Europe Airborne Wind Turbine Market Size, Share, Trends & Growth Forecast Report – Segmented By Turbine Power (Small Turbine, Large Turbine), Application, And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Europe Airborne Wind Turbine Market Size

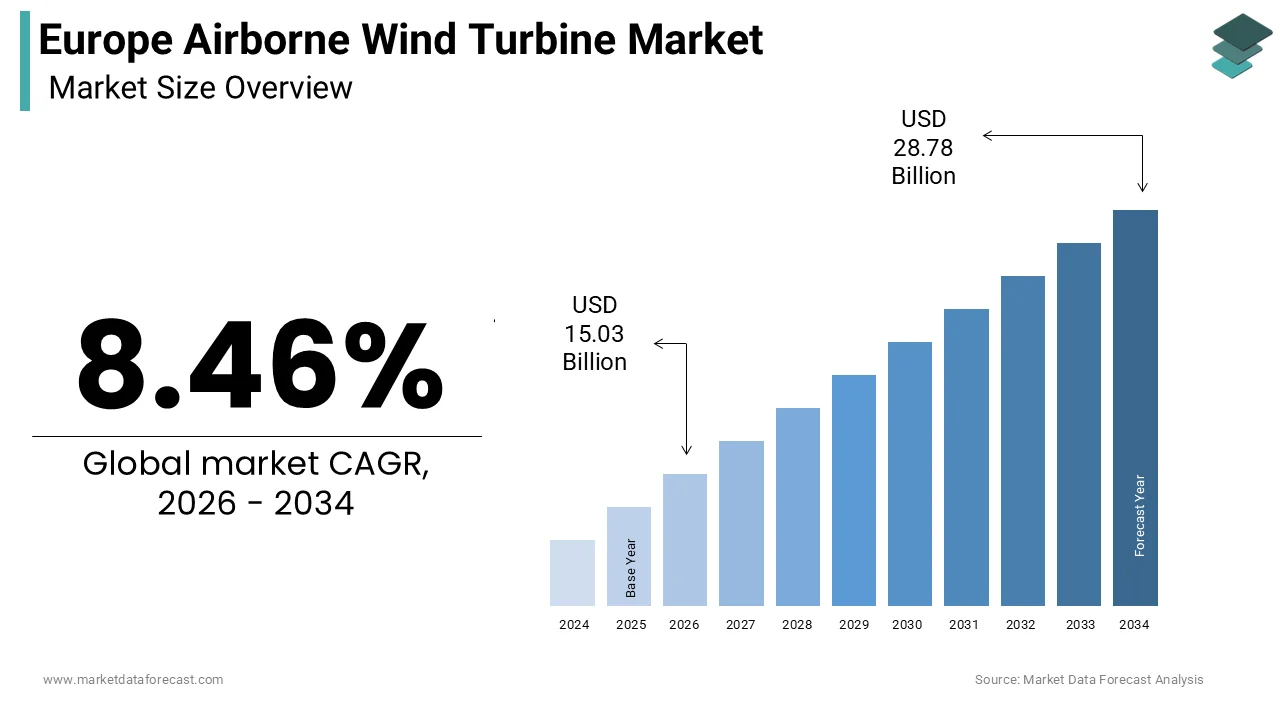

The Europe Airborne Wind Turbine market size was calculated at USD 13.86 billion in 2025 and is anticipated to reach USD 28.78 billion by 2034, from USD 15.03 billion in 2026, growing at a CAGR of 8.46% during the forecast period.

Airborne wind turbine technology represents a paradigm shift in renewable energy generation by harnessing high-altitude winds that remain largely untapped by conventional tower-based systems. These innovative devices operate at altitudes ranging from 200 to 600 meters, where wind speeds are significantly stronger and more consistent than those found near the ground surface. The European Union has demonstrated substantial commitment to advancing this sector through various research initiatives aimed at decarbonizing the energy landscape. According to the International Energy Agency, high-altitude wind resources hold the potential to supply a significant portion of global energy needs if fully exploited. As per the European Environment Agency, Europe possesses exceptional wind potential, particularly in coastal regions and elevated terrains where airborne systems can achieve high capacity factors compared to traditional installations. As per Eurostat data, renewable energy accounted for a substantial share of the European Union’s gross final energy consumption in recent years, creating fertile ground for disruptive technologies. According to the German Aerospace Center, airborne wind energy systems require significantly less material than conventional turbines, offering advantages in resource efficiency. This technological evolution aligns with the European Green Deal objectives, targeting climate neutrality by 205,0 while addressing land-use constraints and visual impact concerns associated with traditional wind farms.

