Global Cloud Supply Chain Management Market Size, Share, Trends & Growth Forecast Report By Solution (Demand Planning & Forecasting, Inventory & Warehouse Management, Transportation Management, Order Management, Procurement & Sourcing, Others), Service (Training & Consulting, Support & Maintenance, Managed Services), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organization Size (Large Enterprises, SMEs), Industry Vertical, User Type, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2024 to 2033

Global Cloud Supply Chain Management Market Size

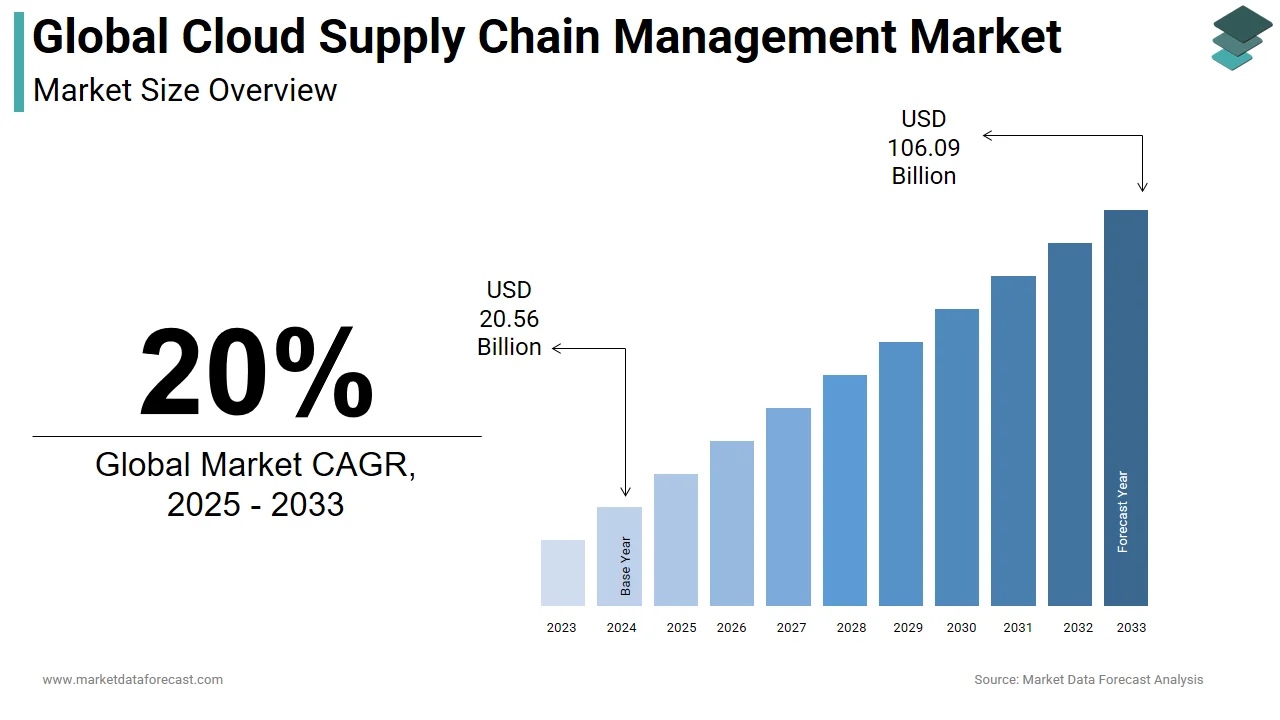

The global cloud supply chain management (SCM) market was valued at USD 20.56 billion in 2024 and is projected to reach USD 106.09 billion by 2033, growing at a CAGR of 20% from 2024 to 2033.

The increasing adoption of cloud-based services by various enterprises has digitized the supply chain industry. Organizations restructure their supply chain into a digital supply network that not only unites the physical flows of products and services but also provides affordable, efficient, and secure integration through redundant and endlessly scalable systems and easier integration with existing systems.

Increased investment in IoT, a revolutionary technology with promising potential for the supply chain, is expected to stimulate the market. Monitoring and supervision are the main areas of deployment of IoT in supply chain management. Technology allows warehouse and fleet managers to track their cargo and inventory. It helps with crucial features such as real-time location tracking and emergency forecast planning.

MARKET TRENDS

The retail industry faces the challenge of a sluggish economy, declining sales and store margins, and rising labor costs. Players, therefore, need tools that allow organizations to manage paper documents and manage more efficient structured and unstructured data to stay competitive. Thus, most of the key players are adopting cloud-based technologies to transform their supply chains with unprecedented visibility and vision of data. Technological integrations are aimed at understanding the customer journey and making substantial improvements.

