Global Cancer Diagnostics Market Size, Share, Trends & Growth Forecast Report By Product, Application, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$116.82 BnMarket Estimate, 2026

$124.06 BnMarket Forecast, 2034

$200.74 BnCAGR, 2026–2034

6.2%Global Cancer Diagnostics Market Size

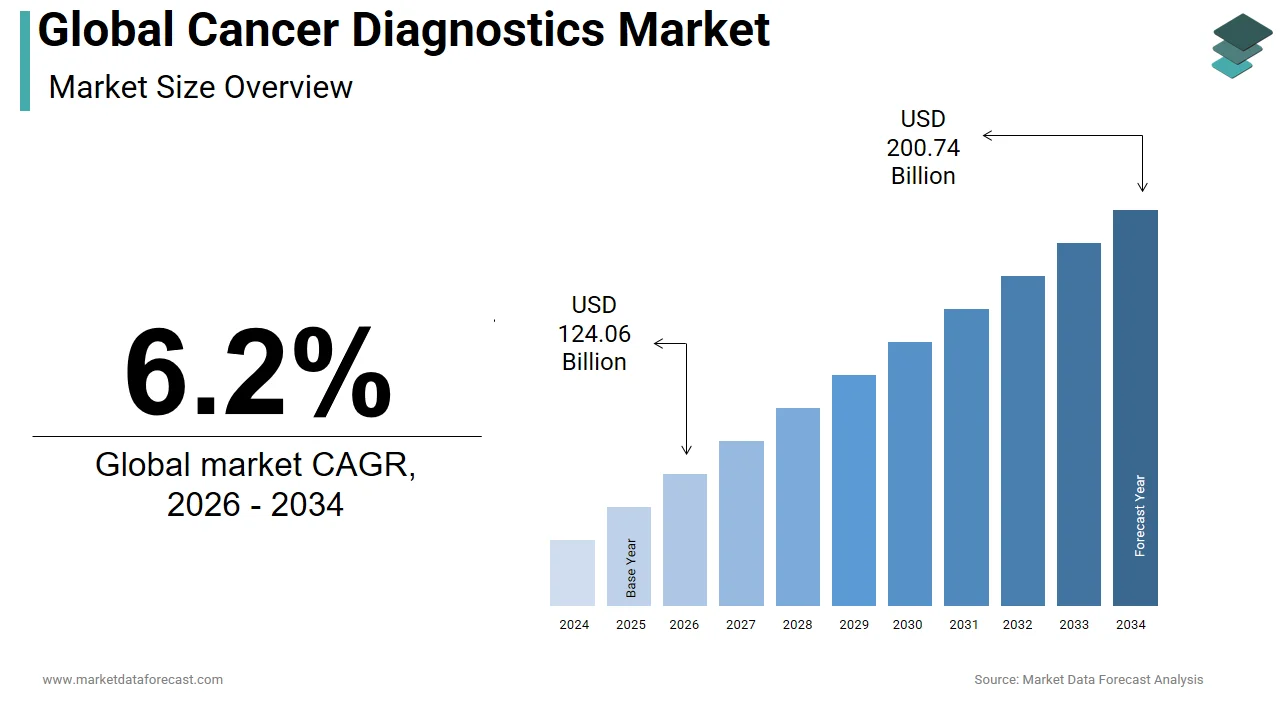

The size of the global cancer diagnostics market was worth USD 116.82 billion in 2025. The global market is anticipated to grow at a CAGR of 6.2% from 2026 to 2034 and be worth USD 200.74 billion by 2034, up from USD 124.06 billion in 2026.

MARKET DRIVERS

The continuous rise in the number of cancer patients is the primary market growth factor. Cancer is one of the leading causes of death worldwide and has been heightening at a startling rate. In 2018, the World Cancer Research Fund International found about 18 million recorded cancer cases worldwide. The continual innovation of products and the increasing need for advanced diagnosis of several diseases are prime market growth factors. In addition, the growing number of cancer cases raises the demand for screening tests and imaging methods to control disease progression. Governments and corporations are taking independent and collaborative initiatives to raise awareness about early cancer diagnosis benefits. Moreover, cancer research institutes and private bodies invest massively in research projects to launch advanced diagnostic tools in the market, proficient in diagnosing the disease much before the symptoms appear.

