Europe Advanced Infusion Systems Market Research Report By Application, Product, End-User & Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) – Industry Size, Share, Trends & Growth Forecast (2026 to 2034)

Market Size, 2025

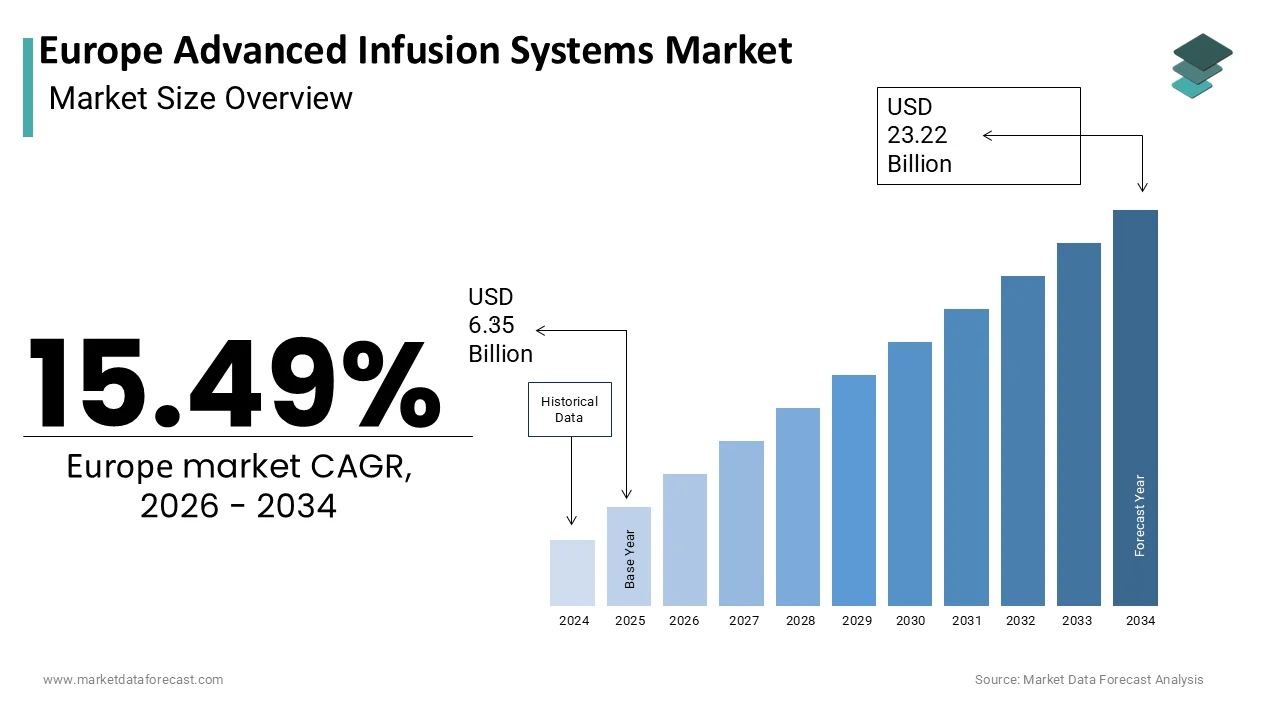

$6.35 BnMarket Estimate, 2026

$7.34 BnMarket Forecast, 2034

$23.22 BnCAGR, 2026–2034

15.49%Europe Advanced Infusion Systems Market Summary

Market Size & Growth

- The Europe Advanced Infusion Systems Market was valued at USD 6.35 billion in 2025.

- Expected to reach USD 23.22 billion by 2034, growing at a CAGR of 15.49% from 2026 to 2034.

- Germany leads the regional market with a 25.1% share in 2024; the UK holds second place with 18.1%.

Key Market Segments

- By Application Type: Chemotherapy, Diabetes, Pain Management, Clinical Nutrition, Asthma Treatment

- By Product Type: Volumetric Infusion System (largest, 2024), Ambulatory Infusion System (fastest-growing, CAGR 9.1%), Syringe Infusion System, Patient Controlled Analgesia Pump, Elastomeric Infusion System, Implantable Infusion System, Disposable Infusion System

- By End-User: Hospitals (dominant), Ambulatory Surgical Centers (fastest-growing, CAGR 7.8%), Diagnostic Centers

- By Country: UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe

Key Drivers

- Rising cancer burden in Europe — an estimated 2.74 million new cancer cases were diagnosed in the EU in 2022, driving demand for precise chemotherapy infusion protocols.

- EU digital health mandates, including the European Health Data Space regulation (in force 2024), requiring interoperable medical device connectivity with hospital information systems.

- Expansion of ambulatory and home-based infusion therapy, particularly OPAT and biologic infusions, supported by national reimbursement frameworks in Germany and the Netherlands.

Key Restraints

- Extended certification timelines under EU Medical Device Regulation (EU MDR), significantly increasing time-to-market for new devices.

- Persistent shortages of clinical engineering personnel across Europe, limiting device maintenance and fleet modernization.

