Global Boat and Yacht Transportation Market Size, Share, Trends & Growth Forecast Report – Segmented By Vessel Type (Superyachts, Small and Medium Recreational Boats), Service Type, And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Global Boat and Yacht Transportation Market Report Summary

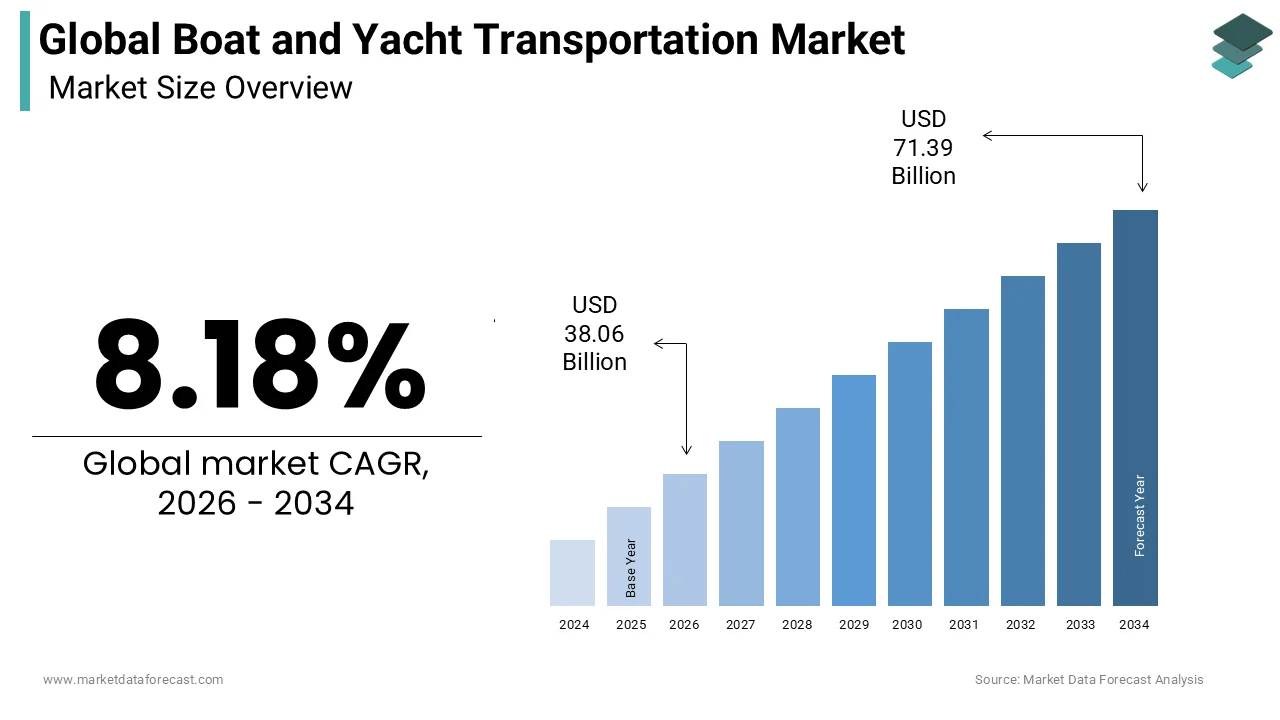

The global Boat and Yacht Transportation Market was valued at USD 35.18 billion in 2025 and is projected to reach USD 71.39 billion by 2034, growing from USD 38.06 billion in 2026 at a CAGR of 8.18% during the forecast period. Market growth is driven by increasing international yacht ownership, rising cross-border marine tourism, growing participation in global boating events, and expanding demand for specialized marine logistics services. Advancements in heavy-lift shipping technologies, digital logistics platforms, and customized transportation solutions are further supporting market expansion.

Key Market Trends

- Rising demand for international yacht relocation and transport services

- Increasing use of heavy-lift and semi-submersible transport vessels

- Growth in luxury yacht ownership and global marine tourism

- Expansion of digital logistics tracking and fleet management solutions

- Increasing demand for specialized transport of oversized and high-value vessels

Segmental Insights

- Based on Vessel Type, the superyachts segment dominated the global boat and yacht transportation market in 2025 by accounting for the largest share of the market. Growth is driven by the increasing number of luxury yacht owners requiring specialized transport, higher vessel values, and demand for secure long-distance shipping services.

- Based on Service Type, the heavy-lift and semi-submersible shipping services segment held the leading share of the market in 2025, supported by its capability to safely transport large yachts over long distances while minimizing operational risks and fuel consumption.

Regional Insights

- Europe dominated the global boat and yacht transportation market by accounting for 34.5% of the market share in 2025. The region's leadership is supported by its large concentration of yacht owners, well-established marinas, leading yacht manufacturers, and strong marine logistics infrastructure.

