Europe Aquaponics Market Size, Share, Trends & Growth Forecast Report – Segmented By Facility Type (Greenhouse, Building Based Indoor Farms, Others), Equipment, Component, Produce, Application, Growing Mechanism, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Aquaponics Market Size

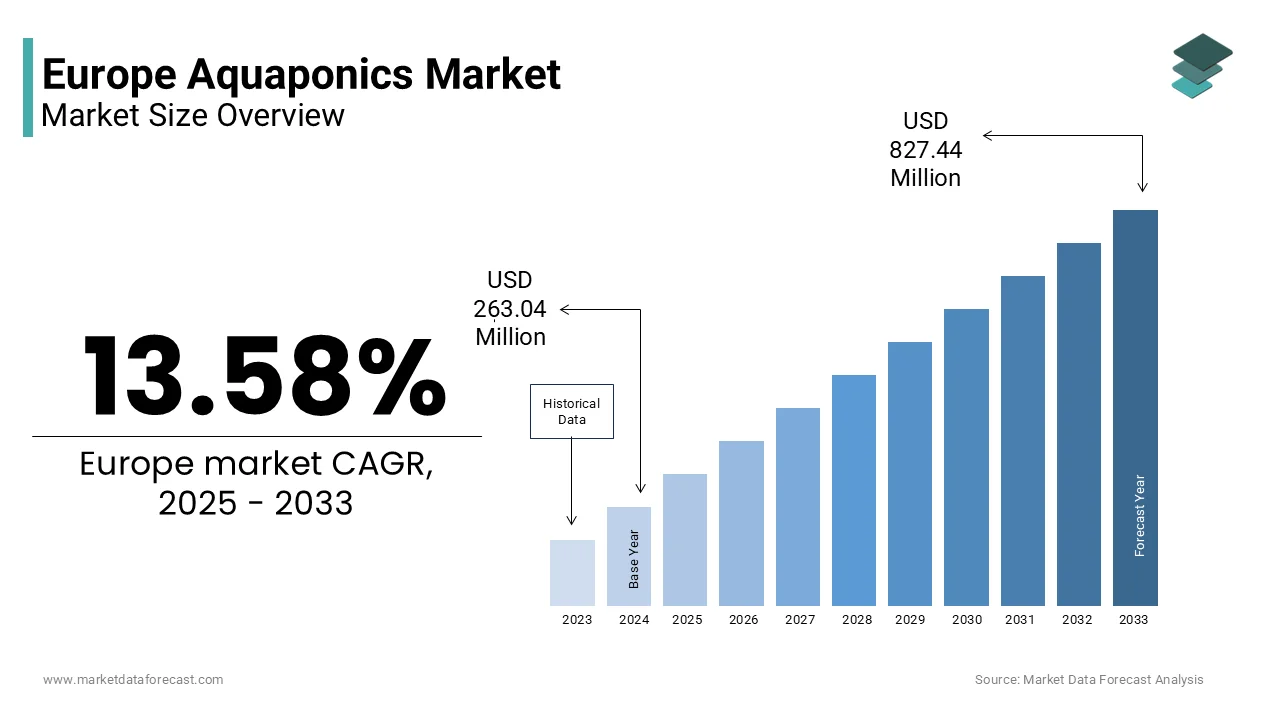

The Europe aquaponics market size was valued at USD 263.04 million in 2024 and is projected to reach USD 827.44 million by 2033 from USD 298.76 million in 2025, growing at a CAGR of 13.58%.

Aquaponics is an integrated agri food system that combines recirculating aquaculture with soilless crop cultivation in a symbiotic closed loop where fish waste provides nutrients for plants and plants purify water for fish. This circular model aligns with the European Union’s Farm to Fork Strategy objectives of reducing chemical inputs water consumption and land use while enhancing local food resilience. Unlike conventional agriculture aquaponics operates in controlled environments, ranging from urban rooftops to repurposed industrial buildings, enabling year round production of leafy greens herbs and freshwater fish with minimal environmental footprint. According to the European Environment Agency (EEA), conventional agriculture accounts for a substantial share of the EU's freshwater withdrawals and greenhouse gas emissions, increasing the strategic importance of water and nutrient-efficient alternatives. Furthermore Eurostat points out that a significant majority of Europeans reside in urban areas where access to fresh, locally grown produce often remains limited. The European Commission’s Horizon Europe program has allocated substantial funding to support urban and vertical farming innovations, including aquaponics, as part of its mission for 100 climate-neutral cities by 2030. This policy and demographic convergence positions aquaponics not as a niche experiment but as an emerging pillar of Europe’s sustainable food future.

