Global Personal Protective Equipment (PPE) Market Size, Share, Trends & Growth Forecast Report By Product (Head, Eye & Face Protection, Hearing Protection, Protective Clothing, Respiratory Protection, Protective Footwear, Fall Protection, Hand Protection, Disposable Gloves and Others), End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Personal Protective Equipment (PPE) Market Size

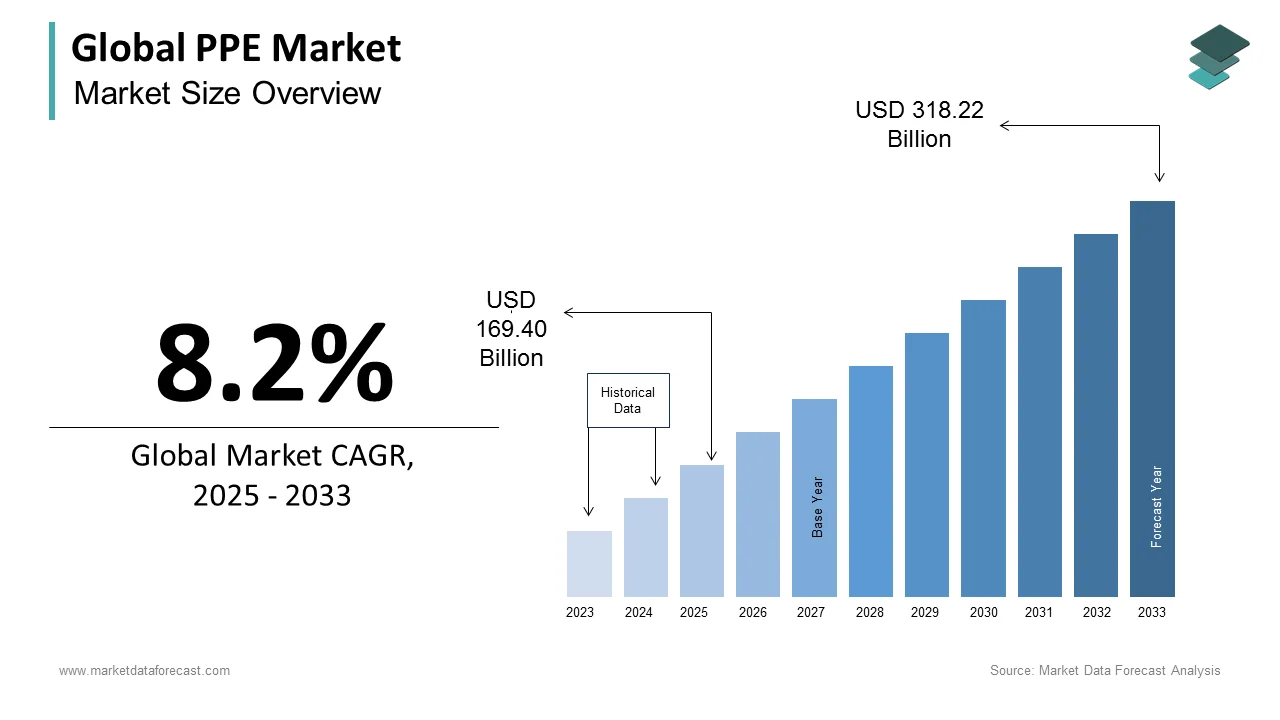

The size of the global PPE market was worth USD 156.56 billion in 2024. The global market is anticipated to grow at a CAGR of 8.2% from 2025 to 2033 and be worth USD 318.22 billion by 2033 from USD 169.40 billion in 2025.

The Personal Protective Equipment (PPE) is a broad range of gear designed to safeguard individuals from occupational health and safety risks across industrial, healthcare, construction, and emergency response environments. PPE includes respiratory protection devices, protective clothing, helmets, goggles, gloves, and hearing protection equipment, each engineered to mitigate exposure to physical, chemical, biological, and environmental hazards. The imperative for PPE has been reinforced by rising awareness of workplace safety, tightening regulatory frameworks, and global public health emergencies. As per the International Labour Organization, over 2.78 million workers die annually due to work-related accidents or diseases in preserving human capital. As per the World Health Organization, 15% of the global disease burden among workers is attributable to occupational risks, many of which can be reduced through effective PPE deployment.

