Asia Pacific Sterility Testing Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Product (Kits & Reagents, Instrument, Services), Test Type, Application, End-User, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$253 MnMarket Estimate, 2026

$278 MnMarket Forecast, 2034

$591 MnCAGR, 2026–2034

9.87%Asia Pacific Sterility Testing Market Report Summary

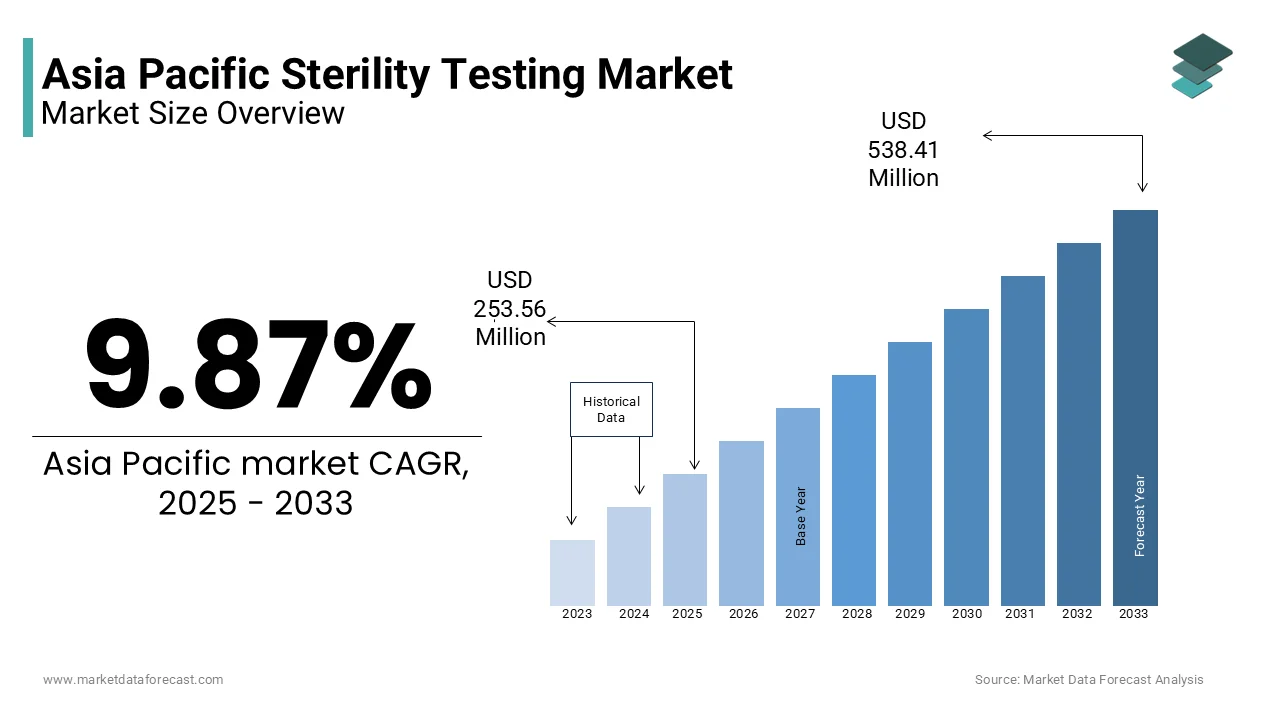

The Asia Pacific sterility testing market was valued at USD 253.56 million in 2025, is estimated to reach USD 278.59 million in 2026, and is projected to reach USD 591.56 million by 2034, growing at a CAGR of 9.87% during the forecast period from 2026 to 2034. The growth of the Asia Pacific sterility testing market is driven by expanding pharmaceutical and biotechnology industries, increasing production of sterile drugs and biologics, and stringent regulatory requirements for product safety and quality assurance. Rising investments in life sciences research, growing adoption of advanced sterility testing technologies, and increasing demand for quality control in pharmaceutical manufacturing are further supporting market expansion. Additionally, government initiatives promoting domestic pharmaceutical production and healthcare innovation are contributing to sustained market growth across the region.

Key Market Trends

-

Rising production of sterile pharmaceuticals, biologics, and cell and gene therapies is driving demand for advanced sterility testing solutions.

-

Increasing regulatory emphasis on product quality and patient safety is accelerating the adoption of validated sterility testing methods.

-

Growing automation of microbiological testing laboratories is improving testing efficiency, accuracy, and turnaround times.

