irrigation systems. These trends indicate that non-agricultural applications are gaining momentum, positioning this segment as a key growth engine in the Asia Pacific Smart Irrigation Market.

COUNTRY-LEVEL ANALYSIS

India Smart Irrigation Market Analysis

India remains among the top contributors to the Asia Pacific Smart Irrigation Market by holding a share of 18.4% in 2024. The country’s position is largely influenced by its vast agricultural base and strong policy backing for water-efficient technologies. Simultaneously, the rapid proliferation of agritech startups is playing a pivotal role in driving adoption. Companies like Fasal, Netafim India, and Intello Labs are offering cloud-connected sensor-based irrigation solutions tailored for smallholder farmers. A study by NASSCOM noted that agritech funding in India crossed USD 350 million in 2023, with irrigation-focused startups receiving a significant portion. Moreover, the Indian Space Research Organisation (ISRO) has launched satellite-based irrigation advisory services, providing real-time crop-specific recommendations to over 10 million farmers. These combined efforts are reinforcing India’s leadership position in the regional smart irrigation landscape.

China Smart Irrigation Market Analysis

China maintains the leading position in the Asia Pacific Smart Irrigation Market. This dominance is primarily driven by the country’s aggressive push toward digital agriculture and large-scale mechanization. Under the 14th Five-Year Plan, the Chinese government has prioritized smart irrigation as part of its broader strategy to achieve food security and sustainable resource management. A key growth enabler is the massive integration of IoT and AI technologies in state-backed agricultural projects. These systems utilize real-time data from soil sensors and weather stations to optimize water delivery, improving irrigation efficiency. Moreover, collaborative ventures between domestic tech giants and global agritech firms are accelerating innovation. Further, the government’s “Digital Village” initiative aims to bring smart irrigation tools to rural areas, leveraging mobile apps and blockchain traceability. These strategic interventions underscore China’s sustained leadership in shaping the future of smart irrigation in the Asia Pacific region.

Japan Smart Irrigation Market Analysis

Japan occupies a prominent position in the Asia Pacific Smart Irrigation Market. Despite its relatively smaller agricultural footprint compared to China and India, Japan’s advanced technological infrastructure and strong focus on automation make it a key player in the adoption of smart irrigation solutions. A major factor propelling market growth is the integrated use of robotics and AI in precision farming, particularly in controlled-environment agriculture. Apart from these, government incentives and research collaborations are fostering innovation in irrigation technologies. The New Energy and Industrial Technology Development Organization (NEDO) has funded multiple pilot projects integrating solar-powered smart irrigation systems with autonomous drones for crop monitoring. These initiatives reflect Japan’s commitment to maintaining high agricultural productivity despite a shrinking labor force and aging population, solidifying its role as a key market in the Asia Pacific region.

South Korea Smart Irrigation Market Analysis

South Korea holds a significant position in the Asia Pacific Smart Irrigation Market. The country’s well-developed digital infrastructure and proactive government policies have fostered the adoption of smart irrigation technologies, particularly in greenhouse farming and urban agriculture. The main growth drivers are the strong support from the Rural Development Administration (RD, which has been actively promoting smart farming through subsidies and R&D funding. In Jeju Island and Gyeonggi Province, pilot projects incorporating IoT-based soil moisture sensors have demonstrated a reduction in water usage while maintaining optimal crop yields, as per a 2023 RDA report. Moreover, the rise of vertical farming and indoor agriculture in urban centers is further boosting demand for efficient irrigation solutions. Companies like Farm8 and Sk Agrotech have introduced AI-integrated irrigation systems that adjust water delivery based on real-time environmental conditions.

