Global Enterprise Software Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Deployment Type, Application, and Region – Industry Forecast From 2026 to 2034

Global Enterprise Software Market Size

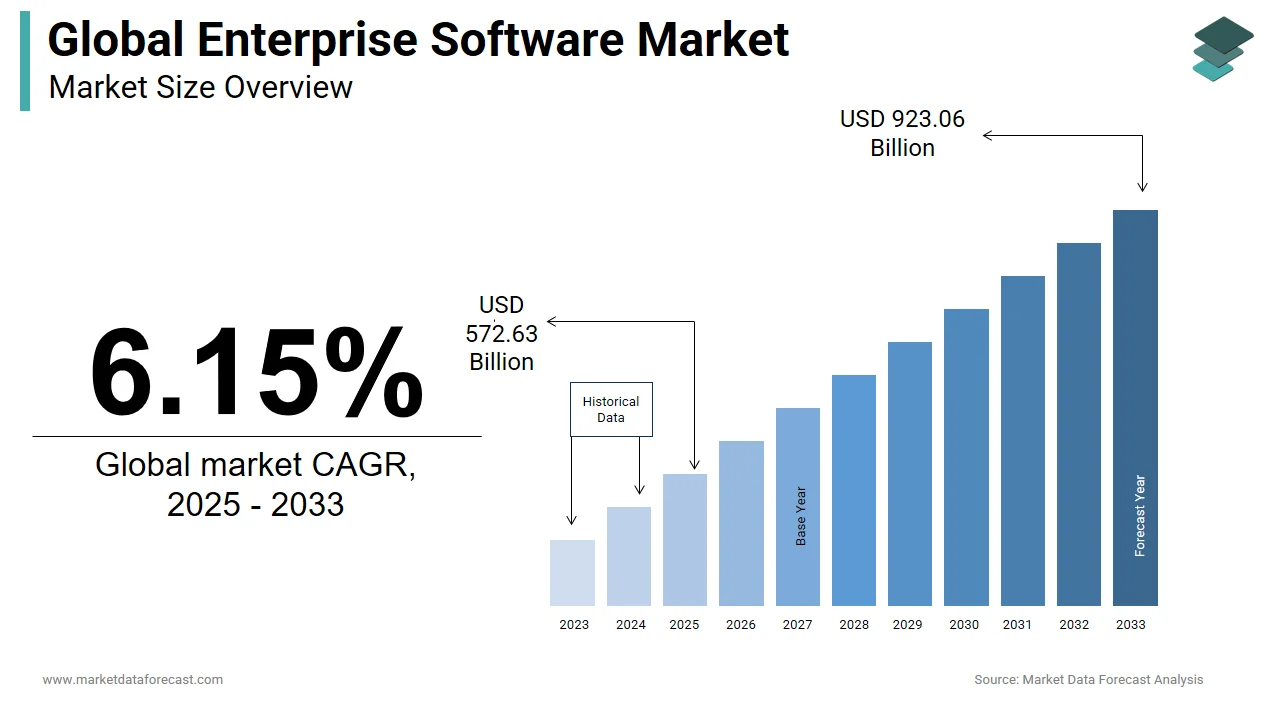

The size of the global enterprise software market was worth USD 572.63 billion in 2025. The global market is anticipated to reach USD 979.84 billion by 2034 from USD 607.85 billion in 2025, growing at a CAGR of 6.15% from 2026 to 2036.

Enterprise software is computer software used by large organizations to manage and automate their day-to-day operations. This domain includes customer relationship management systems enterprise resource planning platforms and supply chain management tools that serve as the digital backbone of modern corporations. As organizations navigate an increasingly interconnected global economy the reliance on integrated software ecosystems has become indispensable for maintaining competitive agility and operational transparency. The definition extends beyond mere automation to include intelligent decision support systems that leverage real time data analytics. According to research, the global datasphere, the total volume of data created, captured, copied, and consumed worldwide, was projected to reach 175 zettabytes by 2025. Research highlights that nearly 30% of this global data pool is processed in real-time, necessitating an industry-wide migration from legacy enterprise hardware endpoints to localized edge and centralized cloud-native storage repositories. Furthermore, as documented in a comprehensive labor study released by the World Bank Group, technology-driven automation produces complex trade-offs between labor efficiency and workforce headcount. The data demonstrates that while advanced digital solutions systematically boost medium-term output, a 10% technology-driven leap in labor productivity corresponds with a 1% contraction in overall employment within emerging market and developing economies (EMDEs) during the initial year of adoption. The market is not merely about selling licenses but about enabling digital transformation strategies that redefine business models. With remote work becoming a permanent fixture for many entities, the demand for cloud-based collaborative enterprise tools has surged, fundamentally altering how businesses perceive software utility and integration requirements in their daily workflows.

