Global Automotive Software Market Size, Share, Trends, & Growth Forecast Report, Segmented By Application (Safety System, Infotainment and Telematics, Powertrain, Chassis), Product (Operating System, Middleware, Application Software) And By Country (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa), Industry analysis Forecast 2026 to 2034

Global Automotive Software Market Size

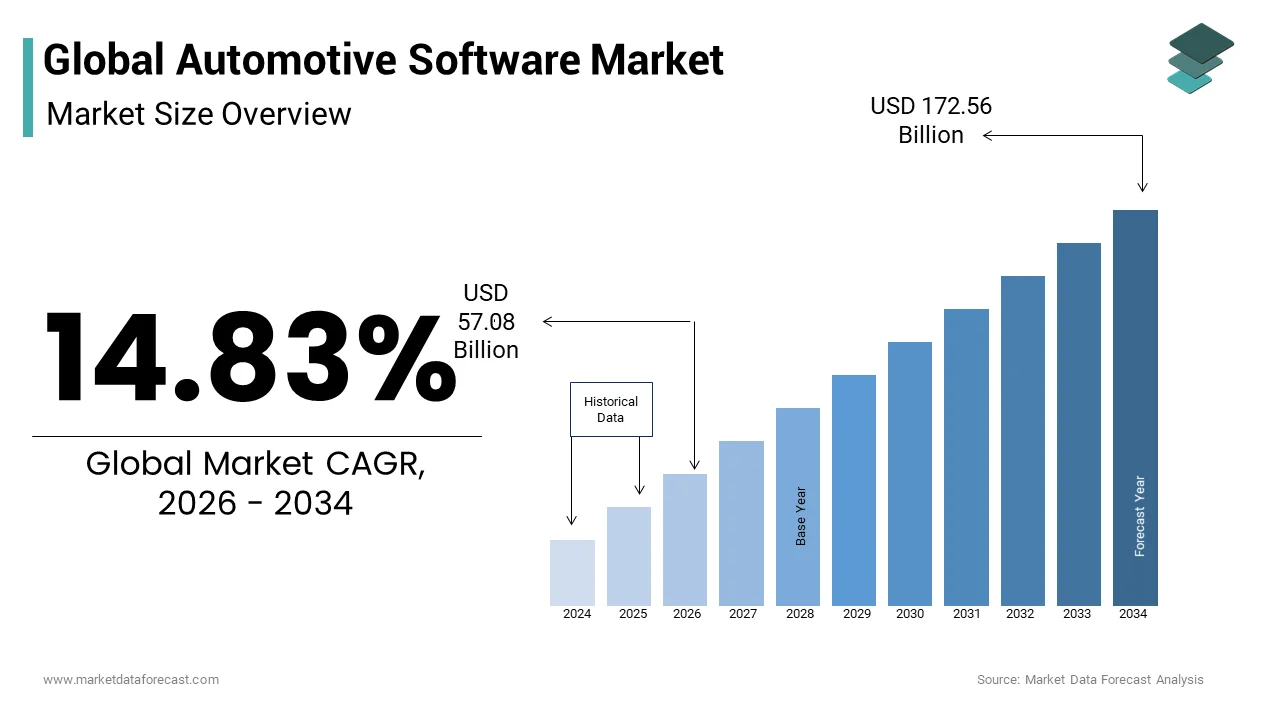

The global automotive software market size was valued at USD 49.71 billion in 2025 and is anticipated to reach USD 57.08 billion in 2026 to reach USD 172.56 billion by 2034, growing at a CAGR of 14.83% during the forecast period from 2026 to 2034.

Introduction to the Automotive Software Market

Automotive software is the digital backbone of modern vehicles. It consists of the code, operating systems, and applications that control everything in a car, from the engine and brakes to the entertainment system and driver-assistance features. As vehicles evolve into software defined platforms the integration of millions of lines of code has become central to modern automotive engineering. This transformation shifts the market focus from mechanical hardware to digital architecture enabling features such as over the air updates predictive maintenance and personalized user experiences. According to the IEEE Spectrum, a modern premium vehicle contains close to 100 million lines of software code, far surpassing the codebase complexity of advanced fighter jets like the F-22 Raptor. A study reveals that electronic components have risen to account for approximately 40% of a new car’s total manufacturing cost, a sharp increase from just 18% in the year 2000. Regulatory bodies worldwide are increasingly mandating cybersecurity standards and data privacy protections which further drives the need for robust software solutions. The transition towards electric mobility requires sophisticated battery management systems and energy optimization algorithms that rely entirely on advanced software frameworks. Consumers expect seamless connectivity similar to smartphones creating pressure on manufacturers to deliver intuitive interfaces and continuous feature enhancements. This paradigm shift necessitates collaboration between traditional automakers and technology firms to develop scalable secure and efficient software architectures that support the next generation of intelligent mobility solutions.