MARKET RESTRAINTS

Yet, high-cost therapy and low compensation policies in the world's developing countries may hinder the market growth. The increasing use of diagnostic tests coupled with advancements that enable accurate and quicker results has escalated diagnostics costs. The majority of the population cannot afford advanced diagnostic imaging methods, thus impeding the market growth rate. Although various screening procedures enable disease detection at an early stage, they pose certain risk factors that negatively affect health, such as nausea and diarrhea. Also, the cost entailed in performing a diagnosis is relatively high. Therefore, the damaging effects of imaging solutions and the high price of diagnosis are expected to hinder the market growth. In addition, large-scale investments by medical corporations and low profit-cost quotient, and a scarcity of skilled professionals pose restrictions to this market's growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-User, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Abbott Laboratories Inc., F. Hoffmann-La Roche Ltd, Siemens Healthcare GmbH, Thermo Fisher Scientific Inc., GE Healthcare |

SEGMENTAL ANALYSIS

By Product Insights

The technology segment comprises imaging, molecular diagnostics, biopsy, and others. In 2024, imaging technology led the segment due to its popularity among oncologists worldwide as primary cancer diagnosis screening. Imaging modalities such as MRI and CT scans are widely popular because of their inherent features such as non-invasive, quick, and pain-free preliminary screening. Due to technological advancement in next-generation sequencing and cancer biomarkers for early identification of different cancers, Molecular diagnostics are anticipated to be the fastest-growing segment.

By Application Insights

Other cancers (than listed above) are currently dominating the application segment due to the rise in public health awareness programs and proactive undertakings by government healthcare departments to encourage early detection and curb the mortality rate connected with cancer globally. Lung cancer is anticipated to grow faster during the forecast period due to the constant rise in tobacco consumption and the rise in air pollution at an alarming rate.

By End-User Insights

The hospital segment leads with the highest shares of the market owing to the growing number of hospitals with an increasing patient pool. In addition, diagnostic laboratories are also gaining traction in gaining the highest shares due to the increasing demand for the early detection of diseases.

