Global Courtesy Car Market Size, Share, Trends & Growth Forecast Report By Service Provider (Car Rental Companies, Independent Repair Garages, Dealerships / Franchise Garages, OEMs [Original Equipment Manufacturers]), Duration of Use (Long-term, Medium-term, Short-term), Usage Scenario (Accident Replacement, General Repair / Service, Scheduled Maintenance Support, Recall Campaigns), and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Market Size, 2025

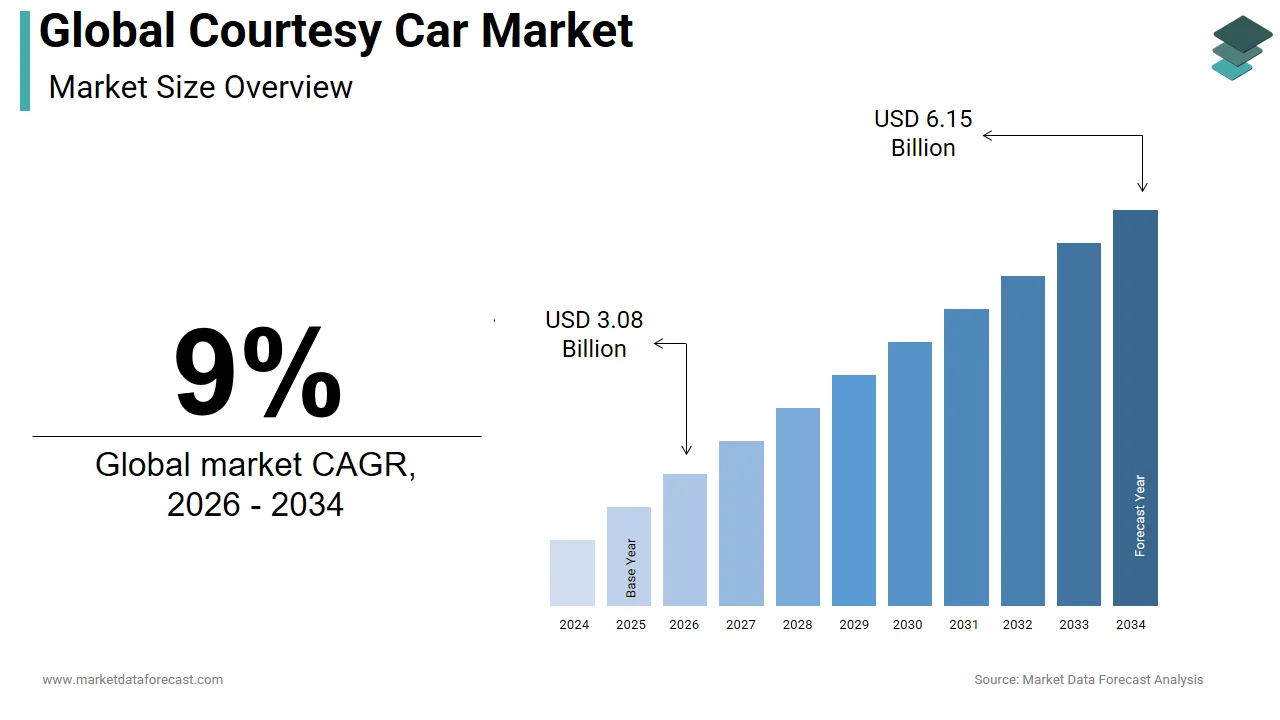

$2.83 BnMarket Estimate, 2026

$3.08 BnMarket Forecast, 2034

$6.15 BnCAGR, 2026–2034

9%Global Courtesy Car Market Summary

The global courtesy car market was valued at USD 2.83 billion in 2025, is estimated to reach USD 3.08 billion in 2026, and is projected to reach USD 6.15 billion by 2034, growing at a CAGR of 9% from 2026 to 2034. The market is driven by increasing customer expectations, rising frequency of vehicle recalls and repairs, and strategic integration of digital platforms and electric vehicles in courtesy car services.

Key Market Trends & Insights

- North America accounted for the largest market share in 2025.

- Asia Pacific is expected to expand at the fastest growth rate from 2026 to 2034.

- Dealerships and franchise garages segment held a significant market share of 45% in 2024.

- Based on duration, short-term use accounted for the largest share in 2025.

- Based on usage scenario, general repair/service segment accounted for the largest share in 2025.

Market Size & Forecast

- 2025 Market Size: USD 2.83 Billion

- 2026 Estimated Market Size: USD 3.08 Billion

- 2034 Projected Market Size: USD 6.15 Billion

- CAGR (2026 to 2034): 9%

- North America: Largest market in 2025

- Asia-Pacific: Fastest-growing market

Global Courtesy Car Market Size

The global courtesy car market was valued at USD 22.83 billion in 2025, is estimated to reach USD 3.08 billion in 2026, and is projected to reach USD 6.15 billion by 2034, growing at a CAGR of 9% from 2026 to 2034.

The Courtesy Car Market refers to the ecosystem of temporary vehicle provisions offered by automotive dealerships, insurance firms, and rental agencies to customers whose vehicles are undergoing repairs or are otherwise unavailable for use. These vehicles serve as a goodwill gesture or service recovery mechanism, ensuring customer convenience and retention during periods of vehicle downtime. As per insights from the Society of Motor Manufacturers and Traders, over 78% of consumers consider the availability of a courtesy vehicle as a significant factor influencing their choice of auto repair centers. Furthermore, insurance providers in developed markets have increasingly adopted the inclusion of courtesy car coverage as a standard or optional add-on within comprehensive motor insurance plans. The market spans both luxury and economy segments, with offerings ranging from compact cars to premium sedans, depending on the provider and client agreement. According to data from the European Automobile Manufacturers' Association, approximately 62% of all authorized service centers across Europe offer some form of courtesy vehicle program, reflecting the growing integration of such services within post-sales support frameworks. This trend is also mirrored in emerging economies where rising consumer expectations and increasing vehicle ownership are driving service providers to adopt similar practices.

