Global Distributed Energy Generation Systems Market Size, Share, Trends, & Growth Forecast Report – Segmented By Technology (Solar PV, Combined Heat and Power, Wind Turbines, Piston Engines, Micro Turbines, and Fuel Cells), End-User (Residential, Commercial and Industrial), Application (Off-Grid and On-Grid), & Region - Industry Forecast From 2024 to 2032

Global Distributed Energy Generation Systems Market Size

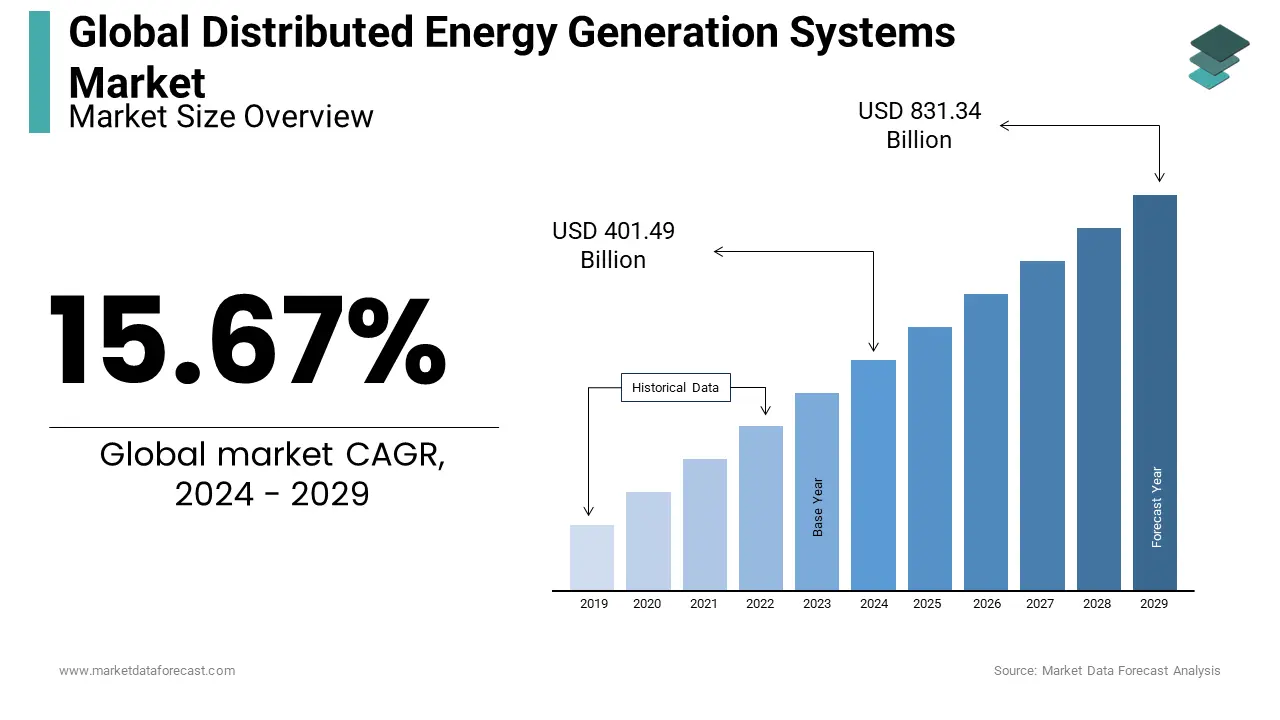

The Global Distributed Energy Generation Systems Market was valued at USD 401.49 billion in 2024 and is estimated to reach USD 1488.19 billion by 2033 from USD 464.40 billion in 2024 and registering a CAGR of 15.67% during the forecast period.

Distributed Energy Generation Systems refer to decentralized energy production units that generate electricity at or near the point of consumption, as opposed to centralized power plants that transmit electricity over long distances. These systems typically include technologies such as solar photovoltaics (PV), small wind turbines, microgrids, fuel cells, and combined heat and power (CHP) units. The growing emphasis on clean energy, energy security, and digitalization in the power sector has significantly propelled the adoption of these systems across residential, commercial, and industrial sectors.

MARKET DRIVERS

Rising Demand for Decentralized and Resilient Power Solutions

One of the primary drivers of the Distributed Energy Generation Systems Market is the increasing demand for decentralized and resilient power solutions, particularly in the wake of rising grid instability and extreme weather events. According to the European Network of Transmission System Operators for Electricity (ENTSO-E), the number of major power outages in Europe increased by 25% between 2018 and 2022, which is prompting both public and private entities to invest in localized energy generation systems. In the United States, the Department of Homeland Security has emphasized the importance of resilient power infrastructure for critical facilities such as hospitals, data centers, and military bases. Moreover, businesses and households are increasingly adopting rooftop solar and battery storage to reduce dependency on centralized utilities and mitigate risks associated with blackouts.

