Europe Active Implantable Medical Devices Market Size, Share, Trends & Growth Forecast Report By Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2025 to 2033)

Europe Active Implantable Medical Devices Market Summary

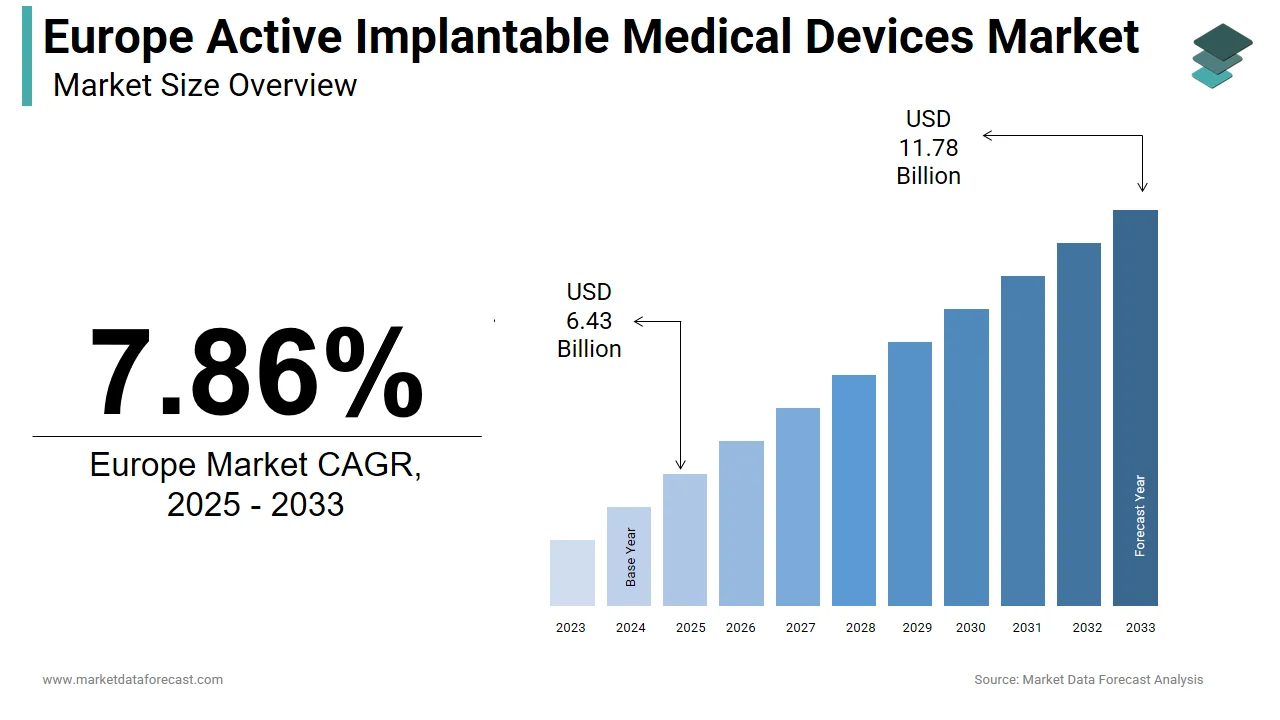

The Europe active implantable medical devices market was valued at USD 5.96 billion in 2024 and is projected to reach USD 11.78 billion by 2033, growing at a CAGR of 7.86% from 2025 to 2033. Market growth is driven by Europe’s rapidly aging population, the rising burden of cardiovascular and neurological disorders, and increasing reliance on life-sustaining implantable technologies such as pacemakers, implantable cardioverter defibrillators, neurostimulators, and cochlear implants. Continued advancements in device miniaturization, neuromodulation, and remote monitoring, along with supportive reimbursement frameworks in major European economies, are reinforcing market expansion.

Active implantable medical devices are battery-powered or externally controlled systems surgically implanted to monitor, regulate, or stimulate physiological functions. In Europe, these devices are deeply integrated into chronic disease management pathways, particularly for cardiac rhythm disorders, Parkinson’s disease, epilepsy, chronic pain, and hearing loss, positioning them as critical enablers of long-term patient outcomes and healthcare system resilience.