MARKET DRIVERS

Urbanization and Demand for Hyperlocal Food Are Driving System Adoption

The region’s high degree of urbanization boosts the growth of the Europe aquaponics market. Cities are seeking resilient localized food production models that reduce supply chain vulnerability and food miles. A significant majority of the population resides in urban environments where access to fresh food frequently relies on extensive logistics vulnerable to disruption. Global events have underscored the fragility of these supply chains, prompting several large cities to incorporate urban farming into their municipal food strategies. Some metropolitan areas are setting specific goals for increasing the amount of locally produced food, favoring methods that provide high output in limited space. Aquaponics is becoming a key element in urban food plans due to its capacity for producing substantial yields of both fish and plants in confined areas using fewer resources than conventional farming. Previously industrial areas and underutilized spaces within cities are increasingly being transformed into production sites to bolster local food security. Cities are supporting these efforts with new zoning rules and financial aid to promote the growth of indoor farming facilities. This urban policy support coupled with consumer willingness to pay premiums for traceable local food fuels commercial and community scale adoption.

EU Policy Support for Circular Agriculture Is Accelerating Investment and Innovation

The European Union’s regulatory and funding architecture actively promotes aquaponics as a model of circular bioeconomy that aligns with multiple Green Deal priorities, and ultimately propels the Europe aquaponics market forward. Policy frameworks have begun to acknowledge closed-loop nutrient systems within agricultural support programs. Initial programs within specific regions have started disbursing financial support to aquaponic operations demonstrating certain water recycling and production methods. Urban development initiatives are funding projects that integrate fish and vegetable production into residential complexes, aiming to enhance local food security and community engagement. Regulatory guidelines for aquaculture systems are being revised, leading to the classification of certain water recycling methods as having a low environmental impact. At the national level, agricultural programs are providing co-financing opportunities for innovative farming startups that achieve specific sustainability benchmarks. This multi level policy endorsement transforms aquaponics from a marginal practice into a bankable agri tech venture with institutional backing.

MARKET RESTRAINTS

High Capital and Operational Complexity Deter Small Scale Adoption

Aquaponics systems require significant upfront investment and continuous technical management that exhibits formidable barriers for individual farmers and community groups, and thereby restricts the growth of the Europe aquaponics market. The initial investment required for a commercial-scale aquaponics facility generally involves a substantial capital outlay, presenting a considerable financial barrier for new ventures. Unlike hydroponics which uses synthetic nutrients aquaponics depends on maintaining a delicate microbial and biological balance where ammonia spikes pH fluctuations or oxygen drops can collapse both fish and plant populations within hours. Small-scale aquaponic businesses in Germany and the EU face notable challenges in achieving sustained commercial viability and operational success. Achieving comprehensive EU organic certification for aquaponics produce is currently not possible due to regulatory requirements that mandate plant cultivation in soil and restrict the use of fish-derived nutrients as fertilizer in certified organic crop production. These financial knowledge and regulatory gaps limit scalability beyond well funded agri tech startups and institutional pilots despite strong consumer interest.

Lack of Harmonized EU Regulations Creates Legal and Market Uncertainty

A fragmented regulatory gray zone, where national interpretations of fish farming, plant production, and food safety rules create inconsistency and compliance risk, impedes the expansion of the Europe aquaponics market. The lack of a harmonized legal definition across national jurisdictions results in facilities being managed as distinct aquaculture and horticulture operations, which can lead to divergent regulatory requirements. This fragmented approach means that the animal and plant components may fall under separate inspection regimes, potentially causing administrative duplication and inconsistent operational guidelines for water quality. Retailers and operators face liability concerns due to the absence of specific, overarching food safety guidance tailored to the produce from these integrated systems, unlike established guidelines for other farming methods. A significant amount of time and resources is expended annually by operators on navigating the varied national permitting processes across different regions. This regulatory ambiguity deters institutional investment and prevents the development of standardized food safety protocols necessary for supermarket supply. The absence of a coherent EU framework under the Sustainable Food Systems Law means aquaponics is confined to small-scale, local experiments and struggles to become a scalable industry.