Leading Application Segment

The Chemotherapy segment held the largest share of 29.1% in 2024. The Diabetes segment is forecast to register the highest CAGR of 8.2% from 2025 to 2033.

Key Players

Becton Dickinson (BD Alaris), B. Braun Melsungen AG, Fresenius Kabi, Baxter International Inc., Medtronic Inc., Terumo Corporation, CareFusion Corporation, AngioDynamics Inc., Johnson and Johnson, F. Hoffmann-La Roche Ltd., I-Flow Corporation, Hospira Inc.

Europe Advanced Infusion Systems Market Size

The Europe Advanced Infusion Systems Market is projected to grow from USD 6.35 billion in 2025 to USD 7.34 billion in 2026 and reach USD 23.22 billion by 2034, registering a CAGR of 15.49% during the forecast period from 2026 to 2034.

Advanced infusion systems are medical devices engineered to deliver precise volumes of fluids, medications, and nutrients intravenously with enhanced safety monitoring and connectivity capabilities. These systems include smart pumps with dose error reduction software, wireless interoperability with electronic health records, nd integrate,d pressure sensors to detect occlusions or infiltration. In Europe, their deployment is driven not by technological novelty alone but by systemic imperatives in patient safety and healthcare efficiency. According to multiple sources, healthcare bodies across the European Union acknowledge that medication errors represent a significant burden on public health and patient safety, which emphasizes the importance of prevention at all stages of care. As per research, healthcare systems globally are increasingly focusing on the preventability of medication errors, with a strong trend towards implementing technological safeguards to improve patient outcomes. Furthermore, the European Commission and the World Health Organization actively promote the development and adoption of digital health solutions, emphasizing the critical role of data sharing and interoperable medical devices in modern, integrated care pathways. A substantial volume of patient care activities in the EU involves intravenous therapy, which emphasizes the continuous need for robust and effective systems within the region’s healthcare infrastructure to ensure patient safety. Their role extends beyond acute care into oncology,gy home care, re and ambulatory settings, reflecting a broader shift toward precision drug delivery and remote patient monitoring.

MARKET DRIVERS

Escalating Burden of Chronic and Oncological Conditions Requiring Complex Infusion Protocols

The rising prevalence of chronic diseases, particularly cancer, cardiovascular disorders, and autoimmune conditions, has intensified demand for sophisticated infusion therapies, thereby contributing to the growth of the European advanced infusion systems market. These therapies require precise dosing and continuous monitoring. According to the European Cancer Information System (ECIS), an estimated 2.74 million new cancer cases were diagnosed in the European Union in 2022, with a projected 2.7 million new cases for 2024, reflecting the massive burden of cancer on the continent. Many of these therapies, such as monoclonal antibodies and targeted kinase inhibitors, necessitate extended infusion durations and narrow therapeutic windows where even minor dosing deviations can trigger severe toxicity. As per sources, the adoption of smart infusion systems in EU hospitals is increasing, driven by the need to improve patient safety, reduce medication errors, and manage the growing prevalence of chronic conditions like cancer. Similarly, patients with rheumatoid arthritis or multiple sclerosis receiving biologic infusions in day hospitals rely on advanced systems that ensure consistent flow rates and document administration for regulatory compliance. This clinical complexity transforms infusion pumps from basic delivery tools into indispensable safety gatekeepers within modern therapeutic pathways across oncology rh, rheumatology, and neurology.

EU Mandates for Health Technology Interoperability and Digital Care Integration

Regulatory frameworks across the region are increasingly requiring medical devices to operate within connected digital ecosystems to enhance care coordination and data transparency, which in turn drives the expansion of theEuropeane advanced infusion systems market. The European Union's evolving digital health strategy and initiatives like the European Health Data Space are increasingly promoting the adoption of standardized communication protocols to enhance the interoperability of medical devices, such as infusion systems, with hospital information systems, moving towards a more connected healthcare ecosystem. Moreover, the European Health Data Space regulation, which entered into force in 2024, establishes a framework that fosters a single market for interoperable electronic health record systems and promotes the secure reuse of health data for secondary purposes, including post-market surveillance and clinical decision support, driving a trend toward more comprehensive data integration. Countries like Denmark and the Netherlands have already made interoperability a prerequisite for public hospital procurement. This regulatory trajectory compels healthcare providers to replace legacy pumps with advanced models not merely for safety but to comply with national digital health strategies th, thereby accelerating adoption across public and private institutions.

MARKET RESTRAINTS

Stringent and Prolonged Regulatory Approval Timelines Under the EU MDR

The transition to the European Union Medical Device Regulation has significantly extended the time and cost required to bring new infusion systems to market. This poses a major restraint to theEuropeane advanced infusion systems market. According to the transition toEuropeanDR has substantially increased, the time required for device certification has substantially increased compared to the former Medical Devices Directive framework. Stricter regulatory requirements, particularly for clinical evaluation and risk management documentation, contribute significantly to the extended certification timelines. As per studies, submissions for advanced, software-driven devices frequently encounter non-conformities related to demonstrating compliance with evolving cybersecurity and software validation requirements. Smaller innovators and startups struggle to meet these demands due to limited regulatory expertise and financial resources. Consequently, the pace of technological refresh in European hospitals has slowed with many institutions retaining older non-smart pumps beyond their inte,nded service life. This barrier not only stifles innovation but also delays the dissemination of safety-enhancing features such as predictive occlusion detection or AI drsafety-enhancingts across the healthcare system.

