Europe Anticoagulant Rodenticides Market Size, Share, Trends & Growth Forecast Report By Chemical Type, By Formulation Type, By Target Pest, and By Country (United Kingdom, Germany, France, Italy, Spain, Netherlands, Belgium, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Anticoagulant Rodenticides Market Report Summary

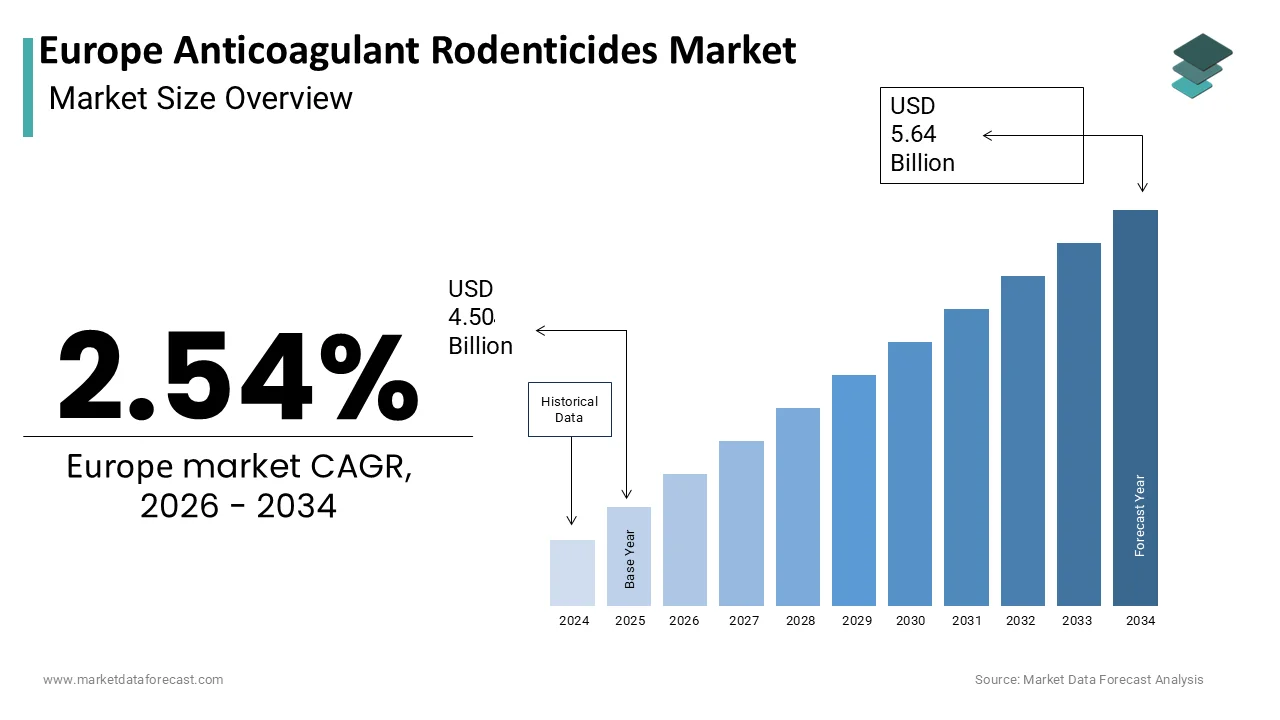

The Europe Anticoagulant Rodenticides Market was valued at USD 4.50 billion in 2025 and is projected to reach USD 5.64 billion by 2034, growing from USD 4.62 billion in 2026 at a CAGR of 2.54% during the forecast period. Growth is driven by increasing urbanization and waste management challenges, stringent food safety regulations for agricultural storage, and integration of digital smart bait station monitoring. Secondary poisoning concerns and rising genetic rodent resistance are shaping market dynamics.

Key Market Trends

- Rising adoption of combined anticoagulant formulations to overcome multi-drug resistance

- Growing integration of smart bait stations with sensor-based digital monitoring

- Increasing development of bio-based and reduced-risk anticoagulant formulations

- Rising regulatory restrictions on outdoor and amateur second-generation anticoagulant use

- Growing pressure from animal welfare advocacy groups pushing non-lethal alternatives

Segmental Insights

- Based on chemical type, second-generation anticoagulants dominated the market in 2025, driven by superior potency against resistant rat and mouse populations.

- Based on formulation type, bait stations led the market in 2025, driven by EU regulatory mandates requiring tamper-resistant containers.

- Based on target pest, rats dominated the market in 2025, driven by their significant public health and infrastructure damage impact.

