Europe Blood Screening Market Research Report By Technology, Product & End User, By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis From 2026 to 2034

Market Size, 2025

$0.68 BnMarket Estimate, 2026

$0.74 BnMarket Forecast, 2034

$1.48 BnCAGR, 2026–2034

9.1%Europe Blood Screening Market Summary

The Europe Blood Screening Market size was valued at USD 0.62 billion in 2024 and is anticipated to reach USD 1.36 billion by 2033, growing at a CAGR of 9.1% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- Europe dominated the global market with a largest share in 2024.

- Europe is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 9.1%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 0.62 billion

- 2025 Market Size: USD 0.68 billion

- 2033 Projected Market Size: USD 1.36 billion

- CAGR (2024–2033): 9.1%

- Europe: Largest market in 2024

- Europe: Fastest-growing region

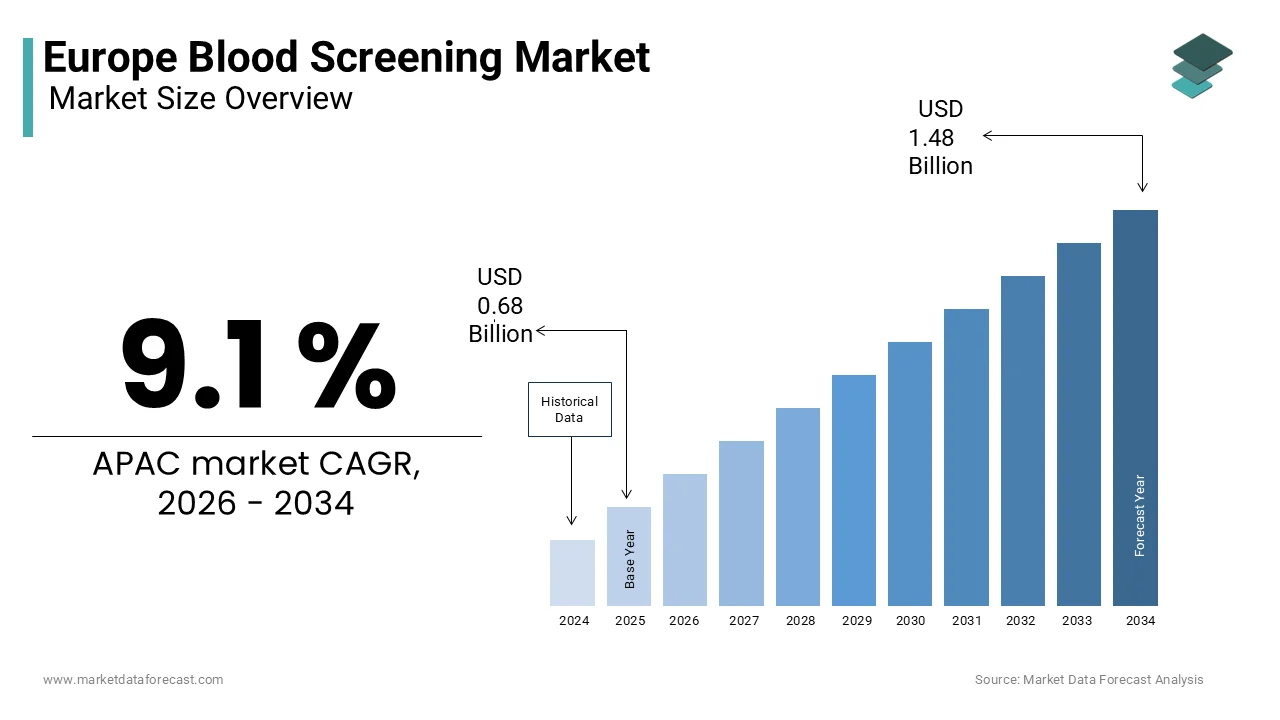

Europe Blood Screening Market Size

The europe blood screening market was valued at USD 0.68 billion in 2025, is expected to have 9.1 % CAGR from 2026 to 2034, and be worth USD 1.48 billion by 2034 from USD 0.74 billion in 2026.

The European Blood Screening Market refers to the systematic process of analyzing donated blood for infectious agents and other contaminants before it is used in transfusions or medical treatments. This market encompasses a range of diagnostic technologies and assays designed to detect pathogens such as HIV, hepatitis B and C, syphilis, and emerging threats like West Nile virus and Zika virus. Blood screening is a critical component of public health infrastructure across Europe, ensuring the safety of blood supplies and minimizing the risk of transfusion-transmitted infections.