MARKET OPPORTUNITIES

Integration With Renewable Energy and Smart Building Systems Is Unlocking New Site Potential

Aquaponics is increasingly being embedded into net zero energy buildings and renewable microgrids creating symbiotic infrastructure that enhances both food and energy resilience. This integration is expected to drive the growth of the Europe aquaponics market. A growing number of buildings are being identified as potential candidates for deep energy improvements and may be able to incorporate aquaponic systems that leverage existing heating, ventilation, and air conditioning infrastructure for water temperature management. Certain developments have incorporated aquaponic units into residential living spaces where heat generated from data center operations is repurposed to sustain aquatic life. Rooftop aquaponics installations have been paired with solar thermal technology in specific housing projects to fulfill both hot water requirements and fresh food production for residents. Aquaponic water bodies show potential to function as components within building thermal systems, assisting in absorbing surplus heat during warmer periods and releasing it when the climate is cooler. This convergence of food energy and architecture transforms aquaponics from a standalone farm into a functional component of the circular urban metabolism.

Expansion of Educational and Social Farming Programs Is Building Workforce and Community Support

It is gaining traction as an educational and social inclusion tool across European schools municipalities and rehabilitation centers by fostering public understanding and skilled labor pipelines, which in turn offers fresh prospects for the Europe aquaponics market. Educational institutions across several European regions are increasingly incorporating integrated aquatic and plant cultivation systems to facilitate instruction in biological sciences and sustainability principles. Publicly supported initiatives have facilitated the establishment of urban cultivation sites to serve as vocational training hubs for individuals seeking to re-enter the workforce. National curricula are evolving to include practical applications of circular economy concepts through hands-on engagement with food production technology. Employment support programs are utilizing controlled-environment agriculture as a medium for developing technical skills among displaced populations and the long-term unemployed. There is a visible shift toward integrating agricultural technology into social reintegration strategies to prepare participants for roles within emerging ecological sectors. These initiatives not only build technical capacity but also generate community buy in by linking food production with social equity and education. The European Social Fund has allocated significant amount to expand such programs recognizing aquaponics as a vehicle for green jobs and local empowerment beyond pure commercial output.

MARKET CHALLENGES

Limited Access to Certified Organic Fish Feed Restricts Market Premiumization

The absence of EU-certified organic fish feed compatible with aquaponic systems prevents operators from accessing high-value organic produce and fish markets, despite their chemical-free operations. This poses a major challenge to the European aquaponics market. Regulatory frameworks establish specific minimum thresholds for the inclusion of organic components in fish feed. Despite these guidelines, a significant portion of commercially available aquaculture feeds predominantly utilize ingredients that do not meet organic certification standards. The use of plant-derived alternatives often presents nutritional challenges, specifically concerning the presence of essential amino acids critical for efficient fish development. Observations from production environments indicate that fish receiving partially organic diets exhibit slower growth rates compared to those on conventional feeding regimens. This difference in growth performance affects production timelines and has an impact on the overall economic feasibility of organic aquaculture operations. Consequently, even aquaponic farms using organic seeds and zero pesticides cannot label their vegetables or fish as organic limiting their ability to command price premiums in retail channels. Europe's most profitable sustainable food market will not include aquaponics until the EU either sanctions viable organic feed mixtures or establishes a temporary certification process.