Regional Insights

- United Kingdom led the market in 2025, supported by pioneering stewardship schemes and high urban rat infestation rates in London and Manchester.

- Germany holds a significant share, driven by its robust industrial base and widespread first-generation anticoagulant resistance in the north.

- France is a prominent market supported by rodent control needs for wine and grain export quality protection.

- Italy contributes notably due to its extensive tourism industry and historic city infrastructure favoring rodent habitats.

- Liquid formulations is the fastest-growing formulation segment, projected at a CAGR of 8.2%, driven by suitability for dry industrial environments like mills and warehouses.

Competitive Landscape

The market is highly competitive, with manufacturers focusing on regulatory compliance, resistance-breaking formulations, and digital monitoring integration. Companies are investing in biodegradable formulations and smart bait station technology to align with EU Green Deal sustainability objectives.

Prominent players in the market include BASF SE, Bayer AG, Syngenta AG, Liphatech SAS, PelGar International Ltd., Rentokil Initial plc, Bell Laboratories Inc., Neogen Corporation, JT Eaton & Co. Inc., SenesTech Inc., UPL Limited, and Zapi S.p.A.

Europe Anticoagulant Rodenticides Market Size

The Europe Anticoagulant Rodenticides Market is projected to grow from USD 4.50 billion in 2025 to USD 4.62 billion in 2026 and reach USD 5.64 billion by 2034, registering a CAGR of 2.54% during the forecast period from 2026 to 2034.

Anticoagulant rodenticides are chemical agents designed to control rodent populations by inhibiting blood clotting mechanisms, leading to internal hemorrhage and eventual death. These substances primarily include first-generation compounds such as warfarin and chlorophacinone and second-generation active ingredients like bromadiolone, difenacoum, and brodifacoum, which are more potent and effective against resistant strains. The regulatory landscape in Europe is strictly governed by the European Union Biocidal Products Regulation, which mandates rigorous assessment of environmental risks, particularly secondary poisoning of non-target species. According to the Food and Agriculture Organization, rodents cause significant damage to crops and stored food products, with estimates suggesting that they destroy approximately 5% of global grain supplies annually. In urban environments, public health concerns drive demand as rodents are vectors for diseases such as leptospirosis and hantavirus. As per reports from the European Centre for Disease Prevention and Control, the risk of rodent-borne diseases is rising in European cities due to factors like climate change and waste management challenges. The market is characterized by a shift toward integrated pest management strategies that combine chemical control with sanitation and exclusion methods. Professional pest control operators constitute the primary end users, adhering to strict application protocols to minimize ecological impact. The tension between effective pest control and biodiversity conservation shapes product development, focusing on reduced persistence in the environment and targeted delivery systems. This dynamic ensures that anticoagulant rodenticides remain essential tools despite growing scrutiny from environmental advocates and regulatory bodies.

MARKET DRIVERS

Increasing Urbanization and Waste Management Challenges Fuel Rodent Population Growth

Rapid urbanization across Europe has created ideal habitats for rodent proliferation, which is driving the sustained demand for effective anticoagulant rodenticides and is a key market driver for the European anticoagulant rodenticides market. Cities provide abundant shelter in sewage systems, basements, and waste disposal facilities, while improper waste management offers consistent food sources. According to the European Centre for Disease Prevention and Control, leptospirosis remains a persistent public health concern in the European Union, with hundreds of cases reported annually. The concentration of human populations in metropolitan areas such as London, Paris, and Berlin exacerbates infestation levels, requiring intensive chemical control measures. As per estimates from urban pest management experts, rodent activity in major European cities has seen a notable increase in recent years due to warmer winters and increased outdoor dining cultures. The expansion of underground transport networks further facilitates rodent movement, allowing populations to spread rapidly across large geographic areas. Professional pest control services are increasingly contracted by municipalities and private property owners to manage these infestations, relying heavily on second-generation anticoagulants for their efficacy against large colonies. The economic cost of rodent damage to infrastructure, including electrical wiring and insulation, runs into millions of euros annually, prompting proactive treatment programs. Furthermore, the tourism sector in historic European cities faces reputational risks from visible rodent activity, necessitating discreet and effective control solutions. This urban pressure ensures a steady baseline demand for anticoagulant products despite regulatory restrictions on amateur use.