Persistent Shortages of Skilled Clinical Engineering Personnel for System Maintenance

The effective operation and maintenance of these systems depend on a specialized workforce of clinical engineers and biomedical technicians, which further obstructs the growth of the European advanced infusion systems market. Their numbers are critically insufficient across much of Europe. According to sources, there is a recognized challenge regarding sufficient clinical engineering staffing levels in healthcare systems, particularly in certain regions of Europe. As per a study, the maintenance and updating of complex medical devices, such as infusion pumps, face resource constraints, which can lead to operational delays and potential safety concerns. This gap compromises device reliability and safety. The availability of appropriately certified and trained biomedical engineers to manage and update specialized medical equipment varies across different countries and regions, impacting equipment readiness and compliance. Lack of expert support can cause even high-end systems to malfunction and compromise safety. The absence of harmonized training pathways and career incentives for clinical engineers further exacerbates this structural constraint, limiting the real-world impact of infusion technology investments.

MAR,KET OPPORTUNITIES

Expansion of Ambulatory and Home-Based Infusion Therapy Across Europe

The shift towards delivering complex infusion therapies outside traditional hospitals is providing new opportunities for the European advanced infusion systems market. This expansion creates a robust European corridor for portable and user-friendly advanced infusion systems. According to research, A steady trend toward dehospitalization for various medical treatments, including intravenous antibiotic courses and biologic infusions, is widely observed across Europe, driven by efforts to improve efficiency and patient quality of life. Countries like Germany and the Netherlands have established national frameworks for home infusion care reimbursed under statutory health insurance. The German healthcare system is expanding the use of home-based intravenous therapy (Outpatient Parenteral Antimicrobial Therapy, or OPAT) as a cost-effective alternative to inpatient care, with the aid of new practice guidelines and technological advancements in remote patient monitoring. These devices enable real-time clinician oversight while preserving patient autonomy. Manufactreal-time responding with pocket-sized elastomeric pumps and ambulatory syringe drivers equipped wipocket-sized connectivity and low occlusion alarms tailored for non-clinical environments. This care model not only reduces hospital bed pressure but also aligns with patient preferences for treatment at home, thereby unlocking a high compliance and high value segment beyond acute care walls.

Integration of Artificial Intelligence for Predictive Infusion Safety

The incorporation of artificial intelligence into these sophisticated medical devices offers major potential for anticipating and preventing adverse events before they occur, which is expected to fuel the growth of the European advanced infusion systems market. Leading European hospitals are piloting next-generation pumps that use machine learning algorithms to analyze next-generation flow and patient vital sign data to predict complications such as infiltration or extravasation. AI-enabled infusion systems detect subtle pressure deviations that are not identifiable by conventional sensors. These systems are designed to reduce the frequency of infiltration incidents within clinical environments. Research initiatives are currently focused on validating these predictive models across diverse patient populations. Apart from these, AI-driven systems can personalize infusion rates based on individual pharmacokinetic profiles derived from electronic health records. In Finland, the national health agency is testing an adaptive insulin infusion protocol,s that adjusts delivery in real time using glucose trend data. This evolution from reactive to proactive safety not only enhances clinical outcomes but also positions advanced infusion systems as dynamic components of precision medicine ecosystems.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Networked Infusion Devices

The growing exposure to cyber threats can compromise patient safety and data integrity, and this greatly degrades the growth of the European advanced infusion systems market. This is because infusion systems are becoming increasingly connected to hospital networks. Medical devices, including essential equipment like infusion pumps, sometimes contain critical vulnerabilities. Common security weaknesses may include unpatched operating systems, weak authentication methods, or unencrypted data transmission. Simulated cyberattacks have demonstrated the potential for unauthorized actors to remotely alter the functions of some smart pumps. Devices lacking specific security mechanisms, such as secure boot features, can be more susceptible to remote tampering. Hospitals often struggle to apply security patches due to regulatory constraints requiring revalidation after any software modification. As per the European Coordination Group for Medical Devices m, any institutions operate mixed fleets of infusion pumps with incompatible firmware, making enterprise-wide protection unfeasible. This cyber fragility not only risks direct patient harm but also deters procurement of the most connected devices, particularly in resource-constrained public hospitals. Interoperable inf,usion systems cannot reach their full potential until the EU MDR implements harmonized cybersecurity standards and streamlined patching processes, which are currently hindered by legitimate safety and compliance concerns.