Energy Intensity of Climate Control Undermines Environmental Benefits in Northern Climates

The environmental advantage of aquaponics is significantly offset in colder European regions by the high energy demand for heating water and maintaining greenhouse temperatures during winter months, which slows down the expansion of the Europe aquaponics market. Energy requirements for climate control in Northern European aquaponic sites are comparable to other energy-intensive facilities. The operational energy needed for maintaining temperatures in controlled aquaponic settings is substantially greater than that used in conventional open-field farming. Locations experiencing short winter daylight periods require extra energy input for supplemental lighting to support plant development. Most commercial operations in the area still depend on standard energy sources rather than utilizing integrated renewable heating options. Adoption of sustainable thermal energy sources is not yet widespread in the sector, despite the availability of renewable utilities. The carbon footprint of winter vegetable production might be higher than that of produce imported from Spain or Morocco if low-carbon thermal energy sources are unavailable. This paradox challenges the green narrative of aquaponics and necessitates site specific energy planning to ensure true environmental benefit across Europe’s diverse climatic zones.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 13.58% |

| Segments Covered | By Facility Type, Equipment, Component, Produce, Application, Growing Mechanism, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Nelson and Pade, Inc., The Aquaponic Source, Inc., Practical Aquaponics (Pty) Ltd., Green Life Aquaponics, Backyard Aquaponics Pty Ltd, Aquaponic Lynx LLC, Portable Farms Aquaponics Systems, Stuppy Greenhouse, Inc., Aquaponik Manufactory GmbH, and Aponic Ltd |

SEGMENTAL ANALYSIS

By Facility Type Insights

The greenhouses segment dominated the Europe aquaponics market by accounting for a 58.1% share in 2024. This segment is favored for their balance of environmental control natural light utilization and cost efficiency compared to fully indoor systems. Commercial aquaponic operations in warmer and central regions tend to use protective structures to extend cultivation periods and reduce reliance on supplemental lighting. In a region known for its expertise in protected cultivation, integrated facilities show greater productivity for certain crops per unit area compared to soil-based methods, using substantially less water. A government incentive program providing financial assistance for adopting integrated production methods appears to be accelerating the transition among existing cultivators. A comparable regional initiative supports converting unused cultivation areas into integrated production modules, which assists local economic revitalization efforts. Greenhouses leverage Europe’s strong protected cultivation heritage while minimizing energy demand, critical for economic viability, making them the default choice for scalable commercial production.

The building based indoor aquaponic farms segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 19.7% from 2025 to 2033 due to urban land scarcity policy incentives for vertical agriculture and integration into smart city infrastructure. An increasing number of European cities are incorporating localized food production into municipal climate action plans. Some urban centers are using economic incentives, such as tax abatements, to promote food production in repurposed industrial spaces. Certain new residential developments are mandated to include on-site food production systems. These systems are often chosen for their efficiency in producing both protein and produce within one cycle. Studies suggest that climate-controlled indoor cultivation methods in former industrial buildings can achieve faster annual production cycles than traditional greenhouses. Furthermore, the EU’s Renovation Wave Strategy allocates funding for energy positive buildings where aquaponic water bodies act as thermal buffers reducing HVAC loads. This convergence of urban regeneration energy efficiency and hyperlocal food security makes indoor integration the vanguard of next generation aquaponics.

By Equipment Insights

The pumps and valves segment led the Europe aquaponics market and captured a share of 32.5% of the Europe aquaponics market in 2024. The leading position of the pumps and valves segment is driven by its critical role in maintaining continuous water circulation, the lifeblood of system functionality. Leading practices in commercial aquaponics emphasize designing systems with high energy efficiency, often using a single primary pump, and incorporating robust backup measures to prevent system failure. The failure of a single pump can lead to oxygen depletion and system collapse within hours making reliability and energy efficiency paramount. The aquaponics sector is increasingly adopting high-efficiency pump technology in compliance with regional energy efficiency directives, moving towards more sustainable and power-saving operations. Advancements in motor technology mean that modern high-efficiency pumps provide significant energy savings and reduced operational costs compared to older, less efficient models. Manufacturers have developed corrosion resistant variants specifically for aquaponic saline and organic load conditions. Pumping solutions are a critical and enduring requirement in both greenhouse and indoor cultivation facilities due to the significant amount of energy consumed by water movement systems.

