Global Active Implantable Medical Devices Market Size, Share, Trends & Growth Forecast Report By Product and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Active Implantable Medical Devices Market Report Summary

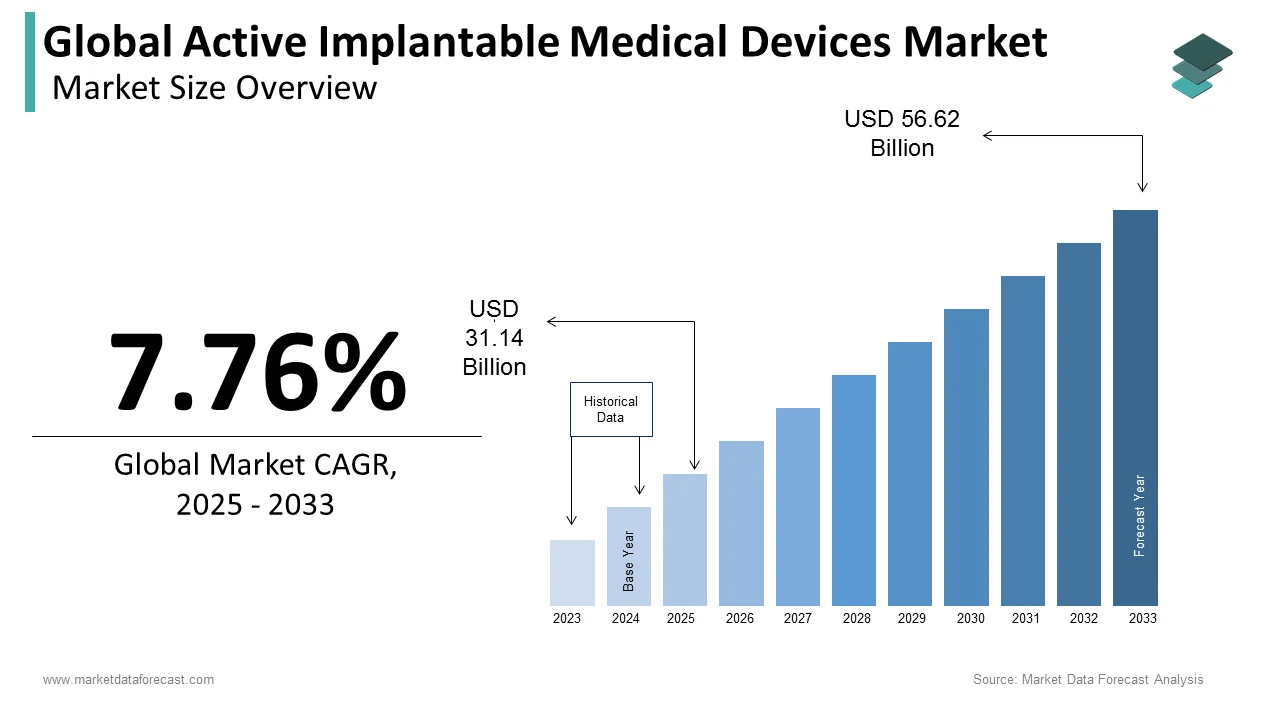

The global active implantable medical devices market was valued at USD 31.14 billion in 2025, is estimated to reach USD 33.56 billion in 2026, and is projected to reach USD 61.02 billion by 2034, growing at a CAGR of 7.76% from 2026 to 2034. Market growth is driven by the rising prevalence of chronic diseases, increasing demand for advanced cardiac and neurological treatments, and continuous technological advancements in implantable devices. These devices, including pacemakers, defibrillators, and neurostimulators, play a crucial role in improving patient outcomes and quality of life. Additionally, the aging global population, growing healthcare expenditure, and increasing adoption of minimally invasive procedures are further fueling market expansion.

Key Market Trends

- Rising demand for implantable cardiac and neurological devices.

- Increasing adoption of minimally invasive surgical procedures.

- Advancements in device miniaturization and battery technology.

- Growing prevalence of cardiovascular and neurological disorders.

- Expansion of remote monitoring and smart implant technologies.

Segmental Insights

- Based on product, the implantable cardiac pacemakers segment dominated the market by capturing 38.5% share in 2025, driven by the high prevalence of cardiac disorders and widespread clinical use.

- The subcutaneous implantable cardioverter defibrillator (S-ICD) segment is projected to register the fastest CAGR of 14.2% from 2026 to 2034, supported by its minimally invasive nature and reduced risk of complications.