Key Market Trends & Insights

- Germany dominated the European market in 2024, supported by high implantation volumes, strong reimbursement coverage, and advanced cardiac care infrastructure.

- Cardiac pacemakers remain the largest product segment, reflecting sustained demand for rhythm management in aging populations.

- Neurostimulators are the fastest-growing segment, driven by rising neurological disease prevalence and adoption of neuromodulation therapies.

- Minimally invasive implantation techniques are improving patient eligibility and reducing hospital stays across Europe.

- AI-enabled and connected implants are gaining traction, enhancing therapeutic precision and post-implant monitoring.

- Western Europe leads in adoption, while Central and Eastern Europe present long-term growth opportunities as access improves.

Market Size & Forecast

- 2024 Market Size: USD 5.96 Billion

- 2025 Market Size: USD 6.43 Billion

- 2033 Projected Market Size: USD 11.78 Billion

- CAGR (2025–2033): 7.86%

- Largest Country Market (2024): Germany

- Fastest-Growing Segment: Neurostimulators

Key Report Takeaways

- By product, implantable cardiac pacemakers accounted for 37.5% market share in 2024, supported by universal reimbursement and high procedural volumes.

- Neurostimulators are projected to grow at a 14.04% CAGR, driven by increasing adoption of deep brain, spinal cord, and vagus nerve stimulation therapies.

- By clinical application, cardiovascular disorders remain the largest demand driver, while neurological indications represent the fastest-expanding use case.

- By country, Germany held 21.9% of the European market in 2024, followed by the United Kingdom and France.

- Regulatory stringency under EU MDR and high implantation costs remain key restraints, while AI integration and minimally invasive surgery present major growth opportunities.

Europe Active Implantable Medical Devices Market Size

The size of the Europe active implantable medical devices market was valued at USD 5.96 billion in 2024. This market is expected to grow at a CAGR of 7.86% from 2025 to 2033 and be worth USD 11.78 billion by 2033 from USD 6.43 billion in 2025.

Active implantable medical devices refer to battery-powered or externally controlled medical systems surgically embedded within the human body to monitor, regulate, or stimulate physiological functions. These include cardiac pacemakers, implantable cardioverter defibrillators, neurostimulators, and cochlear implants, among others. In Europe, the clinical urgency to address chronic and age-related disorders has intensified reliance on such life-sustaining technologies. According to Eurostat, more than one‑fifth of the European Union population was aged 65 years or older in 2023, which reflects a demographic reality that amplifies dependency on implantable therapeutic solutions. As per the European Heart Rhythm Association (EHRA), over a million people in Europe live with implanted cardiac rhythm management devices, which underlines the deep clinical integration of such technologies. Furthermore, the European Medicines Agency (EMA) has streamlined regulatory classification for active implants under the Medical Devices Regulation (2017) to enhance safety and traceability while supporting continued innovation. The convergence of an aging populace, rising prevalence of neurological and cardiovascular conditions, and evolving healthcare infrastructure continues to shape a distinct clinical and technological ecosystem for active implantable devices across European nations. These devices are increasingly positioned not only as therapeutic interventions but as strategic enablers of long‑term patient outcomes and healthcare system resilience.

MARKET DRIVERS

Rising Burden of Cardiovascular Diseases Elevates Device Adoption

The growing patient population suffering from cardiovascular diseases across Europe is primarily driving the active implantable devices market expansion in Europe. Cardiovascular diseases remain the leading cause of mortality across the European Union, accounting for nearly 35% of all deaths, according to the European Cardiovascular Disease Statistics. As per Eurostat, diseases of the circulatory system account for about one-third of all deaths in the EU. This enduring health crisis drives consistent demand for active implantable solutions such as pacemakers and implantable cardioverter defibrillators, which offer life-prolonging rhythm management for arrhythmia patients. In Germany alone, over three hundred thousand pacemaker implantations have been performed cumulatively over the past decade, as documented by the German Cardiac Society, reflecting sustained clinical reliance on such interventions. According to national registry summaries, annual pacemaker implantations in Germany typically exceed thirty thousand per year. Moreover, the European Society of Cardiology estimates that sudden cardiac death affects between 300,000 and 400,00 individuals annually in Europe, which is creating a compelling imperative for preventive implantable technologies. As per the ESC Atlas, sudden cardiac death represents a substantial share of cardiac mortality across Europe. National health systems increasingly recognize the long-term cost-effectiveness of these devices, with countries like France and Italy integrating them into standardized cardiac care pathways. The growing incidence of atrial fibrillation, which impacts over eleven million Europeans as per Eurostat, further compounds device dependency. According to European epidemiology reviews, atrial fibrillation prevalence continues to rise with aging demographics and comorbidities. Consequently, the persistent cardiovascular mortality burden serves not merely as a clinical statistic but as a foundational driver reinforcing both public health policy and clinical practice in favour of active implantable adoption across the continent.

