Europe Aerostat Systems Market Size, Share, Trends, & Growth Forecast Report, Segmented By Application (Defense, Environmental Monitoring, Infrastructure Protecting, Traffic Monitoring, Sport, Educational, Live shows and music, Entertainment, and Others), Product Type, Class, Component, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Aerostat Systems Market Size

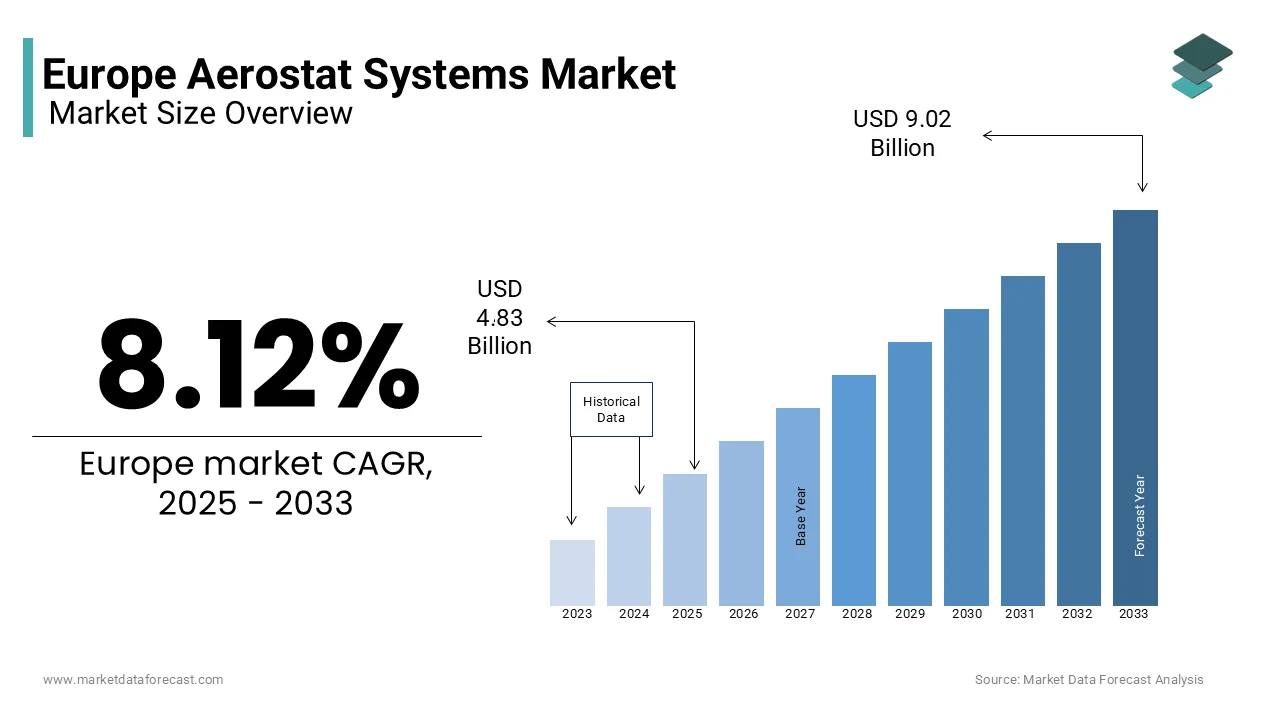

The Europe aerostat systems market was size was valued USD 4.83 billion in 2025 and is anticipated to reach USD 5.22 billion in 2026 to reach USD 9.75 billion by 2034, growing at a CAGR of 8.12% from 2026 to 2034.

An aerostat system is a persistent, lighter-than-air (LTA) aerial platform that stays aloft using the buoyancy of a lifting gas (typically helium) rather than aerodynamic wings or rotors. These systems provide persistent aerial presence at altitudes ranging from 300 to 5000 meters, offering a cost-effective alternative to manned aircraft and satellites for border security, disaster management, and telecommunications. The operational landscape in Europe is distinct due to the continent's extensive land borders and the stringent regulatory environment governed by the European Union Aviation Safety Agency. According to Frontex data, the external land borders of the European Union stretch approximately 9,600 kilometers, while the external sea borders cover roughly 44,000 kilometers. This combined 53,000+ kilometer perimeter creates a massive logistical challenge for continuous monitoring that traditional patrol methods cannot efficiently cover. Furthermore, the European Commission's "State of the Digital Decade" report indicates that 55% of rural households in member states are still not served by any advanced network (VHCN), driving interest in aerostats as high-altitude platform stations to bridge the persistent connectivity gap. The proliferation of cross-border security threats and the need for rapid response during natural disasters have intensified the demand for these stationary airborne assets. Unlike unmanned aerial vehicles with limited flight endurance, aerostats can remain aloft for weeks or even months, providing uninterrupted data streams. This capability transforms them into critical infrastructure for national security and digital inclusion, aligning with the strategic autonomy goals of the European Union while adhering to strict airspace management protocols.

