Europe Aquaponics System Market Size, Share, Trends & Growth Forecast Report, Segmented By Equipment, Production Type, Components, End User, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU), Industry Analysis Forecast From (2026 to 2034)

Europe Aquaponics System Market Size

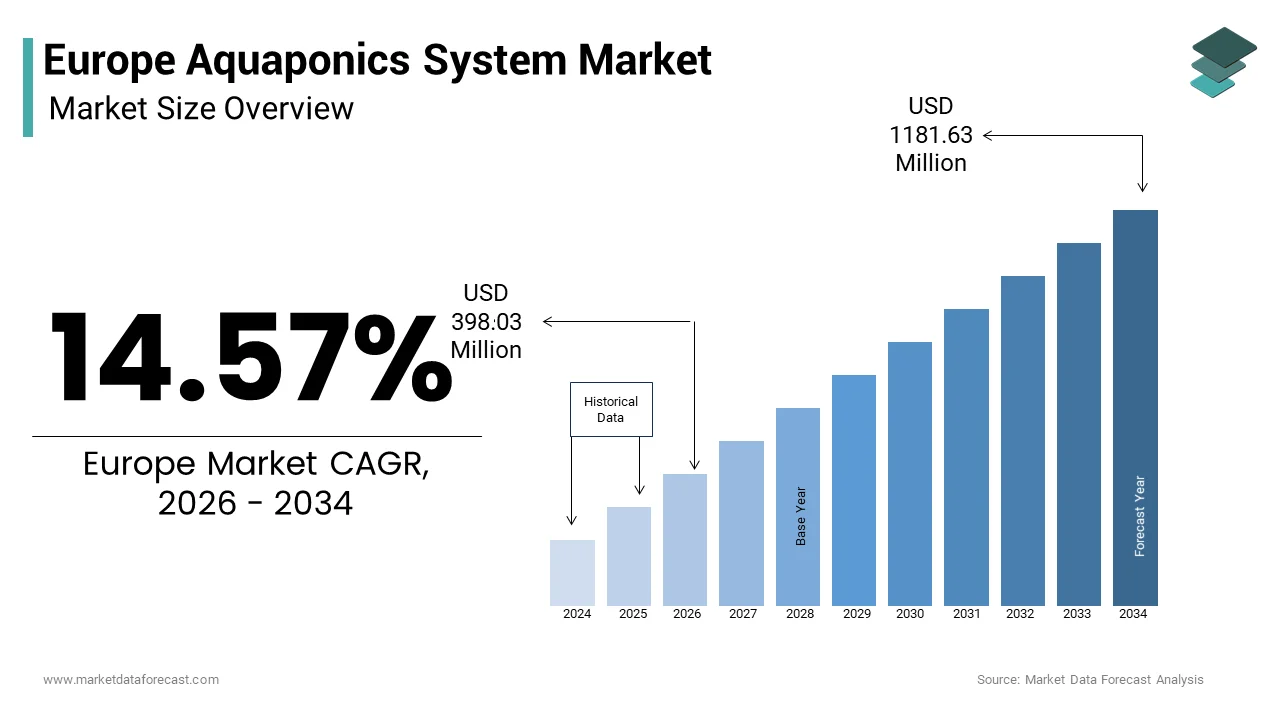

The European aquaponics system market size was valued at USD 347.41 million in 2025 and is anticipated to reach USD 398.03 million in 2026 and USD 1181.63 million by 2034, growing at a CAGR of 14.57% during the forecast period from 2026 to 2034.

An aquaponics system is a platform that symbiotically combines recirculating aquaculture and hydroponic crop cultivation within a closed-loop ecosystem. In this system, nutrient-rich water from fish tanks is channeled to grow beds where plants absorb dissolved waste as fertilizer while simultaneously purifying the water for return to the fish habitat. This dual output model yields both protein and fresh produce with minimal external inputs, making it a compelling solution for sustainable urban and peri-urban agriculture. According to the European Commission, the EU imports a notable share of its seafood and faces declining arable land availability within, agricultural soil degradation affecting twenty-five percent of European farmland, as per the Joint Research Centre. As per Eurostat, urban areas now house seventy-five percent of the EU population, creating demand for localized food systems that reduce transport emissions and enhance food security. These ecological, demographic, and policy forces position aquaponics as a strategic component of Europe’s transition toward circular and resilient food production.

