Global Automotive Fuel Tank Market Size, Share, Trends & Growth Forecast Report Segmented By Capacity (Less Than 45 Liter, 45 To 70 Liter, Above 70 Liter), Material Type, Vehicle Type, Fuel Type, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2026 to 2034

Global Automotive Fuel Tank Market Report Summary

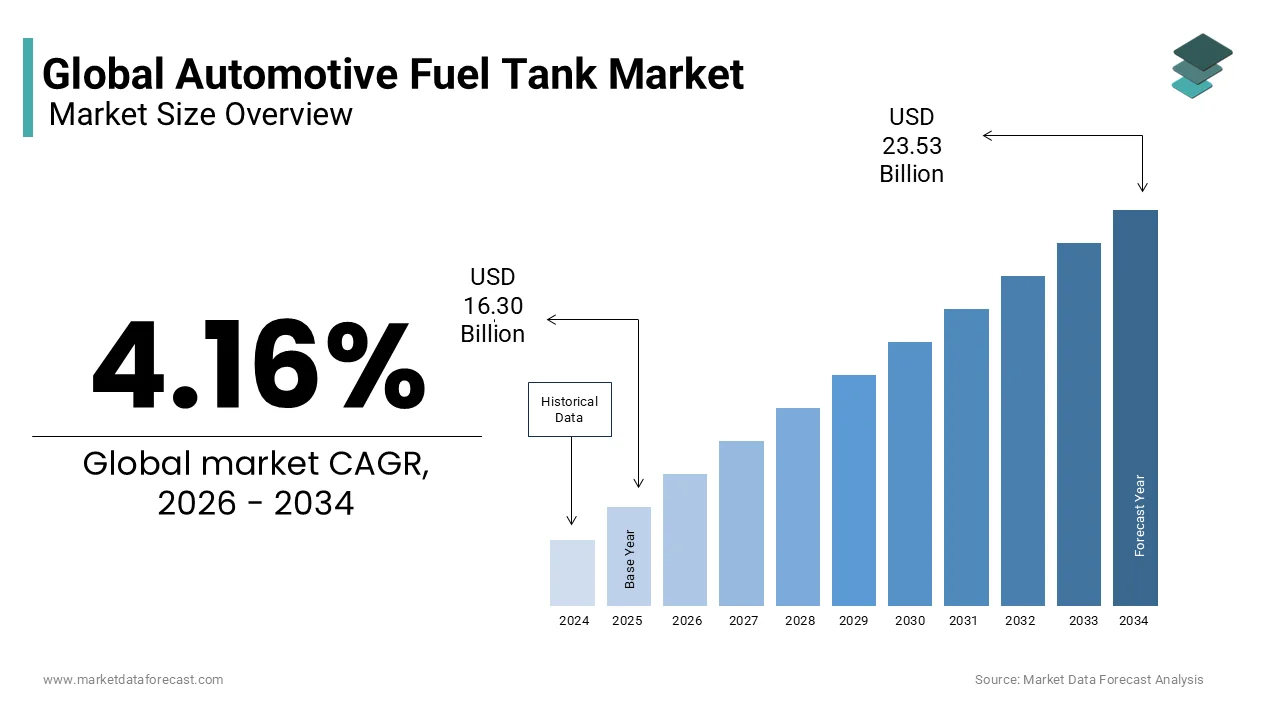

The global automotive fuel tank market was valued at USD 16.30 billion in 2025, is estimated to reach USD 16.98 billion in 2026, and is projected to reach USD 23.53 billion by 2034, growing at a CAGR of 4.16% during the forecast period from 2026 to 2034. The growth of the global automotive fuel tank market is driven by increasing vehicle production, rising demand for lightweight automotive components, and stringent fuel efficiency and emission regulations. Automakers are increasingly adopting advanced fuel tank materials and designs to reduce vehicle weight, improve fuel economy, and enhance safety. Additionally, continuous advancements in plastic fuel tank technologies, growing demand for commercial vehicles, and the need for durable, corrosion-resistant fuel storage systems are supporting market expansion.

Key Market Trends

-

Increasing adoption of lightweight plastic fuel tanks is improving vehicle fuel efficiency and reducing emissions.

-

Growing demand for high-capacity fuel tanks in commercial vehicles and SUVs is supporting market growth.

-

Advancements in multilayer plastic fuel tank technologies are enhancing durability, safety, and evaporative emission control.

-

Rising investments in advanced manufacturing processes are improving fuel tank design and production efficiency.

-

Increasing focus on regulatory compliance and fuel system safety is driving innovation in automotive fuel tank technologies.

Segmental Insights

-

Based on capacity, the 45 to 70 liters segment dominated the global automotive fuel tank market and accounted for 54.9% of the market share in 2025. The segment's leadership is attributed to its widespread adoption across passenger cars and light commercial vehicles, offering an optimal balance between driving range, vehicle weight, and fuel efficiency.

-

Based on material type, the plastic fuel tanks segment held the largest share of the global automotive fuel tank market in 2025. The segment's dominance is driven by their lightweight construction, corrosion resistance, design flexibility, and ability to meet stringent emission standards.

