Global Commercial Aircraft Landing Gear Market Size, Share, Trends & Growth Forecast Report By Landing Gear Type, By Aircraft Type, By End User, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Commercial Aircraft Landing Gear Market Summary

Market Size & Growth

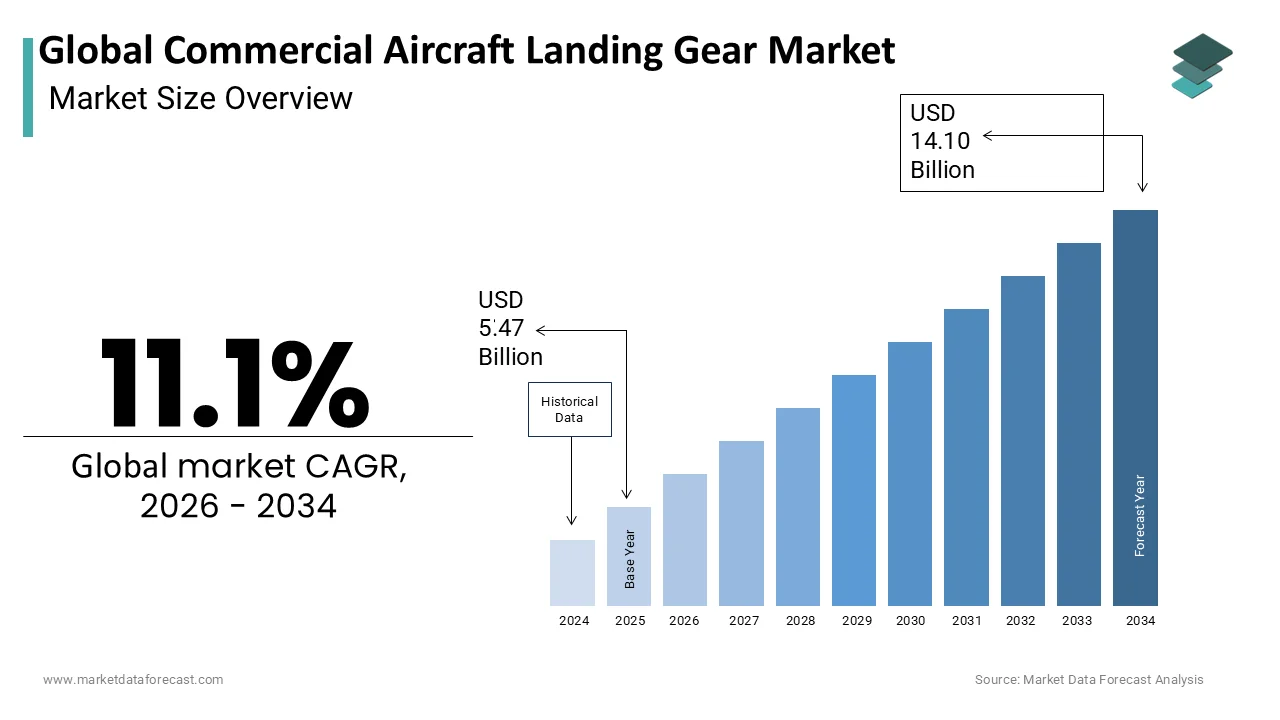

- The Global Aircraft Landing Gear Market was valued at USD 5.47 billion in 2025.

- Expected to reach USD 6.07 billion in 2026 and USD 14.10 billion by 2034, growing at a CAGR of 11.1% from 2026 to 2034.

- North America led the market in 2025; Asia Pacific is the fastest-growing region.

Key Market Segments

- By Landing Gear Type: Main Landing Gear (largest share in 2025), Nose Landing Gear (fastest CAGR of 6.8%, 2026–2034)

- By Aircraft Type: Narrowbody Aircraft (largest share in 2025), New-Generation Aircraft (fastest CAGR of 7.5%, 2026–2034)

- By End User: Aftermarket (largest share in 2025), Original Equipment Manufacturer (fastest CAGR of 6.2%, 2026–2034)

- By Geography: North America, Europe, Asia Pacific, Latin America, Middle East and Africa

Key Drivers

- Global air passenger traffic reached approximately 4.52 billion in 2025, with 2025 air travel demand up 5.3% year-over-year, per ICAO and IATA data.