MARKET DRIVERS

Rising Adoption of Electric Vehicles Driving Complex Energy Management Needs

The rapid global adoption of electric vehicles is a key reason behind the expansion of the automotive software market. This is due to the intricate energy management requirements of battery-powered platforms. Unlike internal combustion engines electric powertrains rely heavily on software to optimize battery performance regulate thermal conditions and maximize driving range. According to the International Energy Agency global electric car sales surpassed 14 million units in 2023 representing a significant portion of new vehicle registrations worldwide. Each of these vehicles requires sophisticated battery management systems that monitor cell health balance charge levels and predict remaining range with high accuracy. Software algorithms play a crucial role in regenerative braking systems which recover energy during deceleration and feed it back into the battery pack. The complexity of managing high voltage systems safely necessitates redundant software controls and real time monitoring capabilities to prevent overheating or electrical failures. Automakers are investing heavily in developing proprietary software stacks that integrate charging infrastructure navigation and energy consumption data to provide users with seamless ownership experiences. The need for regular software updates to improve charging speeds and efficiency further drives demand for robust over the air update capabilities. As governments implement stricter emission regulations and phase out fossil fuel vehicles the reliance on software for electric vehicle operation will continue to intensify. This technological dependency ensures that software development remains a core competency for automotive manufacturers aiming to compete in the electrified mobility landscape.

Increasing Consumer Demand for Connected and Personalized In Vehicle Experiences

Growing consumer expectations for connected and personalized in vehicle experiences are significantly driving the demand for advanced solutions, which fuels the growth of the automotive software market. Modern drivers view their vehicles as extensions of their digital lives expecting seamless integration with smartphones cloud services and smart home devices. Sources reveal that over 60% of premium car buyers view advanced connectivity and personalized infotainment architectures as vital differentiators when finalizing their vehicle purchase. This shift has prompted automakers to develop sophisticated infotainment systems that support voice recognition augmented reality navigation and streaming entertainment. Software enables the creation of user profiles that store preferences for seating position climate control and media settings providing a tailored experience for every driver. The rise of subscription based services allows manufacturers to offer premium features such as enhanced navigation maps or performance boosts on demand generating recurring revenue streams. Connectivity also facilitates vehicle to everything communication which enhances safety by sharing real time traffic and hazard data with other road users. The integration of artificial intelligence allows systems to learn user habits and proactively suggest routes or services improving convenience and satisfaction. As 5G networks expand globally the bandwidth available for in vehicle applications increases enabling richer content and faster response times. This consumer driven demand for digital engagement compels manufacturers to prioritize software innovation and user interface design to maintain brand loyalty and competitive advantage in an increasingly tech focused market.

MARKET RESTRAINTS

High Complexity of Integration and Legacy System Compatibility Issues

The immense complexity of integrating new software with legacy vehicle architectures limits the growth of the automotive software market. Traditional automobiles were designed with distributed electronic control units that operate independently making it difficult to implement centralized software platforms required for modern features. SAE International establish that transition bottlenecks stem from scaling traditional, fragmented legacy Electronic Control Unit (ECU) topologies up to modern, centralized software-defined computing zones. Many established automakers struggle with fragmented software environments where different suppliers provide incompatible systems for various vehicle components. This lack of standardization leads to integration challenges that can cause system conflicts bugs and performance issues. The sheer volume of code involved in modern vehicles increases the likelihood of errors requiring rigorous testing and validation processes that delay product launches. Additionally maintaining compatibility between new software updates and existing hardware components poses ongoing technical hurdles for engineering teams. The transition from hardware defined to software defined vehicles requires a fundamental restructuring of development processes which many traditional manufacturers find difficult to execute efficiently. These integration difficulties result in higher production costs and potential reliability concerns that can damage brand reputation. Until industry-wide standards for software architecture and communication protocols are widely adopted, integration remains highly complex. Hence, this complexity will continue to hinder rapid innovation and market expansion.

