Global Converged Infrastructure Market Size, Share, Trends, & Growth Forecast Report By Type (Certified Reference Systems & Integrated Infrastructure, Hyper Converged Systems and Integrated Platforms) and Regional - (2025 to 2033)

Global Converged Infrastructure Market Size

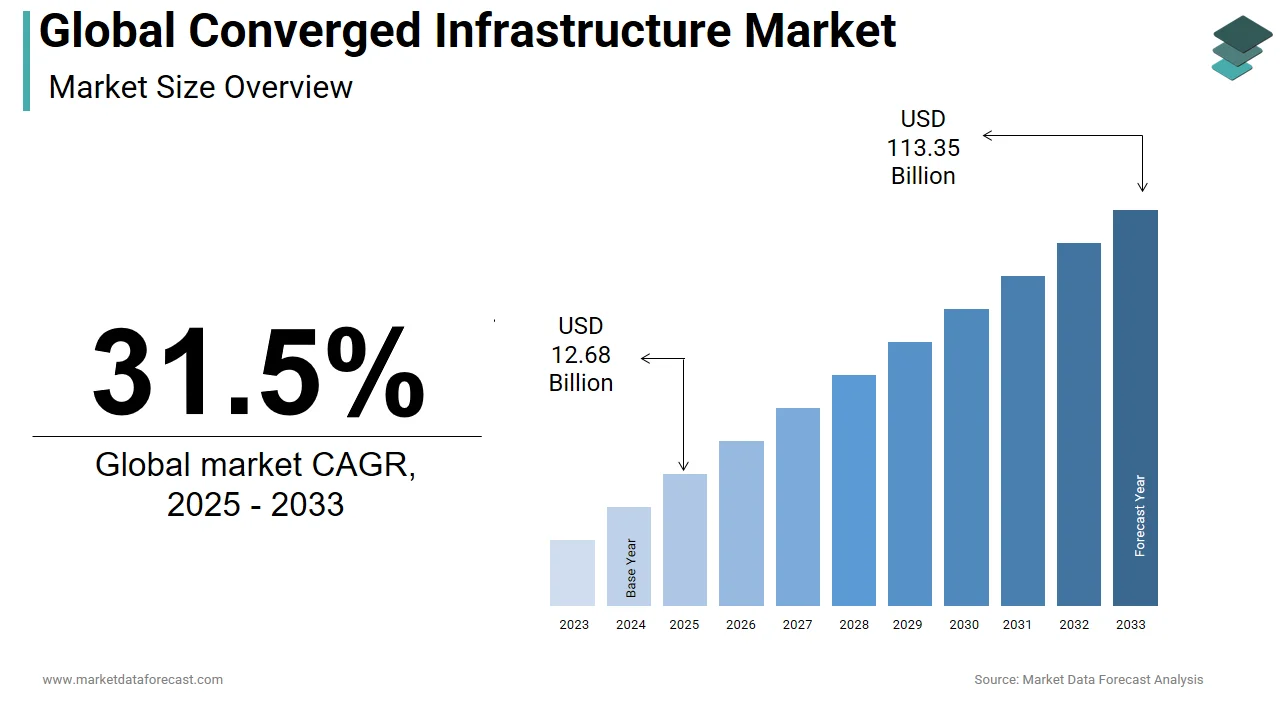

The size of the global converged infrastructure market was worth USD 9.64 billion in 2024. The global market is predicted to be worth USD 113.35 billion by 2033 from USD 12.68 billion in 2025, growing at a CAGR of 31.5% from 2025 to 2033.

The converged infrastructure market is growing rapidly as it lowers the total cost of operating an IT infrastructure and offers a high level of flexibility for businesses. Converged infrastructure has reduced the burden of implementing and managing networks, storage, servers, and other applications for data-driven businesses. Converged infrastructure solutions enable businesses to achieve agility and automation through the use of tightly coupled hardware and software products.

MARKET DRIVERS

The key driver for the development of the global converged infrastructure market is the escalating call to improve IT operational efficiency, improve data protection, and reduce the cost of IT and the aging of traditional data centers.

