- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

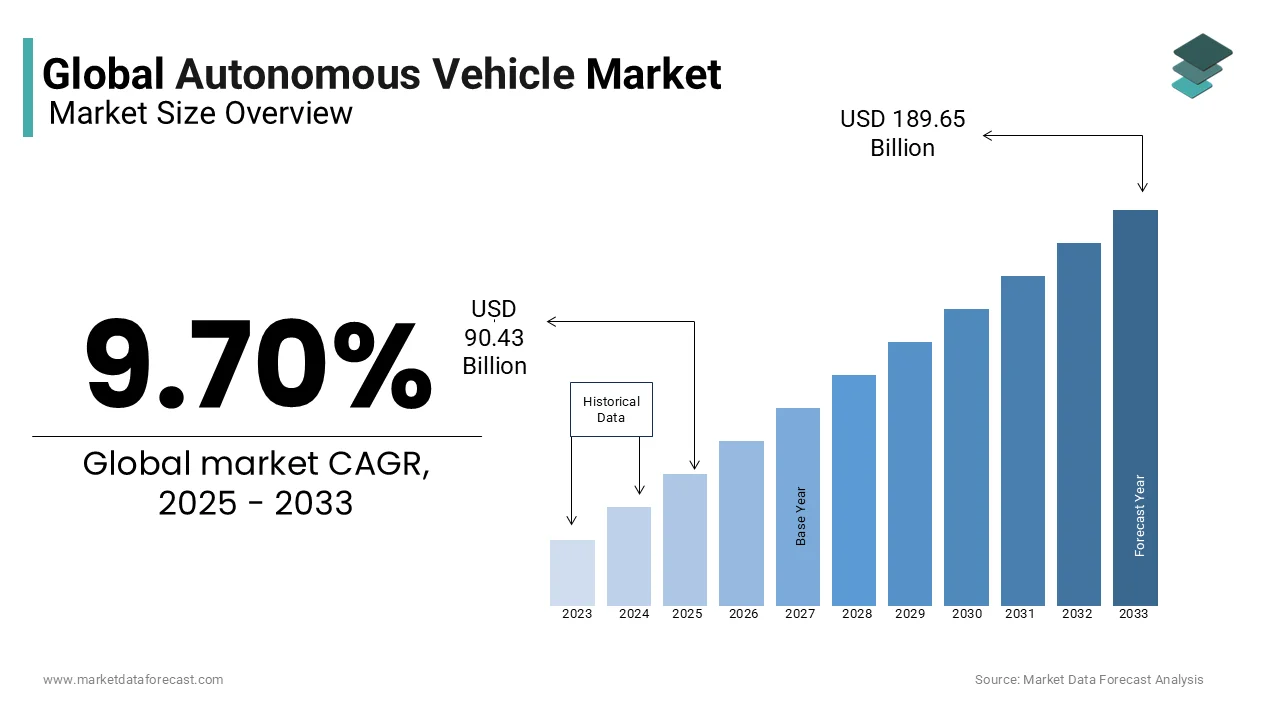

Market Size, 2025

$34.74 BnMarket Estimate, 2026

$39.26 BnMarket Forecast, 2034

$104.36 BnCAGR, 2026–2034

13%Global Autonomous Vehicle Market Size

The global autonomous vehicle market was valued at USD 34.74 billion in 2025 and is anticipated to reach USD 39.26 billion in 2026 from USD 104.36 billion by 2034, growing at a CAGR of 13% during the forecast period 2026 to 2034.

The global automotive industry is experiencing a time of wide-ranging and transformative changes with the shift in customer behavior, as well as the expanding usage of stringent environmental guidelines. Factors like increasing safety and security concerns, growing demand for dependable transportation frameworks, andthe approach of progressive trends, such as the transition from car ownership to "Mobility as a Service" (MaaS), are expected to drive the interest in autonomous vehicles. These vehicles are the key to changing urban transportation to the point of being indistinguishable in the next few years. There are both conventional OEMs and new vehicle engineers who are working in this biological system to improve and introduce completely autonomous vehicles on the road. These vehicles will have propelled features from conventional cars that will enhance the driving experience for travelers.

Autonomous vehicles, otherwise called self-driving vehicles, use artificial intelligence (AI) programming, light detection & ranging (LiDAR), and RADAR sensing technology, which is additionally used to screen a 60-meter range around the vehicle and to shape a functioning 3D map of the immediate environment. The vehicle is intended to travel between destinations without a human administrator. They consolidate sensors and software to control, explore, and drive the vehicle. Most self-driving frameworks make and maintain an internal map of their environment based on a wide array of sensors, similar to radar.