Stringent Cybersecurity Regulations and Data Privacy Compliance Burdens

Strict cybersecurity regulations and data privacy compliance requirements further impose substantial operational burdens on developers in the automotive software market. This restricts agility and increases costs. As vehicles become more connected they become vulnerable to cyberattacks that can compromise safety and steal personal data. According to the United Nations Economic Commission for Europe new regulations such as UN R155 mandate that manufacturers implement robust cybersecurity management systems to obtain vehicle type approval. Compliance with these standards requires extensive documentation continuous monitoring and regular audits which divert resources from innovation and product development. The General Data Protection Regulation in Europe and similar laws globally require automakers to ensure that user data collected by vehicles is processed securely and transparently. Failure to comply can result in hefty fines and legal liabilities making risk management a top priority. Implementing encryption secure boot mechanisms and intrusion detection systems adds layers of complexity to software architecture. The need to protect against evolving threats means that security measures must be constantly updated requiring dedicated teams and ongoing investment. These regulatory pressures force manufacturers to adopt conservative approaches to software deployment potentially slowing down the release of new features. The balance between openness for innovation and strict security compliance remains a delicate challenge that constrains the speed at which new software solutions can be brought to market while ensuring full legal adherence.

MARKET OPPORTUNITIES

Expansion of Over the Air Update Capabilities Creating New Revenue Streams

The widespread adoption of over the air update capabilities is a key growth area for automakers to generate recurring revenue and enhance customer loyalty through continuous software improvements, which is expected to propel the automotive software market. Unlike traditional models where features were fixed at purchase over the air updates allow manufacturers to add new functionalities fix bugs and improve performance remotely. Studies indicate that deploying Over-the-Air (OTA) software updates can slash physical automotive manufacturer warranty and software recall costs by approximately 50%. This capability enables the introduction of subscription based services such as advanced driver assistance features premium navigation maps and entertainment packages that users can activate on demand. Automakers can leverage data from vehicle usage to tailor offerings and personalize recommendations increasing conversion rates for digital services. The ability to continuously improve the vehicle post sale transforms the ownership experience and extends the lifecycle value of the car. Manufacturers can also use over the air updates to optimize battery performance in electric vehicles or enhance fuel efficiency in hybrid models providing tangible benefits to users. This shift towards software as a service model aligns with broader technology trends and appeals to consumers accustomed to digital subscriptions. By building robust over the air infrastructure companies can create sustainable revenue streams that are less dependent on initial vehicle sales. This opportunity encourages investment in cloud infrastructure and software development talent to support long term digital service ecosystems.

Integration of Artificial Intelligence for Autonomous Driving Advancements

The integration of artificial intelligence into automotive software offers transformative opportunities for advancing autonomous driving technologies and enhancing vehicle safety, which is likely to promote the expansion of the automotive software market. AI algorithms process vast amounts of data from sensors cameras and radar to make real time decisions about navigation obstacle avoidance and traffic management. NVIDIA highlight that transitioning vehicles from basic driver-assist features to fully autonomous Level 4/5 self-driving systems creates an immediate requirement for centralized processing platforms exceeding 2,000 TOPS (Trillions of Operations Per Second) of computational power. Machine learning models enable vehicles to improve their driving behavior over time by learning from diverse scenarios and edge cases encountered on the road. This continuous learning capability is essential for achieving higher levels of autonomy where human intervention is minimal or unnecessary. AI also enhances predictive maintenance by analyzing vehicle data to identify potential failures before they occur reducing downtime and repair costs. Natural language processing improves voice assistant interactions making them more intuitive and responsive to user commands. The development of digital twins allows manufacturers to simulate and test software updates in virtual environments before deploying them to physical vehicles accelerating innovation cycles. Partnerships between automakers and AI specialists facilitate the development of specialized chips and software stacks optimized for autonomous tasks. As regulatory frameworks for autonomous vehicles evolve the ability to demonstrate safe and reliable AI decision making will become a key competitive differentiator. This technological frontier opens new markets for mobility as a service and robotic taxis driven by advanced software intelligence.