Stringent Food Safety Regulations and Agricultural Storage Requirements Drive Commercial Demand

The imperative to maintain high standards of food safety and hygiene in agricultural storage and processing facilities is further contributing to the European anticoagulant rodenticides market expansion. Rodents contaminate stored grains and processed foods with urine, feces, and hair, leading to substantial economic losses and health hazards. According to the European Food Safety Authority, maintaining compliance with safety limits is a priority, with strict monitoring of supply chains to prevent contamination and spoilage. Strict compliance with Hazard Analysis and Critical Control Points standards requires facilities to implement robust pest control protocols, including the strategic placement of anticoagulant baits. As per industry standards, post-harvest losses due to pest infestation can be significant in poorly managed storage units, necessitating reliable chemical interventions. The consolidation of agricultural operations into larger industrial complexes has increased the scale of potential infestations, requiring professional-grade rodenticides that offer long-lasting protection. Second-generation anticoagulants are preferred in these settings due to their single-feed efficacy, which reduces the frequency of bait replenishment and labor costs. Additionally, the export orientation of European agricultural products demands adherence to international phytosanitary standards that prohibit rodent presence in shipments. This commercial pressure drives continuous investment in advanced bait formulations that remain palatable and effective under varying storage conditions, ensuring the integrity of the food supply chain.

MARKET RESTRAINTS

Environmental Concerns Regarding Secondary Poisoning of Non-Target Wildlife

The significant risk of secondary poisoning to non-target wildlife is a major restraint on the Europe anticoagulant rodenticides market, which is leading to stricter regulatory limitations. Predators and scavengers such as barn owls, red kites, and foxes consume poisoned rodents, accumulating lethal doses of anticoagulants in their tissues. According to research from the Royal Society for the Protection of Birds, studies indicate that residues of second-generation anticoagulant rodenticides are frequently found in predatory bird populations, highlighting the severity of ecological impact. The European Chemicals Agency has responded by imposing restrictions on the concentration and packaging of certain active ingredients to mitigate these risks. As per the European Union Biocidal Products Regulation, several second-generation substances have been restricted for outdoor use and amateur applications, limiting market accessibility. Environmental NGOs actively campaign against the widespread use of persistent anticoagulants, arguing that they disrupt local ecosystems and biodiversity. This public pressure influences policymakers to favor non-chemical alternatives or less toxic first-generation compounds, which are often less effective against resistant rodent strains. The requirement for specialized training and certification for professional users further restricts the pool of authorized applicators, increasing operational costs for pest control companies. Consequently, manufacturers face higher compliance burdens and limited distribution channels, slowing market growth and forcing innovation in safer delivery mechanisms.

Development of Genetic Resistance in Rodent Populations Reduces Product Efficacy

The emergence of genetic resistance in common rodent species significantly undermines the effectiveness of existing anticoagulant rodenticides, which is further impeding the regional market growth. Prolonged exposure to first- and second-generation anticoagulants has selected for rodents with mutations in the VKORC1 gene, which confer resistance to vitamin K antagonists. According to research published by the University of Hohenheim, resistance to first-generation anticoagulants is widespread in brown rat populations across Germany and France, with prevalence rates often exceeding 50% in urban areas. Even second-generation compounds face declining efficacy as resistance traits spread through rodent communities, requiring higher doses or alternative active ingredients. As per monitoring data from pest management experts, resistance patterns reveal a growing trend of multi-drug resistance, complicating pest management strategies. This biological adaptation forces pest control professionals to rotate products or integrate non-chemical methods, increasing complexity and cost. Regulatory bodies are hesitant to approve new, stronger anticoagulants due to environmental concerns, leaving the industry with a shrinking arsenal of effective tools. The need for continuous resistance monitoring and tailored treatment plans reduces the ease of use that previously drove mass market adoption. Manufacturers must invest heavily in research to develop novel modes of action or resistance-breaking formulations, which is a slow and expensive process. This scientific challenge limits the long-term viability of traditional anticoagulant products and drives a shift toward integrated pest management approaches.

MARKET OPPORTUNITIES

Integration of Digital Monitoring Systems with Smart Bait Stations

The integration of digital technology into rodent control infrastructure presents a significant opportunity for the Europe anticoagulant rodenticides market by enhancing efficiency and reducing environmental exposure. Smart bait stations equipped with sensors and connectivity features allow real-time monitoring of bait consumption and rodent activity, enabling precise application of anticoagulants. According to market research, the adoption of digital pest management solutions is steadily growing in Europe as companies seek to optimize service delivery and reduce labor costs. These systems minimize the amount of rodenticide used by alerting technicians only when refilling is necessary, thereby reducing the risk of non-target exposure and environmental contamination. As per performance data from pest control service providers, smart stations improve treatment success rates through data-driven decision-making and timely interventions. The ability to generate detailed reports on infestation trends helps clients demonstrate compliance with food safety and hygiene regulations. Manufacturers partnering with technology firms can offer bundled solutions that combine high-quality anticoagulant baits with intelligent hardware, creating added value for professional users. This technological evolution aligns with the European Green Deal objectives by promoting resource efficiency and reducing chemical usage. The premium pricing potential for smart systems offers higher margins compared to traditional products, driving revenue growth. Furthermore, the data collected contributes to a better understanding of rodent behavior and resistance patterns, informing future product development.