MARKET DRIVERS

Through the Internet of Things, vehicle drivers improve their performance by accepting the ongoing input from rapid in-memory computing frameworks built into associated cars. These built-in computers offer highlights such as gathering, examining, and storing data, which helps make decisions. The wide selection of related cars is expected to create rewarding opportunities for autonomous and semi-autonomous vehicles.

The rapid development of economies guarantees vigorous improvement from transport infrastructure to the advancement of smart cities. Numerous countries, for example, Mexico, Canada, and the US, are implementing digital infrastructure to encourage connectivity among vehicles and infrastructure to collect essential data, thereby decreasing traffic congestion and increasing road security. The advancement of smart cities is likely to drive this market substantially.

MARKET RESTRAINTS

Due to steady innovative advancements, the software in these vehicles needs to be often upgraded to keep them compatible with the outside environment. Likewise, the expense of all components and the sensor assembly in autonomous cars is more than riding in vehicles. In addition, the proportion of premium buyers to that of economic purchasers is very low universally, as it is hard for ordinary people to manage the cost of high-end cars. Therefore, a high introductory price combined with maintenance costs hampers the reception of autonomous vehicles.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13% |

| Segments Covered | By Level of Automation, Component, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Uber Technologies Inc., Daimler AG, Google Inc., Toyota Motor Corp, Nissan Motor Co., Ltd., Volvo Cars, General Motors Company, Volkswagen AG, Tesla Inc., BMW, and Others. |

SEGMENTAL ANALYSIS

By Level of Automation Insights

Features such as versatile cruise control or pathkeeping are part of level 1 of automation. In level 2, the vehicle framework can control the braking, steering, or acceleration of the vehicle. These highlights can be applied together, and the coordination between at least two of these technologies encourages a vehicle to be of Level 2 status.

In level 3, the vehicle framework can recognize the environment around it, utilizing sensors such as LiDARs, and make decisions, such as passing a slower-moving vehicle before it. The vehicle framework can oversee most parts of driving, including checking the environment. The system prompts the driver to mediate when it experiences a situation it can't navigate. In level 4, the vehicle can function without human interruption; however, only in specific conditions. There is an alternative to overriding the vehicle framework functions manually. At this level, the vehicles can work as driverless vehicles in any street condition. These vehicles are being created to be utilized as Robo-taxis, such as Waymo, among others.

By Component Insights

Vehicle-sharing services, such as car or taxi sharing, are foreseen to reach an ideal adoption rate, as individuals are expected to utilize these services more regularly because of affordability and comfort. This aspect is anticipated to increase interest in autonomous vehicles during the projected time.

By Application Insights

Some of the advantages of automation in this field include savings in the cost of work and a decrease in carbon dioxide emissions on the earth through advanced driving. These variables are relied upon to increase the interest in autonomous vehicles during the estimated period.

REGIONAL ANALYSIS

Western Europe establishes the predominant portion of the global autonomous vehicles market because of the high adoption rate of such vehicles in the region. North America is the second leading market for autonomous vehicles, following Western Europe. North America and Europe secured the greater part of the global market in 2018 and are expected to continue to expand their market share during the predicted time, attributable to the expanding launch of semi-autonomous car models and developing improvements towards semi-autonomous vehicle systems among players in the automotive industry.

China, India, and Japan are the significant manufacturing nations of autonomous vehicles in the Asia Pacific, which is estimated to surpass Europe and North America in interest in autonomous vehicles. The reception of autonomous vehicles in developing regions such as Latin America and the Middle East & Africa is evaluated to be lower than that in the different areas. However, the market for autonomous vehicles is growing in developing nations.

COMPETITIVE LANDSCAPE

The Autonomous Vehicle Market is a high-stakes global race defined by technological prowess, regulatory navigation, and ecosystem partnerships. Tesla’s camera-only, fleet-learning approach contrasts with Waymo’s lidar-redundant, safety-certified model, while GM’s Cruise leverages manufacturing scale for purpose-built robotaxis. Traditional automakers like BMW and Volvo collaborate with tech firms to accelerate development, while Chinese players like Baidu and Pony.ai challenge with localized AI. Regulatory hurdles and safety incidents intensify scrutiny.

KEY MARKET PLAYERS

These are the market players that dominate the global autonomous vehicles market.

- Uber Technologies Inc.

- Daimler AG

- Waymo (Alphabet/Google) (US)

- Google Inc.