MARKET DRIVERS

Enhanced Customer Experience Demand

A primary driver of the Courtesy Car Market is the escalating demand for enhanced customer experience in the automotive after-sales domain. In today's competitive landscape, customer satisfaction directly correlates with brand loyalty, prompting service providers to extend value-added services such as temporary vehicle usage. As per findings published by J.D. Power, over 81% of vehicle owners who received a courtesy car during service reported higher satisfaction levels compared to those who did not. Additionally, the American Customer Satisfaction Index noted that dealerships offering courtesy vehicles witnessed a 23% increase in repeat customer visits over two years. This behavioral shift underscores how integral these services have become in maintaining long-term client relationships. Insurance companies, too, leverage courtesy vehicles as part of claims management strategies, particularly in regions like North America and Western Europe where policyholders increasingly expect seamless mobility solutions post-accident. The Insurance Information Institute states that nearly 45% of comprehensive auto insurance policies in the U.S. now include optional or bundled courtesy car benefits, further fueling market growth.

Vehicle Recall and Warranty Claim Frequency

Another influential driver is the rising frequency of vehicle recalls and extended warranty claims, necessitating prolonged periods of vehicle unavailability. As per data from the National Highway Traffic Safety Administration, over 24 million vehicles were recalled in the United States alone in 2023, marking a 32% increase from the previous year. This surge in recalls, primarily due to software glitches and component defects, has led to an uptick in the need for temporary mobility solutions. Automakers and dealerships are responding by expanding their in-house fleet of courtesy vehicles to manage customer expectations and maintain operational efficiency. A study conducted by the Automotive Aftermarket Industry Association revealed that dealerships with structured courtesy car programs reported a 17% improvement in service turnaround perception among customers. Moreover, original equipment manufacturers are integrating courtesy vehicle logistics into their recall management protocols to ensure minimal disruption. For instance, Tesla's mobile service units and loaner vehicle programs have been instrumental in mitigating customer inconvenience during software updates or hardware replacements. This proactive approach not only enhances brand reputation but also drives the demand for temporary vehicle provisioning across global markets.

MARKET RESTRAINTS

Fleet Maintenance and Insurance Cost Burden

One of the principal restraints affecting the Courtesy Car Market is the escalating cost burden associated with fleet maintenance and insurance liabilities. Service providers and insurers are confronted with rising overheads due to vehicle depreciation, fuel expenses, and administrative costs linked to managing temporary vehicle allocations. According to the National Automobile Dealers Association, the average annual cost of maintaining a courtesy vehicle fleet has increased by 28% over the past three years, largely driven by rising fuel prices and supply chain disruptions affecting spare parts availability. Furthermore, insurance premiums for courtesy vehicles have surged as insurers face higher liability risks, particularly in urban areas where accident rates are elevated. The Insurance Institute for Highway Safety reported that courtesy vehicles are involved in accidents at a rate 15% higher than privately owned vehicles, contributing to increased claims and litigation exposure. These financial pressures are prompting some smaller dealerships to either reduce or eliminate their courtesy vehicle offerings, particularly in price-sensitive markets. Additionally, regulatory compliance costs related to vehicle safety inspections and emissions standards further strain operational budgets, limiting scalability and constraining market expansion, especially among independent service providers.

Vehicle and Driver Shortage Constraints

Another significant restraint is the shortage of available vehicles and qualified drivers, which has intensified in the post-pandemic era. The global semiconductor shortage and supply chain bottlenecks have led to a marked decline in new vehicle inventory, affecting the availability of cars for temporary allocation. As per data from IHS Markit, global light vehicle production declined by 9.2% in 2023 compared to pre-pandemic levels, directly impacting dealership inventories. Concurrently, the rental and leasing sector, which often supplies vehicles to courtesy car programs, has faced its own inventory constraints. The American Rental Association indicated that rental car availability dropped by 18% in major metropolitan areas between 2022 and 2023. Compounding this issue is the driver shortage, particularly in regions like North America and parts of Europe, where labor market disruptions have reduced the pool of available chauffeurs or delivery personnel for vehicle handover processes. This constraint is especially critical for insurance-based courtesy programs that rely on on-demand vehicle delivery. Consequently, service delays and limited vehicle options have led to declining customer satisfaction, as reported by the Consumer Reports Auto Survey, which found that 34% of respondents expressed dissatisfaction with courtesy vehicle availability during recent service visits.

MARKET OPPORTUNITIES

Digital Platform Integration and Mobility-as-a-Service

An emerging opportunity within the Courtesy Car Market lies in the integration of digital platforms and mobility-as-a-service (MaaS) models. Digitalization enables service providers to streamline vehicle allocation, track usage, and enhance customer communication through mobile apps and cloud-based systems. According to McKinsey & Company, over 60% of automotive service providers globally are investing in digital transformation initiatives, with a significant focus on integrating mobility solutions into their existing service ecosystems. This shift allows for real-time vehicle tracking, automated booking systems, and dynamic fleet management, significantly improving operational efficiency. Furthermore, partnerships with ride-hailing and car-sharing platforms offer scalable alternatives to traditional courtesy vehicle models. For example, several European insurers have begun collaborating with companies like Uber and Bolt to provide ride credits as an alternative to physical vehicle loans. The International Transport Forum reported that such digital mobility integrations can reduce service delivery costs by up to 25% while improving customer convenience. This trend is particularly prominent in urban markets where vehicle ownership is declining in favor of shared mobility solutions, presenting a lucrative avenue for market players to diversify their offerings and cater to evolving consumer preferences.

