Global Automotive Glass Market Size, Share, Trends & Growth Forecast Report, Segmented By Product (Tempered, Laminated and Others), Application (Windscreen, Backlite, Sidelite and Sunroof), End-use (Original Equipment Manufacturer and Aftermarket Replacement), Vehicle (Passenger Car, Light Commercial and Heavy Commercial) and Region (North America, Europe, Latin America, Asia-Pacific, Middle East and Africa), Industry Analysis From 2026 to 2034

Market Size, 2025

$28.33 BnMarket Estimate, 2026

$29.86 BnMarket Forecast, 2034

$45.48 BnCAGR, 2026–2034

5.40%Global Automotive Glass Market Size

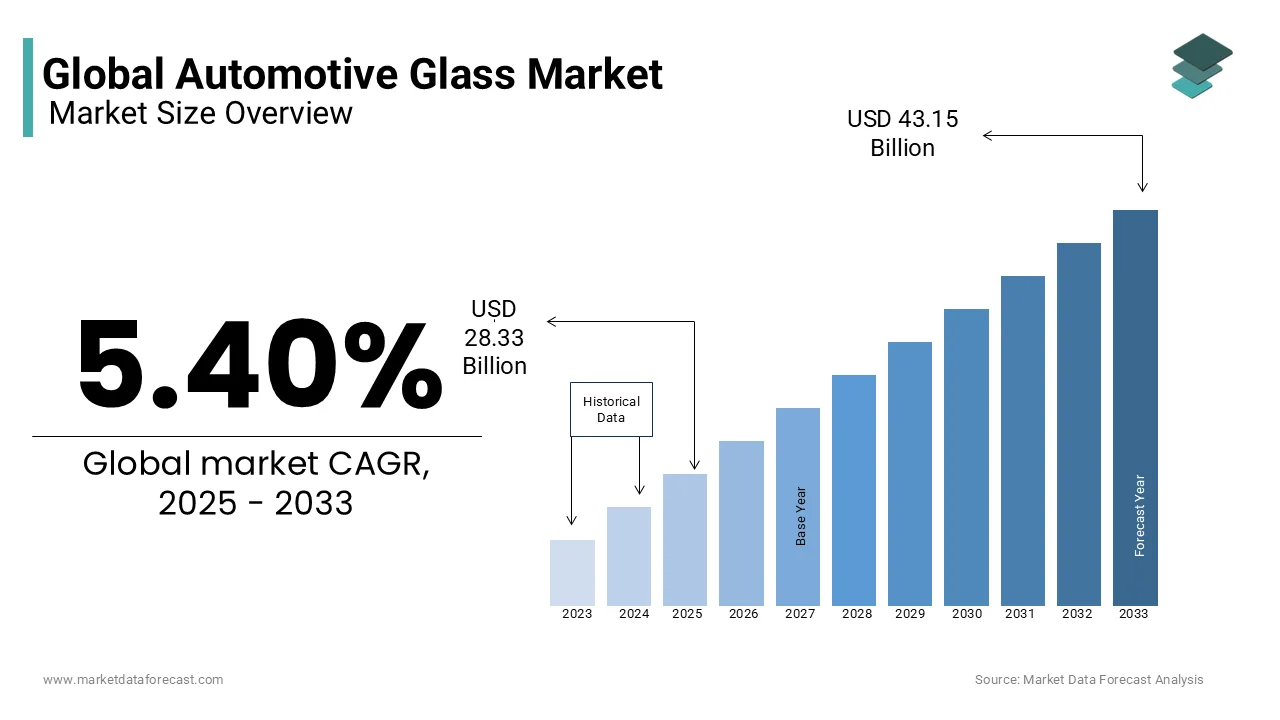

The global automotive glass market was valued at USD 28.33 billion in 2025, and it is anticipated to reach USD 29.86 billion in 2026, from USD 45.48 billion by 2034, growing at a CAGR of 5.40% during the forecast period from 2026 to 2034.