KEY MARKET DRIVERS

Escalating Demand for Persistent Border Surveillance and Security

The intensifying need for continuous and cost-effective border surveillance accelerates the growth of the Europe aerostat systems market. Traditional manned patrols and rotating drone flights often result in coverage gaps and exorbitant operational costs, whereas tethered aerostats provide unwavering eyes-in-the-sky capabilities for extended durations. According to the European Border and Coast Guard Agency (Frontex), illegal border crossing detections decreased by approximately 38% in 2024 compared to the previous year, although specific routes like the Western African route saw varying increases, prompting governments to adapt monitoring strategies for shifting migration patterns. Aerostats equipped with electro-optical and infrared sensors can detect movement day and night over vast stretches of difficult terrain such as mountains and dense forests. Research indicates that the operational cost per flight hour for an aerostat system is approximately 80 to 90% lower than that of a manned helicopter, making it a cost-efficient alternative for persistent, 24/7 aerial surveillance. The ability to integrate these platforms with ground-based radar and command centers allows for real-time situational awareness, which is crucial for intercepting unauthorized entries. Furthermore, the rising geopolitical tensions in Eastern Europe have accelerated the deployment of these systems for early warning and force protection. This strategic imperative to secure national frontiers without exhausting military budgets drives sustained investment in advanced aerostat technologies.

Critical Need for Rapid Deployment Communication Relays in Disaster Zones

The growing frequency of extreme weather events and natural disasters in the region encourages the utilization of these systems as emergency communication hubs, which further escalates the expansion of the Europe aerostat systems market. When terrestrial infrastructure fails due to floods, earthquakes, or storms, aerostats can be rapidly deployed to restore vital communication links for first responders and affected populations. As per sources, economic damages from extreme weather events across Europe are escalating rapidly, with recent years consistently ranking among the costliest on record due to intensified flooding and storms. These tethered platforms can carry cellular base stations and radio repeaters to altitudes where line-of-sight coverage is maximized, effectively bridging the gap until permanent infrastructure is repaired. The European Commission's Civil Protection Mechanism has increasingly recognized the value of high-altitude platforms for coordinating relief efforts in isolated regions. Studies by the Joint Research Centre (JRC) and the Copernicus Emergency Management Service have highlighted that utilizing satellite mapping and unmanned systems can significantly improve situational awareness and response speeds during flood scenarios (such as the 2024 Central Europe floods), though specific metrics on aerostat communication restoration vary by deployment. Their ability to hover precisely over disaster zones without requiring runways or complex launch facilities makes them indispensable for humanitarian missions. The shift toward proactive disaster preparedness strategies ensures that government agencies and emergency services prioritize the acquisition of these versatile airborne assets.

KEY MARKET RESTRAINTS

Stringent Airspace Regulations and Certification Complexities

The rigorous airspace regulations and complex certification processes imposed by European aviation authorities pose a significant restraint on the widespread deployment of these systems and on the Europe aerostat systems market. Operating tethered balloons in shared airspace requires meticulous coordination to avoid conflicts with commercial aviation, general aviation, and other unmanned aircraft, leading to lengthy approval timelines. As per the European Union Aviation Safety Agency, obtaining operational authorization for beyond visual line of sight flights involving tethered assets involves a multi-layered risk assessment that can delay projects by several months. The lack of harmonized rules across different member states further complicates cross-border operations, forcing manufacturers to navigate a fragmented regulatory landscape. According to multiple studies, the integration of non-traditional aerial assets into existing European air traffic systems remains a significant technical hurdle, often resulting in localized coordination challenges between operators and air traffic control units. The requirement for specific lighting, transponders, and fail-safe mechanisms adds to the technical and financial burden on operators. In addition, restrictions on flight heights in urban areas limit the potential applications for smart city monitoring and telecommunications. A unified and streamlined regulatory framework is not yet established specifically for lighter-than-air systems. Consequently, these bureaucratic hurdles will continue to hinder market expansion and innovation.

