Global Cardiac Mapping Market Size, Share, Trends & Growth Forecast Report By Product (Contact Cardiac Mapping Systems [Electro-Anatomical, Basket Catheter, Traditional Endocardial], Non-contact Systems), Indication (Atrial Fibrillation, Atrial Flutter, AVNRT, Other Arrhythmias), End-User (Hospitals, Clinics, Diagnostic and Imaging Centers), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Market Size, 2025

$589.94 MnMarket Estimate, 2026

$644.28 MnMarket Forecast, 2034

$1,306 MnCAGR, 2026–2034

9.23%Global Cardiac Mapping Market Size

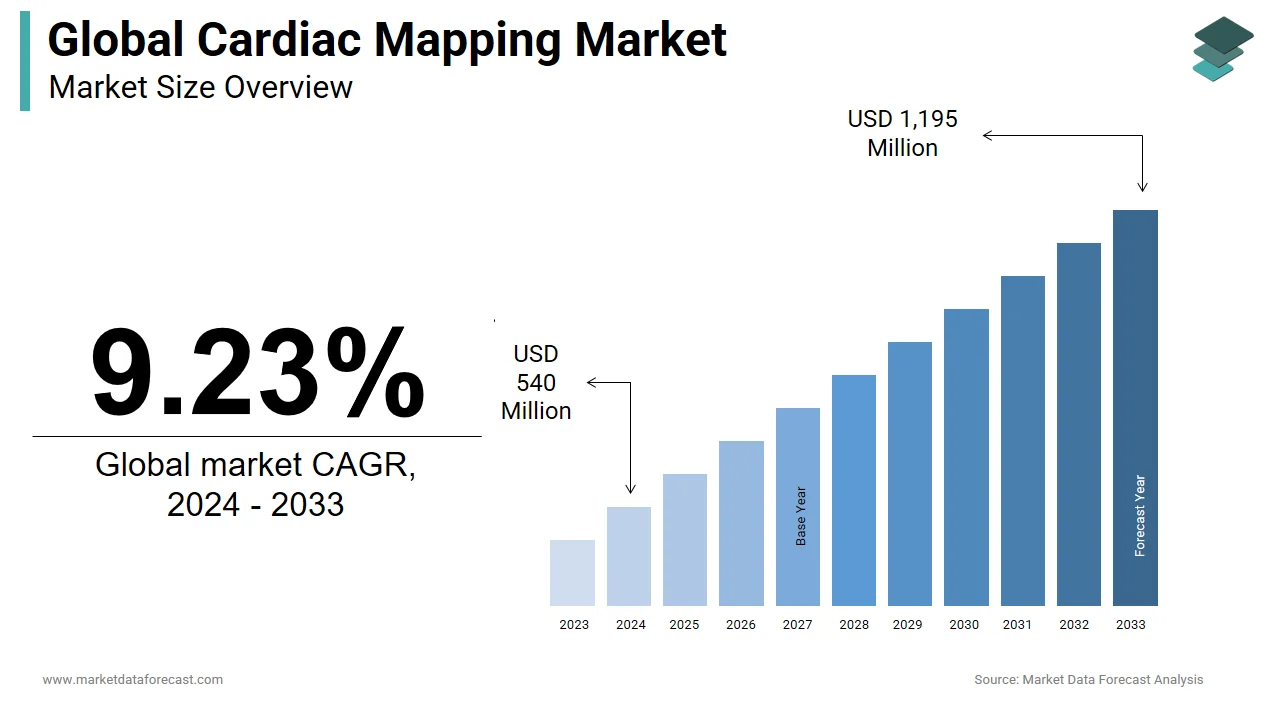

The global cardiac mapping market was valued at USD 589.94 million in 2025, is estimated to reach USD 644.28 million in 2026, and is projected to reach USD 1,306 million by 2034, growing at a CAGR of 9.23% from 2026 to 2034.

Cardiac mapping is a critical diagnostic and therapeutic procedure used to identify the electrical pathways and abnormalities in heart rhythm. It plays a central role in managing arrhythmias, particularly atrial fibrillation (AFib), by enabling electrophysiologists to visualize the heart’s electrical activity and locate areas responsible for irregular rhythms. The process involves the use of specialized catheters and software systems that generate 3D or 4D anatomical and electrical maps of the cardiac chambers. With the rising prevalence of cardiovascular diseases globally, the demand for advanced cardiac mapping technologies has surged, leading to rapid innovation in this sector.