Expansion into Emerging Bio-Based and Reduced Risk Formulations

The development of bio-based and reduced-risk anticoagulant formulations offers a promising avenue for market expansion amidst tightening environmental regulations. Innovations in formulation technology aim to enhance biodegradability and reduce persistence in the environment while maintaining efficacy against resistant rodent strains. According to the European Bioplastics association, the demand for sustainable agricultural and pest control inputs is rising, with consumers and regulators favoring products with lower ecological footprints. New formulations incorporating natural attractants and encapsulation technologies protect the active ingredient from degradation and reduce accidental ingestion by non-target species. As per research from institutes focusing on sustainable chemistry, microencapsulated anticoagulants show improved stability and targeted release profiles, minimizing environmental leakage. These advanced products appeal to environmentally conscious customers, including organic farms and green building projects that require certified low-impact pest control solutions. Regulatory agencies are more likely to approve novel formulations that demonstrate reduced toxicity to non-target organisms, facilitating faster market entry. Manufacturers investing in green chemistry can differentiate their brands and capture niche market segments willing to pay premium prices for sustainable options. Collaborations with academic institutions accelerate the discovery of new active ingredients derived from natural sources. This shift toward eco-friendly products aligns with broader societal trends toward sustainability and responsible chemical use, ensuring long-term market relevance.

MARKET CHALLENGES

Complex and Fragmented Regulatory Approval Processes Across Member States

Navigating the complex and fragmented regulatory landscape for biocidal products poses a significant challenge for manufacturers in the Europe anticoagulant rodenticides market. While the European Union Biocidal Products Regulation provides a framework for authorization, individual member states retain authority over specific usage conditions and national restrictions. According to the European Chemicals Agency, the process for renewing approvals for active substances can take several years, involving extensive data requirements and high costs. Divergent national interpretations of environmental risk assessments lead to inconsistent market access, with some countries banning substances approved elsewhere. As per reports from industry associations, the administrative burden of maintaining compliance across member states increases operational costs and delays product launches. Small and medium-sized enterprises struggle to meet the financial and technical demands of the regulatory process, limiting competition and innovation. Frequent changes in regulatory status create uncertainty for distributors and end users, who must constantly adapt to new rules. The lack of harmonization hinders the free movement of goods within the single market, reducing economies of scale. Manufacturers must maintain dedicated regulatory affairs teams to monitor legislative developments and manage submissions, straining resources. This regulatory volatility discourages investment in new product development and forces companies to focus on maintaining existing portfolios rather than innovating.

Public Perception and Pressure from Animal Welfare Advocacy Groups

Negative public perception and intense pressure from animal welfare organizations present a persistent challenge to the Europe anticoagulant rodenticides market. Critics argue that anticoagulants cause prolonged suffering to rodents through internal bleeding and also harm protected wildlife through secondary poisoning. According to the Special Eurobarometer survey on biodiversity, there is overwhelming public support for nature protection and ethical standards in environmental management. Animal rights groups actively lobby governments to restrict or ban the use of second-generation anticoagulants, citing ethical concerns and ecological damage. As per reports from animal welfare organizations, the visibility of dead rodents in urban areas generates public outcry and complaints to local authorities, leading to restrictive municipal ordinances. This social license to operate is eroding, forcing pest control companies to adopt more transparent and humane practices. The stigma associated with chemical rodenticides drives demand for non-lethal alternatives even when they are less effective or more expensive. Manufacturers face reputational risks and must invest in public relations efforts to justify the necessity of their products for public health and food safety. The emotional nature of the debate makes it difficult to communicate scientific evidence regarding the necessity of population control. This societal shift requires the industry to adapt its messaging and product offerings to align with evolving ethical standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Chemical Type, Formulation Type, Target Pest, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, Germany, France, Italy, Spain, Netherlands, Belgium, Sweden, Rest of Europe |

| Market Leaders Profiled | BASF SE, Bayer AG, Syngenta AG, Liphatech SAS, PelGar International Ltd., Rentokil Initial plc, Bell Laboratories, Inc., Neogen Corporation, JT Eaton & Co., Inc., SenesTech, Inc., UPL Limited, Zapi S.p.A. |