-

Expanding investments in pharmaceutical manufacturing and biotechnology research are creating new opportunities for sterility testing providers.

-

Continuous advancements in rapid microbiological methods and automated testing systems are enhancing quality control processes.

Segmental Insights

-

Based on product, the kits and reagents segment dominated the Asia Pacific sterility testing market by accounting for 47.0% of the market share in 2025. The segment's leadership is attributed to the essential role of consumables in both manual and automated sterility testing workflows and their recurring demand across pharmaceutical and biotechnology laboratories.

-

Based on test type, the membrane filtration segment held the largest share of 62.7% of the Asia Pacific sterility testing market in 2025. The segment's dominance is driven by its broad applicability, high sensitivity, and compatibility with a wide range of pharmaceutical formulations, including products with antimicrobial properties.

-

Based on application, the pharmaceuticals segment accounted for 49.0% of the Asia Pacific sterility testing market revenue in 2025. The segment's growth is supported by increasing sterile drug manufacturing, stringent quality control requirements, and expanding pharmaceutical production capacities.

-

Based on end user, the pharmaceutical sector dominated the Asia Pacific sterility testing market by accounting for 63.3% of the market share in 2025. The segment's leadership is attributed to the large-scale production of sterile medicines, vaccines, and injectable products, along with strict regulatory compliance requirements.

Regional Insights

-

The Asia Pacific sterility testing market is witnessing robust growth due to increasing pharmaceutical production, expanding biotechnology research, and strengthening regulatory frameworks for product quality and safety.

-

China dominated the Asia Pacific sterility testing market by accounting for 28.3% of the regional market share in 2025. The country's leadership is supported by its large pharmaceutical and biotechnology industries, continuous government investments in life sciences, and growing focus on advanced quality assurance practices.

Competitive Landscape

The Asia Pacific sterility testing market is highly competitive, with leading companies focusing on advanced microbiological testing technologies, automation, and rapid sterility testing solutions to strengthen their market positions. Manufacturers are investing in research and development, strategic collaborations, and product innovation to improve testing accuracy, regulatory compliance, and operational efficiency for pharmaceutical and biotechnology manufacturers. Key players operating in the Asia Pacific sterility testing market include Avance Biosciences, Boston Scientific Corporation, Paragon Bioservices, Inc., Merck KGaA, Thermo Fisher Scientific, Inc., Charles River Laboratories International, Inc., Avista Pharma Solutions, and DYNALABS LLC.

Asia Pacific Sterility Testing Market Size

Asia Pacific Sterility Testing market size was valued at USD 253.56 million in 2025, and is expected to reach USD 591.56 million by 2034 from USD 278.59 million in 2026. The market's promising CAGR for the predicted period is 9.87% during the forecast period.

Sterility testing is a critical quality control process employed to ensure that pharmaceutical, biotechnological, and medical device products are free from viable microorganisms. In the Asia Pacific region, sterility testing has become an essential component of regulatory compliance, especially in sectors such as injectables, ophthalmics, implants, and tissue-based products. With rising healthcare expenditure, growing prevalence of infectious diseases, and increasing regulatory emphasis on product safety, the demand for robust sterility assurance mechanisms has surged.

The Asia Pacific region is witnessing significant investments in healthcare infrastructure and life sciences R&D, particularly in countries like China, India, Japan, and South Korea.

Moreover, the expansion of biosimilars and personalized medicine markets in the region is further driving the need for highly sensitive and compliant sterility testing frameworks.

MARKET DRIVERS

Expansion of Biopharmaceutical Manufacturing Capacity

One of the key drivers propelling the Asia Pacific sterility testing market is the rapid expansion of biopharmaceutical manufacturing facilities. Countries like India and China have emerged as major global hubs for active pharmaceutical ingredient (API) production and biologics manufacturing.

Biopharmaceuticals, including monoclonal antibodies, vaccines, and cell therapies, require stringent sterility assurance due to their sensitivity to microbial contamination and direct administration into the human body. These products often lack terminal sterilization steps, making in-process and final sterility testing indispensable.

For instance, in India, the government’s National Biopharma Mission has facilitated the establishment numerious biotech startups and manufacturing units since its launch in 2017, each requiring regulatory-grade sterility testing.

In addition, the rise in contract development and manufacturing organizations (CDMOs) in Southeast Asia, particularly in South Korea and Singapore, has amplified demand for outsourced sterility testing services.