Electric Vehicle Adoption and Sustainability Focus

Another key opportunity stems from the growing emphasis on sustainability and the adoption of electric vehicles (EVs) within courtesy fleets. As governments worldwide implement stricter emissions regulations and incentivize green transportation, service providers are increasingly transitioning to electric or hybrid courtesy vehicles. The International Energy Agency reported that global electric car sales surpassed 14 million units in 2023, marking a 35% year-on-year increase, which is encouraging automotive stakeholders to align their service offerings with environmental goals. Dealerships and insurers are leveraging this trend by introducing eco-friendly courtesy vehicles as part of their corporate social responsibility initiatives. For instance, BMW and Mercedes-Benz have begun deploying electric courtesy cars in select European markets, with early data from the European Environment Agency indicating a 20% improvement in customer perception scores among environmentally conscious consumers. Additionally, the lower maintenance and fuel costs associated with EVs offer long-term economic benefits. BloombergNEF estimates that the total cost of ownership for electric vehicles is expected to reach parity with internal combustion engine vehicles by 2026, making them a financially viable option for expanding courtesy fleets sustainably.

MARKET CHALLENGES

Regulatory Compliance Complexity

A major challenge confronting the Courtesy Car Market is the complexity of regulatory compliance across different jurisdictions. Varying laws related to vehicle safety standards, insurance coverage, and cross-border usage create operational hurdles for providers operating in multi-regional markets. For example, the European Union mandates that all courtesy vehicles must undergo periodic technical inspections and meet specific emissions criteria, while certain U.S. states require separate insurance policies for temporary vehicle usage. The World Bank's Logistics Performance Index highlights that regulatory inconsistencies contribute to a 12% increase in logistics and administrative costs for cross-border vehicle movements. Additionally, liability issues become more pronounced when courtesy vehicles are used in regions with differing traffic laws or insurance frameworks. In countries like India and Brazil, where regulatory frameworks are still evolving, service providers often face ambiguity in defining responsibility during accidents or vehicle misuse. The International Association of Automotive Manufacturers has noted that inconsistent enforcement of vehicle safety norms leads to increased compliance risks, particularly for multinational dealerships. Such regulatory fragmentation not only raises operational costs but also limits the scalability of courtesy vehicle programs in emerging markets, thereby constraining market growth.

Cybersecurity Risks in Connected Vehicles

Another significant challenge is the heightened cybersecurity risk associated with connected courtesy vehicles. As modern vehicles are increasingly equipped with telematics systems, infotainment interfaces, and remote diagnostic capabilities, they become vulnerable to data breaches and cyberattacks. According to a report by KPMG, over 67% of automotive service providers have reported at least one cybersecurity incident related to their courtesy vehicle fleets in the past two years. These incidents range from unauthorized access to customer data to remote manipulation of vehicle functions. The rise in connected vehicle technologies has also expanded the attack surface, with hackers targeting vehicle communication systems to gain control over navigation, braking, or engine functions. The Center for Automotive Research states that the average modern vehicle contains over 100 million lines of code, creating numerous entry points for malicious actors. Furthermore, the lack of standardized cybersecurity protocols across manufacturers and service providers exacerbates the issue. In 2023, the National Institute of Standards and Technology emphasized the urgent need for unified cybersecurity frameworks to protect connected vehicle ecosystems. As courtesy vehicles often change hands multiple times and operate outside secure environments, ensuring consistent data protection becomes a logistical and technological challenge, deterring some providers from expanding their digital service offerings.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service Provider, Duration of Use, Usage Scenario, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Enterprise Mobility (Enterprise Rent-A-Car, Alamo, National), Hertz Global Holdings, Europcar Mobility Group, Accident Courtesy Car (ACC), Marigold Services Ltd, Vehicle Replacement Group, Cogent Hire, QuestGates, Cooper Solutions (FullCover), RowlyGO, and Co-Wheels. |

SEGMENTAL ANALYSIS

By Service Provider Insights

Dealerships and franchise garages segment represent the dominant force in the global courtesy car market, commanding approximately 45% of the total market share according to industry analysis from Frost & Sullivan. This segment's supremacy stems from their strategic positioning within the automotive ecosystem and their direct relationship with vehicle manufacturers. The primary driver behind this dominance is the comprehensive after-sales service integration that dealerships offer as part of their customer retention strategies. As per data from the National Automobile Dealers Association, over 89% of franchised dealerships in North America provide courtesy vehicles as standard service offerings, significantly higher than independent garages or rental companies. This widespread adoption is fueled by manufacturers' mandates that require dealers to maintain customer satisfaction metrics above 85%, with courtesy vehicles being a critical component in achieving these benchmarks. The financial backing and infrastructure support from OEMs enable dealerships to maintain larger and more diverse courtesy vehicle fleets compared to independent operators.

The second major factor propelling dealership dominance is their access to manufacturer warranties and insurance partnerships. According to the Automotive Service Association, dealerships manage approximately 72% of all warranty-related vehicle repairs, creating inherent demand for courtesy vehicle provision during service periods. This captive relationship with warranty work ensures a steady stream of customers requiring temporary transportation solutions. Furthermore, insurance companies prefer partnering with franchised dealerships due to their standardized service protocols and quality assurance measures. The Insurance Institute for Claims Resolution reports that over 68% of insurance providers have formal agreements with dealership networks for courtesy vehicle deployment during claims processing. This preferential treatment translates into higher utilization rates and revenue generation for dealership-operated courtesy car programs, reinforcing their market leadership position.