The market includes both traditional serological testing methods and advanced molecular diagnostics such as nucleic acid testing (NAT), which has gained traction due to its ability to detect infections at earlier stages than conventional techniques.

Germany, the UK, and France lead in terms of technological adoption and regulatory framework development, while Eastern European countries are gradually upgrading their blood screening protocols under the guidance of the World Health Organization (WHO) and regional health authorities.

MARKET DRIVERS

Increasing Demand for Safe Blood Transfusions Across Healthcare Facilities

One of the primary drivers of the European Blood Screening Market is the growing requirement for safe and uncontaminated blood in hospitals, trauma centers, and specialized clinics. With an aging population and a rise in chronic diseases such as cancer and cardiovascular disorders, the number of blood transfusions conducted annually across Europe has been steadily increasing.

According to the European Blood Alliance (EBA), more than 2.3 million patients received blood transfusions in 2024 across major EU nations alone, underscoring the critical role of blood screening in preventing transfusion-related infections.

Moreover, the prevalence of infectious diseases that can be transmitted through blood including HIV, hepatitis B and C, and syphilis has necessitated stringent donor screening and laboratory testing protocols. In response, national blood services have upgraded their screening infrastructure, particularly in countries like the Netherlands and Sweden, where automated high-throughput systems are now standard.

Additionally, the European Directorate for the Quality of Medicines & HealthCare (EDQM) has reinforced regulatory standards for blood banks, mandating comprehensive screening procedures to ensure patient safety. These factors collectively drive continuous investment in advanced diagnostic tools and reagents, strengthening the overall market landscape.

Adoption of Advanced Diagnostic Technologies and Molecular Assays

A significant factor fueling growth in the EEuropeanBlood Screening Market is the increasing adoption of advanced diagnostic technologies, particularly nucleic acid testing (NAT) and next-generation sequencing (NGS) platforms. Unlike traditional immunoassays, NAT allows for the early detection of viral pathogens by identifying their genetic material, thereby reducing the window period during which infections may go undetected. According to the Paul-Ehrlich-Institut (PEI), Germany’s federal institute for vaccines and biomedicines, over 80% of blood donation centers in Germany had implemented NAT-based screening for HIV, HBV, and HCV by mid-2024, significantly improving blood safety metrics.

In addition, the integration of automation and digital diagnostics into blood screening workflows has enhanced efficiency and reduced human error in test interpretation. Countries like the UK and France have invested heavily in centralized blood testing laboratories equipped with real-time PCR and multiplex assay capabilities, allowing for simultaneous detection of multiple pathogens from a single sample. With ongoing advancements in AI-driven diagnostics and point-of-care testing, the region continues to push the boundaries of blood screening accuracy and speed.

MARKET RESTRAINTS

High Costs Associated with Advanced Screening Technologies

One of the key constraints affecting the European Blood Screening Market is the high capital and operational expenditure associated with implementing and maintaining advanced diagnostic technologies. While nucleic acid testing (NAT) and next-generation sequencing (NGS) offer superior sensitivity and faster turnaround times, they also require significant investments in equipment, trained personnel, and consumables.

In addition, ongoing expenses related to reagent procurement, software updates, and compliance with evolving regulatory requirements further strain budgets. A 2024 analysis by the European Blood Alliance (EBA) revealed that nearly 40% of blood donation centers in Eastern Europe were unable to adopt NAT due to financial limitations, leading to continued reliance on older, less sensitive immunoassay methods. This disparity in technology access creates inconsistencies in blood safety standards across the region and hampers efforts to uniformly reduce the risk of transfusion-transmitted infections.

Regulatory Complexity and Compliance Challenges

Another major restraint influencing the EEuropeanBlood Screening Market is the complexity of regulatory frameworks governing blood safety standards across different member states. While the European Union has established directives under the Blood Safety and Quality Directive (2002/98/EC), implementation varies significantly between countries due to differences in local oversight structures and enforcement mechanisms. According to the European Directorate for the Quality of Medicines & HealthCare (EDQM), harmonization of blood screening protocols remains incomplete, with discrepancies observed in testing requirements, documentation processes, and quality control measures.