MARKET DRIVERS

Accelerated Digital Transformation Initiatives Driving Operational Efficiency

The urgent mandate for digital transformation across traditional industries is the main factor propelling the enterprise software market. Organizations are no longer viewing technology as a support function but as a core strategic asset essential for survival and growth. This shift is driven by the need to streamline operations, reduce manual errors, and enhance decision-making speed through automated workflows. Research confirms that successful enterprise agility transformations drive a 20% to 30% improvement in employee engagement and highly correlated gains in customer satisfaction by realigning internal operational models around customer-centric journeys. The demand is particularly acute in sectors such as manufacturing and logistics, where real-time visibility into supply chains is crucial. For instance, the adoption of Internet of Things-enabled enterprise software allows firms to predict maintenance needs and optimize inventory levels dynamically. According to sources, over 75 percent of large enterprises will have adopted at least four low-code or no-code development tools for both IT application development and citizen development initiatives. This democratization of software creation accelerates deployment times and reduces dependency on specialized technical teams. Consequently, businesses are investing heavily in modular and scalable software architectures that can adapt to changing market conditions rapidly. The pressure to deliver seamless customer experiences across multiple touchpoints further compels organizations to integrate disparate systems into unified platforms, thereby fueling sustained demand for comprehensive enterprise software solutions that offer end-to-end process automation and analytics capabilities.

Surge in Remote and Hybrid Work Models Necessitating Collaborative Tools

The structural shift toward remote and hybrid work environments is a powerful driver of the enterprise software market. This trend fundamentally changes how teams interact and collaborate. With physical offices no longer serving as the central hub for all business activities, organizations require robust digital infrastructure to maintain productivity and cohesion among distributed workforces. This transition has amplified the need for cloud-based communication project management and human capital management solutions that ensure continuity regardless of geographical location. According to a study by Stanford University, working from home increases performance by 13 percent due to fewer breaks and sick days, plus a quieter working environment, which validates the operational viability of remote arrangements. To support this model, enterprises are deploying advanced collaboration suites that integrate video conferencing, instant messaging, and document sharing into a single interface. As per official financial disclosures released by Microsoft Corporation, the platform surpassed 280 million monthly active users as of January 2023, expanding further to 320 million MAUs by late 2023 to solidify its market footprint across unified enterprise collaboration, cloud calling, and application integration environments. Furthermore, the need to monitor employee well-being and productivity without invasive surveillance has led to the rise of people analytics platforms within enterprise software portfolios. These tools help managers understand work patterns and identify burnout risks, ensuring sustainable productivity levels. The permanence of hybrid work models means that investment in these digital collaboration frameworks is not a temporary measure but a long-term strategic imperative driving continuous innovation and expansion in the enterprise software market.

MARKET RESTRAINTS

Complexity of Legacy System Integration Impeding Agile Deployment

The profound difficulty associated with integrating new modern solutions with existing legacy systems is a significant restraint to the enterprise software market. Many large corporations operate on outdated infrastructure that was not designed to communicate with contemporary cloud based applications creating substantial technical debt and interoperability challenges. This fragmentation leads to data silos where critical information remains trapped in isolated systems preventing organizations from achieving a unified view of their operations. Enterprise architecture data compiled by Deloitte Consulting LLP highlights legacy modernization as a structural priority for security, compliance, and AI integration. However, projects regularly face timeline adjustments due to complex dependencies, making thorough data mapping and phase-based governance essential to managing corporate budget constraints. Studies show that 60% to 80% of corporate IT budgets are consumed by maintenance ('keeping the lights on'), severely restricting capital allocations for competitive software innovation and digital transformation. Technical deployment frameworks published by Accenture PLC emphasize that data silos and disparate legacy schemas represent primary roadblocks in ERP overhauls. Mitigating these integration delays requires structural investments in automated semantic data middleware and unified data lakes to ensure clean cross-system compatibility. This lag time reduces the return on investment and discourages smaller firms from adopting advanced software solutions. Additionally the risk of data loss or corruption during migration processes creates hesitation among decision makers who fear operational disruptions. The shortage of skilled professionals who understand both ancient coding languages and modern architecture further exacerbates this issue making it a persistent barrier to widespread and rapid enterprise software adoption across established industries.