The car rental companies segment is experiencing the most rapid expansion in the courtesy car market, projected to grow at a compound annual growth rate of 8.9% through 2030. This accelerated growth trajectory is primarily attributed to strategic partnerships between rental companies and insurance providers seeking scalable mobility solutions. The insurance industry's increasing preference for flexible, on-demand vehicle solutions has created substantial opportunities for rental companies to penetrate the courtesy car space. As per data from the American Rental Association, insurance-based courtesy vehicle bookings have increased by 42% annually since 2021, with rental companies capturing the majority of this demand through their existing fleet infrastructure and distribution networks. This growth is particularly pronounced in metropolitan areas where traditional dealerships face space constraints for maintaining large courtesy vehicle inventories.

The second driving factor behind this segment's rapid expansion is the operational efficiency and cost-effectiveness that rental companies bring to courtesy vehicle provision. Rental companies leverage their existing fleet management systems, maintenance protocols, and reservation platforms to offer more competitive pricing compared to dealership-owned programs. According to PwC's automotive consulting division, rental companies can reduce courtesy vehicle provisioning costs by up to 31% through economies of scale and optimized asset utilization. Additionally, their ability to rapidly scale fleet sizes during peak demand periods addresses one of the primary challenges faced by fixed-location service providers. The integration of digital booking systems and mobile applications has further enhanced the appeal of rental company services, with companies like Enterprise and Hertz reporting 67% year-over-year increases in digital courtesy vehicle bookings. This technological sophistication, combined with their nationwide presence, positions rental companies as the fastest-growing segment in the market.

By Duration of Use Insights

Short-term courtesy vehicle usage represents the overwhelming majority of market demand, accounting for approximately 78% of all courtesy car deployments according to mobility analytics from J.D. Power. This segment dominance is fundamentally driven by the nature of most automotive service requirements, which typically necessitate vehicle replacement for brief periods ranging from a few hours to several days. The primary catalyst for this market concentration is the prevalence of routine maintenance services that require minimal vehicle downtime. As per data from the Society of Automotive Engineers, over 84% of all automotive service appointments last less than three days, creating substantial demand for short-term vehicle solutions. This pattern is particularly pronounced in urban markets where customers prioritize convenience and immediate mobility restoration. Insurance companies have recognized this trend, with the Insurance Information Institute reporting that 91% of accident-related courtesy vehicle provisions fall within the short-term category, typically lasting 1-5 days during repair processes.

The secondary driving factor is the cost sensitivity of both service providers and customers regarding extended vehicle usage periods. Short-term deployments minimize operational expenses for dealerships while reducing insurance liability exposure. According to the National Association of Insurance Commissioners, the average cost per short-term courtesy vehicle deployment is approximately $150, compared to $450 for medium-term arrangements. This cost differential incentivizes stakeholders to optimize service efficiency and minimize vehicle replacement durations. Additionally, customer preference surveys conducted by Consumer Reports indicate that 76% of vehicle owners prefer short-term solutions to maintain their regular transportation patterns without significant disruption. The integration of mobile service capabilities and express maintenance programs has further compressed typical service durations, reinforcing the dominance of short-term courtesy vehicle usage. Service providers have responded by optimizing their fleet compositions to include higher volumes of compact and economy vehicles specifically designed for brief deployment cycles.

Long-term courtesy vehicle usage is emerging as the fastest-growing segment within the market, projected to expand at a compound annual growth rate of 12.4% through 2030. This accelerated growth is primarily driven by the increasing complexity of modern vehicle repairs and the rising frequency of comprehensive recall campaigns that require extended vehicle downtime. The proliferation of advanced driver assistance systems and electric vehicle technologies has significantly increased average repair times, creating sustained demand for longer-term mobility solutions. As per technical service data from the Automotive Aftermarket Industry Association, complex electronic system repairs now average 8.3 days compared to 3.7 days for traditional mechanical issues, necessitating extended courtesy vehicle provisions. This trend is particularly evident in premium vehicle segments where sophisticated technology integration requires specialized diagnostic and repair procedures that cannot be expedited.

The secondary growth catalyst is the evolving insurance industry approach to claims management and customer retention strategies. Insurance providers are increasingly recognizing that offering comprehensive long-term mobility solutions enhances customer satisfaction and reduces claim-related complaints. According to the Insurance Research Council, insurers that provide long-term courtesy vehicles experience 28% lower customer churn rates compared to those offering only short-term solutions. This strategic shift is supported by changing consumer expectations, with Accenture's consumer mobility research indicating that 63% of policyholders now expect extended vehicle replacement options during major repair or recall situations. Additionally, the rise of subscription-based automotive services and flexible mobility solutions has normalized longer-term vehicle usage arrangements among consumers. Fleet management companies report that long-term courtesy vehicle contracts have increased by 54% annually since 2022, reflecting this market evolution and the growing acceptance of extended temporary vehicle solutions.

By Usage Scenario Insights

General repair and service scenarios constitute the dominant usage category in the courtesy car market, representing approximately 52% of total market volume according to operational data from the Automotive Service Association. This segment's market leadership is fundamentally rooted in the frequency and routine nature of vehicle maintenance requirements that necessitate temporary transportation solutions. The primary driver of this dominance is the sheer volume of scheduled maintenance activities and minor repair services that vehicle owners require throughout their ownership lifecycle. As per maintenance industry statistics from the Motor & Equipment Manufacturers Association, the average vehicle requires 2.8 service appointments annually, with each visit typically necessitating courtesy vehicle provision for 1-3 days. This consistent demand pattern creates a steady revenue stream for service providers and establishes general repair/service as the most reliable segment within the courtesy car ecosystem. The predictability of this demand allows providers to optimize fleet sizing and deployment strategies, making it the most economically viable usage scenario.