- FAA-mandated Instructions for Continued Airworthiness require fixed-interval landing gear inspections and overhauls, sustaining steady aftermarket MRO demand.

- The global commercial airliner fleet is projected to expand more than 30% by 2030, per Oliver Wyman, directly increasing landing gear procurement and overhaul needs.

Key Players

Safran Landing Systems, Collins Aerospace (RTX Corporation), Liebherr-Aerospace, Héroux-Devtek Inc., Parker Hannifin Corporation, GKN Aerospace, Meggitt PLC (Parker Meggitt), CIRCOR Aerospace, Sumitomo Precision Products Co., Ltd., AAR Corp., Eaton Corporation plc, Honeywell International Inc.

Global Commercial Aircraft Landing Gear Market Size

The Global Aircraft Landing Gear Market is projected to grow from USD 5.47 billion in 2025 to USD 6.07 billion in 2026 and reach USD 14.10 billion by 2034, registering a CAGR of 11.1% during the forecast period from 2026 to 2034.

Commercial aircraft landing gear is the complete undercarriage system that supports the plane's weight on the ground, absorbs impact during touchdown, and enables steering and braking. These complex assemblies include struts, wheels, brakes, tires, and retraction mechanisms engineered to withstand immense kinetic energy and repetitive stress cycles. As global air travel rebounds, the operational intensity on these components has surged, necessitating robust engineering and frequent overhaul services. According to data from the International Civil Aviation Organization (ICAO), global passenger traffic surpassed pre-pandemic highs to reach approximately 4.52 billion, while IATA confirmed that 2025 air travel demand surged by 5.3%, intensifying aircraft utilization rates. The Federal Aviation Administration (FAA) enforces strict, manufacturer-defined Instructions for Continued Airworthiness (ICA) and Airworthiness Directives for landing gear components, guaranteeing steady aftermarket MRO demand. ACI Europe reveals that the European airport network welcomed a record 2.6 billion passengers in 2025, drastically increasing flight cycle counts for regional narrow-body fleets. Commercial aircraft operations subject shock absorbers and braking systems to persistent wear, with short-haul narrow-body variants executing up to 4 to 5 landing cycles daily. Oliver Wyman projects the global commercial airliner fleet to expand by over 30% by 2030, a trajectory that directly escalates landing gear procurement and overhaul. The shift towards heavier wide-body aircraft for long-haul routes further intensifies the technical requirements for landing gear systems, which must support higher maximum takeoff weights. This dynamic environment underscores the importance of advanced materials and precision engineering in sustaining safe and efficient aviation operations worldwide.

MARKET DRIVERS

Surging Global Air Passenger Traffic and Fleet Utilization

The exponential growth in global air passenger volumes is a primary driver of the commercial aircraft landing gear market. This compels airlines to increase fleet utilization and the frequency of flights. Higher utilization rates result in more landing cycles per aircraft, accelerating the wear and tear on landing gear components such as shock struts, bearings, and brake assemblies. The surge in traffic forces airlines to maximize the operational hours of each aircraft, leading to more frequent maintenance checks and component replacements. To ensure baseline structural safety, national civil aviation regulators mandate that aircraft landing gear undergo thorough overhauls based on flight cycles, ensuring steady revenue for certified MRO facilities. Additionally, the expansion of low-cost carriers in emerging markets has introduced newer fleets with high daily utilization profiles, further driving the need for durable and reliable landing gear solutions. The pressure to minimize ground time while maintaining safety standards prompts airlines to invest in advanced monitoring technologies and quick turnaround maintenance protocols. This operational intensity directly fuels the demand for both original equipment manufacturer supplies and aftermarket support, making fleet utilization a pivotal driver of market growth.

