Global Blood Screening Market Size, Share, Trends & Growth Analysis Report By Technology, Product, End User and Region - Industry Forecast (2026 to 2034)

Market Size, 2025

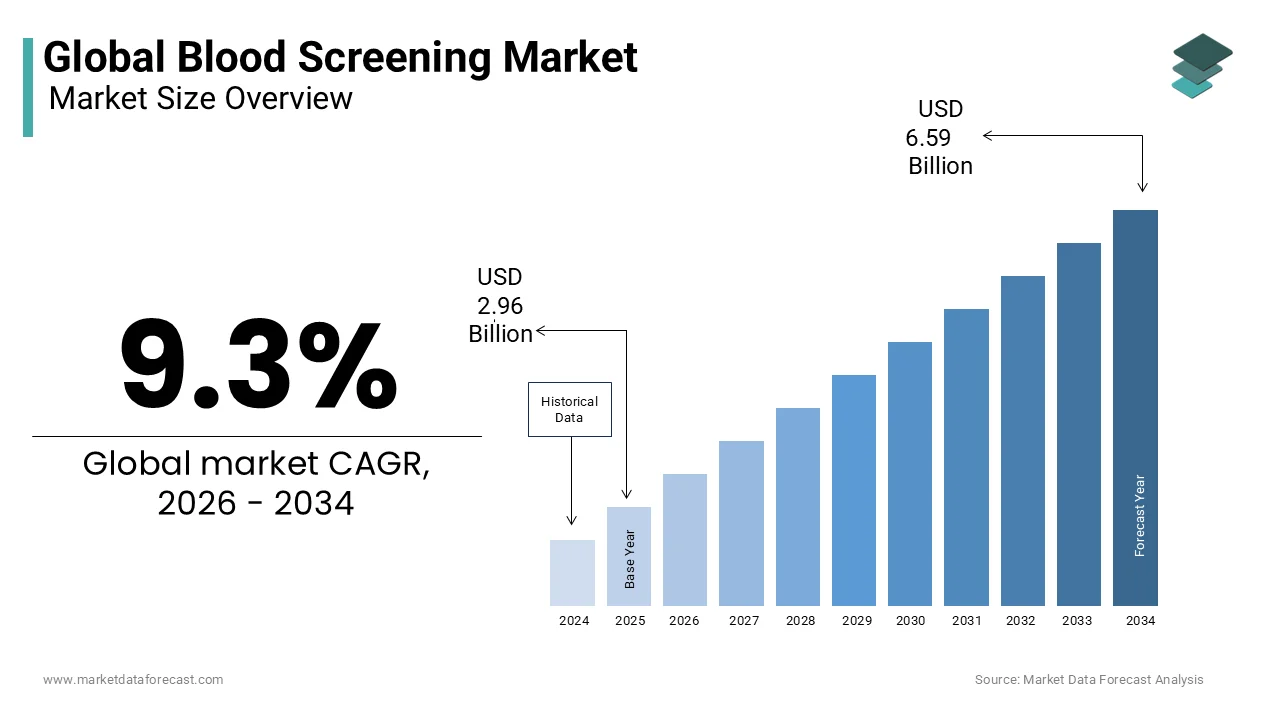

$2.96 BnMarket Estimate, 2026

$3.24 BnMarket Forecast, 2034

$6.59 BnCAGR, 2026–2034

9.3%Global Blood Screening Market Size

The global blood screening market was valued at USD 2.96 billion in 2025 and increased to USD 3.24 billion in 2026. The market is projected to reach USD 6.59 billion by 2034, growing at a CAGR of 9.3% from 2026 to 2034.

Blood screening refers to a variety of tests performed on blood samples to diagnose illnesses including AIDS, hepatitis, and syphilis, as well as other clinical situations, including pregnancy. It aids in detecting and preventing diseases and a range of other conditions such as infections and cancer. Before donating blood, blood donors are subjected to screening to prevent the transmission of infection. Blood is a liquid-based biological substance that has multiple cells and proteins floating in it. It is a fluid that contains red blood cells, white blood cells, and platelets and circulates throughout the body. Through capillaries, arteries, and veins, it transports oxygen and nutrients to the body's cells. It also aids the body's removal of metabolic waste and carbon dioxide. Blood screening aids in detecting and preventing illnesses and a range of other diseases such as infections and cancer.The nucleic acid amplification test was initially introduced in six European countries, France, Germany, Italy, Spain, the UK, and Switzerland, in early 1999 and 2001.

MARKET DRIVERS

Y-O-Y in growth in the number of blood donations, the prevalence of newer pathogens, and the increased incidence of contagious diseases are primarily accelerating the growth rate of the global blood screening market.