Australia Smart Irrigation Market Analysis

Australia holds a notable position in the Asia Pacific Smart Irrigation Market. The country’s arid climate, coupled with its advanced agricultural technology ecosystem, positions it as a leader in smart irrigation adoption, particularly in viticulture, dairy farming, and broadacre cropping. One of the primary factors driving market growth is the ongoing modernization of irrigation infrastructure in response to prolonged droughts. According to the Australian Bureau of Meteorology, the Murray-Darling Basin—Australia’s largest agricultural region—experienced below-average rainfall for six consecutive years up to 2023, prompting increased investment in precision irrigation. Besides, collaborative research initiatives involving universities and agritech firms are accelerating innovation. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) has partnered with private enterprises to develop satellite-linked irrigation systems that provide real-time soil moisture data. These advancements are instrumental in supporting Australia’s goal of achieving sustainable water management in agriculture amid increasingly unpredictable climate conditions.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific Smart Irrigation Market is marked by a dynamic mix of global leaders and emerging regional players striving to capture market share through innovation and strategic positioning. As demand for water-efficient agricultural solutions grows, companies are intensifying efforts to differentiate themselves through technological advancements, localized offerings, and enhanced customer engagement. The market features a blend of established irrigation technology providers and agile agritech startups, each contributing unique value propositions to the evolving landscape. While multinational corporations leverage their extensive R&D capabilities and global experience, domestic firms capitalize on regional expertise and cost-effective deployment models. The increasing convergence of agriculture with digital technologies is further reshaping competitive dynamics, encouraging cross-industry collaboration between software developers, hardware manufacturers, and agricultural stakeholders. This evolving ecosystem fosters continuous innovation but also raises the bar for market entry and sustainability. As governments push for sustainable farming practices and digital agriculture adoption accelerates, the competitive intensity is expected to rise, prompting players to refine their strategies and adapt to the diverse needs of farmers across the Asia Pacific region.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific smart irrigation system market.

- Hunter Industries

- Rain Bird Corporation

- Netafim

- HydroPoint Data Systems, Inc.

- Rachio Inc

- The Toro Company

- Calsense

- Galcon

- Blossom

- Green Electronics LLC (RainMachine)

Top Players In The Market

- One of the leading players in the Asia Pacific Smart Irrigation Market is Netafim, a global pioneer in drip and micro-irrigation technologies. The company has been instrumental in introducing precision irrigation solutions tailored for diverse climatic and agricultural conditions across the region. Netafim actively collaborates with governments, agritech firms, and research institutions to promote sustainable water usage and improve farm productivity. Its strong presence in India, China, and Australia shows its regional influence and commitment to advancing smart farming practices.

- Another key player is The Toro Company, known for its advanced irrigation and turf management systems. In the Asia Pacific region, Toro has focused on delivering durable and technologically sophisticated irrigation solutions suited for both agriculture and landscaping applications. Through localized product development and strategic partnerships, the company has strengthened its foothold in high-growth markets such as Japan, South Korea, and Southeast Asia. Its emphasis on innovation and customer-centric offerings makes it a prominent contributor to the market’s evolution.

- Rain Bird Corporation is another major participant shaping the smart irrigation landscape in Asia Pacific. With a long-standing reputation for quality irrigation products, Rain Bird offers automated and sensor-based irrigation systems that cater to large-scale farms, golf courses, and urban green spaces. The company has invested significantly in expanding its distribution network and technical support infrastructure across the region. By aligning with local distributors and leveraging digital platforms, Rain Bird continues to enhance its market visibility and service capabilities in the Asia Pacific smart irrigation domain.

Top Strategies Used By Key Market Participants

Key players in the Asia Pacific Smart Irrigation Market are increasingly adopting strategic partnerships and collaborations to expand their regional footprint. By teaming up with local agritech startups, government bodies, and research institutions, companies can tailor their products to meet specific regional needs while gaining access to new customer bases and regulatory insights.

Another widely used strategy is technology integration and digital innovation . Leading firms are embedding IoT, cloud analytics, and AI into irrigation systems to offer real-time monitoring and automation. This enhances system efficiency and attracts tech-savvy farmers and agribusinesses looking for data-driven solutions that optimize water use and crop yield.

Moreover, localized distribution and after-sales support have become critical strategies for sustaining growth. Companies are investing in regional service centers, training programs, and direct-to-farmer engagement models to ensure seamless installation, maintenance, and troubleshooting. This approach not only improves customer satisfaction but also builds long-term brand loyalty in a competitive and evolving market environment.

RECENT MARKET NEWS

- In February 2024, Netafim launched a new line of solar-powered smart irrigation controllers designed specifically for off-grid farming communities in Southeast Asia. This initiative aimed at improving accessibility for smallholder farmers while reinforcing the company’s commitment to sustainable agriculture.

- In May 2024, The Toro Company partnered with an Australian agritech startup to integrate AI-based soil moisture analytics into its irrigation systems. This collaboration was intended to enhance precision irrigation capabilities and provide real-time decision-making tools to farmers across Australia and New Zealand.