-

Based on vehicle type, the passenger cars segment accounted for 68.5% of the global automotive fuel tank market share in 2025. The segment's growth is supported by high passenger vehicle production, continued reliance on internal combustion engine vehicles, and sustained demand for efficient and durable fuel storage systems despite the increasing adoption of electric vehicles.

Regional Insights

-

The global automotive fuel tank market is witnessing steady growth due to increasing automotive production, advancements in fuel system technologies, and growing demand for lightweight vehicle components.

-

North America dominated the global automotive fuel tank market by accounting for 27.2% of the market share in 2025. The region's leadership is supported by strong demand for large-capacity fuel tanks in pickup trucks, SUVs, and commercial vehicles, along with a well-established automotive manufacturing industry and continuous investments in advanced fuel system technologies.

Competitive Landscape

The global automotive fuel tank market is highly competitive, with manufacturers focusing on lightweight materials, advanced fuel storage technologies, and regulatory compliance to strengthen their market position. Companies are investing in research and development, production capacity expansion, and strategic collaborations to improve fuel tank durability, safety, and environmental performance while meeting the evolving requirements of the global automotive industry. Key players operating in the global automotive fuel tank market include Magna International Inc., OPmobility SE, TI Fluid Systems plc, Kautex Textron GmbH & Co. KG, YAPP Automotive Systems Co. Ltd., Fuel Total Systems Co. Ltd., Sakamoto Industry Co. Ltd., Yachiyo Industry Co. Ltd., SRD Holdings Ltd., Donghee Industrial Co. Ltd., Continental AG, Forvia (Faurecia Hydrogen Solutions), Hexagon Composites ASA, Yutaka Corporation, Lumax Industries Ltd., Cangzhou Mingzhu Plastic Co. Ltd., Unipres Corporation, and SKH Metals Ltd.

Global Automotive Fuel Tank Market Size

The global automotive fuel tank market size was valued at USD 16.30 billion in 2025, and is expected to be worth USD 23.53 billion by 2034 from USD 16.98 billion by 2026. The market is growing at a CAGR of 4.16% during the forecast period.

Automotive fuel tanks are specialized containment systems designed to store liquid fuels, such as gasoline, diesel, and alternative fuels like hydrogen, within motor vehicles. These components are critical for vehicle safety and operational efficiency, requiring robust engineering to prevent leakage, evaporation, and structural failure under dynamic driving conditions. The industry is currently navigating a significant transitional phase where traditional internal combustion engine requirements coexist with emerging needs for hybrid and hydrogen-powered platforms. According to the Energy Institute, global oil demand for road transport reached over 100 million barrels per day in 2023, indicating that despite the rise of electrification, liquid fuel infrastructure remains deeply entrenched in global mobility. As per data from Eurostat, approximately 80% of new automotive fuel tanks registered in the EU in 2024 still utilized internal combustion or hybrid powertrains, necessitating continued production of advanced fuel storage solutions. Modern fuel tanks have evolved from simple metal containers to complex multi-layer plastic assemblies integrated with evaporative emission control systems and onboard refueling vapor recovery units. The shift toward lightweight materials aims to reduce overall vehicle mass, thereby improving fuel economy and reducing carbon emissions. Regulatory frameworks, such as the Euro 7 standards mandate near-zero evaporative emissions, which is forcing manufacturers to adopt sophisticated barrier technologies and sealing mechanisms. This regulatory pressure drives innovation in material science and manufacturing processes, ensuring that fuel tanks meet stringent safety and environmental criteria while accommodating the spatial constraints of modern vehicle architectures, including plug-in hybrid electric vehicles that require space for both fuel and battery packs.

MARKET DRIVERS

Stringent Evaporative Emission Regulations Driving Advanced Material Adoption

Global environmental agencies are enforcing increasingly rigorous standards to minimize hydrocarbon emissions from vehicle fuel systems and this directly drive the adoption of advanced multi-layer plastic fuel tanks and is a key market driver. According to the United States Environmental Protection Agency, the final evaporative emission standards for light-duty vehicles range from 0.300 to 0.500 grams per test, depending on the vehicle category. As per data from the California Air Resources Board, traditional single-layer high-density polyethylene tanks cannot meet these permeation limits, necessitating the use of fluorinated barriers or ethylene vinyl alcohol layers that reduce fuel vapor transmission by up to 95%. Manufacturers are compelled to integrate complex onboard refueling vapor recovery systems that capture fumes during refueling and redirect them to the engine for combustion. The European Union Euro 7 regulation further tightens these requirements by mandating real-world driving emission tests that include evaporative losses under various temperature conditions. According to industry analysis, the implementation of these standards has increased the complexity and cost of fuel tank production but is essential for regulatory compliance. The shift toward plug-in hybrid vehicles also intensifies this driver, as these vehicles may sit idle for extended periods on electric power, allowing fuel to stagnate and increase vapor pressure. Consequently, automakers prioritize fuel tanks with superior barrier properties and thermal stability to ensure compliance throughout the vehicle lifecycle. This regulatory landscape ensures that even as electrification grows, the remaining internal combustion and hybrid vehicles must utilize state-of-the-art fuel containment technologies to minimize their environmental footprint.