MARKET DRIVERS

Expansion of High-Risk Industrial Sectors in Emerging Economies

The proliferation of industrial activities in developing regions in manufacturing, mining, and oil & gas is driving the growth of the personal protective equipment market. As per the International Energy Agency, global energy demand from emerging economies grew by 4.2% in 2023. This industrial surge necessitates stringent worker safety protocols in high-exposure environments where risks of chemical exposure, falls, and machinery-related injuries are elevated. Additionally, the ASEAN Occupational Safety and Health Network indicates that workplace injury rates in Southeast Asia remain above 3.5 per 1,000 workers by prompting stricter enforcement and corporate investment in safety gear. Multinational corporations operating in these regions are also adopting global safety standards, which is further driving the procurement of certified PPE.

Rising Awareness of Occupational Health and Safety Standards

A shift in workplace safety culture has emerged globally with organizations increasingly prioritizing employee well-being as both an ethical obligation and a strategic imperative, which is additionally to enhance the growth of the personal protective equipment market. As per the International Labour Organization, only 30% of the world’s workforce was covered by effective occupational safety and health programs in 2022. As per the European Agency for Safety and Health at Work, workplace safety training programs have expanded by 38% across EU member states since 2019, directly correlating with increased PPE adoption.

MARKET RESTRAINTS

Counterfeit and Substandard PPE Products in Developing Markets

The circulation of non-compliant products in low- and middle-income countries where regulatory oversight is fragmented is inhibiting the growth of the personal protective equipment market. In India, the Bureau of Indian Standards seized over 12,000 units of fake N95 masks in 2023 alone, revealing systemic gaps in quality enforcement. The Global Health Security Initiative identifies weak customs inspections and limited product traceability as key enablers of illicit PPE trade, with counterfeit respirators often selling at 50–70% lower prices than certified alternatives. This price disparity incentivizes cost-driven procurement, especially among small and medium enterprises. While regulatory bodies like the European Committee for Standardization (CEN) and ANSI in the U.S. enforce rigorous testing protocols, harmonization of global standards remains elusive.

High Costs of Advanced PPE Limiting Adoption in SMEs

The elevated cost of high-performance and smart PPE systems among small and medium-sized enterprises (SMEs) in developing economies is hindering the growth of the personal protective equipment market. As per the International Finance Corporation, SMEs constitute over 90% of businesses worldwide and employ approximately 50% of the global workforce.

MARKET OPPORTUNITIES

Integration of IoT and Wearable Technology in Smart PPE

The integration of digital technologies in real-time hazard detection and workforce safety management is creating new opportunities for the growth of the personal protective equipment market. Smart PPE, embedded with sensors, GPS, and biometric monitoring systems, enables continuous tracking of vital signs, environmental conditions, and location data, thereby enhancing emergency response and preventive care. Furthermore, data generated by smart PPE is increasingly being integrated into enterprise risk management systems, enabling predictive analytics and compliance automation.

Strengthening of Regulatory Frameworks in Emerging Markets

Governments across developing regions are intensifying efforts to formalize occupational safety regulations, creating a fertile environment for PPE market expansion. As per the International Labour Organization, over 100 countries have either introduced or revised their national occupational safety and health policies since 2020, with notable legislative advancements in Indonesia, Nigeria, and Bangladesh. In Indonesia, the Ministry of Manpower enacted Regulation No. 20 of 2022, mandating PPE provision in all formal-sector workplaces and imposing penalties for non-compliance, affecting over 60 million workers. Moreover, multilateral initiatives such as the ILO’s SafeYouth@Work program are building institutional capacity in vocational training and enforcement. In Vietnam, factory inspections increased by 52% between 2021 and 2023 following new directives from the Ministry of Labour, Invalids and Social Affairs, directly boosting demand for certified protective gear. These regulatory shifts are not only expanding legal mandates but also fostering a cultural transition toward accountability, where employers face reputational and financial risks for negligence.

MARKET CHALLENGES

Supply Chain Fragmentation and Raw Material Volatility

The constant disruptions due to reliance on a geographically concentrated and chemically intensive supply chain are a great challenge factor for the growth of the personal protective equipment market. Key materials such as melt-blown polypropylene for respirators, nitrile for gloves, and aramid fibers for flame-resistant clothing are predominantly sourced from a limited number of countries, creating vulnerability to geopolitical and environmental shocks.