This surge in biopharmaceutical output not only increases the volume of sterility tests conducted but also necessitates investment in modern microbiology labs equipped with automated detection systems and aseptic processing technologies.

Rising Incidence of Healthcare-Associated Infections (HAIs)

Another significant driver of the Asia Pacific sterility testing market is the increasing incidence of healthcare-associated infections (HAIs), which has prompted stricter infection control measures and enhanced sterility requirements for medical devices and injectable drugs.

In a study published by the WHO in 2021, approximately 15% of hospital patients in Southeast Asia acquired at least one HAI during their stay, compared to a global average of 7%. This alarming trend has led regulatory bodies such as Australia's Therapeutic Goods Administration (TGA) and China's National Medical Products Administration (NMPA) to implement more rigorous sterility validation standards for medical products.

Medical devices, especially implantables and surgical tools, are now subject to extensive sterility testing throughout their lifecycle. Simultaneously, the increasing use of prefilled syringes and auto-injectors in chronic disease management has raised concerns about microbial contamination risks. As healthcare-associated infections continue to pose serious public health challenges, manufacturers are compelled to invest heavily in sterility testing infrastructure and personnel training to meet evolving regulatory expectations and patient safety benchmarks.

MARKET RESTRAINTS

High Cost of Advanced Sterility Testing Equipment and Infrastructure

One of the primary restraints affecting the growth of the Asia Pacific sterility testing market is the high cost associated with setting up and maintaining advanced sterility testing facilities. Sterility testing requires specialized cleanroom environments, automated microbial detection systems, and trained microbiologists, all of which entail substantial capital and operational expenditures.

Moreover, ongoing maintenance, calibration of equipment, and compliance with Good Manufacturing Practice (GMP) standards add recurring costs that many small and medium-sized enterprises (SMEs) struggle to absorb.

In regions such as Vietnam and the Philippines, where the domestic pharmaceutical industry is still emerging, the lack of financial accessibility to such infrastructure limits the ability of local manufacturers to conduct in-house sterility testing. Consequently, they rely on foreign or regional CROs, which increases lead times and costs. These financial barriers hinder the widespread adoption of sterility testing, particularly among budget-constrained players, thereby slowing down market penetration and delaying regulatory approvals for new sterile products in parts of the Asia Pacific.

Regulatory Complexity and Divergent Compliance Standards

A major challenge restraining the Asia Pacific sterility testing market is the lack of harmonized regulatory standards across different countries in the region. Unlike the United States and the European Union, where the USP and Ph. Eur. guidelines provide a unified framework, Asia Pacific nations have varying regulatory requirements for sterility testing methodologies and documentation.

As per the Asia-Pacific Economic Cooperation (APEC) Regulatory Harmonization Steering Committee, these inconsistencies result in extended approval timelines and increased compliance costs for multinational pharmaceutical firms.

Additionally, according to the International Society for Pharmaceutical Engineering (ISPE), approximately 30% of sterility test failures in the region were attributed to deviations in methodology caused by misinterpretation of local regulations rather than actual product contamination. Such discrepancies not only delay market entry but also increase the burden on laboratories to maintain multiple testing protocols simultaneously.

Given the fragmented nature of regulatory enforcement in the Asia Pacific, manufacturers face difficulty achieving uniform sterility validation across national borders, limiting the scalability of operations and impeding the overall growth of the sterility testing sector in the region.

MARKET OPPORTUNITIES

Growth of Biosimilar and Cell & Gene Therapy Markets

The expanding biosimilar and cell and gene therapy sectors in the Asia Pacific present a substantial opportunity for the sterility testing market. With aging populations and rising incidence of chronic and oncologic diseases, the demand for advanced therapeutic solutions is surging, particularly in China, India, and South Korea.

These complex biological products must undergo rigorous sterility testing due to their susceptibility to microbial contamination and absence of terminal sterilization steps.

Cell and gene therapies represent another rapidly growing segment. In 2022, China authorized over 20 new cell therapy clinical trials, as per the China Food and Drug Administration (now NMPA). Many of these therapies involve autologous or allogeneic cellular manipulations, which mandate real-time sterility monitoring and end-product testing to ensure patient safety.

Furthermore, government initiatives such as India’s Biotechnology Industry Research Assistance Council (BIRAC) and Singapore’s Biomedical Sciences Initiative are accelerating the development of regenerative medicine platforms, each requiring dedicated sterility testing modules.

