Global Combine Harvester Market Size, Share, Trends & Growth Forecast Report, Segmented By Product (Self-Propelled, Tractor Pulled And PTO Powered), Class (Class 4 And 5, Class 6, Class 7, Class 8 And Class 9 And 10), And By Region (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa), Industry Analysis From 2025 to 2033

Global Combine Harvester Market Size

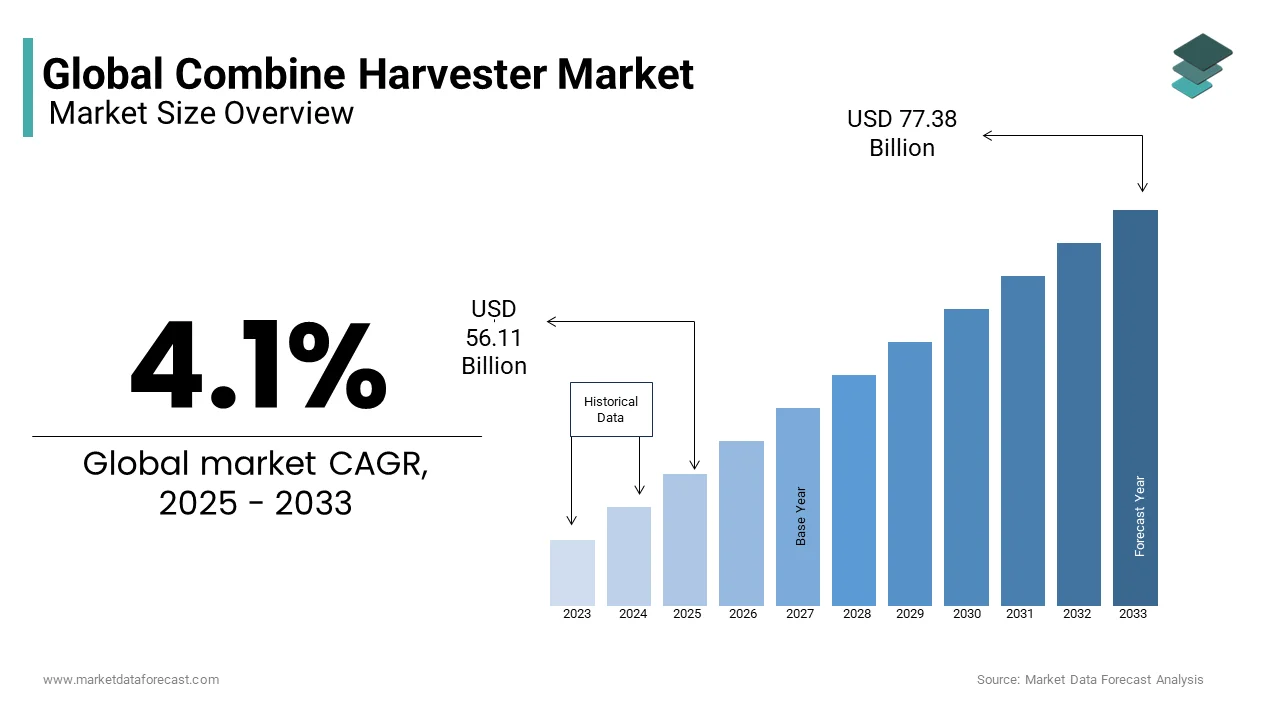

The global combined harvester market was valued at USD 53.90 billion in 2024 and is anticipated to reach USD 56.11 billion in 2025 from USD 77.38 billion by 2033, growing at a CAGR of 4.1% during the forecast period from 2025 to 2033.

A combine harvester is a self-propelled agricultural machine engineered to efficiently harvest a variety of grain crops by integrating three core operations: reaping, threshing, and winnowing into a single continuous process. Modern combines are equipped with advanced features such as GPS-guided auto steering, grain loss sensors, and real-time yield mapping capabilities that enhance field efficiency and reduce operator fatigue. These machines are indispensable in large-scale cereal production systems where timely harvesting is critical to prevent shattering, lodging, and post-harvest losses. Over 700 million hectares of cereal crops are harvested globally each year, with mechanization rates exceeding 90% in North America, Europe, and Australia.

