Asia Pacific Switchgear Market Market Research Report – Segmented By Voltage Type ( Low Voltage, Medium Voltage, High Voltage), Insulation, End-User, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Market Size, 2025

$121.45 BnMarket Estimate, 2026

$130.37 BnMarket Forecast, 2034

$229.93 BnCAGR, 2026–2034

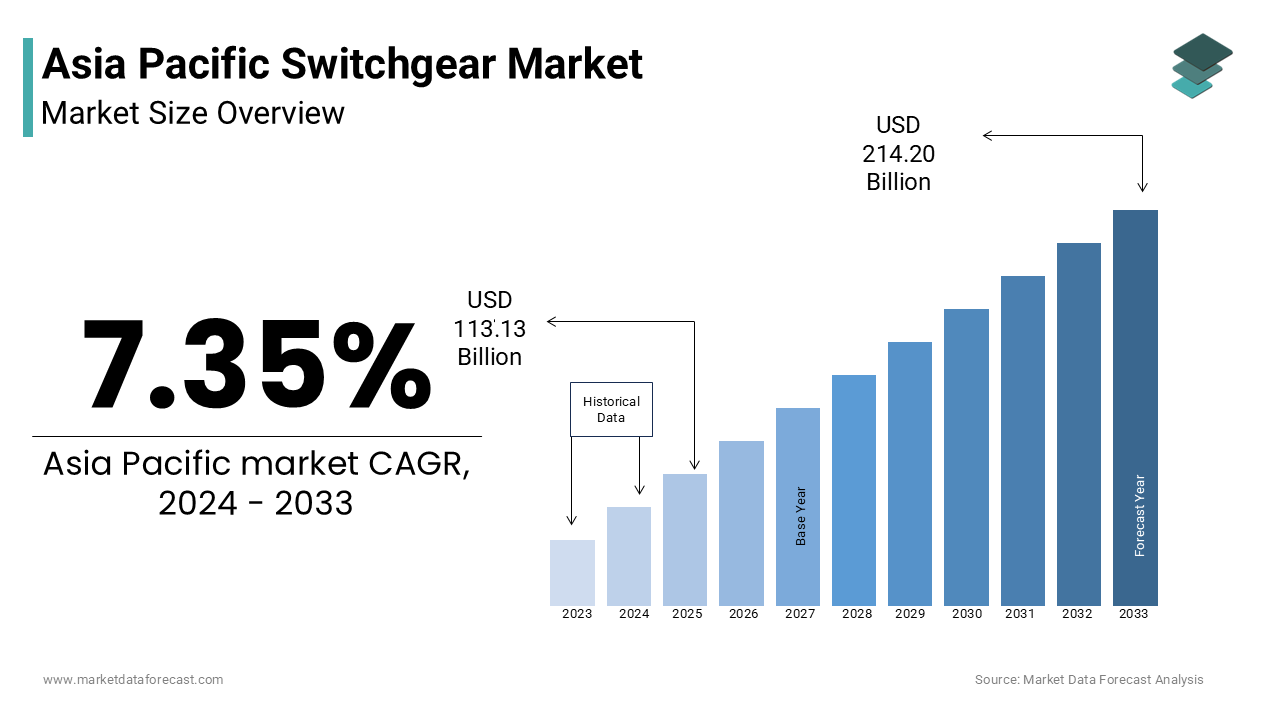

7.35%Asia Pacific Switchgear Market Size

The Asia Pacific switchgear market size was valued at USD 121.45 billion in 2025 and is anticipated to reach USD 130.37 billion in 2026 from USD 229.93 billion by 2034, growing at a CAGR of 7.35% during the forecast period from 2026 to 2034.

Switchgear in electrical systems is used for controlling, protecting, and isolating electrical equipment across various industries. In the Asia Pacific region, switchgear plays a foundational role in managing power distribution networks, industrial operations, and infrastructure development. It encompasses both low voltage (LV) and medium voltage (MV) systems, serving applications in energy, manufacturing, transportation, and commercial sectors. The Asia Pacific switchgear market is being shaped by rapid urbanization, growing investments in renewable energy integration, and government-led infrastructure projects. Countries like China, India, Japan, and South Korea are at the forefront of adopting advanced switchgear technologies that offer higher reliability, remote monitoring, and improved safety features.

