Global Digital Payments Market Size, Share, Trends, & Growth Forecast Report by Type (Solutions & Services), Solution Type (Payment Processing, Payment Gateway, Payment Wallet, POS Solution, Payment Security, and Fraud Management), Deployment Mode (On-Premises and Cloud), Organization Size (SMEs and Large Enterprises), & Region - Industry Forecast From 2026 to 2034

Global Digital Payments Market Report Summary

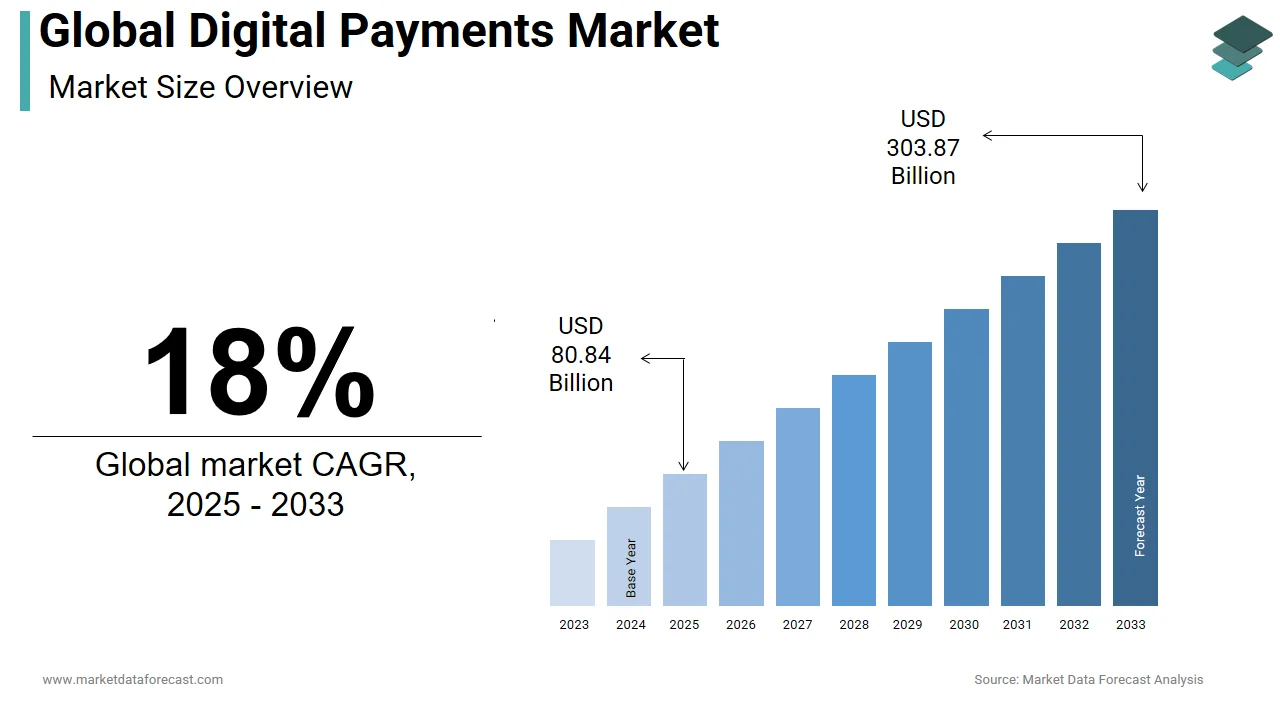

The global digital payments market was valued at USD 80.84 billion in 2025 and is projected to grow from USD 95.39 billion in 2026 to USD 358.56 billion by 2034, registering a robust CAGR of 18% from 2026 to 2034. Market growth is driven by the rapid adoption of cashless transactions, increasing smartphone penetration, expanding e-commerce activities, and growing consumer preference for seamless digital payment experiences. Businesses and consumers are increasingly adopting digital payment platforms due to convenience, speed, security, and integration with digital commerce ecosystems. The continued expansion of fintech innovation, real-time payment systems, and cloud-based payment infrastructure is further accelerating global market growth.

Key Market Trends

- Rising adoption of mobile wallets and contactless payment solutions.

- Increasing integration of artificial intelligence and fraud detection technologies in payment systems.

- Growing demand for real-time and cross-border payment processing solutions.

- Expansion of cloud-based digital payment platforms and fintech ecosystems.

- Strengthening focus on consumer data security, regulatory compliance, and digital identity verification.

Segmental Insights

- Based on type, the solutions segment dominated the global digital payments market in 2025 by accounting for 61.4% market share, driven by increasing deployment of payment platforms, transaction management systems, and digital payment gateways.

- Based on solution type, the payment processing segment led the market by capturing 35.5% share in 2025, supported by rising transaction volumes across e-commerce, retail, banking, and digital service platforms.

- Based on deployment mode, the cloud segment held the leading position with 64.6% market share in 2025, driven by scalability, cost efficiency, enhanced security capabilities, and rapid deployment benefits.

- Based on organization size, the large enterprises segment accounted for 54.6% share in 2025, supported by the substantial volume of global transactions, complex payment infrastructures, and increasing investment in advanced payment technologies.