Stringent Data Privacy Regulations Increasing Compliance Burdens

The escalating landscape of global data privacy regulations is a formidable barrier to the enterprise software market. This imposes rigorous compliance requirements that increase operational costs and complexity. Governments worldwide are enacting stricter laws to protect consumer data forcing software vendors and their clients to implement robust security measures and transparent data handling practices. The General Data Protection Regulation in Europe and the California Consumer Privacy Act in the United States set high standards for data consent storage and deletion which enterprise software must strictly adhere to. A study showed that approximately 12% of large international firms allocated over $10 million toward data compliance frameworks. This operational investment aligns with avoiding severe regulatory exposure under the EU General Data Protection Regulation (GDPR), which allows penalties up to €20 million or 4% of worldwide annual turnover. This financial burden is particularly heavy for mid sized enterprises that lack the resources of larger competitors. As per IBM the global average cost of a data breach reached 4.45 million dollars in 2023 highlighting the severe financial risks associated with non compliance or security failures. These regulations also limit the ability of software providers to utilize customer data for training artificial intelligence models or improving services without explicit consent thereby stifling innovation potential. Furthermore the fragmented nature of international privacy laws requires enterprises to customize their software configurations for different jurisdictions adding layers of administrative overhead. This regulatory uncertainty often leads to delayed product launches and increased legal scrutiny which dampens the pace of market expansion and forces vendors to prioritize compliance over feature development.

MARKET OPPORTUNITIES

Expansion of Artificial Intelligence Capabilities Enhancing Predictive Analytics

The deep integration of artificial intelligence and machine learning capabilities to enhance predictive analytics and decision making is a major opportunity for the enterprise software market. As businesses generate unprecedented volumes of data the ability to extract actionable insights from this information becomes a key competitive differentiator. Enterprise software vendors are increasingly embedding AI driven modules that can forecast market trends optimize supply chains and personalize customer interactions in real time. According to research published by Salesforce, Inc., 84% of CIOs and IT leaders state that AI will have a significant or transformative impact on their organizational productivity, driving accelerated enterprise deployment of autonomous agents, CRM intelligence, and data integration engines. This trend opens avenues for vendors to offer premium tiers of service that provide advanced analytical tools previously accessible only to tech giants. By leveraging natural language processing and computer vision enterprise applications can automate complex tasks such as contract review and quality control thereby reducing operational costs significantly. Moreover the rise of generative AI offers opportunities for creating dynamic content and personalized marketing campaigns directly within customer relationship management platforms. This evolution transforms enterprise software from passive record keeping tools into proactive strategic partners that drive revenue growth and operational efficiency. Vendors who successfully integrate these intelligent capabilities can capture greater market share and command higher pricing power due to the tangible value delivered through enhanced automation and insight generation.

Growth of Industry Specific Cloud Solutions Addressing Niche Needs

The growing demand for industry-specific cloud solutions provides a clear path for the enterprise software market. These platforms are designed to address the specific regulatory and operational needs of vertical markets. Generic enterprise software often fails to address the nuanced needs of sectors such as healthcare finance and manufacturing leading to a gap that specialized vendors can fill. These tailored solutions offer pre configured workflows compliance frameworks and terminology that resonate with industry professionals reducing implementation time and training costs. Longitudinal data from the Flexera State of the Cloud Report highlighted that during peak pandemic digital acceleration, 92% of large enterprises adopted a multi-cloud architecture. This operational framework has matured into hybrid governance models focused on taming cross-platform complexity and integrating specialized SaaS endpoints. In the healthcare sector for instance enterprise software that integrates electronic health records with billing and compliance modules is seeing rapid adoption due to its ability to streamline patient care and administrative processes. Research underscores a massive surge in enterprise demand for industry-specific vertical clouds. Driven by regulatory compliance, digital sovereignty laws (like GDPR), and specialized data models, vertical cloud applications remain among the fastest-expanding segments within the broader enterprise cloud ecosystem. This specialization allows vendors to build deeper relationships with clients by offering consultative services and continuous updates aligned with industry changes. Furthermore niche solutions often benefit from network effects within specific professional communities leading to higher retention rates and lower churn. By focusing on verticals enterprise software providers can differentiate themselves in a crowded market and achieve sustainable growth through targeted innovation that directly solves pressing industry specific pain points rather than offering one size fits all functionalities.

