Global Chemical Tankers Market Size, Share, Trends & Growth Forecast Report - Segmentation by Product Type (Organic Chemicals, Inorganic Chemicals, Vegetable Oils & Fats), Fleet Type, Fleet Material, and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) – Industry Analysis (2026 to 2034)

Market Size, 2025

$30.5 BnMarket Estimate, 2026

$32.04 BnMarket Forecast, 2034

$47.01 BnCAGR, 2026–2034

4.9%Global Chemical Tankers Market Report Summary

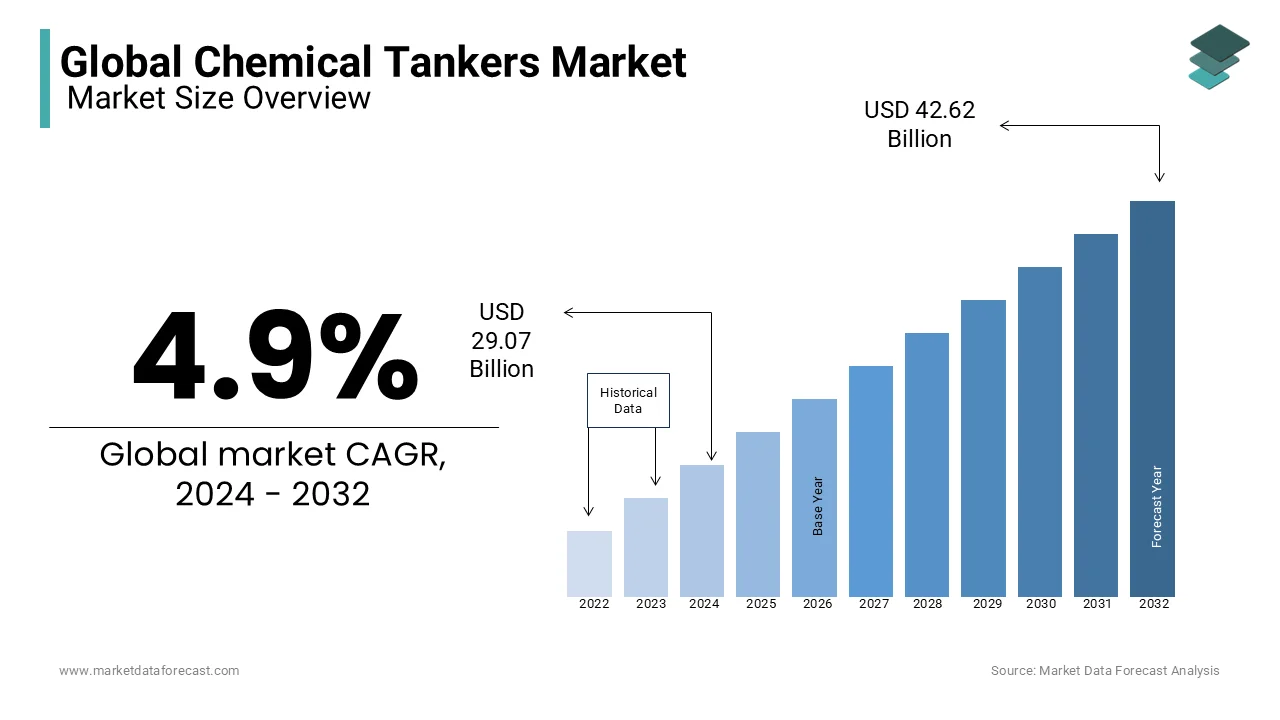

The global chemical tankers market was valued at USD 30.54 billion in 2025, is estimated to reach USD 32.04 billion in 2026, and is projected to reach USD 47.01 billion by 2034, growing at a CAGR of 4.91% during the forecast period. Market growth is driven by increasing global trade of chemicals and petrochemicals, rising demand for safe and efficient transportation of liquid bulk cargo, and expansion of industrial production across emerging economies. The need for specialized vessels with advanced safety and storage capabilities is further supporting market expansion. In addition, growing investments in maritime logistics and fleet modernization are contributing to steady growth of the chemical tankers market.

Key Market Trends

- Rising global trade in chemicals and petrochemicals is driving demand for chemical tankers.

- Increasing focus on safety and regulatory compliance is supporting adoption of advanced tanker designs.

- Growing investments in fleet modernization and expansion are boosting market growth.

- Expansion of chemical manufacturing in emerging economies is enhancing trade volumes.

- Technological advancements in vessel design and coating materials are improving operational efficiency.

Segmental Insights

- Based on product, the organic chemicals segment was the largest and held 65.8% of the global chemical tankers market share in 2025. This dominance is attributed to high demand for transportation of organic chemicals used in industrial and manufacturing processes.

- Based on fleet type, the deep sea vessels segment accounted for a substantial share of the chemical tankers market in 2025. The segment’s growth is driven by increasing long distance trade and international shipping activities.