The grow lights segment is expected to exhibit a noteworthy CAGR of 21.7% during the forecast period due to the expansion of indoor aquaponic farms in Northern Europe and advancements in energy efficient LED technology. Facilities in northern latitudes are increasingly relying on artificial lighting solutions to compensate for periods of limited natural light. Modern lighting technologies are demonstrating improved energy efficiency compared to older systems while maintaining comparable light intensity. Specialized lighting programs are being developed to optimize the growth of particular crops and help control competing organisms in shared water environments. Regulations are encouraging the market to move toward high-efficiency lighting systems that meet new operational requirements. The expansion of indoor aquaponics in high-latitude urban centers is transforming grow lights from mere auxiliary tools into primary productivity engines that facilitate continuous harvesting throughout the year, irrespective of external climate conditions.

By Component Insights

The bio filters segment was the largest segment in the Europe aquaponics market by holding a 28.7% in 2024. The supremacy of the bio filers segment is attributed to its indispensable role in converting toxic ammonia from fish waste into plant usable nitrates through nitrifying bacteria. In an aquaculture system lacking efficient biofiltration, ammonia levels rise rapidly to concentrations that are harmful to fish health. European operators increasingly use fluidized bed or moving bed bio reactor designs that provide high surface area per volume enabling compact yet highly effective treatment. A variety of effective plastic biofilter media, such as K1 and K3, are widely used in commercial aquaponic systems to manage water quality. The implementation of advanced biological filtration in closed aquaculture and aquaponic systems substantially minimizes the need for frequent and extensive water exchanges compared to traditional methods. Tighter regulations on nutrient discharge necessitate that biofiltration serves as the crucial heart of system stability and compliance, establishing it as the most valuable and technically specified component in aquaponic installations.

The rearing tanks segment is predicted to witness the highest CAGR of 18.9% over the forecast period. The rapid expansion of the rearing tanks segment is fuelled by the shift toward higher density fish production and modular system designs that prioritize fish welfare and harvest efficiency. Operational guidelines in some areas now advocate for reduced biomass per water volume. This shift often requires aquaculture facilities to use larger or more rearing units. Funded projects are subject to material rules, requiring food-grade materials for tanks, and often mandate integrating permanent ports for continuous water quality tracking. Companies like Aquaculture Systems Europe have introduced conical bottom tanks that simplify waste removal and fish grading reducing labor costs, according to sources. Additionally, the rise of species diversification, beyond tilapia to include perch and pike, demands species specific tank geometries and flow patterns. This focus on fish health productivity and automation is transforming rearing tanks from passive containers into intelligent production units.

REGIONAL ANALYSIS

Netherlands Aquaponics Market Analysis

The Netherlands was the top performer in the Europe aquaponics market and captured a 22.3% share in 2024. The dominance of this country is driven by its world leading greenhouse horticulture expertise and strong policy support for circular food systems. The number of commercial aquaponic facilities in the country has shown an increase, with numerous operations currently active. A significant concentration of these operations has been observed in a key agricultural region where many facilities leverage locally available heat sources to regulate water temperature throughout the year. Government programs encourage the adoption of specific water recycling and chemical input standards, providing financial incentives for systems that meet high environmental performance benchmarks. Companies like Urban Farmers and ECF Farmsystems have pioneered modular containerized aquaponics now exported globally. The Netherlands Food and Consumer Product Safety Authority has also developed streamlined permitting protocols specific to aquaponics reducing approval times to few months. This fusion of technological prowess regulatory agility and export orientation ensures the Netherlands remains Europe’s aquaponics innovation and scaling hub.

Germany Aquaponics Market Analysis

Germany followed closely in the Europe aquaponics market and held a 18.1% share in 2024. The growth of the German market is propelled by its strong engineering base and federal support for urban food resilience. Public funding is being allocated to numerous aquaponic projects that prioritize integration into buildings and connection with renewable energy sources. An urban farm in a major city shows substantial production of vegetables and fish within a restricted area, serving local enterprises. A common trend among recent aquaponic startups involves utilizing domestically produced key system components, which reportedly leads to reliable functionality. Furthermore, Germany’s strict animal welfare laws have driven adoption of low density rearing tanks with real time monitoring compliant with EU fish welfare guidelines. This combination of precision engineering public investment and ethical production standards positions Germany as a high integrity market for scalable urban aquaponics.

