- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Europe Autoimmune Monoclonal Antibodies Market Summary

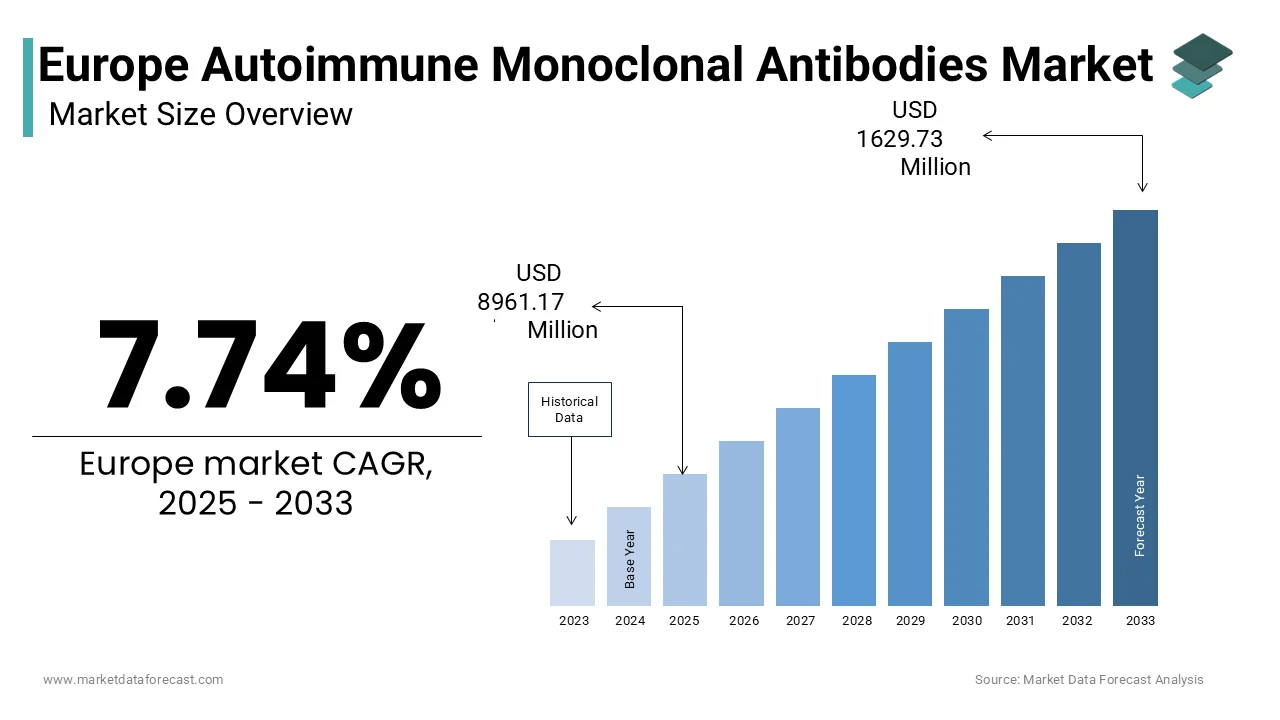

The Europe autoimmune monoclonal antibodies market was valued at USD 8.32 billion in 2024, is estimated to reach USD 8.96 billion in 2025, and is projected to grow to USD 16.30 billion by 2033, registering a CAGR of 7.74% from 2025 to 2033, driven by rising autoimmune disease prevalence, early biologic adoption in treatment algorithms, regulatory acceleration for high-need therapies, and expanding use of patient-centric biologic delivery formats.