MARKET CHALLENGES

Shortage of Skilled Software Engineering Talent in the Automotive Sector

A critical shortage of skilled software engineers with expertise in automotive specific domains is a significant challenge to the industry’s ability to innovate and scale, and thereby holds back the growth of the automotive software market. Traditional automotive engineering focuses on mechanical and electrical systems leaving a gap in software development capabilities within established manufacturers. According to the Bureau of Labor Statistics the demand for software developers is projected to grow by 25 percent from 2022 to 2032 much faster than the average for all occupations. Automakers struggle to compete with technology giants for top talent who offer higher salaries and more flexible work environments. The specialized knowledge required for embedded systems real time operating systems and functional safety standards further narrows the pool of qualified candidates. This talent gap leads to project delays increased outsourcing costs and reliance on third party suppliers for critical software components. Training existing employees to bridge this skills gap takes time and resources which slows down transformation initiatives. The competition for AI and machine learning experts is particularly intense as these skills are essential for autonomous driving development. Without a sufficient workforce of skilled professionals manufacturers risk falling behind in the race to develop software defined vehicles. Addressing this challenge requires strategic partnerships with universities revised recruitment strategies and investment in internal training programs to build a sustainable pipeline of automotive software talent.

Fragmentation of Software Standards and Interoperability Issues

The lack of unified software standards and interoperability issues among different suppliers and platforms create significant inefficiencies and integration challenges for automakers in the automotive software market. Each component supplier often uses proprietary software protocols making it difficult to ensure seamless communication between various vehicle systems. The AUTOSAR Consortium focus on harmonizing standard infrastructure layers, though developers struggle to balance these rigid embedded standards with highly customized, data-heavy open-source operating systems. This fragmentation forces manufacturers to develop custom middleware to bridge gaps between incompatible systems increasing development time and cost. Inconsistent update mechanisms across different electronic control units can lead to synchronization issues and security vulnerabilities. The absence of common application programming interfaces hinders the development of third party apps and services that could enhance the user experience. Interoperability problems also complicate the integration of vehicles with smart city infrastructure and other connected devices limiting the potential of vehicle to everything communication. Standardization efforts are often slow due to competing interests among major players and the rapid pace of technological change. This lack of cohesion results in duplicated efforts and wasted resources as each automaker reinvents solutions for common problems. Fragmented software ecosystems will continue to hinder efficiency, innovation, and digital service delivery in modern vehicles. This issue will persist until the market converges on open and universal standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.83% |

| Segments Covered | By Application, Product, and Region. |

|

Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Adobe Systems Software Ireland Ltd., Airbiquity, BlackBerry Limited, Microsoft Corporation, Wind River Systems Inc., Atego, Green Hills Software, MontaVista Software, LLC, Autonet Mobile, Inc., GoogleTop of FormBottom of Form, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

In 2025, the application software segment dominated and held a substantial share of the automotive software market. Its direct interface with end users and its critical role in vehicle functionality drive the dominance of this segment. This layer includes infotainment systems navigation apps and driver assistance interfaces which are primary differentiators for modern vehicles. Research indicates that while application software represents the main point of consumer differentiation, it is part of a balanced stack where middleware and operating systems command up to 35% of total software-defined vehicle value. The dominance is driven by consumer demand for seamless connectivity and personalized experiences that mimic smartphone usability. Automakers invest heavily in developing intuitive user interfaces and integrating third party applications such as streaming services and productivity tools. The rise of over the air updates allows manufacturers to continuously enhance application features post purchase creating recurring engagement. High performance computing platforms enable complex graphical rendering and real time data processing required for advanced applications. The proliferation of electric vehicles further boosts this segment as digital cockpits become central to the driving experience replacing traditional physical controls. Consumers prioritize vehicles with robust app ecosystems leading manufacturers to prioritize application development in their design strategies. The ability to monetize these applications through subscriptions adds financial incentive for automakers to expand this segment. As vehicles evolve into mobile living spaces the importance of application software in defining brand identity and customer satisfaction continues to grow solidifying its market leadership.