Automotive glass encompasses the specialized, treated glass used in motor vehicles. Designed to withstand harsh driving conditions, impacts, and temperature fluctuations, it acts as a critical structural and safety component. These components are critical for structural integrity, passenger safety, and aesthetic appeal, evolving from simple transparent barriers to sophisticated integrated systems featuring heads up displays and sensor compatibility. The industry is heavily influenced by vehicle production volumes and regulatory mandates regarding occupant protection. Data published by the International Organization of Motor Vehicle Manufacturers (OICA) reveals that global motor vehicle production climbed to 96.4 million units, establishing a massive, high-volume baseline for structural OEM glass and glazing supplies. Safety regulations play a pivotal role. Federal structural compliance frameworks governed by NHTSA under FMVSS No. 216a dictate strict load-bearing parameters for vehicle roofs to withstand up to 3.0 times the vehicle’s unloaded weight, acknowledging that preserving cabin integrity during a crash relies on reinforced structural pillar engineering. Furthermore, the shift toward electric vehicles necessitates lightweight materials to extend battery range, driving innovation in thin yet durable glass compositions. Consumer preferences for panoramic roofs and enhanced acoustic insulation also shape product development. Studies show that panoramic glass features and multi-panel sunroof configurations capture up to 59% of the premium automotive roof market sector, increasingly integrated by global OEMs as a primary aesthetic and design-premium selling feature. The aftermarket segment remains robust due to high incidence of stone chips and cracks, with insurance claims data indicating millions of replacements annually. This dynamic landscape combines technological advancement with stringent safety requirements, positioning automotive glass as a vital component in modern mobility.

MARKET DRIVERS

Stringent Safety Regulations Mandate Advanced Glazing Solutions

Global regulatory bodies enforce rigorous safety standards that contribute to the growth of the automotive glass market. These standards compel automakers to adopt advanced automotive glass technologies. Governments worldwide mandate the use of laminated glass for windshields to prevent ejection during collisions and tempered glass for side windows to minimize injury from shattering. The World Health Organization (WHO) indicates that road traffic injuries cause 1.19 million annual deaths, driving international safety groups like Euro NCAP to implement strict, multi-point crash avoidance and structural integrity protocols to mitigate occupant risk. These regulations require glass to withstand specific force thresholds and maintain visibility under stress, driving investment in stronger interlayers and chemically strengthened materials. The introduction of pedestrian protection laws in Europe and Asia further influences design, requiring windshields to absorb impact energy and reduce head injury criteria scores. Automakers must comply with these evolving standards to sell vehicles in key markets, ensuring consistent demand for high quality certified glass. Additionally, regulations regarding ultraviolet radiation blocking mandate that automotive glass filter out harmful rays, protecting occupants and interior materials. Compliance with these legal frameworks is non negotiable, forcing manufacturers to continuously upgrade their production capabilities and material formulations. This regulatory pressure ensures that automotive glass remains a high value component rather than a commodity, sustaining revenue growth through mandatory technological enhancements and safety driven replacements.

Rising Production of Electric Vehicles Drives Lightweighting Innovations

The rapid expansion of the electric vehicle sector significantly propels the automotive glass market. This creates urgent demand for lightweight materials that enhance battery efficiency and driving range. Electric vehicles carry heavy battery packs, making weight reduction in other components critical for maximizing mileage. The International Energy Agency (IEA) confirm that global electric car sales reached 14 million units as early as 2023, expanding the consumer volume baseline requiring specialized lightweight materials to maximize battery range. Automakers respond by utilizing thinner glass substrates and advanced polymer interlayers that reduce overall vehicle weight without compromising safety or acoustic performance. Panoramic glass roofs, popular in electric models for their spacious feel, require specialized structural glass that can support roof loads while remaining light. Manufacturers develop chemically strengthened glass that allows for reduced thickness while maintaining durability against stone chips and thermal stress. The integration of solar control coatings helps manage cabin temperature, reducing the load on air conditioning systems and preserving battery life. As electric vehicle platforms evolve, the surface area of glass per vehicle increases, with some models featuring glass areas exceeding 5 square meters. This trend toward extensive glazing surfaces directly boosts volume demand. Furthermore, the premium positioning of many electric vehicles encourages the adoption of high end features like electrochromic dimming glass. The synergy between electrification goals and material science innovation ensures that automotive glass manufacturers play a crucial role in the success of the electric mobility transition.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Manufacturing Margins

Fluctuating costs of essential raw materials such as silica sand, soda ash, and limestone are a major hindrance for the growth of the automotive glass market. This squeezes manufacturer profit margins. These inputs are energy intensive to process, and their prices are closely linked to global energy markets and supply chain stability. Energy accounts for up to 30 percent of the total production cost for float glass, making manufacturers highly vulnerable to spikes in electricity and fuel prices. Geopolitical tensions and trade restrictions further disrupt supply chains, leading to shortages and price volatility for specialized additives used in coated and tempered glass. Automakers often resist passing these increased costs onto consumers, pressuring suppliers to absorb margin erosion. Long term contracts may not fully protect against sudden market shifts, creating financial uncertainty for glass producers. Small and medium sized manufacturers struggle more than large conglomerates to hedge against these fluctuations, potentially leading to market consolidation. The need for continuous capital investment in energy efficient furnaces adds to the financial burden. Cost volatility will remain a persistent challenge in the automotive glass sector. This uncertainty will continue to limit profitability and expansion capabilities until stable energy policies and raw material supply chains are established.