- Based on fleet material, the coated tanks segment dominated with 55.7% of the global chemical tankers market share in 2025, supported by enhanced corrosion resistance, safety, and compatibility with a wide range of chemical cargo.

Regional Insights

- The global chemical tankers market is experiencing steady growth across regions, supported by industrial expansion and global trade activities.

- Asia Pacific was the leading region in 2025, driven by its position as a major manufacturing hub for chemicals and petrochemicals, with countries such as China, India, and South Korea contributing significantly to market demand.

Competitive Landscape

The global chemical tankers market is moderately competitive, with key players focusing on fleet expansion, operational efficiency, and compliance with international safety standards to strengthen their market position. Companies are investing in advanced vessel technologies, strategic partnerships, and global logistics networks. Prominent players in the global chemical tankers market include Bahri, Stolt Nielsen, Odfjell, Navig8, MOL Chemical Tankers, Nordic Tankers, Wilmar International, MISC Berhad, Team Tankers, Iino Kaiun Kaisha, and others.

Global Chemical Tankers Market Size

The global chemical tankers market size was valued at USD 30.54 billion in 2025, and the global market size is expected to reach USD 47.01 billion by 2034 from USD 32.04 billion in 2026. The market is growing at a CAGR of 4.91% during the forecast period.

A chemical tanker is a specialized type of tanker ship designed to transport various liquid chemical products in bulk, including industrial chemicals, acids, alcohols, and edible oils. These ships are engineered with sophisticated cargo handling systems and coated tanks to safely carry a wide array of substances ranging from basic petrochemicals to high value specialty chemicals. The operational integrity of this sector is paramount given the hazardous nature of the cargo which includes acids alcohols and solvents. According to the International Maritime Organization (IMO), the transport of dangerous goods by sea is governed by strict international codes. Specifically, bulk liquid chemical transport is mandated by the International Bulk Chemical Code (IBC Code), which sets global standards for ship design, construction, and equipment to prevent environmental and safety hazards. This regulatory framework ensures safety and environmental protection during transit. As reported by the United Nations Conference on Trade and Development, the vast majority of global trade is transported by sea. Separately, chemical tankers are recognized for their essential function in the chemical industry's supply chain. The complexity of logistics is heightened by the need for segregation of incompatible cargoes and precise temperature control. The market is influenced by industrial production levels in key manufacturing hubs such as Asia and North America. Furthermore, the shift towards cleaner energy sources has increased the transport of biofuels and chemical intermediates used in renewable technologies. The strategic positioning of terminal infrastructure and the availability of skilled crew members also dictate market dynamics. This sector remains integral to the global economy facilitating the movement of essential raw materials for pharmaceuticals agriculture and consumer goods industries.

MARKET DRIVERS

Expansion of the Global Petrochemical Industry Drives Demand for Specialized Transportation Vessels

The continuous expansion of the global petrochemical industry is a key driver for the chemical tankers market. It necessitates the safe and efficient transport of both raw materials and finished products. Petrochemicals are the building blocks for countless everyday items including plastics fertilizers and synthetic fibers. Reports from the International Council of Chemical Associations highlight that the global chemical industry serves as a massive engine for the world economy, with its total economic footprint, including direct and indirect activities, accounting for a significant portion of global gross domestic product. This growth is particularly pronounced in emerging economies where urbanization and industrialization are accelerating. According to the International Energy Agency, petrochemical feedstocks are projected to be the primary driver of global oil demand through the middle of the century, eventually representing the largest single component of oil consumption as demand for traditional transport fuels declines. This surge in production requires a corresponding increase in shipping capacity to move products from manufacturing hubs in the Middle East and Asia to consumption centers in Europe and North America. The diversity of chemical products necessitates specialized vessels with stainless steel or epoxy coated tanks to prevent contamination and ensure purity. Additionally, the trend towards on purpose production of light olefins and aromatics has increased the volume of trade in these specific commodities. The integration of new production facilities in regions like the United States Gulf Coast further amplifies the need for reliable maritime logistics. Hence, the chemical tanker fleet must expand and modernize to handle increasing volumes and maintain supply chain efficiency. This direct correlation between industrial output and shipping demand sustains the growth trajectory of the market.