MARKET DRIVERS

Escalating Demand for High-Capacity Factor Renewable Energy Sources

The imperative to maximize energy yield per installed capacity drives substantial interest in airborne wind turbine systems, which is one of the major factors driving the Europe airborne wind turbines market growth. Conventional wind turbines typically achieve capacity factors influenced by variable wind conditions at lower altitudes, whereas airborne systems operating at heights of 300 to 500 meters can consistently capture stronger winds. According to the European Wind Energy Association, wind resources above 200 meters contain higher kinetic energy than those available at standard hub heights. This superior resource availability enables airborne systems to achieve competitive capacity factors, as documented by technical assessments from various research institutions. According to the International Renewable Energy Agency, increasing capacity factors directly reduces the levelized cost of electricity, making airborne solutions increasingly competitive. According to federal studies, Germany has identified numerous suitable sites for high-altitude wind harvesting. Furthermore, according to the European Commission Joint Research Centre, optimizing capacity factors through altitude exploitation could significantly reduce the number of installations needed to meet identical energy targets. This efficiency gain addresses critical land-scarcity issues in densely populated European regions while maintaining grid stability through more predictable power output.

Stringent Material Efficiency and Circular Economy Compliance Requirements

European regulatory frameworks increasingly mandate sustainable manufacturing practices and minimal resource consumption, which is further contributing to the Europe airborne wind turbines market expansion. Traditional wind turbines demand large quantities of steel, concrete, and composite materials per megawatt of installed capacity, according to lifecycle assessments. In contrast, airborne wind systems utilize far less material per megawatt, representing a significant reduction in raw material requirements as confirmed by research from wind energy institutes. The European Circular Economy Action Plan establishes targets for material efficiency requiring manufacturers to minimize waste and extend product lifecycles, which inherently favors lightweight airborne designs. According to Eurostat, the European Union imports a high percentage of its critical raw materials, creating strategic vulnerabilities that airborne technology helps mitigate through reduced dependency. Research organizations demonstrate that airborne systems generate significantly less embodied carbon during manufacturing phases compared to tower-based equivalents. Additionally, reports suggest that the simplified structural design of airborne systems produces much lower amounts of non-recyclable composite waste compared to traditional wind farms.

MARKET RESTRAINTS

Complex Regulatory Approval Processes for Low-Altitude Airspace Utilization

Airborne wind turbine deployment faces significant regulatory hurdles stemming from overlapping jurisdictions governing aviation safety, telecommunications, and energy infrastructure across European nations, which is primarily hampering the regional market growth. The European Union Aviation Safety Agency mandates comprehensive risk assessments for any object operating above 150 meters, requiring extensive coordination with civil aviation authorities, military radar systems, and air traffic control networks. According to data from air navigation safety organizations, thousands of low-altitude flight operations occur daily across European airspace, creating complex integration challenges for tethered airborne energy systems. Each member state maintains distinct authorization procedures with lengthy approval timelines, as stated by wind energy industry associations. National regulatory agencies indicate that obtaining permits for experimental airborne installations requires compliance with diverse frameworks, including electromagnetic compatibility standards, noise emission limits, and visual impact assessments. Furthermore, telecommunications institutes emphasize potential interference concerns with existing infrastructure, necessitating additional technical certifications. Reports suggest that a limited number of submitted applications for high-altitude energy projects receive approval within the first year due to complex documentation and safety requirements. These bureaucratic complexities increase project development costs significantly, according to industry surveys.