SEGMENTAL ANALYSIS

By Chemical Type Insights

The second-generation anticoagulants segment dominated the market by capturing the largest share of the regional market in 2025 due to their superior potency and efficacy against rodent populations that have developed resistance to first-generation compounds and the widespread prevalence of genetic resistance in brown rats and house mice across major European urban centers, which renders older chemicals like warfarin ineffective. According to research from the University of Hohenheim, resistance to first-generation anticoagulants exceeds 50% in rat populations in Germany and France, necessitating the use of stronger active ingredients such as bromadiolone and difenacoum. These second-generation compounds require only a single feeding to deliver a lethal dose, ensuring rapid population control in high-density infestations common in cities and agricultural storage facilities. As per the European Chemicals Agency, despite regulatory restrictions on outdoor use, second-generation anticoagulants remain the standard for professional pest control operators who manage severe infestations in industrial and commercial settings. Their longer half-life in rodent tissues ensures mortality even if the animal consumes sub-lethal amounts over several days, providing a safety margin for application efficiency. The economic imperative to minimize crop loss and infrastructure damage drives commercial users to prioritize effectiveness over cost, leading to sustained demand for these high-performance chemicals. Professional applicators are trained to mitigate environmental risks through precise placement, making these potent agents viable within strict regulatory frameworks. This balance of high efficacy and managed risk solidifies the dominance of second-generation anticoagulants in the professional sector.

On the other end, the combined anticoagulants segment is estimated to grow at a promising CAGR of 7.5% over the forecast period in the European market owing to the growing need to overcome multi-drug resistance and enhance bait acceptance and the formulation of products that mix different active ingredients or combine anticoagulants with non-anticoagulant agents to target resistant rodents through multiple physiological pathways. According to studies published by the Journal of Pest Science, combination baits show significantly higher mortality rates in resistant populations compared to single active ingredient products, as they reduce the likelihood of survival through genetic mutation. As per monitoring data, the emergence of super-resistant strains in urban areas has prompted pest control professionals to adopt rotation strategies and mixed formulations to maintain control efficacy. These combinations often include cholecalciferol or other synergists that accelerate blood clotting inhibition, reducing the time to death and minimizing the window for secondary poisoning risks. Manufacturers are investing in research to develop proprietary blends that comply with environmental regulations while maximizing kill rates. The ability to address complex resistance profiles makes combined anticoagulants attractive for difficult infestations in sensitive environments such as food processing plants and historic buildings. Regulatory bodies are increasingly recognizing the value of integrated chemical approaches, leading to faster approval processes for novel combinations. This innovation pipeline supports robust growth as the industry seeks sustainable solutions to the escalating resistance challenge.

By Formulation Type Insights

The bait stations segment led the market by holding the leading share of the European market in 2025. The dominance of bait stations segment in the European market can be credited to their enhanced safety profile, compliance with regulatory standards, and effectiveness in protecting baits from environmental degradation and the stringent European Union Biocidal Products Regulation, which mandates that amateur use of rodenticides must be in tamper-resistant containers to prevent access by children, pets, and non-target wildlife. According to the European Chemicals Agency, a high percentage of consumer-grade anticoagulant products are now sold exclusively in pre-filled bait stations, reflecting this regulatory shift. Professional pest control operators also prefer bait stations as they allow for precise placement, monitoring of consumption, and easy removal of unused bait, reducing environmental leakage. As per industry data from the European Pest Control Association, the use of secured stations significantly reduces accidental secondary poisoning incidents compared to loose bait applications. Bait stations protect the active ingredient from moisture and sunlight, maintaining palatability and potency for extended periods, which improves cost-efficiency for large-scale operations. The modular design of modern stations facilitates integration with digital monitoring systems, enabling real-time data collection on rodent activity. This technological compatibility enhances service value for commercial clients requiring detailed reporting for audit purposes. The combination of regulatory compliance, operational efficiency, and safety assurance ensures that bait stations remain the dominant formulation type across both residential and professional sectors.

On the other side, the liquid formulations segment is predicted to record a CAGR of 8.2% over the forecast period in the European market owing to their suitability for water-scarce environments and specific rodent behavioral preferences and the increasing recognition that rodents in dry conditions or those feeding on dry grains prefer liquid sources over solid baits, which is making liquid anticoagulants highly effective in certain scenarios. For instance, liquid baits demonstrate higher acceptance rates in industrial settings such as mills and warehouses where dust and dry materials dominate the environment. Liquid formulations allow for flexible application methods, including drip lines and reservoirs that can reach inaccessible voids and cavities where solid blocks cannot be placed. The ability to mix liquid concentrates with attractants enhances palatability and ensures consistent dosing across large infestations. Recent advancements in stabilizer technology have improved the shelf life and weather resistance of liquid products, which is addressing previous concerns about evaporation and spillage. Regulatory approvals for professional use of liquid anticoagulants have expanded in several member states, recognizing their utility in integrated pest management programs. The reduced risk of mold growth compared to moist solid baits makes them ideal for long-term monitoring stations. This versatility and targeted efficacy in challenging environments drive the rapid adoption of liquid formulations among professional applicators seeking comprehensive control solutions.

By Target Pest Insights

The rats segment dominated the market by accounting for the leading share of the European market in 2025. The growth of the rats segment in the European market can be credited to their larger size, greater reproductive potential, significant impact on public health and infrastructure, and the extensive damage caused by brown rats and black rats to sewage systems, electrical wiring, and building foundations, which necessitates aggressive control measures. According to the European Centre for Disease Prevention and Control, rats are primary vectors for diseases such as leptospirosis and salmonellosis, posing serious health risks in urban environments with dense human populations. As per municipal data from major European cities, rat infestations have shown an upward trend in the last decade due to climate change and inadequate waste management, driving sustained demand for potent rodenticides. The larger body mass of rats requires higher doses of anticoagulants, leading to greater volume consumption of products compared to the mouse control. Commercial and industrial facilities prioritize rat control to prevent costly structural damage and regulatory fines related to hygiene violations. Second-generation anticoagulants are particularly effective against rats due to their single-feed lethality, which is crucial for controlling large colonies quickly. The visibility of rat activity generates immediate public pressure on authorities to implement control programs, ensuring consistent market demand. Professional pest control contracts heavily focus on rat eradication due to the complexity and scale of infestations. This critical need for public health protection and asset preservation solidifies rats as the primary target for anticoagulant applications.

On the other end, the mice segment is estimated to register a CAGR of 6.5% over the forecast period in the European market due to their ability to infiltrate smaller spaces, thrive in insulated modern buildings, changes in construction practices that favor energy-efficient designs with ample voids, and insulation materials that provide ideal nesting sites for house mice. According to the British Pest Control Association, mouse-related service requests have become increasingly prominent in many regions due to their proliferation in residential and commercial properties. As per data from housing associations, mouse infestations are increasingly reported in new-build developments where small entry points are often overlooked during construction. The smaller size of mice allows them to survive on minimal food sources, making them resilient in clean environments where sanitation is high. Modern anticoagulant formulations are being optimized for mouse palatability with smaller bait sizes and enhanced attractants to ensure adequate intake. The difficulty in detecting mouse infestations until they become severe drives proactive treatment programs in the property management sector. Regulatory focus on indoor pest control has led to the development of safer bait stations specifically designed for mouse control in sensitive areas. The increasing frequency of mild winters due to climate change allows mouse populations to breed year-round, further accelerating growth. This shift in pest dynamics positions mice as a rapidly expanding segment requiring specialized control strategies.

COUNTRY LEVEL ANALYSIS

UK Anticoagulant Rodenticides Market Analysis

The UK dominated the market by capturing the leading share of the European market in 2025 and is likely to see sustained demand for high-end professional services as urbanization and infrastructure challenges persist over the next few years. The country faces significant rodent pressure in historic cities and modern infrastructure, driving consistent demand for professional pest control services. According to the British Pest Control Association, rodent-related call-outs have increased by 15% in recent years due to warmer winters and changes in waste disposal practices. The UK has been a pioneer in implementing stewardship schemes such as the Campaign for Responsible Rodenticide Use, which promotes best practices and reduces environmental impact. As per data from local councils, London and Manchester report some of the highest rat infestation rates in Europe, necessitating intensive municipal control programs. The ban on second-generation anticoagulants for amateur use has shifted the market toward professional services and safer consumer products. Research institutions in the UK lead global efforts in understanding rodent resistance patterns, informing product development. The strong presence of major pest control companies ensures high service standards and adoption of advanced technologies. Government support for public health initiatives reinforces the importance of effective rodent control. The UK’s proactive approach to regulation and education maintains its leadership role in the regional market.