Regional Insights

The global digital payments market is experiencing rapid expansion across major regions, supported by increasing digitalization, growing fintech adoption, and evolving payment regulations.

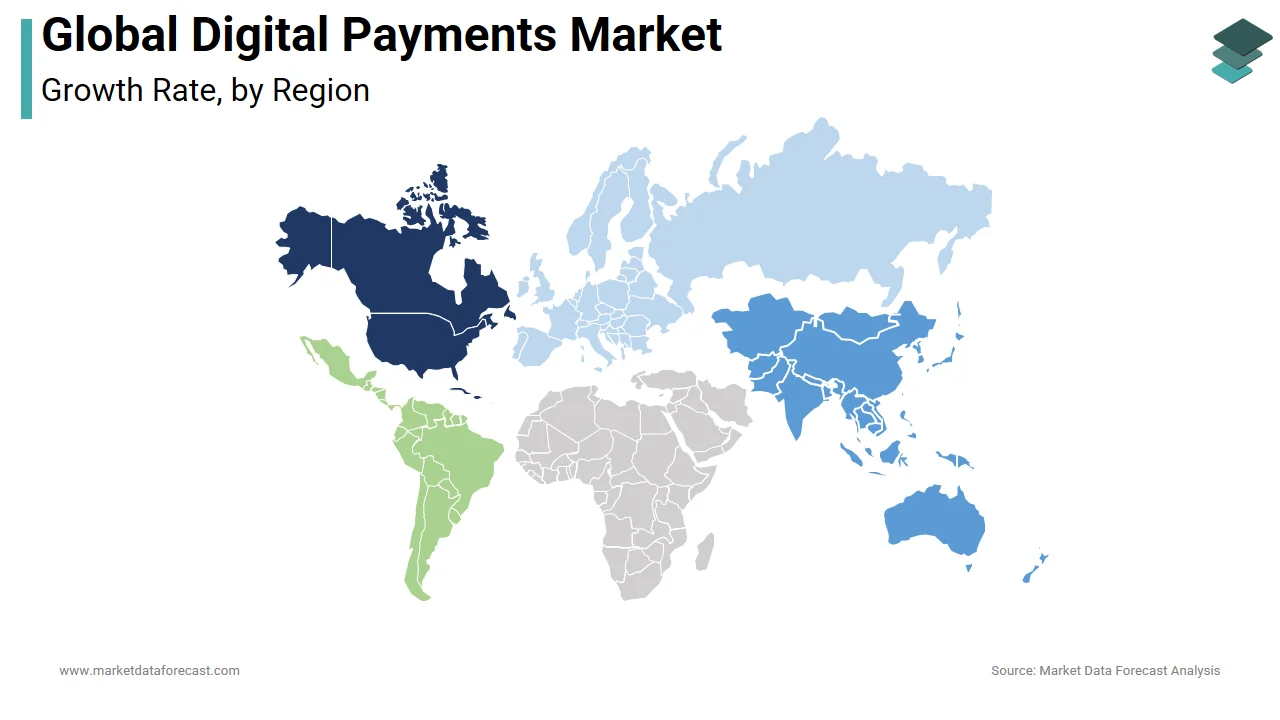

- Asia-Pacific dominated the global market in 2025, driven by widespread mobile payment adoption, large digital consumer populations, expanding e-commerce ecosystems, and strong fintech innovation across major economies.

- North America held a significant share of the global market in 2025, supported by high credit card penetration, advanced payment infrastructure, and early adoption of innovative digital payment models.

- Europe remains a key regional market, characterized by a strong emphasis on consumer protection, data privacy regulations, open banking initiatives, and efforts to promote competition and innovation within the financial services sector.

Competitive Landscape

The global digital payments market is highly competitive, with technology companies, payment processors, financial institutions, and fintech providers continuously innovating to enhance transaction speed, security, and user experience. Market participants are focusing on cloud-based payment platforms, AI-driven fraud prevention, real-time payment capabilities, and cross-border transaction solutions to strengthen market positioning. Strategic partnerships, acquisitions, and investments in digital financial infrastructure are shaping competitive dynamics across the market.

Prominent companies operating in the global digital payments market include Alipay, Amazon Pay, Apple Pay, Tencent, Stripe, Adyen, Google Pay, First Data, PayPal, Fiserv, Visa Inc., and Mastercard.

Global Digital Payments Market Size

The global digital payments market was worth USD 80.84 billion in 2025. The global market is predicted to reach USD 95.39 billion in 2026 and USD 358.56 billion by 2034, growing at a CAGR of 18% from 2026 to 2034.

Digital payments encompass electronic transactions where money is transferred from one party to another without the physical exchange of cash or checks. This ecosystem includes credit, debit cards, mobile wallets, bank transfers, and cryptocurrency transactions. The fundamental shift toward cashless economies has redefined consumer behavior and merchant operations globally. As per the World Bank, approximately 1.4 billion adults remained unbanked in 2021, yet digital payment adoption continues to rise even among previously excluded populations due to mobile penetration. According to the European Central Bank, card payments accounted for 54% of the total number of noncash payments in the euro area in 2022, indicating a strong preference for electronic methods over traditional instruments. As per the Bank for International Settlements, real-time payment systems are now operational in around 60 countries, facilitating instant settlement and enhancing liquidity management for businesses. The integration of artificial intelligence and blockchain technology has further secured these transactions while reducing fraud rates. According to the United Nations Conference on Trade and Development, global e-commerce sales reached 26.7 trillion US dollars in 2019, which directly correlates with increased demand for secure digital payment gateways. This market is not merely a financial tool but a critical infrastructure component supporting modern economic activity and financial inclusion across diverse geographies.