Limited Grid Integration Infrastructure for Distributed High-Altitude Generation

The existing European electrical grid infrastructure remains predominantly designed for centralized power injection from large-scale conventional wind farms and thermal plants, which is further impeding the growth of the European market. According to transmission system operator networks, many transmission systems operate without the smart grid capabilities necessary to accommodate variable injection points from numerous small-scale airborne installations. According to the International Electrotechnical Commission, integrating airborne systems requires advanced power electronics capable of managing voltage fluctuations caused by dynamic tether movements, which current substations may not efficiently process. National ministries state that upgrading distribution networks to handle bidirectional power flows from distributed renewable sources requires substantial investments through 2030. According to the European Commission Joint Research Centre, airborne systems operating at varying altitudes produce power quality issues, including harmonic distortions that existing grid codes do not adequately address. Transmission operators indicate that connecting airborne installations in remote mountainous regions demands extensive new infrastructure construction. Furthermore, energy regulators state that current market mechanisms often fail to properly value the grid services provided by airborne systems.

MARKET OPPORTUNITIES

Expansion into Offshore and Remote Island Energy Independence Initiatives

European island communities and offshore installations present compelling opportunities for the Europe airborne wind turbines market. According to the European Commission, thousands of inhabited islands exist within European waters, many of which depend on imported fossil fuels for electricity generation. Official ministry reports state that island communities often spend significantly more on diesel-generated electricity compared to mainland grid power, creating strong economic incentives for alternative solutions. Airborne wind systems offer particular advantages in these locations due to their minimal foundation requirements and ability to withstand marine environments. Authorities indicate that offshore wind resources at altitudes above 200 meters contain high energy density, making airborne systems ideal for floating platform deployments. Oil and gas industry bodies estimate that decommissioned platforms could host airborne wind installations, reducing infrastructure costs by repurposing existing mooring systems. Clean energy initiatives document that replacing diesel generators with airborne wind systems could significantly reduce carbon emissions annually across island communities.

Integration with Hybrid Renewable Energy Storage Systems

The convergence of airborne wind technology with advanced energy storage solutions creates synergistic opportunities for the expaturbine the Europe airborne wind turbines market. For instance, hybrid systems combining airborne wind with battery storage achieve high round-trip efficiencies while maintaining stable capacity factors throughout operating cycles. Energy agencies state that coupling airborne systems with hydrogen electrolyzers enables the production of green hydrogen at competitive costs when operating at high capacity factors enabled by consistent high-altitude winds. Research centers demonstrate that integrated airborne wind and compressed air energy storage facilities can provide continuous power output, addressing intermittency concerns that plague conventional renewable sources. Hydrogen initiatives identify that airborne wind farms located in high-wind corridors could supply a notable portion of projected European green hydrogen demand. Renewable energy associations indicate that hybrid installations reduce balance-of-system costs through shared infrastructure, including grid connections and maintenance facilities. Research programs have allocated significant funding specifically for integrated airborne wind and storage technologies, recognizing their potential to transform renewable energy reliability.

MARKET CHALLENGES

Unpredictable Atmospheric Conditions Affecting Tether Dynamics and Control Systems

Airborne wind turbines face operational challenges stemming ,from complex atmospheric phenomena including turbulence, wind shear, and sudden gust events that compromise tether stability and control algorithm performance. According to meteorological forecasting centers, wind variability increases with altitude, experiencing higher turbulence intensities at operational heights than at levels where conventional turbines operate. Meteorological institutes document that extreme wind events occur with higher frequency at airborne operating altitudes, requiring robust emergency landing protocols and reinforced tether materials. Technical assessments reveal that cyclic loading from atmospheric turbulence reduces tether lifespan, necessitating frequent replacements. Research councils indicate thof at wind direction changes because control system oscillations that reduce energy capture efficiency during transitional periods. Scientific institutes state that ice accumulation on tethers during winter months increases weight, altering aerodynamic profiles and requiring heated cable systems that consume a portion of generated power. Space agency meteorological data shows that lightning strikes at operating altitudes occur frequently.