This regulatory fragmentation complicates cross-border collaboration among blood banks and diagnostic service providers, limiting the potential for centralized screening hubs and standardized reporting systems. Furthermore, frequent revisions to guidelines such as those issued by the Paul-Ehrlich-Institut (PEI) in Germany and the Medicines and Healthcare products Regulatory Agency (MHRA) in the UK require constant adaptation by laboratories, increasing administrative burdens and operational delays.

MARKET OPPORTUNITIES

Expansion of Point-of-Care and Decentralized Screening Solutions

A promising opportunity in the Europe Blood Screening Market lies in the expansion of point-of-care (POC) and decentralized screening technologies that enable rapid, on-site testing of donated blood. Traditional centralized blood screening models often involve delays due to transportation and batch processing, especially in remote or underserved regions. However, advances in miniaturized diagnostic platforms and portable PCR devices have made it feasible to conduct preliminary screenings directly at collection centers or mobile donation units.

Pilot programs in Italy and Spain have demonstrated the effectiveness of such systems in expediting donor screening and reducing backlog in emergency situations.

Furthermore, the European Investment Bank (EIB) has announced funding initiatives aimed at supporting decentralized diagnostics in Eastern Europe, where infrastructure gaps persist.

Integration of Artificial Intelligence and Data Analytics in Blood Screening

An emerging opportunity shaping the European blood screening market is the integration of artificial intelligence (AI) and data analytics into diagnostic workflows to improve accuracy, efficiency, and predictive capabilities. AI-powered algorithms are increasingly being used to interpret complex test results, identify anomalies, and optimize resource allocation in blood screening laboratories.

Additionally, machine learning models are being deployed to analyze historical screening data and predict trends in infectious disease prevalence, enabling proactive adjustments to testing protocols.

Collaborations between academic institutions and diagnostic companies such as Siemens Healthineers and Roche Diagnostics are accelerating the development of AI-integrated screening platforms tailored for European markets.

MARKET CHALLENGES

Shortage of Skilled Professionals in Diagnostic Laboratories

A major challenge facing the European Blood Screening Market is the shortage of skilled professionals required to operate and maintain advanced diagnostic equipment. As blood screening technologies become more sophisticated incorporating molecular diagnostics, automation, and digital pathology there is a growing demand for trained technicians, laboratory scientists, and bioinformaticians who can interpret complex test results accurately.

This issue is exacerbated by an aging workforce and limited recruitment incentives, resulting in longer turnaround times and increased pressure on existing personnel.

To address this gap, several governments and private sector players have launched training initiatives. For example, the German Society for Clinical Chemistry and Laboratory Medicine (DGKL) partnered with universities to develop specialized certification courses in molecular diagnostics.

Emergence of Novel Pathogens and Need for Rapid Test Development

Another pressing challenge confronting the European Blood Screening Market is the unpredictable emergence of novel pathogens that require rapid development and deployment of new screening assays. Recent outbreaks of diseases such as monkeypox, avian influenza, and tick-borne encephalitis have highlighted the vulnerability of existing screening protocols to newly identified threats.

Developing reliable assays for these emerging viruses often takes months, during which time there is an elevated risk of contaminated blood entering the supply chain.

Regulatory agencies such as the European Medicines Agency (EMA) are working closely with diagnostic manufacturers to streamline approval processes for emergency-use tests. However, balancing speed with accuracy remains a challenge, particularly when dealing with low-prevalence but high-risk infections.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Product & End User, and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Becton, Dickinson and Company, Thermo Fisher Scientific Inc, Ortho Clinical Diagnostics |

SEGMENT ANALYSIS

By Technology Insights

The Nucleic Acid Amplification (NAT) segment held the largest share of theEuropeane Blood Screening Market, accounting for 42.4% of the total market value in 2024. This dominance is primarily driven by NAT’s superior ability to detect viral pathogens at an early stage, significantly reducing the window period during which infections may go undetected through conventional methods.

One of the key drivers behind NAT’s leadership is its widespread adoption across major European countries such as Germany, France, and the UK, where blood safety regulations are highly stringent. According to the Paul-Ehrlich-Institut (PEI), a significant portion of blood donation centers in Germany have fully integrated NAT-based screening for HIV, HBV, and HCV, contributing to a substantial decline in post-transfusion infection rates.