Complexity of Integration with Advanced Driver Assistance Systems

The increasing integration of Advanced Driver Assistance Systems sensors and cameras into automotive glass offers a technical and logistical restraint on the global market. This is due to heightened manufacturing complexity and calibration requirements. Modern windshields serve as mounting platforms for cameras, radar, and lidar sensors that enable features like lane keeping assist and automatic emergency braking. Also, there is necessity of precise optical clarity and specific bracket placements during manufacturing, increasing production tolerances and rejection rates. Any distortion or imperfection in the glass can interfere with sensor accuracy, posing safety risks and liability issues. Post replacement calibration of these systems requires specialized equipment and trained technicians, adding time and cost to aftermarket services. The lack of standardized calibration procedures across different vehicle brands complicates repair processes. Glass manufacturers must collaborate closely with technology providers to ensure compatibility, slowing down product development cycles. Defects in sensor integration can lead to costly recalls and reputational damage. The technical barrier to entry rises as vehicles become more autonomous, limiting the number of suppliers capable of meeting these stringent requirements. This complexity restricts market participation to large players with significant research and development resources, stifling competition and innovation from smaller entities.

MARKET OPPORTUNITIES

Development of Smart Glass Technologies Offers Premium Differentiation

The emergence of smart glass technologies is a key growth area for the automotive glass market. This development enables premium differentiation and enhanced user experiences. Electrochromic glass, which can change its tint level electronically, allows drivers to control sunlight exposure and cabin temperature without mechanical shades. This technology improves energy efficiency by reducing air conditioning load and enhances comfort by minimizing glare. Augmented reality heads up displays project navigation and safety information directly onto the windshield, transforming the glass into an interactive interface. Manufacturers are developing transparent conductive coatings that enable these functions while maintaining optical clarity. The integration of antenna systems into glass for 5G connectivity and vehicle to everything communication further adds value. As autonomous driving features evolve, smart glass can provide entertainment and productivity options for passengers, creating new revenue streams. Automakers seek unique selling points in a competitive market, and smart glass offers visible technological sophistication. Partnerships between glass makers and software developers accelerate innovation, bringing these features to mid tier vehicles. The ability to customize transparency and display content aligns with the trend toward personalized mobility experiences, opening lucrative niches for early adopters.

Expansion of Panoramic Roof Designs Increases Glass Surface Area

The growing popularity of panoramic and fixed glass roofs offers a substantial opportunity for volume growth in the automotive glass market. This trend is driven by consumers who prioritize airy and spacious cabin environments. Design trends favor large uninterrupted glass surfaces that enhance aesthetic appeal and natural light penetration, significantly increasing the amount of glass per vehicle. The J.D. Power APEAL Study demonstrate that premium interior layout configurations, cabin space perception, and luxury structural comfort options remain pivotal factors in elevating total vehicle satisfaction scores for SUV owners. These roofs require specialized laminated glass with high strength to meet rollover safety standards while remaining lightweight. Manufacturers innovate with curved and bent glass technologies to create seamless designs that integrate with vehicle body lines. The use of infrared reflective coatings helps manage heat gain, addressing consumer concerns about cabin temperature. As compact and mid size vehicles adopt this feature previously reserved for luxury models, the total addressable market expands. Production efficiencies in bending and tempering large format glass allow cost reductions, making panoramic roofs more accessible. Aftermarket customization also grows, with owners upgrading standard roofs to glass variants. This trend drives demand for high quality large format glass panels, boosting revenue per unit. Suppliers who can deliver complex shapes with consistent quality gain competitive advantages, securing long term contracts with automakers seeking to enhance vehicle appeal through design innovation.

MARKET CHALLENGES

Supply Chain Disruptions Affect Production Continuity

Persistent supply chain disruptions are serious barriers to the automotive glass market. This causes production delays and inventory shortages for manufacturers and automakers. The just in time manufacturing model leaves little buffer for interruptions in the delivery of raw materials or finished glass components. Automotive glass plants require continuous operation of furnaces, making unplanned shutdowns due to material scarcity extremely costly and damaging to equipment. Dependence on single source suppliers for specialized chemicals or equipment increases vulnerability to localized disruptions. Geopolitical conflicts and trade barriers further complicate international sourcing strategies, forcing companies to rethink their global footprint. The shortage of skilled labor in logistics and manufacturing exacerbates these issues, slowing down recovery efforts. Automakers may penalize suppliers for missed deliveries, straining business relationships and impacting future contract bids. Inventory buildup to mitigate risks ties up capital and increases storage costs. The lack of visibility across multi tier supply chains makes proactive management difficult. Companies must invest in digital tracking and diversified sourcing, but these transitions take time and resources. Until supply chains become more resilient, the risk of production halts remains a critical operational challenge.