Key Market Highlights

- 2024 value: USD 8.32 billion

- 2025 (est): USD 8.96 billion

- 2033 (forecast): USD 16.30 billion

- CAGR (2025–2033): 7.74%

Quick Growth Drivers

- Rising diagnosed prevalence of rheumatoid arthritis, IBD, multiple sclerosis, and lupus

- Earlier inclusion of biologics in European treatment guidelines

- EMA accelerated and PRIME approval pathways

- Strong clinical outcomes from targeted cytokine and receptor inhibition

- Expansion of self-administered subcutaneous monoclonal antibodies

Principal Restraints

- Strict pricing and reimbursement controls across EU healthcare systems

- Delayed reimbursement approvals post-EMA authorization

- Step-therapy requirements limiting early biologic access

- Intensifying biosimilar competition eroding originator pricing power

High-Value Opportunities

- Growth of subcutaneous and at-home biologic administration

- Increasing integration of real-world evidence (RWE) in payer decisions

- Expansion into previously underserved autoimmune indications

- Lifecycle management via label expansion and pediatric approvals

Key Market Challenges

- Complex biologic manufacturing and cold-chain logistics

- Supply vulnerabilities from batch failures and energy disruptions

- Fragmented diagnostic and treatment protocols across EU countries

- High cost of maintaining biologic production scalability

Fastest-Growing Segments

- Humanized monoclonal antibodies: ~13.3% CAGR — improved safety & lifecycle extension

- Systemic lupus erythematosus (SLE): ~14.0% CAGR — first disease-specific biologics

- Self-injectable biologics: fastest emerging delivery format

Regional Leadership & Dynamics

- Germany (22.3%) — rapid access, strong reimbursement, biologic manufacturing base

- France — early access via temporary authorization and centralized hospitals

- United Kingdom — NICE-led evidence-based adoption and registry strength

- Italy — national pricing reforms improving biologic penetration

- Spain — biosimilar-led savings reinvested into novel biologics

What Wins Commercially (Competitive Edge)

- Fully human and humanized antibody platforms

- EMA-aligned accelerated approval strategies

- Strong real-world registry data supporting reimbursement

- Subcutaneous delivery with digital adherence tools

- Regional manufacturing and supply-chain resilience

Top Strategic Ask for Executives

- Prioritize next-generation human and humanized antibodies

- Expand self-administration and device-integrated biologics

- Leverage RWE for faster payer acceptance

- Balance innovation with biosimilar defense strategies

- Strengthen European manufacturing and cold-chain infrastructure

Leading Players

Some of the companies that are playing a dominating role in the Europe autoimmune monoclonal antibodies market include:

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson

- Novartis AG

- GlaxoSmithKline plc

- AstraZeneca plc

- Bristol-Myers Squibb

- Amgen Inc.

- Biogen Inc.

- UCB

- Takeda Pharmaceutical Company Ltd.

Europe Autoimmune Monoclonal Antibodies Market Size

The europe autoimmune monoclonal antibodies market size was valued at USD 8317.40 million in 2024, is expected to have 7.74% CAGR from 2025 to 2033, and be worth USD 1629.73 million by 2033 from USD 8961.17 million in 2025.

Monoclonal antibodies engineered to modulate or suppress aberrant immune responses have become pivotal in managing chronic autoimmune conditions. These biopharmaceuticals specifically target immune system components such as cytokines or cell surface receptors involved in inflammatory pathways, offering precision therapy for diseases like rheumatoid arthritis, psoriasis, Crohn's disease, and multiple sclerosis. The European autoimmune monoclonal antibodies market encompasses therapeutic agents approved and utilized within the European Economic Area, where clinical efficacy and regulatory frameworks shape access and adoption. According to the European Medicines Agency, biologics,s including monoclonal antibodies, es have received conditional or full marketing authorization for autoimmune indications as of early 2024. The prevalence of autoimmune disorders continues to rise, with the European League Against Rheumatism noting that a significant proportion of the European population suffers from at least one autoimmune disease. As per the World Health Organization Regional Office for Europe, the burden of non-communicable inflammatory diseases has intensified due to aging demographics and environmental triggers, reinforcing the necessity for advanced biologic interventions. This therapeutic segment remains integral to Europe’s strategy in achieving long-term disease control and improving patients’ quality of life through scientifically validated immunomodulatory mechanisms.