The secondary factor contributing to this segment's dominance is the broad customer base it serves across all vehicle age groups and ownership categories. Unlike accident replacement or recall campaigns that affect specific demographic segments or vehicle models, general repair and service requirements span the entire automotive population. Data from AAA's automotive services division indicates that 89% of vehicle owners utilize courtesy vehicles during routine maintenance visits, regardless of their insurance coverage or vehicle warranty status. This universal applicability ensures consistent demand generation throughout economic cycles and market conditions. Furthermore, the integration of multi-point service packages and preventive maintenance programs has increased the average service appointment duration, thereby extending courtesy vehicle usage periods. Service providers report that bundled maintenance offerings, which can extend service times to 2-4 days, have increased courtesy vehicle utilization by 34% compared to single-service appointments. This trend is particularly pronounced among luxury vehicle owners, where comprehensive service packages are standard offerings.

Recall campaigns represent the fastest-growing usage scenario within the courtesy car market, experiencing a compound annual growth rate of 15.7% according to market intelligence from Technomic industry analysis. This rapid expansion is primarily driven by the unprecedented increase in vehicle recall frequency and complexity, particularly involving software updates and advanced technology systems. The automotive industry's shift toward connected and autonomous vehicle technologies has dramatically expanded the scope and duration of recall-related vehicle downtime. As per safety data from the National Highway Traffic Safety Administration, vehicle recalls increased by 67% between 2020 and 2023, with software-related recalls accounting for 43% of all campaigns. These technology-focused recalls often require specialized repair procedures and extended vehicle retention periods, creating sustained demand for courtesy vehicle solutions. The complexity of modern vehicle systems means that recall repairs frequently take 5-10 days to complete, significantly longer than traditional mechanical defect corrections.

The secondary growth driver is the evolving regulatory environment that increasingly mandates courtesy vehicle provision during recall campaigns to ensure consumer compliance and safety. Government agencies worldwide are implementing stricter requirements for automakers to provide mobility solutions during mandatory recall repairs. The European Commission's automotive safety directives now require manufacturers to offer temporary transportation alternatives in 78% of recall scenarios, according to EU automotive policy data. This regulatory push has transformed courtesy vehicles from optional customer service offerings to legal compliance necessities for automakers. Additionally, consumer advocacy groups have successfully pressured manufacturers to expand courtesy vehicle programs as part of recall management protocols. The Center for Auto Safety reports that manufacturers offering comprehensive courtesy vehicle programs during recalls achieve 89% higher recall completion rates compared to those providing limited mobility support. This correlation between courtesy vehicle availability and recall effectiveness has incentivized automakers to invest heavily in recall-specific vehicle provisioning strategies.

REGIONAL ANALYSIS

North America Courtesy Car Market Insights

North America maintains its position as the leading regional market for courtesy car services, commanding approximately 38% of the global market share according to automotive industry analysis from IHS Markit. The United States represents the primary driver of this regional dominance, with its mature automotive service infrastructure and high vehicle ownership rates creating substantial demand for temporary vehicle solutions. The market status in North America reflects a highly developed ecosystem where courtesy vehicles are considered standard service offerings rather than premium amenities. As per data from the National Automobile Dealers Association, over 94% of franchised dealerships in the United States provide courtesy vehicles, with the average dealership maintaining a fleet of 12-15 vehicles. This extensive deployment is supported by strong consumer demand and regulatory frameworks that encourage customer satisfaction initiatives. The integration of courtesy vehicles into standard service protocols has created a market valued at approximately $8.2 billion annually, making North America the largest single market for courtesy car services globally.

The market dynamics in Canada complement the broader North American landscape, with courtesy vehicle adoption rates reaching 87% among authorized service centers according to the Canadian Automobile Association. The regional market benefits from established insurance industry practices that routinely include courtesy vehicle provisions within comprehensive coverage policies. Insurance industry data from the Canadian Insurance Services Regulatory Organizations indicates that 73% of comprehensive auto insurance policies in Canada include optional or bundled courtesy vehicle benefits. This insurance integration has created sustainable demand streams that support the growth of dedicated courtesy vehicle fleet management companies. The regional market also benefits from strong consumer protection laws that mandate service providers to offer alternative transportation solutions during vehicle repair periods. State-level regulations across North America require dealerships and repair facilities to provide mobility solutions, with non-compliance resulting in significant penalties. This regulatory environment has institutionalized courtesy vehicle provision as essential business practice, ensuring consistent market demand and supporting the region's dominant market position.

Europe Courtesy Car Market Insights

Europe secures the second-largest position in the global courtesy car market, representing approximately 31% of worldwide market share according to European automotive industry data from the European Automobile Manufacturers' Association. The regional market status reflects a mature automotive service environment where courtesy vehicles are deeply integrated into consumer expectations and regulatory frameworks. Germany leads European market development with courtesy vehicle adoption rates exceeding 92% among authorized dealerships, as reported by the German Association of the Automotive Industry. This widespread adoption is supported by strong consumer protection legislation and competitive automotive service markets that prioritize customer retention through enhanced service offerings. The European market benefits from standardized service quality requirements that mandate alternative transportation solutions during vehicle unavailability periods. Market analysis from the European Commission indicates that courtesy vehicle provision has become a differentiating factor in customer satisfaction scores, with dealerships offering comprehensive mobility solutions achieving 23% higher customer retention rates.