MARKET DRIVERS

Rising Smartphone Penetration Driving Transaction Volume

Smartphone proliferation is one of the major factors fuelling the digital payment adoption by providing ubiquitous access to financial services and is driving the global digital payments market expansion. As per the International Telecommunication Union, global mobile cellular subscriptions reached 8.9 billion in 2023, which translates to a penetration rate exceeding 110% in many developed regions. This widespread device ownership enables consumers to utilize mobile banking applications and digital wallets seamlessly. In India, the Unified Payments Interface processed over 10 billion transactions in a single month during early 2024, demonstrating how mobile infrastructure supports massive transaction volumes. The convenience of carrying multiple payment instruments in a single device reduces friction at point-of-sale terminals. According to GSMA Intelligence, there were 5.4 billion unique mobile subscribers globally in 2023, with 4.3 billion using mobile internet services. This connectivity allows merchants in remote areas to accept digital payments without expensive hardware investments. The ease of downloading payment apps and linking them to bank accounts has lowered entry barriers for first-time users. According to the Pew Research Center, 85% of Americans own a smartphone, which facilitates contactless payments and peer-to-peer transfers. The continuous improvement in mobile network speeds, such as 5G deployment, ensures faster transaction processing times, enhancing user experience. This technological backbone creates an environment where digital payments become the default choice rather than an alternative method.

Government Initiatives Promoting Cashless Economies

National governments worldwide are actively implementing policies to reduce cash dependency and enhance financial transparency through digital channels, which is further fuelling the global market growth. According to the Reserve Bank of India, digital transactions accounted for 95% of the total volume of noncash retail payments in 2023, following aggressive promotion of the Digital India campaign. Similarly, the European Commission launched the Instant Payments Regulation, which mandates that banks offer euro instant payments by October 2025, aiming to standardize and accelerate cross-border transactions within the union. China has integrated digital yuan pilots in over 26 cities, with hundreds of millions of individual wallets opened as part of its central bank digital currency strategy. These state-led initiatives often include tax incentives for merchants who adopt digital payment systems and penalties for large cash transactions to discourage illicit activities. According to the Organization for Economic Cooperation and Development, several member countries have set targets to achieve near-zero cash usage in public sector transactions by 2030. According to the Swedish government, only 9% of all transactions in Sweden were conducted in cash in 2022, reflecting successful policy implementation. Such regulatory frameworks create a conducive environment for fintech innovation and encourage traditional banks to upgrade their digital infrastructure. The push for financial inclusion also drives governments to subsidize digital payment access for rural populations, ensuring equitable economic participation.

MARKET RESTRAINTS

Cybersecurity Threats Undermining Consumer Trust

Persistent cybersecurity vulnerabilities pose significant risks to the digital payments ecosystem by exposing sensitive financial data to malicious actors, which is primarily hampering the expansion of the digital payments market. As per the Identity Theft Resource Center, there were 3,205 data breaches in the United States in 2023, affecting over 353 million individuals, which erodes confidence in digital platforms. Fraudulent activities, such as phishing scams, card skimming, and account takeovers, result in substantial financial losses for both consumers and institutions. According to the Federal Trade Commission, consumers lost more than 10 billion US dollars to fraud in 2023, with investment and impostor scams being prevalent vectors. These incidents compel users to revert to cash or limit their digital transaction frequency due to fear of unauthorized access. The complexity of securing multiple endpoints, including mobile devices, cloud servers, and payment gateways, creates numerous attack surfaces for hackers. According to IBM Security, the average cost of a data breach reached 4.45 million US dollars in 2023, highlighting the economic burden on companies. Small and medium enterprises often lack resources to implement robust security measures, making them vulnerable targets. The evolving nature of cyber threats requires continuous investment in advanced encryption, multi-factor authentication, and biometric verification. However, the frequent occurrence of high-profile breaches, despite these measures, sustains consumer apprehension. This trust deficit slows down adoption rates, particularly among older demographics who perceive digital payments as inherently risky compared to tangible cash transactions.

Regulatory Fragmentation across Jurisdictions

Divergent regulatory frameworks across different countries create compliance complexities that hinder the seamless expansion of digital payment providers, which is another significant impediment to the growth of the digital payments market. As per the Bank for International Settlements, over 130 countries are exploring or piloting central bank digital currencies, each with distinct legal requirements and operational standards. Payment service providers must navigate varying anti-money laundering laws, data protection regulations, and licensing procedures when operating internationally. The General Data Protection Regulation in Europe imposes strict guidelines on customer data handling, which differs significantly from regulations in Asia or North America. According to the World Bank, doing business across borders involves adapting to multiple regulatory regimes, which increases operational costs and delays market entry. For instance, India requires local data storage for payment information, while other jurisdictions allow cross-border data flows under specific conditions. This fragmentation forces companies to maintain separate compliance teams and technology stacks for different regions, reducing economies of scale. The lack of harmonized standards for interoperability between different payment systems further complicates cross-border transactions. Merchants face challenges in accepting payments from foreign customers, due to incompatible regulatory requirements. These legal uncertainties discourage innovation and limit the ability of fintech firms to offer unified global solutions. The constant evolution of regulations requires continuous monitoring and adaptation, straining resources, especially for smaller players in the market.