MARKET DRIVERS

Expanding Diagnosed Prevalence of Complex Autoimmune Disorders Fuels Therapeutic Demand

The rising prevalence of multifactorial autoimmune diseases across Europe continues to amplify demand for advanced biologics such as monoclonal antibodies, which is one of the key factors propelling the growth of the European autoimmune monoclonal antibodies market. According to the European Crohn’s and Colitis Organisation, more than 3 million people in Europe live with inflammatory bowel disease (IBD), with prevalence steadily increasing over the past decade. While incidence rates vary by country, Western Europe has reported sustained growth in Crohn’s disease and ulcerative colitis diagnoses. The Atlas of MS (Multiple Sclerosis International Federation, 2023) confirms that Europe has the highest regional prevalence of multiple sclerosis globally, with over 1 million individuals affected. These figures reflect improved diagnostic protocols, heightened awareness, and broader access to specialist care. Early and accurate diagnosis enablthe es timely initiation of monoclonal antibody therapy, which is often reserved for moderate to severe disease stages where conventional treatments fail. National health systems in Germany, France, and the United Kingdom have updated clinical guidelines to incorporate biologics earlier in treatment algorithms, supported by real‑world evidence of sustained remission. As a result, the expanding pool of eligible patients directly enlarges the addressable market for autoimmune monoclonal antibodies, underpinning sustained demand despite pricing pressures or reimbursement complexities.

Accelerated Regulatory Endorsement Pathways for High‑Need Biologics Enhance Market Accessibility

Europe’s progressive regulatory mechanisms for biologics targeting high unmet medical needs serve as a critical enabler for monoclonal antibody adoption in autoimmune care, which is further favouring the European autoimmune monoclonal antibodies market expansion. The European Medicines Agency (EMA) has implemented adaptive pathways and PRIME (Priority Medicines) schemes that expedite evaluation and approval timelines for innovative therapies. According to the EMA’s 2023 annual report, biologics represented a significant share of medicines granted accelerated assessment, particularly those indicated for immune‑mediated inflammatory diseases. This regulatory agility ensures faster patient access to cutting‑edge monoclonal antibodies such as those targeting interleukin‑23 or Janus kinase pathways. Furthermore, the harmonized approval process across the EU eliminates redundant national reviews, allowing manufacturers to scale commercialization efficiently. Countries such as Sweden and the Netherlands have integrated health technology assessment bodies that align reimbursement decisions with EMA milestones, reducing time to market by several months compared to previous decades. The European Commission’s Innovative Medicines Initiative has also funded cross‑border consortia generating robust clinical data to support label expansions. These structural advantages incentivize investment in autoimmune biologic pipelines and ensure clinically validated therapies reach patients without undue delay, reinforcing therapeutic uptake across diverse European healthcare systems.

MARKET RESTRAINTS

Stringent Pricing and Reimbursement Constraints Limit Broad Utilization

Despite strong clinical efficacy, the high acquisition cost of monoclonal antibodies encounters resistance within Europe’s cost‑conscious healthcare frameworks, which is a major restraint to the growth of the European autoimmune monoclonal antibodies market. National pricing authorities in Germany, France, and Italy enforce rigorous health technology assessments that often result in delayed or partial reimbursement. According to the European Observatory on Health Systems and Policies (2023), biologic therapies for autoimmune conditions face an average reimbursement approval lag of 9–14 months following EMA authorization. Several countries impose restrictive treatment criteria that limit monoclonal antibody use exclusively to patients who have failed multiple conventional therapies, thereby shrinking the eligible patient pool. In Spain, rheumatology guidelines confirm that biologics are typically reserved for patients who fail conventional DMARDs, which limits access to roughly one‑third of rheumatoid arthritis patients. Budget impact thresholds further hinder adoption; in the United Kingdom, NICE applies a cost‑effectiveness threshold of £20,000–£30,000 per QALY, and biologics exceeding this threshold have historically faced rejection or restricted use. These fiscal gatekeeping mechanisms, while aimed at sustainability, inadvertently delay patient access and constrain market expansion despite compelling clinical evidence.