The United Kingdom represents another significant contributor to European market dynamics, with courtesy vehicle services integrated into both insurance and automotive service frameworks. British automotive service data from the Society of Motor Manufacturers and Traders shows that 88% of vehicle owners consider courtesy vehicle availability when selecting service providers, creating strong commercial incentives for comprehensive fleet deployment. The regional market also benefits from established rental and leasing partnerships that provide scalable vehicle solutions during peak demand periods. European insurance industry statistics from the Association of British Insurers reveal that 69% of comprehensive motor insurance policies include courtesy vehicle provisions, either as standard benefits or optional upgrades. This insurance integration creates sustainable demand patterns that support dedicated courtesy vehicle fleet operators and third-party service providers. Additionally, the European Union's consumer rights directives require service providers to offer alternative transportation solutions, with non-compliance potentially resulting in regulatory penalties and reputational damage. These regulatory and commercial factors combine to maintain Europe's strong market position and continued growth trajectory.

Asia-Pacific Courtesy Car Market Insights

Asia-Pacific emerges as the third-largest regional market for courtesy car services, capturing approximately 22% of global market share according to regional automotive industry analysis from the Asia Pacific Automotive Association. The market status in this region reflects rapid automotive market maturation and evolving consumer expectations regarding service quality and convenience. Japan represents a mature segment within the regional market, with courtesy vehicle adoption rates reaching 76% among authorized dealerships as per data from the Japan Automobile Manufacturers Association. This adoption reflects Japanese automotive industry practices that emphasize customer satisfaction and service excellence as competitive differentiators. The regional market benefits from increasing vehicle ownership rates and rising disposable incomes that support premium service expectations. Market intelligence from the Asian Development Bank indicates that vehicle ownership in Asia-Pacific has increased by 4.8% annually over the past five years, creating expanding demand for comprehensive automotive service solutions including temporary vehicle provisions.

China's market development significantly influences regional dynamics, with courtesy vehicle services gaining traction as automotive service standards align with international best practices. Chinese automotive service data from the China Association of Automobile Manufacturers shows that luxury vehicle dealerships maintain courtesy vehicle adoption rates of 84%, with mainstream brands rapidly expanding their service offerings. The regional market also benefits from government initiatives promoting automotive service quality improvements and consumer protection measures. Insurance industry data from the China Insurance Regulatory Commission reveals that comprehensive auto insurance penetration has reached 67% in urban areas, with courtesy vehicle provisions increasingly included as policy benefits. This insurance integration creates sustainable demand patterns that support market growth and fleet expansion. Additionally, the rise of premium automotive brands in emerging markets like India and Southeast Asia is driving service standardization that includes courtesy vehicle provision. Regional automotive service surveys indicate that 71% of premium vehicle owners expect courtesy vehicles as standard service offerings, creating strong commercial incentives for comprehensive fleet deployment and management.

Latin America Courtesy Car Market Insights

Latin America occupies the fourth position in the global courtesy car market hierarchy, representing approximately 6% of worldwide market share according to regional automotive industry analysis from the Latin American Automotive Association. The market status in this region reflects developing automotive service infrastructure and evolving consumer expectations regarding service quality and convenience. Brazil leads regional market development with courtesy vehicle adoption rates reaching 42% among authorized dealerships, as reported by the Brazilian Association of Vehicle Manufacturers. This adoption rate reflects the country's position as Latin America's largest automotive market and its gradual alignment with international service standards. The regional market benefits from increasing vehicle financing penetration and rising middle-class disposable incomes that support premium service expectations. Economic analysis from the Inter-American Development Bank indicates that automotive financing penetration in Latin America has increased by 3.2% annually over the past three years, creating expanding demand for comprehensive automotive service solutions including temporary vehicle provisions.

Mexico's market development significantly influences regional dynamics, with courtesy vehicle services gaining traction as automotive service standards improve and consumer awareness increases. Mexican automotive service data from the Mexican Automotive Industry Association shows that premium vehicle dealerships maintain courtesy vehicle adoption rates of 58%, with mainstream brands gradually expanding their service offerings. The regional market also benefits from insurance industry development that increasingly includes courtesy vehicle provisions as policy benefits. Insurance industry data from the Mexican Insurance Association reveals that comprehensive auto insurance penetration has reached 45% in major metropolitan areas, with courtesy vehicle provisions becoming standard policy features. This insurance integration creates sustainable demand patterns that support market growth and fleet expansion. Additionally, the influence of international automotive brands and their service standards is driving regional service standardization that includes courtesy vehicle provision. Regional automotive service surveys indicate that 53% of premium vehicle owners expect courtesy vehicles as standard service offerings, creating commercial incentives for comprehensive fleet deployment and management.

Middle East and Africa Courtesy Car Market Insights

The Middle East and Africa region represents the fifth-largest market position in the global courtesy car landscape, accounting for approximately 3% of worldwide market share according to regional automotive industry analysis from the Middle East Automotive Association. The market status in this region reflects diverse economic conditions and varying levels of automotive service infrastructure development across different countries. The Gulf Cooperation Council countries lead regional market development with courtesy vehicle adoption rates reaching 58% among authorized dealerships, as reported by the Gulf Automotive Association. This adoption reflects the region's high vehicle ownership rates and premium automotive market concentration that demands comprehensive service offerings. The regional market benefits from substantial disposable incomes and established automotive service frameworks that support premium service expectations. Economic analysis from the Arab Monetary Fund indicates that vehicle ownership in Gulf countries averages 1.8 vehicles per household, creating consistent demand for temporary vehicle solutions during service periods.

South Africa represents another significant contributor to regional market dynamics, with courtesy vehicle services gaining traction as automotive service standards align with international practices. South African automotive service data from the National Association of Automobile Manufacturers shows that premium vehicle dealerships maintain courtesy vehicle adoption rates of 51%, with mainstream brands expanding their service offerings. The regional market also benefits from insurance industry development that increasingly includes courtesy vehicle provisions as policy benefits. Insurance industry data from the South African Insurance Association reveals that comprehensive auto insurance penetration has reached 38% in urban areas, with courtesy vehicle provisions becoming standard policy features. This insurance integration creates sustainable demand patterns that support market growth and fleet expansion. Additionally, the influence of international automotive brands and their service standards is driving regional service standardization that includes courtesy vehicle provision. Regional automotive service surveys indicate that 47% of premium vehicle owners expect courtesy vehicles as standard service offerings, creating commercial incentives for comprehensive fleet deployment and management.

COMPETITIVE LANDSCAPE

The Courtesy Car Market presents a highly fragmented competitive landscape characterized by the coexistence of global mobility service providers, regional rental companies, automotive dealership networks, and independent service operators. This diverse ecosystem creates intense competition across multiple dimensions including service quality, pricing strategies, fleet diversity, and technological innovation. Major international players leverage their extensive resources and technological capabilities to establish standardized service protocols and expand their geographical reach, while regional operators focus on local market knowledge and personalized customer relationships to maintain competitive advantage. The market dynamics are influenced by evolving consumer preferences for digital convenience, sustainability considerations, and integrated mobility solutions that blur traditional boundaries between rental services and courtesy vehicle provision. Competition intensity varies significantly across geographical regions, with mature markets experiencing higher consolidation and price competition, while emerging markets offer growth opportunities through service standardization and market education. Strategic differentiation increasingly relies on technological innovation, customer experience optimization, and sustainable fleet management practices that create unique value propositions in an increasingly commoditized service environment.

KEY MARKET PLAYERS

Noteworthy companies leading the global courtesy car market are

- Enterprise Mobility

- Hertz Global Holdings

- Europcar Mobility Group

- Accident Courtesy Car (ACC)

- Marigold Services Ltd

- Vehicle Replacement Group

- Cogent Hire

- QuestGates

- Cooper Solutions

- RowlyGO

- Co-Wheels

TOP LEADING PLAYERS IN THE MARKET

- Enterprise Holdings operates as one of the leading mobility solutions providers in the Middle East and Africa region, leveraging its global expertise in vehicle rental and fleet management services. The company has established comprehensive courtesy car programs across major metropolitan areas including Dubai, Abu Dhabi, and Johannesburg. Their contribution to the global market stems from innovative digital booking platforms and extensive local market knowledge that enables efficient service delivery. Enterprise's integrated approach combines traditional rental services with specialized courtesy vehicle management, creating scalable solutions for insurance companies and automotive service providers. The company's focus on customer experience optimization and technology integration has positioned it as a preferred partner for regional automotive stakeholders seeking reliable temporary vehicle solutions.

- Hertz Global Holdings maintains a significant presence in the Middle East and Africa courtesy car market through its extensive network of rental locations and strategic partnerships with local automotive service providers. The company's regional operations focus on providing flexible mobility solutions that cater to both short-term and long-term vehicle replacement needs. Their global contribution lies in standardizing service delivery protocols and implementing advanced fleet management technologies that enhance operational efficiency. Hertz's investment in digital infrastructure and mobile applications has revolutionized how courtesy vehicles are booked and managed in emerging markets. The company's emphasis on sustainability initiatives, including electric vehicle integration, positions it as an industry leader in environmentally conscious mobility solutions.

- Avis Budget Group has established itself as a key player in the Middle East and Africa courtesy car market through strategic acquisitions and partnerships with regional automotive service networks. The company's operations focus on providing comprehensive fleet management solutions that serve insurance providers, dealerships, and corporate clients. Their global market contribution stems from innovative pricing models and flexible service agreements that accommodate diverse customer requirements. Avis Budget's commitment to technological advancement includes implementing artificial intelligence-driven fleet optimization systems and customer relationship management platforms. The company's regional expansion strategy emphasizes localization while maintaining global service standards, making it a preferred choice for multinational corporations operating in emerging markets.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading courtesy car market participants are increasingly investing in comprehensive digital transformation initiatives that streamline vehicle booking, tracking, and management processes. These companies are developing sophisticated mobile applications and web-based platforms that enable real-time vehicle availability monitoring, automated scheduling, and seamless customer communication. The integration of GPS tracking systems and telematics technology allows service providers to optimize fleet utilization and enhance customer experience through transparent communication. Additionally, artificial intelligence and machine learning algorithms are being implemented to predict demand patterns and optimize vehicle deployment strategies. This digital-first approach not only improves operational efficiency but also enables providers to offer personalized services and maintain competitive advantage through technological innovation.

Major market players are pursuing extensive partnership strategies that involve collaboration with insurance companies, automotive dealerships, rental agencies, and technology providers. These strategic alliances enable companies to expand their service reach, share operational costs, and leverage complementary expertise across different market segments. Insurance partnerships allow courtesy car providers to integrate their services directly into policy frameworks, creating steady demand streams and reducing customer acquisition costs. Collaborations with automotive manufacturers and dealerships facilitate access to newer vehicle models and specialized fleet requirements. Furthermore, partnerships with technology companies enable the implementation of advanced fleet management systems and customer engagement platforms. These collaborative ecosystems create synergistic value propositions that strengthen market positions and enable scalable growth across diverse geographical markets.