MARKET DRIVERS

Increasing Prevalence of Arrhythmias and Cardiovascular Diseases

The escalating incidence of arrhythmias and broader cardiovascular diseases (CVDs) is one of the most significant drivers fueling the growth of the cardiac mapping market. Atrial fibrillation (AFib), in particular, has become a major public health concern globally. According to the American Heart Association, over 12.1 million people in the U.S. are projected to be diagnosed with AFib by 2030, up from 5.2 million in 2016. As the population ages, the risk of developing arrhythmias increases due to structural changes in the heart and prolonged exposure to risk factors such as hypertension, diabetes, and obesity. For instance, as per the data from the National Institute on Aging, individuals aged 65 and older are five times more likely to develop AFib compared to younger adults. This demographic shift is particularly pronounced in developed nations but is also gaining momentum in emerging economies. Consequently, healthcare providers are increasingly adopting advanced cardiac mapping systems to ensure early diagnosis and targeted interventions. Moreover, improved awareness among physicians and patients about minimally invasive treatments has led to higher procedural volumes. These trends show how rising disease burden and aging populations are catalyzing demand for sophisticated cardiac mapping technologies across the globe.

Technological Advancements in Mapping Systems

Rapid technological innovations in cardiac mapping systems are playing a pivotal role in expanding the market. Modern systems now offer high-resolution 3D and 4D mapping capabilities, allowing for more precise identification of arrhythmogenic substrates and facilitating targeted ablation therapy. Companies such as Abbott, Boston Scientific, and Biosense Webster have introduced next-generation platforms like the EnSite X, RHYTHMIA HDx, and CARTO 3, respectively, which integrate artificial intelligence, faster signal processing, and reduced fluoroscopy exposure, enhancing both safety and efficacy.

According to a report published by the Journal of Interventional Cardiac Electrophysiology, the adoption of high-density mapping systems increased by over 40% between 2020 and 2023, attributed largely to their ability to improve procedural success rates. Apart from these, the integration of robotic-assisted navigation and contact force sensing technology has significantly improved lesion formation accuracy during ablation procedures. Furthermore, the miniaturization of catheter-based sensors and the development of non-contact mapping systems have enabled faster and safer procedures. These advancements not only reduce procedural time but also lower complication rates, thereby increasing physician confidence and patient acceptance.

MARKET RESTRAINTS

High Cost of Advanced Cardiac Mapping Equipment

The widespread adoption of cardiac mapping technologies is the high cost associated with advanced equipment and procedures is one of the primary restraints impeding the market. These expenses place a significant financial burden on healthcare institutions, especially in low- and middle-income countries where budget constraints are acute. Even in developed markets, reimbursement limitations and inconsistent coverage policies can discourage hospitals from investing in these technologies. In emerging economies, where public healthcare spending remains limited, affordability becomes even more prohibitive. Consequently, despite growing clinical demand, financial barriers remain a key obstacle to market expansion. Until pricing models become more accessible or financing mechanisms improve, the adoption of advanced mapping systems will likely remain constrained in many regions.

Shortage of Trained Professionals and Complex Procedure Requirements

The scarcity of skilled electrophysiologists and trained technical personnel required to operate advanced mapping systems effectively is a significant barrier to the growth of the cardiac mapping market. Cardiac mapping is a highly specialized procedure that demands expertise in both cardiology and electrophysiology, along with proficiency in interpreting complex electrical signals and navigating 3D mapping interfaces. However, there remains a substantial gap in workforce availability to meet the rising demand for these services. According to the Heart Rhythm Society, as of 2023, there were fewer than 6,000 board-certified cardiac electrophysiologists in the United States, serving a population where millions suffer from arrhythmias. Globally, the disparity is even more pronounced. In addition, the complexity of cardiac mapping procedures requires extensive training, typically involving years of postgraduate education and hands-on experience. Training programs remain limited in many regions, slowing the development of a robust talent pipeline

MARKET OPPORTUNITIES

Expansion of Telemedicine and Remote Mapping Technologies

The emergence and adoption of telemedicine and remote cardiac mapping technologies present a significant opportunity for the cardiac mapping market. These innovations allow for real-time monitoring and diagnosis of cardiac arrhythmias beyond traditional hospital settings, expanding access to care, particularly in rural and underserved areas. Remote mapping technologies leverage cloud-based platforms and secure data transmission protocols to enable specialists to interpret cardiac electrical activity without being physically present at the patient site. Besides, companies such as Medtronic and Abbott have begun integrating remote connectivity features into their cardiac mapping systems, enabling real-time collaboration between electrophysiologists across different locations. This trend is especially promising in countries with uneven distribution of specialist care. In India, for example, the Apollo Telehealth network reported that remote cardiac diagnostics reached over 2 million patients in rural areas in 2022. Similarly, in the U.S., the Veterans Health Administration implemented a nationwide tele-cardiology program that successfully expanded access to complex arrhythmia care.