Vulnerability to Adverse Weather Conditions and Operational Limitations

The inherent vulnerability of aerostat systems to severe weather conditions acts as a critical brake on their reliability and operational uptime in various European regions, which negatively impacts the expansion of the Europe aerostat systems market. High winds, heavy precipitation, and lightning strikes pose significant risks to tethered platforms, often necessitating grounding procedures that disrupt continuous mission profiles. As per sources, climate change is altering the predictability and intensity of weather patterns across Europe, with extreme heat and rainfall currently presenting a more measurable increase in frequency than wind-based extremes for the 2024 period. Strong gusts can cause tether instability or structural damage, while ice accumulation on the envelope can alter buoyancy and compromise flight safety. The operational ceiling for many aerostat models is strictly limited during adverse weather, reducing their effectiveness precisely when monitoring capabilities are most needed during storms. According to a study, airborne surveillance platforms operating in temperate zones must account for significant seasonal variability, as high-wind and icing conditions remain the primary limiting factors for maintaining continuous aerial coverage. The need for robust mooring systems and weather-hardened designs increases the initial capital expenditure and maintenance costs. This susceptibility to environmental factors creates hesitation among potential adopters who require guaranteed uptime for critical security and communication missions, thereby restraining market growth.

KEY MARKET OPPORTUNITIES

Integration of 5G and Beyond for High Altitude Platform Stations

The integration of aerostat systems with fifth-generation and future wireless networks opens up major possibilities for the Europe aerostat systems market. This approach addresses connectivity gaps in remote and rural areas. These platforms can serve as High Altitude Platform Stations that beam high-speed internet directly to underserved communities, bypassing the need for expensive terrestrial infrastructure rollout. European digital policy is aggressively targeting universal gigabit coverage by 2030, with rural areas remaining the primary focus for new infrastructure investments and alternative delivery technologies. Aerostats offer a flexible and scalable alternative to satellites with lower latency and higher bandwidth capacity for localized coverage. The European Commission's Connectivity Toolbox explicitly identifies high-altitude platforms as a key technology for achieving the Digital Decade targets by 2030. Temporary aerial base stations are increasingly being tested as a viable alternative to permanent tower construction in geographically challenging areas where traditional infrastructure deployment is economically prohibitive. The ability to reposition these assets dynamically allows operators to provide temporary capacity boosts during large events or emergencies. This convergence of telecommunications policy and aerospace technology opens new revenue streams for manufacturers and service providers alike.

Expansion of Environmental Monitoring and Climate Research Applications

The burgeoning focus on climate change mitigation and environmental protection offers a substantial prospect for the deployment of aerostat systems in scientific research and pollution monitoring, which is expected to boost the expansion of the Europe aerostat systems market. These platforms provide stable, long-duration vantage points for collecting atmospheric data, tracking greenhouse gas emissions, and monitoring deforestation or illegal dumping activities. Stricter European emission standards are forcing member states to adopt more granular monitoring techniques, leading to a significant increase in the use of high-resolution sensors and satellite-based tracking for methane leaks. Aerostats can carry sophisticated spectrometers and lidar sensors to altitudes inaccessible to drones for extended periods, enabling comprehensive vertical profiling of the atmosphere. The European Space Agency has increasingly collaborated with aerostat manufacturers to validate satellite data and calibrate remote sensing instruments. Advanced aerostat platforms are proving more effective than short-endurance aircraft for atmospheric research because they can hover at fixed altitudes for extended periods, providing much higher temporal resolution for weather and pollution data. The push for green deal initiatives and carbon neutrality drives public funding for projects that utilize these systems for precise environmental auditing. This alignment with sustainability goals positions aerostats as essential tools for the next generation of ecological stewardship in Europe.

KEY MARKET CHALLENGES

Technical Complexity of Mooring and Station Keeping in Urban Environments

The technical complexity associated with mooring and maintaining station keeping in densely populated urban environments is a persistent challenge for the Europe aerostat systems market. Deploying large tethered platforms in cities requires sophisticated anchoring solutions that minimize ground footprint while ensuring stability against turbulent wind flows caused by skyscrapers and urban canyons. The intricate architecture of modern cities creates complex micro-scale meteorological phenomena that significantly challenge the flight stability of persistent aerial platforms, requiring sophisticated real-time tension and ballast management. The logistical difficulty of transporting and assembling large envelopes in confined spaces further complicates deployment logistics. Implementing persistent aerial systems in dense urban settings is hindered by the physical difficulty of securing stable mooring sites and the logistical complexity of integrating these platforms into crowded city-level airspace. Besides, the visual impact and noise generated by winch operations can lead to public opposition and zoning restrictions. Developing compact, automated, and silent mooring stations that can operate safely amidst pedestrian traffic and existing infrastructure requires significant engineering innovation. Technical hurdles must be overcome with reliable and unobtrusive solutions. Otherwise, the penetration of aerostat systems into smart city applications will remain limited.

High Initial Capital Expenditure and Maintenance Cost Barriers

The substantial initial capital expenditure required for acquiring advanced aerostat systems, coupled with ongoing maintenance costs, poses a severe barrier to the Europe aerostat systems market. This is particularly true for smaller nations and private entities. High-end systems equipped with multi-sensor payloads, redundant power supplies, and reinforced envelopes involve significant upfront investment that strains public budgets and corporate balance sheets. The high entry price for advanced persistent surveillance technology remains a significant barrier for local security agencies, often limiting the adoption of high-altitude systems to national defense or large-scale border initiatives. Furthermore, the specialized nature of these assets necessitates regular inspection of the envelope material, tether integrity, and helium purity, leading to recurring operational expenses. The shortage of skilled technicians capable of maintaining these complex systems in Europe exacerbates the cost burden. The ongoing operational expenses associated with gas replenishment, sensor calibration, and structural upkeep represent a major portion of the total ownership cost, often influencing the long-term feasibility of persistent aerial monitoring programs. The economic uncertainty and competing fiscal priorities in the post-pandemic era make it difficult for stakeholders to justify such large capital outlays without guaranteed returns. This financial barrier restricts market growth to only the wealthiest government clients and limits the diversification of the user base.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 8.12% |

| Segments Covered | By Application, Product Type, Class, Component, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | CNIM, A-NSE, TCOM, L.P., Raven Industries, Inc., Carolina Unmanned Vehicles Inc., HEMERIA, ILC Dover LP, Altaeros, Aeronord SAS, and ALLSOPP HELIKITES LTD. |

SEGMENTAL ANALYSIS

By Application Insights

The defense segment dominated the Europe aerostat systems market and accounted for a 48.4% share in 2025. The dominance of the segment is primarily driven by the urgent requirement for persistent surveillance along the continent's extensive and often porous borders to counter illegal migration and cross-border threats. Apart from these, a key factor is the strategic shift toward cost-effective force multiplication where aerostats provide continuous coverage that manned aircraft cannot sustain due to fuel constraints and crew fatigue. As per the European Border and Coast Guard Agency (Frontex), total detections of unauthorized border crossings decreased by approximately 38% in 2024 (falling to ~239,000), although specific routes such as the Western African route saw an increase of 18%. This mixed threat landscape has prompted member states to maintain persistent surveillance. Furthermore, the geopolitical instability in Eastern Europe has accelerated defense spending on early warning systems and force protection assets that can operate for weeks without landing. According to multiple studies, the operational cost per hour for tethered aerostat systems is estimated to be significantly lower than that of traditional manned helicopters (often cited as ~10–20% of the cost), making them an economically viable solution for long-endurance, 24/7 border monitoring missions. The ability to integrate these platforms with existing command and control networks allows for real-time intelligence sharing across NATO allies. This combination of fiscal efficiency, operational endurance, and heightened security concerns solidifies the defense sector as the primary revenue generator in the market.