Strict Regulatory Mandates and Safety Compliance Requirements

Stringent regulatory frameworks and mandatory safety compliance standards also boost the expansion of the commercial aircraft landing gear market. This ensures continuous investment in high-quality components and maintenance services. Aviation authorities such as the Federal Aviation Administration and the European Union Aviation Safety Agency enforce rigorous certification processes for landing gear systems due to their critical role in aircraft safety. These regulations require airlines to adhere to fixed-interval inspections based on flight cycles or calendar time, regardless of visible wear, ensuring proactive maintenance. The regulatory pressure drives airlines and maintenance providers to source certified parts from approved manufacturers, limiting the use of unverified alternatives. Furthermore, the increasing age of the global fleet means that older aircraft require more frequent and extensive landing gear overhauls to remain compliant with current safety norms. The legal liability associated with non-compliance acts as a powerful motivator for airlines to prioritize high-quality landing gear solutions. Consequently, regulatory mandates ensure a stable and predictable demand for certified landing gear products and services, sustaining market growth through compulsory adherence to safety protocols.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Supply Chain Dynamics

The substantial capital investment required for manufacturing commercial aircraft landing gear and the complexity of its global supply chain restrict the growth of the global commercial aircraft landing gear market. Landing gear systems are among the most expensive components of an aircraft, often accounting for 3 to 5 percent of the total aircraft value, due to the use of specialized high-strength materials like titanium and ultra-high-strength steel. Aerospace supply chain monitors show that manufacturing backlogs for major structural forgings can extend production lead times for landing gear components past 18 months, impacting aircraft delivery schedules. This prolonged production cycle is exacerbated by the limited number of qualified suppliers capable of meeting stringent aerospace standards, resulting in a concentrated supply base. The high cost of raw materials and the energy-intensive forging processes further inflate production expenses, making it difficult for manufacturers to reduce prices. Additionally, the logistical challenges of transporting heavy and oversized landing gear components across international borders add to the overall cost and complexity. The reliance on single-source suppliers for critical subcomponents increases vulnerability to disruptions, whether from geopolitical tensions or natural disasters. High costs and logistical complexities continue to constrain the agility and profitability of the commercial aircraft landing gear market. This constraint will persist until manufacturing processes become more efficient and supply chains more resilient.

Technical Obsolescence and Integration Challenges with New Aircraft Designs

The rapid evolution of aircraft design and the introduction of new materials are significant technical constraints for the commercial aircraft landing gear market. This requires continuous adaptation and innovation. Modern aircraft such as the Boeing 787 and Airbus A350 utilize composite materials for fuselages and wings, which have different thermal and structural properties compared to traditional aluminum alloys. According to the Society of Automotive Engineers, integrating metallic landing gear systems with composite airframes requires specialized interface designs to prevent galvanic corrosion and manage stress distribution effectively. This incompatibility necessitates extensive research and development efforts, increasing the time and cost associated with certifying new landing gear systems. Furthermore, the trend towards lighter aircraft to improve fuel efficiency places greater demands on landing gear to maintain strength while reducing weight, pushing the limits of current material science. Retrofitting older fleets with updated landing gear is often economically unviable, leading to premature retirement of otherwise airworthy aircraft. These technical hurdles require manufacturers to constantly innovate, creating a barrier to entry for smaller players and slowing the widespread adoption of advanced landing gear technologies across the global fleet.

MARKET OPPORTUNITIES

Adoption of Additive Manufacturing and Advanced Materials

The integration of additive manufacturing and advanced lightweight materials presents a significant opportunity for the commercial aircraft landing gear market. This enhances performance and reduces production lead times. Traditional forging methods for landing gear components are time-consuming and material-intensive, whereas 3D printing allows for the creation of complex geometries with minimal waste. The weight reduction is crucial as airlines seek to lower operating costs and meet environmental targets. Also, the use of advanced composites and nanomaterials offers improved fatigue resistance and corrosion protection, extending the service life of landing gear parts. The European Union Aviation Safety Agency has started issuing guidelines for the certification of additively manufactured aerospace parts, facilitating broader adoption. Furthermore, additive manufacturing enables on-demand production of spare parts, reducing inventory costs and improving supply chain resilience. This technological advancement allows for rapid prototyping and customization, accelerating the development cycle for new aircraft programs. As the technology matures and costs decrease, the adoption of additive manufacturing will transform the landing gear supply chain. This transformation offers lucrative opportunities for market innovation and efficiency gains.