- North America is expected to maintain steady market growth due to high yacht ownership rates, expanding recreational boating activities, and well-developed marine transportation networks.

- Asia-Pacific is projected to witness the fastest growth over the forecast period, driven by rising luxury spending, expanding marina infrastructure, and increasing demand for yacht transportation services across emerging economies.

- Latin America is expected to experience moderate market expansion, supported by growing marine tourism, improving port infrastructure, and increasing recreational boating activities.

- Middle East and Africa are expected to maintain strategic importance in the market due to their luxury yacht destinations, expanding marina developments, and increasing demand for premium yacht logistics services.

Competitive Landscape

The global boat and yacht transportation market is highly competitive, with companies focusing on specialized marine logistics, secure vessel handling, digital shipment tracking, and customized transportation solutions. Market participants are investing in heavy-lift vessels, advanced logistics technologies, and global transportation networks to strengthen their market positions.

Key players operating in the global boat and yacht transportation market include Sevenstar Yacht Transport, Peters & May, DYT Yacht Transport, Dockwise Yacht Transport, Yacht Path, GAC Group, Compass Logistics International, Able Boat Transport, Joule Yacht Transport, Associated Boat Transport, uShip, Total Quality Logistics, A1 Auto Transport, Horizon Yacht Charters, and Coast to Coast Boat Transport.

Global Boat and Yacht Transportation Market Size

The global boat and yacht transportation market size was calculated at USD 35.18 billion in 2025 and is anticipated to reach USD 71.39 billion by 2034, from USD 38.06 billion in 2026, growing at a CAGR of 8.18% during the forecast period.

Boat and yacht transportation includes specialized logistics services dedicated to the maritime relocation of recreational vessels, luxury yachts, and commercial boats across domestic and international waters. This sector utilizes heavy-lift ships, semi-submersible carriers, and float-on/float-off vessels to transport watercraft that cannot or should not navigate long distances under their own power. The industry serves high-net-worth individuals, charter companies, and boat manufacturers requiring safe and efficient delivery solutions. According to the National Marine Manufacturers Association, the United States recreational boating industry recorded approximately 262,000 new powerboat sales in 2024, creating a substantial base for subsequent transportation needs as owners relocate or upgrade vessels. As per the Mediterranean Yacht Brokers Association, the Mediterranean region hosts approximately 45% of the global superyacht fleet, necessitating robust seasonal transportation networks between winter storage locations in the Caribbean or Florida and summer cruising grounds in Europe. As per the International Maritime Organization, strict regulations govern the stowage and securing of cargo on deck, directly influencing operational protocols for yacht carriers. The complexity of transporting oversized assets requires specialized port infrastructure capable of handling extreme dimensions and weights. Insurance providers mandate rigorous risk assessment procedures for marine transit, affecting service pricing and availability. The market operates within a niche segment of global logistics where precision timing and damage prevention are paramount due to the high value of the cargo. Seasonal migration patterns drive demand peaks, requiring flexible capacity management from service providers. Technological advancements in vessel tracking and condition monitoring enhance transparency for clients during transit.

MARKET DRIVERS

Rising Global Wealth Concentration Drives Luxury Asset Mobility

The accumulation of wealth among high-net-worth individuals globally is promoting the growth of the boat and yacht transportation market. Affluent consumers increasingly view luxury yachts as essential lifestyle assets rather than mere leisure items, leading to higher ownership rates and more frequent international movement. According to the Knight Frank Wealth Report, the number of ultra-high net worth individuals worldwide increased by 4.2% in 2024, reaching record levels that correlate strongly with luxury asset acquisition. These individuals often maintain multiple residences in different climatic zones, necessitating the seasonal relocation of their vessels to optimize usage throughout the year. According to the Superyacht Times, the global superyacht order book remains robust with over 600 vessels under construction, indicating sustained future demand for delivery and repositioning services. Owners prefer professional transportation over self-navigation to avoid wear and tear on engines and hulls, preserve crew rest periods, and mitigate navigation risks in unfamiliar waters. The trend toward larger vessels exceeding 50 meters in length further drives demand for specialized heavy lift capabilities that standard marinas cannot accommodate. As per Credit Suisse global wealth data, the top 1% of the population holds nearly 45% of global wealth, providing a stable customer base for premium logistics services. This demographic prioritizes convenience and security, willing to pay premiums for insured, door-to-door transportation solutions that ensure their assets arrive in pristine condition. The globalization of luxury lifestyles means yachts are no longer confined to home ports but circulate globally among exclusive destinations.