Regional Insights

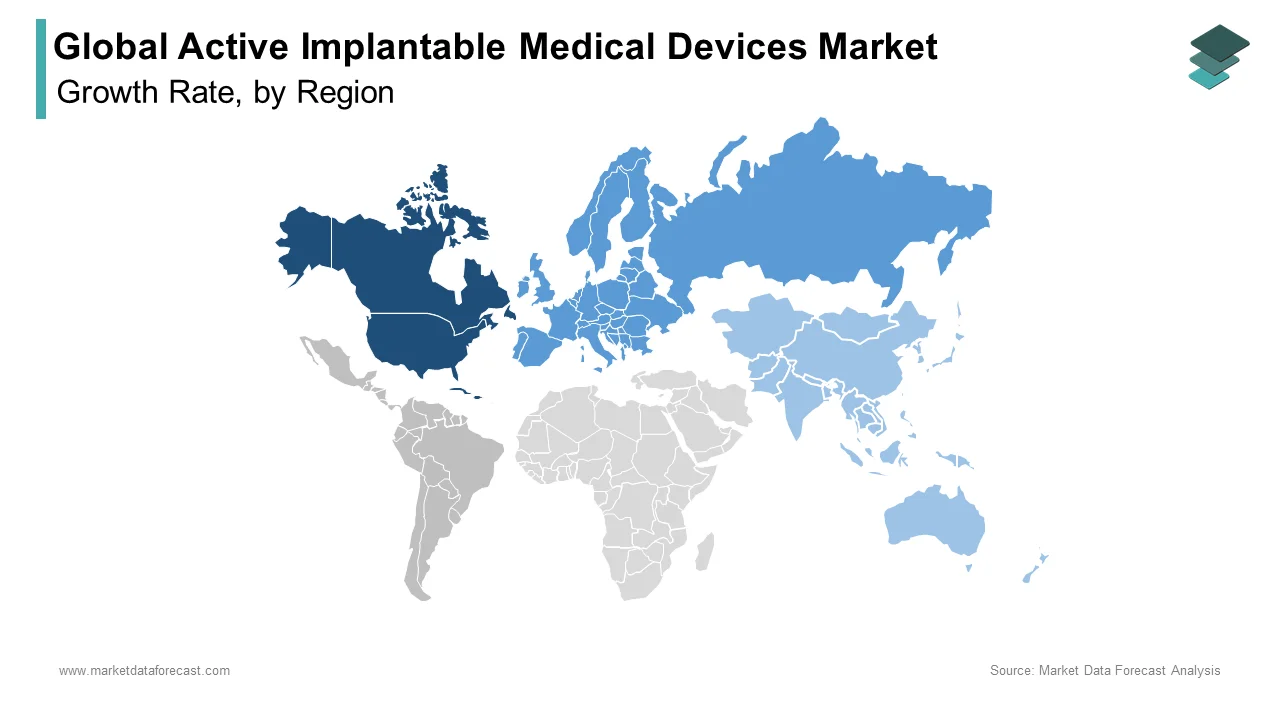

The global active implantable medical devices market is witnessing strong growth across major regions due to advancements in healthcare infrastructure and rising disease burden.

-

North America led the market in 2025 with 45.1% share, supported by advanced healthcare systems and high adoption of innovative medical technologies.

-

Europe followed with 28.6% share in 2025, driven by strong regulatory frameworks and increasing healthcare investments.

-

Asia-Pacific is emerging as the fastest-growing region due to large population bases, improving healthcare infrastructure, and rising awareness of advanced treatment options.

Competitive Landscape

The global active implantable medical devices market is highly competitive, with the presence of leading medical device manufacturers focusing on innovation, product development, and strategic partnerships. Companies are investing in R&D to develop advanced, safer, and more efficient implantable devices, along with expanding their global footprint.

Prominent companies operating in the global active implantable medical devices market include Medtronic PLC, Abbott Laboratories, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, LivaNova, Cochlear Limited, MED-EL, Sonova Holding AG, William Demant Holding A/S, and Nurotron Biotechnology Co. Ltd.

Global Active Implantable Medical Devices Market Size

The size of the global active implantable medical devices market was worth USD 31.14 billion in 2025. The global market is anticipated to grow at a CAGR of 7.76% from 2026 to 2034 and be worth USD 61.02 billion by 2034 from USD 33.56 billion in 2026.

An Active Implantable Medical Device (AIMD) is a high-risk medical device that is surgically or medically introduced into the human body and relies on an external power source (like a battery) to function. Unlike passive implants such as stents or joint replacements, these devices rely on an internal power source, typically a battery, to operate complex algorithms for cardiac rhythm management, neurostimulation, drug delivery, and hearing restoration. The definition includes pacemakers, implantable cardioverter defibrillators, cochlear implants, deep brain stimulators, and insulin pumps that actively interact with bodily systems. As per data from the World Health Organization, cardiovascular diseases remain the leading cause of death globally, accounting for a substantial number of deaths annually, which establishes a critical and enduring demand for life-sustaining active implants. According to the Centers for Disease Control and Prevention, several million adults in the United States live with heart failure, a condition frequently managed through advanced device therapy. The market operates under stringent regulatory frameworks like the European Union Medical Device Regulation and Food and Drug Administration guidelines to ensure long-term biocompatibility and electrical safety. Eurostat indicates that the proportion of individuals aged sixty-five and older in the European Union has increased recently, creating a demographic imperative for technologies that manage age-related organ degradation. This sector represents the convergence of microelectronics, biomaterials science, and clinical medicine, aiming to extend life expectancy and improve quality of life for patients with chronic debilitating conditions.