Another factor driving the converged infrastructure market is the cloud-based converged infrastructure solutions that provide ample opportunity for businesses. Converged infrastructure helps IT companies innovate by providing a simplified path to the cloud, where companies can experience and use a wide and growing range of innovation and specialized software and services. The rising need for an alternative solution to the cloud is one of the key reasons that will drive the growth in the size of the converged infrastructure market. However, they can face business risks and lose millions of dollars if their manufacturing plants have unplanned downtime.

Additionally, cloud platforms are susceptible to issues of higher latency, regulatory compliance, and data security. To overcome these issues, enterprises are adopting the converged system which not only meets regulatory compliance but also ensures low latency. These systems bring cloud-like flexibility to on-premises data centers and provide greater data security. The introduction of fast non-volatile memory or NVMe and Storage Class Memory (SCM) in these converged systems will boost the global converged infrastructure market during the outlook period. These storage devices benefit converged systems through optimal use of the storage infrastructure and the ability to modify software. NVMe takes advantage of the low internal latency parallelism inherent in flash storage devices. Likewise, SCM offers very fast performance with ultra-low latency.

The BFSI industry has registered the highest demand in the global converged infrastructure market in 2020, and this trend is expected to continue during the forecast period.

Since the financial sector is very influential in meeting the needs of its clients. With the rise of digitization, this sector has taken on the challenge of offering great digital experiences. Hence, the proliferation of quick digital transformation strategies presently consists of converged infrastructure to escalate the agility of your infrastructure. Additionally, finance companies are looking to HMI to increase agility and reduce costs for strategic initiatives such as IT distribution and remote / branch offices, virtual office deployment, mission-critical applications, and recovery after disaster. This is an important factor that is expected to drive the growth of the converged infrastructure market within the BFSI industry.

MARKET RESTRAINTS

High costs and lack of knowledge about converged infrastructure are restraining the market growth of the global converged infrastructure market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 31.5% |

| Segments Covered | By Type and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Cisco System Inc., Dell EMC, Hewlett-Packard Company, IBM Corporation, NetApp Inc., Oracle Corporation, Symantec, Teradata, VMware, Fujitsu, Hitachi Data Systems and Others. |