Increasing blood donations among people is one of the significant factors propelling the global blood screening market during the forecast period. Blood donation among the people has increased from 3.4% in 2008 to 3.6% in 2010. Nearly 2million people donate blood regularly in Germany every year. Additionally, factors such as a high patient pool and increasing disposable income of the people across the regions are likely to propel the market. Advancing healthcare infrastructure, raising awareness regarding maintaining blood safety, and rising healthcare expenditure are expected to drive the blood screening market during the forecast period. Acquisitions and mergers and critical developments, and supply chain trends are driving the market. Moreover, initiatives, investment, and funding the government to create awareness among the people about the safety blood donation influence market growth. In addition, technological advancements in blood screening methods drive market growth. Over the forecast period, rising technical developments and introducing new technologies such as pathogen reduction technology, microbiological screening, and multiplexing are likely to provide significant revenue possibilities for companies in the target market. The most common blood-screening tests include screening donated blood in blood banks for transfusion-transmitted pathogens and blood testing for infectious illnesses in hospitals and clinical laboratories, which positively impacts the market revenue.

Furthermore, emerging countries worldwide provide lucrative growth opportunities for market players operating the market, thereby increasing market growth. growing blood campaigns across the developing countries and increasing voluntary blood donors uplift the market growth. Growing need to diagnose samples and increasing infectious diseases is elevating the demand of the market. The government has taken so many initiatives to bring awareness among the people related to donating blood and screening before transfusion, which accelerates the blood screening market growth.

The global blood screening market is expected to grow rapidly shortly and to provide lucrative growth opportunities such as the emergence of microbiology screening, multiplexing, and pathogen reduction technologies. Also, factors like the increasing economies of developing nations and technological improvements are expected to offer another set of opportunities for the market's growth.

MARKET RESTRAINTS

The primary factor restraining the blood screening market is the high cost, which needed to be reduced. Lack of awareness among the people about donating blood may also hamper market growth. Lack of lab technicians among the hospitals and clinical laboratories may also restrict the market growth over the review period. Strict regulations to approve new screening devices into the market over the analysis period may limit the growth. The availability of other alternative technologies like digital immunoassays restricts the blood screening market growth over the period.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Analysed | By Technology, Product, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Becton, Dickinson and Company, Thermo Fisher Scientific Inc., Ortho Clinical Diagnostics |

SEGMENTAL ANALYSIS

By Technology Insights

Based on technology, the nucleic acid amplification segment is expected to dominate the global blood screening market due to factors such as the increasing applications of NAT technology and the growing number of blood donations.The Elisa segment is expected to occupy the second-largest share in the global blood screening market over the period due to the low cost and standard increase of infectious diseases.

By Product Insights

Based on the product, the reagents & kits segment is accounted for the largest share and maintains its dominance over the period. Cost-effectiveness and specificity in examining the appearance of various elements drive this market segment to the extent.The instruments segment accounts for the highest share in the market due to the introduction of new devices into the market by key players.

By End User Insights

Based on end-user, the blood bank segment is contributing a significant share of the revenue. Moreover, it is likely to grow further during the forecast period due to factors like increasing organ transplantation surgeries, increasing awareness about blood donation and safety, and increasing investments from private and public organizations.