MARKET DRIVERS

Expansion of Large-Scale Cereal Farming Drives Mechanization Demand

The global consolidation of farmland into larger operational units has intensified the need for high-capacity harvesting equipment to manage vast cereal acreages within narrow weather-dependent windows. The expansion of cereal farming is substantially to fuel the growth of the Combine Harvester Market. In Europe, farms exceeding 250 hectares now account for 58% of total arable land, up from 42% in 2010. This structural shift favors machinery with wide headers, high throughput, and rapid field mobility.

Labor Shortages in Rural Agriculture Accelerate Adoption of Harvesting Automation

The persistent and worsening shortages of seasonal agricultural labor have compelled farmers worldwide to substitute human labor with mechanical harvesting solutions, which is also propelling the growth of the Combine Harvester Market. Even in India, the National Sample Survey Office estimates a decline in agricultural wage laborers in Punjab and Haryana, where the country’s wheat heartland is prompting government subsidies for custom hiring centers offering combine services.

MARKET RESTRAINTS

High Initial Investment and Operating Costs Limit Accessibility for Smallholders

The new models, depending on capacity and technology features, require huge capital investments, where a lack of support is likely to hamper the growth of the combine harvester market. Therefore, the high capital investment and operating costs are limiting the growth of the Combine Harvester Market. Operating expenses further compound the challenge, with fuel maintenance and skilled operator requirements adding 15 to 25 US dollars per hour. Although custom hiring services exist in countries like China and Brazil, inconsistent availability and seasonal price spikes during peak harvest reduce reliability.

Limited Suitability for Diverse or Mixed Cropping Systems Constricts Versatility

The uniform monocultures of cereals such as wheat, rice, barley, and soybeans, which perform poorly in heterogeneous or intercropped fields common in developing regions, are another attribute degrading the growth of the combine harvester market. In Nigeria, maize is frequently intercropped with cowpea or cassava by creating height and maturity disparities that cause grain loss and machine blockage during combine operation. The rice fields often transition to vegetables or legumes within weeks by requiring rapid equipment reconfiguration that standard combines cannot support.

MARKET OPPORTUNITIES

Integration of Precision Agriculture Technologies Unlocks Data-Driven Harvesting

The modern harvesting systems are evolving into mobile data collection platforms that generate field-level insights for future agronomic decisions, with the sole to of creating new opportunities for the growth of the combine harvester market. Equipped with yield monitors, moisture sensors, and geospatial mapping tools, they enable variable rate management and harvest loss reduction at sub-field resolution. Similarly, grain loss sensors lowered header losses by up to 32% through automatic reel and cutter bar adjustments.

Growth of Custom Hiring and Shared Machinery Models Expands Market Access

The rise of machinery service cooperatives and digital rental platforms for small and medium-scale farmers who cannot afford ownership is also amplifying the growth of the combine harvester market. The custom hiring centers in India now serve over 35 million hectares annually, with combined usage growing at 12% per year. The Agrosmart platform connects equipment owners with nearby farms using AI-driven scheduling, increasing machine utilization from fifty to over 80% annually, as per Embrapa. These service-based models not only broaden market penetration but also optimize asset utilization by creating new revenue streams for equipment owners while enhancing timeliness and reducing post-harvest losses for end users.

MARKET CHALLENGES

Climate-Induced Harvest Window Compression Increases Operational Pressure

The rising climate volatility is shortening and destabilizing traditional harvest periods by demanding faster and more reliable harvesting capacity, which is one of the major challenges for the growth of the combine harvester market. The frequency of extreme rainfall events during autumn has increased by 28% in major grain belts since 2000. The wet conditions caused an estimated 4.2% yield loss in Midwestern corn from stalk lodging and ear rot.

Shortage of Skilled Technicians Hinders Maintenance and Uptime

The increasing complexity of modern combines that feature electrohydraulic systems, telematics, and automated controls has outpaced the availability of trained service personnel in many agricultural regions. This factor is also slowly declining the growth of the combine harvester market. In India, few mechanics nationwide are trained on advanced harvesting machinery despite over three hundred thousand combines in operation. This gap leads to prolonged downtime during peak season, with the International Rice Research Institute noting average repair delays of three to five days in Southeast Asia due to parts and expertise shortages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.1% |

| Segments Covered | By Product, Class, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AGCO, CLAAS, CNH Industrial, Deere & Company, Dewulf, Kubota Agricultural Machinery, Kuhn Group, Lely Group, Lovol Heavy Industry, Ploeger, Pottinger, Preet Group, SDF, Sampo Rosenlew, and Others. |