Expansion of Maintenance, Repair,r and Overhaul Services in Emerging Markets

The growing aviation sector in emerging countries provides a substantial opening for the expansion of maintenance, repair, and overhaul services for commercial aircraft landing gear, which is expected to accelerate the growth of the global market. Countries in Asia Pacific and the Middle East are experiencing rapid fleet growth, creating a heightened demand for localized MRO capabilities to reduce turnaround times and logistics costs. Airlines in these regions are increasingly partnering with global MRO providers to establish joint ventures and training centers, ensuring high-quality service standards. The aging global fleet also contributes to this opportunity, as older aircraft require more frequent and extensive landing gear overhauls. The International Civil Aviation Organization supports capacity-building initiatives in developing nations to enhance technical expertise and regulatory compliance. Furthermore, the rise of low-cost carriers in these markets, which operate high-utilization aircraft, creates a steady stream of recurring maintenance revenue. By establishing capacity-building, companies can offer faster service and competitive pricing, capturing a larger share of the growing aftermarket. This geographic expansion not only diversifies revenue streams but also strengthens customer relationships through improved service accessibility and responsiveness.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Raw Material Shortages

Supply chain vulnerabilities and shortages of critical raw materials are major challenges to the commercial aircraft landing gear market. This impacts production schedules and cost stability. The manufacturing of landing gear relies heavily on specialized alloys such as titanium and high-strength steel, which are subject to fluctuating global prices and availability. This volatility makes it difficult for manufacturers to maintain consistent pricing and profit margins. The concentration of suppliers for these specialized materials increases the risk of disruption; a high-severity issue at a single facility can ripple through the entire supply chain. Additionally, the energy-intensive nature of metal processing makes the industry susceptible to energy price fluctuations and regulatory changes related to carbon emissions. Mitigating these risks requires diversified sourcing strategies and long-term contracts, which may not always be feasible in energy-intensive industries. These vulnerabilities will continue to pose significant operational and financial challenges for landing gear manufacturers. This will remain true until supply chains become more resilient and raw material long-term stability stabilizes.

Skilled Labor Shortage in Specialized Manufacturing and Maintenance

An acute shortage of skilled labor in specialized manufacturing and maintenance roles further hinders the expansion of the commercial aircraft landing gear market. The production and overhaul of landing gear systems require highly trained engineers, metallurgists, and technicians with expertise in precision machining and non-destructive testing. This shortage leads to increased labor costs and longer turnaround times for both manufacturing and maintenance activities. As per the Federal Aviation Administration, the average age of certified aviation maintenance technicians is rising, with many nearing retirement and insufficient younger workers entering the field to replace them. The complexity of modern landing gear systems, which integrate advanced sensors and materials, demands continuous training and upskilling, which many organizations struggle to provide adequately. Additionally, the high-pressure environment and strict regulatory requirements can lead to burnout and high turnover rates among existing staff. Addressing this challenge requires coordinated efforts between industry stakeholders and educational institutions to develop targeted training pipelines. If high pressure or shortage is alleviated, the industry will face constraints in scaling production and maintaining high-quality service levels, impacting overall market efficiency and growth potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Landing Gear Type, Aircraft Type, End User, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America Europe Asia-Pacific Latin America Middle East & Africa |

| Market Leaders Profiled | Safran Landing Systems, Collins Aerospace (RTX Corporation), Liebherr-Aerospace, Héroux-Devtek Inc., Parker Hannifin Corporation, GKN Aerospace, Meggitt PLC (Parker Meggitt), CIRCOR Aerospace, Sumitomo Precision Products Co., Ltd., AAR Corp., Eaton Corporation plc, Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Landing Gear Type Insights

The main landing gear segment dominated the commercial aircraft landing gear market and accounted for a substantial share in 2025. This dominance of the segment was driven by its critical role in supporting the majority of the aircraft's weight and absorbing impact forces during landing. Also, this segment accounts for a significant share of the total landing gear value per aircraft because it consists of multiple complex assemblies, including struts, bogies, and braking systems that must withstand extreme stress. To combat structural fatigue cracks and runway debris corrosion, airframe manufacturers define strict inspection protocols in their Instructions for Continued Airworthiness (ICA), which national civil aviation regulators enforce through mandatory maintenance cycles. The higher frequency of maintenance events for the main gear compared to the nose gear further solidifies its market dominance. Airlines prioritize the reliability of main landing gear to prevent costly delays and ensure passenger safety, leading to consistent procurement of replacement parts and overhaul services. The structural integrity of the main landing gear is paramount for safe aircraft operation, making it the most heavily invested component in the landing gear ecosystem.