REGIONAL ANALYSIS

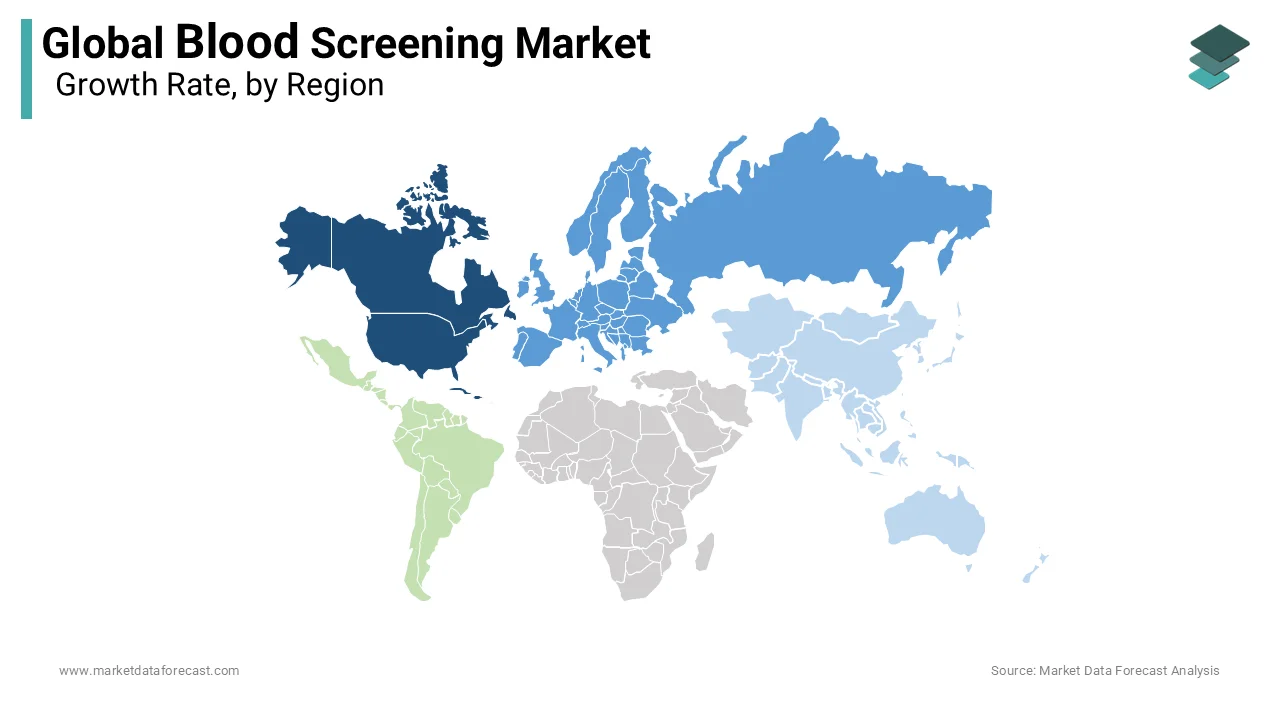

Regionally, North America accounted for the majority of the global market share in 2024 due to the existence of many key players and the acquisition of blood screening procedures. In this region, the US is expected to lead the blood screening market due to advanced technologies in using these for screening.

Europe occupies the second-largest share in the blood screening market over the analysis period due to factors like the growing number of steps taken by the government and other organizations in blood donations, screening & transfusion activities over different countries. Germany is projected to hold the largest share in the blood screening market. It is estimated to maintain its position over the period due to growth in awareness about blood donation in the country of this region.

At the same time, Asia-Pacific is expected to have a quick and fast growth rate in the blood screening market over the analysis period. The market growth owes to the growing number of blood donations, a moderate increase of new pathogens, and a great appearance of high-quality infrastructure towards clinical and hospital laboratories in the blood screening market during the period. China, Japan, and India are significant contributors to the blood screening market due to the increasing concentration of key players in existing countries.

The blood screening market of the Latin America region is considered to have stable and steady growth over the period, which owes to government initiatives in bringing awareness among the people. Growing awareness about the safety of the blood bolsters market growth of this region. Mexico is leading the market and continues its dominance over the period, followed by Brazil and Argentina.

The blood screening market of the Middle East & Africa region is projected to have a slow and least share due to the growing number of blood donations. Also, factors like cost, strict government regulations for the product approval of new screening devices may hamper the blood screening market growth during the forecast period. Therefore, UAE, Africa, GCC, KSA, and other countries majorly contribute to the market.

KEY MARKET PLAYERS

The most promising companies dominating the Global Screening Market profiled in this report are Becton, Dickinson and Company, Thermo Fisher Scientific Inc., Ortho Clinical Diagnostics, Danaher Corporation, Abbott Laboratories, Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd, Grifols, Siemens AG, and Beckman Coulter, Inc.

RECENT HAPPENINGS IN THE MARKET

-

Grifols develop a product called procleix Babesia Assay for screening donors in the Procleix panther system. FDA approved this product in Feb 2023.

-

Siemens Healthneers wholly acquired Epocal Inc. in 2017 to expand its blood gas portfolio.

- In Jan 2018, Bio-Rad Laboratories Inc. received approval from the FDA for implementing IH-centrifuge L and IH-incubator L instruments in manual blood typing methods.

MARKET SEGMENTATION

This research report on the global blood screening market has been segmented and sub-segmented based on the technology, product, end-user, and region.

By Technology

- Nucleic Acid Amplification

- Elisa

- Rapid Test

- NGS

- Western Blotting

By Product

- Instrument

- Reagent & Kits

- Software

By End User

- Blood bank

- Hospital

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the blood screening market, and why is it important?

The blood screening market encompasses tests and technologies used to detect infectious agents and diseases in blood samples to ensure the safety of blood transfusions and donations. It is critical for reducing the risk of transfusion-transmitted infections (TTIs) and maintaining public health.

How big is the global blood screening market, and what is its expected growth?

The market size and growth projections vary, but it is typically expected to grow steadily due to increasing awareness, rising blood donation rates, and technological advancements. (Current figures can be checked for the latest data.)

Who are the key players in the blood screening market?

Major companies include Grifols S.A., Abbott Laboratories, Bio-Rad Laboratories, Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, and Ortho Clinical Diagnostics.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com