Additionally, Buy Online and Store Pickup is a trend towards a breakthrough in the market in 2019 that has been adopted by several large retailers to increase the frequency of their stores. Walmart, the largest retailer in the US, has installed in-store collection towers and leveraged technologies, such as cloud computing software, mobile devices, and inventory and chain data-linked architectures that enable store websites and associates. Store-coordinated online ordering, store inventory, and cross-store shipping are stimulating the market.

Customer loyalty has become more important than before due to an increase in market players with the growth of electronic commerce. Cloud computing helps improve the customer experience by capturing and analyzing data from many sources, identifying patterns and forecasting needs, and providing on-demand services. It also enables retailers to access all commercial content from central business applications to provide fast responses and exceptional service to customers, setting them apart from their competitors.

MARKET DRIVERS

One of the main drivers in the global cloud supply chain management market is cost sustainability, which is linked to usage.

This is the best possible product management while offering a superior field of customization in online markets, giving the organization an advantageous position compared to its competitors. Plus, it's also the adaptability and coordination of multiple plans offering enhanced IT-based designs that help drive this all-inclusive market. At the same time, the viable oversight of information overload and information-related adaptability adds to certain imperative factors that decisively affect the market and spur overall growth.

MARKET RESTRAINTS

With each of these engines, there are also some limitations that pose challenges to cloud SCM market growth, such as the security associated with cloud applications. Security concerns include the dangers identified by pirated information or the confusion of information that structures a notable concern for the organization that uses these administrations. Another real restriction on the use of these frameworks would be reliance on focal access to verify the information along with the identified hazards, breaking down the entire framework, which also affects the market in general. The proactive idea of this innovation, which enables faster transport of item data, is likely to give this market opportunities in the coming years.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 20% |

| Segments Covered | By Solution, Service, Deployment Model, Organization Size, Industry Vertical, User Type, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | SAP SE, Infor Inc., Oracle Corporation, The Descartes Systems Group Inc., JDA Software Group Inc., Manhattan Associates Inc., Logility Inc., Kinaxis Inc., IBM Corporation, and Others. |