High Capital Intensity and Energy Requirements Limit Entry

High capital intensity and significant energy consumption is creating substantial barriers to entry and expansion for participants in the automotive glass market. Establishing a float glass production facility requires hundreds of millions of dollars in investment for furnaces, molding machines, and quality control systems. The National Glass Association (NGA) document that float glass production requires float line furnaces to burn continuously at 1,500°C without interruption, making energy inputs an exceptionally high and unyielding baseline expense for manufacturers. Transitioning to cleaner energy sources to meet environmental regulations requires additional capital expenditure for retrofitting or building new eco friendly plants. The long payback period for these investments discourages new entrants and limits the agility of existing players to respond to market changes. High fixed costs mean that manufacturers must maintain high utilization rates to achieve profitability, making them vulnerable to downturns in vehicle production. Regulatory compliance for emissions and waste disposal adds to the financial burden. Smaller companies struggle to compete with established giants who benefit from economies of scale and established customer relationships. The need for continuous research and development to keep pace with technological advancements further strains financial resources. Access to affordable financing becomes critical, yet interest rate fluctuations can increase borrowing costs. This capital intensive nature consolidates the market among a few large players, limiting competition and innovation diversity while exposing the industry to systemic financial risks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.40% |

| Segments Covered | By product, application, end-user, vehicle, and region. |

| Various Analyses Covered | Global, Regional, Country-Level Analysis, Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Saint-Gobain (France), Asahi Glass (Japan), Fuyao Glass (China), Samvardhana Motherson (India), Webasto (Germany), Xinyi Glass (China), Nippon Sheet Glass (Japan), Gentex Corporation (US), Corning (US), Magna International (Canada), and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The laminated glass segment dominated the automotive glass market and accounted for a 40.9% share in 2025. Its mandatory use in windshields and its superior safety characteristic prevent occupant ejection during collisions, which contributes to the dominance of this segment. This product type consists of two layers of glass bonded with a polyvinyl butyral interlayer which holds shattered pieces together upon impact. The widespread adoption of Advanced Driver Assistance Systems further cements this dominance as these systems require optically clear and stable mounting surfaces for cameras and sensors integrated into the windshield. Global safety directives governed by UNECE and North American DOT frameworks mandate multi-layer laminated glass for front windshields to absorb occupant impact energy, mitigate the risk of passenger ejection, and prevent dangerous shattering. The increasing surface area of windshields in modern vehicles to enhance aerodynamics and cabin spaciousness drives volume demand. Furthermore, laminated glass offers excellent acoustic insulation properties which are increasingly valued by consumers seeking quieter cabin environments. The inability to substitute this product with tempered glass for front applications ensures a consistent and inelastic demand base. Manufacturers continuously innovate with thinner yet stronger interlayers to reduce weight while maintaining safety performance, aligning with automotive lightweighting trends. This combination of regulatory compulsion safety necessity and technological integration sustains the market leadership of laminated glass.

However, the tempered glass segment is predicted to witness the highest CAGR of 4.8% between 2026 and 2034 owing to its extensive application in side windows backlites and sunroofs. This product undergoes thermal or chemical treatment to increase its strength compared to normal glass and shatters into small granular chunks instead of sharp shards when broken. The rising production of electric vehicles which often feature expansive glass roofs to create an airy cabin atmosphere significantly boosts demand for large format tempered glass. Manufacturers are developing chemically strengthened tempered glass that allows for thinner profiles contributing to overall vehicle weight reduction and improved battery efficiency. The aftermarket sector also contributes to this growth as side windows are more susceptible to break ins and accidental damage than windshields. Innovations in heating elements embedded within tempered rear windows for defrosting and antenna integration add functional value. The cost effectiveness of tempered glass compared to laminated alternatives makes it the preferred choice for non critical visibility areas. As vehicle designs evolve toward greater transparency and openness, the volume of tempered glass required per unit continues to rise. This trend is driving robust segment growth.