On the other hand, the nose landing gear segment is estimated to register the fastest CAGR of 6.8% from 2026 to 2034. This accelerated growth is propelled by the increasing integration of advanced steering mechanisms and sensor technologies into nose gear assemblies to enhance ground maneuverability and safety. The nose landing gear also houses critical avionics and radar equipment in many aircraft models, linking its growth to the broader trend of aircraft digitalization. Furthermore, the rising incidence of foreign object damage to nose gear tires and struts due to increased runway traffic necessitates more frequent replacements and repairs. The development of lightweight composite materials for nose gear doors and fairings also contributes to this growth as manufacturers seek to reduce overall aircraft weight. These technological advancements and operational requirements position the nose landing gear segment for rapid expansion in the coming years.

By Aircraft Type Insights

The narrowbody aircraft segment led the commercial aircraft landing gear market and captured a significant share in 2025. This leading position of the segment was attributed to the high volume of these aircraft in global fleets and their intensive daily utilization rates. Narrowbody aircraft such as the Airbus A320 family and Boeing 737 series constitute a notable share of the global commercial fleet. Narrowbody aircraft typically accumulate 3 to 5 flight cycles daily, creating a high-frequency landing environment that accelerates mechanical wear on structural components. The widespread adoption of narrowbody aircraft by low-cost carriers further amplifies this demand, as these airlines prioritize high asset utilization to maximize profitability. The standardized design of narrowbody landing gear allows for economies of scale in manufacturing and aftermarket services, making it a lucrative segment for low-cost suppliers. Additionally, the ongoing production of new-generation narrowbody aircraft ensures a steady stream of original equipment manufacturer orders. The combination of large fleet size and high operational intensity makes the narrowbody segment the primary driver of revenue in the commercial aircraft landing gear market.

However, the new-generation aircraft segment is anticipated to witness the fastest CAGR of 7.5% during the forecast period due to the recovery of long-haul international travel and the introduction of new heavy-lift aircraft models. Widebody aircraft such as the Boeing 787 and Airbus A350 feature larger and more complex landing gear systems capable of supporting higher maximum takeoff weights, which increases the value per unit. The retirement of older widebody models and their replacement with fuel-efficient variants also contributes to this growth, as new aircraft require state-of-the-art landing gear solutions. Furthermore, the increasing cargo capacity of widebody aircraft supports the growth of air freight, which demands robust landing gear capable of handling heavy payloads. These factors collectively propel the widebody segment to become the fastest-growing area in the market.

By End User Insights

In 2025, the aftermarket segment held the majority share of the commercial aircraft landing gear market because of the recurring nature of maintenance, repair, and overhaul activities required throughout the aircraft lifecycle. Landing gear components are subject to strict regulatory inspection intervals based on flight cycles or calendar time, ensuring a steady demand for aftermarket services regardless of new aircraft sales. Legal maintenance frameworks approved by the FAA require landing gear overhauls to match the manufacturer's strict calendar or flight-cycle limits, which typically occur every 8 to 12 years. Commercial aircraft registries show that the global active mainline fleet exceeds 29,000 units, with an expanding wave of mid-life airframes driving a surge in scheduled heavy maintenance spending. The aging global fleet further boosts this segment, as older aircraft require more frequent interventions to maintain airworthiness. Airlines and maintenance providers prioritize genuine parts and certified services to comply with safety regulations, sustaining high margins for aftermarket suppliers. Additionally, the trend towards extending the service life of existing aircraft rather than purchasing new ones enhances the importance of the aftermarket. The complexity of landing gear systems necessitates specialized expertise and equipment, creating high barriers to entry and reinforcing the dominance of established aftermarket players. This consistent and predictable demand stream makes the aftermarket segment the largest contributor to market revenue.