Escalating Neurological Disorders Spur Demand for Neuromodulation Implants

Neurological conditions, including Parkinson’s disease, epilepsy, and chronic pain, have seen a marked rise across Europe, intensifying the need for advanced neuromodulation therapies, which is further boosting the European active implantable devices market growth. As per the European Brain Council, around one in three Europeans is affected by a brain disorder annually, with associated healthcare costs exceeding hundreds of billions of euros. Deep brain stimulation devices and spinal cord stimulators have emerged as pivotal interventions, particularly for treatment-resistant cases. The number of Parkinson’s disease patients in Europe is projected to exceed 1.2 million by 2030, according to the European Parkinson’s Disease Association, which illustrates the expanding addressable patient pool. As per Parkinson’s Europe projections, case numbers are expected to climb with population aging. In the United Kingdom, over 15,000 individuals currently live with deep-brain stimulators, as reported by the National Health Service, demonstrating established clinical protocols. According to NHS sources, tens of thousands of patients have received DBS in the UK to date. Similarly, the European Registry of Epilepsy Surgery documents a 30% increase in vagus nerve stimulator implants over the last 5 years, driven by pharmacoresistant epilepsy affecting nearly one million Europeans. As per European epilepsy registries, device uptake has grown in line with treatment needs for drug‑resistant cases. National reimbursement frameworks in countries like Sweden and the Netherlands now routinely cover neuromodulation procedures for qualifying patients, thereby removing financial barriers to access. This confluence of epidemiological pressure, clinical validation, and supportive healthcare policies establishes neurological disorders as a powerful catalyst for active implantable medical device utilization throughout Europe.

MARKET RESTRAINTS

Stringent Regulatory Pathways Delay Market Entry and Innovation Cycles

The European Union’s Medical Devices Regulation, which became fully applicable in 2021, imposes rigorous conformity assessment procedures for active implantable devices, significantly extending the time to market, which is a significant restraint to the growth of the European market. According to the European Commission, a substantial share of notified body capacity is currently allocated to high-risk device evaluations, including active implants, which is contributing to review backlogs. As per a study published by the European Society for Medical Innovation, the average approval timeline for novel active implants has increased by 8 to 12 months under the new framework compared to the prior Medical Devices Directive. As per industry transition analyses, MDR timelines for high‑risk devices have lengthened by close to a year versus legacy pathways. This delay particularly affects small and medium-sized enterprises, which represent nearly 40% of Europe’s medtech innovators, as noted by MedTech Europe, and often lack resources to navigate prolonged compliance processes. According to MedTech Europe, SMEs constitute the majority of the region’s medtech company base and face disproportionate regulatory burdens. Moreover, the requirement for comprehensive post-market surveillance, including the Unique Device Identification system, adds operational complexity and financial burden. In 2022, the European Medicines Agency reported that 22% of new implantable device applications required multiple resubmissions before achieving certification, further slowing clinical availability. As per competent authority summaries, resubmission rates for complex implant dossiers are materially higher under MDR. These regulatory hurdles, while enhancing patient safety, inadvertently suppress timely access to next-generation therapies, thereby constraining market dynamism and potentially driving innovation toward less regulated geographies.