Integration of Artificial Intelligence and Machine Learning in Mapping Software

The integration of artificial intelligence (AI) and machine learning (ML) into cardiac mapping software represents a transformative opportunity for the market. These technologies enhance the precision and efficiency of arrhythmia detection by analyzing vast datasets of cardiac electrical activity, identifying patterns, and predicting potential sources of abnormal rhythms. AI-assisted mapping systems can automate data interpretation, reduce procedural variability, and accelerate decision-making for electrophysiologists. Several leading manufacturers have already introduced AI-enhanced platforms. Similarly, Abbott’s EnSite X platform utilizes AI to streamline the creation of high-density activation maps, reducing the time required for complex ablation procedures. According to a 2023 article published in Nature Cardiovascular Research, AI-integrated mapping systems demonstrated a reduction in procedural time and an increase in first-pass success rates in treating atrial fibrillation. Beyond procedural benefits, AI also supports better patient stratification and personalized treatment planning.

MARKET CHALLENGES

Regulatory Complexity and Lengthy Approval Processes

The intricate and time-consuming regulatory approval process for new devices and software enhancements is a significant challenge facing the cardiac mapping market. Given the life-critical nature of cardiac interventions, regulatory bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) impose stringent evaluation criteria for device safety, efficacy, and interoperability. The delay hampers the timely commercialization of innovative products and discourages smaller firms from entering the market. Furthermore, evolving regulatory standards, such as the EU’s Medical Device Regulation (MDR) enacted in 2021, have imposed stricter post-market surveillance requirements, increasing compliance costs for manufacturers. In Asia, regulatory harmonization remains a challenge. China’s National Medical Products Administration (NMPA) and India’s Central Drugs Standard Control Organization (CDSCO) have distinct approval pathways that differ significantly from Western frameworks, necessitating separate clinical trials and documentation. As a result, multinational companies face extended timelines to launch new mapping technologies in these high-growth markets. These regulatory hurdles not only slow down product innovation but also limit patient access to cutting-edge cardiac mapping solutions.

Limited Reimbursement Coverage in Emerging Markets

Reimbursement limitations represent a formidable challenge to the expansion of the cardiac mapping market, particularly in emerging economies. Despite growing awareness and technological advancements, inadequate or inconsistent reimbursement policies hinder the adoption of advanced cardiac mapping procedures. Many national health systems either do not cover or provide minimal reimbursement for complex electrophysiological studies and ablation procedures involving high-end mapping systems. In addition, in India, the National Health Authority under Ayushman Bharat provides limited coverage for cardiac ablation, often excluding newer mapping technologies due to cost considerations. Even in developed markets, reimbursement pressures persist. In Germany, the Federal Joint Committee (G-BA) has imposed strict criteria for funding high-cost cardiac interventions, requiring extensive clinical evidence before approving coverage. These financial barriers significantly impact hospital procurement decisions and patient uptake.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Indication, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Abbott, Acutus Medical, Biosense Webster, BIOTRONIK, Boston Scientific Corporation, EP Solutions SA, Koninklijke Philips N.V., Lepu Medical, Medtronic, and MicroPort Scientific Corporation |

SEGMENTAL ANALYSIS

By Product Insights

The contact cardiac mapping systems segment dominated the global cardiac mapping market by accounting for 65.9% of total revenue in 2024. The superior accuracy and reliability these systems offer in identifying arrhythmogenic substrates are one key driver behind the growth of the contact cardiac mapping systems segment. These systems rely on direct electrode-tissue interaction to generate high-resolution electrical maps of the heart, making them the preferred choice for complex arrhythmia diagnostics and ablation guidance. According to a 2023 study published in Heart Rhythm, contact mapping has demonstrated up to 90% procedural success rates in treating atrial fibrillation when used with real-time contact force monitoring. Leading platforms such as Biosense Webster’s CARTO 3 and Abbott’s EnSite X are widely adopted due to their integration of contact force sensing technology, which improves lesion formation consistency. The growing number of catheter ablation procedures globally is another major factor contributing to the growth of the segment.