An aquaponics system is a platform that symbiotically combines recirculating aquaculture and hydroponic crop cultivation within a closed-loop ecosystem. In this system, nutrient-rich water from fish tanks is channeled to grow beds where plants absorb dissolved waste as fertilizer while simultaneously purifying the water for return to the fish habitat. This dual output model yields both protein and fresh produce with minimal external inputs, making it a compelling solution for sustainable urban and peri-urban agriculture. According to the European Commission, the EU imports a notable share of its seafood and faces declining arable land availability within, agricultural soil degradation affecting twenty-five percent of European farmland, as per the Joint Research Centre. As per Eurostat, urban areas now house seventy-five percent of the EU population, creating demand for localized food systems that reduce transport emissions and enhance food security. These ecological, demographic, and policy forces position aquaponics as a strategic component of Europe’s transition toward circular and resilient food production.

MARKET DRIVERS

EU Policy Support for Circular Agriculture Drives System Adoption

The European Union’s robust policy framework promoting circular economy principles in agriculture is a key driver for Europe's aquaponics system market growth. The European Green Deal’s Farm to Fork Strategy explicitly encourages resource-efficient food production models that minimize wastewater and chemical inputs. As per the European Environment Agency, aquaponics systems reduce freshwater consumption compared to conventional agriculture and eliminate synthetic fertilizer runoff, which accounts for a portion of nitrogen pollution in EU waterways. National implementations further amplify this support, with the Netherlands allocating funds through its program to scale urban aquaponics. Similarly, Germany’s Federal Ministry of Food and Agriculture funded community aquaponics hubs under its initiative in 2023. These coordinated policy instruments provide technical validation and financial backing, and regulatory legitimacy that de-risk and municipal investment in aquaponics infrastructure across Europe.

Rising Urbanization and Demand for Hyperlocal Food Production

The region’s accelerating urbanization has intensified consumer and institutional demand for hyperlocal food systems, further propelling the expansion of the European Aquaponics market. These hyperlocal food systems shorten supply chains and enhance traceability, conditions ideally met by aquaponics. According to Eurostat, seventy-five percent of the EU population resided in urban areas in 2023, with cities experiencing growth in urban food initiatives since 2020. Municipal governments are responding by repurposing vacant lots and rooftops for integrated food production. Educational institutions are also key adopters. Furthermore, urban consumers demonstrate a strong willingness to pay premiums for locally grown produce. This convergence of spatial constraints, environmental awareness, and experiential learning is transforming aquaponics from an agricultural novelty into a functional urban infrastructure asset.

MARKET RESTRAINTS

High Initial Capital Investment and Operational Complexity

Substantial upfront costs and the technical expertise required for system management continue to restrict the growth of the European Aquaponics system market. A standard commercial-scale aquaponics unit capable of producing one ton of fish and five tons of vegetables annually requires a notable initial investment, according to the European Aquaponics Association. This includes expenses for tanks, pumps, biofilters, climate control, and water quality monitoring systems. Operational complexity further deters entry as successful management demands interdisciplinary knowledge in ichthyology, horticulture, microbiology, and fluid dynamics. Moreover, access to affordable financing remains limited as most European agricultural subsidies under the Common Agricultural Policy exclude aquaponics due to its classification outside traditional farming categories. These financial and knowledge gaps restrict market participation primarily to well-capitalized enterprises or publicly funded pilots, thereby slowing mainstream commercial diffusion.