High Total Cost of Ownership Beyond Initial Procurement

The financial burden of deploying these systems extends far beyond the purchase price, which further inhibits the expansion of the European advanced infusion systems market. It includes software licensing, engineering, maintenance, and integration expenses that strain healthcare budgets. According to a study, the total cost of ownership for a smart infusion pump may exceed its initial acquisition cost because of ongoing fees for necessary software updates, safety certifications, and support agreements. In public hospitals across Italy and Spain, where capital budgets are tightly controlled, these hidden costs have led to underutilization of purchased features or delays in fleet renewal. As per research, many smart pumps in hospitals might not have the most current drug information available because of challenges in consistently funding the recurring subscription fees. Furthermore, integrating smart pumps with existing hospital health records can present technical challenges, sometimes requiring the development of customized software to ensure proper communication between the systems. This economic reality forces institutions to make trade-offs between technological sophistication and fiscal sustainability,y thereby limiting equitable access to the safest infusion technologies ac,, ross Europe’s diverse healthcare systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application Type, Product Type, End-Users, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Hospira, In,c. AngioDynamics, Inc., Medtronic, Inc., Terumo Corporation, Johnson & Johnson, CareFusion Corporation, Animas Corporation, Baxter International, Inc., B. Braun Melsungen AG, I-Flow Corporation, and F. Hoffmann-La Roche Ltd. |

The chemotherapy segment captured the leading share of 29.1% of tEuropeanope advanced infusion systems market in 2024. The leading position of tEuropanEuropeanmotherapy segment is attributed to high precision requirements for cytotoxic agent delivery in oncology, and the EU regulatory classification of chemotherapy drugs as high-risk medications. Chemotherapy agents operate within extremely narrow therapeutic windows where dosing inaccuracies can lead to life-threatening toxicity or treatment failure. According to sources, life-threatening therapies in European hospitals generally utilize volumetric or syringe infusion pumps featuring integrated drug libraries and dose limits to mitigate potential calculation errors. In addition, European healthcare facilities administer intravenous chemotherapy to a significant number of patients annually. The complexity of multi-drug regimens, often involving sequential infusions of anthracycline and monoclonal antibodies, demands pumps capable of programmable multi-step protocols with air embolism and occlusion detection. Smart infusion systems are utilized in oncology centers for the administration of high-risk chemotherapeutic agents. This clinical necessity transforms advanced infusion technology from optional to essential in oncology units across Europe. Under the current guidance for high-risk medicines, certain potent pharmaceutical agents are designated as requiring enhanced safeguards during administration. This classification compels hospitals to deploy infusion systems with dose error reduction software and mandatory staff override documentation. Within the framework of safe medication practices, member states are encouraged to ensure that the delivery of chemotherapy aligns with established safety standards. In Germany, national bodies oversee regular reviews of drug library compliance within oncology settings. These regulatory imperatives institutionalize the use of advanced systems far beyond individual clinician preference, creating a structurally resilient demand base that outpaces other application areas.

The diabetes application segment is predicted to witness the highest CAGR of 8.2% from 2025 to 2033. The rapid expansion of the diabetes application segment is propelled by rithe sing adoption of insulin pump therapy among type 1 diabetes patients, and integration of digital health ecosystems and remote monitoring capabilities. Europe is witnessing a significant shift toward continuous subcutaneous insulin infusion as first-line therapy for type 1 diabetes p, particularly among pediatric and adult populations. National health systems are increasingly covering advanced systems that integrate with continuous glucose monitors to enable hybrid closed-loop functionality. These systems, classified as advanced infusion closed-loop under EU MDR, require precise basal and bolus delivery algorithms that dynamically adjust based on real-time glucose trends, thereby reducing hypoglycemic events. Modern insulin infusion systems are no longer standalone devices but components of broader digital diabetes management platforms. Insulin pumps that have Bluetooth-enabled data sharing capabilities may qualify for reimbursement under certain national digital health benefit schemes in various countries. These devices allow the sharing of data to clinician portals and caregiver applications. Statutory health insurers in certain countries may provide coverage for cloud-connected pumps. This coverage is often based on evidence that remote monitoring can support patient health outcomes. Furthermore, specific guidelines have been issued for the secure transmission of glycemic data, which helps ensure compliance with data protection regulations while enabling telehealth support. This convergence of medical device innovation, data privacy assurance, and payer recognition transforms diabetes infusion systems into dynamic tools for preventive care, accelerating adoption beyond traditional endocrinology clinics into primary care and home settings.

By Product Type Insights

The volumetric infusion system segment was the largest in the European advanced infusion systems market and captured a sha.1% in 2024. Factors such as its versatility and regulatory entrenchment in high acuity settings have mainly contributed to the prominence of the volumetric infusion system segment. Volumetric pumps are the standard of care for fluid resuscitation, antibiotic delivery, nd vasoactive support in intensive care units across Europe. These systems offer superior accuracy for large volume infusions, typically delivering between one and nine hundred ninety-nine milliliters per hour with built-in air detection and pressure monitoring essential for unstable patients. National clinical guidelines in countries like the UK and France mandate volumetric over syringe pumps for fluid boluses and maintenance therapy due to their robustness and alarm systems. This institutional standardization ensures consistent procurement regardless of budget fluctuations. Under the EU Medical Device Regulation, volumetric infusion systems are classified as Class IIb devices, requiring comprehensive clinical evaluation and post-market surveillance. The European Commission's interoperability roadmap further requires all new volumetric pumps to support standardized data exchange with hospital information systems using IHE profiles. Many public hospitals procuring new volumetric pumps now require integrated electronic prescribing verification to prevent medication errors. This regulatory scaffolding elevates volumetric systems from commodity equipment to critical safety infrastructure, thereby securing their central role in hospital formularies and publi,,c procurement tenders across the region.