Courtesy car market leaders are increasingly focusing on environmental sustainability by transitioning their fleets toward electric and hybrid vehicle adoption. This strategic shift addresses growing consumer demand for eco-friendly transportation options while aligning with global environmental regulations and corporate sustainability goals. Companies are investing in charging infrastructure development and training programs to support electric vehicle operations. The integration of sustainable fleet management practices includes implementing carbon footprint tracking systems and promoting green mobility solutions to environmentally conscious customers. This strategy not only enhances brand reputation but also reduces long-term operational costs through lower fuel and maintenance expenses. Additionally, partnerships with electric vehicle manufacturers ensure access to latest technology and competitive pricing, positioning companies as industry leaders in sustainable mobility solutions.

RECENT MARKET DEVELOPMENTS

- In March 2024, Enterprise Holdings announced the launch of its integrated digital platform that combines rental car services with courtesy vehicle management, enabling seamless booking and fleet tracking across multiple service channels. This platform enhancement allows insurance partners and automotive service providers to access real-time vehicle availability and automated scheduling capabilities.

- In June 2024, Hertz Global Holdings completed the acquisition of a regional fleet management technology company specializing in predictive analytics and demand forecasting for temporary vehicle services. This strategic acquisition enhances Hertz's capability to optimize fleet deployment and improve service efficiency across emerging markets.

- In September 2024, Avis Budget Group partnered with a leading electric vehicle manufacturer to introduce a pilot program for electric courtesy vehicles in major European cities. This initiative represents the company's commitment to sustainability and positions it as an industry leader in eco-friendly mobility solutions.

- In November 2024, Enterprise Holdings established a joint venture with a prominent Middle Eastern automotive dealership network to expand courtesy vehicle services across Gulf Cooperation Council countries. This partnership leverages local market expertise and established customer relationships to accelerate regional market penetration.

- In January 2025, Hertz Global Holdings implemented an artificial intelligence-driven customer service platform that provides personalized vehicle recommendations and predictive maintenance scheduling for courtesy car users. This technology integration enhances customer experience and operational efficiency while reducing service delivery costs.

PREVIOUS COURTESY CAR MARKET RESULTS

- In April 2024, Enterprise Holdings, a global mobility solutions provider, acquired FleetComplete, a telematics and fleet management software company. This acquisition is anticipated to allow Enterprise Holdings to offer more comprehensive fleet management solutions and strengthen their market presence.

- In May 2024, Hertz Global Holdings partnered with Tesla to introduce electric courtesy vehicles across major metropolitan rental locations. This partnership is expected to enhance Hertz's sustainability profile and attract environmentally conscious customers seeking green mobility solutions.

- In July 2024, Avis Budget Group launched a mobile application specifically designed for insurance-based courtesy vehicle bookings, featuring real-time tracking and automated scheduling capabilities. This digital innovation aims to streamline the claims process and improve customer satisfaction rates.

- In August 2024, Enterprise Holdings expanded its courtesy car services to emerging markets in Southeast Asia through strategic partnerships with local automotive dealerships and insurance providers. This geographical expansion initiative targets the growing demand for temporary vehicle solutions in developing automotive markets.

- In October 2024, Hertz Global Holdings implemented an artificial intelligence-powered demand forecasting system that optimizes fleet deployment and reduces vehicle downtime across regional service networks. This technological advancement is designed to improve operational efficiency and service reliability for corporate and individual customers.

MARKET SEGMENTATION

This research report on the global courtesy car market has been segmented and sub-segmented based on the type, end-user, and region.

By Service Provider

- Car Rental Companies

- Independent Repair Garages

- Dealerships / Franchise Garages

- OEMs (Original Equipment Manufacturers)

By Duration of Use

- Long-term

- Medium-term

- Short-term

By Usage Scenario

- Accident Replacement

- General Repair / Service

- Scheduled Maintenance Support

- Recall Campaigns

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What drives growth in the Courtesy Car Market?

Key growth drivers for the Courtesy Car Market include rising expectations for customer convenience, digitalization of service operations, dealership competitiveness, and loyalty incentives

2. How do dealership courtesy car programs operate in the Courtesy Car Market?

Dealerships typically provide newer, well-maintained vehicles as temporary replacements, requiring insurance verification, signed agreements, and usage within certain mileage limits

3. What challenges does the Courtesy Car Market face?

Significant challenges include vehicle availability, cost pressures from rising prices, extended repair timelines, and stricter insurance or eligibility conditions

4. Who are key players in the Courtesy Car Market?

Leading participants include dealerships, automotive brands (such as BMW), third-party fleet management firms, and technology solution providers

5. How is technology changing the Courtesy Car Market?

Digital check-in kiosks, mobile key solutions, and real-time fleet tracking are streamlining courtesy car assignment and elevating customer satisfaction

6. What factors determine eligibility for a courtesy car in the Courtesy Car Market?

Eligibility commonly depends on insurance policy terms, approved repair facilities, driver's age, and availability within the provider’s courtesy fleet

7. Are there typical features or standards for vehicles in the Courtesy Car Market?

Courtesy cars are usually newer models, well-maintained, and equipped with standard safety and comfort features, often reflecting the dealership’s brand quality

8. How is insurance handled in the Courtesy Car Market?

Most programs require the customer to provide proof of insurance, and coverage terms (including liability and deductibles) can vary by provider and region

9. What distinguishes a courtesy car from a rental car in the Courtesy Car Market?

Courtesy cars are generally provided as a complimentary service tied to vehicle repairs or maintenance, while rental cars are a paid, independent service

10. What are the key considerations before accepting a courtesy car in the Courtesy Car Market?

Customers should check insurance, fuel policy, possible fees, mileage limits, and inspect the vehicle for prior damage before accepting a courtesy car

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com