Lack of Harmonized Regulatory Framework for Aquaponic Produce

The absence of a unified EU regulatory classification for aquaponics creates legal ambiguity that impedes market access, commercial scaling, and growth of theEuropeane aquaponics system market. Currently, a quaponic farms fall into a gray zone between aquaculture and horticulture regulations, with national authorities applying inconsistent standards for water reuse, fish welfare, and produce safety. As per the European Food Safety Authority, no specific microbiological criteria exist for vegetables grown in aquaponic systems despite their exposure to fish waste-derived nutrients. This fragmentation complicates cross-border trade and discourages investment as entrepreneurs face unpredictable compliance costs. A 2023 policy review by the European Parliament’s Committee on Agriculture acknowledged these gaps and called for a dedicated aquaponics regulatory pathway, but implementation remains pending.

MARKET OPPORTUNITIES

Integration into Urban Regeneration and Social Farming Initiatives

Its integration into urban regeneration and social inclusion programs offers new opportunities for the growth of the European aquaponics system market. This transforms underutilized spaces into productive community assets. Municipalities across Europe are repurposing abandoned industrial sites, basements, and rooftops for aquaponic farms that serve dual purposes of food production and social cohesion. These initiatives align with the EU’s Cohesion Policy, which prioritizes inclusive growth and green job creation in post-industrial regions. The European Social Fund has funded many such projects since 2021, providing vocational training in system operation, maintenance, and marketing. Aquaponics becomes a tool for urban resilience and community development by linking food sovereignty with social empowerment.

Advancement in Modular and Containerized System Designs

The development of modular and containerized systems is unlocking new prospects for the expansion of the European aquaponics system market. This advancement gives possibilities in space-constrained non-traditional settings across Europe. These prefabricated units, housed in repurposed shipping containers or standardized structures, can be rapidly installed on rooftops, parking lots, peri-urban brownfields with minimal site preparation. Companies have pioneered plug-and-play designs that integrate IoT sensors, automated feeding, and remote monitoring, enabling operation by non-specialists, scalable, turnkey solutions, lower entry barriers, reduced setup time, and offer predictable yields, which makes aquaponics viable for entrepreneurs, institutions, and municipalities seeking resilience, localized food production without major infrastructure investment.

MARKET CHALLENGES

Limited Consumer Awareness and Market Differentiation

Low consumer recognition and weak market differentiation in Europe affect premium pricing, brand loyalty, and the growth of the European aquaponics system market. This knowledge gap is exacerbated by the absence of a certified aquaponics label recognized by the EU, which prevents clear shelf communication. Retailers remain hesitant to allocate dedicated space without proven demand, as per studies. Furthermore, confusion persists between aquaponics, aquaculture, and hydroponics, leading to misinformed purchasing decisions. So, aquaponic producers struggle to convey their environmental and nutritional advantages without coordinated public education campaigns and a unified certification standard, and thereby limit market penetration beyond niche eco-conscious segments.

Technical Knowledge Gaps and Workforce Shortages

The shortage of skilled professionals, who can design o,, operate, and troubleshoot integrated aquaponic systems, constrains the expansion of the European aquaponics system market. Unlike conventional agriculture or aquaculture, re aquaponics requires a hybrid skill set spanning fish physiology, plant nutrition, la plantutrition water chemistry, and system engineering. According to sources, fewer accredited training programs in aquaponics exist across the entire EU, with most concentrated in the Netherlands and Germany. This deficit leads to suboptimal system performance, including fish mortality c,, rope failure, and energy inefficiency. Enrollment remains low at universities like BOKU in Vienna and SLU in Sweden despite their specialized courses because of limited career visibility. The sector will continue to rely on self-taught practitioners until structured vocational pathways and professional certification standards are established. This hinders scalability, reliability, nd investor confidence in this technically demanding agricultural innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.57% |

| Segments Covered | By Equipment, Production, End-user, And Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,c & Rest of Europe |

| Market Leaders Profiled | Nelson & Pade Inc., Urban Farms AG, ECF Farm Systems GmbH, Backyard Aquaponics Pty Ltd, My Aquaponics, Colorado Aquaponics, and Green Life Aquaponics. |