- In August 2024, Rain Bird Corporation expanded its regional presence by opening a dedicated smart irrigation training and demonstration center in South Korea. The facility serves as a hub for farmer education, technical support, and product testing tailored to local agricultural conditions.

- In November 2024, Jain Irrigation Systems signed a memorandum of understanding with an Indian state government to deploy smart irrigation solutions across 100,000 hectares of farmland under a subsidized program. This move aimed to strengthen the company’s rural outreach and policy alignment.

- In January 2025, Hunter Industries introduced a mobile app-enabled irrigation control system for commercial landscaping projects in Singapore and Malaysia, targeting urban green space management and enhancing user experience through remote monitoring and automation.

MARKET SEGMENTATION

This research report on the Asia Pacific Smart Irrigation Market is segmented and sub-segmented into the following categories.

By Irrigation Controller

- WeaWeather-basedntrollers

- Sensor-based controllers

By Hardware and Network Components

- Sensor

- Water/flow meter

- Smart detection system

By Application

- Agriculture

- Non-agriculture

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is smart irrigation?

Smart irrigation refers to the use of advanced technologies such as sensors, automation systems, weather forecasting, and data analytics to optimize water usage in agriculture. These systems deliver precise amounts of water exactly when and where it's needed, improving efficiency and reducing waste.

Why is the Asia Pacific region becoming a key market for smart irrigation?

The Asia Pacific region faces increasing pressure on water resources due to rapid population growth, urbanization, and climate change. Countries like India, China, Australia, and Thailand are experiencing frequent droughts and declining groundwater levels. Smart irrigation offers a sustainable solution by enabling farmers to conserve water while maintaining crop yields, making it an essential technology for future agricultural practices in the region.

Which countries are leading the adoption of smart irrigation in the Asia Pacific?

China and India are at the forefront due to their massive agricultural sectors and growing government support for water-saving technologies. Australia is also a leader, especially in precision farming and large-scale commercial applications. Other emerging markets include Thailand, Vietnam, Indonesia, and South Korea, where adoption is being driven by both public and private sector initiatives.

How does government policy influence the growth of smart irrigation in Asia Pacific?

Governments across the region are playing a major role in promoting smart irrigation through subsidies, training programs, and investment in rural digital infrastructure. For example, India’s Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) encourages micro-irrigation systems, while China has launched national campaigns to modernize its agricultural water management systems. In Australia, water rights regulations encourage farmers to adopt efficient irrigation methods.

Who are the key players in the Asia Pacific smart irrigation market?

While global companies like Netafim, Jain Irrigation Systems, and The Toro Company have a strong presence in the region, local manufacturers and startups are gaining traction by offering cost-effective and region-specific solutions. Indian and Chinese firms, in particular, are developing affordable smart irrigation kits tailored for smallholder farmers.

How is mobile technology supporting smart irrigation in Asia Pacific?

Mobile phones are playing a crucial role in expanding access to smart irrigation tools. Many farmers now use smartphone apps to monitor soil moisture levels, receive alerts about optimal watering times, and even control irrigation systems remotely via IoT-enabled devices. Mobile connectivity has made these technologies accessible even in rural areas, helping bridge the digital divide in agriculture.

What impact does climate change have on the demand for smart irrigation?

Climate change has led to more erratic rainfall patterns, prolonged droughts, and rising temperatures—especially in parts of South and Southeast Asia. These changes make traditional irrigation methods less effective and increase the need for smarter, data-driven approaches. Smart irrigation systems help farmers adapt to changing environmental conditions by ensuring water is used efficiently and sustainably.

Are smallholder farmers adopting smart irrigation technologies?

Yes, but adoption is gradual. While initial costs can be a barrier, awareness campaigns, government subsidies, and the availability of modular, plug-and-play systems are encouraging small-scale farmers to try smart irrigation. In countries like India and Bangladesh, cooperative models are emerging where groups of farmers share smart irrigation equipment, lowering individual costs and increasing accessibility.

How is AI and IoT transforming smart irrigation in the region?

Artificial intelligence (AI) and the Internet of Things (IoT) are enabling more precise and automated irrigation decisions. For example, AI-powered platforms analyze historical and real-time data from sensors and satellites to predict crop water needs. IoT devices allow for remote control and monitoring of irrigation systems via smartphones or tablets—making it easier for farmers to manage water use effectively.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com