Stringent Environmental Regulations Promote the Adoption of Eco Friendly Vessel Designs and Operations

Stringent environmental regulations are significantly fuelling growth within the chemical tankers market. Consequently, shipowners are compelled to invest in newer, more efficient, and environmentally friendly vessels. The International Maritime Organization has implemented rigorous standards to reduce greenhouse gas emissions and prevent marine pollution. The International Maritime Organization has established an ambitious framework to decarbonise global shipping, transitioning from its original reduction goals to a more rigorous commitment of achieving net-zero greenhouse gas emissions by or around the middle of the century. This regulatory pressure mandates the adoption of advanced technologies such as exhaust gas cleaning systems and energy efficient design indices. As per the European Maritime Safety Agency the enforcement of the Sulphur Cap regulation has led to a significant shift towards low sulphur fuels and alternative propulsion systems. Shipowners are increasingly ordering new builds that comply with the Energy Efficiency Design Index requirements which mandate lower carbon intensity. These modern vessels not only meet regulatory standards but also offer operational cost savings through improved fuel efficiency. The phase out of older less efficient tonnage creates opportunities for new construction orders. Furthermore investors and charterers are prioritizing sustainability credentials leading to higher demand for green vessels. This regulatory driven renewal cycle stimulates shipbuilding activity and enhances the overall quality of the global fleet. The transition towards decarbonization thus acts as a catalyst for market modernization and technological advancement.

MARKET RESTRAINTS

Volatility in Crude Oil Prices Impacts Operational Costs and Freight Rate Stability

Volatility in crude oil prices is a major hurdle for the Chemical Tankers Market expansion. This instability creates uncertainty in both operational costs and freight rates, hindering market growth. Bunker fuel constitutes a significant portion of operating expenses for shipping companies and fluctuations in oil prices directly affect profitability. According to the U.S. Energy Information Administration crude oil prices have experienced substantial swings ranging from negative values during demand shocks to over 100 dollars per barrel during geopolitical tensions. This unpredictability makes it difficult for shipowners to plan long term budgets and set competitive freight rates. As per the Baltic Exchange volatile fuel costs can erode profit margins especially when freight rates do not adjust quickly enough to reflect increased expenses. High fuel prices may also lead to slower steaming practices to conserve fuel which reduces vessel availability and disrupts supply chains. Conversely sudden drops in oil prices can lead to inventory build ups and subsequent corrections in chemical production affecting cargo volumes. The lack of price stability discourages investment in new vessels and limits financial flexibility for operators. Additionally hedging strategies to mitigate fuel price risks add complexity and cost to business operations. This economic uncertainty hampers strategic planning and can delay fleet expansion projects. Oil price volatility will remain a persistent challenge for the industry. This will continue until energy markets stabilize or alternative fuels become cost-competitive.

Geopolitical Tensions and Trade Disputes Disrupt Established Shipping Routes and Supply Chains

Geopolitical tensions and trade disputes are significant restraints to the chemical tankers market. They disrupt established shipping routes, causing supply chain inefficiencies. Conflicts in key maritime chokepoints such as the Strait of Hormuz and the Red Sea can lead to vessel diversions increased insurance premiums and delays. According to UN Trade and Development (UNCTAD), geopolitical instability and the resulting rerouting around major canals caused container freight rates to surge by over 140 percent in 2024, with total shipping distances (ton-miles) increasing nearly three times faster than trade volume. Trade wars between major economies such as the United States and China have resulted in tariffs and retaliatory measures that alter trade flows and reduce cargo volumes. As per the World Trade Organization restrictions on chemical imports and exports can fragment global markets and reduce overall trade efficiency. Sanctions on specific countries may prohibit certain shipping activities limiting market access for operators. These disruptions force companies to seek alternative routes which are often longer and more expensive. The uncertainty surrounding international relations also dampens investor confidence and slows down capital expenditure in the sector. Furthermore the risk of asset seizure or detention in conflict zones adds a layer of operational risk. Such geopolitical factors create an unpredictable business environment that complicates logistics planning and increases operational risks. The industry must remain agile to navigate these complex political landscapes while maintaining service reliability.

MARKET OPPORTUNITIES

Growing Demand for Biofuels and Renewable Chemicals Opens New Cargo Segments

The growing demand for biofuels and renewable chemicals offers a great opportunity for the Chemical Tankers Market. This trend opens new cargo segments and diversifies revenue streams. Many governments have implemented strict carbon reduction policies, fostering a surge in green energy demand. As a result, the production of renewable feedstocks, including bioethanol and biodiesel, is experiencing rapid expansion. According to the International Energy Agency (IEA), global biofuel demand is projected to grow by 30 percent by 2030 (relative to 2024 levels), with the strongest expansion occurring in emerging economies like Brazil, India, and Indonesia. These liquids require specialized transportation similar to traditional chemicals creating demand for versatile tanker fleets. As per the Renewable Fuels Association the export of biofuels from producing nations to consuming regions is increasing necessitating reliable maritime logistics. Chemical tankers with stainless steel tanks are well suited for transporting these sensitive cargoes without contamination. The shift towards a circular economy also boosts the trade in recycled chemical feedstocks which require careful handling. Shipowners who adapt their fleets to handle these emerging commodities can capture early mover advantages. Furthermore partnerships with biofuel producers and traders can secure long term charter agreements. This transition aligns with global sustainability goals and provides a growth avenue beyond traditional petrochemicals. Chemical tanker operators can position themselves as enablers of the green energy transition. By doing so, they can enhance their market relevance and resilience.