MARKET OPPORTUNITIES

Expansion into Unbanked Populations in Emerging Markets

The vast unbanked population in emerging economies is a substantial opportunity for the digital payments market. As per the World Bank Findex Database, approximately 1.4 billion adults globally lacked access to formal financial services in 2021, with the majority residing in developing nations. Mobile money platforms have demonstrated success in bridging this gap by allowing users to store value and make transactions via basic feature phones. According to the GSMA, mobile money accounts in Sub-Saharan Africa registered strong growth, with active accounts reaching 184 million users in 2023. This demographic represents a lucrative market for payment processors who can offer low-cost alternatives to conventional banking. The ability to provide microloans, insurance products, and savings accounts through digital channels enhances customer lifetime value. According to the International Finance Corporation, small and medium enterprises in emerging markets face a financing gap of 5.2 trillion US dollars, which digital payments can help address by creating credit histories. Governments in these regions are increasingly partnering with fintech firms to distribute social welfare benefits digitally, reducing leakage and corruption. The low infrastructure requirements for mobile-based payments enable rapid scaling in rural areas, where brick-and-mortar branches are economically unviable. Capturing this segment requires tailored solutions that address literacy barriers and trust issues, but offers long-term growth potential as these economies develop.

Integration of Artificial Intelligence for Personalized Services

The incorporation of artificial intelligence into digital payment platforms enables hyper-personalized financial services that enhance user engagement and retention, which is another prominent opportunity for the global market. AI algorithms analyze transaction patterns to offer customized budgeting tools, spending insights, and predictive analytics that help consumers manage their finances effectively. As per the McKinsey Global Institute, artificial intelligence could deliver additional annual economic value of up to 2.6 trillion US dollars across marketing and sales applications, including personalized financial recommendations. Payment providers use machine learning to detect fraudulent transactions in real time, with accuracy rates exceeding 95%, reducing false positives and improving customer experience. Chatbots powered by natural language processing handle customer inquiries instantly, reducing operational costs for financial institutions. According to PwC, 72% of business leaders believe that AI will be the business advantage of the future, particularly in customer service and risk management. The ability to offer dynamic pricing, loyalty rewards, and targeted promotions, based on individual behavior, increases transaction frequency. AI-driven credit scoring models assess alternative data sources, enabling lending to individuals with thin credit files. This technological advancement transforms payment platforms from mere transaction conduits into comprehensive financial wellness partners. The continuous learning capability of AI systems ensures that services evolve with changing consumer preferences, maintaining competitive relevance. Early adopters of AI technologies gain significant market share by delivering superior user experiences that traditional banks struggle to match.

MARKET CHALLENGES

Interoperability Issues Between Payment Systems

The lack of seamless interoperability between different digital payment networks creates friction for users and merchants alike, which is a significant challenge to the digital payments market expansion. As per the European Central Bank, while instant payment schemes exist in many countries, cross-border compatibility remains limited, causing delays and higher costs for international transactions. Consumers often need multiple apps to pay different merchants, depending on the accepted payment protocol, leading to wallet fatigue. In Southeast Asia, the Association of Southeast Asian Nations has been working toward regional payment connectivity, but full integration is still years away, according to recent assessments. Merchants face technical challenges in integrating various payment gateways, which increases setup costs and maintenance burdens. According to the World Bank, fragmented payment ecosystems reduce efficiency and hinder the growth of digital commerce, particularly for small businesses. The absence of universal standards means that funds transferred between different platforms may take days to settle, unlike instantaneous transfers within the same network. This inefficiency discourages users from adopting newer payment methods if they cannot easily move money between their preferred providers. Regulatory bodies are attempting to mandate interoperability, but progress is slow due to competing commercial interests among major players. The resulting silos prevent the creation of a unified digital payment landscape that maximizes convenience for end users. Until standardized protocols are widely adopted, the market will remain fragmented, limiting its overall potential.