Biosimilar Competition Erodes Commercial Exclusivity and Price Integrity

The proliferation of biosimilars across Europe exerts downward pricing pressure and challenges the commercial viability of originator monoclonal antibodies, which further hampers the regional market expansion. Once patent protection expires, multiple biosimilar entrants rapidly capture market share due to aggressive pricing and supportive procurement policies. According to the European Commission’s 2024 Biosimilars Report, biosimilar versions of infliximab and adalimumab achieved average market penetration of around 65% across the EU within three years of launch. This competitive intensity forces originator companies to slash prices significantly. In Germany, adalimumab’s reference product price declined by more than 50% between 2018 and 2023 following biosimilar introductions. National payers actively incentivize biosimilar substitution through preferential formulary placement and volume‑based discounts. According to OECD data, biosimilar uptake in autoimmune indications reduced per‑patient annual biologic expenditure by 30–40% in countries such as Denmark and the Netherlands. While this enhances affordability, it simultaneously compresses innovation incentives and limits reinvestment in next‑generation monoclonal antibodies, thereby reshaping the market’s long‑term growth trajectory.

MARKET OPPORTUNITIES

Emergence of Subcutaneous Self‑Administration Platforms Enhances Patient Adherence and Market Reach

The shift toward patient‑centric delivery formats, particularly subcutaneous self‑administered monoclonal antibodies, is a notable opportunity for the European autoimmune monoclonal antibodies market. These formulations reduce dependency on clinical infusion centers, improve treatment continuity, and elevate quality of life. According to EFPIA (European Federation of Pharmaceutical Industries and Associations), a majority of newly approved autoimmune monoclonal antibodies since 2020 have featured subcutaneous delivery options. Real‑world data from Sweden’s national rheumatology registry confirms adherence rates above 85% for self‑injectable biologics compared to ~68% for intravenous alternatives. Pharmaceutical companies have responded by investing in user‑friendly injector devices and digital adherence tools integrated with smartphone applications. In France, the Haute Autorité de Santé has explicitly endorsed subcutaneous routes in updated psoriatic arthritis guidelines due to demonstrated improvements in persistence and reduced hospital visits. This modality also aligns with Europe’s post‑pandemic emphasis on decentralized care models. Consequently, the convenience and autonomy afforded by self‑administration are expanding the eligible demographic to include working adults and rural residents who previously faced logistical barriers to biologic therapy.

Integration of Real‑World Evidence in Regulatory and Reimbursement Decision Making Opens Strategic Pathways

Europe’s increasing reliance on real‑world evidence (RWE) is reshaping market access strategies for autoimmune monoclonal antibodies by validating long‑term effectiveness beyond controlled trials, which is another prominent opportunity for the European autoimmune monoclonal antibodies market. According to the European Network for Health Technology Assessment (EUnetHTA), more than 30 European countries now incorporate RWE into at least half of biologic reimbursement evaluations. The British Society for Rheumatology’s Biologics Register, tracking over 20,000 patients since 2001, has provided pivotal insights into the durability and safety of monoclonal antibodies in diverse clinical settings, directly influencing NICE recommendations. Similarly, Germany’s Gemeinsamer Bundesausschuss (G‑BA) mandates post‑authorization safety studies that feed into benefit assessments. This evidence‑rich environment allows manufacturers to demonstrate value through outcomes such as work productivity, retention,n and hospitalization avoidance. Data from the Nordic Arthritis Registry showed a 40% reduction in joint surgery rates among rheumatoid arthritis patients treated with specific monoclonal antibodies over five years. By bridging the gap between trial efficacy and real‑world performance, such data strengthens payer confidence and accelerates adoption.