This shift toward precision medicine and advanced therapies is expected to drive demand for sterility testing services, particularly for rapid microbial detection technologies and aseptic processing validation, offering new growth avenues for both in-house QA labs and third-party service providers across the Asia Pacific.

Increasing Adoption of Rapid Microbial Detection Technologies

The adoption of rapid microbial detection technologies is opening new opportunities for the Asia Pacific sterility testing market. Traditional sterility testing methods, based on compendial culture techniques, often take up to 14 days to yield results—too slow for fast-moving biopharma supply chains. In response, many laboratories are transitioning to rapid microbiological methods (RMMs), which can detect microbial contamination within hours.

Countries like Japan and South Korea are leading the way in adopting technologies such as adenosine triphosphate (ATP) bioluminescence, flow cytometry, and nucleic acid amplification-based assays.

Similarly, in India, several CROs have integrated automated microbial detection systems such as Bact/Alert and BacT/ALERT 3D to expedite sterility analysis for injectables and vaccines.

Beyond speed, these technologies offer better sensitivity and reproducibility, aligning with the demands of the biopharma industry for real-time data and process monitoring.

MARKET CHALLENGES

Shortage of Skilled Microbiologists and Technical Personnel

A critical challenge impeding the growth of the Asia Pacific sterility testing market is the acute shortage of skilled microbiologists and technical personnel capable of conducting complex sterility assessments. Sterility testing is a highly specialized discipline that requires expertise in aseptic technique, microbial identification, and regulatory compliance—skills that remain scarce in many parts of the region.

Even in more developed economies like China and Malaysia, the ratio remains below optimal levels relative to the burgeoning pharmaceutical and medical device industries.

This talent gap is exacerbated by the limited availability of hands-on training programs and accredited certification courses in sterility assurance. For instance, in India, despite hosting over 3,000 pharmaceutical companies, only 12 institutions offer specialized training in pharmaceutical microbiology, as reported by the Association of Microbiologists of India in 2022.

Consequently, many organizations encounter delays in validating sterility protocols and launching new sterile products. Some resort to outsourcing, increasing dependency on a few large CROs, while others compromise on testing rigor, risking regulatory non-compliance.

Addressing this challenge will require strategic partnerships between academia, industry, and regulators to develop standardized educational pathways and practical training modules tailored to sterility testing needs.

Logistical Difficulties in Sample Transportation and Temperature Control

Logistical complexities related to the transportation and temperature stability of sterility samples pose a significant challenge in the Asia Pacific sterility testing market. Given the perishable nature of microbiological specimens, maintaining an unbroken cold chain from the point of collection to the testing laboratory is crucial to prevent false-negative results or microbial proliferation.

However, in geographically diverse and infrastructurally uneven regions such as Southeast Asia and Oceania, ensuring consistent refrigeration and timely delivery of samples remains a formidable task.

Moreover, cross-border logistics for outsourced sterility testing exacerbate the problem. Such logistical hurdles not only prolong testing cycles but also elevate the risk of regulatory rejection, particularly for time-sensitive products like vaccines and live biotherapeutics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.87% |

| Segments Covered | By Product, Test Type, Application, End-User, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Avance Biosciences (U.S.), Boston Scientific Corporation (U.S.), Paragon Bioservices, Inc (U.S.), Merck KGaA (Germany), Thermo Fisher Scientific, Inc. (U.S.), Charles River Laboratories International, Inc. (U.S.), Avista Pharma Solutions (U.S.), and DYNALABS LLC. (U.S.), and others |

SEGMENTAL ANALYSIS

By Product Insights

Among these, Kits & Reagents accounted for the largest market share of 47% in 2025. This dominance stems from the essential role these consumables play in both manual and automated sterility testing workflows.

One of the key drivers behind this segment’s lead is their high consumption rate across laboratories conducting sterility assessments on a daily basis. Each sterility test requires a fresh set of media, filters, and reagents, resulting in consistent demand.

Another major factor is the growing adoption of ready-to-use media and pre-filled growth media kits , which eliminate preparation steps and reduce contamination risks.

Moreover, the increasing number of sterility testing facilities—particularly in China and India—is further fueling demand for consumables.

Services is emerging as the fastest-growing segment , projected to register a CAGR of 13.6%. This rapid expansion reflects a strategic shift among pharmaceutical and biotech firms toward outsourcing sterility testing functions.