High Costs of Implantation and Long-Term Management Limit Accessibility

Despite universal healthcare coverage in most European nations, the total cost burden associated with active implantable medical devices remains a barrier to equitable access and hampers the growth of the European active implantable devices market. As per OECD health accounts, typical procedure costs for cardiac implantable devices in Europe span from the mid‑teens to mid‑thirty thousand euros, depending on system and setting. In lower-income member states such as Romania and Bulgaria, national health budgets allocate less than 2 euros per capita annually for high-end implantables, according to the European Observatory on Health Systems and Policies, restricting patient eligibility. As per health system spending profiles, constrained per‑capita budgets limit access to high‑technology interventions. Even in wealthier nations, variations persist. The German Institute for Quality and Efficiency in Health Care found that only 68% of eligible heart failure patients receive cardiac resynchronization therapy due to localized funding constraints. According to IQWiG‑linked evaluations, uptake of CRT among eligible cohorts remains below full coverage due to regional resource limits. Additionally, long-term maintenance, such as battery replacements for neurostimulators occurring every 5 to 7 years, incurs recurrent expenses that some national systems only partially reimburse. As per payer schedules, replacement cycles for implantable neurostimulators generate ongoing costs that are variably reimbursed. These financial limitations disproportionately affect rural and socioeconomically disadvantaged populations, thereby creating a treatment gap that undermines the potential public health impact of these life-enhancing technologies across the European region.

MARKET OPPORTUNITIES

Integration Of Artificial Intelligence in Implant Functionality Opens New Therapeutic Frontiers

The convergence of artificial intelligence with active implantable devices is redefining therapeutic precision and patient outcomes across Europe, which is a promising opportunity for the European active implantable medical devices market. AI-enabled pacemakers, for instance, now adapt pacing algorithms in real time based on individual physiological patterns, reducing arrhythmia episodes by up to 40% as demonstrated in a 2024 multicenter trial coordinated by the European Heart Rhythm Association. As per EHRA multicenter evaluations, adaptive pacing algorithms have reported substantial reductions in arrhythmic events versus conventional programming. In the neuromodulation space, adaptive deep brain stimulators using machine learning to detect and respond to Parkinsonian tremor signatures have shown a 35% improvement in motor function over conventional systems, according to clinical data from the Charité University Hospital in Berlin. As per Charité clinical reports, closed‑loop DBS systems have demonstrated notable motor improvements in controlled cohorts. The European Innovation Council has allocated over two hundred million euros since 2022 to support AI-driven implantable medical device startups, reflecting institutional recognition of this frontier. According to EIC funding disclosures, cumulative deep‑tech allocations since 2022 exceed two hundred million euros for AI‑linked MedTech initiatives. Regulatory bodies, including the European Medicines Agency, have initiated pilot programs to fast-track AI-integrated implants under the Innovation Task Force framework, thereby accelerating clinical translation. As per EMA pilot notices, innovation support pathways for AI‑enabled devices are under active evaluation. Moreover, public acceptance is rising. A Eurobarometer survey from 2023 revealed that 2% of Europeans aged fifty and above expressed willingness to receive AI-enhanced implants if proven safe. According to Eurobarometer polling, a majority of older respondents indicate conditional acceptance of AI‑augmented medical technologies. This technological inflection point not only enhances therapeutic efficacy but also enables predictive health monitoring, transforming active implants from reactive interventions to proactive health management platforms across European healthcare ecosystems.

Expansion of Minimally Invasive Surgical Techniques Enhances Device Adoption Rates

Advancements in minimally invasive surgical approaches have significantly lowered procedural risks and recovery times associated with active implantable device insertion, thereby broadening patient eligibility, which is another prominent opportunity for the regional market. Transvenous leadless pacemaker implantation, for example, now requires only local anaesthesia and a single-day hospital stay compared to traditional open chest procedures. As per the European Association for Cardio Thoracic Surgery, the share of new pacemaker implants using minimally invasive techniques in Western Europe has risen markedly in recent years. Similarly, the adoption of percutaneous cochlear implantation has reduced surgical complications by 30% according to data from the European Academy of Otology and Neurotology, enabling access for elderly and comorbid patients previously deemed high risk. As per the EAONO datasets, complication rates are materially lower with percutaneous approaches versus traditional methods. National surgical training programs in countries like the Netherlands and Denmark have integrated these techniques into standard curricula, ensuring consistent skill dissemination. According to the European Society of Minimally Invasive Neurological Therapy, a 50% increase in outpatient neurostimulator placements since 2021 has further eased strain on hospital resources. As per ESMINT activity reports, outpatient neuromodulator procedures have expanded substantially post‑2021. These procedural innovations not only improve clinical outcomes but also align with Europe’s broader healthcare efficiency objectives by shortening hospital stays and minimizing postoperative care needs, thus creating a favorable procedural environment for active implantable device utilization.