Inadequate Training and Improper Use of PPE Among Workers

The insufficient training and inconsistent usage practices are also hindering the growth of the personal protective equipment market. As per the National Institute for Occupational Safety and Health, nearly 53% of workplace injuries involving PPE occur due to incorrect fitting, misuse, or premature removal, rather than equipment failure. A 2023 study conducted by the Canadian Centre for Occupational Health and Safety revealed that only 41% of industrial workers in surveyed facilities could correctly demonstrate the donning and doffing procedures for chemical-resistant suits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | 3M, Honeywell International, Inc., DuPont, Cardinal Health, Medline Industries, Inc., Kimberly-Clark Corporation, Ansell Ltd., MSA Safety Inc., and O&M Halyard, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The protective clothing segment was the largest and held 22.3% of the personal protective equipment (PPE) market share in 2024, with its indispensable role across high-risk industries such as chemicals, oil & gas, and pharmaceuticals, where exposure to hazardous substances necessitates full-body protection. The widespread adoption of chemical-resistant suits, flame-retardant garments, and anti-static apparel with its a function in preventing dermal injuries and long-term occupational illnesses. The nuclear and hazardous waste management sectors further amplify this trend; the World Nuclear Association notes that each nuclear facility deploys an average of 1,200 protective suits monthly during maintenance cycles.

The respiratory protection segment is likely to grow with an expected CAGR of 9.8% in the coming years, with escalating exposure to airborne hazards in both industrial and urban environments. In industrial settings, the prevalence of silica dust, welding fumes, and volatile organic compounds has intensified regulatory action. According to the U.S. Occupational Safety and Health Administration, over 2.3 million workers in construction and manufacturing are exposed to respirable crystalline silica, which is prompting a 2023 enforcement initiative that mandates powered air-purifying respirators (PAPRs) in high-exposure zones.

By End-User Insights

The construction sector was accounted in holding 28.7% of the personal protective equipment market in 2024, with the inherently hazardous nature of construction activities, which involve elevated workspaces, heavy machinery, and exposure to particulates and noise. Additionally, the adoption of Building Information Modeling (BIM) and safety-integrated project planning has institutionalized PPE audits in procurement cycles. As per the Construction Industry Institute, 64% of major contractors now tie subcontractor payments to verified safety equipment usage.

The healthcare sector is growing with a CAGR of 10.4% during the forecast period, with the escalating biohazard exposure and systemic vulnerabilities exposed during recent pandemics. As per the World Health Organization, 14 million healthcare workers globally are exposed to bloodborne pathogens annually, with needlestick injuries affecting 3 million each year. Additionally, aging populations in Japan and Germany are increasing hospitalization rates. As per the Organisation for Economic Co-operation and Development, OECD countries saw a 17% rise in inpatient days between 2019 and 2023.

REGIONAL ANALYSIS

Asia-Pacific Personal Protective Equipment (PPE) Market Analysis

Asia-Pacific was the top performer in the global PPE market with 36.8% of the share in 2024, with the rapid industrialization and a vast labor force engaged in high-risk sectors. As per the International Labour Organization, Asia-Pacific employs nearly 70% of the global industrial workforce, with India alone adding 12 million new industrial jobs between 2020 and 2023. Meanwhile, India’s National Policy on Safety, Health, and Environment at the Workplace, introduced in 2023, requires all factories to conduct biannual safety audits with documented PPE provision.

North America Personal Protective Equipment (PPE) Market Analysis

North America PPE market held 22.3% of the share in 2024 owing to the stringent regulatory frameworks and high levels of workplace safety institutionalization. The growing awareness and rising prominence of safety are majorly influencing the growth of the personal protective equipment market. Canada complements this trend with its proactive stance on mining safety.

Europe Personal Protective Equipment (PPE) Market Analysis

Europe PPE market growth is likely to be driven by harmonized regulations and a strong emphasis on worker rights. The European Union’s Personal Protective Equipment Regulation (EU) 2016/425 establishes a unified certification framework by ensuring that 98% of PPE sold in the bloc meets Category II or III safety standards, as verified by the European Commission. The transition to green energy is also shaping demand. WindEurope states that offshore wind installations in the North Sea will require 15,000 technicians by 2030, each needing fall protection and weather-resistant gear. In Scandinavia, Norway’s petroleum safety authority mandates dual-layer respiratory protection for all offshore platform workers, reflecting the region’s risk-averse approach.