MARKET CHALLENGES

Complex Manufacturing and Cold Chain Logistics Impede Supply Chain Resilience

The production of monoclonal antibodies involves highly sophisticated biomanufacturing processes that are vulnerable to technical disruptions and capacity limitations, which is a major challenge to the growth of the European autoimmune monoclonal antibodies market. These large‑molecule therapeutics require precise cell culture conditions, extensive purification steps, and rigorous quality control, resulting in extended lead times and elevated production costs. According to the European Biopharmaceutical Review, a single batch failure in a bioreactor can lead to losses exceeding €10–15 million and delay supply by 3–6 months. Furthermore, most monoclonal antibodies are temperature‑sensitive, which demands uninterrupted cold‑chain logistics from manufacturing sites to end users. As per the EMA monitoring reports, ~12% of biologic shipments in Southern and Eastern Europe experienced temperature excursions in 2023, risking product stability and patient safety. Rural healthcare facilities often lack adequate cold storage infrastructure, constraining distribution reach. Geopolitical events such as energy shortages or trade restrictions further exacerbate vulnerabilities, as seen during the 2022 natural gas crisis that threatened bioreactor operations in Germany. These supply chain complexities not only increase operational risk but also limit the ability to respond swiftly to surges in demand or new indication approvals.

Heterogeneous Diagnostic and Treatment Protocols Across European Nations Create Market Fragmentation

The absence of standardized autoimmune disease management approaches across European countries introduces significant variability in monoclonal antibody uptake and reimbursement eligibility, which further challenges the expansion of the European autoimmune monoclonal antibodies market. Clinical guidelines differ markedly in diagnostic criteria, treatment escalation thresholds, and preferred biologic sequences. According to a 2023 comparative analysis by EULAR (European Alliance of Associations for Rheumatology), 27 distinct treatment algorithms exist for rheumatoid arthritis across the EU. In Italy, patients must demonstrate failure of two synthetic DMARDs before biologic access, whereas in Norway, monoclonal antibodies may be considered after one. Such disparities stem from differing interpretations of clinical evidence, local epidemiology, and health budget priorities. Consequently, pharmaceutical companies face complex market entry strategies requiring country‑specific health economic dossiers and stakeholder engagement. Delays in aligning national protocols with pan‑European recommendations further fragment commercial execution. This lack of harmonization not only impedes equitable patient access but also inflates operational costs for manufacturers seeking to navigate divergent regulatory and prescriber expectations, ultimately diluting market potential despite uniform scientific validation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Source, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | GlaxoSmithKline plc (U.K.), AstraZeneca plc (U.K.), F. Hoffmann-La Roche Ltd. (Switzerland), Bristol-Myers Squibb (U.S.), Johnson & Johnson (U.S.), Innovent Biologics, Inc. (China), Takeda Pharmaceutical Company Ltd. (Japan), Amgen Inc. (U.S.), Biogen Inc.(U.S.), and UCB Company (Belgium). |

SEGMENTAL ANALYSIS

By Source Insights

The human monoclonal antibodies segment commanded the highest share of 55.8% of the regional market in 2024. The dominance of the human monoclonal antibodies segment in this regional market is driven by their superior clinical tolerability, reduced immunogenicity, and enhanced pharmacokinetic profiles compared with murine, chimeric, or humanized counterparts. Human antibodies closely mimic natural immune proteins, minimizing the risk of anti‑drug antibody formation, which is a critical consideration in chronic autoimmune management where long‑term therapy is standard. According to the European Medicines Agency (EMA), more than 70% of newly approved monoclonal antibodies for autoimmune indications between 2020 and 2024 were fully human constructs. Regulatory preference for human sequences also influences market dynamics, as agencies increasingly require robust immunogenicity data before granting marketing authorization. Furthermore, leading pharmaceutical developers have pivoted their pipelines toward fully human platforms such as phage display and transgenic mouse technologies, accelerating commercial availability. Patient adherence improves significantly with human antibodies due to fewer infusion‑related reactions, a factor reinforced by national rheumatology registries in Germany and Sweden showing discontinuation rates below 6% for human agents versus 12% for chimeric alternatives. These combined clinical and commercial advantages solidify the human segment’s leadership across Europe’s autoimmune therapeutic landscape.