Growth of Hybrid Electric Vehicles Sustaining Demand for Compact Fuel Systems

The rapid expansion of the hybrid electric vehicle segment provides a sustained demand driver for automotive fuel tanks, as these vehicles require optimized storage solutions that coexist with large battery packs. According to the U.S. Energy Information Administration, hybrid and electric vehicles surpassed 16% of total U.S. light-duty vehicle sales in 2023, reflecting consumer preference for vehicles that offer electric efficiency without range anxiety. As per data from the Japan Automobile Manufacturers Association, hybrid vehicles often utilize smaller fuel tanks compared to conventional cars to save weight and space, yet these tanks must maintain high structural integrity and safety standards. The integration of fuel tanks in hybrid platforms requires innovative shapes and mounting configurations to accommodate battery modules, typically located under the rear seats or in the trunk area. Manufacturers are developing compact, high-capacity tanks using blow-molding techniques that allow for complex geometries fitting into irregular spaces within the vehicle chassis. According to reports from major automakers, the average fuel tank capacity in hybrid vehicles has decreased by 10% to 15% compared to their internal combustion counterparts, but the frequency of production remains high due to strong market uptake. The need for lightweight materials is even more critical in hybrids to offset the weight of the battery system, ensuring that overall vehicle efficiency is maximized. This trend supports the continued relevance of fuel tank manufacturers who must adapt their designs to serve the unique architectural constraints of hybrid powertrains while maintaining cost-effectiveness and safety compliance in a competitive market.

MARKET RESTRAINTS

Rapid Electrification Reducing Long-Term Demand for Liquid Fuel Storage

The accelerating transition toward battery electric vehicles represents a significant restraint on the automotive fuel tank market, as these vehicles eliminate the need for liquid fuel storage entirely. According to BloombergNEF, battery electric vehicles are projected to account for over 50% of global automotive fuel tank sales by 2035, which implies a substantial reduction in the addressable market for traditional fuel tanks. As per data from the European Commission, several member states have announced bans on the sale of new internal combustion engine vehicles by 2035, creating a definitive timeline for the decline of fuel tank demand in key markets. Automakers are increasingly allocating research and development budgets toward battery technology and electric drivetrains rather than optimizing internal combustion components, including fuel systems. This strategic shift reduces the incentive for suppliers to innovate in fuel tank technology beyond basic compliance requirements. According to industry analysis, the total volume of fuel tanks produced globally is expected to peak in the coming years before entering a structural decline as electrification penetrates deeper into commercial and passenger segments. The residual market will likely be confined to hybrid vehicles and regions with slower electrification adoption, but the overall growth trajectory is negative. Suppliers face the challenge of managing excess capacity and retooling facilities for other automotive components as original equipment manufacturers phase out internal combustion platforms. This long-term structural shift forces fuel tank manufacturers to diversify their product portfolios or risk obsolescence in a rapidly changing automotive landscape.

Volatility in Raw Material Prices Impacting Production Costs

The automotive fuel tank market faces significant margin pressure due to the volatility of raw material prices, particularly for high-density polyethylene and specialized barrier resins used in manufacturing. According to the World Bank commodity price index, the price of crude oil-derived plastics has shown significant fluctuation due to geopolitical tensions and supply chain disruptions affecting petrochemical markets. As per data from the American Chemistry Council, the cost of resins used for creating fuel-impermeable barriers is subject to inflationary pressure driven by limited production capacity and high energy costs. These cost increases are difficult to pass on to automakers, who operate on thin margins and demand annual price reductions from suppliers. The reliance on specific grades of polymers that meet strict automotive safety and permeation standards limits the ability of manufacturers to switch to cheaper alternatives without extensive requalification processes. According to industry reports, the energy-intensive nature of plastic extrusion and blow molding means that rising electricity and natural gas prices further exacerbate production costs. Small and medium-sized suppliers struggle to absorb these fluctuations, leading to potential supply disruptions or consolidation in the sector. The lack of long-term fixed-price contracts for raw materials exposes manufacturers to spot market risks, which is making financial planning challenging. This economic instability hinders investment in new technologies and forces companies to prioritize cost containment over innovation, potentially slowing the development of next-generation fuel storage solutions.