COMPETITIVE LANDSCAPE

The competitive landscape of the PPE market is characterized by a blend of established multinational corporations and agile regional manufacturers vying for dominance across diverse industrial and healthcare applications. Intense competition is driving innovation in material science, with a focus on lightweight, breathable, and sustainable protective fabrics. The post-pandemic era has intensified scrutiny on supply chain resilience, which is prompting firms to localize production and diversify sourcing. Strategic collaborations with governments, insurance providers, and industrial operators are enabling firms to embed their solutions into broader safety ecosystems.

KEY MARKET PLAYERS

The major players operating in the global PPE market profiled in this report are

- 3M

- Honeywell International, Inc.

- DuPont

- Cardinal Health

- Medline Industries, Inc.

- Kimberly-Clark Corporation

- Ansell Ltd.

- MSA Safety Inc.

- O&M Halyard, Inc.

TOP LEADING PLAYERS IN THE MARKET

- 3M Company has maintained a dominant presence in the Asia Pacific PPE market through continuous innovation and localized manufacturing capabilities. The company offers a comprehensive portfolio, including N95 respirators, hearing protection devices, and reflective protective clothing, tailored to regional industrial and healthcare demands. In 2023, 3M expanded its respiratory protection production line in Shanghai to meet rising demand from China’s healthcare and construction sectors. It also launched a new range of lightweight half-face respirators designed for tropical climates, enhancing user comfort in Southeast Asia. Collaborating with government agencies in India and Australia, 3M has supported safety training programs to promote correct PPE usage. The company’s investment in R&D centers in Singapore and Japan enables rapid adaptation to regional regulatory standards. Furthermore, 3M’s digital procurement platforms have streamlined B2B supply chains across the region, which is improving accessibility for SMEs.

- Honeywell International Inc. plays a pivotal role in shaping the Asia Pacific PPE market by integrating advanced technology into traditional protective gear. The company’s offerings span smart respiratory systems, connected gas detectors, and high-performance protective suits used extensively in oil & gas, petrochemicals, and electronics manufacturing. In 2022, Honeywell opened a new safety innovation hub in Gurugram, India, to develop climate-adaptive PPE for South Asian workers. It introduced the Honeywell Forge for Safety platform across major industrial sites in South Korea and Japan, enabling real-time monitoring of worker exposure and equipment status. The company strengthened its supply chain by expanding manufacturing at its facility in Changshu, China, to ensure faster delivery across the region. Honeywell also partnered with Japan’s Industrial Safety and Health Association to standardize smart PPE protocols in robotics-driven factories. Its collaboration with Singapore’s Ministry of Manpower on AI-powered hazard prediction systems has set new benchmarks in proactive safety management.

- Ansell Limited is headquartered in Australia which holds a strategic advantage in the Asia Pacific market due to its regional roots and deep understanding of local occupational hazards. Specializing in hand protection and protective apparel, Ansell serves industries ranging from electronics assembly in Vietnam to mining in Indonesia. In 2023, the company launched Ansell Edge, a digital platform in Thailand and Malaysia that uses predictive analytics to optimize glove selection and replacement cycles, reducing workplace injuries by up to 30% as reported in internal trials. Ansell expanded its manufacturing footprint in Sri Lanka and China to enhance supply resilience and reduce lead times. It also introduced biodegradable nitrile gloves in response to increasing environmental regulations across ASEAN nations. The company actively engages with regional trade bodies such as the ASEAN Occupational Safety and Health Network to influence policy development. Ansell’s acquisition of a specialty cleanroom glove producer in South Korea in early 2024 strengthened its position in the semiconductor and pharmaceutical sectors.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the PPE market are deploying a range of strategic initiatives to consolidate their positions and respond to dynamic regulatory and technological landscapes. Product innovation remains a central pillar, with companies investing heavily in smart PPE embedded with sensors for real-time health and environmental monitoring. Firms like Honeywell and 3M are integrating IoT platforms to enable predictive safety analytics by enhancing value beyond basic protection. Strategic acquisitions are being leveraged to expand technological capabilities, as seen in Ansell’s purchase of niche glove manufacturers to strengthen its cleanroom portfolio. Geographic expansion, particularly into high-growth emerging markets, is another strategy, supported by localized manufacturing and distribution networks to ensure compliance and reduce delivery times. Partnerships with government agencies and industrial consortia are fostering standardization and training, improving end-user adherence. Additionally, sustainability is becoming a competitive differentiator, with leaders introducing recyclable materials and eco-conscious packaging. Digital transformation is also prominent, with cloud-based procurement systems and AI-driven risk assessment tools being rolled out to enterprise clients. These multifaceted strategies reflect a shift from commoditized PPE supply to integrated, intelligence-driven safety ecosystems.