- Toyota Motor Corp

- Nissan Motor Co. Ltd

- Volvo Cars

- General Motors Company

- Volkswagen AG

- Tesla Inc., BMW.

Volvo and Chinese internet service provider Baidu have joined hands to create and mass-produce self-driving electric cars in China. Volvo will offer its aptitude for advanced innovations in the auto industry, whereas Baidu gives its autonomous driving platform, Apollo.

Top Players In The Market

- Tesla leads the Autonomous Vehicle Market through its vertically integrated approach, combining proprietary AI chips, real-world data from millions of fleet vehicles, and over-the-air software updates. Its Full Self-Driving (FSD) Beta program continuously evolves via neural net training from actual driver interactions. Recently, Tesla expanded FSD to international markets, introduced its “AI Day” to showcase Dojo supercomputer progress, and began retrofitting older models with Hardware 4. It also launched its robotaxi prototype, “Cybercab,” which is signaling intent to disrupt mobility-as-a-service.

- Waymo, under Alphabet, pioneers the Autonomous Vehicle Market with its safety-first, lidar-centric approach and commercial robotaxi services. Operating in multiple U.S. cities, Waymo One offers fully driverless rides, validated by billions of simulated and real-world miles. Recently, Waymo expanded its autonomous trucking pilot with Uber Freight and partnered with Geely’s Zeekr to co-develop next-gen robotaxi platforms for global deployment. It also enhanced its “Waymo Driver” AI with improved behavior prediction in complex urban environments.

- General Motors drives the Autonomous Vehicle Market through its majority-owned subsidiary, Cruise, which develops and deploys all-electric, purpose-built robotaxis. Cruise’s Origin vehicle, designed without manual controls, targets urban ride-hailing. Despite regulatory pauses, GM recently resumed limited driverless operations in Phoenix and Austin, enhanced its AI simulation capabilities, and integrated GM’s Ultium battery platform for extended range. It also deepened partnerships with Microsoft for cloud-based AI training and Honda for global expansion.

Top Strategies Used By The Key Market Participants

Key players deploy massive real-world and simulated datasets to train AI perception systems. They develop proprietary silicon and neural networks for edge processing. Strategic OEM partnerships enable scalable vehicle integration. Regulatory engagement and safety validation remain top priorities. Subscription and mobility-as-a-service models monetize autonomy. Over-the-air updates enable continuous improvement. Urban geofenced deployments allow controlled scaling. Cybersecurity and ethical AI frameworks build public trust. Vertical integration from hardware to software ensures system optimization.

The Autonomous Vehicle Market is a high-stakes global race defined by technological prowess, regulatory navigation, and ecosystem partnerships. Tesla’s camera-only, fleet-learning approach contrasts with Waymo’s lidar-redundant, safety-certified model, while GM’s Cruise leverages manufacturing scale for purpose-built robotaxis. Traditional automakers like BMW and Volvo collaborate with tech firms to accelerate development, while Chinese players like Baidu and Pony.ai challenge with localized AI. Regulatory hurdles and safety incidents intensify scrutiny.

RECENT MARKET NEWS

- A self-driving car service being tried by Waymo opened up to more individuals in the Phoenix, Arizona area in late 2018.

- Waymo anticipated that organizations should be keen on utilizing the autonomous ride service to carry clients to and from shops.

- Self-driving vehicle innovation is likely to be utilized in long-haul trucking since distant parts of routes can be monotonous highway stretches with fewer factors to deal with than on local streets.

- In late 2019, Hyundai became the newest car producer to offer autonomous rides in the US market.

- Las Vegas: Not long from now, you could ride one, two, or three wheels or maybe none at all. Some innovators played with long-established ideas like the bicycle or scooter by including artificial intelligence, electric power, and other technologies.

- Adjustments of the bicycle, implanted with new tech for the associated generation, showed up at CES. French start-up Wello showed its open-sided, three-wheeled car-bike that depends on accelerating, electric force, and solar panels on the roof, currently being used by French postal services.

- Forget driverless cars, SDE's innovative autonomous navigation system - Genesis – can transform any boat or ship into an unmanned vessel. From securing the coastline to clearing waste, the potential for this innovation is boundless.

MARKET SEGMENTATION

This research report on the global autonomous vehicle market is segmented and sub-segmented into the following categories.

By Level of Automation

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

By Component

- Hardware

- Software

- Service

By Application

- Civil

- Robo taxi

- Ride hail

- Rideshare

- Self-driving truck

- Self-driving bus.

By Application

- Civil

- Robo taxi

- Ride hail

- Rideshare

- Self-driving truck

- Self-driving bus.

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa