Global Cookware Market Size Share, Trends, and Growth Analysis Report, Segmented By Product (Core Cookware, Specialized Cookware, Accessories), Material, End User, Distribution Channel & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Cookware Market Summary

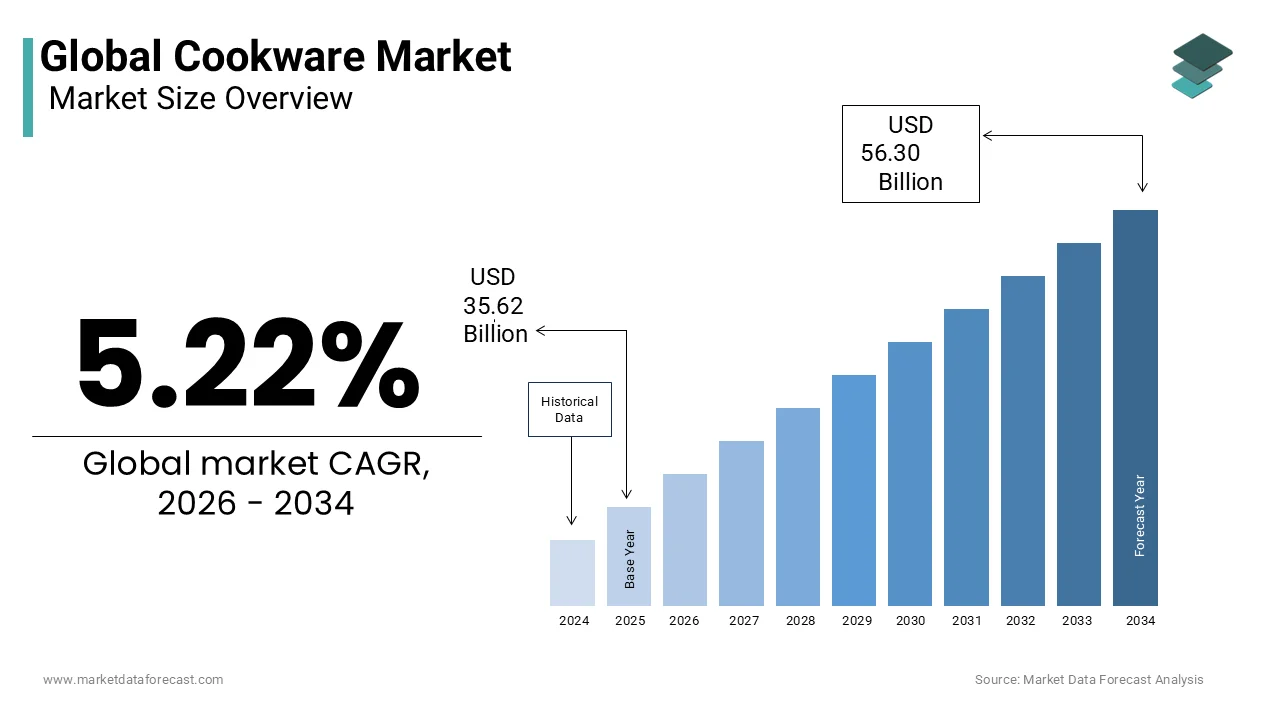

The global cookware market, valued at USD 35.62 billion in 2025, is projected to reach USD 56.30 billion by 2034 at a CAGR of 5.22%, driven by home cooking trends, health-conscious material shifts, and e-commerce expansion.

Market Snapshot

- 2025 Market Size: USD 35.62 billion

- 2026 Estimate: USD 37.48 billion

- 2034 Forecast: USD 56.30 billion

- CAGR (2026–2034): 5.22%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Sustained post-pandemic home cooking habits

- Rising consumer concern over PFAS and toxic coatings

- Growth of induction cooktops and smart kitchens

- Premiumization and aesthetic cookware branding

- Expansion of online and direct-to-consumer (DTC) sales

Principal Restraints

- High cost of premium and induction-compatible sets

- Environmental footprint of metal extraction and coatings

- Declining lifespan of some PFAS-free alternatives

- Inflation-driven reduction in discretionary spending

High-Value Opportunities

- Smart cookware with IoT temperature monitoring

- Induction-ready ferromagnetic designs

- PFAS-free ceramic and hybrid coatings

- DTC brand expansion in emerging markets

- Circular and recyclable cookware programs

Key Market Challenges

- Performance trade-offs in eco-friendly coatings

- Counterfeit cookware in price-sensitive markets

- Raw material price volatility (steel, aluminum, copper)

- Regulatory pressure on chemical coatings

Leading Players

Some of the companies that are playing a dominating role in the global cookware market include:

- Groupe SEB

- Meyer Corporation

- Zwilling J.A. Henckels

- Newell Brands

- Tramontina

- TTK Prestige

- Hawkins Cookers Limited

- Tefal

- All-Clad

Global Cookware Market Size

The global cookware market size was valued at USD 35.62 billion in 2025 and is anticipated to reach USD 37.48 billion in 2026 and USD 56.30 billion by 2034, growing at a CAGR of 5.22% during the forecast period from 2026 to 2034.

The cookware is a broad range of vessels and utensils designed for food preparation on stovetops, in ovens, or via induction heating, including pots, pans, kettles, and specialty cooking implements. Constructed from materials such as stainless steel, cast iron, aluminum, ceramic, and non-stick composites, cookware serves as an interface between heat sources and culinary outcomes. Its relevance extends beyond utility to health, energy efficiency, and cultural cooking practices. In developed economies, the shift toward home cooking post-pandemic has intensified demand for high-performance, durable, and non-toxic cookware.

MARKET DRIVERS

Rising Home Cooking Trends Post-Pandemic and Urbanization of Food Culture

The global resurgence in home cooking is propelling the growth of the cookware market. After the pandemic, consumers have retained the habit of preparing meals at home, driven by health awareness, cost sensitivity, and a growing interest in culinary experimentation. According to the Food Marketing Institute, 78% of U.S. households reported cooking more frequently at home in 2023 than in 2019, with millennials and Gen Z leading the trend through social media-driven food culture. Platforms like Instagram and TikTok have popularized techniques such as sous vide, stir-frying, and Dutch oven baking, increasing demand for specialized cookware.

Increasing Awareness of Food Safety and Toxicity in Cooking Surfaces

The growing consumer awareness about chemical leaching from low-quality cookware is additionally driving the growth of the cookware market. Traditional non-stick coatings containing perfluoroalkyl substances (PFAS) have come under scrutiny due to their potential health risks when overheated. According to the U.S. Centers for Disease Control and Prevention, PFAS chemicals are detectable in the blood of nearly 98% of Americans, raising concerns about long-term exposure from cookware and food packaging. In response, regulatory bodies such as the European Chemicals Agency have proposed restrictions on PFAS use, accelerating demand for safer alternatives like ceramic, hard-anodized aluminum, and pure stainless steel. A 2023 survey by the Consumer Reports National Research Center found that 64% of American consumers consider non-toxic materials a top factor when buying cookware. Companies like All-Clad and GreenPan have capitalized on this trend by introducing PFAS-free ceramic coatings and transparent material sourcing.

MARKET RESTRAINTS

High Cost of Premium and Technologically Advanced Cookware

The rising price of high-performance and multi-layered cookware is a significant barrier to mass-market adoption, particularly in developing economies, and is restricting the growth of the cookware market. Premium induction-compatible and non-toxic cookware sets often retail above $200, placing them beyond the reach of price-sensitive consumers. Even in developed markets, economic inflation has curtailed spending; the U.S. Bureau of Labor Statistics reported that consumer spending on household equipment declined by 3.2% in real terms in 2023 due to rising interest rates and cost-of-living pressures. Additionally, advanced materials like titanium-reinforced ceramic or copper-core composites require complex manufacturing, further inflating prices.

Environmental Impact of Cookware Production and Disposal

The environmental footprint of cookware manufacturing and end-of-life disposal presents a growing restraint on market sustainability. Similarly, non-stick coatings often contain fluoropolymers that are non-biodegradable and release toxic fumes when incinerated. According to the United Nations Environment Programme, only 12% of global metal waste is effectively recycled, with cookware rarely collected in municipal recycling streams due to composite materials and contamination. In landfills, these products can leach metals over time, posing ecological risks. While some brands have introduced take-back programs, such as Scanpan’s recycling initiative in Denmark, systemic challenges in material separation and consumer participation limit scalability. These environmental concerns are increasingly scrutinized by regulators and eco-conscious consumers, pressuring the industry to adopt circular design principles.

MARKET OPPORTUNITIES

Expansion of Smart and Induction-Ready Cookware for Modern Kitchens

The proliferation of induction cooktops and smart home ecosystems is unlocking a high-growth niche within the cookware market. Induction cooking, which uses electromagnetic fields to heat pots directly, requires ferromagnetic materials such as cast iron or magnetic stainless steel. According to the European Copper Institute, induction hobs accounted for over 50% of cooktop sales in Western Europe in 2023, driven by energy efficiency and safety advantages. This shift necessitates compatible cookware, creating demand for induction-optimized designs. Simultaneously, smart cookware embedded with temperature sensors and Bluetooth connectivity is emerging; June Life’s smart frying pan, for example, syncs with mobile apps to guide cooking precision. Brands like Samsung and T-fal are integrating IoT capabilities into pans and pots, offering real-time feedback and recipe automation, thereby transforming traditional kitchen tools into intelligent culinary assistants.

Growth of E-Commerce and Direct-to-Consumer Branding in Emerging Markets

The digital retail platforms are revolutionizing cookware distribution in regions with an underdeveloped brick-and-mortar retail infrastructure. In Southeast Asia, e-commerce sales of home and kitchen products grew by 38% year-on-year in 2023, as reported by Google, Temasek, and Bain & Company in their annual e-Conomy SEA report. Online marketplaces like Shopee and Amazon India enable global brands to reach urban consumers in Indonesia, Vietnam, and the Philippines without establishing physical stores. Direct-to-consumer (DTC) models, exemplified by U.S.-based Great Jones and Sweden’s Koenig, allow for agile branding, personalized marketing, and rapid feedback loops. In India, Nykaa Home and Flipkart experienced a 52% increase in premium cookware sales in 2023, which is driven by rising internet penetration and digital payment adoption.

MARKET CHALLENGES

Material Innovation vs. Performance Trade-Offs in Non-Stick and Eco-Friendly Coatings

The non-toxic and sustainable cookware is rising by achieving optimal performance without compromising safety or durability, which is restricting the growth of the cookware market. Ceramic and diamond-infused coatings, marketed as PFAS-free alternatives, often exhibit shorter lifespans than traditional PTFE-based non-stick surfaces. According to Consumer Reports testing in 2023, ceramic-coated pans lost non-stick performance after an average of 60 uses, compared to over 100 for high-end PTFE variants. Additionally, some eco-friendly composites lack thermal conductivity, leading to uneven heating and user dissatisfaction.

Counterfeit and Substandard Products in Price-Sensitive Markets

The growing threat from counterfeit and substandard products in online marketplaces and informal retail channels is hindering the growth of the global cookware market. These imitations often use inferior metals, false labeling, and hazardous coatings, posing health and safety risks. In 2023, India’s Bureau of Indian Standards conducted raids across 15 states and seized over 12,000 units of fake non-stick cookware containing banned chemicals, as reported by the Ministry of Consumer Affairs. Similarly, the UK’s Trading Standards confiscated counterfeit pans in 2022 that released toxic fumes when heated beyond 200°C. These products, often sold at 50–70% lower prices, undercut legitimate brands and erode consumer trust. The lack of standardized labeling and enforcement in developing markets exacerbates the issue.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material, End User, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Groupe SEB, Meyer Corporation, Zwilling J.A. Henckels, Newell Brands, Tramontina, TTK Prestige, Hawkins Cookers Limited, Calphalon, Fissler, All-Clad, Farberware, Scanpan, Tefal |

SEGMENTAL ANALYSIS

By Product Type Insights

The core segment was the largest by holding 62.3% of the cookware market share in 2025, with its universal necessity in daily food preparation across cultures and household types. The average household uses core cookware multiple times per day by emphasizing durability and versatility. According to the U.S. Department of Agriculture, over 85% of American meals are prepared at home, necessitating a functional set of primary cooking vessels.