SEGMENTAL ANALYSIS

By Equipment Insights

The pumps and valves segment held the prominent share of 28.5% of the European Aquaponics System Market by equipment in 2024. The dominance of the pumps and valves segment is driven by their critical role in maintaining continuous water circulation between fish tanks and grow beds, a non-negotiable requirement for system functionality. Without reliable pumping infrastructure, nutrient transport,t, and waste removal collapse, leading to fish mortality and crop failure. Energy efficiency is a key consideration, with the European Commission mandating minimum efficiency standards for water pumps used in agricultural applications since 2021. In Germany and the Netherlands, a share of new aquaponics installations utilizes variable frequency drive pumps that reduce energy consumption, as per studies. Apart from these, the integration of smart valves with IoT sensors enables automated flow control based on real-time water quality data, which further strengthens the centrality of this equipment category in system reliability and operational sustainability.

The Grow Lights segment is predicted to witness the highest CAGR of 18.3% from 2025 to 2033. The expansion of the grow lights segment is driven by the expansion of indoor and vertical aquaponics farms in urban environments where natural sunlight is insufficient or unavailable. As per Eurostat, a portion of aquaponics installations in cities have been located in basements, repurposed warehouses, or multistory vertical farms, necessitating artificial lighting for photosynthesis. Advances in LED technology have dramatically improved spectral efficacy, with full-spectrum LEDs now delivering photosynthetic photon flux densities exceeding two hundred micromoles per square meter per second at fifty percent lower energy consumption than traditional high-pressure sodium lamps, according to the Technical University of Denmark. The EU’s Green Public Procurement criteria have also prioritized energy-efficient lighting in publicly funded urban agriculture projects. These technological, economic, and policy tailwinds position grow lights as the most dynamic equipment segment in Europe’s controlled environment aquaponics ecosystem.

By Production Insights

The vegetables & fruits segment accounted for a 42.5% share of the European Aquaponics System Market in 2025. Strong consumer demand for pesticide-free leafy greens, herbs, and vine crops has significantly contributed to the dominance of the vegetables & fruits segment. Lettuce, kale, basil, and cherry tomatoes are the most commonly cultivated due to their fast growth, shallow root systems,,s and high market value. According to the European Commission, urban consumers purchase significant tons of leafy greens annually, with a growing preference for locally grown produce. Aquaponically grown vegetables command a price premium in markets and specialty retailers. Municipal food security programs in cities like Copenhagen and Barcelona also prioritize vegetable production to address urban food deserts. These market, nutritional, and policy advantages make vegetables and fruits the cornerstone output of Europe’s aquaponics economy.

The Herbs and Others segment is estimated to register the fastest CAGR of 21.1% from 2025 to 2033. The rapid growth of the herbs and others segment is fueled by rising demand from high-end restaurants, gourmet retailers, and herbal supplement manufacturers for fresh aromatic and medicinal plants grown in contaminant-free environments. Basil, mi, cilantro, and parsley are particularly suited to aquaponics due to their rapid turnover and high water uptake efficiency. As per research, the businesses for fresh culinary herbs in the EU grew, with chefs increasingly specifying hyperlocal and traceable sources. The compact spatial footprint of herb cultivation also enables high-density vertical stacking, maximizing yield per square meter in space-constrained urban farms. These culinary, therapeutic, and spatial efficiencies position herbs as the highest growth production category in Europe’s value-added aquaponics landscape.

By End Users' Insights

The Commercial segment dominated theEuropeane Aquaponics System Market by capturing 53.6% share in 2024. The prominence of the commercial segment is driven by the rise of urban agri-tech enterprises supplying fresh produce and fish to local markets. These operations range from containerized farms on city rooftops to large-scale greenhouse integrations in peri-urban zones. According to research, many commercial aquaponics ventures were operational across the EU with notable annual revenues. Companies have secured contracts with supermarket chains to supply pesticide-free greens and tilapia. The economic model is further strengthened by circular revenue streams, including educational tours, workshops, and system sales. National support programs amplify viability. These enterprises benefit from short supply chains, low transport emissions, and prepremium pricingich aligns with ty mandates and consumer preferences for traceable food. This convergence of economic policy and market demand solidifies commercial operations as the dominant end-user segment.

The Education & Research segment is anticipated to witness the fastest CAGR of 24.7% during the forecast period, owing to the integration of aquaponics into formal and informal learning environments as a hands-on tool for teaching circular economy, biology, and sustainability principles. As per sources, primary and secondary schools across Finland, the Netherlands, and the Netherlands installed educational aquaponics units under national STEM initiatives. Universities are equally active with institutions operating advanced research aquaponics facilities funded by Horizon Europe grants to study nutrient cycling, fish welfare, and crop optimization. Apart from these, vocational training centers use aquaponics to teach green skills in alignment with the EU Pact for Skills. These institutional adoptions not only build future workforce capacity but also normalize aquaponics as a legitimate agricultural method, thereby accelerating broader societal acceptance and innovation diffusion.

COUNTRY ANALYSIS

Netherlands Aquaponics System Market Analysis

The Netherlands led the European Aquaponics System Market by occupying 22.5% share in 2024. Factors such as its world-class agri tech ecosystem, strong policy support, and dense urban population have primarily contributed to the domination of the Netherlands in the regional market. The country is the EU’s second-largest agricultural exporter, and it leverages its expertise in controlled environment agriculture to pioneer scalable aquaponics solutions. The Dutch government’s initiative hhhasnvestedamount since 2020 in urban food innovation, including aquaponics hubs in Rotterdam and Wageningen. Aquaponics is part of Dutch urban agriculture and sustainable innovation. The Netherlands actively explores and employs aquaponics as a sustainable method for food production, particularly in urban areas. Research institutions like Wageningen University collaborate closely with companies to develop climate-resilient crop fish combinations. Apart from these, the Netherlands hosts Europe’s largest aquaponics trade fair, GreenTech Amsterdam, which attracts over ten thousand professionals annually. These synergies of innovation policy and market access make the Netherlands the undisputed leader in European aquaponics development and commercialization.

Germany Aquaponics System Market Analysis

Germany was the second largest in the European aquaponics system market by capturing 18.3% share in 2024. The growth of Germany is fuelled by robust public funding, strong engineering capabilities, and high consumer demand for sustainable food. Many commercial and community aquaponics projects were active in Germany, according to sources, and allocated funds under its Sustainable Urban Food Systems program. The country’s Energiewende energy transition policy incentivizes renewable-powered urban agriculture with solar-integrated container farms proliferating in Berlin, Hamburg, and Munich. German engineering firms have developed precision control systems for pH, dissolved oxygen, andtemperature that are now exported across Europe. Furthermore, consumer awareness is high. The presence of research clusters like the Berlin Food Network and strong vocational training in green technologies further sustains Germany’s prominence in both technological advancement and practical implementation of aquaponics.

France Aquaponics System Market Analysis

France grew steadily in tthe Europeanaquaponics system market due to national food sovereignty strategies and urban regeneration policies. The French Ministry of Agriculture’s Innovation Agricole program funded forty-seven aquaponics projects focusing on repurposed industrial sites in Lyon, Marseille, and Lille. As per research, a portion of Frenchmunicipalities haveh adopted urban agriculture charters that include aquaponics as a tool for social inclusion and food resilience. The country also leads in educational integration, with over nine hundred schools operating aquaponics. Consumer demand is strong in metropolitan areas where organic and local food markets have grown. Besides, French startups like Aquaponie France have developed modular systems using recycled materials, aligning with the national circular economy roadmap. These coordinated efforts across public policy education and entrepreneurship position France as a dynamic and socially embedded aquaponics market in Western Europe.