A primary reason for this surge is the escalating demand for contract testing solutions , especially among small and mid-sized enterprises (SMEs) that lack in-house capabilities.

Also, there is a notable rise in clinical trial activity and biosimilar development , both of which require extensive third-party validation. As per the 2023 regional outlook of the International Society for Pharmaceutical Engineering (ISPE), Asia Pacific accounted for 41% of global Phase I and Phase II clinical trials involving sterile injectables, most of which relied on external CROs for sterility evaluation.

Furthermore, regulatory pressures for adherence to international standards are prompting companies to engage accredited service providers capable of delivering ISO 14644-1 compliant testing environments and USP <71> validated results. These trends collectively underscore the accelerating momentum of the services segment in the sterility testing ecosystem.

By Test Type Insights

The Membrane Filtration method held the biggest market share at 62.7% in 2025. This dominance is attributed to the method’s broad applicability and compatibility with a wide array of formulations, particularly those with antimicrobial properties.

A key driver underpinning the popularity of membrane filtration is its superior efficiency in processing liquid and semi-liquid samples such as injectables, ophthalmics, and vaccines. Unlike direct inoculation, it allows for the concentration of microorganisms from large sample volumes onto a single filter, enhancing detection sensitivity.

In addition, the standardization of membrane filtration protocols by pharmacopoeias like the USP and Ph. Eur. has contributed to its widespread adoption.

Furthermore, the expansion of biopharma manufacturing zones in China and India has led to increased investment in high-throughput membrane filtration systems.

Direct Inoculation is emerging as the fastest-growing segment, expected to expand at a CAGR of 11.2% through 2034. Though traditionally less prevalent than membrane filtration, this method is gaining traction due to evolving application needs and technological advancements.

One of the core reasons behind its accelerated growth is the increasing use of direct inoculation for solid and semi-solid medical products, including implants, surgical devices, and certain tissue-based materials. These cannot be easily processed using membrane filtration due to solubility or particulate issues.

Additionally, improvements in broth formulation and incubation technology have enhanced the reliability and turnaround time of direct inoculation methods.

Moreover, in countries like Thailand and Vietnam, where smaller-scale biomanufacturers predominate, the cost-effectiveness and simplicity of direct inoculation make it an attractive option. These converging factors are positioning direct inoculation as a rapidly growing alternative within the Asia Pacific sterility testing framework.

By Application Insights

Pharmaceuticals remained the prominent segment, accounting for 49% of total market revenue in 2025. This strong hold is primarily due to the sheer volume of sterile drug production and the stringent sterility requirements enforced by regulatory authorities across the region.

Sterile injectables, eye drops, and inhalants constitute a significant portion of pharmaceutical output, all of which must undergo comprehensive sterility testing before release.

Another key driver is the large-scale generic drug manufacturing base in India and China, which supplies to both domestic and global markets. As reported by the Indian Drug Manufacturers' Association, over 80% of India’s pharmaceutical exports require sterility certification under WHO-GMP standards, significantly boosting testing volumes.

In addition, the expansion of Contract Development and Manufacturing Organizations (CDMOs) in South Korea and Singapore has intensified demand for sterility assurance services.

Lastly, regulatory tightening by bodies like the TGA in Australia and NMPA in China has mandated more frequent sterility evaluations throughout the product lifecycle.

Biological Manufacturing is experiencing the highest growth , projected to expand at a CAGR of 14.3%. This surge is fueled by the rapid proliferation of biologics and advanced therapy medicinal products (ATMPs) across the region.

One of the main contributors to this growth is the dramatic increase in monoclonal antibody (mAb) and vaccine production, particularly in response to the ongoing demand for immunotherapies and pandemic preparedness.

Moreover, the advent of cell and gene therapies in countries such as Japan and India is pushing manufacturers to adopt real-time sterility monitoring and aseptic processing controls. According to the Japanese Ministry of Health, Labour and Welfare, approvals for regenerative medicine products increased by 40% between 2021 and 2023, each requiring multiple rounds of sterility testing during development and commercialization.

Additionally, government-backed investments in biotechnology parks and innovation hubs are facilitating capacity expansion. With biological manufacturing continuing to outpace traditional pharmaceutical growth, sterility testing within this segment is positioned for sustained acceleration across the Asia Pacific.

By End-User Insights

The Pharmaceutical sector led the market , commanding a share of 63.3% in 2025. This overwhelming lead is primarily attributable to the vast scale of sterile drug manufacturing and the deep-rooted regulatory mandates governing product safety.