MARKET CHALLENGES

Shortage of Skilled Technical Talent Hindering Implementation Success

The acute shortage of skilled technical talent required to implement, manage, and optimize complex software systems is one of the most pressing challenges facing the enterprise software market. As enterprises adopt more sophisticated technologies such as artificial intelligence blockchain and advanced analytics the demand for professionals with specialized expertise far exceeds the available supply. This talent gap leads to prolonged implementation cycles increased project costs and suboptimal utilization of software capabilities. According to sources there could be a global shortfall of 85 million workers by 2030 if current hiring trends continue with the technology media and telecommunications sector facing some of the most severe shortages. As per CompTIA the tech industry added approximately 200000 net new jobs in the United States alone in 2022 yet vacancies remain unfilled due to a lack of qualified candidates. This scarcity forces companies to compete aggressively for talent driving up salary expectations and increasing turnover rates which disrupts continuity in software projects. Moreover the rapid pace of technological change means that existing employees require constant upskilling to remain effective placing additional strain on organizational resources. Without adequate human capital even the most advanced enterprise software cannot deliver its promised value leading to frustration among stakeholders and potential abandonment of digital initiatives. Addressing this challenge requires a concerted effort from both vendors and clients to invest in training programs and develop more intuitive user interfaces that reduce the dependency on highly specialized technical staff for routine operations.

Escalating Cybersecurity Threats Undermining Trust and Adoption

The escalating frequency and sophistication of cybersecurity threats pose a significant hurdle for the enterprise software market. This undermines trust and complicates the adoption of new technologies. As enterprise systems become more interconnected and cloud based they present larger attack surfaces for malicious actors seeking to steal sensitive data or disrupt operations. High profile breaches erode confidence in software vendors and force organizations to adopt a cautious approach to digital transformation. A study revealed that 74 percent of all breaches included the human element with people being involved via error privilege misuse use of stolen credentials or social engineering. As per Cybersecurity Ventures cybercrime damages are predicted to cost the world 10.5 trillion dollars annually by 2025 highlighting the massive economic impact of these security failures. This threat landscape necessitates continuous investment in security infrastructure encryption and monitoring tools which adds to the total cost of ownership for enterprise software. Vendors must constantly update their products to patch vulnerabilities and comply with evolving security standards which can slow down innovation cycles. Furthermore the fear of reputational damage and legal liability makes chief information officers hesitant to migrate critical workloads to new platforms. This caution acts as a brake on market growth as organizations prefer to stick with known albeit outdated systems rather than risk exposure to novel threats. Ensuring robust security therefore remains a critical hurdle that vendors must overcome to sustain momentum in the enterprise software sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Deployment Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Microsoft Corporation, Infor Inc., Kronos Incorporated, IBM Corporation, SAP AG, Oracle Corporation, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The Application Software segment dominated the enterprise software market and accounted for a substantial share in 2025. This dominance of the segment was driven by its direct impact on core business functions and operational efficiency. Organizations rely on integrated digital platforms to manage customers, streamline supply chains, and optimize resources, fueling this segment's growth. The widespread adoption of Customer Relationship Management systems allows firms to personalize interactions and improve retention rates which are vital in competitive markets. According to Salesforce companies using CRM solutions see an average increase of 29 percent in sales productivity demonstrating tangible returns on investment. Furthermore Enterprise Resource Planning systems provide a unified view of financial and operational data enabling better strategic decision making. The integration of Business Intelligence tools within application suites empowers managers to visualize complex data sets and identify trends rapidly. Research emphasize that enterprise demand is shifting rapidly toward intelligence-infused applications. Driven by big data ecosystems, organizations are prioritizing investments in predictive analytics and data pipeline automation to anchor structural market intelligence. This segment leads because it addresses immediate pain points related to workflow automation and customer engagement making it indispensable for modern enterprises seeking agility and growth in a digital first economy.

On the other hand, the Software as a Service segment is estimated to register the fastest CAGR of 18.3% from 2026 to 2034 due to its flexibility scalability and lower upfront costs compared to traditional on premise solutions. This rapid expansion is further driven by the increasing preference for subscription based models that allow businesses to adjust their software usage according to fluctuating demand without significant capital expenditure. The Flexera State of the Cloud Report reveals that 89% of enterprise organizations operate a multi-cloud strategy. Flexera’s structural insights indicate this architecture is driven by a desire to avoid vendor lock-in, balance specialized public cloud workloads, and optimize hybrid cloud infrastructure costs across multiple cloud vendors. The ability to access applications from any location supports the global trend toward remote and hybrid work environments ensuring business continuity regardless of physical office presence. Technical whitepapers published by Microsoft Corporation outline that migrating legacy infrastructure to managed cloud ecosystems minimizes internal IT overhead related to continuous server maintenance, server patching, and physical security upgrades. This structural shift allows enterprise tech teams to reallocate internal capital toward strategic application engineering and digital adoption. SaaS providers continuously deliver new features and security patches automatically ensuring that clients always operate on the latest version without disruption. This model also facilitates faster deployment times allowing organizations to realize value from their software investments more quickly than with traditional licensing models. The scalability of SaaS enables small and medium sized enterprises to access enterprise grade tools that were previously affordable only to large corporations thereby expanding the total addressable market significantly.