But the original equipment manufacturer segment is likely to experience the fastest CAGR of 6.2% between 2026 and 2034 owing to the resurgence of aircraft deliveries and the launch of new programs. Aviation manufacturing forecasts indicate a steady ramp-up in commercial aircraft production schedules as tier-one supply bottlenecks gradually resolve and demand for fuel-efficient models grows. Original equipment manufacturers require advanced landing gear systems that integrate with next-generation aircraft designs featuring composite materials and improved aerodynamics. The development of next-generation aircraft lines allows tier-one landing gear suppliers to secure multi-year OEM single-source production agreements. The backlog of orders for single-aisle aircraft remains strong, ensuring a steady pipeline of OEM business for the next decade. Furthermore, the development of urban air mobility vehicles and regional jets introduces new categories of landing gear requirements, expanding the addressable market. The strategic partnerships between airframers and landing gear manufacturers facilitate co-development of customized solutions, enhancing the competitive advantage of OEM suppliers. These dynamics position the OEM segment for robust growth as the aviation industry expands its fleet capacity.

COUNTRY LEVEL ANALYSIS

North America Commercial Aircraft Landing Gear Market Analysis

North America outperformed other regions in the global commercial aircraft landing gear market and accounted for a commanding share in 2025. The regional market shows a mature aviation infrastructure and the presence of major aerospace manufacturers. The region benefits from a large domestic fleet and high levels of air travel activity, driving consistent demand for landing gear maintenance and replacements. The FAA shows that the United States operates one of the largest passenger fleets globally, with thousands of mainline commercial aircraft maintaining scheduled cycles that demand routine landing gear overhauls. IATA reveals that North American carriers control approximately one-quarter of global air transport activity, driving intensive aircraft utilization and predictable landing gear component degradation. The presence of major maintenance, repair, and overhaul facilities in the United States reveals that Canada supports a robust aftermarket ecosystem. Government initiatives promoting aviation safety and infrastructure modernization further stimulate investment in landing gear upgrades. The region also serves as a hub for research and development, with universities and private firms collaborating onnext-generationn materials and designs. Strong regulatory frameworks enforced by the Federal Aviation Administration ensure high standards for landing gear performance and safety. These factors collectively sustain North America's leadership in the market, with ongoing innovations and a next-generation regulatory environment supporting continued growth and technological advancement.

Europe Commercial Aircraft Landing Gear Market Analysis

Europe maintains a significant share in the global commercial aircraft landing gear market because of a dense network of airports and stringent environmental and safety regulations. The region is home to major aircraft manufacturers such as Airbus, which influences landing gear design and procurement standards across the continent. Operational data from airline groups like Airlines for Europe (A4E) shows that fleet streamlining across European low-cost carriers significantly reduces supply chain friction for critical landing gear components. Traffic data from ACI Europe indicates that Europe handles more than 2 billion passengers annually, generating dense flight frequencies that place intense structural stress on narrow-body landing gear units. The European Green Deal imposes strict emissions targets, prompting airlines to adopt newer, more efficient aircraft that feature advanced lightweight landing gear technologies. Collaborative research initiatives funded by the European Commission focus on sustainable aviation technologies, including eeco-friendlymanufacturing processes for landing gear components. The presence of specialized suppliers in countries like France, Germany, and the United Kingdom strengthens the regional supply chain. Regulatory harmonization across member states simplifies compliance for manufacturer-friendly operators. These elements combine to create a sophisticated market that prioritizes innovation, sustainability, and safety, ensuring Europe remains a key player in the global landing gear industry.

Asia Pacific Commercial Aircraft Landing Gear Market Analysis

Asia Pacific is the fastest-growing region in the commercial aircraft landing gear market, fueled by rapid economic expansion and increasing air travel demand. Countries such as China, India, and Japan are investing heavily in airport infrastructure and fleet modernization to accommodate rising passenger numbers. IATA solidifies the Asia-Pacific region's position as the world's largest aviation market, driving massive forward procurement of new airframes and specialized landing assets. The Ministry of Civil Aviation in India highlights the widespread expansion of the domestic fleet under the RCS-UDAN scheme, a trend that commercial aviation operators directly tie to an increased demand for regional turboprop landing gear maintenance. Local manufacturing capabilities are strengthening, with joint ventures between international suppliers and domestic firms establishing production facilities in the region. The growing middle class and urbanization trends contribute to higher disposable incomes and increased travel frequency. Additionally, the rise of low-cost carriers in Southeast Asia intensifies aircraft utilization, accelerating landing gear wear and replacement cycles. Government support for aviation development and favorable regulatory environments further encourage market growth. These dynamics position Asia Pacific as a critical growth engine, offering substantial opportunities for landing gear manufacturers and service providers to expand their footprint.