France Aquaponics Market Analysis

France maintains a significant position in the Europe aquaponics market due to its integration of aquaponics into rural revitalization and educational programs. A government initiative has facilitated the establishment of integrated farming and learning centers to provide operational training to agricultural workers and unemployed individuals. In certain southern regions, support exists for repurposing existing agricultural land for integrated food production systems, sometimes incorporating renewable energy and local aquatic species. Research suggests that utilizing specific herb varieties as companion plants can enhance yields and naturally manage common agricultural pests. Additionally, a national legal framework encourages using previously developed or non-agricultural sites for food production, offering incentives such as expedited permits for qualifying integrated farming operations. This blend of social inclusion ecological innovation and land use policy makes France a unique bridge between rural tradition and urban sustainability.

Sweden Aquaponics Market Analysis

Sweden grew steadily in the Europe aquaponics market owing to its leadership in energy integrated urban food systems and cold climate innovation. New residential developments in certain urban areas are increasingly required to incorporate on-site food production. Aquaponics is frequently chosen for this purpose, offering both food production and thermal regulation benefits. Observations indicate that water tanks in these systems help decrease reliance on district heating during winter due to heat exchange. Financial incentives, such as grants, are available in some regions to partially fund the implementation costs of these systems, provided they are powered by renewable energy. Companies like Nordic Harvest combine vertical aquaponics with waste heat from data centers achieving year round production in Stockholm’s harsh winters. Furthermore Sweden’s strict chemical prohibition aligns perfectly with aquaponics’ pesticide free model. This systemic integration of food energy and urban planning positions Sweden as a pioneer in climate resilient aquaponics.

United Kingdom Aquaponics Market Analysis

The United Kingdom is predicted to expand in the European aquaponics market from 2025 to 2033 due to rapid growth in urban agri tech and post Brexit food security strategies. There has been recent growth in the number of new commercial aquaponic ventures, with discernible concentrations emerging in several major urban areas. Government innovation initiatives focusing on sustainable packaging have provided funding that has enabled the development of systems utilizing recycled materials. A notable urban aquaponic farm operates on a substantial scale, supplying local grocery retailers with large quantities of produce and fish while integrating sustainable practices like water and energy capture. Aquaponics is recognized as an "Innovative Production System" within the current agricultural transition framework, making related projects eligible for funding opportunities to enhance resource efficiency. Despite leaving the EU the UK’s focus on domestic food resilience and urban innovation sustains its dynamic and fast evolving aquaponics landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe aquaponics market is characterized by a blend of innovation driven startups and engineering focused SMEs operating in a pre commercial yet policy supported environment. The market lacks dominant incumbents allowing agile players like ECF Farmsystems Urban Farmers and Nordic Harvest to differentiate through system integration energy efficiency and urban applicability. Unlike mature agricultural sectors competition here centers on technological reliability circular performance and alignment with municipal climate and food security goals rather than price. Barriers to entry remain high due to capital intensity and technical complexity yet public funding from Horizon Europe national ministries and city grants lowers risk for qualified operators. Regulatory fragmentation persists but leaders proactively engage in standard setting to shape certification pathways. The competitive edge lies in proving year round economic viability while delivering on sustainability promises—transforming aquaponics from a demonstration project into a bankable component of Europe’s resilient food future.

KEY MARKET PLAYERS

Some of the notable key players in the European aquaponics market are

- Nelson and Pade, Inc.

- The Aquaponic Source, Inc.

- Practical Aquaponics (Pty)Ltd.

- Green Life Aquaponics

- Backyard Aquaponics Pty Ltd

- Aquaponic Lynx LLC

- Portable Farms Aquaponics Systems

- Stuppy Greenhouse, Inc.

- Aquaponik manufactory GmbH

- Aponic Ltd

Top Players in the Market

- ECF Farmsystems is a Germany based pioneer in modular aquaponics technology with a strong footprint across Europe and emerging markets in the Middle East and Africa. The company designs scalable containerized and greenhouse integrated systems that combine recirculating aquaculture with vertical plant cultivation optimized for urban and peri urban environments. ECF leverages German engineering to ensure energy and water efficiency with proprietary biofilter and monitoring technologies validated by the Technical University of Berlin. It also partnered with Berlin’s municipal housing authority to integrate aquaponic units into social housing complexes supporting local food resilience. ECF Farmsystems has set a global standard for replicable urban aquaponics due to its use of standardized modular design and policy-aligned deployment.