MARKET DRIVERS

Surging Global Prevalence of Chronic Cardiac and Neurological Disorders

The escalating global burden of chronic cardiac arrhythmias and neurological disorders is driving the active implantable medical devices market. These disorders require continuous electronic intervention, making the devices essential for survival and symptom management. Conditions such as bradycardia, ventricular tachycardia, Parkinson's disease, and essential tremor often become refractory to pharmacological treatments, making device implantation the standard of care. According to statistics from the Global Burden of Disease Study, the number of people living with atrial fibrillation doubled between 1990 and 2019, reaching over 59 million cases worldwide, directly correlating with increased pacemaker and defibrillator implantation rates. The National Institute of Neurological Disorders and Stroke reports that nearly one million people in the United States alone live with Parkinson's disease, a figure expected to rise significantly as the population ages, driving demand for deep brain stimulation systems. Furthermore, the increasing incidence of sudden cardiac arrest among younger populations due to lifestyle factors and undiagnosed congenital defects has expanded the addressable market for implantable cardioverter defibrillators. Data from the American Heart Association indicates that survival rates for out-of-hospital cardiac arrest remain low, prompting aggressive adoption of primary prevention devices in high-risk patients. The chronic nature of these diseases requires devices that function reliably for years, creating a recurring replacement cycle that sustains market volume. Improved diagnostic capabilities and widespread screening are accelerating the identification of eligible candidates for active implants. Consequently, demand growth remains robust across both developed and emerging healthcare systems.

Technological Advancements in Miniaturization and Battery Longevity

The rapid evolution of engineering capabilities further propels the expansion of the active implantable medical devices market. These capabilities have enabled significant miniaturization of device components and substantial extensions in battery life. Consequently, these advancements are reducing surgical risks and improving patient acceptance. Modern active implants are increasingly leadless, subcutaneous, or injectable, minimizing the invasiveness of procedures and lowering the risk of infection associated with traditional transvenous leads. As per research findings published in the Journal of the American College of Cardiology, the introduction of leadless pacemakers has significantly reduced complication rates compared to conventional systems, encouraging earlier intervention in moderate-risk patients. Advances in lithium-ion and solid-state battery technologies now allow devices to operate for 15 to 20 years on a single charge, drastically reducing the frequency of replacement surgeries and the associated healthcare costs. The Food and Drug Administration notes that newer generation neurostimulators feature rechargeable batteries that can last for many years, offering a viable solution for young patients requiring lifelong therapy. Furthermore, the integration of micro-electromechanical systems allows for the embedding of multiple sensors within tiny form factors, enabling closed-loop systems that automatically adjust therapy based on real-time physiological feedback. Data from industry patent filings shows a notable increase in innovations related to energy harvesting and wireless charging for implants over recent years. These technological breakthroughs not only enhance clinical outcomes but also alleviate patient anxiety regarding device maintenance, broadening the willingness to undergo implantation and driving market expansion.

MARKET RESTRAINTS

High Procedural Costs and Reimbursement Constraints

Prohibitive costs, complex surgical procedures, and ongoing expenses for programming and follow-up care represent the most formidable restraints hindering the growth of the active implantable medical devices market. These challenges are all exacerbated by tightening reimbursement policies. The upfront cost of a single advanced device, such as a biventricular pacemaker or a cochlear implant, can be substantial, excluding hospital fees and surgeon charges, placing a heavy financial burden on healthcare systems and uninsured patients. According to multiple studies, reimbursement rates for cardiac device implants have faced pressure in real terms over the past decade, prompting hospitals to focus more on cost-effectiveness and resource management for these advanced therapies. In developing nations, where out-of-pocket expenditure constitutes a large portion of healthcare spending, the vast majority of eligible patients cannot afford these life-saving interventions. Research indicates that in low-income countries, only a very small fraction of patients who require pacemakers actually receive them due to significant cost barriers and a lack of specialized infrastructure. Furthermore, insurance providers are increasingly implementing prior authorization hurdles and strict clinical criteria to limit coverage to only the most severe cases, delaying access for many. The economic pressure to reduce healthcare spending leads to longer wait times and restricted availability of newer, more expensive technologies. High costs will remain a significant barrier to market penetration, particularly in resource-constrained environments. This will continue until cost-reduction strategies such as localized manufacturing or value-based pricing models become widespread.