By Application Insights

The windscreen application segment led the automotive glass market and captured a 35.5% share in 2025 because it is the most critical safety component of the vehicle glazing system and is subject to the strictest regulatory standards. Every passenger and commercial vehicle requires a front windshield made of laminated glass to ensure driver visibility and structural support. Consolidated global industrial indices published by the International Organization of Motor Vehicle Manufacturers (OICA) confirm that total global vehicle output surpassed 96 million units, driving a massive baseline demand for primary automotive glazing components. The integration of complex technologies such as heads up displays rain sensors and camera mounts for autonomous driving features directly into the windscreen increases its value and complexity. These advanced features necessitate precise manufacturing tolerances and optical clarity which barriers to entry for low quality competitors. Replacement rates for windscreens are higher than other glass components due to exposure to road debris stone chips and cracks which compromise structural integrity and sensor functionality. Insurance policies often cover windscreen repair or replacement encouraging timely maintenance and sustaining aftermarket volume. The trend toward larger and more curved windscreens to improve aerodynamics and aesthetic appeal further drives revenue growth. Manufacturers invest heavily in research to develop glasses that support 5G connectivity and enhanced acoustic damping. This indispensability combined with technological enrichment ensures the windscreen segment remains the largest contributor to market revenue.

On the contrary, the sunroof application segment is estimated to register the fastest CAGR of 6.2% during the forecast period owing to consumer preference for premium features and open cabin experiences in both luxury and mainstream vehicles. Panoramic sunroofs have transitioned from exclusive luxury options to standard features in many mid range sedans and sport utility vehicles enhancing perceived value and comfort. The shift toward electric vehicles has accelerated this trend as manufacturers use large glass roofs to compensate for the lack of engine noise and create a sense of spaciousness. Technological advancements in solar control coatings allow these large glass areas to manage heat gain effectively addressing previous consumer concerns about cabin temperature. The use of lightweight tempered glass for sunroofs supports vehicle efficiency goals while providing durability against hail and impact. Aftermarket customization of sunroofs also contributes to growth as owners seek to upgrade older models. Manufacturing innovations in bending and tempering large curved glass panels have reduced production costs making panoramic roofs more accessible. The aesthetic appeal and natural light benefits drive continuous adoption across various vehicle segments ensuring sustained high growth rates for this application category.

By End Use Insights

In 2025, the original equipment manufacturer segment held the majority share of the automotive glass market due to its direct correlation with global vehicle production volumes and the mandatory inclusion of glazing in every new unit. The International Organization of Motor Vehicle Manufacturers (OICA) confirms that global automotive manufacturing reached 96.4 million units, establishing a massive, high-volume production baseline for complete structural OEM glass assemblies. The tight integration of glass with vehicle design and safety systems means that automakers establish long term supply contracts with major glass manufacturers ensuring stable and predictable demand. The trend toward larger glass surfaces and integrated technologies in new vehicles increases the value per unit supplied to OEMs. Electric vehicle platforms often feature unique glass configurations such as fixed panoramic roofs which drive higher revenue per vehicle compared to traditional internal combustion engine cars. Quality standards for OEM glass are extremely high requiring zero defects and precise dimensional accuracy to fit automated assembly lines. Collaborative development between glass suppliers and automakers leads to customized solutions that differentiate brands. The consolidation of automotive production in Asia and Europe concentrates demand among key suppliers who can scale efficiently. While aftermarket volumes are significant they cannot match the sheer scale of initial equipment installation. This foundational link to vehicle manufacturing secures the OEM segment's leading position in the market.

But the aftermarket replacement segment is anticipated to witness the fastest CAGR of 5.5% from 2026 to 2034. This rapid expansion of the segment is supported by the increasing age of the global vehicle fleet and the high frequency of glass damage from road hazards. A study demonstrate that the average age of light vehicles on U.S. roads has climbed to a record high of 12.8 years, substantially expanding the operational volume of aging vehicles requiring out-of-warranty aftermarket maintenance and component replacement. Stone chips cracks and stress fractures are common occurrences that compromise safety and visibility necessitating timely replacement. Insurance coverage for glass repair encourages vehicle owners to address damage promptly rather than delaying until failure. The complexity of modern windshields with embedded sensors requires specialized calibration services which increases the value of aftermarket transactions. Independent repair shops and specialized glass service providers expand their networks to meet rising demand improving accessibility for consumers. The lack of standardized calibration procedures across different vehicle brands creates opportunities for skilled technicians to charge premium rates. Online platforms facilitating easy booking and mobile repair services enhance customer convenience driving volume growth. As vehicles become more technologically advanced the cost and complexity of replacement increase boosting revenue. The steady accumulation of older vehicles ensures a consistent and growing base of potential customers for aftermarket glass services.