By Deployment Type Insights

In 2025, the Proprietary Software segment held the majority share of the market because of the need for customized solutions that align precisely with unique organizational processes and security requirements. Large enterprises often prefer proprietary deployments because they offer greater control over data infrastructure and the ability to tailor functionalities to specific industry regulations. This segment dominates in sectors where intellectual property protection and competitive differentiation are paramount as custom built software provides features that off the shelf solutions cannot match. The long term ownership model appeals to companies with stable IT budgets that prefer capital expenditure over recurring operational expenses. Furthermore proprietary systems allow for deeper integration with legacy hardware and specialized machinery particularly in manufacturing environments where standard interfaces may not suffice. The ability to own the source code ensures that businesses are not dependent on vendor roadmaps for critical updates giving them autonomy over their technological evolution and risk management strategies in highly regulated or competitive industries.

However, the application service providers segment is anticipated to witness the fastest CAGR of 15.5% during the forecast period. This is because organizations increasingly outsource complex IT management tasks to focus on core competencies. The shortage of skilled developers and the growing complexity of internal software systems are driving this segment’s growth. These providers offer expertise in monitoring performance managing security patches and ensuring high availability which reduces the operational burden on internal teams. Application Service Providers also facilitate quicker adoption of new technologies by handling the technical intricacies of implementation and integration. This model is particularly attractive to mid sized enterprises that lack the resources to build extensive in house IT departments but still require robust software support. The flexibility to scale services up or down based on business needs allows companies to remain agile while benefiting from the provider's economies of scale and specialized knowledge in emerging technologies such as artificial intelligence and cloud security.

By Application Insights

The Customer Information Management segment led the enterprise software market and captured a significant share in 2025. This leading position of the segment was attributed to the critical importance of understanding and engaging customers in a highly competitive global economy. Organizations prioritize this application because it consolidates data from multiple touchpoints to create a unified view of the customer journey enabling personalized marketing and improved service delivery. As per Salesforce 76 percent of customers expect consistent interactions across departments which necessitates robust information management systems that break down data silos. This segment dominates because effective customer data management directly correlates with increased retention rates and higher lifetime value. The integration of artificial intelligence into these systems allows for predictive analytics that anticipate customer needs and preferences before they are explicitly stated. Furthermore stringent data privacy regulations such as the General Data Protection Regulation require sophisticated management tools to ensure compliance while maintaining data utility. According to sources, the global volume of unstructured and real-time machine data is expanding at unprecedented scales. This rapid influx forces modern organizations to transition from legacy, manual ingestion pipelines to highly automated Customer Data Platforms (CDPs) capable of sorting compliance-heavy enterprise metrics synchronously. This application remains central to business strategy as it transforms raw data into actionable intelligence that drives sales marketing and support efficiencies across the organization.

On the contrary, the energy management segment is likely to experience the fastest CAGR of 12.2% over the forecast period owing to increasing regulatory pressure for sustainability and the rising cost of energy resources. Organizations are adopting enterprise software to monitor optimize and reduce energy consumption across facilities and operations as part of broader environmental social and governance initiatives. According to energy optimization analyses published by the International Energy Agency (IEA), the smart deployment of digital tech, such as learning algorithms, smart lighting, and IoT thermostats, can cut total energy use within commercial and residential buildings by 10%. On a wider scale, research supported by the World Economic Forum (WEF) notes that digital solutions across the highest-emitting industrial sectors could help reduce global greenhouse gas emissions by up to 20% by 2050. This growth is driven by the need for real time visibility into energy usage patterns which allows firms to identify inefficiencies and implement corrective measures immediately. Energy management systems integrate with Internet of Things sensors to automate lighting heating and cooling systems based on occupancy and weather conditions leading to significant cost savings. The rise of renewable energy sources also requires sophisticated software to manage grid integration and storage efficiently. Furthermore, government incentives and tax credits for green initiatives encourage adoption of these tools. Corporate sustainability goals are becoming increasingly ambitious. Consequently, the demand for precise data tracking and reporting capabilities provided by energy management software will continue to accelerate rapidly across all industrial sectors.