Sterile formulations such as injectables, ophthalmic solutions, and inhalers form a substantial portion of the pharmaceutical industry’s portfolio, necessitating rigorous sterility validation at every stage of production. According to the World Health Organization, over 55% of medicines consumed in Southeast Asia in 2023 were parenteral or topical formulations, all of which require sterility assurance prior to distribution.

Another key factor driving this segment is the massive presence of generic drug manufacturers in India and China , who supply to both domestic and international markets. .

Additionally, the expansion of Contract Manufacturing Organizations (CMOs) in South Korea and Singapore has further intensified demand for outsourced sterility testing.

Moreover, regulatory tightening by agencies like the Therapeutic Goods Administration (TGA) in Australia and the National Medical Products Administration (NMPA) in China has resulted in more frequent sterility audits and batch-specific validations, reinforcing the pharmaceutical industry’s central role in shaping the sterility testing market.

The Biotech industry is witnessing the most rapid expansion , anticipated to grow at a CAGR of 15.1%. This swift advancement is being propelled by the burgeoning production of advanced therapeutic products, including biosimilars, monoclonal antibodies, and cell and gene therapies.

A primary catalyst for this growth is the surge in biologics pipeline development , especially in China, Japan, and South Korea.

Moreover, the increasing government support for biotech innovation has played a critical role in scaling up sterility testing demand. In India, the Department of Biotechnology invested over USD 250 million in 2022–2023 to establish specialized biomanufacturing clusters, all of which incorporate in-house microbiology labs for sterility assurance.

Also, the rising number of clinical trials focused on cell and gene therapies is intensifying the need for real-time sterility monitoring and contamination-free processing. This confluence of scientific progress, policy backing, and expanding therapeutic applications is positioning the biotech sector as the fastest-growing contributor to sterility testing demand in the Asia Pacific.

REGIONAL ANALYSIS

China

China had the largest share of the Asia Pacific sterility testing market at 28.3% in 2025. This dominance is underpinned by its massive pharmaceutical and biotech industries, coupled with continuous government support for life sciences innovation.

A key growth driver is the expansion of biopharmaceutical manufacturing, particularly in regions like Shanghai, Suzhou, and Beijing.

Moreover, the National Medical Products Administration (NMPA) has strengthened sterility testing regulations, mandating stricter compliance with USP and Ph. Eur. standards.

Additionally, the explosion of contract research and manufacturing organizations (CRMOs) has amplified demand for outsourced sterility testing. These factors collectively reinforce China’s leadership in the Asia Pacific sterility testing domain.

India

India serves as a global hub for generic drug manufacturing and active pharmaceutical ingredient (API) production, both of which require stringent sterility certifications for export-bound products.

A major driver of this growth is the extensive network of WHO-GMP-certified facilities. These facilities are required to perform routine sterility testing to meet international regulatory standards, especially for injectables destined for the US and EU markets.

Additionally, government initiatives like Production Linked Incentive (PLI) schemes have spurred investments in domestic pharmaceutical infrastructure.

India is also experiencing a booming biotech startup ecosystem. Many of these startups focus on biosimilars and novel therapeutics, which inherently require rigorous sterility validation.

Furthermore, the expansion of contract testing laboratories such as SGS India and Eurofins Scientific has boosted accessibility to sterility testing services, enabling smaller manufacturers to comply with regulatory mandates without setting up in-house labs.

Japan

Japan is a key player in the market. Its mature pharmaceutical industry and strict adherence to international sterility standards contribute to its prominent position in the regional market.

The Japanese Ministry of Health, Labour and Welfare (MHLW) enforces rigorous sterility testing protocols aligned with USP and Ph. Eur. guidelines.

A key growth factor is the expansion of regenerative medicine and ATMP (Advanced Therapy Medicinal Products) development.

Additionally, pharmaceutical exports continue to drive sterility testing demand, particularly to North America and Europe. Moreover, investment in automation and rapid microbial detection technologies is gaining traction. Top Japanese firms such as Fujifilm Diosynth Biotechnologies and Takeda Pharmaceutical have upgraded their microbiology labs with ATP bioluminescence and flow cytometry-based sterility assays. With a robust regulatory framework and a strong emphasis on innovation, Japan remains a key player in the Asia Pacific sterility testing arena.

South Korea – Innovation-Driven Growth

South Korea is positioning itself as a key innovation hub in the region. This relatively compact but technologically advanced market is distinguished by its emphasis on cutting-edge pharmaceutical and biotech development.