The ambulatory infusion system segment is estimated to register the fastest CAGR of 9.1% during the forecast period due to the expansion of home-based and outpatient parenteral therapy programs, and technological convergence with telemedicine and real-time monitoring. European healthcare systems are actively shifting complex infusions out of hospitals to reduce costs and improve patients' quality of life. Home-based intravenous antibiotic therapy is a widely utilized treatment method for various infections. This approach involves administering antibiotics directly into the bloodstream in a home setting, providing a convenient alternative to traditional inpatient care. Similarly, the use of biologics for rheumatological and immunological conditions via home infusion is a well-established practice. Ambulatory pumps, ps lightweight bbattery-poweredand often wearable, are essential enablers of this dehospitalization trend. These outcomes have prompted reimbursement reforms that explicitly fund advanced ambulatory systems as part of integrated care packages. Next-generation ambulatory pumps now incorporate cellular or Bluetooth connectivity to transmit infusion data to clinical teams in real time. Additionally, EU cybersecurity certification schemes now include specific modules for wearable infusion devices en,, ensuring data integrity without compromising usability. This fusion of mobility, connectivity, and regulatory trust positions ambulatory systems as the cornerstone of Europe’s future decentralized care model.

By End User Insights

The hospitals segment dominated the European advanced infusion systems market by accounting for a substantials Europeann 2024. The dominance of the hospitals segment is driven by its role as the primary site for complex intravenous therapy. Hospitals administer the vast majority of high-risk infusions i, including chemotherapy, vasoactive drugs, and total parenteral nutrition under strict protocols that mandate advanced safety features. National patient safety initiatives require hospitals to maintain fleets of smart pumps with up to date drug libraries and interoperability with electronic prescribinup-to-daup-to-date This regulatory and operational concentration ensures hospitals remain the core demand engine despite growth in outpatient settings. Unlike decentralized ambulatory centers,s hospitals benefit from consolidated purchasing power through national or regional group purchasing organizations. Furthermore, hospital capital budgets, often supported by EU structural funds for digital health modernization, allomulti-yearar investment cycles for fleet renewal. This institutional multi-year infrastructure sustains high volume, consistent demand that outpaces the fragmented ambulatory and diagnostic sectors.

The ambulatory surgical centers segment is anticipated to witness the fastest CAGR of 7.8% over the forecast period, owing to the rise of complex same-day surgical procedures requiring postoperative infusion, and payer incentives for cost-efficient care delivery models. Ambulatory surgical centers in Europe are increasingly performing procedures that historically required inpatient admission ncluding orthopedic arthroscopies, hernia repair,s and minor oncology interventions. According to sources, a notable shift has been observed in the practice of performing surgical procedures, with a growing number of them now conducted in outpatient settings. These cases often necessitatepostoperative pain management via patient-controlled analgesia or antiemetic infusions during recovery. As per sources, regulatory standards are evolving in certain regions, implementing new requirements for the availability and capabilities of medical equipment in high-volume ambulatory centers. This regulatory shift compels rapid technology adoption even among small independent facilities. National health insurers across Europe actively reimburse procedures at ambulatory centers at higher relative rates to encourage hospital diversion. These financial incentives drive investment in compact re, liable infusion systems tailored for short stay environments. Manufacturers have responded with space-saving modular pumps that meet both clinical safety and spatial constraints of ambulatory recovery bays. This alignment of clinical capability, payer policy,y and facility economics fuels accelerated adoption in a previously underpenetrated segment.

COUNTRY LEVEL ANALYSIS

Germany Advanced Infusion Systems Market Analysis

Germany was the top performer in the European advanced infusion systems market and captured a 25.1% share in 2Europeanhe supremacy of the German market is credited to its dense network of university hospitals s, stringent patient safety regulations, and robust public health insurance coverage for high technology medical devices. Germany’s statutory health insurers cover advanced infusion therapy for home-based oncology and antibiotic treatment w, with a significant number ofhome-basedenrolled. Additionally, the Medical Device Regulation enforcement agency BfArM conducts annual a,udits of infusion pump drug library compliance in critical care units, ensuring continuous system updates. This ecosystem of regulation, reimbursement, and quality control sustains both high volume and high soph,istication in device utilization across acute and ambulatory settings.