The specialized segment is expected to grow with an expected CAGR of 9.3% from 2025 to 2033, with the increasing diversity of cooking techniques adopted globally, fueled by culinary media, cultural fusion, and appliance innovation. The global air fryer market, which reached 52 million units sold in 2023, as per Statista, has created demand for compatible cookware that withstands high heat and fits compact baskets. Similarly, the popularity of Asian cuisine has boosted wok sales; in the UK, Waitrose reported a 47% increase in wok purchases in 2023, attributing it to rising interest in stir-frying.

By Material Insights

The stainless steel segment was the largest by accounting for 38.2% of the cookware market share in 2025, with durability, corrosion resistance, and compatibility with all heat sources, including induction. The material’s inert nature prevents metallic leaching, aligning with consumer demand for food safety. According to the International Stainless Steel Forum, global stainless steel production reached 57 million metric tons in 2023, with a significant portion allocated to consumer durables. Brands like All-Clad and Cuisinart have popularized layered stainless steel across North America and Europe.

The ceramic and glass-based cookware segment is anticipated to witness a CAGR of 8.7% during the forecast period, with the rising consumer preference for non-toxic, PFAS-free alternatives to traditional non-stick coatings. Ceramic coatings, typically made from inorganic minerals like silica, do not release harmful fumes when overheated, unlike PTFE-based surfaces. The U.S. Environmental Protection Agency has flagged PFAS as persistent environmental pollutants, prompting a shift toward safer materials. A 2023 survey by the Consumer Reports National Research Center found that 61% of respondents actively avoided non-stick pans with synthetic coatings, favoring ceramic options.

By End User Insights

The residential segment held a prominent share of the cookware market in 2025. According to the United Nations, 56% of the world’s population lived in urban areas in 2023, with higher disposable incomes enabling spending on quality kitchenware. In China, the average household spent ¥1,200 ($170) annually on kitchen utensils in 2023, as reported by the National Bureau of Statistics, driven by rising middle-class aspirations. Millennials and Gen Z are investing in aesthetically pleasing, Instagram-worthy cookware, blending functionality with lifestyle branding. Brands like Caraway and Great Jones have capitalized on this trend with direct-to-consumer models by offering curated sets in designer colors.

By Distribution Channel Insights

The online segment is likely to grow with an expected CAGR of 10.2% during the forecast period, with the digital adoption, enhanced e-commerce logistics, and the appeal of direct-to-consumer (DTC) branding. In 2023, global e-commerce sales of home and kitchen products reached $184 billion, as reported by Statista, with cookware as a top-performing category. Platforms like Amazon, Flipkart, and JD.com offer extensive product comparisons, customer reviews, and fast delivery, reducing purchase friction. DTC brands such as Our Place and Field Company leverage social media and influencer marketing to build communities around their products, achieving higher margins and customer loyalty.

REGIONAL ANALYSIS

Asia Pacific Cookware Market Insights

Asia Pacific was the top performer of the global cookware market with a 39.3% share in 2025, with its vast population, rich culinary traditions, and rising urban middle class. China is the largest producer and consumer, manufacturing over 80% of the world’s non-stick cookware, according to the China Household Electrical Appliances Association. The region’s diverse cooking methods, such as wok-based stir-frying in China, tawa-based roti-making in India, and clay-pot cooking in Southeast Asia, fuel demand for specialized and multi-material products.