MARKET OPPORTUNITIES

Development of Hydrogen Fuel Tank Technologies for Zero-Emission Mobility

The emergence of hydrogen fuel cell vehicles presents a significant opportunity for the global automotive fuel tank market. According to the Hydrogen Council, global hydrogen production for mobility is expected to scale significantly by 2030, driving demand for specialized Type IV composite fuel tanks capable of storing hydrogen at 700 bar pressure. As per data from the International Renewable Energy Agency, several governments, including Japan, Germany, and South Korea, are investing billions in hydrogen infrastructure, creating a supportive ecosystem for fuel cell vehicle adoption. These composite tanks utilize carbon fiber-reinforced polymers, which offer high strength-to-weight ratios essential for maximizing vehicle range and efficiency. Manufacturers with expertise in plastic molding and composite materials are well-positioned to capture this growing niche market. According to industry analysis, the market for hydrogen storage systems is projected to grow at a compound annual growth rate of 35% through 2030, as commercial trucks and buses increasingly adopt fuel cell technology. The technical complexity of hydrogen tanks allows for higher value propositions compared to traditional plastic fuel tanks, improving profit margins for suppliers. Collaborations between automotive OEMs and energy companies are accelerating the standardization of hydrogen refueling interfaces and tank specifications. This transition enables fuel tank manufacturers to leverage their existing knowledge of fluid containment while entering a high-growth segment aligned with global decarbonization goals.

Expansion into Lightweight Plastic Solutions for Improved Vehicle Efficiency

The ongoing imperative to reduce vehicle weight for improved fuel efficiency and extended electric range creates opportunities for advanced lightweight plastic fuel tank solutions. According to the U.S. Department of Energy, reducing vehicle weight by 10% can improve fuel economy by 6% to 8%, making lightweighting a critical design objective for automakers. As per data from the European Association of Automotive Suppliers, plastic fuel tanks are up to 50% lighter than equivalent steel tanks, offering significant weight savings that contribute to overall vehicle efficiency. Manufacturers are developing thinner-wall technologies and optimized rib structures that maintain structural integrity while minimizing material usage. The flexibility of plastic allows for complex shapes that maximize volume utilization within irregular chassis spaces, further enhancing packaging efficiency. According to industry reports, the demand for high-performance engineering plastics in automotive applications is growing steadily as manufacturers seek to replace metal components wherever possible. The recyclability of modern plastic fuel tanks also aligns with circular economy initiatives, allowing manufacturers to recover and reuse materials at the end of vehicle life. Innovations in multi-layer co-extrusion enable the production of tanks with enhanced barrier properties using less material, reducing both weight and cost. This trend supports the continued evolution of fuel tank technology even in a declining market for internal combustion engines, as every gram saved contributes to meeting stringent efficiency targets.

MARKET CHALLENGES

Complexity of Manufacturing Multi-Layer Barrier Structures

The production of modern fuel tanks involves complex multi-layer co-extrusion and blow-molding processes that require precise control and significant capital investment, which is posing a major challenge for the automotive fuel tank market. According to data from the Society of Plastics Engineers, creating a five- or six-layer structure with alternating layers of high-density polyethylene and barrier materials requires specialized machinery and tight process tolerances. Any deviation in layer thickness or adhesion can compromise the tank permeation performance, leading to costly recalls and regulatory non-compliance. As per industry analysis, the defect rate in multi-layer tank production is higher than in single-layer manufacturing, requiring advanced quality control systems and skilled operators. The integration of additional components, such as rollover valves, vent lines, and level sensors, into the tank during the molding process adds further complexity and potential points of failure. According to reports from major manufacturers, the cycle time for producing complex-shaped tanks is longer than for simple containers, reducing overall production throughput and increasing unit costs. The need for post-molding treatments to enhance barrier properties introduces additional steps and environmental handling requirements. These manufacturing challenges limit the number of suppliers capable of producing high-quality fuel tanks, creating a consolidated market with high entry barriers. Smaller players struggle to compete due to the high cost of equipment and the technical expertise required managing these intricate processes effectively.

Safety Risks Associated with High-Pressure and Alternative Fuels

The introduction of alternative fuels, such as compressed natural gas and hydrogen, introduces new safety challenges that require rigorous testing and validation protocols for fuel storage systems, which is further challenging the automotive fuel tank market expansion. According to the National Highway Traffic Safety Administration, hydrogen fuel tanks must withstand extreme pressures up to 700 bar and survive severe crash scenarios without rupturing or leaking, which demands extensive physical and computational testing. As per data from the Compressed Gas Association, the storage of compressed gases requires different material properties and design considerations compared to liquid fuels, including resistance to hydrogen embrittlement in metal components and permeation in composites. The lack of historical data on long-term performance of these new tank types in real-world conditions creates uncertainty for manufacturers and regulators. According to industry reports, the certification process for hydrogen tanks is lengthy and expensive, involving burst tests, cycle fatigue tests, and fire resistance evaluations that can take years to complete. Any safety incident involving alternative fuel tanks could have severe reputational and legal consequences for manufacturers, slowing down adoption rates. The handling of flammable gases during manufacturing and assembly also requires specialized safety infrastructure and training, increasing operational costs. Manufacturers must balance the need for lightweight, high-capacity storage with uncompromising safety standards, which often conflict in terms of material selection and design optimization. This tension creates a persistent engineering challenge that requires continuous innovation and validation to ensure public trust and regulatory approval.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.16% |

| Segments Covered | By Capacity, Material Type, Vehicle Type, Fuel Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Magna International Inc., OPMOBILITY SE, TI Fluid Systems plc, Kautex Textron GmbH & Co. KG, YAPP Automotive Systems Co. Ltd., Fuel Total Systems Co. Ltd., Sakamoto Industry Co. Ltd., Yachiyo Industry Co. Ltd., SRD Holdings Ltd., Donghee Industrial Co. Ltd., Continental AG, Forvia (Faurecia Hydrogen Solutions), Hexagon Composites ASA, Yutaka Corporation, Lumax Industries Ltd., Cangzhou Mingzhu Plastic Co. Ltd., Unipres Corporation, and SKH Metals Ltd |