Supportive Government Policies and Renewable Energy Targets

Supportive government policies and ambitious renewable energy targets are playing a crucial role in accelerating the growth of the Distributed Energy Generation Systems Market. Across Europe, North America, and parts of Asia, governments are implementing feed-in tariffs, net metering regulations, tax incentives, and subsidies to encourage the adoption of decentralized energy solutions.

For instance, the European Commission has mandated that member states achieve at least a 42.5% share of renewable energy in their final energy consumption by 2030 under the revised Renewable Energy Directive (RED III). This policy framework has spurred widespread investment in rooftop solar, community microgrids, and behind-the-meter energy storage systems. Similarly, in the United States, the Inflation Reduction Act (IRA) of 2022 introduced significant tax credits for residential and commercial solar installations, making distributed energy generation more financially viable for end-users.

MARKET RESTRAINTS

High Initial Capital Investment and Cost Barriers

High initial capital investment remains a significant barrier to widespread adoption. Technologies such as rooftop solar PV, battery storage, and microgrids require substantial upfront costs for equipment, installation, and system integration. According to the International Renewable Energy Agency (IRENA), the average cost of installing a residential solar-plus-storage system in Europe ranges between €8,000 and €14,000 per kilowatt, depending on system size and local labor rates. Additionally, financing options for distributed energy projects remain limited in many regions, particularly in developing economies where access to credit is constrained. Even in developed markets like the United States and Germany, payback periods for distributed systems often exceed five to seven years, discouraging immediate adoption.

Regulatory and Grid Integration Challenges

Regulatory complexities and grid integration issues pose a major challenge to the expansion of the Distributed Energy Generation Systems Market. Many countries lack standardized regulations for interconnecting distributed energy resources (DERs) with the main grid, leading to inconsistent approval processes and technical barriers. According to the International Energy Agency (IEA), only 18 out of 30 European Union member states had fully harmonized technical standards for DER grid connection as of 2022. Furthermore, the existing electrical grid infrastructure in many regions was designed for centralized power flows and struggles to accommodate bidirectional energy movement from distributed generators. The European Network of Transmission System Operators for Electricity (ENTSO-E) highlights that voltage fluctuations and congestion risks increase as more small-scale producers inject electricity into the grid without adequate coordination. Utilities and regulators are working to implement smart grid technologies and dynamic pricing models, but progress remains slow due to regulatory inertia and resistance from traditional utility operators.

MARKET OPPORTUNITIES

Expansion of Smart Cities and Digital Energy Infrastructure

One of the most promising opportunities for the Distributed Energy Generation Systems Market lies in the rapid development of smart cities and the integration of digital energy infrastructure. Governments and urban planners across Europe, North America, and Asia are investing heavily in smart city initiatives that emphasize sustainability, energy efficiency, and resilience. According to the European Commission's Smart Cities and Communities Initiative, over 100 cities in the EU have launched large-scale smart energy projects since 2020, incorporating distributed solar, microgrids, and intelligent energy management systems. The rise of Internet of Things (IoT)-enabled energy devices and advanced analytics platforms is further enhancing the potential of distributed generation. These technologies allow for real-time monitoring, load balancing, and predictive maintenance, optimizing energy use at both individual and district levels.

Growth of Prosumer Markets and Peer-to-Peer Energy Trading

The emergence of prosumer markets where individuals and businesses both produce and consume electricity is opening up new avenues for growth in the Distributed Energy Generation Systems Market. Enabled by blockchain-based peer-to-peer (P2P) energy trading platforms, prosumers can now sell excess electricity directly to neighbors or local consumers, bypassing traditional utility companies. This model not only empowers consumers but also enhances grid stability by decentralizing energy flows and reducing reliance on centralized infrastructure. In Germany, for example, the number of registered prosumers grew by 18% in 2022, supported by favorable regulatory frameworks and declining solar plus storage costs. The Fraunhofer Institute estimates that decentralized electricity exchanges could account for up to 10% of total retail energy sales in Europe by 2030.