High Initial Capital Expenditure and Limited Financing Mechanisms

The substantial upfront investment requirements for airborne wind turbine development create financial barriers despite promising long-term operational economics and levelized cost advantages. For instance, prototype development and certification costs for airborne systems remain high, reflecting the nascent stage of technology maturation. Development banks state that a small percentage of renewable energy projects receiving financing involve airborne technologies due to perceived technology risks and the lack of proven track records. Venture capital funding for airborne wind startups represents a minor share of total renewable energy venture investments, according to market analysis. Development agencies indicate that insurance premiums for airborne installations are higher than conventional wind projects due to limited actuarial data on failure modes. Innovation funds state that airborne projects struggle to qualify for traditional power purchase agreements because off-takers, demand long operational histories which most developers cannot provide. Green investment banks state that debt financing costs for airborne projects remain elevated compared to established renewable technologies, reflecting lender risk perceptions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.46% |

| Segments Covered | By Turbine Power, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Kitepower B.V., SkySails Power GmbH, EnerKíte GmbH, Kitemill AS, Ampyx Power B.V., Windlift Inc., TwingTec AG, SkySails Group GmbH, KiteKRAFT GmbH, Makani Technologies LLC, Altaeros Energies Inc., eWind Solutions Inc., Kitekraft, Enerkite, Kitepower Europe B.V. |

SEGMENTAL ANALYSIS

By Turbine Power Insights

The small turbine segment dominated the market by capturing the highest share of the European market in 2025 due to its suitability for research and development phases, where risk mitigation is paramoulower-rateders favor systems with lower rated capacities because they require less capital investment during the testing phase, allowing for iterative design improvements. According to the European Commission Joint Research Centre, a majority of active airborne wind energy projects in Europe utilize small-scale prototypes to validate control algorithms and tether dynamics before scaling up. The German Aerospace Center indicates that small turbines can be deployed and retrieved within hours, facilitating extensive field testing cycles that accelerate technological maturation. Furthermore, government departments report that regulatory approval for small-scale installations is significantly faster than for large commercial units due to reduced aviation safety concerns. This agility enables startups to secure venture funding more easily, as investors perceive lower technical risk in smaller deployments. Research organizations state that small turbines achieve technology readiness levels faster than their larger counterparts, providing a competitive advantage in a rapidly evolving market.

On the other side, the large turbine segment is projected to register high growth and showcase a promising CAGR in the European market during the forecast period as utilities seek to replace fossil-fuel baseload capacity with high-yield renewable sources. Large airborne systems with high capacities offer superior capacity factors, making them commercially competitive with conventional offshore wind farms. According to the International Energy Agency, utility-scale airborne projects can achieve a competitive levelized cost of electricity when operating at optimal altitudes, attracting significant interest from major energy providers. Investment banks have committed substantial funding to support the development of large-scale airborne wind farms, recognizing their potential to deliver clean energy. National ministries state that large turbines benefit from economies of scale, where material costs per kilowatt decrease significantly compared to small units. Furthermore, energy agencies report that large installations can connect directly to high-voltage transmission networks, eliminating the need for complex distribution upgrades. This direct grid-integration capability makes large turbines attractive for national energy strategies aiming to decarbonize industrial sectors. National research centers indicate that large airborne systems require less land area per megawatt than solar farms, addressing spatial constraints while delivering consistent power output.

By Application Insights

The onshore segment dominated the market by holding the major share of the global market in 2025 due to easier land-acquisition processes and immediate connectivity to established electrical grids. Terrestrial deployments avoid the complex maritime regulations and harsh corrosive environments associated with offshore installations, reducing operational complexity and maintenance costs. According to the European Environment Agency, a high percentage of suitable high-altitude wind sites in Europe are located within 50 kilometers of existing high-voltage substations, minimizing transmission-upgrade requirements. National regulatory agencies report that onshore airborne projects receive grid-connection approvals faster than offshore equivalents due to simplified logistical coordination. Government departments state that onshore installations benefit from mature supply chains for foundation construction and cable laying, reducing project-development timelines. Furthermore, ministries indicate that agricultural landowners are increasingly willing to lease space for airborne turbines as they occupy minimal ground footprint, allowing continued farming activities. Economic ministries confirm that onshore projects face lower insurance premiums than offshore installations due to easier access for emergency repairs. This accessibility enables faster deployment cycles, allowing developers to respond quickly to changing market demands.