The environmental monitoring segment is estimated to register the fastest CAGR of 16.8% during the forecast period due to the stringent regulatory frameworks established under the European Green Deal which mandate precise and continuous tracking of air quality, greenhouse gas emissions, and industrial pollutants. A major driving factor is the unique capability of aerostats to carry heavy spectral sensors to specific altitudes for extended durations, enabling vertical profiling of the atmosphere that drones and satellites cannot achieve with the same resolution or persistence. As per the European Environment Agency (EEA), while EU methane emissions have fallen by 38% since 1990, atmospheric concentrations continue to rise, driving the enforcement of the new EU Methane Regulation in 2024 to improve measurement and reporting. Furthermore, the increasing frequency of climate-related disasters such as floods and wildfires necessitates rapid deployment of airborne observation posts to assess damage and coordinate relief efforts. According to reports supporting the European Commission (including JRC input), satellite-based monitoring (via Copernicus Sentinel-5P) remains the primary tool for detecting large methane leaks, offering global coverage that surpasses the localized capabilities of ground-based or short-endurance aerial campaigns. The shift toward proactive ecological stewardship and the need for verified emission data drives public and private investment in these specialized airborne platforms, propelling the segment to outpace all others in growth velocity.

By Product Insights

The balloon segment led the Europe aerostat systems market and captured a 56.5% share in 2025. This leading position of the segment is attributed to the inherent simplicity, lower manufacturing costs, and superior station-keeping capabilities of tethered balloons compared to more complex airship designs. An additional factor sustaining this dominance is the widespread adoption of balloon systems for static surveillance and communication relay missions where mobility is secondary to persistence and stability. As per various sources, ethered balloons are increasingly favoured for maritime and land border "persistence" because they can stay aloft for weeks at a significantly lower cost than fuel-heavy patrol aircraft. Furthermore, the modular design of modern balloons allows for rapid deployment and easy maintenance, which is crucial for military and emergency response operations requiring quick setup times. European nations are diversifying their defense spending to include lower-cost, high-endurance surveillance tools as a response to the high operational costs of traditional aerial assets. The proven track record of balloon technology in harsh weather conditions and its compatibility with a wide range of sensor payloads ensures its continued preference among end users. This blend of economic efficiency, operational reliability, and technological maturity secures the balloon segment as the market leader.

The hybrid segment is anticipated to witness the fastest CAGR of 15.4% over the forecast period owing to the innovative combination of aerodynamic lift and buoyant gas which enables these systems to carry heavier payloads and operate in higher wind speeds than traditional balloons. A significant driving factor is the rising demand for mobile yet persistent platforms capable of performing complex missions such as cargo transport, large-scale telecommunications, and dynamic surveillance in challenging environments. As per research, European aerospace research is heavily focused on decarbonisation, leading to selective investment in hybrid platforms that promise significantly lower emissions for heavy-lift logistics. Additionally, the ability of hybrid systems to take off and land vertically without extensive ground infrastructure makes them ideal for operations in rugged terrains and urban settings where runways are unavailable. Hybrid aerial platforms are being positioned as the middle ground between heavy-lift transport and small drones, capable of carrying large medical or relief supplies to regions where traditional runways are unavailable. The versatility to switch between hovering and forward flight opens new application avenues in civil and commercial sectors. This convergence of advanced engineering, operational flexibility, and expanding use cases drives the exceptional growth trajectory of the hybrid segment.

By Component Insights

The payload segment held the majority share of 32.7% of the Europe aerostat systems market in 2025. This supremacy of the segment is credited to the critical importance of advanced sensors, cameras, and communication equipment that define the operational utility and mission success of any aerostat platform. The main factor supporting this leadership is the escalating demand for high-resolution electro-optical, infrared, and radar systems capable of detecting minute details over vast distances for security and scientific applications. As per multiple studies, environmental monitoring is increasingly leveraging high-resolution imaging sensors on tethered platforms to provide persistent, localized data that complements broad-scale satellite observations. Furthermore, the trend toward multi-mission flexibility requires payloads that can be rapidly swapped or upgraded, driving recurring sales of specialized modules for different operational scenarios. According to research, modern defense procurement prioritizes modular sensor suites that allow for rapid technological refreshes, ensuring that long-endurance platforms remain capable against evolving threats without replacing the entire airframe. The continuous advancement in miniaturization and processing power allows for heavier and more capable instrument suites to be lifted, further boosting segment revenue. This reliance on cutting-edge technology to extract actionable intelligence ensures that payloads remain the most valuable component in the market ecosystem.