By Vehicle Insights

The passenger cars segment was the largest in the automotive glass market and occupied a 62.1% share in 2025. This supremacy of the segment was credited to its overwhelming share of global vehicle production and high consumer turnover rates. Consumers prioritize aesthetics comfort and safety in passenger vehicles leading to the adoption of advanced glazing solutions such as acoustic laminated windshields and panoramic sunroofs. The competitive nature of the passenger car market prompts manufacturers to use distinctive glass designs as selling points enhancing brand identity. Frequent model updates and shorter ownership cycles in this segment ensure continuous demand for new glass technologies. The prevalence of compact and subcompact cars in emerging markets expands the volume base while luxury segments in developed markets drive value growth through premium features. Insurance claims for passenger car glass damage are high due to extensive urban driving and exposure to highway debris. The shift toward electric passenger cars further stimulates demand for lightweight and large format glass components. Aftermarket services for passenger cars are well established with widespread availability of replacement parts and skilled technicians. This combination of high volume technological adoption and robust service infrastructure maintains the passenger car segment's dominance.

The light commercial vehicle segment is likely to experience the fastest CAGR of 5.9% over the forecast period. This quick surge of the segment is fuelled by the exponential growth of e commerce and last mile delivery services. These vehicles operate intensively in stop and go traffic increasing the risk of glass damage from debris and minor collisions. Fleet operators prioritize quick and reliable glass replacement to minimize downtime and maintain delivery schedules. The design of modern light commercial vehicles increasingly incorporates larger windshields and side windows to improve driver visibility and safety in congested city environments. Regulatory emphasis on driver safety in commercial operations mandates high quality glazing that meets rigorous standards. The expansion of gig economy platforms has increased the number of independent contractors using personal light commercial vehicles further boosting aftermarket demand. Manufacturers are developing durable and cost effective glass solutions tailored for high usage commercial applications. The electrification of delivery fleets introduces new requirements for lightweight glass to extend driving range. This dynamic growth in logistics and delivery sectors ensures that light commercial vehicles outpace other segments in glass demand expansion.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific remained prominent in the global automotive glass market and accounted for a 45.5% share in 2025. This top position of the APAC market was driven by its status as the world’s largest vehicle manufacturing hub and rapidly growing middle class. China India Japan and South Korea are major production centers hosting facilities of leading global automakers and glass suppliers. The China Association of Automobile Manufacturers (CAAM) confirms that China's total automotive production reached an all-time record of 34.53 million units, creating an unprecedented baseline demand for advanced automotive glazing and structural glass components. Rising disposable incomes in Southeast Asian nations such as Indonesia and Thailand are accelerating vehicle ownership rates expanding the total addressable market. The region benefits from lower labor and production costs attracting investments in advanced glass manufacturing facilities. Government initiatives promoting electric vehicle adoption in China and India further stimulate demand for specialized lightweight and panoramic glass. The vast aftermarket potential is fueled by a large aging vehicle population and increasing awareness of safety standards. Local manufacturers are improving quality and technology capabilities to compete with international players. Urbanization and infrastructure development support higher vehicle usage rates leading to increased replacement frequency. The presence of raw material sources such as silica sand reduces input costs enhancing competitiveness. This combination of production scale consumption growth and policy support sustains Asia Pacific’s leadership in the global automotive glass landscape.

Europe Market Analysis

Europe was positioned second in the global automotive glass market with a 25.3% share in 2025. The region’s market share shows high production of premium vehicles and stringent safety and environmental regulations. Countries like Germany France and Spain are home to major automotive manufacturers who prioritize advanced glazing technologies for luxury and performance models. The European Automobile Manufacturers’ Association (ACEA) indicate that the EU produces over 12 million passenger cars annually, serving as a primary incubator for high-value technology integrations, including digital display windshields and premium smart-glass solutions. Strict Euro NCAP safety ratings mandate high performance laminated glass and pedestrian protection features driving continuous innovation. The European Green Deal pushes for lighter vehicles to reduce emissions encouraging the adoption of thin and strong glass compositions. A well established aftermarket network ensures high replacement rates supported by comprehensive insurance coverage. Consumer preference for sustainable and eco friendly products drives demand for recyclable glass materials and energy efficient manufacturing processes. The region leads in research and development collaborations between glass suppliers and automakers focusing on smart glass integration. High labor costs are offset by automation and technological superiority. The transition to electric mobility is advanced in Europe creating early demand for next generation glazing solutions. This focus on quality regulation and innovation keeps Europe at the forefront of high value automotive glass applications.