REGIONAL ANALYSIS

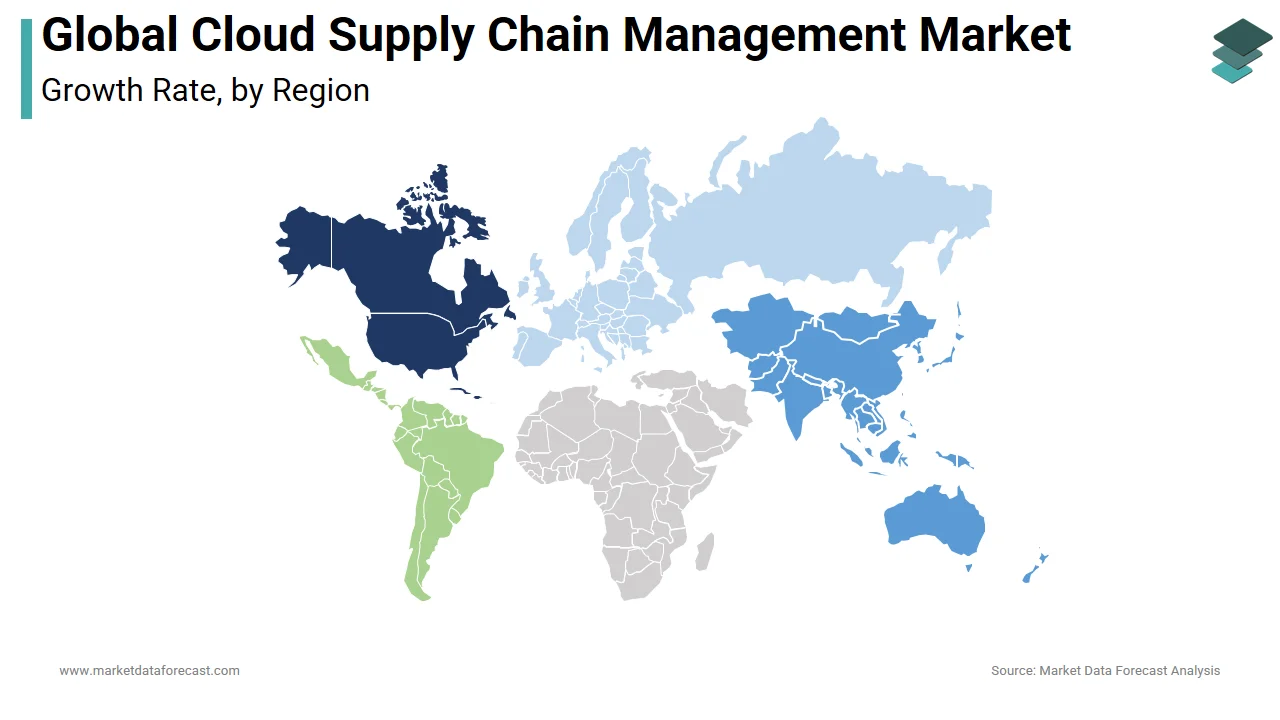

North America defines a remarkable portion of this market, followed by Europe, where the adequacy of costs coupled with innovative advances in supply chain supervision has shaped important objectives behind the growth of this market. Asia-Pacific borders one of the most rapidly developing regions, with China, India, and Japan among the nations contributing to growth. Developing an innovative progression in the monitoring of the store network and the growth of online personalization has been an imperative objective behind this growth in the APAC region.

KEY MARKET PLAYERS

Due to the growing demand for such solutions in the vertical sectors, many new players are entering this market. Some of the key players in the global cloud supply chain management market are SAP SE, Infor Inc., Oracle Corporation, The Descartes Systems Group Inc., JDA Software Group Inc., Manhattan Associates Inc., Logility Inc., Kinaxis Inc., and IBM Corporation.

RECENT MARKET HAPPENINGS

-

In June 2020, Infor, a leader in enterprise software in the cloud, will collaborate with the partner of the Elvenite alliance to offer a combination of modern technologies and successful and reliable implementations for food producers and grocery businesses in the Nordic region around Infor CloudSuite Food and Beverage. This will help food industry customers make smart decisions that enhance Infor's competitiveness.

-

In May 2020, Descartes Systems Group, one of the world leaders in the union of logistics intensive trade companies, announced that InnoAviation Limited, one of the leading service providers and rental of unit load devices (ULD), uses Descartes CORE ULD's tracking solution as part of its service to help airlines track critical shipments of personal protective equipment (PPE) related to COVID-19.

MARKET SEGMENTATION

This research report on the global cloud supply chain management market has been segmented and sub-segmented based on the solution, service, deployment model, organization size, industry vertical, user type, and region.

By Solution

- Demand Planning & Forecasting

- Inventory & Warehouse Management

- Transportation Management

- Order Management

- Procurement & Sourcing

- Sales & Operations Planning

- Product Life-Cycle Management

- Product Master Data Management

- Logistics Management

- Others

By Service

- Training & Consulting

- Support & Maintenance

- Managed Services

By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Industry Vertical

- Retail & Wholesale

- Manufacturing

- Healthcare & Life Sciences

- Food & Beverage

- Transportation & Logistics

- Automotive

- Oil & Gas

- Energy & Utilities

- Hospitality

- Government

- Others

By User Type

- Manufacturers

- Retailers

- Distributors

- Transporters

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What are the major challenges facing the Cloud Supply Chain Management Market?

Major challenges include data security and privacy concerns, integration issues with existing systems, the high initial cost of implementation, and the need for continuous updates and training. Additionally, resistance to change from traditional supply chain management practices can also be a barrier.

What role does Artificial Intelligence (AI) play in Cloud Supply Chain Management?

AI plays a significant role by providing predictive analytics for demand forecasting, optimizing inventory levels, enhancing decision-making processes, automating routine tasks, and improving overall supply chain efficiency. AI algorithms can analyze vast amounts of data to identify patterns and trends that help in strategic planning.

How do Cloud Supply Chain Management solutions enhance sustainability?

These solutions enhance sustainability by optimizing logistics and transportation routes to reduce fuel consumption, minimizing waste through better inventory management, enabling more efficient resource use, and facilitating the implementation of green supply chain practices. Real-time monitoring and analytics also help in tracking and reducing carbon footprints.

What future trends are expected in the Cloud Supply Chain Management Market?

Future trends include the integration of more advanced AI and machine learning capabilities, increased use of blockchain for transparency and security, greater focus on real-time analytics and IoT integration, and the expansion of SCM solutions tailored for specific industries. Additionally, there will be a growing emphasis on sustainability and ethical sourcing in supply chain operations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com