MARKET CHALLENGES

Device Cybersecurity Vulnerabilities Pose Critical Patient Safety Risks

The increasing connectivity of active implantable medical devices to external monitoring systems and hospital networks introduces significant cybersecurity threats that directly impact patient safety, which is majorly challenging the growth of the European active implantable medical devices market. In 2023, the European Union Agency for Cybersecurity identified over one hundred twenty distinct vulnerabilities in commercially available implantable cardiac devices, with 30% classified as high or critical severity. As per ENISA threat landscape assessments, vulnerability counts in connected medical devices include numerous high‑severity findings. A real-world incident documented by the French National Agency for the Safety of Medicines involved unauthorized access to a remote pacemaker monitoring system, potentially enabling life-threatening manipulation of pacing parameters. According to national safety bulletins, unauthorized system access incidents have prompted remediation actions for remote monitoring platforms. As per a study published in the European Journal of Clinical Investigation, 37% of European hospitals lacked dedicated cybersecurity protocols for connected implants in 2022, leaving devices exposed to ransomware and data interception. According to EU clinical audits, a significant share of hospitals reports gaps in device cybersecurity governance. The complexity escalates with the proliferation of home-based remote monitoring, where patients use consumer-grade Wi‑Fi networks that rarely meet clinical security standards. Despite the Medical Devices Regulation requiring manufacturers to implement risk-based cybersecurity measures, enforcement remains inconsistent across member states. These vulnerabilities not only threaten individual patients but also erode clinician confidence and public trust, thereby impeding broader adoption of next-generation connected implants across the European healthcare landscape.

Limited Long-Term Clinical Data Undermines Reimbursement and Adoption Consensus

The absence of robust long-term clinical evidence for newer active implantable devices hampers reimbursement approvals and clinician endorsement across Europe, which is further hampering the regional market expansion. Health technology assessment bodies such as the National Institute for Health and Care Excellence in the United Kingdom and the German Institute for Quality and Efficiency in Health Care routinely require 10-year outcome data for full coverage decisions, yet many next-generation implants have only five-year or shorter follow-up records. As per a 2024 review by the European Network for Health Technology Assessment, fewer than 20% of novel implantable neuromodulation systems submitted since 2020 have completed long-term randomized controlled trials. According to the EUnetHTA synthesis, long‑duration RCT evidence remains limited for recent neuromodulation entrants. This evidence gap leads to fragmented reimbursement, with countries like Spain and Greece often restricting coverage to exceptional compassionate use cases. Consequently, manufacturers face delayed return on investment, which the European Med Tech Association estimates reduces R&D reinvestment by up to 25% for emerging implant categories. As per European MedTech surveys, reduced reimbursement certainty correlates with lower reinvestment rates. Clinicians also express hesitation, with a European Heart Rhythm Association survey revealing that 58% of electrophysiologists prefer established device platforms due to uncertain durability profiles of newer alternatives. According to EHRA polling, most specialists favour proven systems when long‑term performance data are incomplete. Until harmonized post-market surveillance and real-world evidence generation mechanisms mature, this data deficit will continue to stifle equitable access and market consolidation for innovative active implantable solutions in Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, LivaNova PLC, Cochlear Limited, MED-EL, Sonova Holding AG, William Demant Holding A/S, and Nurotron Biotechnology Co. Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The implantable cardiac pacemakers segment commanded 37.5% of the Europe active implantable medical devices market in 2024. This dominance is primarily attributed to the high and sustained prevalence of bradycardia and conduction disorders across aging European populations. As per Eurostat, over 22% of the European Union’s population was aged 65 or older in 2024, a demographic cohort at significantly elevated risk for rhythm disturbances requiring pacing support. Germany recorded around 882 pacemaker implantations per million inhabitants in 2021, which is equivalent to more than 100,000 procedures annually, according to the ESC Atlas of Cardiology. Furthermore, national health systems across Western Europe classify pacemakers as essential medical interventions with near‑universal coverage under statutory insurance schemes. Technological refinements such as leadless designs have also expanded eligibility, with over 45% of new pacemaker implants in Sweden and the Netherlands now utilizing minimally invasive platforms, according to the European Heart Rhythm Association. The combination of demographic pressure, clinical necessity, widespread reimbursement, and continuous device innovation solidifies pacemakers as the cornerstone segment of Europe’s active implantable ecosystem.