MARKET DRIVERS

Expansion of Renewable Energy Infrastructure

One of the key drivers of the Asia Pacific switchgear market is the rapid expansion of renewable energy infrastructure, particularly solar and wind power installations. Governments across the region are aggressively pursuing clean energy targets to reduce carbon emissions and enhance energy security. For instance, as per the International Renewable Energy Agency (IRENA), the Asia Pacific region added over 200 gigawatts of new renewable capacity in 2023, with China and India accounting for nearly half of this growth. These energy sources require robust and efficient switchgear systems to manage variable power inputs, ensure grid stability, and enable seamless integration with existing power networks. Moreover, renewable energy plants often operate under fluctuating conditions, necessitating the use of high-performance switchgear that can handle intermittent loads and protect against surges or faults. This has led to increased deployment of gas-insulated and vacuum circuit breakers, which offer superior performance in such environments.

Industrialization and Smart City Development

Industrialization and the rise of smart city initiatives across the Asia Pacific region are significantly boosting the demand for advanced switchgear systems. Rapid urbanization, coupled with the expansion of manufacturing zones and special economic areas, is driving the need for reliable and intelligent power distribution systems. Smart cities require integrated energy management systems, where switchgear plays a crucial role in ensuring uninterrupted power supply and real-time fault detection. In countries like Singapore, India, and China, the implementation of smart grids and automated substations has created a strong demand for digital switchgear equipped with sensors and remote control capabilities.

MARKET RESTRAINTS

Supply Chain Disruptions and Component Shortages

A major restraint affecting the Asia Pacific switchgear market is the ongoing challenge of supply chain disruptions and shortages of critical components such as semiconductors, copper, and insulating materials. The global semiconductor shortage, which intensified during the pandemic and persisted into 2023, has impacted the production of smart switchgear units that rely on microchips for automation and communication functions. As reported by BloombergNEF, several manufacturers in China and South Korea faced delays in product deliveries due to prolonged lead times for electronic components, directly affecting project timelines and installation schedules.

Additionally, geopolitical tensions and trade restrictions have disrupted raw material flows, leading to price volatility and procurement difficulties. Copper, a primary material used in electrical conductors, saw significant price fluctuations in 2023, driven by supply constraints in South America and rising demand from the EV and renewable sectors.

Regulatory and Compliance Complexities Across Countries

Another significant constraint is the varying regulatory standards and compliance requirements across the Asia Pacific countries. Unlike Europe or North America, where harmonized standards facilitate easier cross-border operations, APAC markets face fragmentation in technical specifications, testing protocols, and certification procedures. For example, while India follows the Indian Standards Institution (BIS) norms, China adheres to GB standards, and Japan has its own set of JIS regulations. This lack of uniformity complicates product design, testing, and approvals, thereby increasing time-to-market and development costs. According to a white paper issued by the Confederation of Indian Industry (CII), many multinational switchgear manufacturers must maintain separate production lines or modify designs to meet local requirements, reducing economies of scale. Moreover, changing environmental regulations such as SF6 gas emission controls in high-voltage switchgear are pushing companies to adopt alternative insulation technologies, which require additional investment and R&D efforts.

MARKET OPPORTUNITIES

Growth in Electric Vehicle Charging Infrastructure

The rapid proliferation of electric vehicles (EVs) across the Asia Pacific region presents a significant opportunity for the switchgear market. As governments push for decarbonization and stricter emissions regulations, the EV sector is expanding at an unprecedented rate. According to the International Energy Agency (IEA), the number of electric cars on APAC roads surpassed 25 million in 2023 with China alone accounting for over two-thirds of this figure. This surge in EV adoption necessitates widespread deployment of charging infrastructure, including fast-charging stations and grid-connected hubs, all of which require high-performance switchgear for safe and efficient power distribution.