North America Market Analysis

North America witnessed steady growth in the global Automotive Glass Market due to high vehicle usage rates, a large existing fleet, and robust aftermarket services. The United States and Canada have some of the highest miles driven per capita globally leading to frequent exposure to road debris and weather related glass damage. According to the Auto Care Association the automotive aftermarket industry in the United States generates hundreds of billions in revenue annually with glass replacement being a significant component. The prevalence of sport utility vehicles and trucks which often feature large windshields and sunroofs boosts volume and value demand. Insurance companies play a crucial role by covering glass repairs with low or zero deductibles encouraging prompt replacement. The region is a leader in adopting advanced driver assistance systems which require specialized windshields with precise optical properties. Major glass manufacturers have strong distribution networks and service centers ensuring wide accessibility. The shift toward electric vehicles particularly in California and other progressive states drives demand for innovative glazing solutions. Labor shortages in the repair sector pose challenges but also drive wages and service values up. Consumer awareness of safety and comfort features supports the adoption of premium glass products. This mature market structure ensures stable and consistent growth driven by replacement needs and technological upgrades.

Latin America Market Analysis

Latin America holds a considerable share of the global automotive glass market. This region exhibits strong growth potential driven by stabilizing economic conditions and expanding local vehicle production. Brazil and Mexico are the primary markets benefiting from foreign investment in automotive manufacturing plants serving both domestic and export markets. Rising urbanization and improving infrastructure in countries like Colombia and Argentina increase vehicle usage and subsequent glass replacement needs. The aftermarket sector is fragmented but growing as consumers become more aware of safety standards and replace damaged glass rather than risking structural integrity. Economic volatility and currency fluctuations can impact purchasing power but essential maintenance remains a priority. Local manufacturers are upgrading technologies to meet international quality standards enabling exports to neighboring regions. Government incentives for automotive industry development encourage investment in supply chain localization. The increasing penetration of insurance products facilitates aftermarket growth by reducing out of pocket costs for consumers. While challenges remain regarding infrastructure and income inequality the long term trend toward motorization and safety consciousness supports gradual market expansion in Latin America.

Middle East and Africa Market Analysis

The Middle East and Africa region is expected to grow notably in the global automotive glass market from 2026 to 2034 due to luxury vehicle consumption in Gulf states and infrastructure development in Africa. Countries like the United Arab Emirates and Saudi Arabia have high per capita income levels leading to strong demand for premium vehicles with advanced glazing features such as tinted and solar control glass. The harsh climate in the Middle East necessitates high performance glass that blocks ultraviolet and infrared radiation to maintain cabin comfort. The aftermarket sector is developing as vehicle ownership rises in emerging African economies. Local production is limited leading to reliance on imports from Europe and Asia which affects pricing and availability. Government initiatives to diversify economies in the Gulf region include automotive manufacturing projects that will boost local OEM demand. Safety regulations are becoming stricter encouraging the adoption of laminated and tempered glass standards. While the market size is small compared to other regions the high value of luxury segment sales and potential for future growth make it an area of interest for specialized suppliers.

COMPETITIVE LANDSCAPE

The competitive landscape of the automotive glass market features intense rivalry among established multinational corporations and emerging regional manufacturers vying for dominance through innovation and cost efficiency. Major players differentiate themselves by offering integrated solutions that combine high performance glass with advanced technologies like augmented reality and connectivity. Regulatory compliance serves as a significant barrier to entry favoring companies with robust quality control systems and certification capabilities. Price competition exists but is secondary to value proposition as automakers prioritize safety reliability and technological integration. Consolidation trends persist as larger entities acquire specialized firms to secure proprietary technologies and expand geographic reach. Collaboration with original equipment manufacturers during early design phases creates sticky relationships and long term contracts. Sustainability credentials increasingly influence purchasing decisions prompting companies to highlight green manufacturing practices. The market remains dynamic with continuous advancements in material science and digital integration driving the need for ever more sophisticated glazing solutions. Intellectual property protection around smart glass technologies creates defensive moats for leading firms.

KEY MARKET PLAYERS

The major key players in the automotive glass market include

- Saint-Gobain (France)

- Asahi Glass (Japan)

- AGC Inc

- Fuyao Glass (China)

- Samvardhana Motherson (India)

- Webasto (Germany)

- Xinyi Glass (China)

- Nippon Sheet Glass (Japan)

- Gentex Corporation (US)

- Corning (US)

- Magna International (Canada)

Top Players In The Market

- Fuyao Glass Industry Group stands as a leading global supplier of automotive glass solutions with extensive manufacturing facilities across multiple continents. The company specializes in producing high quality laminated and tempered glass for windshields side windows and sunroofs. Recent initiatives include expanding production capacity in the United States and Europe to serve local automakers more efficiently and reduce logistics costs. Fuyao invests heavily in research and development to integrate smart technologies such as heads up displays and antenna systems into glass components. Their commitment to sustainability drives the adoption of energy efficient manufacturing processes and lightweight materials. Fuyao solidifies its position as a trusted partner in the global automotive supply chain by strengthening relationships with major original equipment manufacturers and enhancing aftermarket distribution networks. This growth is backed by its unwavering commitment to maintaining rigorous quality standards.