Risks of Device Malfunction, Recall, and Cybersecurity Vulnerabilities

The persistent risk of device malfunction, costly recalls, and emerging cybersecurity threats hampers the expansion of the active implantable medical devices market. These issues undermine physician and patient confidence in active implantable technologies. Despite rigorous testing, electronic components can fail prematurely due to battery depletion, lead fracture, or software glitches, potentially leading to life-threatening situations for dependent patients. As per data from the Food and Drug Administration, there were numerous high-severity recalls of cardiac rhythm management devices in recent years, affecting hundreds of thousands of patients and leading to increased scrutiny of specific brands and technologies. The increasing connectivity of modern implants via Bluetooth or Wi-Fi for remote monitoring introduces vulnerabilities to hacking and unauthorized access, raising fears of malicious manipulation of device settings. The Department of Homeland Security has issued warnings regarding the potential for cyberattacks on connected medical devices, prompting manufacturers to invest heavily in security protocols to protect patient safety. A study published in the journal Heart Rhythm found that anxiety about device reliability affects a significant portion of implanted patients, sometimes impacting their decisions regarding necessary upgrades or replacements. The legal liability associated with device failures results in protracted litigation and substantial financial penalties for manufacturers, discouraging innovation in high-risk categories. These safety and security concerns necessitate extensive post-market surveillance and conservative clinical adoption rates, acting as a brake on market growth despite the clear clinical benefits of these technologies.

MARKET OPPORTUNITIES

Integration of Internet of Medical Things and Remote Patient Monitoring

The deep integration of the Internet of Medical Things (IoMT) offers major opportunities for the growth of the active implantable medical devices market. This integration enables comprehensive remote patient monitoring, allowing clinicians to track device performance and patient physiology in real-time without office visits. This shift transforms active implants from static therapeutic tools into dynamic data nodes that transmit continuous streams of health information to cloud-based platforms for artificial intelligence analysis. According to research from the Mayo Clinic, remote monitoring of cardiac devices has been shown to reduce all-cause mortality and decrease hospitalization rates by enabling early detection of arrhythmias or heart failure decompensation. The Centers for Medicare and Medicaid Services has expanded reimbursement codes for remote physiologic monitoring, creating a sustainable revenue model for providers who adopt these connected solutions. Data from the Healthcare Information and Management Systems Society indicates that a large majority of cardiologists now prefer devices with robust remote capabilities, driving manufacturers to prioritize connectivity features in new product designs. Furthermore, the ability to aggregate large datasets from thousands of implanted devices offers unprecedented opportunities for real-world evidence generation, helping pharmaceutical companies and researchers understand disease progression and treatment efficacy. The convergence of 5G networks and edge computing will further enhance the speed and reliability of data transmission, making remote management the standard of care. Manufacturers can create sticky service-based revenue streams and improve patient outcomes simultaneously by leveraging these digital ecosystems. This approach transforms traditional operating models and provides new value opportunities.

Development of Bioelectronic Medicines for Chronic Disease Management

The emergence of bioelectronic medicines provides a potential prospect to treat chronic systemic diseases such as diabetes, hypertension, and inflammatory disorders, which is likely to boost the expansion of the active implantable medical devices market. This approach treats patients by modulating neural circuits rather than relying solely on pharmaceuticals. This paradigm shift utilizes active implantable neurostimulators to target specific nerves that control organ function, offering a potential cure or long-term remission for conditions that currently require daily medication. As per clinical trial data published in Nature Medicine, vagus nerve stimulation has demonstrated significant efficacy in reducing symptoms of rheumatoid arthritis and Crohn's disease by inhibiting inflammatory cytokine release, opening a new therapeutic frontier. The National Institutes of Health has launched major initiatives like the SPARC program to map the body's electrical signaling pathways, accelerating the development of targeted bioelectronic therapies. Data from venture capital tracking firms shows that investment in bioelectronic medicine startups increased significantly, reflecting strong confidence in the commercial viability of this approach. Unlike drugs, which often have systemic side effects, bioelectronic implants offer localized action with fewer adverse events, appealing to both patients and payers. The potential to replace lifelong drug regimens with a one-time implant procedure presents a compelling value proposition that could disrupt the pharmaceutical market. The addressable market for active implants will expand far beyond cardiology and neurology into endocrinology and immunology. This growth is driven by a deepening understanding of the electroceutical landscape.

MARKET CHALLENGES

Complex Regulatory Pathways and Prolonged Approval Timelines

The increasingly complex and rigorous regulatory landscape is a paramount challenge to the active implantable medical devices market. This landscape governs the approval of high-risk Class III devices. Consequently, this leads to prolonged time-to-market and escalated development costs. Regulatory bodies such as the Food and Drug Administration in the United States and the notified bodies under the European Union Medical Device Regulation demand exhaustive preclinical data, extensive clinical trials, and robust post-market surveillance plans before granting clearance. The implementation of stricter clinical evidence requirements in Europe has led to the withdrawal of several legacy products and slowed the launch of next-generation devices as manufacturers struggle to meet the new standards. Furthermore, the lack of harmonization between global regulatory regimes forces companies to conduct duplicate studies and maintain separate documentation sets, further inflating costs. The uncertainty surrounding regulatory decisions creates a cautious environment for investment, stifling the pace of innovation. Regulatory frameworks need to become more adaptive and streamlined while maintaining safety standards. Until then, the path to commercialization will remain a significant hurdle for the industry.