REGIONAL ANALYSIS

North America Enterprise Software Market Analysis

North America was the top performer in the global enterprise software market and accounted for a 40.5% share in 2025. This position of the North American market was driven by its advanced technological infrastructure and early adoption of digital solutions. The region benefits from a high concentration of leading software vendors and a business culture that prioritizes innovation and efficiency. As per the Bureau of Labor Statistics the United States alone adds thousands of tech jobs annually reflecting the robust demand for skilled professionals who drive software implementation and development. The presence of major technology hubs in Silicon Valley Seattle and New York fosters a competitive ecosystem that accelerates product development and market penetration. According to the National Science Foundation business expenditure on research and development in the computer and electronic products sector exceeds 100 billion dollars annually fueling continuous innovation. Furthermore the widespread availability of high speed internet and cloud infrastructure supports the seamless deployment of enterprise applications across various industries. Regulatory frameworks such as the California Consumer Privacy Act also drive demand for compliant software solutions. The mature venture capital landscape provides ample funding for startups developing niche enterprise tools ensuring a steady pipeline of innovative products. This combination of technical expertise financial resources and supportive infrastructure solidifies North America's leadership in shaping global enterprise software trends and standards.

Europe Enterprise Software Market Analysis

Europe was the next prominent region in the enterprise software market and captured a 25.7% share in 2025. This growth of the European market was supported by the widespread implementation of the General Data Protection Regulation which sets high standards for data handling. The regional market shows a rigorous focus on data privacy and regulatory compliance which shapes software development and adoption patterns. As reported by Eurostat official ICT usage data, 53% of enterprises across the European Union used paid cloud computing services. The data reveals that adoption is highly concentrated in standard software-as-a-service (SaaS) utilities, with 85.2% using it for e-mail and 71.7% for office software. Countries like Germany France and the United Kingdom are leading adopters leveraging enterprise software to enhance manufacturing efficiency and service delivery. Under the legislative framework established by the European Commission's Digital Decade Policy Programme, the European Union targets a minimum of 75% of EU enterprises to adopt cloud computing services, big data analytics, and/or artificial intelligence (AI) by 2030 to secure structural digital competitiveness. The region's strong industrial base particularly in automotive and pharmaceuticals requires sophisticated supply chain and quality management software. Furthermore the push for digital sovereignty encourages the development of local European software providers who offer alternatives to US dominated platforms. This focus on security and local control combined with substantial government funding for digital transformation projects ensures that Europe remains a critical and dynamic market for enterprise software vendors globally.

Asia Pacific Enterprise Software Market Analysis

Asia Pacific is the quickest expanding region in the enterprise software market due to rapid digitalization efforts in major economies such as China India and Japan. The region is witnessing a surge in adoption due to the expansion of the middle class increasing smartphone penetration and government initiatives promoting smart cities and digital economies. According to research endorsed by the Asian Development Bank (ADB) Southeast Asia Development Solutions (SEADS), the digital economy of Southeast Asia (ASEAN) alone is projected to reach $1 trillion in gross merchandise value (GMV) by 2030, driven by the acceleration of e-commerce, digital financial services, and structural digital transformation. China leads in terms of volume due to its massive manufacturing sector adopting industrial internet of things and supply chain management solutions. According to the Ministry of Industry and Information Technology in China the scale of the industrial internet platform market has grown significantly supporting millions of connected devices. India is seeing rapid growth in the service sector with widespread adoption of customer relationship management and human resource software to manage its large workforce. Japan focuses on robotics and automation software to address labor shortages in an aging society. The increasing availability of affordable cloud services and mobile internet infrastructure lowers barriers to entry for small and medium enterprises. This dynamic mix of industrial modernization and service sector expansion positions Asia Pacific as a pivotal growth engine for the global enterprise software market in the coming decade.

Latin America Enterprise Software Market Analysis

Latin America is expected to showcase a promising CAGR in the enterprise software market owing to increasing internet connectivity and a growing startup ecosystem. The region is gradually adopting cloud based solutions to overcome infrastructure limitations and improve operational efficiency in key sectors such as retail banking and telecommunications. As per the Economic Commission for Latin America and the Caribbean digital transformation is seen as a key driver for post pandemic economic recovery with many governments investing in digital public infrastructure. Brazil and Mexico are the largest markets in the region driven by their sizable industrial bases and increasing foreign direct investment in technology. The rise of fintech companies in the region has spurred demand for secure and scalable software platforms that can handle high transaction volumes. Additionally the need to formalize informal business sectors is driving adoption of basic enterprise resource planning and accounting software. While challenges such as currency volatility and regulatory uncertainty persist the growing awareness of digital benefits among business leaders is accelerating adoption. Local partnerships with global vendors are helping to customize solutions for regional needs ensuring that enterprise software becomes more accessible and relevant to Latin American businesses.