SEGMENTAL ANALYSIS

By Capacity Insights

The 45 to 70 liters capacity segment had 54.9% of the global market share in 2025 and is likely to remain the most common configuration over the forecast period, as it addresses the needs of the mass-market, compact, and mid-size vehicle segment. According to data from the International Organization of Motor Vehicle Manufacturers, this capacity range is optimal for vehicles with wheelbases between 2.5 and 2.8 meters, which constitute the majority of global car sales. As per reports from the Society of Automotive Engineers, a 50-liter tank provides a driving range of approximately 600 to 700 kilometers for average gasoline engines, balancing refueling frequency with vehicle weight and interior space utilization. This segment benefits from the high production volume of sedans, hatchbacks, and compact SUVs in emerging markets where affordability and practicality drive consumer choices. Manufacturers have standardized tooling and blow-molding processes for this size range, achieving economies of scale that reduce unit costs significantly. According to industry analysis, over 60% of new vehicle platforms launched in Asia and Europe feature fuel tanks within this capacity bracket to meet regulatory efficiency targets while ensuring adequate range for daily commuting. The modular design of these tanks allows for easy integration into various chassis architectures without major structural modifications. This versatility makes the 45 to 70-liter segment the backbone of the fuel tank industry, supporting mass-market mobility needs across diverse geographic regions.

On the other side, the above 70-liter capacity segment is anticipated to experience a CAGR of 5.1% during the forecast period in the global market as the popularity of larger SUVs and heavy-duty utility vehicles continues to rise in key markets, increasing consumer preference for large sport utility vehicles, pickup trucks, and luxury cars. According to data from J.D. Power, sales of full-size SUVs and trucks in North America have remained robust as buyers prioritize towing capacity and long-distance travel capabilities. As per reports from the Alliance for Automotive Innovation, these larger vehicles require substantial fuel reserves to support heavy-duty operations and extended range expectations, often exceeding 800 kilometers per tank. The rise of premium automotive segments in China and the Middle East further boosts demand for high-capacity tanks that minimize refueling stops during highway driving. Manufacturers are developing robust multi-layer plastic tanks capable of holding up to 100 liters while maintaining structural integrity under heavy loads. According to industry analysis, the average fuel tank size in full-size pickups has increased to accommodate powerful engines and improve payload efficiency. The trend toward adventure tourism and off-road exploration also drives demand for vehicles with extended range capabilities. This segment growth reflects a shift in consumer lifestyle preferences toward larger, more capable vehicles that require proportionally larger fuel storage solutions to maintain operational viability.

By Material Type Insights

The plastic fuel tanks segment dominated the market by capturing the largest share of the global market in 2025 and is projected to maintain their market dominance due to their cost-effectiveness, weight-reduction benefits for mass-market vehicles, superior lightweight properties and resistance to corrosion compared to metal alternatives. According to data from the European Association of Automotive Suppliers, plastic tanks are up to 50% lighter than steel equivalents, contributing significantly to overall vehicle weight reduction and improved fuel economy. As per reports from the Society of Plastics Engineers, high-density polyethylene used in modern tanks provides excellent chemical resistance to ethanol blends and biodiesel, which can corrode metal containers over time. The flexibility of plastic allows for complex shapes that maximize volume utilization within irregular chassis spaces, enhancing packaging efficiency. Manufacturers utilize multi-layer co-extrusion techniques to create barriers that prevent fuel permeation, meeting stringent emission standards. According to industry analysis, the cost of producing plastic tanks has decreased over the last decade due to advancements in blow-molding technology and material recycling. The ability to integrate components such as baffles and sensors directly into the mold reduces assembly time and parts count. This manufacturing efficiency, combined with performance benefits, ensures that plastic remains the preferred material for passenger vehicles and light commercial applications globally.

However, the aluminum fuel tank segment is expected to showcase a CAGR of 6.6% during the forecast period in the global market as manufacturers prioritize thermal performance and aesthetic differentiation. According to data from the Aluminum Association, aluminum tanks offer superior heat dissipation properties, which help maintain fuel temperature stability in high-performance engines and hybrid systems. As per reports from major automakers, aluminum provides a premium look and feel that aligns with brand positioning in the luxury segment while being fully recyclable at the end of vehicle life. The material's high strength-to-weight ratio allows for thinner walls without compromising structural integrity, reducing overall component weight. According to industry analysis, the demand for aluminum in automotive applications is rising as manufacturers seek to replace steel in premium models to achieve higher quality perceptions. Aluminum tanks are also preferred for hydrogen storage liners in fuel cell vehicles due to their compatibility with composite overwrapping. The growing popularity of plug-in hybrids, which require compact and efficient fuel storage solutions, further drives aluminum adoption. This segment growth reflects the industry trend toward premiumization and sustainability, where material choice plays a key role in vehicle differentiation and environmental compliance.