However, the offshore segment is predicted to register a promising CAGR in the global market over the forecast period as governments prioritize marine renewable energy to meet ambitious climate targets. Offshore locations offer consistently stronger winds with less turbulence, resulting in high capacity factors for airborne systems. According to the European Commission, offshore wind resources in European waters could generate significant energy annually, enough to power the entire continent. Industry reports suggest that leasing rounds for offshore renewable energy zones have increased, reflecting intense developer interest. National ministries state that offshore airborne projects qualify for additional subsidies under marine energy strategies, providing financial incentives for developers. Furthermore, energy agencies indicate that offshore installations face fewer visual-impact objections from local communities, accelerating permitting processes. Petroleum and energy ministries confirm that decommissioned oil platforms provide ready-made infrastructure for airborne wind deployments, reducing initial capital costs. Offshore wind deployment centers state that floating airborne systems can be deployed in deeper waters, opening vast new areas for energy generation previously inaccessible to fixed-bottom turbines.

REGIONAL ANALYSIS

Europe held a prominent share of the global airborne wind turbines market in 2025 and is likely to remain the primary hub for airborne wind technology development over the next few years due to its aggressive decarbonization policies and established research ecosystems. Europe maintains its position as the global leader in the airborne wind turbine market, driven by aggressive decarbonization policies and substantial research funding initiatives. The region accounts for a significant portion of the global market share due to strong governmental support and advanced technological infrastructure. According to the European Commission, the Fit for 55 package mandates a reduction in greenhouse gas emissions, creating urgent demand for innovative renewable solutions. Germany leads the region with numerous active pilot projects supported by national ministries. The Netherlands follows closely with significant investments focusing on offshore floating applications. National energy departments report that airborne wind projects are eligible for support schemes guaranteeing stable revenue streams for developers. France has introduced specific zoning laws allowing high-altitude energy harvesting in rural areas, accelerating project approvals. Investment banks have facilitated significant financing for renewable energy innovations, including airborne systems. Nordic countries contribute significantly through cross-border collaborations focusing on cold-climate adaptations. This cohesive policy framework, combined with robust industrial capabilities, ensures Europe remains the primary hub for technology development.

COMPETITION OVERVIEW

The competition in the airborne wind turbine market is characterized by intense innovation and rapid technological evolution as numerous startups and established energy firms vie for dominance in this nascent sector. Market participants differentiate themselves through unique design architectures, such as pumping kite systems versus flygen configuration,s each offering distinct advantages in efficiency and maintenance requirements. The barrier to entry remains high due to complex regulatory approvals and substantial capital requirements for prototypi,ng yet the potential for disruptive impact attracts significant venture capital investment. Competitors focus heavily on demonstrating reliability and cost competitiveness against conventional wind and solar techutility-scaleain credibility with utility scale buyers. Strategic alliances with aerospace companies provide access to adva,nced materials and control systems enhancing product performance. The lack of standardized regulations creates a fragmented landscape where first movers can establish strong brand recognition but also face significant uncertainty regarding future compliance requirements and grid integration standards across different jurisdictions globally.

KEY MARKET PLAYERS

A few major players of the Europe airborne wind turbine market include

- Kitepower B.V

- SkySails Power GmbH

- EnerKíte GmbH

- Kitemill AS

- Ampyx Power B.V

- Windlift Inc

- TwingTec AG,

- SkySails Group GmbH

- KiteKRAFT GmbH

- Makani Technologies LLC

- Altaeros Energies Inc

- eWind Solutions Inc

- Kitekraft

- Enerkite

- Kitepower Europe B.V

Top Strategies Used by Key Market Participants

Key players in the airborne wind turbine market primarily employ strategic partnerships with established energy utilities to validate technology and secure long-term power purchase agreements. Companies heavily invest in research and development to enhance control algorithms and material durability, ensuring reliable operation in turbulen,t high-altitude conditions. Many participants pursue government grants and subsidies to offset high initial capital expenditures associated with prototype development and certification processes. Geographic expansion into regions with favorable wind resources and supportive regulatory frameworks drives market penetration efforts significantly. Firms also focus on intellectual property protection through extensive patent filings to safeguard proprietary technologies and maintain competitive advantages. Collaborative projects with aerospace institutions help leverage advanced materials and automation techniques, reducing manufacturing costs while improving system efficiency and overall performance metrics for commercial viability.