A major driver is the rapid expansion of the domestic biopharmaceutical sector, particularly in the Seoul-Incheon-Busan corridor.

Another factor is the rising number of global clinical trials hosted in South Korea, many of which involve sterile investigational drugs. As per the Korean Ministry of Food and Drug Safety (MFDS), the country witnessed a 21% increase in Phase III clinical trials involving sterile biologics in 2023, all of which required extensive sterility testing.

Moreover, the adoption of digital quality management systems in pharmaceutical manufacturing has improved sterility testing traceability and compliance. Alongside government incentives promoting bio-convergence and personalized medicine, South Korea is leveraging its R&D strengths to carve a distinctive niche in the regional sterility testing market.

Australia

Australia is maintaining a strong foothold due to its well-developed healthcare infrastructure and stringent regulatory environment. Although not the largest market in volume, it is recognized for high-quality sterility assurance practices and a growing presence of contract testing organizations.

The Therapeutic Goods Administration (TGA) enforces strict sterility testing norms aligned with PIC/S GMP standards, compelling both domestic and imported sterile products to undergo thorough validation.

A key growth factor is the expansion of the biotech sector , particularly in Melbourne and Sydney. Many of these firms develop sterile injectables and regenerative therapies, necessitating reliable sterility testing partners.

Additionally, the presence of global CROs and local QA labs such as ALS Limited and Symbiosis Pty Ltd has enhanced accessibility to sterility testing services. With a commitment to quality and innovation, Australia continues to play a vital role in the Asia Pacific sterility testing ecosystem.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific sterility testing market is intensifying due to increasing demand from the pharmaceutical, biotechnology, and medical device sectors. A mix of global giants and regional players coexists, each striving to capture market share through differentiated offerings and enhanced service capabilities. While multinational corporations leverage their technological expertise and established distribution networks, local companies focus on cost-effective solutions and deep-rooted relationships with domestic manufacturers. The shift toward outsourcing sterility testing services has further diversified the competitive landscape, attracting niche contract laboratories that specialize in rapid microbial detection and aseptic processing validation. Additionally, advancements in automation and digital data integration are reshaping service delivery models, compelling firms to continuously innovate and upgrade infrastructure. Regulatory harmonization efforts and the emergence of biosimilar and cell therapy markets are also influencing competitive strategies, prompting companies to align closely with evolving compliance frameworks and industry-specific needs across the region.

KEY MARKET PLAYERS

Some of the key players in the Asia Pacific sterility testing market are

- Avance Biosciences (U.S.)

- Boston Scientific Corporation (U.S.)

- Paragon Bioservices, Inc. (U.S.)

- Merck KGaA (Germany)

- Thermo Fisher Scientific, Inc. (U.S.)

- Charles River Laboratories International, Inc. (U.S.)

- Avista Pharma Solutions (U.S.)

- DYNALABS LLC. (U.S.)

TOP PLAYERS IN THE MARKET

Several global and regional players operate within the Asia Pacific sterility testing market, offering a range of products and services including kits, instruments, and outsourced testing solutions. Among them, Thermo Fisher Scientific , Merck KGaA , and Sartorius AG stand out as key contributors to both the regional and global markets.

Thermo Fisher Scientific is a leading provider of laboratory equipment, consumables, and contract testing services. In the Asia Pacific region, the company plays a crucial role by supplying advanced sterility testing solutions to pharmaceutical and biotech firms. Its extensive product portfolio includes automated microbial detection systems and ready-to-use media, enabling efficient compliance with international sterility standards.

Merck KGaA contributes significantly through its broad range of high-quality microbiology media and reagents used in sterility assurance. The company supports research and quality control across the pharmaceutical and medical device industries in the region. With an emphasis on innovation and regulatory support, Merck enables manufacturers to meet evolving sterility validation requirements.

Sartorius AG is recognized for its cutting-edge filtration-based sterility testing systems and end-to-end solutions tailored for biopharmaceutical production. The company has been actively expanding its presence in the Asia Pacific through strategic partnerships and localized service offerings, strengthening sterility testing infrastructure across emerging markets.

TOP STRATEGIES USED BY KEY PLAYERS

Leading players in the Asia Pacific sterility testing market are employing a range of strategies to consolidate their market position and enhance competitive advantage. One major approach is expanding regional footprint through localized manufacturing and distribution hubs , allowing companies to improve supply chain efficiency and better serve growing pharmaceutical and biotech sectors.