Expansion of International Boat Shows and Events Boosts Logistics Demand

The proliferation of international boat shows and marine exhibitions creates significant periodic demand for specialized transportation services within the boat and yacht transportation market. Major events such as the Monaco Yacht Show, Fort Lauderdale International Boat Show, and Dubai International Boat Show attract thousands of vessels annually, requiring complex logistical coordination for arrival and departure. According to the Monaco Yacht Show organizers, the event features over 120 superyachts each year, many of which are transported specifically for display and potential sale. These events serve as critical sales channels for brokers and manufacturers, making timely and damage-free delivery essential for commercial success. The Fort Lauderdale International Boat Show reported attendance exceeding 100,000 visitors and showcasing hundreds of millions of dollars in marine assets, highlighting the scale of logistical operations required. Transportation providers must coordinate tight schedules to ensure vessels arrive before exhibition deadlines and depart efficiently afterward to avoid costly marina berthing fees. As per the International Boatbuilders Association, participation in multiple shows per season is common for new models, creating recurring transportation contracts. The need for precise handling during loading and unloading at crowded show ports demands highly skilled stevedores and specialized equipment. Insurance requirements for show participation often mandate professional transit rather than owner-operated delivery to minimize liability. The growth of regional boat shows in emerging markets such as Asia and the Middle East further expands the geographic scope of transportation needs. This event-driven demand provides steady revenue streams for logistics companies during peak seasons.

MARKET RESTRAINTS

High Operational Costs and Fuel Price Volatility Restrict Market Growth

The boat and yacht transportation market faces significant restraint from high operational costs associated with specialized vessels and volatile fuel prices, which impact profitability and service pricing. Heavy-lift ships and semi-submersible carriers consume substantial amounts of marine fuel, making them highly sensitive to fluctuations in global oil prices. According to the International Energy Agency, marine bunker fuel prices have remained subject to significant volatility, with average costs fluctuating by over 20% in recent market cycles, increasing operational expenses for shipping companies during peak periods. These costs are often passed on to clients through surcharges, potentially dampening demand among price-sensitive segments of the market. The specialized nature of yacht transport vessels means they have higher maintenance and crewing costs compared to standard cargo ships due to the need for precise handling equipment and experienced personnel. As per the Baltic and International Maritime Council, bunker fuel accounts for a major portion of voyage costs, and sudden price spikes can render certain routes economically unviable without significant rate adjustments. Additionally, the limited number of specialized carriers creates an inelastic supply side, preventing rapid capacity expansion to meet demand spikes. Port fees for handling oversized cargo are also substantially higher than standard container rates, which are adding to the total cost of transportation. Economic downturns may lead owners to defer non-essential relocations or choose cheaper self-navigation options, reducing market volume. The capital-intensive nature of acquiring new heavy-lift vessels further limits market entry and expansion capabilities for smaller operators.

Stringent Environmental Regulations Increase Compliance Burdens

Increasingly rigorous environmental regulations imposed by international maritime bodies act as a major restraint on the boat and yacht transportation market by mandating costly upgrades and operational changes. The International Maritime Organization has implemented stricter emissions standards, including the Carbon Intensity Indicator and Energy Efficiency Existing Ship Index, which require vessels to reduce their carbon footprint significantly. According to the International Chamber of Shipping, initial compliance with these regulations requires investment in new technologies, which can increase capital expenditure by up to 25% for older vessel retrofitting. For specialized yacht carriers, finding compliant fuel sources or retrofitting vessels can be technically challenging and expensive due to their unique design configurations. The European Union Emissions Trading System now includes maritime transport, imposing carbon costs on voyages involving European ports, which increase operational expenses. As per the European Commission, these measures aim to reduce greenhouse gas emissions by 55% by 2030, forcing logistics providers to rethink route planning and vessel utilization. Smaller transportation companies may struggle to absorb these compliance costs, leading to market consolidation or exit. The transition to low-sulfur fuels also affects engine performance and maintenance schedules, requiring additional technical expertise. Regulatory uncertainty regarding future fuel standards creates hesitation in long-term investment decisions for new vessel construction. Clients may face higher rates as providers seek to recover compliance investments, potentially reducing demand for discretionary transportation services. The administrative burden of reporting and verifying emissions data adds complexity to operational workflows.