Additionally, advancements in multiplex NAT platforms allow simultaneous detection of multiple pathogens from a single sample, enhancing efficiency and cost-effectiveness.

The Next-Generation Sequencing (NGS) segment is projected to grow at the fastest rate in the EEuropeanBlood Screening Market, recording a CAGR of 14.7%. This rapid expansion is attributed to NGS's increasing role in pathogen discovery, variant tracking, and comprehensive genomic analysis capabilities that traditional screening technologies cannot match.

A primary driver of this growth is the need for more advanced surveillance mechanisms to detect emerging infectious threats such as monkeypox and new variants of hepatitis viruses.

Moreover, NGS enables retrospective analysis of stored samples, supporting epidemiological research and outbreak tracing. With regulatory support and growing investments in genomic diagnostics, NGS is expected to play a transformative role in shaping the future of blood safety in Europe.

By Product Insights

The Reagents & Kits segment commanded the EEuropeanBlood Screening Market, representing 49.5% of total product demand in 2024. This dominance is credited to the continuous requirement for consumables used in diagnostic assays such as ELISA, NAT, and rapid tests across blood banks and clinical laboratories.

One of the leading factors driving this segment’s growth is the high-frequency usage of reagents in routine screening procedures. Unlike instruments, which are capital-intensive but infrequently replaced, reagents and test kits must be replenished regularly to maintain operational continuity.

Besides, the shift toward multiplex assays capable of detecting multiple pathogens simultaneously has increased the demand for specialized reagent formulations. With ongoing innovations in assay design and regulatory emphasis on comprehensive testing, the reagents and kits segment remains central to the market’s long-term growth trajectory.

The Software segment is anticipated to register the highest growth rate in the European Blood Screening Market, with a projected CAGR of 13.2%. This surge is primarily driven by the increasing integration of digital solutions into laboratory workflow management, data analytics, and quality control processes.

A key factor fueling this growth is the rising adoption of Laboratory Information Management Systems (LIMS) and AI-powered diagnostic tools that enhance test accuracy, streamline reporting, and ensure compliance with regulatory standards.

Furthermore, software platforms are playing a crucial role in predictive analytics and real-time monitoring of contamination risks based on donor profiles and regional disease incidence. As healthcare digitization accelerates across Europe, particularly in countries like the Netherlands and Sweden, the demand for intelligent software solutions in blood screening is expected to expand rapidly.

By End User Insights

The Blood Banks segment had the dominant position in the EEuropeanBlood Screening Market, capturing an 68.1% of total end-user demand in 2024. This lead position is primarily due to the centralized role of blood banks in collecting, processing, and distributing blood units to hospitals and medical facilities, all of which require mandatory screening before use.

One of the key drivers behind this segment’s dominance is the extensive network of national blood services operating across Europe. Countries such as Germany, France, and Italy maintain well-established blood banking infrastructures, ensuring comprehensive screening coverage.

Additionally, regulatory mandates enforced by the European Directorate for the Quality of Medicines & HealthCare (EDQM) require all blood donations to undergo standardized screening using approved methodologies. These developments underscore the continued reliance on blood banks as the primary setting for blood screening activities across the region.

The Hospital segment is projected to witness the fastest growth in the European Blood Screening Market, registering a CAGR of 11.5%. This rapid expansion is driven by the increasing need for urgent, point-of-care blood testing in emergency departments, surgical units, and trauma centers where immediate transfusions are often required.

One of the key factors fueling this growth is the rising number of complex surgeries, organ transplants, and cancer treatments that necessitate real-time compatibility and infection screening. According to the UK National Health Service (NHS), emergency blood transfusions performed in hospitals rose in 2024, prompting greater investment in on-site screening capabilities.

Additionally, hospitals are increasingly adopting decentralized testing models using rapid diagnostic kits and portable NAT devices to expedite results without relying solely on central blood banks. A 2024 survey by the European Society of Clinical Microbiology and Infectious Diseases (ESCMID) found that nearly 35% of surveyed hospitals had introduced rapid HIV/HCV screening systems, enhancing patient safety in critical care settings. With growing pressure to reduce wait times and improve treatment outcomes, hospitals are becoming key contributors to the expansion of the blood screening market.

COUNTRY LEVEL ANALYSIS

Germany had the biggest share of the European Screening Market, accounting for 22.7% of the total market value in 2024. As one of the most technologically advanced healthcare markets in the region, Germany has a well-established framework for blood donation, processing, and screening, supported by robust regulatory oversight and public health initiatives.