Latin America Commercial Aircraft Landing Gear Market Analysis

Latin America grew steadily in the global commercial aircraft landing gear market due to gradual fleet modernization and increasing regional connectivity. The region relies heavily on narrowbody aircraft for domestic and intra-regional flights, which drives demand for standardized landing gear solutions. Year-end economic indicators from IATA demonstrate that Latin American carrier demand expanded at a double-digit rate, fueling continuous flight frequencies and landing gear wear. Brazil and Mexico are the largest markets in the region, with major airlines investing in fleet renewal programs that include new landing gear installations. The availability of financing for aircraft acquisitions is improving, enabling airlines to upgrade to newer models with advanced landing gear technologies. However, budgetary constraints and currency fluctuations pose challenges to the widespread adoption of premium services. Regional collaborations aim to harmonize safety standards and facilitate cross-border maintenance operations. The growing awareness of safety and efficiency is prompting airlines to prioritize certified landing gear components and professional overhaul services. While the market size is smaller compared to other regions, the growth potential is significant as economic stability improves and air travel becomes more accessible to the broader population.

Middle East and Africa Commercial Aircraft Landing Gear Market Analysis

The Middle East and Africa region holds a noteworthy position in the global commercial aircraft landing gear market owing to major hub developments and increasing long-haul connectivity. Gulf carriers operate some of the youngest and most advanced widebody fleets in the world, requiring state-of-the-art landing gear systems to support heavy payloads and long-distance flights. IATA shows that Middle Eastern hubs capture a substantial share of long-haul global transit connections, prompting heavy wide-body aircraft utilization. The Saudi Arabia GACA and UAE GCAA mandate stringent safety oversight, requiring regional MRO stations to adhere to strict inspection regimes for landing gear integrity. Also, the African Union’s Single African Air Transport Market framework aims to eliminate interstate regulatory barriers, an open-skies movement that regional carriers expect will trigger fleet expansions and local landing gear MRO demand. The region's focus on becoming a global aviation hub attracts investment in advanced maintenance facilities and training centers. The harsh environmental conditions, including high temperatures and sand, necessitate specialized landing gear materials and protective coatings, driving innovation in durability. Partnerships with international manufacturers facilitate technology transfer and local capacity building. The growth of air cargo operations also contributes to demand for robust landing gear solutions. These factors collectively support steady market growth, with a focus on reliability and performance in challenging operating environments.

COMPETITIVE LANDSCAPE

The competition in the commercial aircraft landing gear market is intense and characterized by a few dominant players with significant technological expertise. Major companies compete based on product reliability, innovation, and comprehensive after-sales support. The market sees continuous investment in advanced materials such as titanium alloys and composites to reduce weight and improve durability. Strategic partnerships with aircraft manufacturers are crucial for securing long-term supply contracts for new programs. Companies strive to differentiate themselves through digital maintenance solutions that offer predictive insights and reduce downtime. Price competition is moderate as quality and certification compliance take precedence over cost. Geographic expansion into emerging markets offers growth opportunities but requires adaptation to local regulatory standards. The high barriers to entry due to stringent safety regulations limit new competitors. Mergers and acquisitions are common strategies used to consolidate capabilities and expand product portfolios. Overall, the market landscape is shaped by a balance of technological leadership, regulatory adherence, and strategic agility among key participants who prioritize safety and efficiency.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Global Commercial Aircraft Landing Gear Market include

- Safran Landing Systems

- Collins Aerospace (RTX Corporation)

- Liebherr-Aerospace

- Héroux-Devtek Inc.

- Parker Hannifin Corporation

- GKN Aerospace

- Meggitt PLC (Parker Meggitt)

- CIRCOR Aerospace

- Sumitomo Precision Products Co., Ltd.