MARKET OPPORTUNITIES

Integration of Digital Tracking and Monitoring Technologies Offers Efficiency Gains

The adoption of advanced digital tracking and condition monitoring technologies presents a significant opportunity for the boat and yacht transportation market to enhance service quality and operational efficiency. Internet of Things sensors installed on transported vessels can provide real-time data on location, humidity, temperature, and structural stress during transit. According to the International Maritime Organization, digitalization in shipping can improve operational efficiency by up to 20% through optimized routing and predictive maintenance. For high-value yachts, owners demand transparency and assurance that their assets are monitored continuously, creating a competitive advantage for providers offering such services. Blockchain technology can streamline documentation and customs clearance processes, reducing delays at international borders. As per the World Customs Organization, digital trade facilitation measures can reduce document processing times by up to 50% for high-value goods. Transportation companies can use data analytics to predict maintenance needs for their carrier vessels, minimizing downtime and improving reliability. Mobile applications allow clients to track their vessels in real time, enhancing customer experience and trust. The integration of artificial intelligence for route optimization can reduce fuel consumption and transit times, lowering operational costs. Smart contracts can automate insurance claims and payments based on verified sensor data, speeding up resolution processes. These technological advancements enable providers to differentiate themselves in a niche market where service quality is paramount. The ability to offer detailed post-transit reports on vessel condition adds value for insurance purposes and owner peace of mind.

Expansion into Emerging Markets Creates New Revenue Streams

The growing interest in yachting and recreational boating in emerging markets such as the Asia Pacific and the Middle East offers substantial opportunities for expansion in the boat and yacht transportation sector. Countries like China, Singapore, and the United Arab Emirates are witnessing rising wealth levels and increasing participation in luxury marine activities. According to the China Ministry of Transport, the number of registered recreational vessels in China has grown at a compound annual rate of approximately 5% to 8% in recent years, driven by government initiatives to develop coastal tourism infrastructure. The Dubai Maritime City Authority reports significant investment in marina development and yachting facilities, attracting international owners and events. These regions often lack local manufacturing capabilities for large yachts, necessitating importation and transportation from established shipbuilding hubs in Europe and North America. As per the Singapore Tourism Board, the city-state maintains its status as a premier yachting hub in Asia, driving demand for repositioning services. Transportation providers can establish regional hubs or partnerships to serve these growing markets more effectively. The development of new marinas and boat shows in these regions creates localized demand for logistics support. Government policies promoting tourism and luxury consumption support market growth. Early entrants into these markets can establish strong brand recognition and customer loyalty before competition intensifies. The cultural shift toward outdoor and marine leisure activities in these economies ensures long-term demand potential. Providers offering tailored services for local regulatory requirements and cultural preferences will gain competitive advantages.

MARKET CHALLENGES

Complexity of International Customs and Regulatory Compliance Poses Operational Challenges

The boat and yacht transportation market faces significant challenges related to the complexity of international customs regulations and varying national compliance requirements. Each country has distinct rules regarding the temporary importation of vessels, tax exemptions, and documentation, which can cause significant delays if not managed correctly. According to the World Customs Organization, inconsistent application of customs procedures across different jurisdictions creates uncertainty for logistics providers and owners, leading to potential port clearance delays of up to 10 days in some regions. Misclassification of vessels or incomplete paperwork can result in hefty fines, detention of assets, or forced exportation. The Hague Conference on Private International Law notes that legal frameworks for maritime transport vary widely, complicating liability and dispute resolution processes. Transportation providers must maintain extensive legal expertise and local agents in every port of call to navigate these complexities. As per the International Yacht Bureau, changes in tax laws, such as Value Added Tax or import duties, can occur with little notice, affecting cost calculations and client budgets. The temporary admission regime for yachts allows duty-free entry for limited periods but requires strict adherence to time limits and usage restrictions. Violations can lead to severe financial penalties and legal complications for owners. The lack of harmonized international standards for recreational vessel transport means providers must adapt to diverse local practices. This administrative burden increases operational costs and requires meticulous planning to avoid disruptions. Clients often underestimate these complexities, leading to friction and dissatisfaction when delays occur.

Vulnerability to Weather Conditions and Natural Disasters Affects Reliability

The boat and yacht transportation market is inherently vulnerable to adverse weather conditions and natural disasters, which can disrupt schedules and pose risks to cargo safety. Marine transportation relies heavily on favorable sea states for loading and unloading operations, particularly for float-on/float-off methods, which require calm waters. According to the World Meteorological Organization, the frequency of extreme weather events has increased, with data indicating a 15% rise in major storm intensity over the last decade, affecting shipping routes and port operations. Hurricanes, typhoons, and severe storms can force carriers to alter routes, delay departures, or seek shelter, leading to significant schedule disruptions. As per the National Oceanic and Atmospheric Administration, hurricane seasons in the Atlantic and Pacific coincide with peak yachting migration periods, creating logistical conflicts. Damage to port infrastructure from natural disasters can halt operations entirely, leaving vessels stranded or inaccessible. Insurance coverage for weather-related delays is often limited or excluded, placing financial risk on owners and providers. The sensitivity of high-value yachts to saltwater exposure and physical stress during rough seas requires careful route planning and weather routing services. Climate change projections indicate increasing unpredictability in weather patterns, making long-term scheduling more difficult. Providers must invest in advanced meteorological data and flexible contingency planning to mitigate these risks. Communication with clients during disruptions is critical to maintaining trust, but can be challenging when situations evolve rapidly. The inability to guarantee exact arrival dates due to weather factors remains a persistent challenge in managing client expectations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.18% |