Digital Literacy Gaps among Older Demographics

Significant disparities in digital literacy, particularly among older adults, impede the widespread adoption of digital payment solutions, which is another major challenge to the global market growth. As per the Organisation for Economic Cooperation and Development, only 58% of adults aged 55 to 65 possess basic digital skills required to navigate online financial services confidently. This skills gap leads to exclusion from the digital economy, as elderly individuals struggle with interface navigation, password management, and security protocols. In Japan, where 29% of the population is over 65 years old, many seniors prefer cash due to discomfort with technology, according to national surveys. The complexity of modern payment apps, with multiple layers of authentication, confuses users who did not grow up with digital devices. According to AARP, nearly 40% of older adults in the United States report feeling anxious about using digital banking tools, due to fear of making errors. This hesitation results in continued reliance on physical branches and cash transactions, slowing the transition to cashless societies. Financial institutions often design products with younger, tech-savvy users in mind, neglecting the usability needs of older demographics. The lack of adequate training programs and customer support tailored to senior citizens exacerbates the problem. Addressing this challenge requires simplified interfaces, voice-assisted technologies, and community-based education initiatives. Without bridging this literacy divide, a substantial portion of the population remains marginalized from the benefits of digital financial services.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Solution Type, Deployment Mode, Organization Size, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Alipay, Amazon Pay, Apple Pay, Tencent, Google Pay, First Data, PayPal, Fiserv, Visa Inc., MasterCard, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The solutions segment dominated the market by holding the largest share of the 61.4% of the global market in 2025. The growth of solutions segment in the global market is majorly driven by the fundamental need for robust core infrastructure that facilitates seamless electronic transactions. Every digital payment ecosystem relies heavily on underlying software architectures to route authorizations, manage data, and ensure connectivity between merchants, acquirers, and issuing banks. According to the International Data Corporation, global spending on payment software solutions exceeded 45 billion US dollars in 2023, reflecting the massive capital allocation toward building these foundational systems. Financial institutions and fintech companies must continuously invest in upgrading their core processing engines to handle the exponential surge in transaction volumes generated by global electronic commerce. Furthermore, the integration of advanced technologies like artificial intelligence and blockchain directly into these software solutions enhances processing speeds and reduces latency. According to the Bank for International Settlements, noncash payment transactions globally surpassed 1 trillion in 2023, necessitating highly sophisticated and resilient software frameworks to prevent system outages during peak shopping periods. This continuous requirement for technological modernization ensures that solutions remain the most critical and heavily funded component of the entire digital payments value chain.

On the other end, the services segment is a promising segment and is estimated to showcase the fastest CAGR of 16.5% during the forecast period owing to the surging reliance on managed security and compliance services to navigate an increasingly complex regulatory landscape. Digital payment providers face immense pressure to adhere to stringent global data protection mandates and anti-money laundering directives, which require continuous monitoring and expert oversight. According to the Ponemon Institute, the average cost of a data breach in the financial sector reached 5.9 million US dollars in 2023, compelling organizations to outsource their security operations to specialized managed service providers. These services offer round-the-clock threat detection, vulnerability assessments, and incident response capabilities that are often too costly for individual companies to maintain in-house. Furthermore, the implementation of strong customer authentication protocols under regulations like the Revised Directive on Payment Services in Europe necessitates expert consulting to ensure seamless compliance without degrading the user experience. According to the European Central Bank, fraud rates on card payments remained at 0.046% in 2022, but the absolute value of fraud continues to rise, driving merchants to invest heavily in managed fraud prevention services. This critical need for specialized expertise ensures that the services segment experiences the most rapid growth trajectory in the market.

By Solution Type Insights

The payment processing segment dominated the market by commanding for 35.5% of the global market share in 2025 due to its indispensable role as the central nervous system of all electronic financial transactions. Every time a consumer initiates a purchase using a credit card, digital wallet, or bank transfer, the transaction data must be securely encrypted, routed to the issuing bank for authorization, and then returned to the merchant for completion. According to the Nilson Report, global card transaction volume reached 104.8 trillion US dollars in 2023, representing a massive operational scale that requires highly reliable and ubiquitous processing infrastructure. This segment encompasses the core switching and routing technologies that connect millions of merchants with thousands of financial institutions worldwide. The sheer volume of daily transactions necessitates continuous investment in processing hardware and software to ensure high availability and minimal latency. According to the Federal Reserve, the Fedwire Funds Service processed an average daily value of 5.1 trillion US dollars in 2023, highlighting the critical importance of robust processing capabilities for economic stability. Without these foundational processing solutions, the entire digital payments ecosystem would collapse, making it the most dominant and heavily utilized solution type in the global market landscape.

However, the fraud management segment is experiencing the most rapid growth and is predicted to record a CAGR of 21.6% during the forecast period owing to the exponential increase in sophisticated cyber threats and the escalating financial impact of digital payment fraud. As transaction volumes shift decisively toward digital channels, malicious actors have developed increasingly complex methods to exploit vulnerabilities, including account takeovers, synthetic identity fraud, and sophisticated phishing campaigns. According to the Identity Theft Resource Center, data compromises in the financial services sector increased by 24% in 2023, resulting in massive financial losses and severe reputational damage for affected institutions. To combat these evolving threats, merchants and payment providers are aggressively deploying advanced fraud management solutions powered by machine learning and behavioral biometrics. These systems analyze thousands of data points in milliseconds to distinguish between legitimate user behavior and fraudulent activity without introducing friction into the checkout process. According to the Association of Certified Fraud Examiners, organizations lose 5% of their annual revenue to fraud, making the deployment of proactive management solutions a critical financial imperative. The continuous arms race between fraudsters and security professionals necessitates constant updates and enhancements to fraud detection algorithms, ensuring that this segment maintains the highest growth rate in the digital payments market.