Technological Advancements in Digitalization and Automation Improve Operational Efficiency

Technological advancements in digitalization and automation open up big possibilities for the Chemical Tankers Market. These advancements improve operational efficiency and safety, enabling better performance. The integration of Internet of Things sensors artificial intelligence and big data analytics enables real time monitoring of vessel performance cargo conditions and fuel consumption. According to the International Chamber of Shipping digital solutions can reduce fuel consumption by up to 10 percent through optimized routing and speed management. As per DNV GL the adoption of smart shipping technologies enhances predictive maintenance reducing downtime and repair costs. Automated cargo handling systems minimize human error and improve loading and unloading speeds which is critical for maintaining tight schedules. Blockchain technology is being explored to streamline documentation and enhance transparency in the supply chain. These innovations also support compliance with environmental regulations by providing accurate data on emissions and energy usage. Charterers increasingly prefer operators who can provide detailed visibility into shipment status and environmental impact. Investing in digital infrastructure allows companies to differentiate themselves and offer value added services. Furthermore remote inspection capabilities reduce the need for physical surveys saving time and resources. The embrace of digital transformation positions chemical tanker operators to meet the evolving expectations of stakeholders and achieve higher operational excellence. This technological leap fosters a more resilient and responsive shipping ecosystem.

MARKET CHALLENGES

Shortage of Skilled Seafarers Poses a Significant Operational Challenge

A shortage of skilled seafarers poses a significant challenge to the chemical tankers market. It threatens both operational safety and efficiency. Handling hazardous chemical cargoes requires highly trained personnel with specialized knowledge of safety protocols and emergency procedures. The BIMCO/ICS Seafarer Workforce Report projects that the global shipping industry will face a shortfall of nearly 90,000 officers by 2026, driven principally by a growth in the world fleet that is outstripping the rate of new recruitment. Contrary to perceptions of a retention crisis, the BIMCO/ICS Seafarer Workforce Report found that the industry has successfully reduced officer turnover rates in recent years, meaning the workforce challenge is one of recruitment rather than retention. The complexity of modern chemical tankers with advanced cargo handling systems further exacerbates the need for specialized training. Inadequate staffing levels can lead to fatigue increased risk of accidents and regulatory non compliance. Training programs are costly and time consuming creating a barrier to rapid workforce expansion. Additionally geopolitical issues and travel restrictions can hinder crew changes causing logistical bottlenecks. The industry faces pressure to improve working conditions and career prospects to attract young talent. Failure to address this manpower crisis could result in operational delays and increased insurance costs. Ensuring a steady supply of qualified personnel is critical for maintaining the integrity of the chemical supply chain. Companies must invest in training and welfare initiatives to mitigate this pressing challenge.

High Capital Expenditure and Financing Constraints Limit Fleet Expansion

High capital expenditures and financing constraints limit fleet expansion in the chemical tanker market. As a result, operators are struggling to meet growing demand. Building new chemical tankers involves significant upfront costs due to the specialized materials and technologies required for safe cargo transport. Research reflects a surge in newbuild values, with the price of a standard medium-range stainless steel chemical tanker now averaging between $45 million and $50 million, driven by higher shipyard costs and green technology specifications. As per the United Nations Conference on Trade and Development access to finance has become more challenging as banks and investors apply stricter environmental social and governance criteria. Lenders are increasingly hesitant to fund projects involving fossil fuel related assets or older vessel designs. This tightening of credit conditions restricts the ability of smaller operators to upgrade their fleets. High interest rates further increase the cost of borrowing reducing the attractiveness of new investments. The long lead times for ship construction also expose owners to market risks during the building period. Without adequate financial resources companies may struggle to replace aging tonnage or capitalize on market upturns. This financial barrier consolidates the market among larger players with stronger balance sheets. Overcoming these funding hurdles requires innovative financing structures and strong relationships with financial institutions. The high entry barrier thus constrains market growth and competition

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.91% |

| Segments Covered | By Product, Fleet Type, Fleet Material, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa, and Others. |