Biocompatibility Issues and Long-Term Tissue Interaction Risks

The ongoing difficulty in achieving perfect biocompatibility over the extended lifespan of active implants impedes the expansion of the active implantable medical devices market. This arises because the human body often reacts to foreign materials with fibrosis, inflammation, or immune responses that can degrade device performance. Despite advances in coating technologies and material science, the formation of scar tissue around electrodes can increase impedance and reduce the efficacy of stimulation or sensing, necessitating higher energy consumption and more frequent battery replacements. The chronic presence of metallic and polymeric components can also trigger allergic reactions or corrosion, releasing toxic ions into surrounding tissues. The challenge is compounded by the need for devices to withstand the harsh physiological environment of constant movement, pH fluctuations, and enzymatic activity without failing mechanically. Developing materials that truly integrate with biological tissue without eliciting an immune response remains a formidable scientific hurdle. Breakthroughs in bio-integrated electronics and anti-fouling coatings must be achieved. Until then, long-term tissue interaction risks will continue to limit the durability and reliability of active implantable medical devices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Medtronic PLC, Abbott Laboratories, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, LivaNova, Cochlear Limited, MED-EL, Sonova Holding AG, William Demant Holding A/S, and Nurotron Biotechnology Co. Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The Implantable Cardiac Pacemakers segment dominated the global active implantable medical devices market and accounted for a 38.5% share in 2025. This dominance of the segment is driven by the ubiquitous prevalence of bradycardia and heart block conditions across aging populations globally, combined with the established status of pacing therapy as the gold standard for managing slow heart rhythms for over six decades. The main factor sustaining the leadership of pacemakers is the escalating global incidence of bradycardia and atrioventricular conduction blocks, which are intrinsically linked to the aging process and affect millions of individuals who require permanent electrical support to maintain adequate heart rates. Furthermore, the increasing diagnosis of sick sinus syndrome, a condition where the heart's natural pacemaker malfunctions, has surged in the last decade due to improved diagnostic screening and greater awareness among primary care physicians. The chronic nature of these conditions means that once implanted, devices require replacement every 10 to 15 years, creating a consistent and predictable replacement cycle that sustains high market volumes. This demographic inevitability ensures that pacemakers remain the cornerstone of the active implantable device industry. An additional driver is the extensive maturation of pacemaker technology, coupled with robust clinical guidelines that strongly recommend pacing therapy for a wide range of indications, ensuring widespread adoption across diverse healthcare settings from tertiary centers to community hospitals. Modern pacemakers have evolved into highly sophisticated devices featuring rate-responsive sensors, automatic capture management, and remote monitoring capabilities, making them safe and effective for complex patients, including those with comorbidities. As per sources, clinical guidelines recommend permanent pacing for patients with symptomatic bradycardia, high-grade AV block, and certain types of heart failure, providing clear directives for physicians to proceed with implantation. The reliability of these devices is underscored by data showing that modern pacemaker systems have a significant survival rate at five years, fostering high confidence among clinicians. Additionally, the development of dual-chamber and biventricular pacing options has expanded the utility of pacemakers beyond simple rhythm control to include hemodynamic optimization for heart failure patients, further broadening their application. The combination of proven efficacy, clear regulatory pathways, and comprehensive insurance coverage in major markets removes barriers to access, solidifying the pacemaker segment as the dominant force in the active implantable medical devices landscape.

The Subcutaneous Implantable Cardioverter Defibrillator (S-ICD) segment is expected to exhibit a noteworthy CAGR of 14.2% from 2026 to 2034 due to the distinct clinical advantage of eliminating transvenous leads, thereby reducing long-term complications, and the expanding indication criteria to include younger and higher-risk patient populations. The exceptional growth rate of the S-ICD segment is also fuelled by its unique design that places the generator and lead entirely outside the ribcage and vascular system, effectively eliminating the risk of lead fractures, venous occlusions, and endovascular infections that plague traditional transvenous defibrillators. Transvenous leads are historically the weakest link in ICD systems. The S-ICD addresses this critical vulnerability by avoiding direct contact with the heart and blood vessels, significantly reducing the incidence of bloodstream infections, which carry a mortality rate of up to 25 percent. Furthermore, preserving venous access is crucial for patients who may require future pacing or dialysis, making the subcutaneous approach strategically advantageous. Clinical registries have demonstrated that S-ICD systems provide comparable arrhythmia detection and termination efficacy to transvenous systems while offering a superior safety profile regarding lead integrity. As awareness of these long-term benefits spreads, adoption rates are surging, particularly among younger patients who face decades of device dependency and cannot afford the cumulative risk of multiple lead replacements. A further key driver is the broadening of clinical indications and the increasing preference for S-ICD systems among younger patients and those with specific anatomical constraints, driven by the desire to preserve vascular integrity and minimize lifetime procedural risks. Historically restricted to patients without a need for bradycardia pacing or antitachycardia pacing, advancements in programming algorithms and patient selection criteria have expanded the eligible population significantly. The demographic shift towards diagnosing genetic arrhythmia syndromes like Long QT syndrome and Hypertrophic Cardiomyopathy in adolescents and young adults has created a dedicated niche where the longevity and safety of the S-ICD are paramount. Additionally, the aesthetic benefit of a smaller incision and the absence of visible scarring on the chest wall appeals to body-conscious younger demographics. Manufacturers are also investing in smaller form factors and improved sensing algorithms to accommodate a wider range of body habitus, removing previous barriers to implantation. This convergence of expanded eligibility, strong clinical endorsement for youth, and technological refinement is propelling the S-ICD segment to the forefront of market growth.