A key driver of Germany’s leadership position is its strong commitment to blood safety, as demonstrated by the widespread implementation of nucleic acid testing (NAT) in blood banks nationwide. Additionally, the country maintains a highly organized blood supply chain managed by institutions such as the German Red Cross Blood Donor Service.

Furthermore, Germany’s investment in research and development within the diagnostics sector has led to continuous innovation in screening technologies. With strong government backing and a focus on technological advancement, Germany remains at the forefront of blood screening excellence in Europe.

The United Kingdom is maintaining a prominent position due to its advanced healthcare system and rigorous blood safety regulations. Also, the UK National Blood Service plays a pivotal role in overseeing donor screening, testing, and distribution, ensuring that all collected blood undergoes comprehensive pathogen checks before clinical use.

One of the key factors supporting the UK’s strong market presence is its early adoption of multiplex NAT technology, which allows simultaneous detection of multiple viral agents from a single sample.

Additionally, the UK government has invested in digital pathology and AI-driven diagnostics to enhance screening accuracy and efficiency. With a proactive approach to innovation and regulation, the UK continues to solidify its role as a key player in the European blood screening landscape.

France is another key player in the European Blood Screening Market, driven by its strategic emphasis on pathogen surveillance and proactive response to emerging infectious threats. The country’s blood screening infrastructure is managed by the French National Transfusion Institute (INTS), which oversees the collection, testing, and distribution of blood products nationwide.

A major factor contributing to France’s market strength is its investment in advanced molecular diagnostics, including next-generation sequencing (NGS), to detect novel and mutated pathogens.

Apart from these, France has adopted a multi-tiered screening strategy combining ELISA, NAT, and rapid tests to ensure maximum safety across different donation types. The French Ministry of Health has mandated the use of multiplex NAT assays in all major blood centers, reinforcing its commitment to minimizing transfusion risks. With strong institutional support and a forward-looking approach to diagnostic innovation, France remains a key contributor to blood safety advancements in Europe.

Italy is benefiting from recent efforts to modernize its blood donation and testing infrastructure. The country operates under a regionalized model, with autonomous blood centers managing donor recruitment and screening procedures across various provinces.

A significant driver of Italy’s market growth is the increasing deployment of decentralized screening facilities equipped with rapid diagnostic tools and automated NAT systems.

Moreover, Italy has prioritized the integration of digital diagnostics to enhance data management and traceability across the blood supply chain. These advancements are helping Italian blood banks align with EU-wide safety standards while addressing logistical challenges associated with rural and remote areas.

Spain is characterized by a well-coordinated regional blood transfusion system that ensures consistent donor screening practices across autonomous communities. The Spanish National Transfusion Organization (ONT) plays a central role in regulating blood collection, testing, and distribution policies throughout the country.

One of the key factors influencing Spain’s market performance is the implementation of centralized NAT screening hubs, which serve multiple regions and improve cost-efficiency. Besides, Spain has been actively involved in EU-funded projects aimed at improving cross-border blood exchange and harmonizing screening protocols. With continued investment in technology and inter-regional coordination, Spain is strengthening its position in the European blood screening ecosystem.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Prominent Companies dominating the European Blood Screening Market Profiled in the Report are Becton, Dickinson and Company, Thermo Fisher Scientific Inc, Ortho Clinical Diagnostics, Danaher Corporation, Abbott Laboratories, Bio-Rad Laboratories, Inc, F. Hoffmann-La Roche Ltd, Grifols, Siemens AG, and Beckman Coulter, Inc.

The competition in the European Blood Screening Market is marked by a dynamic mix of established diagnostics giants and emerging biotech firms striving to offer superior screening solutions amid rising demand for safe blood products. The market is highly consolidated, with dominant players like Roche, Grifols, and Bio-Rad maintaining strong footholds due to their extensive product portfolios, technological expertise, and well-established distribution networks. However, increasing investments in research and development have allowed newer entrants to challenge traditional leaders by introducing cost-effective, faster, and more sensitive screening methods.