SEGMENT ANALYSIS

By Product Insights

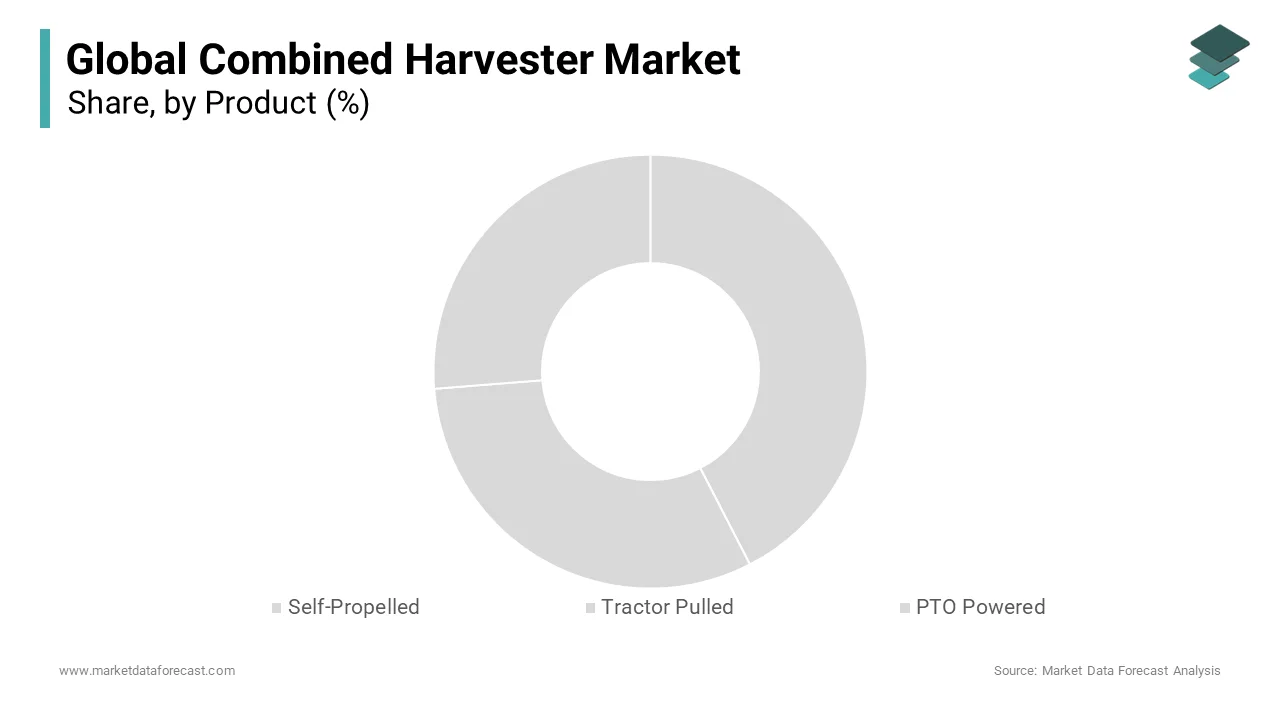

The self-propelled segment was the largest and held a dominant share of the combine harvester market in 2024. A single self-propelled combine can harvest 60 to 80 hectares of wheat per day, which is equivalent to the output of five tractor-pulled units requiring multiple operators and tractors. The farms using self-propelled combines achieve 22% lower labor cost per ton of grain compared to those relying on tractor-mounted systems. Furthermore, their integrated cab environments with climate control, suspension seats, and digital displays reduce operator fatigue during fourteen-hour harvest days.

The tractor-pulled combine segment is expected to grow at the fastest CAGR of 6.8% during the forecast period. Tractor-pulled combines offer a capital-efficient entry point for farmers who already own a medium-horsepower tractor and seek to mechanize harvesting without purchasing a dedicated machine. These systems enable mechanization without straining limited farm capital while allowing the same tractor to be used for tillage, planting, and transport.

By Class Insights

The class 7 segment was the largest by accounting for 31.2% of the combine harvester market share in 2024 due to its optimal balance of power capacity and maneuverability suited for mid to large-scale cereal farms across North America, Europe, and parts of South America.

In Germany, arable farms between 500 and 2000 hectares operate Class 7 units due to their ability to navigate moderately sized fields while maintaining high throughput. Class 7 models achieve the lowest cost per hectare for farms cultivating five hundred to fifteen hundred acres, which represents the majority of commercial operations in the Corn Belt and Northern Plains.