MARKET CHALLENGES

Technological Complexity and System Integration Issues

A major challenge facing the Distributed Energy Generation Systems Market is the technological complexity involved in integrating diverse energy sources, storage units, and control systems into cohesive, efficient, and reliable networks. Unlike conventional power systems that rely on centralized generation, distributed energy setups must manage fluctuating inputs from renewables, variable demand patterns, and grid synchronization requirements. According to the International Electrotechnical Commission (IEC), ensuring interoperability among different hardware and software components remains a persistent obstacle in hybrid systems combining solar, wind, batteries, and diesel generators.

Additionally, the deployment of advanced energy management systems (EMS) and grid-forming inverters requires specialized technical expertise, which is often lacking among smaller installers and end-users. The European Association for Storage of Energy (EASE) reports that over 40% of distributed energy projects face delays due to compatibility issues between equipment from different manufacturers. Standardization efforts are underway, but the absence of universally accepted protocols continues to impede seamless integration and scalability of distributed energy systems across regions.

Cybersecurity Risks in Decentralized Energy Networks

As the Distributed Energy Generation Systems Market expands, cybersecurity threats targeting decentralized energy networks have become an escalating concern. According to the European Union Agency for Cybersecurity (ENISA), the number of reported cyber incidents in the energy sector increased by 38% between 2020 and 2022, with distributed energy systems being particularly vulnerable due to their decentralized nature and reliance on digital communication. The proliferation of Internet of Things (IoT)-based energy management platforms has introduced new entry points for malicious actors seeking to manipulate grid operations, steal consumer data, or disrupt power supply. The U.S. Department of Energy warns that inadequate encryption, weak authentication mechanisms, and outdated firmware in distributed energy devices pose serious risks to grid stability. Addressing these vulnerabilities requires robust cybersecurity frameworks, continuous threat monitoring, and industry-wide collaboration to ensure the secure and resilient operation of next-generation decentralized energy infrastructures.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 15.67% |

| Segments Covered | By Technology, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Siemens AG, General Electric Company, Schneider Electric, Mitsubishi Motors Corporation, Capstone Turbine Corporation, ABB, MCV Energy, Johnson Controls, NEC Energy Solutions, and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

The solar photovoltaic (PV) segment dominated the global Distributed Energy Generation Systems Market by accounting for 43.3% of share in 2024 with the declining cost of solar panels and installation, which has made decentralized solar generation increasingly accessible. Additionally, government incentives such as feed-in tariffs, net metering policies, and tax credits have further accelerated deployment in countries like Germany, the United States, and Japan. Another major driver is the increasing integration of solar PV with battery storage by enabling consumers to manage energy consumption more efficiently.

The fuel cell segment is likely to grow with a CAGR of 11.8% fro2025 5 to 2033. A significant growth driver is the rising demand for clean and reliable backup power solutions, particularly in data centers, healthcare facilities, and remote operations where an uninterrupted energy supply is crucial. Additionally, hydrogen-based fuel cells are gaining traction as part of decarbonization strategies, especially in sectors difficult to electrify through conventional means. The International Energy Agency (IEA) estimates that hydrogen demand could grow by 50% by 2030, with fuel cells playing a pivotal role in distributed energy portfolios.

By End-User Insights

The residential segment was the largest and held 39.8% of the Distributed Energy Generation Systems Market share in 2024 with the growing consumer awareness and preference for self-generated electricity, particularly in regions with high retail electricity prices. For example, in Germany, the Federal Network Agency (Bundesnetzagentur) reported that more than 2.2 million households had installed rooftop solar systems by the end of 2022, many of which were coupled with home battery storage to maximize energy utilization. Additionally, government subsidies and net metering programs have played a crucial role in accelerating residential adoption. In the United States, the Solar Energy Industries Association (SEIA) noted that over 40 states offered net metering policies in 2022 by allowing homeowners to sell excess electricity back to the grid and improve return on investment. Coupled with falling system costs and rising environmental consciousness, these incentives continue to drive robust growth in the residential segment.

The industrial segment is likely to gain huge traction with a CAGR of 10.6% from 2025 to 2033 with the increasing deployment of microgrids and combined heat and power (CHP) systems in large-scale industrial complexes. Moreover, rising energy demands in emerging economies are prompting industries to adopt distributed generation as a reliable alternative to unstable national grids.

By Application Insights

The on-grid application segment was the largest and held a prominent share of the distributed energy generation systems market share in 2024 with the availability of net metering and feed-in tariff mechanisms, which allow consumers to generate their own electricity and sell surplus power back to utilities. Additionally, smart grid modernization initiatives are facilitating seamless bidirectional power flow between distributed generators and the central grid. The U.S. Department of Energy notes that between 2020 and 2022, more than $12 billion was invested in smart grid technologies by enhancing grid stability and supporting the expansion of on-grid distributed energy systems.