Leading Players in the Global Market

- Kite Power Solutions stands as a pioneering entity in the airborne wind energy sector, focusing on developing scalable kitesurfing-inspired technology for commercial electricity generation. The company ground-basedully demonstrated, its ground based generator system which eliminates the n,eed for heavy turbines at altitude thereby reducing material costs significantly. Recent actions include securing substantial funding from European imulti-megawattts to advance their multi megawatt prototype development. They actively collaborate with major utility providers to integrate their high-capacity factor systems into national grids. Their slong-termfocus remains on proving long term reliability through extended field trials in coastal environments where wind resources are most consistent and powerful. This approcost-effectivethem as a leader in cost effective renewable energy solutions that require minimal land use and offer superior energy yields compared to traditional wind farms.

- Makani Power, originally developed by Google ,X has made significant contributions to the technological foundation of airborne wind energy before its operations were scaled back. The company created innovative crosswind flight control algorithms that remain influential in current industry designs. Their legacy includes extensive data on tether dynamics and autonomous flight stability, which continues to inform modern engineering practices. Although direct commercial deployment ceased, the intellectual property and technical insights generated by Makani have been shared with the broader research community. This open source approach has accelerated global innovation, allowing other developers to bypass early-stage experimental hurdles. Their work demonstrated the feasibility of generating power at altitudes previously inaccessible to conventional turbines, establishing critical benchmarks for performance and safety standards in this emerging renewable energy sector.

- EnerKite specializes in pumping kite power systems that utilizeground-basedd generators to convert high-altitude wind energy into electricity efficiently. The company has achieved notable success in demonstrating continuous power generation through automated launch and landing sequences. Recent developments include partnerships with industrial clients to deploy pilot systems for off-grid applications such as mining and remote communities. They focus on robust mechanical designs that withstand harsh environmental conditions, ensuring operational reliability in diverse geographical locations. EnerKite actively participates in international research consortia to standardize testing protocols and safety regulations for airborne wind technologies. Their commitment to modular system architecture allows for easy transportation and rapid installatio,n making their solutions particularly attractive for temporary or mobile energy needs in challenging terrains where traditional infrastructure is unavailable or prohibitively expensive to construct.

MARKET SEGMENTATION

This research report on the Europe airborne wind turbine market has been segmented and sub-segmented based on turbine power, application, and region.

By Turbine Power

- Small Turbine

- Large Turbine

By Application

- Offshore

- Onshore

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the Europe airborne wind turbine market?

The market is driven by Europe's renewable energy targets, technological advancements, and increasing investments in sustainable power generation.

2. What are the key advantages of airborne wind turbines?

They require less material, can access stronger high-altitude winds, reduce installation costs, and have a smaller environmental footprint than conventional wind turbines.

3. Which applications use airborne wind turbines?

They are used for grid electricity generation, off-grid power supply, remote communities, industrial operations, and military applications.

4. What technologies are commonly used in airborne wind energy systems?

Common technologies include kite-based systems, tethered drones, autonomous flying wings, and airborne gliders.

5. What challenges does the Europe airborne wind turbine market face?

Key challenges include regulatory approvals, airspace restrictions, technology commercialization, weather dependency, and high initial development costs.

6. Which end-user sectors are expected to drive market growth?

Utilities, renewable energy developers, defense organizations, mining operations, and remote infrastructure projects are expected to be major end users.

7. What innovations are shaping the airborne wind turbine market?

Innovations include autonomous flight control, AI-based monitoring, lightweight composite materials, advanced tether technologies, and improved energy conversion systems.

8. Which renewable energy sources compete with airborne wind turbines?

They compete primarily with conventional wind turbines, solar power, hydropower, and other emerging renewable energy technologies.

9. What is the future outlook for the Europe airborne wind turbine market?

The market is expected to witness steady growth as technological improvements, supportive regulations, and increasing demand for innovative renewable energy solutions accelerate commercialization.

10. How do airborne wind turbines differ from conventional wind turbines?

Airborne wind turbines operate at higher altitudes using flying devices, while conventional turbines use fixed towers and rotating blades near the ground.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com