In addition to public charging networks, industrial and commercial fleets are transitioning to electric alternatives, further amplifying the demand for switchgear solutions that can manage high-load cycles and ensure grid stability. Companies are increasingly investing in modular and scalable switchgear systems designed specifically for EV charging applications. As per a study conducted by Wood Mackenzie, the integration of bidirectional chargers and vehicle-to-grid (V2G) technologies is expected to drive innovation in switchgear design by creating new revenue streams for manufacturers operating in the APAC region.

Adoption of Digital Substations and Smart Grid Technologies

The transition toward digital substations and smart grid systems is opening up substantial opportunities for switchgear providers in the Asia Pacific market. Traditional power systems are being upgraded to accommodate real-time monitoring, remote diagnostics, and automated fault detection capabilities made possible through intelligent electronic devices (IEDs) and digitally enabled switchgear. As per a report published by Siemens Energy, over 40% of new substation projects in APAC now include digital architecture, which is driven by the need for enhanced grid reliability and cybersecurity.

Countries like Japan, South Korea, and Singapore are leading the way in deploying digital substations, supported by national smart grid initiatives and investments in AI-driven energy management. Meanwhile, emerging economies such as India and Indonesia are focusing on rural electrification programs that integrate smart metering and grid automation, further boosting the demand for next-generation switchgear.

MARKET CHALLENGES

Integration of Legacy Systems with Modern Technologies

One of the foremost challenges confronting the Asia Pacific switchgear market is the integration of legacy infrastructure with modern, digitally enabled systems. Many power distribution networks across the region still rely on outdated equipment installed decades ago, which lacks compatibility with contemporary smart switchgear solutions. This technological disparity not only increases maintenance costs but also limits the scalability of smart grid implementations. Retrofitting old systems with new switchgear often requires extensive engineering modifications, leading to extended downtimes and budget overruns. In countries like Thailand and the Philippines, where power infrastructure modernization efforts are still in early stages, the lack of standardized protocols further complicates interoperability between legacy and new equipment.

Rising Cybersecurity Concerns in Connected Switchgear Systems

As switchgear becomes increasingly connected and digitized, cybersecurity concerns are growing across the Asia Pacific region. With the incorporation of IoT-enabled devices, cloud-based monitoring, and remote control functionalities, switchgear systems are now exposed to cyber threats that could disrupt power distribution and compromise grid integrity. Ensuring secure communication between intelligent switchgear units and central control systems has become a priority for utility operators and regulators alike. However, implementing robust cybersecurity measures often involves significant capital expenditure and specialized expertise, which many regional players may lack.

SEGMENTAL ANALYSIS

By Voltage Type Insights

The low voltage segment dominated the Asia Pacific switchgear market by accounting for 58.3% of the share in 2024. One of the key drivers behind this segment's growth is the rapid expansion of urban infrastructure and smart city initiatives across the region. Countries like India, China, and Indonesia are investing heavily in new construction and modernization of existing power systems. Another major contributing factor is the surge in renewable energy integration, especially solar rooftop installations and small-scale wind projects that operate at low voltage levels. Moreover, industrial automation and factory electrification are boosting LV switchgear adoption. In manufacturing hubs such as Vietnam and Thailand, the rise in production lines requiring precise power control is increasing reliance on compact and modular LV switchgear solutions.

The medium voltage switchgear segment is projected to grow with a CAGR of 7.4% from 2025 to 2033. A primary growth catalyst is the expansion of industrial parks and special economic zones, particularly in emerging economies like India, Indonesia, and the Philippines. These regions are witnessing large-scale investments in sectors such as textiles, automotive, food processing, and pharmaceuticals, all of which require MV switchgear to manage higher loads efficiently. According to McKinsey & Company (2023), India alone plans to establish over 50 new industrial corridors by 2030, significantly boosting demand for MV systems. Additionally, the modernization of national power grids and substations is accelerating the deployment of MV switchgear. Governments across APAC are upgrading aging infrastructure to enhance grid reliability and accommodate rising electricity consumption.