By Vehicle Type Insights

The automotive fuel tanks segment held 68.5% of the global market share in 2025 and is expected to remain the primary consumer of fuel tank systems despite the growth in electric mobility, as they continue to constitute the majority of global production. According to data from the International Organization of Motor Vehicle Manufacturers, over 60 million automotive fuel tanks were produced worldwide in 2023, creating a consistent and large-scale demand for fuel storage systems. As per reports from the European Automobile Manufacturers Association, the majority of these vehicles are equipped with internal combustion or hybrid powertrains, requiring reliable and efficient fuel tanks. The standardization of platform architectures across multiple models allows manufacturers to produce fuel tanks in high volumes, reducing costs and ensuring supply chain stability. Automotive fuel tanks prioritize lightweight and compact fuel tanks to maximize interior space and fuel efficiency, driving innovation in plastic molding technologies. According to industry analysis, the replacement cycle for automotive fuel tank fuel tanks is longer, but the sheer number of new units sold annually sustains market leadership. The diverse range of passenger vehicle segments, from economy compacts to luxury sedans, ensures broad applicability for various fuel tank designs and capacities. This segment dominance is reinforced by the essential role of personal mobility in daily life, making automotive fuel tanks the primary driver of fuel tank consumption.

On the other side, the light commercial vehicles segment is poised for significant expansion and is estimated to register a CAGR of 6.7% during the forecast period as the growth of e-commerce drives the need for more efficient and durable urban logistics fleets. According to data from the United Nations Conference on Trade and Development, global e-commerce sales reached nearly 27 trillion dollars in 2023, necessitating efficient delivery fleets that operate continuously. As per reports from the International Transport Forum, light commercial vehicles, such as vans and pickup trucks, are the backbone of urban logistics, requiring durable and high-capacity fuel tanks to support intensive daily usage. These vehicles often operate in stop-and-go traffic conditions, where fuel efficiency and reliability are critical for operational profitability. Manufacturers are developing robust fuel tanks with enhanced protection against road debris and impacts common in urban environments. According to industry analysis, the fleet renewal rate for delivery vehicles has accelerated as companies seek to modernize their operations with newer, more efficient models. The shift toward hybrid light commercial vehicles also drives demand for specialized fuel tanks that coexist with battery packs. This segment growth reflects the structural transformation of retail and logistics industries, where speed and reliability are paramount, driving sustained investment in commercial vehicle infrastructure.

REGIONAL ANALYSIS

North America Automotive Fuel Tank Market Analysis

North America held the dominant share of 27.2% of the global market in 2025 and is expected to maintain its market share as a key region for large-capacity and high-performance fuel systems. According to data from the Alliance for Automotive Innovation, light trucks and SUVs accounted for over 75% of new vehicle sales in the United States in 2023, driving demand for high-capacity and durable fuel tanks. As per reports from the Environmental Protection Agency, strict evaporative emission standards compel manufacturers to adopt advanced multi-layer plastic tanks with sophisticated vapor recovery systems. The region's mature automotive industry supports a strong supplier base providing innovative solutions for domestic automakers. According to industry analysis, the average fuel tank capacity in North American vehicles is higher than in other regions, reflecting the prevalence of long-distance travel and towing activities. The shift toward hybrid pickups and SUVs further drives demand for specialized fuel tanks that integrate with electric drivetrains. Government incentives for domestic manufacturing encourage local production of automotive components, including fuel tanks. This regional strength is supported by high disposable income and a culture that values vehicle size and capability.

Europe Automotive Fuel Tank Market Analysis

Europe is anticipated to continue leading in the adoption of stringent emission technologies and sustainable manufacturing practices for fuel tanks. According to data from the European Automobile Manufacturers Association, the implementation of Euro 7 emission standards has accelerated the adoption of advanced barrier technologies in fuel tanks to minimize hydrocarbon leaks. As per reports from the European Commission, member states are investing heavily in charging infrastructure, but liquid-fuel vehicles remain prevalent, particularly in rural areas and for commercial transport. Major countries with strong engineering capabilities are driving innovation in plastic molding and composite materials. According to industry analysis, European manufacturers lead in developing recyclable fuel tanks that align with circular economy principles. The high penetration of diesel vehicles in the commercial sector sustains demand for robust fuel storage solutions. Government policies promoting biofuels also influence tank material requirements to ensure compatibility with ethanol and biodiesel blends. This regulatory landscape positions Europe as a hub for technological advancement in fuel containment systems.