However, the middleware segment is predicted to witness the highest CAGR of 18.1% from 2026 and 2034 due to the industry shift towards centralized electronic architectures that require robust communication layers between hardware and applications. According to Vector Informatik the complexity of vehicle networks necessitates sophisticated middleware solutions like AUTOSAR Adaptive to manage data flow and ensure interoperability among diverse components. Middleware acts as the bridge enabling different software modules to communicate efficiently without direct dependency on underlying hardware. The transition from distributed electronic control units to domain controllers increases the need for standardized middleware to simplify integration and reduce development time. Automakers are adopting service oriented architectures which rely heavily on middleware to facilitate dynamic service discovery and communication. The growth of autonomous driving features requires real time data processing and sensor fusion which middleware supports by managing high bandwidth data streams. Standardization efforts by industry consortia promote the adoption of open middleware platforms reducing vendor lock in and accelerating innovation. The ability of middleware to abstract hardware complexities allows software developers to focus on application logic rather than low level details. This efficiency gain drives widespread adoption across vehicle segments making middleware a critical enabler of next generation software defined vehicles.

By Application Insights

The ADAS and safety systems segment led the automotive software market and captured a significant share in 2025. This leading position of the segment was attributed to stringent global safety regulations and increasing consumer awareness of accident prevention technologies. Governments worldwide mandate the inclusion of features such as automatic emergency braking lane keeping assist and blind spot monitoring in new vehicles. Research published by the Insurance Institute for Highway Safety (IIHS) demonstrates that vehicles equipped with functional Advanced Driver Assistance Systems (ADAS) yield lower crash rates, providing the statistical basis for modern safety mandates. Following a multi-phase rollout by the European Parliament, the EU General Safety Regulation legally mandated Intelligent Speed Assistance (ISA) and emergency lane-keeping technologies for all newly registered factory vehicles starting in July 2024. These mandates create a guaranteed demand base for ADAS software regardless of consumer preference. Automakers integrate complex algorithms that process data from cameras radar and lidar sensors to make split second decisions that protect occupants and pedestrians. The software must meet rigorous functional safety standards such as ISO 26262 ensuring reliability under all operating conditions. Insurance companies offer discounts for vehicles with proven safety features further incentivizing consumer adoption. The continuous improvement of sensor accuracy and processing power enables more sophisticated ADAS capabilities enhancing market penetration. As the market moves towards higher levels of automation, the foundational software for safety systems becomes increasingly critical. This crucial role secures their dominance in the segment.

The autonomous driving software segment is estimated to register the fastest CAGR of 22.3% during the forecast period owing to intense investment in self-driving technology and mobility as a service models. Major technology companies and automakers are racing to develop Level 4 and Level 5 autonomous capabilities that eliminate the need for human intervention. According to Waymo autonomous ride hailing services have completed millions of trips demonstrating the viability of fully driverless operations in controlled environments. The software required for autonomy involves deep learning neural networks that interpret complex urban environments predict pedestrian behavior and plan safe trajectories. Massive datasets collected from test fleets are used to train these algorithms improving their decision making accuracy over time. The potential for autonomous trucks to operate 24 hours a day without rest breaks offers significant economic benefits for logistics companies driving commercial adoption. Regulatory frameworks are gradually evolving to permit testing and deployment of autonomous vehicles on public roads in specific regions. Partnerships between chip manufacturers and software developers accelerate the creation of specialized hardware software stacks optimized for autonomous tasks. The promise of reduced traffic congestion and improved road safety motivates government support for autonomous initiatives. As technology matures and costs decline the autonomous driving software segment is poised for exponential growth transforming urban mobility landscapes.

By Vehicle Insights

The passenger cars segment accounted for the majority share of the automotive software market in 2025 because of the high volume of production and intense competition among manufacturers to differentiate their offerings. Consumer expectations for premium digital experiences in personal vehicles drive extensive software integration across all price points. According to a source, global passenger car production exceeded 60 million units annually providing a massive installed base for software deployment. Automakers use software to create unique brand identities through customizable digital cockpits voice assistants and connected services. The rise of electric passenger cars further amplifies software content as battery management and energy optimization rely entirely on digital control systems. Families prioritize safety and entertainment features leading to widespread adoption of ADAS and rear seat infotainment software. The shorter replacement cycle of passenger cars compared to commercial vehicles ensures regular turnover and introduction of new software technologies. Over the air update capabilities allow manufacturers to keep passenger cars relevant and secure throughout their lifecycle enhancing resale value. The competitive landscape forces continuous innovation in user interface design and connectivity features to attract buyers. Marketing campaigns heavily emphasize software capabilities influencing purchasing decisions. The sheer scale of the passenger car market ensures that it remains the primary revenue generator for automotive software suppliers supporting extensive research and development investments.