| Segments Covered | By Type, Service Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, the Middle East and Africa, And Latin America |

| Market Leaders Profiled | Sevenstar Yacht Transport, Peters & May, DYT Yacht Transport, Dockwise Yacht Transport, Yacht Path, GAC Group, Compass Logistics International, Able Boat Transport, Joule Yacht Transport, Associated Boat Transport, uShip, Total Quality Logistics (TQL), A1 Auto Transport, Horizon Yacht Charters, and Coast to Coast Boat Transport. |

SEGMENTAL ANALYSIS

By Vessel Type Insights

The superyachts segment was the leading segment in the boat and yacht transportation market and had the leading share of the global market in 2025 due to their extreme dimensions, high asset worth, and specialized handling requirements. These vessels typically exceed 24 meters in length and often require heavy lift ships or semi-submersible carriers for transport, as they cannot safely navigate long ocean passages under their own power without significant fuel consumption and wear. According to the Superyacht Times, there are over 5,500 superyachts globally, with an average value exceeding 10 million dollars, creating a high-stakes logistics environment where damage prevention is paramount. The complexity of transporting these assets involves intricate engineering assessments to determine load-bearing points and securement strategies that prevent structural stress during transit. As per the International Yacht Bureau, insurance premiums for superyacht transportation are significantly higher than standard vessels, driving owners to select premium logistics providers with proven track records. The seasonal migration of superyachts between the Mediterranean and the Caribbean generates consistent demand for dedicated carrier services. Owners of these vessels prioritize speed and security over cost, allowing service providers to command higher margins. The increasing size of new builds, with many exceeding 80 meters, further necessitates specialized infrastructure at ports and on carrier vessels. This segment drives innovation in lifting technology and stowage optimization as manufacturers push the boundaries of yacht design. The exclusivity of this market means that relationships and reputation are critical factors in securing contracts.

On the other side, the small to medium recreational boats segment is the highest volume segment in the transportation market and is predicted to grow at a promising CAGR in the global market over the forecast period, owing to the widespread ownership of vessels ranging from 6 to 24 meters. These boats are frequently transported via road trailers for domestic moves or via containerized and roll-on/roll-off services for international relocation. According to the National Marine Manufacturers Association, millions of small recreational boats are sold annually in North America and Europe, creating a vast aftermarket for relocation services when owners move residences or sell vessels. The affordability of these vessels makes owners more price sensitive, leading to a competitive landscape among logistics providers offering consolidated shipping options. As per the BoatUS Foundation, a significant portion of boat owners relocate every five to seven years, generating steady demand for domestic transportation services. The standardization of trailer sizes and hull shapes allows for efficient stacking and transport on multi-vehicle carriers, reducing per-unit costs. This segment is highly influenced by seasonal weather patterns, with peak transportation periods occurring in spring and autumn as boats are moved to and from storage facilities. The rise of online boat sales platforms has increased cross-border transactions, requiring streamlined customs and documentation services for smaller vessels. Providers in this segment focus on operational efficiency and network coverage to capture market share.

By Service Type Insights

The heavy lift and semi-submersible shipping services segment led the market by accounting for the major share of the global market in 2025 due to their ability to handle oversized and high-value assets with minimal risk. These vessels allow yachts to be loaded directly onto the deck or into the hold, avoiding the stresses of crane lifting and providing superior stability during transit. According to the Baltic and International Maritime Council, the global heavy lift fleet includes specialized units capable of carrying multiple superyachts simultaneously, optimizing capacity utilization. Semi-submersible ships can flood their decks to allow yachts to float on, a method that significantly reduces the risk of damage during loading and unloading operations. As per the International Maritime Organization, this method is preferred for vessels exceeding 40 meters where crane capacity may be limited or risky. The ability to transport multiple high-value units on a single voyage allows providers to offer competitive rates while maintaining high service standards. This segment requires significant capital investment in specialized vessels and port infrastructure, creating high barriers to entry. The reliability and safety record of heavy lift shipping make it the preferred choice for insurance companies and wealthy owners. Seasonal scheduling is critical, with carriers planning routes months in advance to align with yachting seasons in key regions.