The communication systems segment is likely to experience the fastest CAGR of 17.2% from 2026 to 2034. This rapid expansion is fueled by the urgent need to deploy High Altitude Platform Stations that can provide broadband connectivity to remote rural areas and serve as emergency communication hubs during disasters. A major driving factor is the European Union's Digital Decade initiative which aims to ensure gigabit connectivity for all citizens by 2030, creating a massive market for airborne 5G and beyond networks. As per a study, European regulators are focusing on "full connectivity" targets for 2030, encouraging the use of non-terrestrial networks like aerostats and satellites to reach the final percentage of the population in topographically challenging areas. Additionally, the ability of these systems to act as resilient nodes in tactical military networks ensures secure and jam-resistant communications in contested environments. According to sources, tethered aerial platforms are being utilized as flexible, low-cost "cells-on-wings" to provide 5G coverage in extreme terrain where traditional tower construction is physically or economically unfeasible. The shift toward software-defined radios and adaptive beamforming technologies further enhances the capability and appeal of these systems. This convergence of digital inclusion goals and tactical communication needs propels the communication systems segment to outpace other components in growth velocity.

COUNTRY ANALYSIS

United Kingdom Aerostat Systems Market Analysis

The United Kingdom was the top performer in the Europe aerostat systems market and accounted for a 22.8% share in 2025. The dominance of the UK market is driven by the extensive coastline and overseas territories of the UK which require persistent monitoring capabilities that aerostats uniquely provide for detecting smuggling and unauthorized entries. The nation serves as a hub for aerospace innovation and defense technology, driven by a robust industrial base and strong government commitment to border security and maritime surveillance. As per sources, the United Kingdom is pivotally shifting its defense strategy toward uncrewed and autonomous aerial systems to secure maritime corridors, prioritizing long-range drone technology over traditional lighter-than-air platforms. Furthermore, the presence of leading aerospace manufacturers and research institutions fosters a vibrant ecosystem for developing next-generation hybrid airships and advanced sensor payloads. According to studies, british aerospace funding is increasingly directed toward decarbonisation and green aviation technologies, fostering public-private partnerships that aim to modernize the national industrial base for sustainable flight. The strategic focus on achieving net-zero emissions also drives interest in hybrid aerostats for low-carbon cargo transport to remote islands. This confluence of security imperatives, industrial strength, and sustainability goals ensures the United Kingdom remains the dominant force in the European landscape.

Germany Aerostat Systems Market Analysis

Germany followed closely behind the Europe aerostat systems market and captured a 19.9% share in 2025. The growth of the German market is supported by the rigorous implementation of the European Green Deal which compels German industries to adopt precise air quality monitoring solutions that aerostats can deliver with unmatched persistence. The market status in Germany is defined by its world-class engineering prowess and a strong emphasis on applying aerostat technology for environmental protection and industrial monitoring. As per research, Germany is integrating advanced remote sensing tools into its industrial sector to meet climate neutrality goals, utilizing various aerial platforms to monitor and mitigate carbon emissions at a granular level. Additionally, the country's central location in Europe makes it a strategic testing ground for cross-border security initiatives and disaster response coordination using tethered platforms. Research in Germany is focusing on the automation of ground infrastructure to support the integration of autonomous flight systems into complex, high-density urban environments. The strong automotive and logistics sectors also explore hybrid airships for sustainable freight transport, adding a commercial dimension to the market. This blend of regulatory pressure, technical excellence, and diverse application potential drives Germany's significant standing.

France Aerostat Systems Market Analysis

France maintained a significant position in the Europe aerostat systems market due to its ambitious national defense strategy and leadership in satellite and aerospace technologies. The market status in France is characterized by a strong push for strategic autonomy in surveillance and communication capabilities, reducing reliance on non-European suppliers. A key driving factor is the extensive land and maritime borders of France including overseas departments which necessitate versatile and long-endurance monitoring assets for sovereignty protection. France is modernizing its border and force protection by incorporating persistent surveillance assets into its broader military ecosystem, emphasizing tools that provide continuous situational awareness against hybrid threats. Furthermore, the French space agency CNES actively collaborates with aerostat manufacturers to validate atmospheric data and test new sensor technologies for future space missions. The French government is actively supporting sovereign aerospace innovation, providing significant financial backing to develop next-generation aerial vehicles that can serve both civilian and military logistics. The growing interest in using aerostats for telecommunications in remote rural areas and during major international events further boosts demand. This synergy of defense priorities, space expertise, and digital inclusion initiatives solidifies France as a critical market node.