North America Cookware Market Insights

North America's cookware market held 24.3% of the market share in 2025, with the United States accounting for the vast majority. The region is characterized by high consumer awareness, strong brand loyalty, and a preference for premium, health-focused products. Americans spend an average of $240 per household annually on kitchen tools and cookware, according to the U.S. Bureau of Labor Statistics. The demand for non-toxic materials is particularly strong; a 2023 Consumer Reports survey found that 68% of U.S. shoppers prioritize PFAS-free labels when buying non-stick pans. Brands like All-Clad, Le Creuset, and GreenPan dominate through innovation in multi-ply construction and ceramic coatings. The rise of meal kits and home entertaining has also increased demand for versatile, aesthetically appealing cookware.

Europe Cookware Market Insights

Europe's cookware market growth is likely to grow with Germany, France, and the UK as primary markets. The region is at the forefront of sustainability and regulatory compliance, influencing material preferences and production standards. The European Chemicals Agency has proposed a restriction on PFAS use across all consumer products, expected to take effect by 2026, accelerating the shift to ceramic and stainless steel. Additionally, heritage brands like Le Creuset (France) and WMF (Germany) maintain strong cultural resonance, blending craftsmanship with modern functionality. Europe’s emphasis on durability, safety, and environmental responsibility shapes global trends in responsible cookware consumption.

Latin America Cookware Market Insights

Latin America cookware market growth is likely to be driven by the rising urbanization and a growing middle class seeking modern, durable kitchenware. Brazil and Mexico are major contributors to the cookware market in this region. Retail chains like Casas Bahia and Liverpool are expanding, offering installment plans that make premium sets accessible. Additionally, social media influence is reshaping preferences, with platforms like TikTok promoting international cooking styles that require specific tools.

Middle East & Africa Cookware Market Insights

The Middle East and Africa cookware market growth is likely to grow, with growth concentrated in the Gulf Cooperation Council and South Africa. Urbanization and economic diversification are transforming kitchen culture in the region. South Africa’s middle class is adopting Western-style cooking, with household spending on kitchen appliances rising by 9.3% in 2023, as reported by Statistics South Africa. The UAE has emerged as a hub for premium brands, with retailers like Debenhams and Home Centre offering high-end cookware lines. Additionally, the influx of expatriate populations has introduced diverse culinary practices, necessitating multi-functional tools.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global cookware market include

- Groupe SEB

- Meyer Corporation

- Zwilling J.A. Henckels

- Newell Brands

- Tramontina

- TTK Prestige

- Hawkins Cookers Limited

- Calphalon

- Fissler

- All-Clad

- Farberware

- Scanpan

- Tefal

Top Strategies Used By Key Market Participants

Key players in the cookware market are focusing on material innovation, digital engagement, and regional customization to strengthen their competitive edge. Companies are investing in non-toxic, PFAS-free coatings and multi-layered metal constructions to meet health and performance demands. Expansion into e-commerce and direct-to-consumer models enables greater brand control and customer insights. Sustainability initiatives, including recyclable packaging and energy-efficient manufacturing, align with regulatory and consumer expectations. Collaborations with chefs and influencers, along with interactive content and AR-based product visualization, are being leveraged to drive engagement and trust in an increasingly experience-driven purchasing landscape.

COMPETITION OVERVIEW

The cookware market is characterized by a dynamic interplay between global brands, regional manufacturers, and digitally native startups, creating a fragmented yet innovation-driven competitive environment. While legacy companies leverage heritage, R&D, and distribution scale, agile DTC brands are reshaping consumer expectations through design, storytelling, and sustainability. Competition is intensifying around material safety, particularly in non-stick technologies, where PFAS-free claims are becoming a battleground for trust. Geographic preferences—such as cast iron in North America, aluminum in India, and stainless steel in Europe—require tailored strategies. Premiumization and commoditization coexist, with high-end multi-ply sets competing alongside budget-friendly non-stick pans.

LEADING PLAYERS IN THE COOKWARE MARKET

All-Clad Metalcrafters

All-Clad has established a strong presence in the Asia Pacific market by positioning itself as a premium innovator in multi-ply bonded cookware. While historically dominant in North America, the brand has expanded its reach through high-end department stores and e-commerce platforms in Japan, South Korea, and Australia. In 2023, All-Clad introduced its D3 and D5 stainless steel collections via exclusive partnerships with luxury kitchen retailers in Tokyo and Seoul, emphasizing precision engineering and induction compatibility. The company also launched a digital education initiative in 2025, offering virtual cooking masterclasses in collaboration with celebrity chefs across Singapore and Hong Kong to build brand affinity. By aligning with affluent consumers seeking durable, professional-grade performance, All-Clad is leveraging its heritage in American craftsmanship to gain traction in Asia’s growing premium kitchenware segment, where functionality and prestige are increasingly intertwined.