- AGC Inc is a prominent player in the automotive glass sector leveraging its advanced material science expertise to deliver innovative glazing solutions. The company focuses on developing lightweight and high strength glass products that support vehicle electrification and safety requirements. Recent actions include launching new panoramic roof systems with enhanced solar control properties to improve cabin comfort and energy efficiency. AGC collaborates closely with technology firms to integrate augmented reality features into windshields for next generation vehicles. They expand their global footprint by establishing technical centers in key automotive hubs to provide localized support and rapid prototyping services. Their emphasis on environmental sustainability leads to the development of recyclable glass materials and reduced carbon footprint production methods. This strategic focus on innovation and customer collaboration strengthens AGC’s reputation as a pioneer in advanced automotive glazing technologies.

- Saint Gobain maintains a strong presence in the automotive glass market through its comprehensive portfolio of safety and comfort oriented glazing products. The company emphasizes sustainable development by producing eco friendly glass using recycled materials and renewable energy sources. Recent developments include introducing acoustic laminated glass that significantly reduces noise pollution inside vehicle cabins enhancing passenger experience. Saint Gobain partners with automakers to create customized solutions for electric vehicles focusing on weight reduction and thermal management. They invest in digital tools for precise calibration of advanced driver assistance systems integrated into windshields. The organization expands its service network to offer faster and more reliable aftermarket replacements globally. Saint-Gobain prioritizes innovation, sustainability, and customer-centric solutions. By doing so, it reinforces its leadership role in delivering high-performance automotive glass that meets evolving regulatory and consumer demands.

Top Strategies Used By Key Market Participants

Key players in the automotive glass market primarily focus on technological innovation to integrate smart features such as heads up displays and sensor compatibility into glazing products. Companies invest heavily in research and development to create lightweight and durable materials that support electric vehicle efficiency and safety standards. Strategic expansion of manufacturing facilities in key automotive regions reduces logistics costs and improves supply chain resilience. Partnerships with automakers and technology firms facilitate co development of customized solutions for advanced driver assistance systems. Emphasis on sustainability drives the adoption of eco friendly production processes and recyclable materials to meet regulatory requirements. Enhancing aftermarket service networks ensures quick and reliable replacement options for consumers. Continuous improvement in product quality and optical clarity maintains competitive advantage in a highly regulated industry.

MARKET SEGMENTATION

This research report on the global automotive glass market has been segmented and sub-segmented into the following categories.

By Product

- Tempered

- Laminated

- Others

By Application

- Windscreen

- Backlite

- Sidelight

- Sunroof

By End-Use

- Original Equipment Manufacturer (OEM)

- Aftermarket Replacement (ARG)

By Vehicle

- Passenger Car

- Light Commercial

- Heavy Commercial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the automotive glass market?

The automotive glass market includes all safety and functional glass used in vehicles, such as windshields, side windows, rear windows, and roof glazing.

What is driving growth in the automotive glass market?

Growth is driven by rising vehicle production, stricter safety regulations, and increasing demand for comfort and visibility features.

Which type of glass is most commonly used in vehicles?

Laminated glass is most widely used in windshields due to its high impact resistance and safety performance.

What are the key applications of automotive glass?

Automotive glass is used in windshields, sidelites, backlites, sunroofs, and panoramic roof systems.

How is technology changing automotive glass?

Smart glass, HUD windshields, solar control coatings, and acoustic glazing are enhancing safety, energy efficiency, and driving comfort.

Which vehicles use the most automotive glass?

Passenger vehicles account for the highest automotive glass usage due to higher production volumes and advanced glazing features.

What role does automotive glass play in vehicle safety?

It supports structural integrity, prevents occupant ejection, and enables proper airbag deployment during accidents.

How does electric vehicle growth impact the automotive glass market?

EVs use larger glass areas and panoramic roofs, increasing demand for lightweight and heat-insulating glazing.

What materials are used to manufacture automotive glass?

Automotive glass is mainly made from silica-based tempered or laminated safety glass with specialized coatings.

What are the major challenges in the automotive glass market?

High replacement costs, raw material price volatility, and strict quality standards remain key challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com