United Kingdom Advanced Infusion Systems Market Analysis

The United Kingdom was the second-largest country in theEuropeane advanced infusion systems market and captured a 18.1% share in EuropeanEuropeanhe demand for these systems in the UK is fuelled by its centralized procurement and fortional safety mandates. Through the NHS Supply Chain the UK standardizes infusion pump specifications across all hospital tru,, sts en, ensuring uniform adoption of dose error reduction software and interoperable platforms. The UK also leads in home infusion adoption with a large number of patients receiving intravenous therapy at home in 2023 ma,,inly enabled by connected ambulatory pumps. Post Brexit, the Medicines and Healthcare products Regulatory Agency has maintained EU MDR-aligned requirements while introducing expedited pathways for cybersecurity-certified devices. This blend of centralized oversight, innovation adoption, nd safety governance solidifies the UK’s position a,s a high-compliance and high-performance market.

France Advanced Infusion Systems Market Analysis

France is steadily growing in the European advanced infusion systems market, with its proactive digital health strategy and strong oncology infrastructure. The French government's health initiative requires that new hospital technology be capable of transmitting data electronically to a national medical record system. A number of cancer treatment facilities in France already use a form of specialized equipment that incorporates drug information libraries. France’s statutory health insurance provides full coverage for insulin pumps and ambulatory systems for chronic conditions. Apart from these, the country hosts major R and D hubs for infusion technology, including Becton Dickinson’s European Innovation Center in Paris, which focuses on predictive occlusion detection. This convergence of pol, icy investment, and clinical need fuels sustained market leadership.

Italy Advanced Infusion Systems Market Analysis

Italy continues to hold a significant position in the Europea dvanced infusion systems market due to regional variation and growing investment in home care infrastructure. Northern Italian regions such as Lombardy and Emilia Romagna are continuing to use advanced hospital infusion protocols whilee Southern regions work to ease hospital bed shortages by rapidly expanding home-based infusion programs. According to research, A substantial number of patients received home infusion therapy, supported by various funding sources. More advanced infusion systems have been approved for reimbursement. Prioritization has been given to systems featuring specific language interfaces and remote monitoring capabilities. The country’s high prevalence of chronic diseases further drives demand for insulin and biologic infusion systems. Despite budget constraints, Italy’s decentralized yet innovative landscape offers diversified growth pathways across inpatient and community settings.

Netherlands Advanced Infusion Systems Market Analysis

The Netherlands is likely to expand notably in the European advanced infusion systems market over the forecast period. It serves as Europe’s model for integrated infusion safety ecosystems. Dutch hospitals operate under the national Veilig Medicijnen Gebruik program wh, which requires all infusion pumps to be connected to a central safety server that logs overrides and alerts in real time. The Netherlands also leads in ambulatory infusion w,, with home care organizations using wearable pumps for immunoglobulin and antibiotic therapy covered under the national basic insurance package. Furthermore, the Dutch Medicines Evaluation Board collaborates with manufacturers on pre-market validation of drug library content, ensuring rapid deployment of new protocols. This holistic approach, linking regulation technology and care delivery, makes the Netherlands a benchmark for infusion safety and a fertile ground for next-generation system adoption.

COMPETITIVE LANDSCAPE

The European advanced infusion systems market is characterized by intense competition among established global players and specialized European manufacturers operating within a stringent regulatory and safety-driven environment. Competition is defined not by price but by clinical validation, regulatory ccompliance interoperability, ty and total cost of ownership, hip including training,ning maintenance, and software updates. Leading companies differentiate through proprietary drug library content, predictive safety algorithms, and seamless integration with national digital health infrastructures. The market is highly consolidated in hospital procurement due to centralized tenders, yet fragmented in ambulatory and home care segments, where smaller innovators gain traction with portable and connected devices. Barriers to entry remain high owing to the EU Medical Device Regulation’s demanding clinical evidence and post market surveillance requirements, along with the need for extensive clinical engineering support. National variations in reimbursement interoperability mandates and patient safety standards compel companies to adopt localized strategies rather than pan-European rollouts. Consequently,s successfavors firms that combine deep clinical insight, robust cybersecurity certification, and agile service networks capable of supporting complex hospital ecosystems while adapting to emerging outpatient care models across Europe’s diverse healthcare landscape.

KEY MARKET PLAYERS

Some European companies that are playing a dominating role in the europe advanced infusion systems market include

- Hospira, Inc.

- AngioDynamiEuropeaEuropeanc.

- Medtronic, Inc.

- Terumo Corporation

- Johnson & Johnson

- CareFusion Corporation

- Animas Corporation

- Baxter International, Inc.

- B. Braun Melsungen AG

- I-Flow Corporation

- F. Hoffmann-La Roche Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Becton Dickinson is a global leader in medical technology with a significant footprint in the European advanced infusion systems market through its Alaris smart infusion platform. The company contributes to global standards in infusion safety by integrating dose error reduction software interoperability with electronic health records and predictive analytics. In Europe, BD collaborates closely with national health agencies to align its systems with regional drug libraries and safety protocols. Recently t, the company upgraded its Alaris platform with enhanced cybersecurity features compliant with Ethe EUMedical Device Regulation and launched a cloud-based analytics dashboard for hospital pharmacists to monitor infusion compliance across wards. These innovations reinforce BD’s role as a strategic partner in Europe’s medication safety transformation.