By Insulation Insights

The air-insulated segment was the largest in the Asia Pacific switchgear market by occupying a dominant share in 2024. One of the key reasons for AIS dominance is its extensive use in urban and rural power distribution networks, where budget constraints and accessibility play a crucial role in technology selection. In developing economies such as India, Bangladesh, and Indonesia, governments are prioritizing cost-efficient electrification programs, favoring air-insulated systems that are easier to install and maintain. Another major driver is the high adaptability of AIS in both indoor and outdoor environments, especially in industrial and commercial settings. Unlike gas-insulated alternatives, air-insulated systems do not require specialized enclosures or complex monitoring mechanisms, making them ideal for harsh climates and remote locations. Furthermore, retrofitting and expansion of existing power infrastructure also favor AIS adoption.

The gas-insulated segment is anticipated to register a CAGR of 8.2% in the next coming years. One of the primary growth drivers is the increasing deployment of GIS in densely populated cities, where land availability is limited and compact electrical infrastructure is essential. In megacities like Tokyo, Shanghai, and Mumbai, utilities are opting for GIS due to its smaller footprint, enhanced safety features, and reduced electromagnetic interference. Another key factor is the adoption of GIS in high-reliability applications, particularly in critical infrastructure such as hospitals, airports, and data centers. These sectors demand uninterrupted power supply and minimal maintenance downtime, areas where GIS excels due to its sealed design, longer operational life, and resistance to environmental stressors.

By End-use Insights

The T&D utilities segment was the largest by capturing 48.6% of the Asia Pacific switchgear market share in 2024. Countries like China, India, and Japan are actively upgrading aging infrastructure to improve efficiency and reduce losses. Additionally, the integration of renewable energy sources into the grid is increasing the complexity of power transmission, necessitating advanced switchgear solutions. Wind and solar farms often feed power into the grid intermittently, requiring sophisticated protection and switching mechanisms to prevent disruptions. Moreover, government-led rural electrification programs, particularly in Southeast Asia and South Asia, are expanding the reach of national grids, thereby increasing the demand for T&D-grade switchgear.

The industrial segment is projected to grow with a 7.8% CAGR in the coming years. One of the primary growth enablers is the rise in factory automation and smart manufacturing, particularly in countries like Vietnam, Thailand, and Malaysia. As industries adopt Industry 4.0 technologies, there is a growing need for intelligent switchgear systems that support real-time monitoring, predictive maintenance, and energy optimization. Another key driver is the establishment of new industrial parks and special economic zones, especially in India and Indonesia. These zones attract foreign direct investment and foster the growth of energy-intensive sectors such as automotive, electronics, and chemicals.

REGIONAL ANALYSIS

China Switchgear Market Insights

China was the largest contributor with 35.4% of the Asia Pacific switchgear market share in 2024. The country’s State Grid Corporation and China Southern Power Grid are spearheading nationwide infrastructure upgrades, focusing on smart grid implementation and ultra-high-voltage transmission projects. According to the National Development and Reform Commission (NDRC), China invested over CNY 600 billion (USD 84 billion) in power infrastructure in 2023 alone, significantly boosting procurement of both medium and high voltage switchgear. In addition, the surge in renewable energy integration is shaping switchgear demand. China leads the world in installed solar and wind capacity, and as per the National Renewable Energy Centre (NREL), over 150 GW of new renewable capacity was commissioned in 2023, necessitating advanced switchgear for grid synchronization and protection.

India Switchgear Market Insights

India was positioned second by holding 20.3% of the Asia Pacific switchgear market share in 2024. India’s Power for All initiative, coupled with schemes like Deen Dayal Upadhyaya Gram Jyoti Yojana (DDUGJY) and Saubhagya, has brought electricity access to nearly 98% of the population, as reported by the Ministry of Power. Industrial growth is another major driver. With the Make in India campaign promoting domestic manufacturing, numerous new industrial parks and production units are being established, each requiring robust electrical infrastructure. Additionally, the booming EV and renewable energy sectors are reshaping the market landscape. The government aims to achieve 500 GW of non-fossil fuel-based energy capacity by 2030, which will require extensive deployment of switchgear in solar farms, wind parks, and EV charging stations. Indian companies like BHEL, Crompton Greaves, and Havells are capitalizing on this trend by offering tailored switchgear solutions, while international players are strengthening their foothold through strategic acquisitions and joint ventures.