REGIONAL ANALYSIS

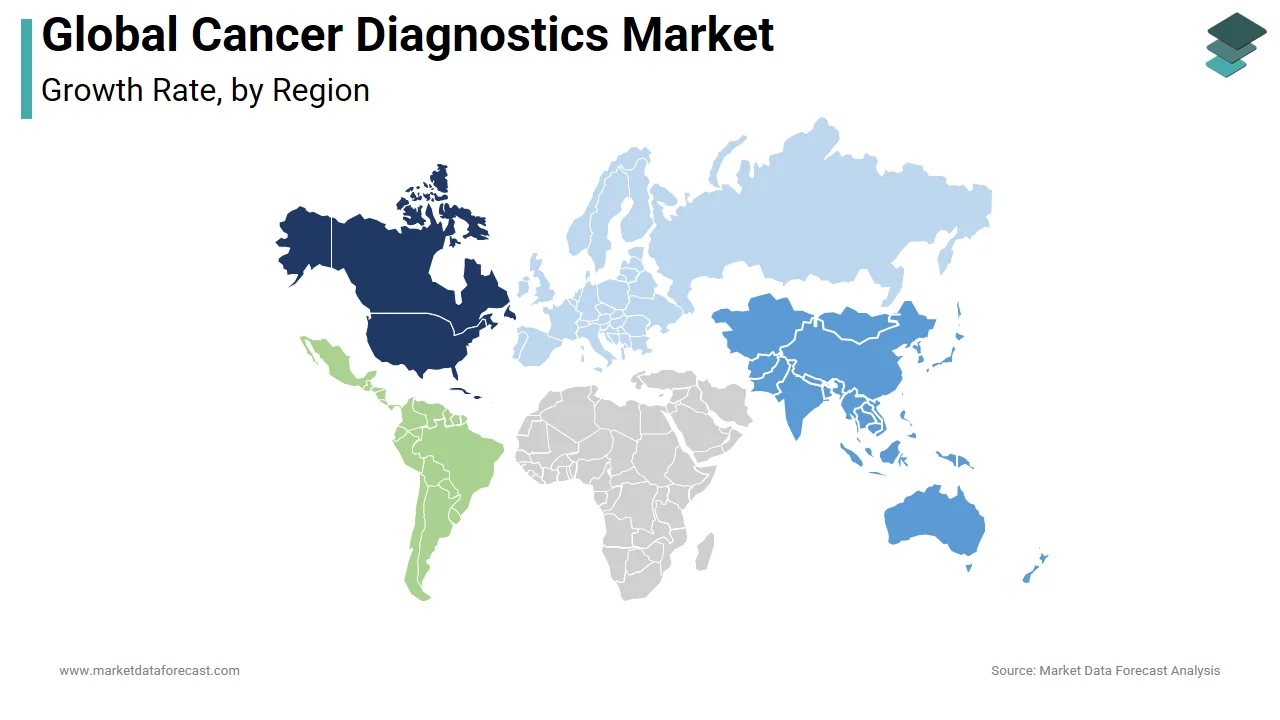

Currently, North America leads the regional segment for the global cancer diagnostics market. American Cancer Society (ACS), in its latest research citings in 2019, approximated 1.7 million new cancer cases to be diagnosed and around 606,880 deaths in America due to cancer. The principal factor driving the cancer diagnostics market growth in the region is the home of market leaders such as Thermo Fisher Scientific, Inc., Hologic, Inc., Qiagen, GE Healthcare, and Danaher Corporation. Europe follows behind in the second position due to the rising predominance of cancer. It focuses on developing advanced technology in cancer diagnostics by strategic collaboration between academic institutes and medical device manufacturers; finally, The Asia Pacific region is expected to manifest widespread growth during the forecast period due to the continual rise in medical tourism and developing healthcare infrastructure.

KEY MARKET PARTICIPANTS

Some of the companies that are playing a dominating role in the global cancer diagnostics market include

- Abbott Laboratories Inc.

- F. Hoffmann-La Roche Ltd

- Siemens Healthcare GmbH

- Thermo Fisher Scientific Inc.

- GE Healthcare

- Hologic Inc.

- Illumina Inc.

- Bio-Rad Laboratories, Inc.

- Agilent Technologies Inc.

- bioMérieux SA

GLOBAL CANCER DIAGNOSTICS MARKET NEWS

- In March 2020, Siemens Healthineers obtained a CE mark for AI-Pathway Companion Prostate Cancer, allowing the company to sell its product in Europe as a medical device, thereby improving its business growth and market position.

- In January 2020, Sysmex launched its ipsogen JAK2 DX reagent, a gene testing kit for blood cancer used to estimate the mutation quantitatively used in diagnosing hematopoietic tumors. This strategy enabled the firm to expand its product offering, thereby extending its product portfolio.

MARKET SEGMENTATION

This research report on the global vascular graft market has been segmented and sub-segmented into the following categories.

By Product

- Tumor biomarkers tests

- Imaging

- Ultrasound and radiology

- Mammography

- MRI scan

- PET scan

- CT scan

- SPECT & others

- Biopsy

- Liquid biopsy

- Immunohistochemistry

- In situ hybridization

By Application

- Bladder cancer

- Breast cancer

- Colon rectal cancer

- Endometrial cancer

- Kidney cancer

- Leukemia

- Liver-lung cancer

- Melanoma

- Non-Hodgkin lymphoma

- Pancreatic cancer

- Prostate cancer

- Thyroid cancer

- Others

By End-User

- Hospitals

- Diagnostic laboratories

- Diagnostic imaging centers

- Cancer research institutes

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What was the size of the cancer diagnostics market?

The global cancer diagnostics market size was valued at USD 110 billion in 2024.

What factors are driving the growth of the cancer diagnostics market?

The growth of the cancer diagnostics market is primarily driven by the increasing incidence of cancer, growing awareness and screening initiatives, and technological advancements in cancer diagnostics.

Who are the key players in the cancer diagnostics market?

Some of the key players operating in the cancer diagnostics market include F. Hoffmann-La Roche AG, Thermo Fisher Scientific, Abbott Laboratories, Illumina Inc., GE Healthcare, Siemens Healthineers, Becton, Dickinson and Company, Bio-Rad Laboratories Inc., Agilent Technologies Inc., and Quest Diagnostics.

Who leads the global cancer diagnostics market?

Diagnostic giants like Roche and Siemens dominate the global cancer diagnostics market innovations in assays and platforms.

What role do hospitals play in the global cancer diagnostics market?

Hospitals integrate diagnostics for comprehensive cancer care in the global cancer diagnostics market workflows.

How prominent is imaging in the global cancer diagnostics market?

MRI and CT scans remain foundational in the global cancer diagnostics market for staging and monitoring.

What impact do labs have on the global cancer diagnostics market?

Reference labs process high-volume biomarkers within the global cancer diagnostics market testing pipelines.

How does liquid biopsy influence the global cancer diagnostics market?

Liquid biopsies enable serial monitoring in the global cancer diagnostics market for treatment response.

What is PCR testing's place in the global cancer diagnostics market?

PCR detects mutations reliably in the global cancer diagnostics market molecular profiling.

What regulations shape the global cancer diagnostics market?

FDA approvals and CLIA standards guide the global cancer diagnostics market assay validations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com