The off-grid application segment is likely to grow with an expected CAGR of 12.3% from 2025 to 2033. One of the key growth drivers is the expansion of off-grid solar and hybrid energy systems in developing economies in Sub-Saharan Africa and parts of South Asia. According to the International Renewable Energy Agency (IRENA), over 20 million people gained access to electricity through off-grid solar solutions in 2022, which is reducing reliance on diesel generators and kerosene lighting. Additionally, microgrid deployments in industrial and military applications are accelerating, providing secure and resilient power for mines, agricultural projects, and disaster relief operations.

REGIONAL ANALYSIS

Europe Distributed Energy Generation Systems Market Insights

Europe was the top performer in the global distributed energy generation systems market by accounting for 24.3% of share in 2024. One of the primary growth drivers is the European Green Deal, which mandates member states to achieve climate neutrality by 2050. Under this initiative, several countries have introduced financial incentives, streamlined permitting processes, and updated grid codes to support distributed generation. Furthermore, the proliferation of prosumer models and peer-to-peer energy trading platforms has empowered consumers to actively participate in energy markets.

North America Distributed Energy Generation Systems Market Insights

North America was the top performer by holding 27.6% of the global Distributed Energy Generation Systems Market in 2024. The Solar Energy Industries Association (SEIA) reported that U.S. solar installations reached a record 24 gigawatts of capacity in 2022, with distributed generation accounting for nearly half of all new deployments. Additionally, California’s Self-Generation Incentive Program (SGIP) has spurred widespread adoption of battery storage, enabling consumers to optimize energy use and reduce peak demand charges. Moreover, utilities and independent power producers are investing heavily in microgrids , particularly in response to increasing climate-related disruptions.

Asia-Pacific Distributed Energy Generation Systems Market Insights

Asia-Pacific Distributed Energy Generation Systems Market was positioned second by holding 11.2% of the share in 2024. A major growth catalyst is the rising deployment of rooftop solar systems in China and India, where governments have launched aggressive renewable energy campaigns. Additionally, Southeast Asian nations are embracing off-grid and microgrid systems to provide electricity access in remote and island communities.

Latin America Distributed Energy Generation Systems Market Insights

Latin America distributed energy generation systems market growth is esteemed to have a prominent growth opportunities in the next coming years. One of the key growth drivers is the expansion of rooftop solar installations in Brazil, Chile, and Mexico, where regulatory reforms and net metering policies have created favorable conditions for distributed generation. Additionally, off-grid and microgrid projects are gaining traction in remote communities, particularly in Andean and Amazonian regions where grid connectivity remains a challenge. The World Bank notes that Colombia and Peru have launched over 200 decentralized energy projects since 2020, funded through public-private partnerships and international grants.

Middle East & Africa Distributed Energy Generation Systems Market Insights

The Middle East and Africa Distributed Energy Generation Systems Market growth is propelled with immense potential, both sub-regions are leveraging distributed energy solutions to enhance energy access, reduce reliance on fossil fuels, and improve grid resilience. In Africa, the deployment of off-grid solar and microgrid systems is addressing energy poverty, especially in Sub-Saharan countries. According to the World Bank, over 20 million people gained electricity access through decentralized solutions in 2022, with Kenya, Nigeria, and Ethiopia leading adoption efforts.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies prominent in the global distributed energy generation systems market include Siemens AG, General Electric Company, Schneider Electric, Mitsubishi Motors Corporation, Capstone Turbine Corporation, ABB, MCV Energy, Johnson Controls, NEC Energy Solutions, and Others.

The competition in the Distributed Energy Generation Systems Market is marked by a dynamic mix of established multinational corporations, agile technology startups, and regional energy solution providers striving to capture growing opportunities in decentralized power generation. While large players leverage their technological expertise, financial strength, and global distribution networks to maintain dominance, smaller innovators are gaining traction by introducing niche products, flexible financing models, and rapid deployment capabilities. The market landscape is further shaped by increasing convergence between energy, information technology, and telecommunications, enabling smarter and more responsive distributed systems.

Innovation remains a key battleground, with companies focusing on modular designs, hybrid configurations, and integrated digital platforms that offer enhanced control and optimization of distributed assets. Additionally, the rising emphasis on sustainability, energy independence, and resilience is driving demand for clean, localized power solutions across both developed and emerging economies. Regulatory support, evolving consumer preferences, and advancements in storage and grid-forming technologies are also influencing competitive dynamics, which is prompting firms to continuously refine their value propositions and operational strategies to stay ahead in this fast-paced sector.