The Class 9 and 10 segment is deemed to grow at a CAGR of 7.4% throughout the forecast period. Over 35 million hectares of grain land with average field sizes exceeding five thousand hectares necessitate fleets of these high-capacity machines. The soybean mega farms in Mato Grosso operate 24-hour harvest shifts using Class 10 combines to avoid yield loss from delayed cutting during rainy periods.

REGIONAL ANALYSIS

North America Market Analysis

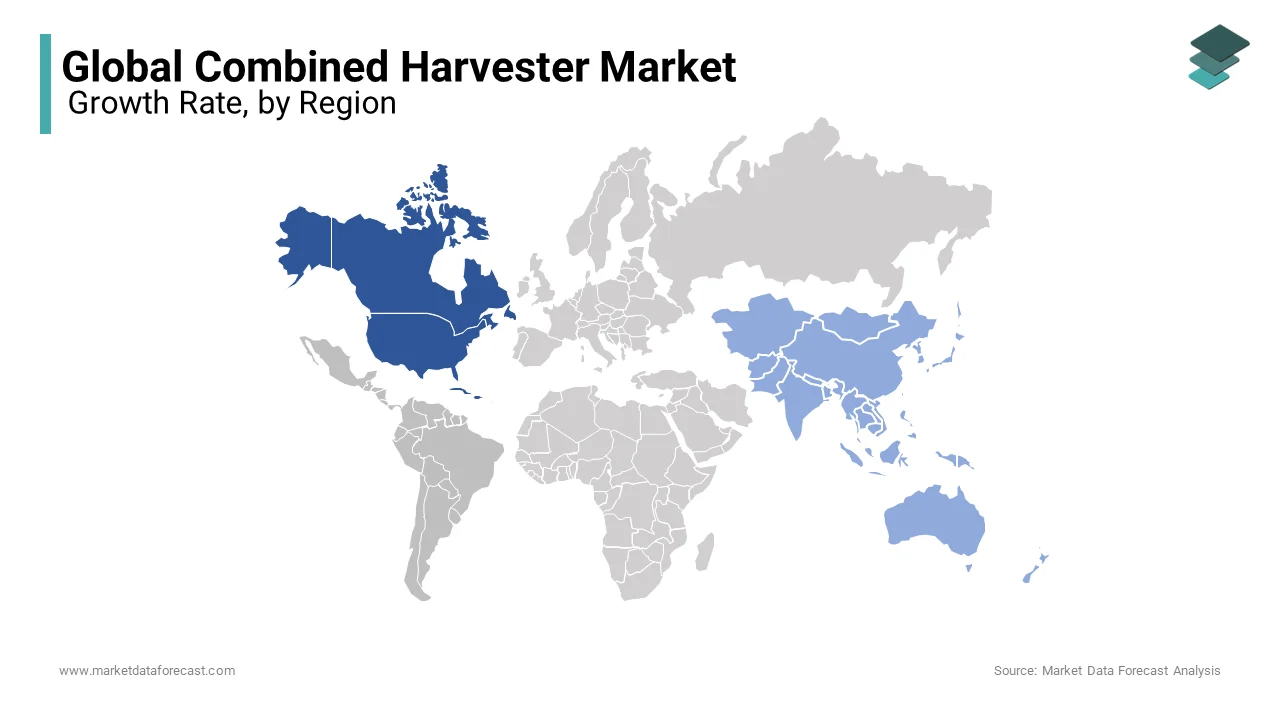

North America was the top performer of the combine harvester market by accounting for 34.2% of share in 2024. The United States alone harvests over 50 million hectares of corn, soybeans, and wheat annually, with over 95% mechanized operations in the Midwest and Great Plains routinely deploying Class 8 to 10 combines equipped with real-time yield mapping and auto unloading systems. Strong dealer networks and financing options from manufacturers like John Deere and CNH Industrial ensure rapid technology turnover.

Europe's combine harvester market was positioned second by capturing 21.2% of the share in 2024 consumption, with the diverse farm structures, stringent emissions regulations, and strong cooperative machinery sharing models. In Eastern Europe, Romania and Ukraine are transitioning from Soviet era equipment to modern self-propelled units as grain exports expand. The region’s blend of regulatory rules, farm diversity, and cooperative culture sustains steady demand for technologically compliant and versatile harvesting solutions.