GLOBAL PERSONAL PROTECTIVE EQUIPMENT (PPE) MARKET NEWS

- In March 2023, 3M launched a new respiratory protection manufacturing line in Shanghai, China, to enhance supply capacity for N95 respirators and powered air-purifying systems, which cater to rising demand from healthcare and industrial sectors across the Asia Pacific.

- In July 2023, Honeywell inaugurated its Safety Innovation Hub in Gurugram, India, focused on developing climate-resilient and digitally connected PPE solutions tailored for South Asian industrial environments by strengthening its regional R&D footprint.

- In November 2023, Ansell introduced the Ansell Edge digital platform in Malaysia and Thailand, utilizing predictive analytics to optimize glove usage and reduce workplace injuries, which is marking a strategic shift toward data-driven safety management.

- In January 2024, MSA Safety acquired a minority stake in a German smart helmet startup to integrate augmented reality and real-time gas detection into its fall protection systems by enhancing its technological edge in the mining and oil & gas sectors.

- In April 2024, Delta Plus Group expanded its manufacturing facility in Vietnam to increase production of chemical-resistant suits and high-visibility apparel, which is targeting export growth to Japan and Australia amid rising industrial safety regulations.

MARKET SEGMENTATION

This research report on the global PPE market has been segmented and sub-segmented based on product, end-user, and region.

By Product

- Head, Eye & Face Protection

- Hearing Protection

- Protective Clothing

- Heat & Flame Protection

- Chemical Defending

- Cleanroom Clothing

- Mechanical Protective Clothing

- Limited General Use

- Others

- Respiratory Protection

- Air-purifying Respirators

- Supplied Air Respirators

- Protective Footwear

- Leather

- Rubber

- PVC

- Polyurethane

- Others

- Fall Protection

- Hand Protection

- Disposable Gloves

- By Type

- General Purpose

- Chemical Handling

- Sterile Gloves

- Surgical

- Others

- By Material

- Natural Rubber

- Nitrile

- Neoprene

- Vinyl

- Others

- Durable Gloves

- Mechanical Gloves

- Chemical Handling

- Thermal/Flame Retardant

- Others

- By Type

- Others

By End-User

- Construction

- Manufacturing

- Oil & Gas

- Chemicals

- Food

- Pharmaceuticals

- Healthcare

- Transportation

- Mining

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the Personal Protective Equipment (PPE) Market?

The PPE Market includes the production and sale of safety equipment designed to protect workers and individuals from injuries and hazards in various industries

2. Which regions dominate the Personal Protective Equipment Market?

North America currently leads with roughly 30% market share, followed by Europe and a rapidly expanding Asia Pacific region

3. What are the key product segments in the PPE Market?

Key segments include hand protection, eye and face protection, respiratory protection, protective clothing, foot protection, and fall protection

4. Which industries are the major end-users of PPE?

Industries such as construction, manufacturing, healthcare, oil & gas, chemicals, and food processing lead PPE consumption

5. What is driving growth in the PPE Market?

Increased workplace safety awareness, strict regulations, expansion of industrial sectors, and COVID-19-induced demand growth

6. How are technological developments influencing the PPE Market?

Innovations include smart PPE with sensors, improved materials for comfort and durability, and environmentally friendly products

7. What are the challenges in the PPE Market?

Supply chain disruptions, high material costs, regulatory compliance complexity, and product counterfeit issues

8. How significant is the healthcare segment in the PPE Market?

Healthcare PPE is a high-growth segment, driven by infection control needs and pandemic preparedness

9. What are the legal standards affecting the PPE Market?

Regulatory bodies like OSHA, NIOSH, ANSI, and international standards set guidelines for PPE compliance

10. What trends are shaping the PPE Market’s future?

Increasing adoption in emerging countries, sustainability focus, integration of IoT in smart PPE, and growing industrial automation

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com