The humanized monoclonal antibodies segment is anticipated to register a promising CAGR of 13.3% over the forecast period, owing to the strategic reformulation of earlier-generation chimeric agents into humanized variants to extend patent life and improve safety without compromising efficacy. Humanized antibodies retain the antigen‑binding specificity of murine origins while replacing ~90% of the protein framework with human sequences, striking a balance between manufacturability and reduced immunogenicity. As per EMA records, 5 humanized monoclonal antibodies received new indication approvals for autoimmune diseases in Europe between 2022 and 2024, including expanded use in pediatric populations. Academic medical centers in France and the Netherlands are leading clinical trials exploring humanized antibodies in treatment‑refractory lupus nephritis, with early phase results showing complete renal response in 34% of patients after six months. Payers also view humanized agents as cost‑effective alternatives to fully human biologics, particularly in middle‑income European countries such as Poland and Portugal, where budget constraints favor mid‑tier pricing. This blend of scientific refinement, regulatory receptivity, and economic pragmatism underpins the segment’s rapid uptake across diverse European healthcare settings.

By Application Insights

The rheumatoid arthritis segment captured 41.4% of the regional market share in 2024. The leading position rheumatoid arthritis segment in the European market is driven by the high disease prevalence, well‑established treatment algorithms incorporating biologics, and extensive insurance coverage. The European League Against Rheumatism (EULAR) reports that over 3 million individuals in the EU live with rheumatoid arthritis, with nearly 40% requiring biologic disease‑modifying antirheumatic drugs due to inadequate response to conventional therapy. National health systems in Germany, the UK, and the Netherlands have integrated monoclonal antibodies into first‑line biologic protocols following methotrexate failure to ensure broad and early access. Furthermore, long‑term registry data such as the British Society for Rheumatology Biologics Register demonstrate that monoclonal antibody use in rheumatoid arthritis correlates with a 50% reduction in joint erosion progression over two years. The availability of multiplemechanisms of action enables personalized treatment, enhancing clinical outcomes and reinforcing physician preference. These structural and clinical advantages sustain rheumatoid arthritis as the cornerstone application for autoimmune monoclonal antibodies across Europe.

The systemic lupus erythematosus (SLE) segment is the fastest-growing application segment and is predicted to witness the fastest CAGR of 14.04% over the forecast period. This surge follows the 2022 EMA approval of the first monoclonal antibody specifically indicated for lupus nephritis, a severe renal manifestation affecting up to 60% of lupus patients. Before this milestone, treatment relied heavily on off‑label corticosteroids and immunosuppressants with significant toxicity profiles. According to the European Reference Network on Rare Rheumatic Diseases, lupus incidence in Southern Europe has risen by 18% since 2015, particularly among women of childbearing age. Real‑world evidence from the French Lupus Cohort shows that monoclonal antibody treatment reduces flare frequency by 52% and hospitalization rates by 37% within the first year. Moreover, ongoing Phase III trials in Italy and Sweden are evaluating next‑generation antibodies targeting type I interferon pathways, a mechanism implicated in lupus pathogenesis. As awareness grows and diagnostic precision improves through autoantibody panels and renal biomarkers, more patients are identified as candidates for biologic intervention, catalyzing unprecedented market expansion in this historically underserved indication.

By End User Insights

The hospitals and clinics segment led the market by holding the dominating share of the European autoimmune monoclonal antibodies market in 2024. The dominating position of the hospitals and clinics segment in this regional market is driven by the centralized nature of biologic administration, which often requires clinical supervision due to infusion protocols, monitoring for acute reactions, and integration with multidisciplinary care teams. In countries such as Germany and France, over 90% of monoclonal antibody doses for autoimmune conditions are delivered in hospital‑based rheumatology or dermatology infusion units. According to Eurostat, Europe has more than 8,000 specialized autoimmune care centers, with the majority embedded within public or university‑affiliated hospitals that manage complex chronic cases. Reimbursement frameworks further reinforce this model; in the UK, the National Health Service bundles biologic costs into hospital activity tariffs, discouraging outpatient or home‑based delivery except for subcutaneous formulations. Additionally, hospitals maintain direct procurement contracts with manufacturers, ensuring supply stability and access to post‑marketing safety programs. The concentration of diagnostic capabilities, therapeutic expertise, and regulatory compliance infrastructure within hospital settings makes them the natural hub for monoclonal antibody deployment across Europe’s fragmented but high‑standard healthcare landscape.