Asia Pacific Market Analysis

Asia Pacific combine harvest market growth is anticipated to have a significant CAGR during the forecast period. IndiaSub-Mission on Agricultural Mechanization has subsidized over two hundred fifty thousand combine harvesters since 2,016, with custom hiring centers now serving 35 million hectares annually. Japan and South Korea are the main high-end contributors for hillside and oorcharombined with advanced hill descent control.

Latin America Market AnalyThe sis

Latin America combine harvester marketexpectedemed to grow with prominent growth opportunities in next coming years. Brazil and Argentina are the largest contributors in the combine harvester market. Government credit programs like Brazil’s Moderagro provide low-interest loans for machinery purchase, boosting new unit sales. Additionally, custom harvesting contractors known as “cosecheros” operate over 30,000 combines serving small and medium farms.

Middle East and Africa Market Analysis

The Middle East and Africa combine harvester market growth is having a steady pace in next coming years due to food security imperatives and irrigation-based cereal expansion. In Saudi Arabia, the domestic barley and sorghum production is carried out with high-capacity combines for desert agriculture.

COMPETITIVE LANDSCAPE

The combine harvester market is characterized by intense rivalry among a few global OEMs who compete on performance reliability, technological sophistication after-sales support rather than price alone. John D,eere CNH Indust,, rial and AGCO dominate the high-end segment with machines exceeding four hundred horsepower, while regional players like Kubota and Preet cater to smalsmall-medium-scalemers in Asia and Africa. Service infrastructure is another critical differentiator, as downtime during harvest can cost thousands of dollars per hour. Regulatory compliance, particularly regarding emissions and noise, levies technical barriers that favor established players with R and D scale.

KEY MARKET PLAYERS

A few of the market players in the global combine harvester market include

- AGCO

- CLAAS

- CNH Industrial

- Deere & Company

- Dewulf

- Kubota Agricultural Machinery

- Kuhn Group

- Lely Group

- Lovol Heavy Industry

- Ploeger

- Pottinger

- Preet Group

- SDF

- Sampo Rosenlew

MARKET SEGMENTATION

This research report on the global combined harvester market is segmented and sub-segmented into the following categories:

By Product

- Self-Propelled

- Tractor Pulled

- PTO Powered

By Class

- Class 4 and Class 5

- Class 6

- Class 7

- Class 8

- Class 9 and Class 10

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What’s driving growth in the combine harvester market in 2025?

AGCO, CLAAS, CNH Indusrial, Deere & Company, Dewulf, Kubota Agricultural Machinery, Kuhn Group, Lely Group, Lovol Heavy Industry, Ploeger, Pottinger, Preet Group, SDF, Sampo Rosenlew. Some of the market players dominating the global combine harvester market.

Which region dominates combine harvester sales?

Rising global food demand, labor shortages in farming, and government subsidies for mechanization—especially in Asia and Africa—are accelerating adoption.

Are farmers shifting to smart or autonomous harvesters?

North America and Europe lead in high-horsepower, tech-enabled models, while Asia-Pacific (led by India and China) is the fastest-growing market by unit volume due to smallholder farm consolidation.

How is climate change affecting harvester design?

Yes—GPS-guided auto-steer, yield mapping, and IoT-enabled diagnostics are now standard on mid-to-high-end models. Fully autonomous prototypes are being tested in the U.S. and EU but remain niche.

Why are used combine harvesters in high demand?

Manufacturers are building more versatile machines that handle wet harvests, uneven terrain, and mixed crops—critical as weather patterns become less predictable.

What’s the biggest challenge for harvester makers today?

High upfront costs ($300K–$700K for new models) push small and mid-sized farms toward certified pre-owned equipment—especially in Latin America and Southeast Asia.

Are electric or hybrid combine harvesters viable yet?

Supply chain volatility (especially for semiconductors and hydraulics) and tightening emissions regulations (EU Stage V, U.S. Tier 4 Final) are raising R&D and production costs.

How is farm size influencing harvester trends?

Not at scale—battery weight and field runtime remain barriers. However, John Deere, CNH, and Kubota are piloting hybrid-electric prototypes for 2027–2030 launch.

Which crops are boosting harvester sales?

Large farms favor high-throughput, 400+ HP models with 40+ ft headers, while small farms in emerging markets drive demand for compact, <150 HP harvesters with multi-crop capability (rice, wheat, soy).

What’s the outlook for 2026–2030?

Wheat, corn, and soy dominate, but rising rice mechanization in India, Bangladesh, and Nigeria is creating strong demand for specialized rice combine harvesters.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com