| Market Leaders Profiled | Bahri (Saudi Arabia), Stolt-Nielsen (UK), Odfjell (Norway), Navig8 (UK), MOL Chemical Tankers (Singapore), Nordic Tankers (Denmark), Wilmar International (Singapore), MISC Berhad (Malaysia), Team Tankers (Bermuda), and Iino Kaiun Kaisha (Japan)., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The organic chemicals segment dominated the chemical tankers market and accounted for a 65.8% share in 2025. Its extensive use in petrochemical derivatives and industrial manufacturing drives the dominance of this segment. Apart from these, the dominance of this segment is primarily attributed to the vast volume of trade in key commodities such as methanol benzene and styrene which are essential feedstocks for the plastics and polymer industries. These substances are produced in massive quantities globally and require specialized maritime transport due to their hazardous nature and high value. The American Chemistry Council indicates that global output of primary chemicals has reached a massive scale, with basic organic building blocks comprising the largest volume of this industrial output to meet global manufacturing needs. The integration of supply chains between major producing regions like the Middle East and consuming markets in Asia and Europe necessitates a robust fleet of chemical tankers. As per the International Energy Agency the demand for organic chemical feedstocks is projected to grow significantly driven by the expanding middle class in emerging economies who consume more plastic based goods. Methanol alone accounts for a substantial portion of seaborne chemical trade with millions of tons shipped annually to support formaldehyde and acetic acid production. The versatility of organic chemicals in creating everyday products from packaging to automotive parts ensures consistent demand. Furthermore the shift towards lighter materials in various industries boosts the consumption of organic derived polymers. This sustained industrial reliance on organic compounds cements their position as the leading product segment in the chemical tanker market requiring continuous logistical support.

The vegetable oils and fats segment is anticipated to witness the fastest CAGR of 7.5% between 2026 and 2034 due to the surge in biofuel production and food security needs. Moreover, the rapid expansion of this segment is fueled by the increasing global demand for biodiesel and renewable diesel which utilize feedstocks such as palm oil soybean oil and used cooking oil. Governments worldwide are implementing mandates to blend biofuels with conventional diesel to reduce carbon emissions driving up the volume of these liquids transported by sea. According to the United States Department of Agriculture, global production of vegetable oils is hitting unprecedented levels, supported by intensified agricultural expansion and higher crop yields across major producing regions in the Southern Hemisphere and Southeast Asia. As per the International Energy Agency, the transition toward cleaner energy sources is driving a substantial increase in biofuel consumption, requiring an efficient maritime logistics network to transport raw feedstocks to global refining centers. The versatility of chemical tankers allows them to carry both edible and non edible oils ensuring efficient utilization of fleet capacity. Additionally, the rising population and changing dietary habits in developing countries increase the demand for edible oils for consumption. The ability of stainless steel tanks to maintain the purity and quality of these sensitive cargoes makes chemical tankers the preferred mode of transport. This dual demand from energy and food sectors positions vegetable oils and fats as the most dynamic growth driver in the product segment.

By Fleet Type Insights

The deep-sea vessels segment led the Chemical Tankers Market and captured a substantial share in 2025 because of the long-distance trade routes connecting major production and consumption hubs. Also. the spearheading of this segment is attributed to the geographical disparity between chemical production centers and end user markets which necessitates long haul maritime transportation. Major producers of petrochemicals and specialty chemicals are located in regions such as the Middle East Northeast Asia and the United States while significant consumption occurs in Europe and other parts of Asia. According to the United Nations Conference on Trade and Development deep-sea shipping accounts for the majority of international chemical trade volumes due to its cost effectiveness for bulk cargo over long distances. Research indicates that average transit times for chemical tankers on major global routes have risen recently, as operators navigate complex geopolitical shifts and environmental restrictions that require longer sailing distances. Deep-sea vessels typically have larger capacities allowing them to achieve economies of scale that reduce the per unit cost of transportation. The complexity of global supply chains requires reliable and scheduled services which deep-sea operators provide through established networks. Furthermore, the ability of these vessels to carry multiple grades of chemicals simultaneously enhances their operational efficiency and profitability. The strategic importance of key chokepoints such as the Suez Canal and the Panama Canal further underscores the reliance on deep-sea logistics. This structural dependence on long distance maritime transport ensures that deep-sea vessels remain the backbone of the global chemical trade infrastructure.

The coastal vessels segment is likely to experience the fastest CAGR of 6.2% over the forecast period owing to regional trade integration and short sea shipping initiatives Moreover, the accelerated growth of this segment is propelled by the increasing emphasis on regional trade agreements and the development of short sea shipping networks that offer faster and more flexible delivery options. In regions such as Europe and Asia coastal shipping provides a vital link between major ports and inland industrial clusters reducing congestion on land based transport modes. The European Commission identifies short sea shipping as a vital pillar of the regional economy, representing a significant portion of total freight activity and serving as a key focus for policies aimed at reducing road congestion. As per the Association of Southeast Asian Nations initiatives to enhance maritime connectivity within the region have led to increased investment in coastal terminal infrastructure and fleet modernization. Coastal vessels are ideal for transporting smaller parcels of chemicals to niche markets and just in time manufacturing facilities. The lower capital expenditure required for coastal operations compared to deep-sea ventures attracts new entrants and encourages fleet expansion. Additionally environmental regulations promoting modal shift from road to water transport benefit coastal shipping due to its lower carbon footprint per ton mile. The rise of regional manufacturing hubs in countries like Vietnam and India further stimulates demand for coastal chemical transport. This combination of policy support infrastructure development and industrial decentralization drives the rapid expansion of the coastal fleet segment.