Middle East and Africa Enterprise Software Market Analysis

The Middle East and Africa region is witnessing gradual but steady growth in the enterprise software market due to government led digital transformation initiatives and diversification efforts away from oil dependence. Countries in the Gulf Cooperation Council are investing heavily in smart city projects and digital government services which require robust enterprise software infrastructure. Saudi Arabia and the United Arab Emirates are leading the way with national visions that prioritize technology adoption in public and private sectors. According to the Dubai Future Foundation the emirate aims to become a global hub for blockchain and artificial intelligence driving demand for specialized enterprise applications. In Africa South Africa Nigeria and Kenya are emerging as tech hubs with growing adoption of mobile based enterprise solutions for agriculture and finance. The expansion of mobile money platforms has created a need for integrated software that manages transactions and customer data securely. While infrastructure gaps remain in some areas the increasing investment in fiber optic networks and data centers is laying the foundation for broader enterprise software adoption across the continent in the near future.

COMPETITIVE LANDSCAPE

The competition in the enterprise software market is intense and characterized by rapid technological innovation and aggressive consolidation activities. Major incumbents compete not only on feature sets but also on ecosystem integration and customer support quality. The rise of cloud native startups has disrupted traditional licensing models forcing established players to adapt quickly. Differentiation increasingly depends on artificial intelligence capabilities and industry specific customization rather than basic functionality. Price competition remains fierce in the small and medium business segment while large enterprises prioritize security and scalability. Vendor lock in strategies are being countered by open standards and interoperability demands from clients. Global reach and local compliance expertise are critical success factors in this fragmented landscape. Companies must balance innovation speed with stability to retain trust in mission critical applications. The battle for talent further intensifies rivalry as skilled developers and data scientists become scarce resources. Ultimately success depends on creating value through seamless integration and actionable insights rather than just selling software licenses.

KEY MARKET PLAYERS

The major players in the global enterprise software market include

- Microsoft Corporation

- Infor Inc.

- Kronos Incorporated

- IBM Corporation

- SAP AG

- Oracle Corporation

TOP PLAYERS IN THE MARKET

- Microsoft Corporation stands as a pivotal force in the enterprise software landscape offering a comprehensive suite of productivity and cloud computing tools. The company leverages its Azure cloud platform to deliver scalable infrastructure and artificial intelligence capabilities to businesses worldwide. Microsoft recently enhanced its Teams application with advanced collaboration features and integrated Copilot artificial intelligence to boost employee productivity. Its focus on hybrid work solutions ensures seamless connectivity for distributed teams while maintaining robust security standards. The company continuously updates its Dynamics 365 suite to provide industry specific customer relationship and enterprise resource planning modules. By integrating LinkedIn data into its sales tools Microsoft offers unique insights into buyer behavior. Its commitment to open source compatibility and cross platform functionality strengthens its appeal among diverse organizational IT environments. Strategic partnerships with other technology leaders further expand its ecosystem enabling interoperability with third party applications. This holistic approach allows Microsoft to maintain a dominant presence in both small business and large enterprise segments globally.

- Oracle Corporation remains a critical provider of database management and enterprise resource planning solutions known for its robust performance and reliability. The company has aggressively shifted its focus toward cloud infrastructure and autonomous database technologies that reduce manual management tasks for clients. Oracle recently expanded its Cloud Infrastructure offerings with dedicated regions for sensitive workloads catering to government and regulated industries. Its Fusion Cloud Applications suite integrates finance human capital and supply chain management into a unified platform. The acquisition of Cerner has positioned Oracle strongly in the healthcare sector enabling better patient data management and operational efficiency. Oracle emphasizes high performance computing and real time analytics to help businesses make faster decisions. Its multi cloud strategy allows customers to run Oracle databases on competing cloud platforms enhancing flexibility. Continuous innovation in Java and middleware technologies ensures that developers have powerful tools for building custom enterprise applications. This blend of legacy strength and cloud innovation keeps Oracle relevant in a rapidly evolving market.