The neurostimulators segment emerged as the fastest-growing product segment in the Europe active implantable medical devices market and is predicted to grow at a CAGR of 14.04% over the forecast period, owing to the rising burden of chronic neurological conditions and the increasing adoption of device‑based alternatives to pharmacological management. Parkinson’s disease affects over 1 million individuals in Europe, and Parkinson’s Europe forecasts this number will surpass 1.4 million by 2030, creating a substantial patient pool for deep brain stimulation. Chronic pain affects nearly 20% of adults across Europe, according to a 2025 systematic review published in PAIN, with spinal cord stimulators gaining traction as opioid‑sparing interventions. National reimbursement reforms have further catalysed growth, with France and Italy approving full coverage for select neurostimulation therapies in 2023 following positive health technology assessments. The European Registry of Neuromodulation reports a 52% increase in implantable pulse generator placements since 2021, largely due to expanded clinical guidelines and multidisciplinary pain centers. Coupled with AI‑enabled adaptive stimulation platforms now entering clinical use, neurostimulators represent the most dynamic growth frontier in Europe’s active implantable landscape.

COUNTRY-LEVEL ANALYSIS

Germany Active Implantable Medical Devices Market Analysis

Germany dominated the active implantable medical devices market in Europe in 2024 with 21.9% of the regional market share. The dominance of Germany in the European market is driven by its advanced cardiac care infrastructure, high procedural volumes, and early adoption of next-generation implants. According to the German Cardiac Society, more than 130,000 cardiac rhythm management devices (pacemakers and defibrillators) are implanted annually in Germany. The statutory health insurance system covers nearly 99% of the population and provides comprehensive reimbursement for all clinically indicated active implants, ensuring equitable access. As per the German Medical Association, more than 800 hospitals are authorized to perform complex device procedures. Continuous investment in electrophysiology training and neuromodulation expertise further reinforces Germany’s position as both a clinical and innovation hub. Recent policy initiatives, such as the Digital Health Applications Ordinance, have also enabled remote monitoring integration, accelerating post-market adoption of connected implants.

United Kingdom Active Implantable Medical Devices Market Analysis

The United Kingdom had the second-largest share of the European active implantable medical devices market in 2024. Despite fiscal constraints within the National Health Service, the UK maintains a strong uptake of high-value implants, particularly in cardiac rhythm management and neurostimulation. According to NHS Digital, more than 18,000 deep-brain stimulators are currently implanted across England and Wales. The UK also leads in post-market surveillance with the National Implant Registry tracking over 900,000 active devices, providing real-world evidence that informs both clinical guidelines and regulatory decisions. Recent approvals for leadless pacemakers and subcutaneous defibrillators have been rapidly incorporated into NICE technology appraisals, shortening adoption cycles. As noted in a 2023 House of Commons Health Committee report, rural areas experience up to 30% longer wait times for implantation due to workforce shortages.

France Active Implantable Medical Devices Market Analysis

France is a promising market for active implantable medical devices in Europe. The centralized healthcare system of France that prioritizes standardized access to life-sustaining technologies is contributing to the growth of the French market. According to the French Society of Cardiology, more than 90,000 cardiac implantable procedures are performed annually, including pacemakers, defibrillators, and loop recorders. France’s national reimbursement agency fully covers all CE-marked active implants provided they align with published clinical indications, ensuring minimal out-of-pocket costs for patients. In neurostimulation, France pioneered nationwide coverage for sacral nerve stimulation in urinary dysfunction and has since extended reimbursement to chronic pain and epilepsy applications following positive outcomes in the French Neuromodulation Registry. As per the Ministry of Health’s “Ma Santé 2022” strategy, more than 60% of implant centers now use certified telemonitoring platforms. These systemic enablers position France as a high-volume, stable growth market within Europe.