By Fleet Material Insights

The coated tanks segment was the largest segment in the Chemical Tankers Market and occupied a share of 55.7% in 2025. This position of the segment is credited to its versatility and cost effectiveness in handling a wide range of chemical cargoes. The prevalence of coated tanks is due to their ability to transport a diverse array of chemical products including acids solvents and clean petroleum products without the high cost associated with stainless steel construction. Epoxy phenolic and zinc silicate coatings provide sufficient protection against corrosion for many standard chemical cargoes making these vessels economically attractive to operators. The International Chamber of Shipping confirms that coated vessels comprise the bulk of the global chemical fleet, providing a cost-effective solution for transporting a wide variety of standard bulk liquids across major trade routes. As per DNV GL advancements in coating technologies have significantly improved the durability and resistance of these tanks allowing them to handle more aggressive cargoes than previously possible. This technological progress extends the operational life of coated vessels and reduces the frequency of dry docking for repairs. Charterers often prefer coated tankers for parcel trades where multiple different cargoes are carried on a single voyage as they offer a good balance between purity and cost. The lower initial investment cost for coated vessels also lowers the barrier to entry for smaller shipping companies. Furthermore, the widespread availability of coated tonnage ensures competitive freight rates for standard chemical shipments. This economic and operational versatility secures the dominant position of coated tanks in the market.

The stainless steel tanks segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 8.2% from 2026 and 2034. This swift expansion of the segment is fuelled by the demand for high purity specialty chemicals and biofuels. The quick surge of this segment is supported by the increasing trade in high value specialty chemicals pharmaceutical ingredients and biofuels which require absolute purity and resistance to contamination. Stainless steel tanks offer superior cleanliness and ease of cleaning making them ideal for sensitive cargoes that cannot tolerate even trace amounts of residue. According to the Specialty Chemicals Magazine the global market for specialty chemicals is expanding at a rate higher than the general chemical industry driving demand for dedicated stainless steel vessels. The Renewable Fuels Association emphasizes the importance of tank integrity and material compatibility when transporting bio-based fuels to ensure that the products remain free from contamination and maintain their chemical properties throughout the voyage. The stringent regulatory requirements for pharmaceutical and food grade chemicals further mandate the use of stainless-steel containment systems. Shipowners are increasingly ordering new builds with stainless steel tanks to capture this premium market segment and secure long-term contracts with high value clients. The durability of stainless steel also reduces long term maintenance costs despite the higher initial investment. Additionally, the growth of the electric vehicle battery market which relies on high purity electrolytes transported in specialized tankers contributes to this trend. This shift towards high value and sensitive cargoes positions stainless steel tanks as the most dynamic growth area in the fleet material segment.

REGIONAL ANALYSIS

Asia Pacific Chemical Tankers Market Analysis

Asia Pacific outperformed other regional markets for chemical tankers in 2025. This growth of the APAC market is driven by its status as the global manufacturing hub for chemicals and petrochemicals with China India and South Korea being key players. It shows robust industrial production and extensive import export activities. The region accounts for the highest volume of chemical trade globally driven by strong domestic demand and export oriented production. The Asian Development Bank indicate that regional economic expansion continues to be anchored by urbanization, though the S&P Global Ratings chemical sector outlook suggests the industry itself must navigate a period of oversupply and cautious demand growth in major markets like China. As per the China Petroleum and Chemical Industry Federation China is the world largest consumer and producer of chemicals necessitating a vast fleet of tankers for both domestic distribution and international trade. The presence of major shipbuilding yards in South Korea and Japan facilitates the construction of new chemical tankers enhancing regional fleet capacity. The increasing integration of supply chains within the Association of Southeast Asian Nations further boosts intra regional trade volumes. Government initiatives to develop chemical industrial parks in countries like India and Vietnam attract foreign investment and increase cargo flows. The region strategic location along major shipping routes also makes it a critical transshipment hub. This combination of production capacity consumption growth and logistical advantage solidifies Asia Pacific dominance in the global chemical tanker market.

North America Chemical Tankers Market Analysis

North America followed closely behind in the chemical tankers market because of the shale gas revolution and increased chemical exports. The expansion of the North American market is attributed to the abundance of low cost natural gas which has spurred a boom in petrochemical production particularly in the United States Gulf Coast. This surge in production has transformed the region into a major exporter of ethylene propylene and other derivatives requiring extensive maritime transport. According to the American Chemistry Council, the business of chemistry is one of the nation's largest exporting sectors, maintaining a consistent trade surplus as shipments to key international markets continue to rise on a multi-year trajectory. As per the U.S. Energy Information Administration the expansion of ethane cracking facilities has led to increased shipments of ethylene and other light hydrocarbons to global markets. The modernization of port infrastructure along the Gulf and East Coasts supports the loading of larger chemical tankers. Canada and Mexico also contribute to regional trade through cross border pipelines and coastal shipping. The focus on sustainability has also increased the production of biofuels and renewable chemicals in the region adding to cargo diversity. Regulatory support for domestic manufacturing and trade agreements facilitate smooth export processes. This export driven growth model ensures steady demand for chemical tankers originating from North American ports.