On the contrary, the commercial vehicles segment is anticipated to witness the fastest CAGR of 16.6% between 2026 and 2034. This swift expansion of the segment is propelled by the need for operational efficiency and fleet management solutions. Logistics companies and transport operators leverage software to optimize routes monitor driver behavior and reduce fuel consumption. Also, the Technology & Maintenance Council (TMC) indicates that integrating connected telematics and fleet management software can reduce commercial fleet operational overhead by up to 15%. The expansion of e commerce has increased demand for last mile delivery vehicles equipped with sophisticated navigation and tracking software. Autonomous trucking initiatives aim to address driver shortages and improve safety on long haul routes requiring advanced software stacks. Regulatory requirements for electronic logging devices and emissions monitoring mandate software integration in commercial fleets. Connectivity enables real time data exchange between vehicles and central dispatch systems improving coordination and responsiveness. The total cost of ownership is a critical metric for commercial operators making software driven efficiency gains highly valuable. Integration with supply chain management platforms allows for seamless coordination of goods movement. As sustainability goals become stricter commercial vehicles require software to manage alternative powertrains and optimize energy usage. The focus on profitability and compliance ensures sustained investment in commercial vehicle software solutions.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the global automotive software market and occupied a 35.7% share in 2025. This supremacy of the regional market was driven by early adoption of connected technologies and strong presence of tech giants. The United States serves as the primary hub with major automotive software developers and technology firms headquartered in Silicon Valley and Detroit. Research indicates that global and domestic automotive OEMs have steadily expanded their R&D spending, shifting corporate strategies specifically toward electric powertrains and software features to comply with upcoming regulatory updates. Strict safety regulations from the National Highway Traffic Safety Administration mandate advanced driver assistance systems boosting software demand. Consumers in North America exhibit high willingness to pay for premium digital features and subscription services. The region benefits from robust telecommunications infrastructure supporting 5G connectivity for vehicles. Major automakers collaborate with technology companies to integrate cloud services and artificial intelligence into their platforms. The presence of venture capital funding supports startups developing innovative automotive software solutions. Government incentives for electric vehicles accelerate the adoption of software intensive powertrains. The mature aftermarket for software upgrades and diagnostics contributes significantly to regional revenue. North America leads in setting trends for software defined vehicles influencing global standards and practices.

Europe Market Analysis

Europe was the next prominent region in the automotive software market and captured a share of 30.3% in 2025. This growth of the European market was fuelled by stringent regulatory frameworks and emphasis on safety and sustainability. Germany France and Sweden are key contributors with established automotive manufacturers investing heavily in software engineering. Following the enforcement of the General Data Protection Regulation (GDPR) by the European Parliament, automotive developers operating within Europe must enforce "privacy-by-design" software architecture to secure connected-car telemetry. The European Green Deal promotes electric mobility driving demand for battery management and energy optimization software. Automakers in Europe prioritize functional safety standards ensuring high reliability of software systems. The region leads in developing open source automotive software platforms through collaborations like Eclipse Foundation. High fuel prices and environmental consciousness encourage adoption of software solutions that improve efficiency. Strong labor unions and engineering traditions support high quality software development. Cross border initiatives promote harmonization of software standards across member states. The focus on sustainable manufacturing extends to software lifecycle management including recycling and updates. Europe remains a center for automotive innovation balancing tradition with digital transformation.

Asia Pacific Market Analysis

Asia Pacific is the fastest growing region in the automotive software market due to rapid electrification and digitalization in China and India. China is the world largest electric vehicle market requiring sophisticated software for battery management and connectivity. According to the China Association of Automobile Manufacturers electric vehicle penetration reached 35 percent in 2023 driving software demand. Local technology firms collaborate with automakers to develop customized infotainment and autonomous driving solutions. India is emerging as a hub for automotive software outsourcing due to skilled engineering talent and cost advantages. Governments in the region support smart city initiatives that integrate vehicles with urban infrastructure. High smartphone penetration influences consumer expectations for seamless in vehicle connectivity. Rapid urbanization increases demand for efficient public transport systems managed by software. The region benefits from competitive manufacturing costs enabling scalable software deployment. Partnerships between local and global players facilitate technology transfer and innovation. Asia Pacific dynamic market environment offers significant opportunities for software providers.