Asia Pacific Automotive Fuel Tank Market Analysis

Asia Pacific is projected to remain the dominant market for automotive fuel tanks, leveraging its massive production base and the continued prevalence of internal combustion engines in emerging economies. According to data from the China Association of Automobile Manufacturers, China produced over 25 million vehicles in 2023, with a significant portion featuring advanced plastic fuel tanks. As per reports from the Japan Automobile Manufacturers Association, Japanese companies lead in hybrid technology, driving demand for compact and efficient fuel storage solutions. The rapid urbanization and rising middle class in India and Southeast Asia increase demand for affordable automotive fuel tanks with reliable fuel systems. According to industry analysis, local manufacturing hubs in Thailand and Indonesia serve as export bases for global automakers, ensuring cost-competitive production. Government initiatives in China to promote new energy vehicles are shifting focus, but internal combustion engines remain dominant in the short term. The region's diverse market requires flexible fuel tank designs, ranging from basic models for entry-level cars to sophisticated units for premium vehicles. This sheer volume and strategic importance make Asia Pacific the central pillar of the global fuel tank industry.

Latin America Automotive Fuel Tank Market Analysis

Latin America is likely to see steady growth as the region continues to modernize its vehicle fleet and integrate with global manufacturing chains. Latin America represents a smaller but growing segment of the global automotive fuel tank market, characterized by gradual economic recovery and increasing vehicle ownership. According to data from the Brazilian Automotive Industry Association, Brazil produced over 2 million vehicles in 2023, with steady demand for fuel tanks compatible with flex-fuel engines. As per reports from the Mexican Automotive Industry Association, Mexico serves as a major production hub for North American markets, exporting vehicles with advanced fuel systems. Argentina, Chile, and Colombia are seeing increased registrations as consumers seek affordable personal transport options. According to industry analysis, the prevalence of older vehicles creates opportunities for aftermarket fuel tank replacements, although OEM fitment remains the primary driver. Local assembly plants help mitigate import tariffs and keep prices competitive. Government efforts to improve road infrastructure and enforce safety regulations are enhancing market stability. The region's youthful population and growing urbanization trends support long-term growth potential. Manufacturers are introducing models tailored to local preferences and fuel types, ensuring relevance in this diverse market.

COMPETITIVE LANDSCAPE

The competitive landscape of the automotive fuel tank market features intense rivalry among established global suppliers and specialized regional manufacturers striving to dominate through technological superiority and cost efficiency. Major corporations leverage extensive global networks and deep engineering expertise to offer comprehensive solutions that integrate seamlessly with modern vehicle platforms. Innovation centers on developing lightweight plastic tanks with advanced barrier properties that comply with strict emission standards while reducing overall vehicle weight. Price pressure from automakers forces suppliers to optimize manufacturing efficiency and reduce component costs without compromising reliability or safety performance. Intellectual property rights regarding multi layer co extrusion techniques and barrier materials become critical differentiators as companies seek to protect their technological advantages. Strategic partnerships with polymer suppliers ensure stable access to high quality raw materials amidst volatile commodity markets. The entry of new players specializing in composite materials for hydrogen storage adds complexity as the market diversifies beyond traditional liquid fuels. Regulatory compliance across diverse regions requires adaptable platforms that meet varying safety and environmental standards. Customer loyalty depends on consistent quality timely delivery and collaborative development capabilities making service excellence as important as product innovation in securing long term contracts.

KEY MARKET PLAYERS

Some of the key players dominating the global automotive fuel tank market are

- Magna International Inc.

- OPMOBILITY SE

- TI Fluid Systems plc

- Kautex Textron GmbH & Co. KG

- YAPP Automotive Systems Co. Ltd.

- Fuel Total Systems Co. Ltd.

- Sakamoto Industry Co. Ltd.

- Yachiyo Industry Co. Ltd.

- SRD Holdings Ltd.

- Donghee Industrial Co. Ltd.

- Continental AG

- Forvia (Faurecia Hydrogen Solutions)

- Hexagon Composites ASA

- Yutaka Corporation

- Lumax Industries Ltd.

- Cangzhou Mingzhu Plastic Co. Ltd.

- Unipres Corporation

- SKH Metals Ltd.

Top Players in the Market

- Kautex Textron GmbH and Co KG stands as a global leader in plastic fuel tank systems leveraging its expertise in blow molding technology to deliver lightweight and emission compliant solutions. The company specializes in multi layer plastic tanks that meet stringent evaporative emission standards for both internal combustion and hybrid vehicles. Recent strategic initiatives include expanding production facilities in Asia and North America to support local automakers and reduce logistics costs. Kautex focuses on integrating complex components such as sensors and valves directly into the tank structure during manufacturing to enhance efficiency. The firm invests heavily in research and development to create innovative barrier materials that improve fuel impermeability. Its commitment to sustainability is evident in the adoption of recycled plastics and energy efficient production processes. Kautex continues to strengthen its position through long term partnerships with major original equipment manufacturers ensuring consistent supply and technological collaboration.