Meyer Corporation

Meyer Corporation, a Hong Kong-based global leader in cookware manufacturing, plays a pivotal role in shaping the Asia Pacific market through localized innovation and extensive distribution. The company owns and operates multiple brands, including Anolon, Circulon, and Farberware, tailored to diverse consumer preferences across urban and rural markets. In 2023, Meyer launched Anolon Advanced Pro, a ceramic non-stick line designed for Asian cooking styles such as stir-frying and simmering, available across Southeast Asia and India. It also invested in a new R&D center in Shenzhen focused on induction-optimized and lightweight designs.

Tefal (Groupe SEB)

Tefal, a flagship brand of France’s Groupe SEB, maintains a significant footprint in the Asia Pacific region through its focus on accessible innovation and health-conscious design. The brand is widely recognized for pioneering non-stick cookware and continues to lead in the transition to safer, PFAS-free coatings. In 2023, Tefal launched its Initium and EasyCook lines in India and Indonesia, featuring Thermo-Spot heat indicators and reinforced ceramic interiors, targeting first-time homeowners and young professionals. In 2025, Tefal partnered with Flipkart and Shopee for exclusive product launches during regional shopping festivals, boosting visibility and sales velocity.

MARKET SEGMENTATION

This research report on the global cookware market is segmented and sub-segmented into the following categories.

By Product

- Core Cookware

- Specialized Cookware

- Accessories

By Material

- Stainless Steel

- Aluminium

- Cast Iron

- Carbon Steel

- Copper

- Ceramic/Glass

- Silicone

- Other Coated Substrates

By End User

- Residential

- Commercial

By Distribution Channel

- Offline Retail

- Online

- B2B/Direct Sales

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What are the main types of cookware?**

Key types include stainless steel, aluminum, cast iron, nonstick, ceramic, copper, and enameled cookware.

2. Which factors are driving the growth of the cookware market?

The factors that are driving the growth of the cookware market are rising urbanization and household formation, increasing popularity of home cooking and healthy lifestyles, growth of e-commerce platforms, and rising demand for premium and durable cookware

3. What challenges does the cookware market face?

The Challenges of the cookware market are Intense price competition from local brands, fluctuating raw material costs (steel, aluminum, copper), and Counterfeit and low-quality products in emerging markets

4. What is the role of nonstick cookware in the market?

Nonstick cookware is widely popular for convenience, ease of cleaning, and reduced oil usage, but faces scrutiny regarding the safety of coatings like PTFE and PFOA.

5. Which materials are most in demand?

Stainless steel and nonstick cookware dominate the market, while cast iron and ceramic are gaining traction among health-conscious consumers.

6. How does consumer lifestyle impact the cookware market?

Trends such as home cooking, kitchen remodeling, and interest in international cuisines increase demand for high-quality and diverse cookware sets.

7. Who are the major players in the cookware market?

Groupe SEB, Meyer Corporation, Zwilling J.A. Henckels, Newell Brands, Tramontina, TTK Prestige, Hawkins Cookers Limited, Calphalon, Fissler, All-Clad, Farberware, Scanpan, Tefal.

8. How has e-commerce impacted the cookware market?

Online platforms have expanded consumer access to global brands, boosted sales of premium cookware, and enabled direct-to-consumer models.

9. What innovations are trending in cookware?

Eco-friendly nonstick coatings (ceramic, water-based), Smart cookware with temperature sensors, and Lightweight, durable materials like anodized aluminum

10. How is the commercial cookware market different from household cookware?

Commercial cookware emphasizes durability, large-scale capacity, and heat resistance, while household cookware focuses on design, convenience, and versatility.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com