Latin America Market Analysis

Latin America is a developing segment of the automotive software market owing to increasing vehicle production and adoption of safety technologies. Brazil and Mexico are the primary markets with expanding automotive industries integrating global software standards. Strategic initiatives funded by the Inter-American Development Bank (IDB) target regional electromobility and public transit digital transformations, establishing the structural baseline needed for intelligent connected vehicle technologies. Economic challenges limit widespread adoption of premium software features but basic safety and telemetry solutions gain traction. Local manufacturers partner with global suppliers to access advanced software capabilities. Regulatory bodies gradually adopt international safety standards mandating basic ADAS features. The growth of ride hailing services creates demand for fleet management and navigation software. Currency fluctuations impact purchasing power but long term trends favor digital integration. Education initiatives aim to build local software engineering capacity. The region relies on imports for advanced software solutions creating opportunities for global providers. Latin America potential for growth lies in affordable connectivity and safety solutions.

Middle East and Africa Market Analysis

Middle East and Africa region is anticipated to expand notably in the automotive software market during the forecast period due to luxury vehicle adoption in Gulf countries and gradual modernization in Africa. The United Arab Emirates and Saudi Arabia invest in smart mobility projects requiring advanced software for autonomous and connected vehicles. Also, the International Monetary Fund (IMF) highlight aggressive non-oil diversification policies across Gulf nations, which have directly funneled sovereign capital into national smart mobility and electric vehicle software ventures. High temperatures and harsh conditions require robust software for thermal management and vehicle monitoring. Africa faces infrastructure challenges but mobile money and telematics solutions gain popularity for logistics. Limited local manufacturing means reliance on imported software enabled vehicles. Government initiatives in smart cities drive pilot projects for autonomous shuttles. The region focuses on high end luxury features in major urban centers. Cybersecurity concerns grow as connectivity increases. Opportunities exist for specialized solutions adapted to local conditions. The market status is evolving with increasing interest in digital mobility solutions.

COMPETITIVE LANDSCAPE

The competition in the automotive software market is characterized by intense rivalry among established technology giants traditional automotive suppliers and emerging startups who strive to dominate the software defined vehicle landscape. These key players leverage their extensive expertise in cloud computing embedded systems and artificial intelligence to develop comprehensive solutions that meet the complex needs of modern automakers. The barrier to entry is significant due to the need for rigorous safety certifications and deep integration with vehicle hardware architectures. Competitors distinguish themselves through unique value propositions such as superior cybersecurity robust over the air update capabilities and advanced user interface designs. Price competition is moderate as reliability and compliance often outweigh cost considerations for buyers in this critical safety segment. However new entrants from the tech industry bring agile development practices and innovative business models that challenge traditional players. Strategic alliances with automakers are critical for securing long term contracts and influencing industry standards. The focus on sustainability and energy efficiency further intensifies competition as firms seek to develop software that optimizes electric vehicle performance and reduces environmental impact through intelligent energy management systems.

KEY MARKET PLAYERS

These are the market players that are dominating the automotive software market.

- Adobe Systems Software Ireland Ltd

- Airbiquity

- BlackBerry Limited

- Microsoft Corporation,

- Wind River Systems Inc.

- Atego

- Green Hills Software

- MontaVista Software

- LLC

- Autonet Mobile, Inc

- GoogleTop of FormBottom of Form

Top Players In The Market

- BlackBerry Limited has transformed from a mobile device manufacturer into a leading provider of automotive cybersecurity and embedded software solutions. The company offers the QNX operating system which powers millions of vehicles globally ensuring high reliability and safety for digital cockpits and autonomous driving systems. BlackBerry recently expanded its partnership with major automakers to integrate artificial intelligence capabilities into vehicle platforms enhancing real time decision making. Its focus on secure over the air updates protects vehicles from cyber threats while enabling continuous feature improvements. By prioritizing functional safety standards and robust encryption protocols BlackBerry strengthens its position as a trusted partner for manufacturers seeking to build secure and scalable software defined vehicles that meet stringent global regulatory requirements and consumer expectations for data privacy.

- Microsoft Corporation leverages its Azure cloud computing platform to provide comprehensive automotive software services including connectivity data analytics and artificial intelligence tools. The company collaborates extensively with global automakers to develop digital vehicle platforms that enable seamless integration of cloud based applications and services. Microsoft recently launched specialized automotive clouds that support over the air updates and predictive maintenance functionalities helping manufacturers reduce downtime and improve customer satisfaction. Its expertise in machine learning allows for advanced driver assistance features and personalized user experiences. By offering scalable infrastructure and developer tools Microsoft empowers automakers to accelerate innovation and deploy software updates efficiently. This strategic focus on cloud native solutions positions Microsoft as a critical enabler of the industry transition towards connected and autonomous mobility ecosystems.