By Deployment Mode Insights

The cloud segment led the market with 64.6% of the global market share in 2025. The growth of cloud segment in the global market primarily due to its unparalleled ability to provide elastic scalability and handle massive fluctuations in transaction volumes without requiring upfront capital investment in physical hardware. Digital payment traffic is inherently unpredictable, with sudden spikes occurring during major shopping events or seasonal sales peaks. According to Amazon Web Services, cloud-based payment architectures can automatically scale computing resources up or down in seconds, ensuring that transaction processing speeds remain consistent even when traffic increases by 500%. This elasticity eliminates the risk of system crashes and lost sales during critical revenue-generating periods. Furthermore, the cloud model operates on a subscription-based, pay-as-you-go pricing structure, which significantly reduces the total cost of ownership for payment providers. According to the Cloud Security Alliance, over 85% of financial services organizations have adopted cloud computing to improve operational agility and reduce infrastructure maintenance costs in 2023. The ability to deploy new features and security patches globally in real time, without downtime, gives cloud-based solutions a distinct operational advantage. This combination of infinite scalability, cost efficiency, and rapid deployment capabilities makes cloud the undisputed leading deployment mode for modern digital payment infrastructure.

However, the on-premises deployment mode segment is emerging as the fastest-growing segment and is predicted to register a CAGR of 15.1% during the forecast period owing to the escalating enforcement of strict data sovereignty and localization laws globally. Governments in various regions are increasingly mandating that sensitive financial data and citizen information must be stored and processed exclusively within national borders, to prevent foreign surveillance and ensure national security. According to the United Nations Conference on Trade and Development, over 80% of countries worldwide have enacted data protection and privacy legislation in 2023, requiring stringent controls over cross-border data flows. Financial institutions and government entities handling critical national payment infrastructure often opt for on-premises solutions to maintain absolute physical control over their servers and guarantee compliance with these localized data mandates. According to the Bank for International Settlements, central bank digital currency pilots and national real-time payment systems frequently rely on localized, on-premises infrastructure to mitigate systemic risks and ensure uninterrupted operation during international network disruptions. This regulatory imperative forces resurgence in on-premises deployments for critical infrastructure, ensuring that this segment experiences rapid growth in specific, high-security and highly regulated verticals, despite the broader trend toward cloud adoption.

By Organization Size Insights

The large enterprises segment held 54.6% of the global market share in 2025 due to the massive scale of their global operations and the immense volume of high-value cross-border transactions they process daily. Multinational corporations and large financial institutions operate complex supply chains and serve millions of customers across dozens of countries, requiring sophisticated payment ecosystems capable of handling multiple currencies and diverse regulatory environments. According to the World Trade Organization, global commercial services exports reached 7 trillion US dollars in 2023, with a significant portion of these B2B transactions facilitated by enterprise-grade digital payment platforms. These large organizations require highly customized payment processing solutions that integrate seamlessly with their enterprise resource planning systems, treasury management software, and global banking networks. According to the Society for Worldwide Interbank Financial Telecommunication, over 45 million messages are processed daily, primarily serving large financial institutions that rely on secure and standardized payment messaging. According to the Association of Corporate Treasurers, 68% of large corporations prioritize the implementation of centralized payment factories to optimize liquidity management and reduce bank fees in 2023. The sheer financial volume and operational complexity of these global entities necessitate massive investments in premium digital payment solutions, securing the dominant market position of the large enterprises segment.

On the other hand, the small and medium enterprises segment is anticipated to showcase a CAGR of 20.2% during the forecast period owing to the widespread proliferation of mobile point-of-sale technologies and low-cost software payment gateways that have dramatically lowered the barriers to entry for digital payment acceptance. Historically, small merchants struggled to accept digital payments due to the high costs of traditional merchant accounts and expensive physical terminal hardware. However, the advent of smartphone-based payment readers and application-based checkout solutions has democratized access to electronic transactions. According to the Small Business Administration, over 80% of small businesses in the United States adopted some form of digital payment acceptance in 2023, reflecting a massive shift in merchant behavior. Companies like Square and PayPal offer plug-and-play solutions with no monthly fees and transparent, flat-rate pricing, making it economically viable for micro-merchants and freelancers to go cashless. According to the International Finance Corporation, digital payment adoption among small businesses in emerging markets increases their average monthly revenue by 15%, by reducing cash-handling costs and expanding their customer base. This unprecedented ease of access and immediate return on investment drives rapid and continuous adoption of digital payment solutions among the vast global small and medium enterprise sector.