- Braun is a Germany-based multinational that plays a pivotal role in the European advGermany-basedn systems landscape through its Space and Vista portfolios of smart and ambulatory pumps. The company is deeply embedded in European healthcare systems offering localized drug libraries m, multilingual interface,s and seamless i,,ntegration with hospital information systems across EU member states. B. Braun emphasizes sustainability and cybersecurity in its device design, reflecting European regulatory priorities. Also, its initiatives str,engthen its commitment to precision infusion across acute and community care settings.

- Fresenius Kabi, a subsidiary of Fresenius SE, is a key European provider of advanced infusion systems with a strong focus on oncology nutrition and pain management applications. The company leverages its integrated model, combining infusion devices with proprietary IV drugs andnutritional solutionsn,s to deliver end to end therapy management. In Europe F,, Fresenius Kabi’s infusion systems are widely adopted in university hospitals and cancer centers due to their validated drug databases and safety protocols. Recently, the company launched a next-generation lumetric pump featuring AAI-drivenocclusion prediction and interoperability with national eHealth records in France and the Netherlands. Aligning advancements in medical devices with real-world clinical applications and strict regulatory guidelines helps Fresenius Kabi solidify its standing as a trusted collaborator for secure and streamlined infusion treatments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European advanced infusion systems market prioritize regulatory compliance Europeanhe EU Medical Device Regulation by embedding cybersecurity features and standardized interoperability protocols into their devices. They invest heavily in localized drug libraries and multilingual software to meet national clinical requirements across diverse healthcare systems. Companies pursue strategic partnerships with public hospital group purchasing organizations and national health agencies to secure large-scale procurement contracts. Innovation focuses on predictive safety analytics remote monitoring and integration with electronic health records to s,,upport decentralize,d care models. Additionally, they expand manufacturing and service infrastructure within Europe to ensure supply chain resilience and rapid post market support for high-reliability clinical operations.

EUROPE ADVANCED INFUSION SYSTEMS MARKET NEWS

- In March 2024 B, Becton Dickinson upgraded its Alaris infusion system with enhanced cybersecurity protocols compliant with EU Medical Device Regulation requirements. This technical enhancement is anticipated to ensure regulatory approval continuity and strengthen theEuropeane Advanced Infusion Systems Market presence.

- In June 2024, B. Br n urope and a new ambulatory infusion pump featuring real-time remote monitoring and Bluetooth connectivity for home-based oncology therapy in Germany and the Netherlands. This product innovation is anticipated to expand access to decentralized care and strengthen the EuEuropeandvanced Infusion Systems Market presence.

- In September 2024, Fresenius Kabi introduced an AI AI-poweredlumetric infusion pump with pr,edictive occlusion detection integrated into national eHealth records in France. This clinical advancement is anticipated to reduce infusion complications and strengthen theEuropeane Advanced Infusion Systems Market presence.

- In November 2024, BectEuropeanankinson partnered with the UK National Health Service to deploy a cloud-based infusion analytics platform across twenty-five hospital trusts. This collaboration is anticipated to improve medication safety oversight and strengthen the Europe Advanced Infusion Systems Market presence.

- In February 2025, B. BrEuropeanpanded its advanced infusion system manufacturing capacity at its Melsungen Germany f, Germany facility to support growing demand for interoperable hospitaldevices. This capacity investment is anticipated to enhance supply reliability and strengthen the Europe Advanced Infusion Systems Market presence.

MARKET SEGMENTATION

This research report on the European advanced infusion systems market is segmented & sub-segmented into the following categories.

By Application Type

- Clinical Nutrition

- Chemotherapy

- Pain Management

- Diabetes

- Asthma Treatment

By Product Type

- Disposable Infusion System

- Elastomeric Infusion System

- Ambulatory Infusion System

- Volumetric Infusion System

- Patient Controlled Analgesia Pump

- Syringe Infusion System

- Implantable Infusion System

By End-Users

- Diagnostic Centers

- Hospitals

- Ambulatory Surgical Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers propelling the Europe Advanced Infusion Systems Market expansion?

The Europe Advanced Infusion Systems Market growth is primarily driven by the increasing prevalence of chronic conditions such as diabetes, cancer, and cardiovascular diseases requiring long-term intravenous therapy, along with the growing geriatric population more susceptible to these ailments. Additional catalysts include technological innovations like smart infusion pumps with real-time monitoring capabilities, improved healthcare infrastructure investments, stringent patient safety regulations minimizing medication errors, and the shift toward home-based care services enabling ambulatory infusion adoption.