Germany Anticoagulant Rodenticides Market Analysis

Germany maintains a significant share in the Europe anticoagulant rodenticides market due to its robust industrial base and stringent environmental regulations enforced by the Federal Environment Agency. The country’s extensive agricultural sector and dense urban centers create diverse demand for both crop protection and urban pest control solutions. According to the German Pest Control Association, resistance to first-generation anticoagulants is widespread in northern regions, requiring the use of second-generation compounds in professional applications. As per data from the Julius Kuehn Institute, rodent damage to stored grain costs the agricultural sector millions of euros annually, driving investment in effective control measures. Germany emphasizes integrated pest management, combining chemical control with sanitation and exclusion techniques to minimize environmental impact. The regulatory framework restricts the outdoor use of certain active ingredients, prompting innovation in bait station design and application methods. Strong manufacturing capabilities support the production of high-quality rodenticides and delivery systems. Public awareness campaigns educate citizens on proper waste management to reduce rodent attractants. The country’s focus on sustainability and precision agriculture influences market trends toward targeted and eco-friendly solutions. Germany’s technical expertise and regulatory rigor shape best practices across the European region.

France Anticoagulant Rodenticides Market Analysis

France occupies a vital position in the Europe anticoagulant rodenticides market, characterized by its large agricultural output and diverse urban environments. The country faces significant challenges from rodent infestations in both rural storage facilities and metropolitan areas like Paris. According to the French Ministry of Agriculture, rodent control is critical for maintaining the quality of wine and grain exports, which are central to the national economy. As per data from municipal authorities in Paris, rat sightings have increased due to tourism-related waste and sewer system complexities, driving demand for professional interventions. France has implemented strict regulations on the use of second-generation anticoagulants, requiring mandatory training for professional applicators. The National Agency for Food, Environmental and Occupational Health Safety monitors residue levels in wildlife to assess environmental impact. Local manufacturers focus on developing formulations suited to Mediterranean and continental climates. Public health initiatives target leptospirosis prevention through coordinated rodent control programs. The cultural emphasis on food quality drives high standards for hygiene in commercial establishments. Government subsidies for sustainable pest management practices encourage adoption of integrated approaches. France’s balanced approach to agricultural productivity and environmental protection sustains steady market growth.

Italy Anticoagulant Rodenticides Market Analysis

Italy holds a growing share in the Europe anticoagulant rodenticides market, driven by its extensive tourism industry and agricultural heritage. The country’s historic cities with complex underground structures provide ideal habitats for rodents, requiring specialized control strategies. According to the Italian National Institute of Health, rodent-borne diseases remain a public health concern, particularly in southern regions with warmer climates. As per data from tourism boards, hotels and restaurants invest heavily in pest control to protect their reputation and comply with hygiene standards. The agricultural sector in the Po Valley faces significant pressure from field mice and rats, affecting crop yields. Italy has adopted European Union regulations while adapting them to local conditions through regional decrees. Professional pest control operators are increasingly using digital monitoring tools to improve efficiency and reduce chemical usage. Public awareness campaigns focus on proper waste disposal to reduce urban infestations. The presence of local manufacturers supports the supply of tailored products for specific regional needs. Government initiatives promote sustainable pest management.

COMPETITIVE LANDSCAPE

The competition in the Europe anticoagulant rodenticides market is characterized by a mix of large multinational chemical corporations and specialized niche manufacturers striving to balance efficacy with environmental safety. Leading players compete primarily on product performance, regulatory compliance,e and technical support rather than price alone due to the specialized nature of professional pest control. The market features moderate consolidation with key entities leveraging their extensive research capabilities to address growing rodent resistance issues. Innovation drives competitive advantage as firms introduce novel formulations and smart delivery systems that align with strict European Union regulations. Regulatory barriers serve as significant entry hurdles favoring established companies with resources to manage complex authorization processes across multiple member states. Regional players maintain strong positions by offering localized solutions and personalized customer service that resonate with domestic pest control operators. The threat of substitution from non-chemical methods remains low for severe infestations but encourages continuous improvement in safety profiles. Competitive intensity is heightened by the need to demonstrate environmental stewardship and reduce secondary poisoning risks. Intellectual property protection plays a vital role as companies safeguard proprietary bait technologies and formulation patents. Collaboration with regulatory bodies and industry groups helps shape standards that favor responsible and effective pest management practices.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Anticoagulant Rodenticides Market include

- BASF SE

- Bayer AG

- Syngenta AG

- Liphatech SAS

- PelGar International Ltd.

- Rentokil Initial plc

- Bell Laboratories, Inc.

- Neogen Corporation

- JT Eaton & Co., Inc.

- SenesTech, Inc.

- UPL Limited

- Zapi S.p.A.