- Elektrobit Automotive GmbH is a prominent supplier of embedded software and electronic solutions specializing in operating systems middleware and user interface technologies. The company provides comprehensive software stacks that support complex vehicle architectures and facilitate the integration of various hardware components. Elektrobit recently enhanced its portfolio with advanced tools for automated testing and validation ensuring high quality software delivery for safety critical applications. Its expertise in AUTOSAR standards enables seamless communication between different vehicle systems improving overall performance and reliability. The company actively collaborates with semiconductor manufacturers to optimize software for next generation chips reducing development time and costs. By focusing on modular and scalable software solutions Elektrobit helps automakers manage increasing complexity and accelerate time to market for innovative digital features in modern vehicles.

Top Strategies Used By Key Market Participants

Key players in the automotive software market primarily employ strategic partnerships with technology firms and semiconductor manufacturers to enhance their technological capabilities and accelerate product development. Companies frequently engage in joint ventures to co develop integrated software platforms that meet specific automotive standards and regulatory requirements. Innovation through research and development remains a central strategy as firms invest heavily in artificial intelligence cloud computing and cybersecurity solutions. Mergers and acquisitions are utilized to acquire specialized software expertise and expand product portfolios quickly. Additionally manufacturers focus on creating open source ecosystems to foster collaboration and reduce development costs for automakers. Digital transformation initiatives including agile development methodologies and continuous integration practices are increasingly adopted to improve software quality and speed up release cycles. These strategies help companies maintain competitive advantage and respond effectively to the rapidly evolving demands of the software defined vehicle landscape.

MARKET SEGMENTATION

This research report on the automotive software Market is segmented and sub-segmented into the following categories.

By Application

- Safety System

- Engine Management System

- Infotainment and Telematics

- Powertrain

- Chassis

By Product

- Operating system

- Middleware

- Application software

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Why is the global automotive software market becoming a key driver of next-generation mobility?

The market is expanding rapidly due to the rise of software-defined vehicles, increasing adoption of connected car technologies, growing electric vehicle production, and advancements in autonomous driving systems.

What is automotive software and how is it used in modern vehicles?

Automotive software consists of embedded programs and digital platforms that manage vehicle functions such as infotainment, ADAS, powertrain control, battery management, connectivity, cybersecurity, and over-the-air (OTA) updates.

How does automotive software improve vehicle performance and the driving experience?

It enhances vehicle safety, enables real-time diagnostics, supports intelligent navigation, optimizes energy management, delivers connected services, and provides seamless in-vehicle user experiences.

Which software segment holds the largest share of the global automotive software market?

Advanced Driver Assistance Systems (ADAS) software accounts for a significant market share due to the growing integration of safety and driver-support features in modern vehicles.

What factors are driving demand for automotive software worldwide?

Increasing vehicle electrification, stricter safety regulations, rising consumer demand for connected features, growth in autonomous driving, and rapid digital transformation across the automotive industry are driving market demand.

Which vehicle segment generates the highest demand for automotive software solutions?

Passenger vehicles generate the highest demand as automakers integrate advanced infotainment systems, connectivity platforms, ADAS, and software-enabled vehicle features.

What technologies are shaping the future of the automotive software market?

Artificial intelligence, cloud computing, edge computing, vehicle-to-everything (V2X) communication, digital twins, cybersecurity platforms, and over-the-air software updates are shaping the future of the market.

How are software-defined vehicles transforming the automotive industry?

Software-defined vehicles enable continuous feature upgrades, remote diagnostics, predictive maintenance, personalized driving experiences, and faster deployment of new functionalities through software updates.

What challenges could affect the growth of the global automotive software market?

Cybersecurity risks, software complexity, semiconductor shortages, regulatory compliance requirements, and integration challenges across vehicle platforms could affect market growth.

Which regions are expected to lead the global automotive software market?

Asia Pacific leads the market due to strong automotive manufacturing and EV production, while North America and Europe continue to drive innovation through autonomous driving, connected mobility, and software-defined vehicle development.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com