REGIONAL ANALYSIS

North America Active Implantable Medical Devices Market Analysis

North America led the global active implantable medical devices market and captured a 45.1% share in 2025. This leading position of the North American market is attributed to its advanced healthcare infrastructure, high reimbursement rates for complex device therapies, a large aging population, and the presence of leading global manufacturers driving innovation and early adoption. The United States serves as the primary engine of growth, characterized by a high volume of implant procedures driven by favorable reimbursement policies from Medicare and private insurers that cover advanced technologies like cardiac resynchronization therapy and neurostimulation. The presence of major industry headquarters in states like California and Minnesota fosters a robust ecosystem of research and development, leading to the rapid commercialization of next-generation devices such as leadless pacemakers and closed-loop neurostimulators. Furthermore, the widespread adoption of remote monitoring technologies, supported by specific reimbursement codes, has enhanced patient management and device longevity. The regulatory environment, while stringent, provides a clear pathway for approval through the Food and Drug Administration, ensuring high safety standards that build physician confidence. The concentration of specialized electrophysiology centers and trained professionals ensures that even complex implants are performed efficiently. This combination of financial support, technological leadership, and clinical expertise ensures that North America remains the largest and most sophisticated market for active implantable medical devices globally.

Europe Active Implantable Medical Devices Market Analysis

Europe followed closely behind in the active implantable medical devices market and occupied a share of 28.6% in 2025 because of a universal healthcare framework, strong emphasis on cost-effectiveness, and varying adoption rates across Western and Eastern member states. The region presents a mature market where regulatory harmonization under the EU Medical Device Regulation is reshaping product availability and clinical practices. The European market is distinguished by its centralized procurement processes and health technology assessment bodies that rigorously evaluate the clinical value and economic impact of new devices before granting reimbursement. Countries like Germany, France, and Italy are key contributors, maintaining high standards of care and investing in specialized heart failure clinics that drive the uptake of cardiac resynchronization therapy. However, the implementation of the new EU Medical Device Regulation has introduced stricter clinical evidence requirements, causing some delays in product launches and forcing manufacturers to consolidate their portfolios. Research indicates that while access to innovative therapies is generally high, disparities exist between Northern and Southern European nations regarding the speed of adoption for premium-priced devices. The region is also a leader in the adoption of bioelectronic medicines, with significant research funding directed toward neurostimulation trials. Despite economic pressures and budget constraints in some public health systems, the commitment to equitable access and the growing burden of chronic diseases ensure steady demand. The focus on real-world evidence and post-market surveillance under the new regulatory regime is setting global benchmarks for device safety and performance.

Asia-Pacific Active Implantable Medical Devices Market Analysis

The Asia-Pacific region is emerging as the most dynamic and rapidly expanding market for active implantable medical devices due to the massive populations of China, India, and Japan, improving healthcare infrastructure, rising disposable incomes, and increasing awareness of advanced cardiac and neurological therapies. While historically underserved, the region is witnessing a transformative shift driven by government initiatives and a growing middle class willing to invest in health. China and India are at the forefront of this expansion, driven by government programs aimed at reducing the burden of non-communicable diseases and expanding insurance coverage to include high-cost medical devices. In India, the Ayushman Bharat scheme is providing health insurance to hundreds of millions of low-income citizens, increasingly covering cardiac device implants that were previously inaccessible. Japan, with its super-aged society, drives demand for advanced heart failure management and neurostimulation technologies, maintaining high per capita implant rates similar to Western countries. The rising prevalence of lifestyle-related conditions such as hypertension and diabetes is accelerating the onset of cardiac arrhythmias, expanding the eligible patient pool. Furthermore, the entry of local manufacturers offering cost-effective alternatives is improving accessibility in rural areas. Although challenges related to uneven distribution of specialists and infrastructure persist, the sheer scale of the population and the rapid pace of economic development position Asia-Pacific as the primary growth engine for the future of the active implantable medical devices market.