A key battleground among competitors is the race to develop integrated diagnostic platforms that combine automation, digital reporting, and real-time analytics to meet the growing expectations of blood banks and hospital labs. Regulatory alignment across European countries presents both opportunities and challenges, as companies must navigate varying national requirements while aiming for pan-European scalability. Additionally, the push for decentralized and point-of-care screening solutions is reshaping competitive strategies, encouraging firms to diversify beyond conventional instruments and reagents into software-enabled diagnostics and cloud-based monitoring systems. With blood safety remaining a top healthcare priority, the intensity of competition is expected to rise further as companies strive to deliver cutting-edge innovations that redefine screening standards.

Top Players in the Market

Grifols (Spain)

Grifols is a leading global player in the blood screening and plasma-derived therapeutics sector. The company plays a crucial role in supplying diagnostic reagents, NAT-based assays, and automated testing systems to European blood banks and hospitals. Grifols contributes significantly to global blood safety by offering comprehensive screening solutions that detect infectious agents such as HIV, hepatitis, and emerging pathogens.

F. Hoffmann-La Roche Ltd (Switzerland)

Roche Diagnostics is a key participant in the European Blood Screening Market, known for its advanced molecular diagnostics platforms. The company provides high-throughput NAT systems and immunoassays that are widely adopted across national blood services. Roche’s innovative technologies enhance early pathogen detection and support regulatory compliance, reinforcing its leadership in the global blood screening industry.

Bio-Rad Laboratories (USA, witha strong presence in Europe)

Bio-Rad has a significant footprint in the European market through its portfolio of immunodiagnostic tests and automation solutions for blood screening. The company supports blood banks and clinical laboratories with reliable ELISA and rapid test kits, ensuring accurate and efficient donor screening. Bio-Rad's commitment to quality and innovation continues to strengthen its position in Europe’s competitive diagnostics landscape.

Top Strategies Used by Key Market Participants

One major strategy employed by key players in the European Blood Screening Market is continuous innovation in molecular diagnostics, particularly in nucleic acid testing (NAT) and next-generation sequencing (NGS). Companies are investing heavily in R&D to develop multiplex assays that allow simultaneous detection of multiple pathogens, enhancing both efficiency and accuracy in blood screening processes.

Another strategic approach is expanding partnerships with public health institutions and national blood agencies. Collaborations enable companies to align their product development with evolving regulatory standards while also securing long-term supply contracts. These alliances help manufacturers gain deeper market penetration and ensure widespread adoption of their diagnostic solutions across regional healthcare networks.

Lastly, digital transformation and integration of AI-driven analytics into blood screening workflows isareecoming a priority. Major players are incorporating software tools that streamline laboratory operations, improve data traceability, and support predictive risk modeling, thereby strengthening their value proposition in an increasingly technology-driven healthcare environment.

RECENT HAPPENINGS IN THE MARKET

In March 2024, Grifols launched a new generation of NAT-based blood screening kits designed to detect emerging viral mutations, enhancing pathogen surveillance capabilities across European blood banks.

In June 2024, Roche Diagnostics partnered with the French National Transfusion Institute to implement AI-integrated diagnostic dashboards aimed at improving donor risk profiling and contamination tracking.

In October 2024, Bio-Rad introduced a fully automated ELISA system tailored for high-volume blood screening centers, streamlining workflow efficiency and reducing manual intervention in test processing.

In January 2024, Qiagen expanded its molecular diagnostics offerings in Germany by launching a portable NAT device for use in mobile blood donation units, supporting rapid on-site screening.

In August 2024, DiaSorin announced the acquisition of a biotech startup specializing in microarray-based multipathogen detection, strengthening its position in the European blood screening diagnostics space.

MARKET SEGMENTATION

This research report on the europe blood screening market has been segmented and sub-segmented into the following categories.

By Technology

- Nucleic Acid Amplification (NAT)

- Next-Generation Sequencing (NGS)

By Product

- Reagent & Kits

- Software

By End User

- Blood banks

- Hospital

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the major drivers of the Europe Blood Screening Market?

Key drivers include rising demand for safe blood transfusions, growing prevalence of infectious diseases (like HIV, HBV, and HCV), advancements in screening technologies, and government initiatives for blood safety.

What is the Europe Blood Screening Market?

The Europe Blood Screening Market involves the testing of donated blood for infectious diseases to ensure its safety before transfusion or use in medical treatments.

Who are the key players in the European blood screening market?

Leading companies include Grifols, Roche Diagnostics, Abbott Laboratories, Bio-Rad Laboratories, and Thermo Fisher Scientific.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com