However, the road transportation segment is estimated to register the fastest CAGR in the global market during the forecast period and serves as the primary method for domestic and short-distance international movement of boats and yachts, particularly for vessels under 20 meters. This segment is characterized by a fragmented network of specialized trucking companies equipped with low loaders and hydraulic trailers capable of handling wide and heavy loads. According to the American Trucking Associations, the oversize load transportation sector handles thousands of boat movements annually within the United States alone, facilitated by an extensive highway network. Road transport offers door-to-door convenience, eliminating the need for port handling and reducing transit times for inland destinations. As per the European Commission, cross-border road transport of recreational vessels within the EU is streamlined by uniform regulations, fostering a robust market for international trucking services. This segment is highly sensitive to fuel prices and regulatory changes regarding axle weights and driver hours. The flexibility of road transport allows for last-minute schedule adjustments, making it ideal for urgent deliveries or show preparations. Permit acquisition for oversize loads is a critical operational component, requiring expertise in local traffic laws. The growth of e-commerce and online boat sales has increased demand for reliable road transport services that can provide real-time tracking and guaranteed delivery windows.

REGIONAL ANALYSIS

Europe Boat and Yacht Transportation Market Analysis

Europe had 34.5% of the global market share in 2025 and is expected to maintain its dominant position in the boat and yacht transportation market over the next few years due to its robust maritime heritage and mature infrastructure. The Mediterranean Sea serves as the world’s premier yachting destination, attracting fleets from around the globe during the summer season. According to the Mediterranean Yacht Brokers Association, the region hosts nearly 45% of the global superyacht fleet, creating intense demand for seasonal repositioning services between winter and summer bases. Major hubs in France, Italy, Spain, and Monaco facilitate complex logistics operations involving heavy lift ships and road transport. As per the European Boating Industry, the region has over 6 million recreational boats, generating substantial domestic transportation needs. The well-developed marina network and specialized shipyards support high-value maintenance and refit activities, further driving transport demand. Regulatory harmonization within the European Union simplifies cross-border movements, although Brexit has introduced new complexities for UK-based operators. The region is also a leader in adopting environmental standards for maritime transport, influencing operational practices. High-net-worth individuals in Europe frequently own multiple vessels, necessitating regular transportation for usage and storage. The presence of major boat shows in Cannes, Genoa, and Monaco sustains periodic spikes in logistics activity. Established logistics providers in Europe benefit from longstanding relationships with brokers and yards.

North America Boat and Yacht Transportation Market Analysis

North America is poised to continue its steady growth pattern as a high-volume logistics hub for the next few years. The United States dominates regional demand, with high levels of boat ownership in states such as Florida, California, and New York. According to the National Marine Manufacturers Association, the US recreational boating industry generates billions in annual economic impact, supporting a robust transportation infrastructure. The Great Lakes region also contributes significantly to seasonal transportation needs as boats are moved for winter storage. As per the US Coast Guard, there are over 11 million registered recreational vessels in the United States, creating a massive aftermarket for road and marine transport services. The popularity of large motor yachts in Florida drives demand for heavy lift services to and from the Caribbean. Cross-border transportation between the US, Canada, and Mexico is facilitated by trade agreements but requires careful customs management. The region faces challenges related to infrastructure aging and regulatory variations between states. High fuel costs and driver shortages impact road transportation efficiency. The market is highly competitive with numerous local and national providers. Growing interest in sustainable boating practices is influencing transportation choices, with some owners opting for slower, more fuel-efficient marine transport over road haulage.

Asia Pacific Boat and Yacht Transportation Market Analysis

Asia Pacific is anticipated to emerge as the most dynamic region for yacht transportation logistics over the next few years as infrastructure investment continues to rise. China, Singapore, Australia, and Thailand are key markets experiencing increased adoption of luxury yachting. According to the China Maritime Safety Administration, the number of registered recreational vessels is growing steadily as coastal tourism develops. Singapore serves as a major hub for superyacht transit and storage, benefiting from its strategic location and world-class port facilities. As per the Singapore Tourism Board, government initiatives to promote marine tourism are attracting international events and owners. Australia has a strong recreational boating culture with significant seasonal movement of vessels along its extensive coastline. The region lacks the mature infrastructure of Europe and North America, creating opportunities for investment in marinas and transport services. Local manufacturing of boats is increasing, driving demand for domestic distribution networks. Regulatory frameworks are evolving to accommodate growing marine leisure activities. Cultural acceptance of yachting as a status symbol is expanding the customer base beyond traditional expatriate communities. Logistics providers are establishing regional partnerships to handle complex cross-border movements. The monsoon season affects operational schedules, requiring flexible planning. Growth in middle-class wealth supports expansion in the small to medium boat segment.