Another prevalent strategy is investing in R&D to develop innovative sterility testing technologies , particularly focusing on rapid microbial detection and automation to meet the rising demand for faster and more reliable results. This not only enhances product portfolios but also aligns with evolving regulatory expectations.

Additionally, forming strategic collaborations with CROs and academic institutions has become a key tactic among market leaders. These partnerships help drive technology adoption, support clinical sterility validation, and facilitate knowledge transfer, thereby reinforcing brand authority and customer trust across the Asia Pacific region.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Thermo Fisher Scientific launched a new line of automated microbial detection systems tailored for sterility testing in biopharma applications. This move was aimed at enhancing accuracy and reducing time-to-result for manufacturers across China and India, improving operational efficiency and compliance readiness.

- In May 2023, Sartorius AG expanded its facility in Singapore to include a dedicated sterility assurance center focused on supporting biologics and vaccine producers in the region. The expansion was designed to offer integrated testing workflows and technical consultations, strengthening its foothold in Southeast Asia.

- In July 2025, Merck KGaA partnered with a leading Japanese pharmaceutical manufacturer to co-develop customized media solutions for sterility validation, ensuring compatibility with novel drug formulations and adhering to stringent regulatory protocols specific to the Asia Pacific market.

- In September 2023, Charles River Laboratories opened a new contract sterility testing lab in Shanghai, aiming to address the rising outsourcing demand from Chinese biotech firms and accelerate product release cycles without compromising sterility assurance.

- In January 2025, Becton Dickinson announced a collaboration with a South Korean biopharma incubator to provide on-site sterility testing training and equipment support, facilitating early-stage companies in meeting international sterility standards and streamlining regulatory submissions.

MARKET SEGMENTATION

This research report on the Asia Pacific sterility testing market has been segmented and sub-segmented based on the following categories.

By Product

- Kits & Reagents

- Services

- Instruments

By Test Type

- Membrane Filtration

- Direct Inoculation

- Other Tests

By Application

- Pharmaceuticals And Biologicals

- Medical Devices

- Other Applications

By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific Sterility Testing Market?

The Asia Pacific Sterility Testing Market comprises products, instruments, kits, and services used to verify the sterility of pharmaceuticals, biologics, medical devices, and other healthcare products across countries in the Asia-Pacific region.

2. What is sterility testing and why is it important?

Sterility testing is a microbiological procedure used to confirm that sterile products are free from viable microorganisms, ensuring product safety, regulatory compliance, and patient protection.

3. What factors are driving the growth of the Asia Pacific Sterility Testing Market?

The market is driven by the rapid expansion of pharmaceutical and biotechnology industries, increasing biologics and vaccine production, stringent regulatory standards, and rising healthcare investments.

4. Which industries use sterility testing in Asia Pacific?

Sterility testing is widely used by pharmaceutical manufacturers, biotechnology companies, medical device manufacturers, contract research organizations (CROs), contract development and manufacturing organizations (CDMOs), and quality control laboratories.

5. What are the major sterility testing methods?

The primary sterility testing methods include membrane filtration, direct inoculation, and rapid microbiological methods, each selected based on product type and testing requirements.

6. Which countries are leading the Asia Pacific Sterility Testing Market?

China, Japan, India, South Korea, and Australia are leading markets due to their expanding pharmaceutical manufacturing, biotechnology research, and strong regulatory frameworks.

7. What products require sterility testing?

Sterility testing is commonly performed on injectable drugs, biologics, vaccines, ophthalmic products, intravenous solutions, implantable medical devices, cell and gene therapies, and surgical products.

8. What are the key challenges in the Asia Pacific Sterility Testing Market?

Major challenges include high testing costs, strict regulatory compliance, lengthy testing procedures, contamination risks during testing, and the need for skilled laboratory personnel.

9. What are the latest trends in the Asia Pacific Sterility Testing Market?

Current trends include the adoption of rapid sterility testing technologies, laboratory automation, digital quality management systems, and increased outsourcing of microbiological testing services.

10. What is the future outlook for the Asia Pacific Sterility Testing Market?

The Asia Pacific Sterility Testing Market is expected to witness steady growth over the forecast period, supported by expanding pharmaceutical manufacturing, increasing investments in biologics, technological advancements in rapid sterility testing, and growing demand for quality assurance in healthcare products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com