REGIONAL ANALYSIS

Asia-Pacific Digital Payments Market Analysis

Asia-Pacific dominated the market by holding the leading share of the global market in 2025. The respective countries across Asia Pacific are likely to experience exponential growth in transaction volumes and further digital expansion over the next few years, driven by unprecedented mobile adoption and state-backed digital infrastructure initiatives. The region is characterized by a unique leapfrog effect, where populations bypassed traditional credit card systems entirely, moving directly from cash to mobile wallets and instant bank transfers. According to the People's Bank of China, mobile payments accounted for 86% of all electronic payments in the country in 2023, demonstrating absolute dominance. Similarly, India has revolutionized retail transactions through its Unified Payments Interface, which processed a staggering 13 billion transactions in 1 single month in early 2024, as per the National Payments Corporation of India. This explosive growth is underpinned by the widespread availability of affordable smartphones and cheap mobile data plans. According to the GSM Association, there were over 750 million unique mobile internet users in the Asia Pacific region in 2023, creating a massive addressable base for digital financial services. Furthermore, aggressive government campaigns to promote cashless economies and distribute social welfare benefits directly into digital accounts have accelerated adoption among rural and unbanked populations. According to the Asian Development Bank, digital financial inclusion has lifted an estimated 10 million people out of extreme poverty in the region, by providing access to microcredit and savings tools. This combination of technological leapfrogging, massive consumer adoption, and strong government support solidifies the absolute dominance of the Asia Pacific region in the global digital payments landscape.

North America Digital Payments Market Analysis

North America accounted for a promising share of the global market in 2025 due to the high credit card penetration, advanced technological infrastructure, and the early adoption of innovative payment models. Unlike the mobile wallet dominance seen in Asia, the North American market is heavily anchored in the traditional credit and debit card networks, which have continuously evolved to incorporate contactless and tokenized technologies. According to the Federal Reserve, card payments accounted for 55% of all noncash transactions in the United States in 2023, with contactless cards making up over 40% of all point-of-sale card interactions. The region is also the global epicenter for fintech innovation and the development of buy-now-pay-later services, which have fundamentally altered consumer spending habits. According to the American Financial Services Association, the buy-now-pay-later market in North America exceeded 100 billion US dollars in transaction volume in 2023, reflecting strong consumer demand for flexible credit options at checkout. Furthermore, the region boasts a highly sophisticated merchant acquiring ecosystem, with intense competition driving down processing fees and improving service quality. According to the Electronic Transactions Association, over 90% of all retail locations in the United States and Canada accept some form of digital payment, including mobile wallets and peer-to-peer transfer applications. This mature ecosystem, combined with continuous technological upgrades and strong consumer trust in digital financial instruments, ensures that North America remains a highly lucrative and stable pillar of the global digital payments market.

Europe Digital Payments Market Analysis

The European market is defined by its strong emphasis on consumer protection, data privacy, and the dismantling of monopolistic practices within the financial sector. The implementation of the Revised Directive on Payment Services has been a transformative force, requiring banks to open their application programming interfaces to third-party providers, thereby fostering intense competition and innovation in account aggregation and payment initiation services. According to the European Central Bank, the number of active payment initiation service providers in the euro area grew by 45% in 2023, reflecting the rapid adoption of open banking solutions by merchants and consumers. Furthermore, the European Commission has aggressively pushed for the standardization of instant payments, mandating that all banks offer euro credit transfers in real time at the same cost as traditional transfers. According to the European Commission, instant payments accounted for 20% of all credit transfers in the euro area in late 2023, a significant increase from previous years. Additionally, the region is witnessing a strong shift toward sustainable and ethical banking, with consumers increasingly demanding transparent and low-fee digital payment options. According to the World Bank, financial inclusion in Europe remains high, with 96% of adults holding an account.

COMPETITIVE LANDSCAPE

The competition in the digital payments market is intensely fierce and highly fragmented, characterized by the constant clash between traditional financial institutions, agile fintech startups, and massive technology conglomerates. Traditional banks leverage their existing customer trust and extensive regulatory licenses, but often struggle with outdated legacy infrastructure that hinders rapid innovation. Conversely, fintech companies and technology giants possess superior technological capabilities and user-centric design but face significant hurdles in navigating complex global regulatory environments and acquiring expensive banking licenses. This dynamic forces continuous consolidation as large payment processors acquire innovative startups to integrate cutting-edge technologies like artificial intelligence and blockchain into their platforms. The market is further complicated by the rise of open banking, which has lowered barriers to entry and allowed new non-traditional players to access customer financial data and initiate payments directly. Consequently, companies are compelled to compete not just on transaction processing fees but on the value of the comprehensive data analytics fraud prevention, and financial management tools they offer to merchants. This relentless pressure drives continuous technological advancement and forces all market participants to aggressively innovate to maintain their relevance and market share in the rapidly evolving global digital payments market landscape today.

KEY MARKET PLAYERS

- Alipay

- Amazon Pay

- Apple Pay

- Tencent

- Stripe

- Adyen

- Google Pay

- First Data

- Paypal

- Fiserv

- Visa Inc

- MasterCard

TOP PLAYERS IN THE MARKET

- PayPal operates as a foundational pillar in the global digital payments landscape, facilitating seamless cross-border commerce and peer-to-peer transfers for hundreds of millions of active users worldwide. The company continuously innovates by integrating advanced fraud protection and expanding its buy now, pay later offerings to enhance consumer checkout experiences. Recently, PayPal launched a proprietary stablecoin pegged to the United States dollar to reduce transaction costs and accelerate settlement times for merchants. Furthermore, the company has heavily invested in artificial intelligence to optimize transaction approval rates and provide personalized financial insights to its vast user base. Through strategic partnerships with major global electronic commerce platforms and continuous enhancements to its mobile application interface, PayPal maintains its position as a highly influential and trusted leader in the digital financial ecosystem.