Top Players in the Distributed Energy Generation Systems Market

Siemens Energy

Siemens Energy is a leading global player in the Distributed Energy Generation Systems Market, offering advanced decentralized energy solutions including microgrids, combined heat and power systems, and digital energy management platforms. The company plays a pivotal role in enabling smart and sustainable energy infrastructure by integrating renewable sources with grid stability technologies. Its comprehensive portfolio supports utilities, industries, and municipalities in transitioning toward resilient and low-carbon energy systems. Siemens’ commitment to innovation and digitalization has made it a trusted partner for governments and enterprises seeking efficient and future-ready distributed energy deployments worldwide.

Schneider Electric

Schneider Electric is a key participant in the Distributed Energy Generation Systems Market, delivering cutting-edge solutions such as solar inverters, battery management systems, and energy automation software. The company's EcoStruxure platform enables seamless integration of decentralized energy assets, enhancing efficiency and reliability for residential, commercial, and industrial users. With a strong focus on sustainability and electrification, Schneider supports the global shift toward decentralized, digitized, and decarbonized energy systems. Its strategic partnerships and localized offerings have strengthened its market presence across diverse regions, which is making it a major force in shaping the future of distributed energy generation.

ABB Ltd.

ABB is a prominent contributor to the Distributed Energy Generation Systems Market, providing modular power solutions, microgrid controllers, and grid-interactive technologies that enhance the performance of decentralized energy networks. The company’s expertise in power electronics and automation enables efficient integration of renewables, storage, and traditional generation sources. ABB supports a wide range of applications including remote off-grid communities, industrial campuses, and utility-scale distributed projects. Through continuous R&D and strategic collaborations, ABB helps accelerate the deployment of intelligent and adaptive energy systems, reinforcing its position as a global leader in the evolving distributed energy landscape.

Major Strategies Used by Key Market Participants

A primary strategy employed by key players in the Distributed Energy Generation Systems Market is technology integration and digitalization, where companies combine hardware with advanced software solutions to optimize system performance and enable real-time monitoring. Another critical approach is strategic partnerships and joint ventures, through which companies collaborate with local developers, utilities, and technology providers to expand market reach and tailor solutions to regional needs. These alliances facilitate access to new geographies, regulatory expertise, and complementary innovations, strengthening competitive positioning in the rapidly evolving distributed energy space.

The product diversification and customization allow market leaders to cater to varied end-users by offering scalable, modular, and application-specific distributed energy systems. This strategy ensures adaptability across residential, commercial, and industrial sectors, fostering long-term customer engagement and sustained growth in a dynamic and fragmented market environment.

RECENT MARKET DEVELOPMENTS

- In February 2023, Siemens Energy launched a next-generation microgrid controller designed to enhance grid stability and integrate multiple renewable energy sources, which is supporting decentralized power systems in remote and urban settings.

- In July 2023, Schneider Electric partnered with a leading battery manufacturer to co-develop an all-in-one energy storage and management solution tailored for residential and small commercial solar installations across Europe and North America.

- In November 2023, ABB introduced a modular hybrid power system specifically aimed at industrial and mining clients, combining solar, diesel generators, and battery storage to reduce fuel consumption and carbon emissions in off-grid operations.

- In March 2024, General Electric Digital expanded its distributed energy management software suite with new AI-driven predictive maintenance features by allowing utilities and prosumers to optimize asset performance and minimize downtime.

- In June 2024, Honeywell launched a cloud-based distributed energy resource management system (DERMS) to help utilities manage bidirectional power flows from rooftop solar, electric vehicles, and behind-the-meter storage, improving grid efficiency and reliability.

MARKET SEGMENTATION

This research report on the global distributed energy generation systems market has been segmented and sub-segmented based on technology, end-user, and region.

By Technology

- Solar PV

- Combined Heat and Power

- Wind Turbines

- Piston Engines

- Micro Turbines

- Fuel Cells

By End-User

- Residential

- Commercial

- Industrial

By Application

- Off-Grid

- On-Grid Network

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the Distributed Energy Generation Systems Market growth rate during the projection period?

The Global Distributed Energy Generation Systems Market is expected to grow with a CAGR of 15.67% between 2025-2033.

What can be the total Distributed Energy Generation Systems Market value?

The Global Distributed Energy Generation Systems Market size is expected to reach a revised size of USD 1488.19 bn by 2033.

Name any three Distributed Energy Generation Systems Market key players?

General Electric Company, Schneider Electric, and Mitsubishi Motors Corporation are the three Distributed Energy Generation Systems Market key players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com