Japan Switchgear Market Insights

Japan switchgear market is growing substantially in the next coming years. Following the Fukushima nuclear disaster, Japan has been transitioning toward a diversified energy mix, incorporating more renewables, LNG, and battery storage systems. According to the Ministry of Economy, Trade and Industry (METI), Japan added over 10 GW of new solar capacity in 2023, which requires modern switchgear to integrate these intermittent sources into the grid effectively. The country is also a leader in smart grid and digital substation technologies, with companies like Toshiba, Hitachi, and Mitsubishi Electric pioneering innovations in IoT-enabled switchgear and condition-monitoring systems. Government-backed initiatives and private sector investments are jointly addressing this challenge by ensuring sustained demand for high-performance switchgear solutions.

South Korea Switchgear Market Insights

South Korea switchgear market growth is driven by the tech-savvy infrastructure and early adoption of smart technologies. South Korea is rapidly evolving into a regional hub for intelligent switchgear and digital substation deployments. The country’s Smart Grid Development Act, introduced in 2011, laid the foundation for widespread adoption of automated power systems. Additionally, the Korean New Deal policy, launched in 2020, emphasizes green growth and digital transformation, directly influencing the power sector. KEPCO’s Digital Grid Initiative includes investments in AI-driven grid management and hydrogen-powered generation, all of which require advanced switchgear capable of handling bidirectional power flows and dynamic load conditions.

Australia Switchgear Market Insights

Australia switchgear market growth is likely to grow in the next coming years. The Australian Energy Market Operator (AEMO) oversees a complex and decentralized grid, integrating a growing share of renewables. According to the Clean Energy Council, renewable energy contributed over 35% of Australia’s electricity generation in 2023 by necessitating advanced switchgear for grid stability and fault protection. Australia is also a leader in grid-forming inverters and hybrid energy systems, particularly in remote mining and off-grid communities. The country’s National Hydrogen Strategy and investment in pumped hydro storage are driving the need for intelligent switchgear capable of managing variable power inputs and bidirectional flows.

COMPETITIVE LANDSCAPE

The Asia Pacific switchgear market is marked by intense competition among global giants and emerging regional players vying for dominance in a rapidly evolving power infrastructure landscape. Established multinational corporations such as Siemens, ABB, and Schneider Electric maintain a strong presence due to their technological expertise, extensive product portfolios, and established distribution networks. However, domestic manufacturers from China, India, and South Korea are gaining traction by offering cost-effective solutions tailored to local needs. These regional players benefit from favorable government policies, lower production costs, and proximity to end-users, allowing them to compete more effectively against global firms. The market is further influenced by shifting energy policies, increasing investments in smart grids, and the push for sustainable and efficient power systems. The convergence of automation, renewable integration, and digital substation technologies is reshaping the competitive landscape, pushing firms to continuously adapt and invest in next-generation solutions that meet evolving market expectations.

KEY MARKET PLAYERS

Key market players in the Asia Pacific Switchgear Market include

- ABB Ltd.

- Siemens AG

- Schneider Electric

- Eaton Corporation

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Larsen & Toubro Limited

- CG Power and Industrial Solutions Ltd.

- Hyundai Electric & Energy Systems Co., Ltd.

- Hyosung Corporation

Top Players in the Asia Pacific Switchgear Market

Siemens Energy

Siemens Energy is a leading global player with a strong presence in the Asia Pacific switchgear market. The company offers a comprehensive portfolio of low, medium, and high voltage switchgear solutions tailored for utility, industrial, and commercial applications. In the APAC region, Siemens plays a pivotal role in advancing smart grid technologies and digital substations. Its focus on innovation, sustainability, and digitalization has positioned it as a preferred partner for governments and private utilities modernizing power infrastructure. Through localized manufacturing and strategic collaborations, Siemens continues to drive technological advancements that influence both regional and global switchgear standards.