Latin America Boat and Yacht Transportation Market Analysis

Latin America is projected to see moderate expansion in its yacht transportation sector over the next few years as tourism infrastructure investments mature. Brazil has a vibrant yachting community centered in Rio de Janeiro and São Paulo, driving demand for domestic and international transport. According to the Brazilian Yacht Club, membership and boat ownership have increased among the affluent population. Mexico benefits from its proximity to the United States, serving as a popular winter destination for American boat owners who require transportation services. As per the Mexican Ministry of Tourism, marine tourism is a priority sector, with investment in marinas and infrastructure. The Caribbean islands associated with Latin America serve as key stops for superyacht itineraries, generating transit demand. Economic volatility in some countries affects market stability, but high-net-worth segments remain resilient. Local logistics providers often partner with international firms to handle complex imports and exports. Regulatory hurdles and customs inefficiencies can delay operations, requiring experienced local agents. The region offers potential for growth as infrastructure improves and political stability enhances investor confidence. Road transportation is limited by geography, making marine transport more critical. Seasonal hurricanes impact scheduling and insurance costs.

Middle East and Africa Boat and Yacht Transportation Market Analysis

The Middle East and Africa region is expected to maintain its strategic importance for high-end yacht logistics over the next few years due to the ongoing development of luxury marine destinations, with the United Arab Emirates and South Africa serving as primary hubs. Dubai has emerged as a global center for superyacht activity, hosting major shows and attracting international owners. According to the Dubai Maritime City Authority, significant investment in marina infrastructure supports the growing fleet. The region serves as a winter destination for European yachts, driving seasonal transportation demand. South Africa has a well-established recreational boating sector with Cape Town serving as a key stopover for global circumnavigations. As per the South African Maritime Safety Authority, regulatory frameworks support safe and efficient marine operations. The rest of Africa has limited infrastructure but potential for growth in coastal tourism destinations. Political instability in certain areas poses risks to logistics operations. High temperatures and harsh marine environments require specialized maintenance and transport considerations. The market is dominated by high-value superyacht movements rather than volume recreational boating. Local providers specialize in high-touch, personalized services for affluent clients. Government visions for tourism diversification support market development. Connectivity to global shipping lanes facilitates efficient repositioning.

COMPETITION OVERVIEW

The boat and yacht transportation market features moderate competition among specialized logistics providers and general heavy lift shipping companies vying for high-value contracts. Market participants differentiate themselves through service quality, safety records, and specialized expertise in handling delicate marine assets. High barriers to entry due to the capital-intensive nature of specialized vessels and the need for technical expertise limit new competitors but encourage continuous improvement among existing players. Companies compete based on reliability, transparency, and customer service rather than price alone, given the high value of the cargo. Technological adoption varies across competitors, with leaders investing in digital tracking and condition monitoring systems to enhance client experience. Service quality, including careful handling and timely delivery, serves as a key differentiator in securing repeat business from wealthy owners and brokers. Geographic reach determines the ability to serve clients requiring global repositioning services between major yachting hubs. Regulatory compliance capabilities also distinguish competitors as adherence to varying international customs and safety standards becomes increasingly complex. The niche nature of the market fosters long-term relationships and loyalty among clients who prioritize trust and security. Collaboration among providers for shared capacity during peak seasons coexists with competition for exclusive contracts. Reputation management is critical as negative incidents can severely damage brand equity in this tight-knit community.

KEY MARKET PLAYERS

A few major players of the global boat and yacht transportation market include

- Sevenstar Yacht Transport

- Peters & May

- DYT Yacht Transport

- Dockwise Yacht Transport

- Yacht Path

- GAC Group

- Compass Logistics International

- Able Boat Transport

- Joule Yacht Transport

- Associated Boat Transport

- uShip

- Total Quality Logistics (TQL)

- A1 Auto Transport

- Horizon Yacht Charters

- Coast to Coast Boat Transport

Top Strategies Used by Key Market Participants

Key players in the boat and yacht transportation market employ several strategic approaches to maintain competitive advantages and drive growth. Service differentiation remains a primary strategy as companies develop specialized handling protocols and premium concierge services to attract high-net-worth clients. Strategic partnerships with marinas, shipyards, and insurance providers facilitate integrated solutions that simplify the logistics process for owners. Geographic expansion into emerging markets allows participants to capture growth opportunities in regions with rising wealth and yachting interest. Investment in digital technologies, such as real-time tracking and automated documentation, enhances operational efficiency and customer transparency. Focus on sustainability drives the adoption of fuel-efficient vessels and optimized routing to reduce environmental impact and comply with regulations. Capacity management through fleet flexibility enables providers to respond effectively to seasonal demand peaks. Brand building through participation in major boat shows and industry events strengthens market visibility and credibility. Risk mitigation strategies, including robust insurance coverage and rigorous safety standards, protect reputations and ensure client confidence.