Italy Aerostat Systems Market Analysis

Italy grew steadily in the Europe aerostat systems market owing to the critical need for persistent maritime surveillance to monitor migrant flows and combat human trafficking, roles for which aerostats offer a cost-effective and enduring solution. The market dynamics in Italy are heavily influenced by its geographical exposure to migration routes across the Mediterranean and its rich heritage in aeronautical engineering. Italy is leveraging its strategic Mediterranean position to expand its maritime surveillance network, increasingly utilizing tethered platforms to monitor migratory flows and enhance early warning capabilities along its coastline. Additionally, Italy's vulnerability to natural disasters such as earthquakes and floods drives the adoption of aerostats for rapid communication restoration and damage assessment. Italian scientific agencies are expanding the use of high-altitude assets to provide specialized data for disaster prevention and the study of atmospheric phenomena in geographically sensitive areas. The presence of skilled manufacturers capable of producing high-quality envelopes and mooring systems supports a robust domestic supply chain. This fusion of geographic necessity, disaster resilience requirements, and industrial capability propels Italy's growth in the market.

Sweden Aerostat Systems Market Analysis

Sweden is predicted to expand notably in the Europe aerostat systems market during the forecast period due to the need for efficient surveillance of sparse populations and critical infrastructure over immense territories where traditional patrols are logistically difficult and expensive. The country serves as a leader in northern European defense and environmental research, distinguished by its unique challenges related to vast forested areas and Arctic conditions. Following its entry into NATO, Sweden is rapidly upgrading its coastal and border monitoring infrastructure, focusing on unmanned systems that provide a comprehensive operational picture of the Baltic region. Furthermore, Sweden's commitment to climate science drives the use of aerostats for collecting detailed atmospheric data in the Arctic, a region experiencing rapid environmental changes. Environmental research in Sweden is trending toward the use of specialized tethered platforms to capture high-resolution data on air pollutants, allowing for more precise tracking of transboundary environmental impacts. The strong local tech ecosystem supports the development of automated and weather-hardened systems capable of operating in extreme cold. This combination of strategic geography, scientific ambition, and technological innovation establishes Sweden as a key growth engine in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe aerostat systems market is characterized by a specialized rivalry between established aerospace giants and agile niche manufacturers who compete on technological sophistication and mission reliability. Large multinational corporations leverage their extensive resources and broad defense portfolios to offer integrated turnkey solutions while smaller firms differentiate themselves through custom engineering and rapid prototyping capabilities tailored to unique client requirements. The battleground has shifted toward the development of hybrid systems that can operate safely in higher wind speeds and carry heavier sensor loads for longer durations than traditional tethered balloons. Regulatory compliance and airspace integration remain critical differentiators where vendors must demonstrate adherence to strict European aviation safety standards to win government contracts. Strategic alliances with local suppliers and research centers become essential for navigating complex procurement processes and fostering innovation in material science. Customers increasingly demand autonomous operation features and seamless data integration with existing command networks which forces competitors to constantly evolve their software and control algorithms. The market sees frequent collaborative projects as companies join forces to share the high costs of developing next generation platforms capable of meeting the dual demands of defense security and climate monitoring in a rapidly changing geopolitical landscape.

KEY MARKET PLAYERS

A few of the market players in the Europe aerostat systems market include

- CNIM, A-NSE

- TCOM, L.P.

- Raven Industries, Inc

- Carolina Unmanned Vehicles Inc.

- HEMERIA

- ILC Dover LP

- Altaeros

- Aeronord Sas

- ALLSOPP HELIKITES LTD.

Top Players In The Market

- Airbus SE stands as a global aerospace leader with a significant footprint in the Europe aerostat systems market through its innovative hybrid airship and high altitude platform projects. The company contributes globally by advancing sustainable aviation technologies and developing versatile lighter than air vehicles for cargo transport and persistent surveillance. Recently Airbus strengthened its European position by collaborating with defense ministries to prototype next generation hybrid aerostats capable of operating in extreme weather conditions for extended durations. The firm actively invests in research partnerships with universities to refine buoyancy control systems and automated mooring technologies essential for urban deployment. Airbus continues to leverage its extensive supply chain and engineering expertise to reduce manufacturing costs while enhancing payload capacities for military and civil applications. Their strategic focus on decarbonizing logistics drives the development of helium fueled freighters that offer low emission alternatives to traditional aircraft. This commitment to innovation and sustainability solidifies their reputation as a premier provider of advanced aerial solutions worldwide.