The non-contact cardiac mapping systems segment is emerging as the fastest-growing segment in the cardiac mapping market and is projected to expand at a CAGR of 8.7% from 2025 to 2033. The reduction in procedure time and radiation exposure associated with non-contact systems is fuelling the growth of the non-contact cardiac mapping systems segment. This rapid growth is primarily driven by technological advancements that allow for faster, more efficient mapping without requiring direct catheter-tissue contact. Systems like CardioInsight’s EnSite Non-Contact Mapping System have gained traction due to their ability to map large cardiac areas simultaneously using body surface electrodes and computational modeling. Also, increasing demand for minimally invasive and safer procedures has boosted adoption. With rising pressure to optimize resource utilization and enhance procedural efficiency, non-contact cardiac mapping is gaining momentum across both developed and developing markets.

By Indication Insights

The atrial fibrillation (AFib) segment led the cardiac mapping market by accounting for 55.5% of total revenue in 2024. This dominance of the AFib segment is credited to the high prevalence of AFib globally and its association with increased risk of stroke, heart failure, and mortality, necessitating precise diagnostic and therapeutic interventions.

According to the Centers for Disease Control and Prevention (CDC), AFib contributes to about 130,000 deaths annually in the United States alone. Moreover, as per projections from the American Heart Association, by 2030, over 12 million Americans will be diagnosed with AFib. This surge in patient volume directly translates into higher demand for cardiac mapping procedures to guide ablation therapy and other rhythm management strategies. Technological evolution in mapping tools tailored for AFib management further supports its leading position. High-density mapping and rotor mapping techniques have become standard in AFib ablation, improving long-term success rates. With an aging global population and rising incidence of comorbid conditions, AFib remains the central focus of cardiac mapping applications, sustaining its dominant market position.

The "Other Arrhythmias" category is experiencing the highest growth rate in the cardiac mapping market and is projected to expand at a CAGR of 9.4% through 2033. A major factor driving this growth is the improved detection and diagnosis of rare arrhythmias facilitated by advanced mapping technologies. This segment includes less common but increasingly recognized rhythm disorders such as ventricular tachycardia, premature ventricular contractions, and inherited arrhythmia syndromes like Brugada syndrome and long QT syndrome. Another significant driver is the expanding application of cardiac mapping in pediatric and congenital heart disease populations. As awareness and clinical expertise grow, so does the utilization of cardiac mapping for these diverse indications, propelling this segment’s rapid expansion.

By End-User Insights

The hospitals segment commanded the cardiac mapping market, representing a substantial share of total usage in 2024. The availability of comprehensive infrastructure, trained specialists, and access to advanced imaging and interventional tools is largely contributes to the dominance of hospital segment. As primary centers for complex cardiovascular care, hospitals are equipped with dedicated electrophysiology (EP) labs where most cardiac mapping and ablation procedures are performed. In addition, hospitals handle the majority of emergency and chronic arrhythmia cases, further reinforcing their role as the epicenter of cardiac mapping utilization. Moreover, the presence of integrated healthcare delivery models in hospitals facilitates seamless coordination between diagnostics, treatment, and post-operative care. As healthcare systems continue to centralize specialized care, hospitals are expected to maintain their stronghold in the cardiac mapping landscape.

The diagnostic and imaging centers segment is emerging as the fastest-growing end-user segment in the cardiac mapping market, projected to grow at a CAGR of 9.2% in the future. A key driver of the diagnostic and imaging centers segment is the rising preference for cost-effective and accessible outpatient settings for non-emergency cardiac diagnostics. This growth is being fueled by the decentralization of cardiac care and the increasing outsourcing of diagnostic services to standalone facilities. Many of these centers are now integrating advanced cardiac imaging and mapping capabilities to meet the growing demand for early-stage arrhythmia screening. Additionally, regulatory and reimbursement changes have encouraged the proliferation of independent diagnostic facilities. As these centers adopt portable and semi-automated mapping solutions, they are playing an increasingly vital role in expanding access to cardiac diagnostics beyond traditional hospital settings.