REGIONAL ANALYSIS

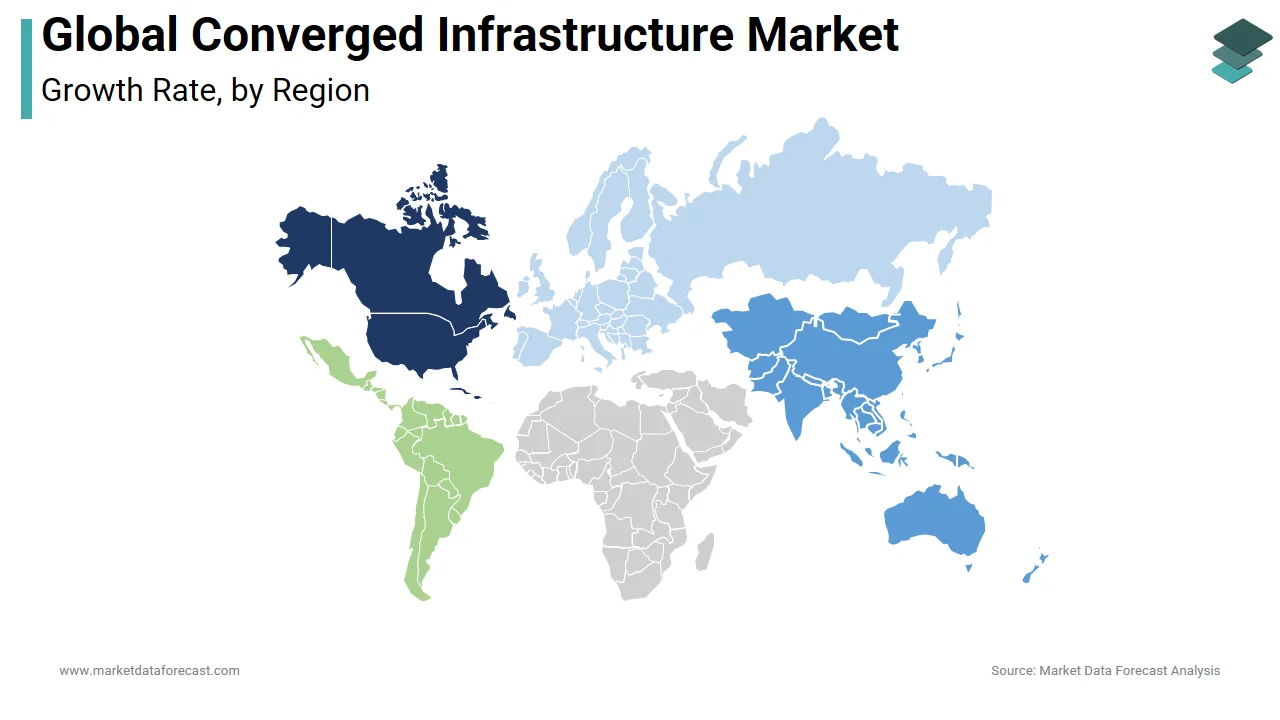

The converged infrastructure market in the Asia Pacific (APAC) is expected to grow at the highest CAGR due to increasing business workload. China, Japan, Australia, India and Singapore are expected to bring significant market share to the converged infrastructure market in the APAC region. Increased awareness of managing data through a common interface with a low total cost of ownership, increasing focus on VDI, server virtualization, and the popularity of using infrastructure-as-a-service solutions are among the main drivers of market growth from converged infrastructure to APAC.

China, Japan and India have great potential for global converged infrastructure suppliers due to the availability of a large proportion of end-user verticals, and favorable economic conditions when expanding services to these regions. The latest 4G tech intervention at APAC is one of the main reasons for the region's rapid digital transformation. This has led to developments in technologies, such as IoT, BYOD, and mobility services, opening up many revenue streams and use cases for businesses. 4G technology is in a development phase at APAC, driven by the large consumer base, favorable policies and rules, and rising calls for data storage and security. All these factors are considered drivers of the converged infrastructure market because of the quick digital transformation and the wide scope for growth.

KEY MARKET PLAYERS

Some of the key players in the global converged infrastructure market include Cisco System Inc., Dell EMC, Hewlett-Packard Company, IBM Corporation, NetApp Inc., Oracle Corporation, Symantec, Teradata, VMware, Fujitsu and Hitachi Data Systems.

RECENT MARKET HAPPENINGS

-

In August 2020, Nutanix launched clusters on AWS for hyper-converged infrastructure in the hybrid cloud. The main targeted use cases are the ability to lift and move workloads to the public cloud, especially in cloud explosion scenarios and disaster recovery uses.

-

In April 2019, NEC introduced a new highly efficient and easy-to-deploy hyperconverged infrastructure solution. NEC Corporation of America and NEC Enterprise Solutions (EMEA) announced a new hyper-converged infrastructure (HCI) solution powered by Scale Computing's HC3 software.

-

In April 2019, MemVerge launched the world's first converged memory infrastructure to power the most demanding workloads in business intelligence and data science and into the future. MemVerge, the inventor of Converged Memory Infrastructure (MCI), today stepped out of stealth and introduced the first system to break down the boundaries between memory and storage to power enterprise-centric workloads on the world's most demanding data.

MARKET SEGMENTATION

This research report on the global converged infrastructure market has been segmented and sub-segmented based on type and region.

By Type

- Certified Reference Systems & Integrated Infrastructure

- Hyper-Converged Systems

- Integrated Platforms

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

Which regions contribute significantly to the global converged infrastructure market share?

Major contributors to the global converged infrastructure market share include North America, Europe, Asia-Pacific, and the Middle East, each with its unique trends and adoption rates.

What factors are driving the growth of the global converged infrastructure market?

The growing demand for integrated and efficient IT solutions, data center modernization initiatives, and the adoption of cloud technologies are driving the growth of the converged infrastructure market.

What is the impact of the COVID-19 pandemic on the global converged infrastructure market?

The COVID-19 pandemic has accelerated the adoption of converged infrastructure solutions as organizations prioritize remote work capabilities, data center efficiency, and digital transformation efforts.

Who are the key players in the global converged infrastructure market?

Cisco System Inc., Dell EMC, Hewlett-Packard Company, IBM Corporation, NetApp Inc., Oracle Corporation, Symantec, Teradata, VMware, Fujitsu and Hitachi Data Systems are some of the major players in the converged infrastructure market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com