- Urban Farmers is a Netherlands headquartered innovator specializing in high density rooftop and greenhouse aquaponics with a focus on circular urban metabolism. The company’s flagship Urban R-ECO system integrates fish production with leafy green and herb cultivation using waste heat from buildings and rainwater harvesting to minimize external inputs. Urban Farmers collaborates closely with University to optimize feed conversion ratios and plant growth recipes under European climatic conditions. It also developed a certified training program for urban farmers now adopted in 12 European cities. Urban Farmers is transforming aquaponics into a civic utility by integrating food production directly into existing urban infrastructure.

- Nordic Harvest is a Sweden based leader in energy integrated vertical aquaponics that leverages Nordic sustainability principles and cold climate innovation. The company operates one of Europe’s largest vertical farms in Taastrup Denmark combining aquaponics with waste heat from a data center to maintain year round production without fossil fuels. It also co authored the Swedish Standards Institute’s guidelines for urban aquaponic food safety. Nordic Harvest leads by example, establishing high standards for climate-resilient urban food through its focus on energy symbiosis, food quality, and clear regulations in Northern Europe and beyond.

Top Strategies Used by the Key Market Participants

Key players in the Europe aquaponics market focus on modular and scalable system design integration with renewable energy and urban infrastructure development of automated monitoring and control technologies partnerships with municipalities and educational institutions for social embedding compliance with evolving EU and national food safety and water recycling standards and creation of premium B2B supply chains targeting restaurants schools and urban consumers seeking hyperlocal traceable produce.

MARKET SEGMENTATION

This research report on the European aquaponics market has been segmented and sub-segmented based on categories.

By Facility Type

- Greenhouse

- Building Based Indoor Farms

- Others

By Equipment

- Pumps & Valves

- Grow Light

- Aeration Systems

- Water Heaters

- Others

By Component

- Rearing Tank

- Settling Basin

- Bio-Filters

- Sump Tank

- Others

By Produce

- Fish

- Fruits & Vegetables

- Others

By Application

- Commercial

- Home Production

- Research & Education

By Growing Mechanism

- Media Filled Grow Beds

- Nutrient Film Technique (NFT)

- Deep Water Culture (DWC)

- Vertical Aquaponics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is aquaponics and how does it work?

Aquaponics is a sustainable farming system that combines aquaculture (fish farming) with hydroponics, where fish waste provides nutrients for plants and plants help purify the water for fish.

2. What is driving the growth of the Europe aquaponics market?

Market growth is driven by increasing demand for sustainable agriculture, water-efficient farming methods, urban farming adoption, and rising awareness of organic food production.

3. Which European countries are leading in aquaponics adoption?

Germany, the Netherlands, France, the UK, and Spain are leading markets due to strong research support, advanced greenhouse infrastructure, and sustainability-focused policies.

4. What are the main components of aquaponics systems used in Europe?

Key components include fish tanks, grow beds, biofilters, water pumps, aeration systems, and monitoring and control units.

5. What crops are commonly grown using aquaponics in Europe?

Leafy greens, herbs, tomatoes, cucumbers, peppers, and strawberries are commonly grown due to high yield efficiency and strong market demand.

6. Which fish species are most commonly used in European aquaponics systems?

Tilapia, trout, carp, catfish, and perch are widely used, depending on climate conditions and local regulations.

7. How does aquaponics support sustainable agriculture in Europe?

Aquaponics reduces water usage, minimizes chemical fertilizer use, lowers environmental impact, and enables year-round food production.

8. What are the key applications of aquaponics systems in Europe?

Applications include commercial farming, urban and rooftop farming, educational and research institutions, and small-scale home systems.

9. What challenges does the Europe aquaponics market face?

Challenges include high initial setup costs, technical complexity, regulatory hurdles, and limited skilled workforce availability.

10. What is the future outlook for the Europe aquaponics market?

The market is expected to grow steadily, driven by innovation, climate-resilient farming needs, and increasing demand for locally produced food.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com