Europe Chemical Tankers Market Analysis

Europe is a key contributor to the chemical tankers market due to its advanced chemical industry and strict environmental regulations. The region leverages its sophisticated chemical industry to maintain a strong presence in the market with Germany France and the Netherlands being major production and trading hubs. The region is a leading importer of raw materials and exporter of high value specialty chemicals and pharmaceuticals. According to the European Chemical Industry Council the chemical sector in Europe generates over 500 billion euros in sales annually supporting significant maritime logistics. As per the Port of Rotterdam Authority the port handles millions of tons of liquid bulk chemicals each year serving as a gateway for European trade. The implementation of stringent environmental regulations such as the European Green Deal drives the demand for cleaner fuels and bio based chemicals which require specialized transport. The well developed inland waterway network connects major ports to industrial hinterlands facilitating efficient distribution. The region focus on circular economy principles increases the trade in recycled chemical feedstocks. Additionally, the presence of major shipping companies and classification societies in Europe influences global standards and practices. This blend of industrial strength regulatory leadership and logistical infrastructure sustains Europes vital role in the chemical tanker market.

Middle East Chemical Tankers Market Analysis

The Middle East holds a substantial share in the global chemical tankers market owing to its vast petrochemical production capabilities and strategic geographic location. Moreover, the Middle East market is defined by its role as a primary supplier of basic petrochemicals and feedstocks to global markets leveraging its abundant oil and gas reserves. Countries like Saudi Arabia and the United Arab Emirates have invested heavily in downstream industries to diversify their economies. As per the Saudi Basic Industries Corporation SABIC is one of the worlds largest diversified chemical companies exporting millions of tons of products annually via sea. The strategic location of the region along major shipping lanes such as the Strait of Hormuz facilitates efficient export to Asia and Europe. Government visions such as Saudi Vision 2030 prioritize the expansion of the chemical sector attracting foreign investment and technology. The development of new industrial cities and ports enhances export capabilities. The focus on producing higher value added chemicals rather than just raw materials increases the complexity and value of shipments. This strategic expansion and geographic advantage ensure the Middle East remains a critical source of chemical cargo for the global fleet.

Latin America Chemical Tankers Market Analysis

Latin America is an emerging player in the chemical tankers market due to growing agricultural chemical demand and biofuel production. Also, Latin America contribution to the market is driven by its strong agricultural sector which requires significant inputs of fertilizers and pesticides as well as its growing biofuel industry. Brazil and Argentina are key players in the region with substantial production of soybeans and sugarcane leading to high demand for agricultural chemicals and biofuel transport. According to the Inter American Development Bank the agricultural sector in Latin America accounts for a significant portion of regional GDP driving imports of agrochemicals. As per the Brazilian Ministry of Mines and Energy Brazil is a leading producer of ethanol and biodiesel requiring specialized tankers for domestic distribution and export. The region also imports large volumes of methanol and other basic chemicals for industrial use. Infrastructure improvements in ports such as Santos and Paranagua enhance handling capacity for liquid bulk cargoes. Economic reforms and trade agreements are gradually improving the business environment for shipping and logistics. The potential for offshore oil and gas development further supports the chemical industry upstream. This combination of agricultural demand biofuel growth and infrastructure development positions Latin America as a growing market for chemical tankers.

COMPETITIVE LANDSCAPE

The competition in the Chemical Tankers Market is characterized by a mix of large integrated operators and smaller niche players vying for market share through service differentiation and operational efficiency. Leading companies compete on the basis of fleet age technical specifications and safety records to secure contracts with major chemical manufacturers. The market is moderately fragmented with several key players holding significant influence over pricing and availability. Competitive advantage is often derived from the ability to offer flexible logistics solutions and maintain high asset utilization rates. Regulatory compliance serves as a critical differentiator as operators with newer eco friendly fleets gain preference among environmentally conscious charterers. Price competition remains intense particularly for standard coated tonnage while specialized stainless steel vessels command premium rates due to limited supply. Strategic alliances and joint ventures are frequently employed to access new markets and share operational risks. The entry of new competitors is barriers by high capital requirements and strict regulatory standards. Overall the market rewards companies that can balance cost efficiency with high service quality and sustainability performance.