Latin America Active Implantable Medical Devices Market Analysis

Latin America holds a promising position in the global market, which is driven primarily by Brazil and Mexico, where a growing private healthcare sector, increasing prevalence of chronic diseases, and gradual improvements in public health coverage are beginning to unlock demand for active implantable devices. The region benefits from a young but rapidly aging population and a strong culture of seeking advanced medical care, though economic volatility remains a hurdle. Brazil is the dominant force in the region, boasting the most sophisticated medical infrastructure in Latin America and a high volume of cardiac procedures performed in both public and private sectors. The private sector, serving the affluent demographic, is quick to adopt the latest technologies such as leadless pacemakers and advanced neurostimulators. In Mexico, proximity to the United States facilitates the flow of medical trends and technologies, with many centers of excellence adopting US-standard protocols for device implantation. However, economic instability and currency fluctuations often inflate the cost of imported devices, limiting access for lower-income populations and causing delays in procurement for public hospitals. Despite these challenges, the growing medical tourism industry and the increasing training of local electrophysiologists are fostering a more conducive environment for market growth. As healthcare reforms progress and economic conditions stabilize, Latin America is poised to see accelerated adoption of active implantable technologies.

Middle East and Africa Active Implantable Medical Devices Market Analysis

The Middle East and Africa region expanded moderately in the global active implantable medical devices market. It is constrained by infrastructure deficits, uneven economic development, and limited access to specialized care in many areas, yet displays pockets of high potential in Gulf Cooperation Council countries and South Africa. The region represents a long-term frontier where strategic investments in healthcare modernization and disease prevention could unleash substantial demand. South Africa and the Gulf states serve as the anchors of advancement in the region, with nations like Saudi Arabia, the UAE, and South Africa investing heavily in world-class medical cities and specialized cardiac centers that offer the full spectrum of active implantable therapies. In South Africa, the private healthcare sector maintains high standards and utilizes advanced devices, while the public sector struggles with resource limitations but is benefiting from international partnerships aimed at improving cardiac care. However, the broader African continent faces significant challenges. The rising prevalence of rheumatic heart disease and hypertension in the region creates a critical need for affordable implantable solutions. Improved political stability and increased foreign direct investment, particularly in the Gulf, are transforming the Middle East and Africa from a marginal player into a meaningful contributor to the global market. This shift is accelerated by top-down government mandates and the urgent need to address rising mortality rates from treatable cardiac conditions.

COMPETITIVE LANDSCAPE

The competition in the active implantable medical devices market is characterized by intense rivalry among a few dominant global conglomerates and specialized niche players striving to deliver superior clinical outcomes through technological differentiation. Major competitors focus heavily on innovation cycles aiming to release smaller, smarter and longer-lasting devices that reduce surgical complexity and improve patient quality of life. The landscape is shifting as companies increasingly compete on the strength of their digital ecosystems and remote monitoring capabilities, which have become critical decision factors for healthcare providers. Rivalry often manifests through aggressive patent litigation and rapid product launches designed to secure first-mover advantages in emerging therapeutic areas like bioelectronic medicine. Smaller firms differentiate themselves by targeting specific unmet needs, such as leadless pacing or directional neurostimulation, that larger entities may overlook initially. Pricing pressure exists due to group purchasing organizations and government tenders, but premium pricing remains sustainable for breakthrough technologies offering distinct clinical benefits. Regulatory compliance and post-market surveillance capabilities are also key battlegrounds as safety records directly influence brand reputation and physician loyalty. Ultimately, the competitive dynamic is driven by the ability to combine engineering excellence with compelling clinical data to win trust in a high-stakes environment.

KEY MARKET PLAYERS

Notable companies operating in the global active implantable medical devices market profiled in this report are

- Medtronic PLC

- Abbott Laboratories

- Boston Scientific Corporation

- BIOTRONIK SE & Co. KG

- LivaNova

- Cochlear Limited

- MED-EL

- Sonova Holding AG

- William Demant Holding A/S

- Nurotron Biotechnology Co. Ltd.

TOP PLAYERS IN THE MARKET

- Medtronic plc stands as a global leader in the active implantable medical devices sector with an extensive portfolio spanning cardiac rhythm management, neurostimulation, and insulin delivery systems. The company plays a pivotal role in advancing life-saving therapies through continuous innovation in miniaturization and connectivity features for pacemakers and defibrillators. Recent actions include the launch of next-generation leadless pacemakers and the expansion of its remote monitoring platforms to enhance patient outcomes globally. Medtronic has also strengthened its position by acquiring specialized bioelectronic medicine firms to diversify into new therapeutic areas like hypertension management. By leveraging vast clinical data and artificial intelligence, the firm optimizes device algorithms for personalized care. Its commitment to improving access in emerging markets through training programs further solidifies its reputation as a dominant force dedicated to alleviating the burden of chronic disease worldwide through advanced technological solutions.

- Abbott Laboratories is a major contributor to the market, renowned for its groundbreaking work in heart failure management and structural heart solutions alongside its robust cardiac rhythm division. The company has revolutionized the industry with the introduction of fully implantable left ventricular assist devices and leadless pacemaker systems that minimize surgical risks. Recent actions involve significant investments in digital health integration, allowing seamless data transmission from implants to clinicians for proactive care management. Abbott has also expanded its neuromodulation portfolio with targeted spinal cord stimulation therapies for chronic pain. The firm focuses heavily on reducing the size of implants while extending battery life to improve patients' quality of life. Through strategic partnerships with research institutions, Abbott accelerates the development of closed-loop systems that automatically adjust therapy based on physiological needs. These efforts demonstrate its dedication to setting new standards in safety and efficacy for patients relying on active implantable technologies across the globe.