Schneider Electric

Schneider Electric is a major contributor to the Asia Pacific switchgear landscape, known for its energy management and automation solutions. The company delivers a wide range of eco-efficient, modular, and smart switchgear systems designed for enhanced reliability and reduced environmental impact. In APAC, Schneider actively supports the transition toward decentralized energy systems, renewable integration, and digital transformation in electrical infrastructure. The company strengthens its position by aligning product development with evolving regulatory and sustainability demands across key markets like India, China, and Southeast Asia.

ABB Ltd.

ABB is a global leader in power technologies and a dominant force in the Asia Pacific switchgear sector. The company specializes in gas-insulated and air-insulated switchgear systems used in transmission, distribution, and industrial applications. ABB’s contributions include pioneering innovations in arc-resistant switchgear, digital protection relays, and condition monitoring systems. In the APAC region, ABB collaborates closely with national utilities and industrial clients to deploy advanced switchgear that enhances grid resilience and operational efficiency. Its commitment to electrification, automation, and sustainable infrastructure makes ABB a key influencer in shaping the future of the global switchgear industry.

Top Strategies Used by Key Market Participants

Localization of Manufacturing and Service Facilities

Key players are increasingly establishing or expanding local production units and service centers across the Asia Pacific region. This strategy allows companies to better serve regional demand, reduce logistics costs, and comply with local regulations. It also enables faster response times to customer needs and facilitates after-sales support, which is crucial in a capital-intensive industry like switchgear manufacturing.

Focus on Digital and Smart Grid Technologies

Leading companies are investing heavily in research and development to integrate digital capabilities into their switchgear offerings. This includes IoT-enabled devices, predictive maintenance tools, and remote monitoring systems that enhance performance and safety. Manufacturers aim to meet the growing demand for intelligent power management solutions driven by urbanization and renewable energy expansion by incorporating these smart technologies.

Strategic Partnerships and Collaborations

To strengthen their foothold in the competitive APAC market, top players are forming alliances with local firms, academic institutions, and government bodies. These partnerships help them gain insights into regional market dynamics, navigate regulatory landscapes, and co-develop customized solutions. Additionally, they enable joint ventures in pilot projects, technology transfer, and capacity-building initiatives, which reinforce long-term business growth and brand credibility.

RECENT MARKET DEVELOPMENTS

- In February 2024, Siemens Energy launched a new smart switchgear manufacturing facility in Singapore, aimed at catering to the growing demand for compact and digitally integrated power systems in Southeast Asia.

- In May 2023, Schneider Electric partnered with a leading Indian engineering firm to develop customized switchgear solutions for the country’s rural electrification and renewable energy projects, by enhancing its regional deployment capabilities.

- In September 2023, ABB announced a collaboration with a Japanese utility provider to supply advanced GIS (Gas-Insulated Switchgear) units for Tokyo’s upcoming smart city initiative, which is strengthening its foothold in Japan’s premium power infrastructure market.

- In November 2024, Hyundai Electric & Energy Systems expanded its R&D center in South Korea to focus on developing eco-friendly switchgear using alternative insulation gases by aligning with the country’s green transition goals and positioning itself as a leader in sustainable power technologies.

SEGMENTAL ANALYSIS

This research report on the Asia Pacific switchgear market is segmented and sub-segmented into the following categories.

By Voltage Type

- Low Voltage

- Medium Voltage

- High Voltage

By Insulation

- Air

- Gas

By End-use

- T&D Utilities

- Commercial & Residential

- Industrial

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the switchgear market in the Asia Pacific region?

The market is primarily driven by rapid urbanization, rising electricity demand, growing renewable energy integration, and government investments in grid modernization and infrastructure.

What are the major challenges faced by the market?

The market faces challenges such as high initial installation and maintenance costs, delays in project execution, and the requirement for skilled professionals to handle advanced switchgear systems.

What are the emerging trends in the Asia Pacific Switchgear Market?

Notable trends include the rise in smart switchgear adoption, growth in gas-insulated switchgear (GIS) usage, and the increasing integration of IoT and automation technologies.

Which segment is expected to grow the fastest in this market?

The medium voltage switchgear segment is expected to witness the fastest growth due to its wide use in both urban and industrial power distribution.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com