Leading Players in the Global Boat and Yacht Transportation Market

- BBC Chartering is a leading global provider of heavy lift and project cargo shipping services with a significant presence in the yacht transportation sector. The company operates a large fleet of multi-purpose vessels equipped with heavy cranes capable of handling superyachts and oversized recreational boats. BBC Chartering recently expanded its service network by establishing dedicated yacht logistics divisions to offer specialized door-to-door solutions for high-net-worth clients. This strategic focus allows the firm to provide comprehensive care, including customs clearance and secure storage. The company invests heavily in vessel modernization to ensure safe and efficient transport of valuable assets. Their expertise in complex stowage planning minimizes risks during transit. BBC Chartering collaborates closely with insurance providers to meet stringent safety requirements. Their global reach enables seamless repositioning of yachts between major cruising grounds such as the Mediterranean and the Caribbean.

- Zeppelin Heavy Lift is a specialized maritime logistics provider known for its expertise in transporting oversized and high-value cargo, including luxury yachts. The company utilizes semi-submersible vessels and heavy-lift ships to ensure the gentle handling of delicate marine assets. Zeppelin recently enhanced its digital tracking capabilities, allowing clients to monitor their vessels in real time throughout the journey. This technological upgrade improves transparency and builds trust among discerning yacht owners. The firm focuses on personalized service offering tailored logistics solutions for unique transportation challenges. Zeppelin maintains strong relationships with port authorities worldwide to facilitate smooth loading and unloading operations. Their team of experienced engineers ensures that each vessel is secured according to the highest industry standards. The company actively participates in international boat shows to showcase its capabilities and connect with potential clients. Their commitment to safety and reliability has established a strong reputation in the niche market.

- Conroy International is a premier specialist in yacht transportation, providing bespoke logistics services for superyachts and classic vessels. The company offers both float-on/float-off and heavy lift options, depending on client preferences and vessel specifications. Conroy recently launched a new premium service package that includes white-glove handling and dedicated customer support throughout the transit process. This initiative strengthens their position in the ultra-luxury segment, where service quality is paramount. The firm employs highly trained staff who understand the specific needs of yacht owners and captains. Conroy maintains a flexible fleet strategy, allowing them to adapt to seasonal demand fluctuations. They prioritize environmental sustainability by optimizing routes to reduce fuel consumption. The company also provides comprehensive insurance advisory services to protect clients against potential risks. Their extensive network of agents ensures efficient handling of customs and regulatory requirements in various jurisdictions.

MARKET SEGMENTATION

This research report on the global boat and yacht transportation market has been segmented and sub-segmented based on vessel type, service type, and region.

By Vessel Type

- Superyachts

- Small and Medium Recreational Boats

By Service Type

- Heavy-Lift and Semi-Submersible Shipping Services

- Road Transportation

By Region

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What is driving the growth of the global boat and yacht transportation market?

Growing yacht ownership, rising international marine trade, increasing recreational boating activities, and expanding luxury tourism are key factors driving market growth.

2. What types of vessels are commonly transported?

The market transports sailing yachts, motor yachts, fishing boats, speedboats, catamarans, and commercial boats of various sizes.

3. Which transportation modes are used in this market?

Road, sea, rail, and air transportation are used depending on the vessel's size, destination, urgency, and transportation cost.

4. Who are the major end users of boat and yacht transportation services?

Private yacht owners, boat manufacturers, marine dealers, yacht brokers, charter companies, and government organizations are the primary end users.

5. What are the major applications of boat and yacht transportation?

These services are used for international yacht deliveries, boat shows, marina transfers, seasonal relocation, maintenance, repairs, and resale transactions.

6. What are the latest trends in the boat and yacht transportation market?

Digital shipment tracking, specialized transport equipment, eco-friendly logistics solutions, and integrated marine logistics services are among the major market trends.

7. What challenges does the market face?

High transportation costs, complex customs procedures, weather-related delays, port congestion, and strict maritime regulations are significant challenges.

8. How is technology improving boat and yacht transportation?

GPS tracking, route optimization, digital documentation, automated logistics management, and specialized lifting and loading equipment are improving transportation efficiency and safety.

9. What factors influence transportation costs?

Costs depend on vessel size and weight, transportation distance, mode of transport, insurance requirements, customs duties, fuel prices, and handling complexity.

10. What is the future outlook for the global boat and yacht transportation market?

The market is expected to grow steadily over the coming years, driven by increasing recreational boating activities, rising international yacht sales, expanding marine tourism, and continued investments in advanced marine logistics solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com