- Yutaka Corporation maintains a strong presence in the automotive fuel tank market by providing high quality plastic and metal fuel storage systems primarily for Asian and global markets. The company is renowned for its advanced manufacturing techniques that ensure superior durability and safety performance under various driving conditions. Recent actions include investing in new production lines for hybrid vehicle fuel tanks which require compact and irregular shapes to accommodate battery packs. Yutaka focuses on lightweighting technologies to help automakers meet fuel efficiency targets while maintaining structural integrity. The corporation emphasizes strict quality control and rapid response capabilities to serve just in time manufacturing requirements. Strategic collaborations with material suppliers enable the development of next generation polymers with enhanced barrier properties. Yutaka actively participates in global automotive exhibitions to showcase its latest innovations and strengthen relationships with key industry stakeholders.

- Magna International Inc serves as a diversified automotive supplier offering comprehensive fuel tank solutions including plastic and metal systems for a wide range of vehicle types. The company leverages its global manufacturing footprint to provide localized support and flexible production capacities for major automakers. Recent strategies involve developing integrated fuel delivery modules that combine tanks pumps and filters into single units to simplify assembly and reduce weight. Magna invests in advanced simulation tools to optimize tank design for maximum volume utilization and crash safety. The firm prioritizes sustainability by implementing circular economy principles in its manufacturing operations and product lifecycle management. Magna collaborates with technology partners to integrate smart sensing capabilities into fuel systems for improved monitoring and diagnostics. Its broad portfolio allows it to serve diverse market segments from economy cars to premium luxury vehicles ensuring resilience against market fluctuations.

Top Strategies Used by Key Market Participants

Key players in the automotive fuel tank market primarily focus on technological innovation to develop lightweight multi layer plastic tanks that meet stringent evaporative emission regulations. Manufacturers invest heavily in research and development to create advanced barrier materials such as fluorinated polyethylene and ethylene vinyl alcohol that minimize fuel permeation. Expansion into emerging markets through local production facilities helps reduce costs and mitigate supply chain risks while meeting regional content requirements. Companies prioritize vertical integration by producing critical components such as sensors and valves in house to ensure quality control and protect proprietary technology. Product differentiation through integrated fuel delivery modules allows suppliers to offer simplified assembly solutions that reduce manufacturing complexity for automakers. Sustainability initiatives drive the adoption of recycled plastics and energy efficient manufacturing processes aligning with global environmental regulations. Strategic partnerships with material scientists and automotive OEMs foster collaborative innovation ensuring that fuel tank designs evolve alongside changing vehicle architectures and powertrain technologies.

MARKET SEGMENTATION

This research report on the global automotive fuel tank market is segmented and sub-segmented into the following categories.

By Capacity

- Less than 45 Liter

- 45 to 70 Liter

- Above 70 Liter

By Material Type

- Plastic – Single-Layer

- Plastic – Multi-Layer/Barrier

- Aluminium

- Steel

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Buses and Coaches

By Fuel Type

- Gasoline

- Diesel

- Flex-Fuel/Ethanol Blends

- Hydrogen

- CNG and LPG

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Automotive Fuel Tank Market?

The Automotive Fuel Tank Market comprises the global production and supply of fuel storage systems used in passenger cars, commercial vehicles, buses, and other automobiles to safely store gasoline, diesel, hydrogen, CNG, LPG, and other fuels.

2. What factors are driving the growth of the Automotive Fuel Tank Market?

The market is driven by increasing vehicle production, growing demand for lightweight fuel tanks, stricter fuel efficiency regulations, and rising adoption of alternative fuel vehicles.

3. What are the major types of automotive fuel tanks?

Automotive fuel tanks are primarily manufactured from single-layer plastic, multi-layer barrier plastic, aluminum, and steel, with plastic fuel tanks gaining popularity due to their lightweight properties.

4. Which vehicle segments use automotive fuel tanks?

Automotive fuel tanks are widely used in passenger cars, light commercial vehicles, medium and heavy commercial vehicles, and buses and coaches.

5. Which fuel types are supported by automotive fuel tanks?

Automotive fuel tanks are designed for gasoline, diesel, flex-fuel/ethanol blends, hydrogen, compressed natural gas (CNG), and liquefied petroleum gas (LPG).

6. Why are plastic fuel tanks becoming more popular?

Plastic fuel tanks offer several advantages, including lower weight, improved corrosion resistance, greater design flexibility, better fuel efficiency, and reduced manufacturing costs compared to metal tanks.

7. Which region dominates the Automotive Fuel Tank Market?

Asia-Pacific holds the largest share of the market due to high automotive production, expanding vehicle ownership, and the presence of major automobile manufacturers in countries such as China, Japan, and India.

8. Which region is expected to witness the fastest growth?

The Asia-Pacific region is projected to register the fastest growth, supported by increasing automobile production, rising commercial vehicle demand, and growing investments in fuel-efficient vehicle technologies.

9. What challenges does the Automotive Fuel Tank Market face?

Key challenges include the growing adoption of battery electric vehicles, fluctuating raw material prices, stringent emission regulations, and the high development costs of advanced fuel storage systems.

10. What is the future outlook for the Automotive Fuel Tank Market?

The Automotive Fuel Tank Market is expected to grow steadily over the coming years, supported by continued demand for fuel-efficient vehicles, innovations in lightweight fuel tank materials, and increasing adoption of alternative fuel storage solutions across the automotive industry.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com