TOP LEADING PLAYERS IN THE MARKET

- BASF SE is a global chemical giant with a significant presence in the European anticoagulant rodenticides market through its professional pest control solutions. The company focuses on developing high-quality active ingredients and formulated baits that meet stringent European regulatory standards. BASF recently expanded its portfolio by introducing innovative bait station designs that enhance safety and reduce environmental exposure. Their commitment to sustainability drives research into biodegradable formulations and reduced-risk products. The firm actively collaborates with pest management professionals to provide training and technical support, ensuring proper application methods. By leveraging its extensive distribution network,k BASF ensures wide availability of its products across major European markets. Recent investments in digital monitoring tools allow customers to track bait consumption and optimize treatment schedules. This integration of chemistry and technology strengthens their position as a leader in effective and responsible rodent control solutions for both urban and agricultural settings.

- Syngenta Group plays a crucial role in the Europe anticoagulant rodenticides market by offering a comprehensive range of pest control products for agricultural and commercial sectors. The company emphasizes integrated pest management strategies combining chemical controls with biological and mechanical methods. Syngenta recently launchedsecond-generationn anticoagulant formulations designed to combat resistant rodent strains while minimizing secondary poisoning risks. Their focus on research and development leads to continuous improvement in bait palatability and efficacy. The firm partners with agricultural cooperatives and facility managers to deliver tailored solutions that address specific infestation challenges. Syngenta also invests in educational programs to promote best practices among users and regulators. By prioritizing environmental stewardship and product innovation, Syngenta maintains a strong reputation for reliability and performance. Their strategic initiatives include expanding production capacity and enhancing supply chain resilience to meet growing demand in the European region.

- PelGar International Ltd is a specialized manufacturer dedicated to the development and production of professional pest control products,s including anticoagulant rodenticides. Based in the United Kingdom, om the company serves the European market with high-quality baits and delivery systems known for their effectiveness and safety. PelGar recently introduced advanced block baits with enhanced weather resistance suitable for diverse climatic conditions. The firm focuses on customer-centric innovation, creating products that simplify applications for pest control technicians. Their recent actions include obtaining additional regulatory approvals for key active ingredients in multiple European countries. PelGar actively participates in industry associations to shape standards and promote responsible use of rodenticides. By maintaining strict quality control and offering excellent technical support, rt PelGar has built a loyal customer base among professional operators. Their commitment to solving complex pest problems through science-based solutions reinforces their competitive position in the specialized European market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe anticoagulant rodenticides market employ several strategic approaches to maintain competitiveness and ensure regulatory compliance. Product innovation remains central as companies develop new formulations that overcome resistance and reduce environmental impact. Manufacturers invest heavily in research and development to create safer bait matrices and more effective active ingredients. Strategic partnerships with pest control associations facilitate training and certification programs that promote best practices and responsible use. Expansion of digital services such as smart monitoring systems enhances value propositions for professional clients by improving efficiency and data accuracy. Companies also focus on regulatory advocacy to navigate complex approval processes and influence policy decisions regarding biocidal products. Sustainability initiatives, including recyclable packaging and eco-friendly ingredients, strengthen brand reputation among environmentally conscious stakeholders. Diversification into integrated pest management solutions allows firms to offer holistic services beyond chemical control. These strategies collectively supportlong-termm growth and adaptation to evolving market dynamics and regulatory landscapes.

MARKET SEGMENTATION

This research report on the europe anticoagulant rodenticides market is segmented and sub-segmented into the following categories.

By Chemical Type

- First-Generation Anticoagulants

- Second-Generation Anticoagulants

- Combined Anticoagulants

By Formulation Type

- Bait Stations

- Pellets

- Blocks

- Powder

- Liquid Formulations

By Target Pest

- Rats

- Mice

- Voles

- Squirrels

- Others

By Country

- UK

- Germany

- France

- Italy

- Spain

- Netherlands

- Belgium

- Sweden

- Rest of Europe

Frequently Asked Questions

1. Which generation leads the market?

Second‑generation anticoagulant rodenticides are the largest segment, while first‑generation products are also widely used and growing in some applications.

2. Which applications are most important?

Main applications include agricultural, industrial/commercial, and residential pest control, with agriculture and industrial sites being major users.

3. Who are the key players?

Key players include BASF, Bayer, Syngenta, Neogen, Rentokil Initial, PelGar International, Liphatech, and other global and regional pest‑control and agrochemical companies.

4. What are the main challenges?

Challenges include strict EU regulations on rodenticide use, concerns about secondary poisoning of non‑target wildlife, resistance development in rodent populations, and pressure to move toward more sustainable pest‑management practices.grandviewresearch+1

5. What is the market outlook?

The outlook is steady, with continued demand expected as rodent pressures persist and professional pest‑control services expand, though growth is moderated by regulatory and environmental constraints.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com