- Adyen serves as a premier global payment platform providing unified commerce solutions that allow multinational merchants to manage online, in-store, and mobile transactions through 1 single integrated system. The company distinguishes itself by owning its entire payment stack, including its acquiring licenses and risk management engines, which ensures maximum reliability and data transparency for enterprise clients. Recently, Adyen expanded its platform capabilities to include comprehensive issuing services, allowing large retailers to create their own branded payment cards and loyalty programs directly within the Adyen ecosystem. The company has also made significant investments in optimizing its global routing algorithms to improve authorization rates and reduce processing costs for international merchants. By focusing exclusively on large enterprise clients and providing highly customized technologically advanced payment infrastructure, Adyen continues to capture significant market share in the premium segment of the global digital payments industry.

- Stripe functions as the critical economic infrastructure for the internet, providing highly flexible and developer-friendly application programming interfaces that enable businesses of all sizes to accept payments and manage their finances globally. The company is renowned for its rapid deployment capabilities and extensive library of integrations that allow startups and enterprise companies alike to build complex payment workflows with minimal coding effort. Recently, Stripe introduced advanced climate and carbon removal payment features, allowing merchants to automatically contribute to environmental sustainability initiatives at the point of sale. The company has also expanded its treasury and issuing products, enabling software platforms to embed comprehensive financial services directly into their offerings for their end users. Through continuous innovation in embedded finance and a relentless focus on improving the developer experience, Stripe remains a dominant force shaping the future of digital commerce and financial technology integration worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key participants in the digital payments market primarily utilize strategic acquisitions to rapidly acquire new technologies, expand their geographic footprint, and integrate complementary services into their existing platforms. Companies frequently engage in extensive partnerships with traditional financial institutions and technology providers to enhance their distribution networks and offer comprehensive bundled solutions to merchants. Furthermore, organizations heavily invest in research and development to integrate advanced artificial intelligence, machine learning, and blockchain technologies into their core processing engines to improve security and transaction speeds. Market leaders also focus on expanding their embedded finance capabilities, allowing non-financial companies to seamlessly integrate payment, lending, and issuing services directly into their digital ecosystems. Finally, companies prioritize obtaining regulatory licenses in new jurisdictions to facilitate cross-border expansion and ensure compliance with evolving global data protection and anti-money laundering mandates.

MARKET SEGMENTATION

This research report on the global digital payments market has been segmented and sub-segmented based on the type, solution type, deployment mode, organization size, and region.

By Type

- Solutions

- Service

By Solution Type

- Payment Processing

- Payment Gateway

- Payment Wallet

- POS Solution

- Payment Security

- Fraud Management

By Deployment Mode

- On-Premises

- Cloud

By Organization Size

- SMEs

- Large enterprises

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the global digital payments market?

The global digital payments market is the worldwide sector enabling electronic money transfers through digital channels including mobile devices, online platforms, and digital wallets, transforming how consumers and businesses conduct transactions globally.

How does the global digital payments market work?

In the global digital payments market, users initiate transactions through digital platforms, payment processors authenticate and transfer funds between accounts, banks and financial institutions facilitate.money movement while technologies ensure secure transaction processing.

What types exist in the global digital payments market?

The global digital payments market includes digital wallets, mobile payments, contactless transactions, online card payments, peer-to-peer transfers, bank transfers, payment gateway transactions, and real-time payment systems serving diverse transaction needs.

Who uses the global digital payments market?

The global digital payments market serves consumers, businesses, e-commerce retailers, financial institutions, merchants, service providers, international traders, and anyone needing convenient secure electronic transaction capabilities for personal or commercial purposes.

What drives the global digital payments market?

The global digital payments market grows due to increasing smartphone adoption, e-commerce expansion, digital banking growth, consumer preference for convenience, technological advancements, cash-to-digital transition, and globalization of cross-border transaction requirements

Who operates in the global digital payments market?

Major players in the global digital payments market include Visa, Mastercard, PayPal, Apple Pay, Google Pay, Amazon Pay, Square, and numerous fintech companies providing payment processing, digital wallet, and transaction facilitation services worldwide

Is the global digital payments market regulated?

The global digital payments market operates under financial regulations, data protection laws, anti-money laundering requirements, payment security standards, and consumer protection regulations ensuring secure compliant electronic transaction processing across jurisdictions.

What technologies are used in the global digital payments market?

Technologies in the global digital payments market include mobile applications, encryption protocols, tokenization, blockchain, artificial intelligence for fraud detection, biometric authentication, cloud computing, and API integration enabling secure efficient transaction processing.

What are the benefits of the global digital payments market?

The global digital payments market offers benefits including transaction convenience, speed, security, global accessibility, reduced cash handling, real-time processing, automated record keeping, and enhanced customer experience for consumers and businesses worldwide.

What are the challenges of the global digital payments market?

The global digital payments market faces challenges including cybersecurity threats, fraud risks, regulatory complexity across countries, technology infrastructure gaps, digital literacy barriers, and consumer trust concerns affecting adoption in emerging market regions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com