KEY MARKET PLAYERS

The major key players in the global chemical tankers market are

- Bahri

- Stolt-Nielsen

- Odfjell

- Navig8

- MOL Chemical Tankers

- Nordic Tankers

- Wilmar International

- MISC Berhad

- Team Tankers

- Iino Kaiun Kaisha

- Others

Top Players in the Market

- Stolt-Nielsen Limited is a global leader in the chemical tanker industry known for its extensive fleet and integrated logistics services. The company operates a diverse range of vessels including stainless steel and coated tankers to handle various chemical cargoes. Stolt-Nielsen contributes to the global market by providing reliable and safe transportation solutions for specialty chemicals and food grade liquids. Recently the company has focused on optimizing its fleet efficiency through digital technologies and sustainable practices. They have invested in new building programs to replace older tonnage with eco friendly vessels that meet stringent environmental regulations. Stolt-Nielsen also expands its terminal network to enhance supply chain integration and customer service. These strategic initiatives strengthen their competitive position and ensure long term growth in the evolving maritime sector while maintaining high safety and operational standards.

- Odfjell SE is a prominent international operator of chemical tankers with a strong commitment to safety and sustainability. The company manages a modern fleet capable of transporting a wide spectrum of liquid bulk chemicals across global trade routes. Odfjell plays a crucial role in the global market by offering specialized services for hazardous and sensitive cargoes. Recent actions include significant investments in dual fuel vessels powered by methanol and other alternative fuels to reduce carbon emissions. The company actively participates in industry collaborations to develop green shipping corridors and promote decarbonization. Odfjell also enhances its digital platforms to provide customers with real time visibility and improved logistical efficiency. Odfjell prioritizes environmental stewardship and technological innovation. This approach reinforces their reputation as a responsible, forward-thinking leader in chemical shipping.

- Navig8 Chemicals is a dynamic player in the global chemical tanker market known for its agile commercial operations and diverse fleet. The company focuses on providing flexible shipping solutions to meet the changing needs of chemical producers and traders. Navig8 contributes to the global market by leveraging its extensive network and market intelligence to optimize vessel deployment. Recent strategies include expanding its presence in key growth regions such as Asia and North America through strategic partnerships and chartering activities. The company invests in advanced analytics and trading tools to enhance decision making and risk management. Navig8 also emphasizes sustainability by incorporating energy efficient technologies into its operations and supporting the transition to cleaner fuels. These efforts enable Navig8 to capture market opportunities and deliver value to stakeholders in a competitive and rapidly changing environment.

Top Strategies Used by the Key Market Participants

Key players in the Chemical Tankers Market primarily focus on fleet modernization and sustainability to comply with evolving environmental regulations. Companies invest heavily in new build vessels equipped with energy efficient technologies and alternative fuel capabilities such as methanol or LNG dual fuel engines. Strategic acquisitions and mergers are common to expand geographic reach and diversify service offerings. Operators also prioritize digital transformation by implementing advanced data analytics and IoT solutions to optimize voyage planning and reduce operational costs. Long term charter agreements with major chemical producers provide revenue stability and mitigate market volatility. Additionally companies enhance their terminal infrastructure to offer integrated logistics solutions and improve customer retention. Sustainability reporting and adherence to ESG criteria are increasingly used to attract investment and meet client expectations. These strategies collectively help participants maintain competitiveness and adapt to the shifting dynamics of the global chemical trade landscape.

MARKET SEGMENTATION

This research report on the global chemical tankers market has been segmented and sub-segmented based on product, shipment route, and region.

By Product

- Organic

- Inorganic

- Vegetable oils & fats

By Fleet Type

- Inland

- Coastal

- Deep-sea

By Fleet Material

- Stainless Steel

- Coated

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are chemical tankers?

Chemical tankers are specialized ships designed to safely transport liquid chemicals in bulk across international waters.

2. What is the chemical tankers market?

The chemical tankers market includes ownership, operation, and chartering of vessels used to transport organic and inorganic chemicals.

3. What factors are driving growth of the chemical tankers market?

Growth is driven by increasing global chemical trade, expansion of petrochemical industries, and rising demand for specialty chemicals.

4. What types of chemicals are transported by chemical tankers?

Chemical tankers transport chemicals such as acids, alcohols, solvents, vegetable oils, and petrochemical products.

5. Which regions are major contributors to the chemical tankers market?

Asia Pacific, Europe, and North America are key regions due to strong chemical production and export activities.

6. How do safety regulations impact the chemical tankers market?

Strict international safety regulations increase demand for modern, compliant vessels and advanced safety systems.

7. What role does fleet modernization play in the market?

Fleet modernization improves fuel efficiency, environmental compliance, and cargo handling safety.

8. Who are the major end users of chemical tanker services?

Major end users include chemical manufacturers, petrochemical companies, and commodity trading firms.

9. What challenges affect the chemical tankers market?

Challenges include high capital investment, regulatory compliance costs, and fluctuating freight rates.

10. What is the future outlook for the chemical tankers market?

The market is expected to grow steadily due to expanding chemical production, trade globalization, and demand for safer transport solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com