REGIONAL ANALYSIS

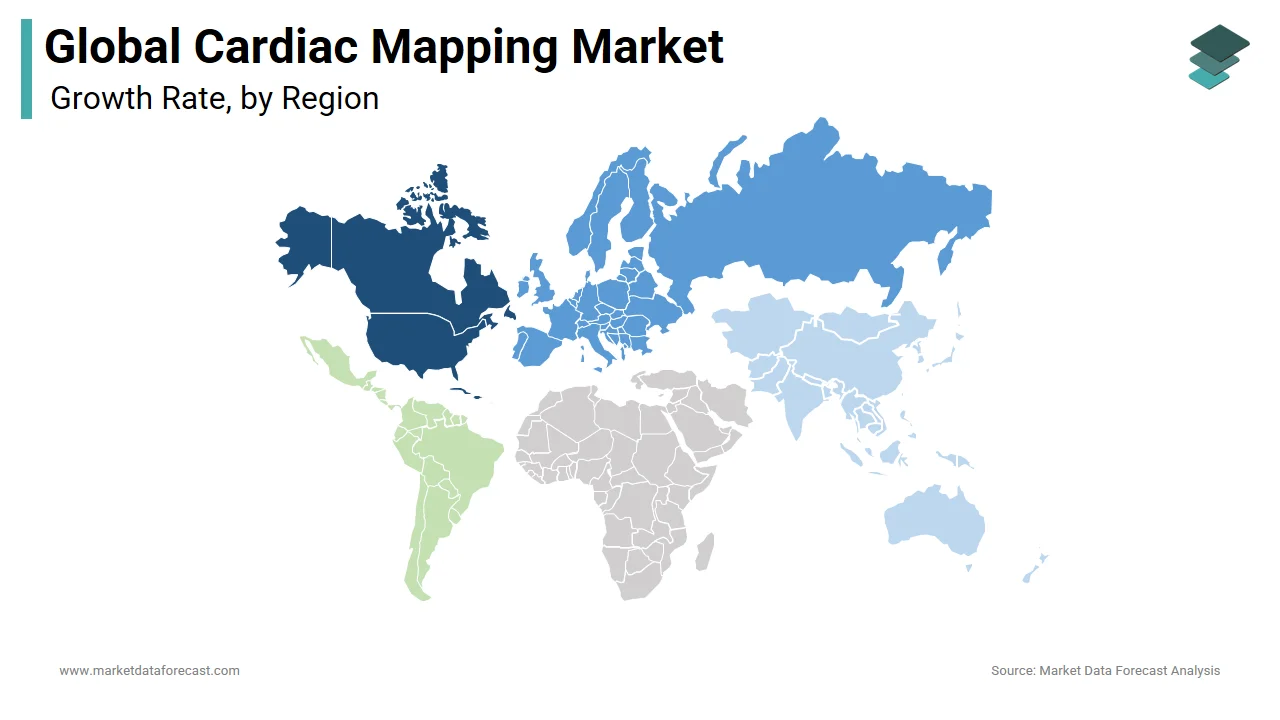

North America Cardiac Mapping Market Analysis

North America held the largest share of the global cardiac mapping market and is estimated at 38.5% in 2024. The region’s dominance is driven by high healthcare expenditure, widespread adoption of advanced medical technologies, and a robust pipeline of innovative cardiac mapping systems. The United States, in particular, leads in terms of both research and clinical application. Also, the presence of major cardiac mapping system manufacturers such as Abbott, Boston Scientific, and Medtronic ensures continuous product development and market penetration. Regulatory support also plays a crucial role. With strong clinical infrastructure and favorable reimbursement policies, North America remains the epicenter of the global cardiac mapping industry.

Europe Cardiac Mapping Market Analysis

Europe is another notable market for cardiac mapping. The region benefits from well-established healthcare systems, a high density of electrophysiology (EP) centers, and proactive government initiatives aimed at reducing cardiovascular mortality. Germany stands out as a key market within Europe, boasting one of the highest numbers of EP labs per capita. Similarly, the United Kingdom has witnessed a steady increase in cardiac mapping adoption, supported by the National Health Service’s investment in digital health infrastructure. Regulatory harmonization through the EU Medical Device Regulation (MDR) has introduced challenges, but it has also raised standards for device quality and safety. Despite initial delays in approvals, companies are adapting to the new framework, ensuring continued innovation. These factors sustain Europe’s strong position in the cardiac mapping market.