2. Which countries dominate the Europe Advanced Infusion Systems Market share?

Germany commands the largest share of the Europe Advanced Infusion Systems Market, accounting for approximately 28.6% of regional revenue in 2024, attributed to its advanced healthcare infrastructure, early adoption of smart infusion devices, and strong medical technology manufacturing sector. The United Kingdom, France, Italy, and Spain also represent significant market contributors, with the UK witnessing notable growth due to its well-established healthcare framework, increasing diabetes prevalence, and expanding geriatric population requiring sophisticated infusion therapy solutions.

3. What types of advanced infusion systems are most commonly used in the Europe Advanced Infusion Systems Market?

The Europe Advanced Infusion Systems Market encompasses several device categories including volumetric infusion pumps for delivering large fluid volumes used in hydration and blood transfusions, syringe infusion pumps for precise small-dose medication administration particularly in pediatric and neonatal care. Additionally, ambulatory infusion pumps provide portable medication delivery allowing patient mobility, while patient-controlled analgesia (PCA) pumps enable self-administered pain management under preset safety parameters, and smart infusion systems integrate wireless connectivity with electronic health records to minimize programming errors.

4. How are smart infusion pumps transforming the Europe Advanced Infusion Systems Market landscape?

Smart infusion pumps are revolutionizing the Europe Advanced Infusion Systems Market by integrating advanced digital technologies including wireless connectivity, real-time patient monitoring, drug library databases with standardized dosing limits, and closed-loop feedback mechanisms. These intelligent devices connect wirelessly with electronic health records (EHRs) to receive medication orders directly, eliminating error-prone manual programming steps and significantly reducing intravenous medication administration errors while enhancing patient safety through programmable alerts and continuous monitoring capabilities that support precision medicine approaches in critical care and oncology settings.

5. What role does EHR interoperability play in the Europe Advanced Infusion Systems Market adoption?

Electronic health record interoperability represents a transformative advancement in the Europe Advanced Infusion Systems Market, enabling smart infusion pumps to wirelessly connect with hospital information systems to receive medication orders automatically. This technological integration eliminates manual data entry errors, ensures accurate dosing through standardized drug libraries, facilitates real-time documentation and monitoring, and supports healthcare digitization initiatives across European hospitals focused on value-based care and patient-centric treatment models that prioritize medication safety and workflow efficiency.

6. What therapeutic applications drive demand in the Europe Advanced Infusion Systems Market?

The Europe Advanced Infusion Systems Market serves diverse therapeutic applications including chemotherapy drug administration for cancer treatment, insulin delivery for diabetes management, pain management through patient-controlled analgesia, antibiotic infusion for infection control, and nutritional therapy for malnourished patients. Critical care settings utilize advanced infusion systems for cardiovascular medication delivery, while home healthcare services increasingly adopt ambulatory infusion devices for chronic disease management, reflecting the market's versatility across inpatient hospital environments, outpatient clinics, and residential care settings throughout Europe.

7. How does the aging population impact the Europe Advanced Infusion Systems Market demand?

The rapidly expanding geriatric population significantly influences the Europe Advanced Infusion Systems Market as elderly individuals demonstrate higher susceptibility to chronic diseases including cancer, diabetes, cardiovascular disorders, and neurological conditions requiring long-term intravenous therapy. This demographic shift creates sustained demand for both hospital-based infusion equipment and portable ambulatory systems enabling home healthcare delivery, while also driving innovation in user-friendly interfaces and safety features tailored to geriatric patient needs across Germany, the United Kingdom, France, Italy, and other European nations with aging demographics.

8. What regulatory factors influence the Europe Advanced Infusion Systems Market development?

The Europe Advanced Infusion Systems Market operates under stringent medical device regulations ensuring high-quality standards, patient safety protocols, and rigorous clinical validation requirements before product approval. These comprehensive regulatory frameworks mandate compliance with European Union medical device directives, post-market surveillance systems, adverse event reporting mechanisms, and adherence to international safety standards, which collectively promote adoption of technologically advanced and clinically validated infusion devices while maintaining patient protection as the paramount priority across all European healthcare settings.

9. How do reimbursement policies affect the Europe Advanced Infusion Systems Market growth?

Favorable reimbursement policies substantially accelerate the Europe Advanced Infusion Systems Market expansion by ensuring healthcare providers receive adequate compensation for advanced infusion therapy services and equipment investments. Supportive insurance coverage frameworks across Germany's universal healthcare model, the United Kingdom's National Health Service, and France's social security system facilitate hospital procurement of smart infusion technologies and enable patient access to home-based infusion care, thereby reducing financial barriers to adoption of next-generation programmable and wearable infusion solutions that enhance treatment outcomes and patient quality of life.

10. What challenges constrain the Europe Advanced Infusion Systems Market expansion?

The Europe Advanced Infusion Systems Market faces several growth constraints including the availability of alternative drug delivery methods such as oral medications and transdermal patches, shortage of trained healthcare professionals skilled in operating sophisticated infusion technologies. Additional barriers encompass high initial equipment costs for smart infusion systems, complex integration requirements with existing hospital information technology infrastructure, stringent regulatory approval timelines delaying product launches, and varying tariff policies across European countries that create market access challenges for manufacturers seeking pan-European distribution.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com