- SAP SE is a global leader in enterprise application software specializing in enterprise resource planning and supply chain management solutions. The company helps businesses of all sizes run at their best by connecting people information and business processes seamlessly. SAP recently accelerated the adoption of its RISE with SAP offering which simplifies the transition to intelligent enterprise cloud solutions. Its Business Technology Platform provides a foundation for integrating data analytics artificial intelligence and application development. SAP emphasizes sustainability by embedding carbon footprint tracking into its core software modules helping clients meet environmental goals. The company serves a vast array of industries including manufacturing retail and utilities with tailored solutions. Its partnership ecosystem includes thousands of consulting and technology partners who extend the value of SAP implementations. Continuous investment in machine learning enables predictive maintenance and demand forecasting capabilities within its applications. SAP’s focus on user experience improvements through Fiori design ensures that complex enterprise tasks are intuitive and efficient. This customer centric innovation strategy reinforces its position as a trusted partner for digital transformation worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the enterprise software market primarily employ mergers and acquisitions to rapidly expand their product portfolios and enter new geographic markets. Companies frequently invest heavily in research and development to integrate artificial intelligence and machine learning capabilities into their existing suites. Strategic partnerships with cloud infrastructure providers enable seamless deployment and scalability for clients. Vendors also focus on enhancing user experience through intuitive interfaces and low code development tools to broaden accessibility. Subscription based pricing models are widely adopted to ensure recurring revenue streams and customer loyalty. Continuous training and certification programs for partners and customers help drive adoption and reduce churn rates. Emphasis on industry specific solutions allows vendors to address niche requirements and differentiate from generic competitors. Robust cybersecurity measures are implemented to build trust and comply with global data privacy regulations. These strategies collectively aim to create sticky ecosystems that lock in customers while delivering continuous value through innovation and service excellence.

MARKET SEGMENTATION

This global enterprise software market research report has been segmented and sub-segmented based on type, deployment, application, and region.

By Type

-

Application Software

-

Business Intelligence (BI)

-

Supply Chain Management (SCM)

-

Customer Relationship Management (CRM)

-

Enterprise Resource Planning (ERP)

-

-

System Software

-

Microsoft Windows

-

iOS

-

Linux

-

-

Software as a Service (SaaS)

-

Cloud Computing

-

By Deployment Type

-

Proprietary Software

-

Outsourcing Software

-

Application Service Providers

By Application

-

Supply Chain

-

Customer Information Management

-

Sales Accounting

-

Web Services

-

Energy Management

-

Government

By Region

-

North America

-

Asia Pacific

-

Europe

-

Latin America

-

Middle East and Africa

Frequently Asked Questions

What is the global enterprise software market?

The global enterprise software market is the worldwide sector providing software applications designed to support essential business activities for large organizations including enterprise resource planning, customer relationship management, business intelligence, and supply chain management solutions.

How does the global enterprise software market work?

In the global enterprise software market, organizations license or subscribe to software applications, deploy them on-premises or cloud-based, integrate with existing systems, and use them to automate workflows, manage resources, analyze data, and optimize business operations efficiently.

What types exist in the global enterprise software market?

The global enterprise software market includes enterprise resource planning, customer relationship management, business intelligence, supply chain management, content management, enterprise performance management, eCommerce software, AI development tools, and project management software serving diverse organizational needs.

Who uses the global enterprise software market?

The global enterprise software market serves large organizations, corporations, multinational companies, government agencies, financial institutions, healthcare providers, manufacturing companies, retail businesses, and any enterprise needing integrated software solutions for managing complex business operations.

What drives the global enterprise software market?

The global enterprise software market grows due to digital transformation initiatives, cloud adoption acceleration, automation demand, data analytics importance, operational efficiency needs, competitive pressure, and increasing reliance on technology for managing business processes globally.

Who operates in the global enterprise software market?

Major players in the global enterprise software market include SAP, Oracle, Microsoft, IBM, Salesforce, Adobe, ServiceNow, Workday, Atlassian, and numerous independent software vendors providing enterprise solutions across various business functionality categories worldwide.

Is the global enterprise software market regulated?

The global enterprise software market operates under data protection laws, cybersecurity regulations, software licensing requirements, intellectual property standards, privacy regulations, and industry-specific compliance requirements ensuring secure compliant enterprise software deployment.

What technologies are used in the global enterprise software market?

Technologies in the global enterprise software market include cloud computing, artificial intelligence, machine learning, blockchain, APIs, microservices, containerization, automation frameworks, data analytics platforms, and integration middleware enabling scalable enterprise software solutions.

What are the benefits of the global enterprise software market?

The global enterprise software market offers benefits including operational efficiency, process automation, data integration, real-time insights, resource optimization, cost reduction, improved collaboration, scalability, better decision-making, and enhanced business performance across organizations globally.

What are the challenges of the global enterprise software market?

The global enterprise software market faces challenges including implementation complexity, integration difficulties with legacy systems, high costs, security concerns, user adoption barriers, customization requirements, vendor dependency, and ongoing maintenance and update management needs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com