United Kingdom Aquaponics System Market Analysis

The United Kingdom expanded moderately in theEuropeane aquaponics system market owing to post-Brexit emphasis on domestic food security and climate-resilient agriculture. Cities have integrated aquaponics into social housing and community center redevelopment projects to address food poverty and skills gaps. The UK’s strong academic base conducts cutting-edge research on cold water aquaponics suitable for temperate climates. Consumer trends also support growth. Despite regulatory uncertainty pppost-Brexit’socus on self-sufficiency and green jobs ensures sustained momentum in aquaponics adoption across commercial and community sectors.

Sweden Aquaponics System Market Analysis

Sweden is likely to grow in the European aquaponics system market from 2025 to 2033 due to its integration of aquaponics into national sustainability and education frameworks. Most municipalities in Sweden are integrating aquaponics systems into their local climate plans to promote sustainable food production, according to sources. Cities such as Stockholm and Gothenburg are using these facilities to supply fresh produce to public institutions, including schools and care centers. The national agricultural authority is also offering financial support for urban farming projects to encourage broader adoption of green infrastructure, as per research. Education is a cornerstone. These systemic policies, educational and infrastructural supports, make Sweden a model for public sector-led aquaponics deployment in Northern Europe.

COMPETITIVE LANDSCAPE

ThEuropeanpe Aquaponics System Market features a fragmented yet dynamic competitive landscape comprising specialized agri-tech startups, engineering firms, and social enterprises. Competition is not primarily price-based but revolves around system reliability, energy efficiency, integration with urban infrastructure, and alignment with public policy goals. Established players like ECF Farmsystems and UrbanFarmers lead in commercial scalability, while organizations such as Back to the Roots dominate the educational and community segments. Barriers to entry remain moderate due to high initial capital costs and technical complexity, but are offset by EU funding opportunities and growing municipal interest. The absence of harmonized regulations creates both challenges and opportunities as early movers shape standards through pilot projects. Differentiation hinges on proprietary control systems,s, crop fish combination,n, and circular design features. As urban food security gains poltractionacti, c competition is increasingly defined by the ability to deliver turnkey solutions that combine food production, education, and social impact within constrained urban environments.

KEY MARKET PLAYERS

A few of the market players in the EEuropeanaquaponics system market include

- Nelson & Pade Inc.

- Urban Farms AG

- Back to the Roots B V

- ECF Farm Systems GmbH

- Backyard Aquaponics Pty Ltd

- My Aquaponics

- Colorado Aquaponics

- Green Life Aquaponics.

Top Players In The Market

- ECF Farmsystems GmbH is a leading innovator in theEuropeane Aquaponics System Market, headquartered in Berlin, Germany. The company designs and deploys modular containerized aquaponics farms that integrate fish and vegetable production for urban environments. ECF’s systems are operational in over fifteen countries and have been installed in supermarkets, schools, and municipal projects across Europe. ECF also partnered with Edeka Group to supply fresh produce from in-store aquaponics units in Berlin and Hamburg. These initiatives demonstrate ECF’s commitment to scalable urban food solutions and deep integration into European retail and community food systems.

- UrbanFarmers AG is a Swiss-based pioneer in commercial aquaponics with a strong presence in Western and Northern Europe. The company specializes in rooftop and greenhouse integrated systems that produce tilapia and leafy greens for urban markets. UrbanFarmers’ flagship project at the Basel Dreispitz site supplies over two tons of vegetables and five hundred kilograms of fish annually to local restaurants and retailers. UrbanFarmers also collaborated with ETH Zurich on nutrient optimization research and expanded its training academy to certify operators across Germany and the Netherlands. These actions reinforce its role as a technology and knowledge leader in sustainable urban agriculture.

- Back to the Roots BV is a Netherlands-based company driving aquaponics adoption through education and modular system design. Originally founded as a social enterprise, the company now supplies turnkey aquaponics units to over five hundred schools, municipalities, and community centers across Europe. Its classroom scale systems are used in national STEM programs in Sweden, Finland, and Belgium to teach circular economy principles. The company also secured funding from the EU’s Urban Innovative Actions program to deploy community aquaponics hubs in Rotterdam and Utrecht. These efforts position Back to the Roots as a bridge between education, social impact, and practical food system innovation.