Asia Pacific Cardiac Mapping Market Analysis

Asia Pacific is poised for rapid expansion due to increasing healthcare investments, rising awareness of cardiac diseases, and growing disposable incomes in emerging economies. Japan leads the region in terms of technological adoption and procedural volume. Meanwhile, India is witnessing a surge in cardiac mapping adoption, driven by rising prevalence of arrhythmias and government-backed initiatives such as Ayushman Bharat, which aims to improve access to specialty care. China is another key player. The Chinese government has been actively promoting domestic manufacturing of cardiac devices and investing in telemedicine infrastructure to bridge rural-urban disparities. As healthcare modernization accelerates across APAC, the region is set to become a critical growth engine for the global cardiac mapping industry.

Latin America Cardiac Mapping Market Analysis

Latin America represents a modest yet growing segment of the cardiac mapping market. Brazil and Mexico lead the region in terms of adoption, driven by improving healthcare infrastructure and rising awareness of cardiac rhythm disorders. However, despite increasing demand, access to advanced cardiac mapping remains limited, particularly in public hospitals. Mexico, on the other hand, has seen gradual improvements in cardiac care, with the Mexican Social Security Institute expanding coverage for electrophysiological studies. Nevertheless, the lack of trained professionals and high equipment costs continue to impede widespread adoption. While growth remains moderate, strategic investments and policy reforms could unlock untapped potential in the years ahead.

Middle East and Africa Cardiac Mapping Market Analysis

The Middle East and Africa collectively indicate low current penetration but growing interest in advanced cardiac diagnostics. Countries such as Saudi Arabia and South Africa are leading the charge in adopting cardiac mapping technologies, supported by investments in healthcare modernization. Saudi Arabia’s Vision 2030 initiative includes substantial funding for healthcare upgrades, including the expansion of cardiology and electrophysiology services. Similarly, South Africa is making strides in improving cardiac care access, though disparities persist between urban and rural regions. Despite progress, affordability and workforce shortages remain barriers. However, partnerships with international device manufacturers and training programs are helping bridge these gaps. As regional healthcare systems continue to evolve, the Middle East and Africa present long-term growth opportunities for the cardiac mapping market.

COMPETITION OVERVIEW

The cardiac mapping market is highly competitive, characterized by the presence of established multinational corporations and emerging players striving to innovate and capture market share. Major players dominate due to their extensive product portfolios, robust R&D capabilities, and strong global distribution networks. However, competition is intensifying as smaller firms introduce differentiated technologies that challenge conventional mapping approaches. Innovation in software integration, real-time data processing, and minimally invasive techniques is reshaping the industry landscape. Additionally, companies are focusing on enhancing user experience through intuitive interfaces and improved workflow efficiency. Strategic mergers and acquisitions are also common, aimed at consolidating market positions and expanding geographic reach. As demand for precise arrhythmia diagnosis grows, manufacturers are under pressure to deliver more efficient, cost-effective, and adaptable solutions. This dynamic environment fosters continuous improvement but also raises the bar for new entrants seeking to establish a foothold in the market.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global cardiac mapping market include

- Abbott

- Acutus Medical

- Biosense Webster

- BIOTRONIK

- Boston Scientific Corporation

- EP Solutions SA

- Koninklijke Philips N.V.

- Lepu Medical

- Medtronic

- MicroPort Scientific Corporation

TOP LEADING PLAYERS IN THE MARKET

Abbott is a global leader in cardiac mapping with its EnSite family of systems, particularly the EnSite X and EnSite Precision platforms. The company has been instrumental in advancing high-resolution 3D mapping and integration with robotic navigation. Abbott's focus on innovation and strategic partnerships has strengthened its position as a dominant player. Its commitment to improving clinical outcomes through enhanced visualization and procedural efficiency continues to influence market growth.

Biosense Webster is a pioneer in electrophysiology and cardiac mapping technologies. Its flagship product, the CARTO 3 system, remains one of the most widely used mapping platforms worldwide. The company consistently invests in research and development to refine ablation guidance, contact force sensing, and automated lesion creation. With a strong global distribution network and continuous product enhancements, Biosense Webster plays a crucial role in shaping the future of cardiac mapping.