- Thales Group operates as a key technology provider in the Europe aerostat systems market specializing in sophisticated payloads and command control integration for tethered platforms. Its global contribution lies in delivering state of the art radar communication and electro optical sensors that enable real time situational awareness for border security and disaster management. To strengthen its market position in Europe Thales recently secured contracts to equip national border agencies with integrated aerostat surveillance networks featuring advanced data fusion capabilities. The company has also expanded its portfolio to include modular payload bays that allow rapid reconfiguration for diverse mission profiles ranging from signals intelligence to environmental monitoring. Thales frequently collaborates with European defense contractors to ensure seamless interoperability of aerostat data within broader network centric warfare architectures. By focusing on cybersecurity and resilient communications Thales empowers operators to maintain reliable links even in contested electromagnetic environments. Their dedication to technological excellence and system integration drives loyalty among government clients seeking robust and scalable airborne solutions.

- RosAeroSystems distinguishes itself in the Europe aerostat systems market through its extensive experience in designing and manufacturing large scale tethered balloons and airships for both civilian and military use. The company contributes globally by supplying durable and cost effective platforms that serve critical roles in atmospheric research telecommunications and regional surveillance. Recent actions to bolster its market presence include the deployment of new augmented reality training simulators for aerostat operators and the introduction of reinforced envelope materials designed to withstand harsh northern climates. RosAeroSystems has also partnered with meteorological institutes to launch long duration observation campaigns that validate climate models using data collected from high altitude stations. The firm actively engages in international exhibitions to showcase its latest hybrid designs that combine the endurance of balloons with the maneuverability of powered airships. RosAeroSystems maintains a strong reputation for delivering mission-critical assets by prioritizing reliability and operational simplicity. These assets perform consistently in remote and challenging environments across the continent.

Top Strategies Used By Key Market Participants

Key players in the Europe aerostat systems market primarily employ strategic partnerships with government defense agencies and research institutions to co develop specialized platforms tailored for specific national security and environmental monitoring needs. Companies frequently invest in research and development to create hybrid designs that combine buoyant lift with aerodynamic propulsion thereby enhancing payload capacity and operational flexibility in adverse weather conditions. Product innovation remains a central strategy where vendors continuously integrate advanced sensor suites and artificial intelligence driven analytics to improve target detection and data processing capabilities. Market participants also focus on expanding service offerings by providing comprehensive maintenance training and lifecycle support packages to ensure high availability and customer retention. Acquiring niche technology startups allows larger firms to rapidly incorporate cutting edge materials and autonomous control systems into their existing product lines. Developing modular payload architectures enables clients to swap equipment quickly for different missions which increases the versatility and value proposition of the systems. Offering flexible financing models helps overcome high initial capital barriers for public sector buyers facing budget constraints.

MARKET SEGMENTATION

This research report on the Europe aerostat systems market is segmented and sub-segmented into the following categories.

By Application

- Defense

- Environmental Monitoring

- Infrastructure Protecting

- Traffic Monitoring

- Sport

- Educational

- Live shows and music

- Entertainment

- Others

By Product Type

- Balloon

- Airship

- Hybrid

By Class

- Large

- Medium

- Compact

By Component

- Envelope/Bladder

- Tether

- Payload

- Payload Platform

- Communication Systems

- Ground Control Station

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are aerostat systems used for in Europe?

Aerostat systems in Europe are primarily used for surveillance, border security, intelligence gathering, communication relay, and weather monitoring.

What are the primary drivers of growth in the European aerostat systems market?

Growth is driven by increasing defense budgets, rising border security concerns, demand for cost-effective surveillance, and advancements in aerostat technology.

What technological advancements are shaping the European aerostat market?

Advances include improved payload capacity, better weather-resistant materials, enhanced radar and sensor integration, and automated operation capabilities.

What is the future outlook for the aerostat systems market in Europe?

The market is expected to see steady growth, driven by increasing security needs, advancements in lightweight materials, and greater adoption for civil and military applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com