- AAR Corp.

- Eaton Corporation plc

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Safran Landing Systems is a global leader in the design and manufacture of integrated landing gear systems for commercial aircraft. The company provides comprehensive solutions including wheels, brakes, and steering mechanisms for major airframers such as Airbus and Boeing. Safran recently expanded its production capacity in North America to meet rising demand for narrowbody aircraft components. This strategic expansion ensures faster delivery times and enhanced support for airline customers. The company invests heavily in research and development to create lightweight materials that improve fuel efficiency. Safran also focuses on digital maintenance tools that predict component wear and optimize overhaul schedules. By integrating advanced sensors into landing gear assemblies, Safran enables real-time health monitoring. These innovations strengthen its position as a preferred partner for next-generation aircraft programs and sustainable aviation initiatives worldwide.

- Collins Aerospace delivers high-performance landing gear systems known for their reliability and durability in demanding operational environments. The company serves a broad range of commercial aircraft platforms with customized engineering solutions. Collins Aerospace recently launched a new electric braking system that reduces weight and maintenance requirements for modern fleets. This innovation aligns with industry trends towards electrification and sustainability. The company actively collaborates with airlines to develop tailored maintenance programs that minimize aircraft downtime. Collins Aerospace also enhances its supply chain resilience by diversifying sourcing strategies for critical raw materials. Its commitment to quality assurance and regulatory compliance ensures consistent performance across global operations. By leveraging advanced manufacturing techniques such as additive manufacturing, Collins Aerospace improves production efficiency. These efforts solidify its reputation as a trusted provider of critical aircraft systems and support long-term customer relationships.

- Héroux-Devtek specializes in the design and production of landing gear components for regional and commercial aircraft. The company offers a wide portfolio of products, including struts, actuators, and structural assemblies. Héroux-Devtek recently secured multiple contracts to supply landing gear systems for new regional jet programs. This achievement highlights its technical expertise and competitive pricing strategy. The company focuses on modular design approaches that simplify assembly and reduce lifecycle costs for operators. Héroux-Devtek also invests in automated manufacturing processes to enhance precision and consistency. Its global service network provides timely support and spare parts availability to customers worldwide. By prioritizing innovation and customer satisfaction,n Héroux-Devtek maintains a strong presence in niche market segments. The company continues to explore partnerships with emerging aircraft manufacturers to expand its reach. These strategic actions reinforce its role as a key contributor to the global landing gear ecosystem.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the commercial aircraft landing gear market primarily focus on technological innovation and strategic partnerships to maintain a competitive advantage. Companies invest heavily in research and development to create lightweight materials and advanced braking systems. These innovations enhance fuel efficiency and reduce maintenance costs for airlines. Strategic collaborations with airframers ensure early integration of landing gear designs into new aircraft programs. Expansion of global maintenance networks improves service accessibility and customer retention. Adoption of digital technologies such as predictive analytics optimizes component lifecycle management. Diversification of supply chains mitigates risks associated with raw material shortages. Emphasis on sustainability drives the development of eco-friendly manufacturing processes. These strategies collectively drive market growth and enhance the overall reliability of aviation infrastructure.

MARKET SEGMENTATION

This research report on the global commercial aircraft landing gear market is segmented and sub-segmented into the following categories.

By Landing Gear Type

- Main Landing Gear

- Nose Landing Gear

By Aircraft Type

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Aircraft

- Freighter Aircraft

By End User

- Original Equipment Manufacturer (OEM)

- Aftermarket

By Country

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is driving growth in the market?

Growth is being driven by air traffic expansion, airline fleet growth, demand for lightweight components, and the need for better fuel efficiency and operational performance.

2. Which aircraft segment leads the market?

Wide-body aircraft currently hold a strong market position, while regional jets are expected to grow the fastest.

3. Which region shows strong growth?

EMEA shows notable growth, supported by airline industry expansion in the region

4. What technologies are important in this market?

Important technologies include steering systems, actuation systems, and brake systems.

5. Why is weight reduction important?

Weight reduction helps improve fuel efficiency and maintain the ideal balance between payload and flight range.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com