Italy Active Implantable Medical Devices Market Analysis

Italy is expected to exhibit a prominent CAGR in the European active implantable medical devices market over the forecast period. According to ISTAT, nearly 24% of Italians are aged 65 or older. As documented by the Italian Association of Arrhythmology and Cardiac Pacing, more than 75,000 pacemaker procedures are conducted annually across the country. Regional healthcare autonomy, however, leads to disparities in device access, with northern regions such as Lombardy achieving implant rates 30% higher than southern provinces due to better-resourced cardiology departments. Despite these imbalances, Italy has made significant strides in adopting newer technologies, with the Italian Heart Rhythm Society reporting that leadless pacemakers now account for more than 20% of new implants in major tertiary centers. National efforts to standardize implantation protocols through the Ministry of Health’s chronic care program are gradually reducing geographic inequities and supporting market consolidation.

Netherlands Active Implantable Medical Devices Market Analysis

The Netherlands is projected to grow at a healthy CAGR in the Europe active implantable medical devices market over the forecast period due to its highly efficient and integrated healthcare model. Despite a relatively small population, the country achieves among the highest per capita implantation rates in Europe. According to the Netherlands Heart Registry, more than 12,000 active devices are implanted annually. Universal health insurance combined with stringent outcome-based procurement ensures rapid uptake of clinically superior technologies, including subcutaneous defibrillators and adaptive neurostimulators. As noted by the Dutch Society for Cardiology, more than 70% of pacemaker procedures are performed in ambulatory surgical centers. Moreover, the Netherlands actively participates in European clinical trials, with the European Clinical Research Infrastructure Network confirming Dutch centers contributed to 15% of patient enrollment in CE-marked neurostimulation studies between 2021 and 2024. This blend of operational efficiency, clinical excellence, and research engagement solidifies the Netherlands as a high-performance niche market within the European landscape.

COMPETITIVE LANDSCAPE

The Europe active implantable medical devices market features intense competition among established multinational corporations with deep clinical and regulatory expertise. The landscape is characterized by continuous innovation in device functionality, battery life, and digital integration rather than price-based rivalry. Leading firms differentiate through robust clinical evidence, proprietary algorithms, and seamless health system interoperability. Regulatory complexity under the Medical Devices Regulation has raised barriers to entry, limiting disruption from smaller players and reinforcing incumbency advantages. Nevertheless, niche innovators in neuromodulation and bioelectronic medicine are gaining traction through strategic collaborations with academic hospitals. National differences in reimbursement approval timelines and physician training protocols create fragmented adoption patterns requiring localized commercial strategies. Competitive positioning increasingly hinges on post-implant services, including remote monitoring, cybersecurity assurance, and long-term patient management platforms. As a result, companies are shifting from product-centric to outcome-centric value propositions to align with Europe’s emphasis on health system efficiency and patient safety.

KEY MARKET PLAYERS

The leading companies operating in the Europe active implantable medical devices market include:

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- LivaNova PLC

- Cochlear Limited

- MED-EL

- Sonova Holding AG

- William Demant Holding A/S

- Nurotron Biotechnology Co. Ltd.

TOP PLAYERS IN THE MARKET

- Medtronic plc maintains a leading position in the Europe active implantable medical devices market through its comprehensive portfolio spanning cardiac rhythm management, neurostimulation, and implantable monitoring systems. The company has consistently advanced device miniaturization and remote monitoring capabilities tailored to European regulatory and clinical standards. In early 2024, Medtronic received CE Mark approval for its next-generation Micra AV2 leadless pacemaker, enabling physiological pacing in a broader patient group. The firm also expanded its digital health collaboration with European hospital networks to integrate implant data into national electronic health records, enhancing post-procedural care pathways across Germany, France, and the Netherlands.

- Boston Scientific Corporation plays a pivotal role in Europe’s implantable device landscape with a strong emphasis on innovative cardiac and neuromodulation solutions. The company’s Rhythmia cardiac mapping system and Vercise Genus deep brain stimulator are widely adopted in tertiary centers across Western Europe. In 2023, Boston Scientific launched its first European real-world evidence program for implantable loop recorders in partnership with academic institutions in Sweden and Italy to validate long-term outcomes. The firm also enhanced its direct training initiatives for implanting physicians through simulation-based centers in Munich and Paris, reinforcing clinical adoption and procedural precision.