Boston Scientific has significantly expanded its footprint in the cardiac mapping space through acquisitions and internal development. The company’s RHYTHMIA HDx and FARMAPORTAL platforms offer high-density mapping capabilities that improve diagnostic accuracy and procedural efficiency. Boston Scientific emphasizes integrating artificial intelligence into mapping workflows and expanding access to advanced electrophysiology tools across diverse healthcare settings, contributing substantially to market evolution.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players in the cardiac mapping market is continuous technological innovation, with companies investing heavily in R&D to enhance mapping precision, reduce procedural complexity, and integrate AI-driven analytics. These advancements help differentiate products in a competitive landscape and meet evolving clinical demands.

Another key approach is strategic collaborations and partnerships, where firms engage in joint ventures, academic alliances, and co-development agreements to accelerate technology adoption and expand their clinical evidence base. These collaborations also facilitate regulatory approvals and faster market entry for new solutions.

Lastly, expanding into emerging markets through localized offerings and distribution networks is a critical growth strategy. Companies are tailoring their product portfolios to suit regional healthcare infrastructures and cost constraints, enabling broader access while strengthening their global presence.

GLOBAL CARDIAC MAPPING MARKET NEWS

- In February 2024, Abbott launched an updated version of its EnSite X cardiac mapping system with enhanced AI-assisted interpretation features, aiming to improve diagnostic accuracy and streamline electrophysiology lab workflows.

- In May 2023, Biosense Webster expanded its global training initiative by opening a new Electrophysiology Education and Innovation Center in Singapore, designed to train physicians on advanced cardiac mapping and ablation techniques across the Asia-Pacific region.

- In November 2023, Boston Scientific announced a collaboration with a leading AI healthcare startup to integrate machine learning algorithms into its RHYTHMIA cardiac mapping platform, enhancing signal analysis and procedural decision-making capabilities.

- In July 2024, Medtronic introduced a next-generation catheter compatible with its cardiac mapping systems, featuring improved sensor resolution and contact force feedback to support more effective ablation procedures.

- In January 2024, Biotronik expanded its presence in Latin America by partnering with a regional distributor to increase access to its CARDIOBEAT GX cardiac mapping and ablation solutions in underserved markets.

MARKET SEGMENTATION

This research report on the global cardiac mapping market has been segmented and sub-segmented based on product, indication, end-user, and region.

By Product

- Contact Cardiac mapping systems

- Electro-anatomical mapping

- Basket catheter mapping

- Traditional endocardial catheter mapping

- Non-contact Cardiac mapping systems

By Indication

- Atrial Fibrillation

- Atrial Flutter

- AVNRT

- Other Arrhythmias

By End-User

- Hospitals

- Clinics

- Diagnostic and Imaging Centers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global cardiac mapping market?

The global cardiac mapping market provides 3D systems catheters localizing arrhythmia circuits guiding ablation across atrial fibrillation VT procedures worldwide comprehensively.

Why grow the global cardiac mapping market?

The global cardiac mapping market expands with AFib prevalence minimally invasive EP procedures fluoroscopy-free navigation demands strategically worldwide continuously.

What drives the global cardiac mapping market?

Rising arrhythmias EP lab expansion propels the global cardiac mapping market alongside contact mapping precision catheter technologies significantly worldwide.

Which systems lead the global cardiac mapping market?

Contact electroanatomical mapping dominates the global cardiac mapping market offering precise 3D localization real-time catheter tracking comprehensively worldwide reliably.

What role do EP labs play in the global cardiac mapping market?

Electrophysiology labs utilize maximum volumes mapping AF circuits using the global cardiac mapping market basket catheters ablation catheters consistently worldwide.

How does 3D mapping function in the global cardiac mapping market?

Electroanatomical systems reconstruct chamber geometry voltage maps identifying scar rotors in the global cardiac mapping market ablation target identification effectively worldwide.

Which arrhythmias define the global cardiac mapping market?

Atrial fibrillation leads AVNRT atrial flutter follow diverse EP procedures in the global cardiac mapping market circuit characterization strategically worldwide comprehensively.

What challenges face the global cardiac mapping market?

Complex VT mapping obese patients challenge the global cardiac mapping market requiring high-density catheters AI interpretation technically continuously worldwide.

How does AF ablation use the global cardiac mapping market?

Pulmonary vein isolation wide area circumferential ablation utilize the global cardiac mapping market voltage gap identification durable lesion assessment effectively worldwide.

What innovations shape the global cardiac mapping market?

AI rotor detection ultra-high density mapping trend enhancing the global cardiac mapping market substrate characterization ablation outcomes seamlessly worldwide continuously.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com