- Boston Scientific Corporation is a key player known for its diverse range of active implants, including deep brain stimulators, sacral nerve stimulators, and advanced cardiac defibrillators. The company excels in developing minimally invasive solutions that address complex neurological and cardiovascular conditions with high precision. Recent actions include the commercialization of directional deep-brain stimulation systems that offer greater control over symptom management for Parkinson's disease patients. Boston Scientific has also enhanced its cardiac portfolio with subcutaneous implantable cardioverter defibrillators that eliminate lead-related complications. The firm actively pursues growth through strategic acquisitions of innovative startups specializing in bioelectronic medicine and smart sensor technology. By focusing on user-centric design and robust remote monitoring capabilities, Boston Scientific ensures its devices meet the evolving needs of both clinicians and patients. This relentless pursuit of innovation and clinical excellence strengthens its market position as a trusted provider of critical therapies that restore health and improve longevity for individuals worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the active implantable medical devices market primarily employ strategic acquisitions and partnerships to expand their product portfolios and gain access to cutting-edge technologies in bioelectronics and digital health. Companies frequently invest heavily in research and development to create smaller, more efficient devices with extended battery life and enhanced connectivity features for remote monitoring. Another major strategy involves obtaining regulatory approvals in multiple regions simultaneously to accelerate global market entry and maximize commercial potential. Market participants are also focusing on building comprehensive ecosystems that integrate devices with cloud-based analytics platforms to provide actionable insights for clinicians. Establishing strong relationships with key opinion leaders and clinical centers helps firms validate their technologies through robust real-world evidence generation. Additionally, companies are expanding into emerging markets by localizing manufacturing and offering tailored financing solutions to overcome cost barriers. These strategies collectively enable leaders to drive innovation and capture significant market opportunities.

MARKET SEGMENTATION

This research report on the global active implantable medical devices market has been segmented and sub-segmented based on the product and region.

By Product

- Implantable Cardioverter Defibrillators

- Transvenous Implantable Cardioverter Defibrillators

- Biventricular Implantable Cardioverter Defibrillators (ICDs)/Cardiac Resynchronization Therapy Defibrillators (CRT-Ds)

- Dual-Chamber Implantable Cardioverter Defibrillators

- Single-Chamber Implantable Cardioverter Defibrillators

- Subcutaneous Implantable Cardioverter Defibrillator

- Transvenous Implantable Cardioverter Defibrillators

- Implantable Cardiac Pacemakers

- Ventricular Assist Devices

- Implantable Heart Monitors/Insertable Loop Recorders

- Neurostimulators

- Spinal Cord Stimulators

- Deep Brain Stimulators

- Sacral Nerve Stimulators

- Vagus Nerve Stimulators

- Gastric Electrical Stimulators

- Implantable Hearing Devices

- Active Hearing Implants

- Passive Hearing Implants

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which devices lead the global active implantable medical devices market?

Implantable cardioverter defibrillators (ICDs), neurostimulators, and pacemakers are among the leading devices in the global active implantable medical devices market

2. What factors are driving growth in the global active implantable medical devices market?

Rising chronic cardiovascular and neurological disorders, aging demographics, demand for minimally invasive procedures, and innovation in device technology drive the market

3. How do neurostimulators contribute to the global active implantable medical devices market?

Neurostimulators manage chronic pain and neurological disorders, significantly boosting adoption and growth within the global active implantable medical devices market

4. What is the role of implantable drug pumps in the global active implantable medical devices market?

Implantable drug pumps enable targeted drug delivery for cancer and arthritis, expanding treatment options and stimulating growth in the global active implantable medical devices market

5. How do technological innovations impact the global active implantable medical devices market?

Miniaturization, longer battery life, wireless connectivity, and MRI-safe designs enhance device performance and patient outcomes in the global active implantable medical devices market

6. Which regions dominate the global active implantable medical devices market?

North America leads the market, followed by Europe and Asia Pacific, due to advanced healthcare infrastructure and growing patient populations

7. How does the aging population affect the global active implantable medical devices market?

An increasing elderly population with chronic conditions drives demand for implantable devices, propelling growth in the global active implantable medical devices market

8. What challenges does the global active implantable medical devices market face?

Key challenges include high device costs, stringent regulatory pathways, frequent product recalls, and limited reimbursement in developing countries

9. How is AI integrated in the global active implantable medical devices market?

AI enables remote monitoring and predictive analytics, improving patient management and broadening market opportunities in the global active implantable medical devices market

10. What are MRI-safe implantable devices in the global active implantable medical devices market?

MRI-safe devices allow patients to undergo MRI scans safely, increasing device adoption and patient convenience in the global active implantable medical devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com