- Abbott Laboratories contributes significantly to the European active implantable market through its focus on miniaturized sensing and pacing technologies. Its Aveir VR leadless pacemaker received CE Mark in late 2023, marking a strategic expansion beyond its established Confirm Rx implantable cardiac monitor. Abbott has deepened its digital integration by linking its implantable devices to the LibreView platform, enabling cardiologists and primary care teams to access synchronized cardiac and metabolic data. The company also initiated a pan-European post-market registry in early 2024, tracking over ten thousand patients to support health technology assessments and reimbursement dossiers in Southern and Eastern European countries.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe active implantable medical devices market prioritize regulatory compliance through early alignment with the Medical Devices Regulation to accelerate CE Mark approvals. They invest heavily in real-world evidence generation via national registries and post-market surveillance to support reimbursement applications. Strategic partnerships with academic medical centers facilitate clinical validation and physician training. Companies are integrating digital health platforms to enable remote monitoring and data interoperability with European electronic health systems. Additionally, they are expanding indications for existing platforms through supplementary clinical trials to access broader patient populations. Product miniaturization and battery longevity enhancements remain central to engineering roadmaps. Finally, firms are tailoring market access strategies by country to navigate fragmented reimbursement landscapes across Western and Central Europe.

MARKET SEGMENTATION

This Europe active implantable medical devices market research report is segmented and sub-segmented into the following categories.

By Product

- Implantable Cardioverter Defibrillators

- Transvenous Implantable Cardioverter Defibrillators

- Biventricular Implantable Cardioverter Defibrillators (ICDs)/Cardiac Resynchronization Therapy Defibrillators (CRT-Ds)

- Dual-Chamber Implantable Cardioverter Defibrillators

- Single-Chamber Implantable Cardioverter Defibrillators

- Subcutaneous Implantable Cardioverter Defibrillator

- Transvenous Implantable Cardioverter Defibrillators

- Implantable Cardiac Pacemakers

- Ventricular Assist Devices

- Implantable Heart Monitors/Insertable Loop Recorders

- Neurostimulators

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Sacral Nerve Stimulators

- Vagus Nerve Stimulators

- Gastric Electrical Stimulators

- Implantable Hearing Devices

- Active Hearing Implants

- Passive Hearing Implants

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe active implantable medical devices market?

Chronic heart diseases and neurological disorders propel the Europe active implantable medical devices market. Tech advances like leadless designs boost adoption.

2. Who are key players in the Europe active implantable medical devices market?

Leaders in the Europe active implantable medical devices market include Medtronic, Abbott, Boston Scientific, and BIOTRONIK. They dominate pacemakers and ICDs.

3. What is the CAGR of the Europe active implantable medical devices market?

The Europe active implantable medical devices market forecasts 7.0-7.86% CAGR through 2033, driven by cardiovascular applications.

4. Which countries dominate the Europe active implantable medical devices market?

Germany leads the Europe active implantable medical devices market, followed by France and UK via advanced healthcare systems.

5. What are ICDs in the Europe active implantable medical devices market?

Implantable cardioverter defibrillators grow at 7.8% in the Europe active implantable medical devices market for arrhythmia prevention.

6. How does aging impact the Europe active implantable medical devices market?

21% elderly population drives the Europe active implantable medical devices market through chronic condition prevalence.

7. What trends shape the Europe active implantable medical devices market?

MRI-compatible and subcutaneous devices trend in the Europe active implantable medical devices market for safety.

8. Are pacemakers dominant in the Europe active implantable medical devices market?

Pacemakers hold major share in the Europe active implantable medical devices market for bradycardia treatment.

9. How competitive is the Europe active implantable medical devices market?

Oligopolistic competition defines the Europe active implantable medical devices market with regulatory barriers.

10. What role do hospitals play in the Europe active implantable medical devices market?

Hospitals grow at 6.9% in the Europe active implantable medical devices market via implantation infrastructure.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com