Top Strategies Used By The Key Market Participants

Key players in theEuropeane Aquaponics System Market primarily focus on developing modular and containerized systems, forging partnerships with municipalities and retailers, integrating smart monitoring technologies, securing public funding through EU and national grants,,s and embedding educational components to build awareness and workforce capacity. Companies invest in energy-efficient designs that align with the European Green Deal and leverage urban regeneration policies to access underutilized spaces. Strategic collaborations with supermarkets, universities, and vocational institutions enhance market validation and user training. Besides, firms pursue certifications for organic or sustainable production to differentiate their output and command premium pricing. These multifaceted strategies address technical, economic, and social barriers to scale while positioning aquaponics as a viable component of Europe’s resilient food future.

MARKET SEGMENTATION

This research report on the European Aquaponics system market is segmented and sub-segmented into the following categories.

By Equipment

- Pumps and valves

- Water heaters

- Grow lights

- Fish purge systems

- Water quality testing

- Aeration systems

- Others

By Production Type

- Fish

- Vegetables & fruits

- Herbs and others

- Components

- Rearing tanks

- Biofilter

- Settling basin

- Sump

- Hydroponics subsystem

- Others

By End-users

- Commercial

- Education & Research

- Household

- Community

- Y-o-Y Growth Analysis, By End-user

- Market Attractiveness Analysis, By End-user

- Market Share Analysis, By End User

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is aquaponics, and why is it gaining attention in Europe?

Aquaponics is a closed-loop farming method that combines aquaculture (fish farming) with hydroponics (soilless crop cultivation), using fish waste as natural fertilizer. It’s attracting interest in Europe due to its water efficiency, zero chemical inputs, and alignment with circular economy principles.

Which European countries are leading in aquaponics adoption?

The Netherlands, Germany, France, Spain, and the UK are at the forefront, supported by urban farming initiatives, research institutions, and EU funding for sustainable food innovation.

How does EU policy support aquaponics development?

While not yet fully classified under organic or conventional farming rules, aquaponics benefits from Horizon Europe grants, CAP eco-schemes, and national programs promoting resource-efficient food production and urban agriculture.

What are the main applications of aquaponics in Europe?

Most systems focus on high-value leafy greens (lettuce, kale), herbs (basil, mint), and freshwater fish like tilapia or trout—primarily serving local restaurants, farmers’ markets, and community food projects.

Are commercial-scale aquaponics farms viable in Europe?

While still niche, larger operations are emerging—especially in repurposed industrial buildings—but face challenges in energy costs, regulatory clarity, and achieving consistent profitability without subsidies.

Who are the key players in the European aquaponics market?

Notable companies include ECF Farmsystems (Germany), UrbanFarmers (Switzerland), Back to the Roots (France), and InFarm (which explores integrated models)—many combining modular design, IoT monitoring, and education services.

How is technology improving aquaponics efficiency?

Smart sensors for pH, dissolved oxygen, and nutrient levels—paired with AI-driven automation—help optimize fish health and plant growth while reducing labor and resource waste.

What are the biggest barriers to market growth?

High startup costs, complex permitting (due to dual regulation of fish and crops), limited consumer awareness, and competition from established greenhouse and hydroponic producers slow widespread adoption.

Is aquaponics recognized under EU organic standards?

Not currently—EU organic regulations require soil-based cultivation, excluding hydroponic and aquaponic systems. However, advocacy groups are pushing for reform to include soilless sustainable methods.

What’s the market outlook for 2025–2030?

The Europe aquaponics system market is expected to grow steadily, driven by urbanization, food security concerns, and demand for hyperlocal, chemical-free produce—though scalability hinges on policy evolution and cost reductions in renewable energy integration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com