The diagnostic laboratories segment is estimated to exhibit a CAGR of 10.3% over the forecast period, owing to the rising integration of monoclonal antibodies as critical reagents in immunoassays, flow cytometry, and companion diagnostic platforms that guide therapeutic selection. Laboratories increasingly utilize monoclonal antibodies to detect autoantibodies such as anti‑dsDNA or anti‑CCP, which inform both diagnosis and biologic eligibility. As per the European Federation of Clinical Chemistry and Laboratory Medicine (EFCLM), over 60% of tertiary care laboratories in Europe adopted monoclonal antibody‑based diagnostic kits between 2021 and 2023 to improve assay specificity and reduce false positives. National screening initiatives also contribute; in Sweden, a nationwide program for early rheumatoid arthritis identification relies on monoclonal antibody reagents to process over 200,000 serum samples annually. Furthermore, the EU’s In Vitro Diagnostic Regulation mandates higher analytical validation standards, driving demand for highly consistent monoclonal reagents over polyclonal alternatives. As precision medicine gains traction, diagnostic labs are evolving from passive testing venues to active decision‑support partners, embedding monoclonal antibodies into predictive and monitoring workflows that directly influence treatment pathways.

COUNTRY LEVEL ANALYSIS

Germany Autoimmune Monoclonal Antibodies Market Analysis

Germany stood as the largest national contributor to theEuropeane autoimmune monoclonal antibodies market by holding a 22.3% share in 2024. The leading position of Germany in the European market is driven by its robust biopharmaceutical infrastructure, high disease awareness, and rapid adoption of innovative biologics through the early benefit assessment process overseen by the Federal Joint Committee. As per the German Society for Rheumatology, over 800,000 autoimmune patients received biologic therapies in 2024, the highest volume in Europe. The statutory health insurance system covers nearly all approved monoclonal antibodies without prior step therapy requirements, facilitating immediate patient access. Germany also hosts over 30 clinical trial sites dedicated to next‑generation autoimmune biologics, accelerating real‑world evidence generation. Manufacturing presence from companies like Boehringer Ingelheim and partnerships with Charité Berlin further strengthen the ecosystem. With over 400 specialized rheumatology centers and digitized health records enabling treatment tracking, Germany maintains unmatched scale and sophistication in monoclonal antibody deployment.

France Autoimmune Monoclonal Antibodies Market Analysis

France commanded the second leading share of the European market in 2024. The prominent position of France in the European market is attributed to the progressive reimbursement policies and high physician engagement. Temporary authorization for use is granted to promising monoclonal antibodies while full assessment proceeds, enabling patient access within six months of EMA approval. As per the French National Health Insurance Fund, over 450,000 patients received autoimmune monoclonal antibody therapy in 2023, with rheumatoid arthritis and psoriasis accounting for 70% of use. The country’s centralized hospital network, particularly Assistance Publique Hôpitaux de Paris, ensures standardized protocols and pharmacovigilance. France also leads in biosimilar transition programs; data from the National Agency for Medicines and Health Products Safety shows that over 60% of infliximab prescriptions shifted to biosimilars without compromising outcomes. Ongoing investments in biologic registries and patient‑reported outcome platforms further enhance therapeutic personalization, solidifying France’s role as a high‑volume, high‑quality market.

United Kingdom Autoimmune Monoclonal Antibodies Market Analysis

The United Kingdom is anticipated to grow at a promising CAGR in the European market during the forecast period, owing to the rigorous evidence‑based adoption guided by NICE. Despite post‑Brexit regulatory autonomy, the UK maintains alignment with EMA approvals, ensuring timely access to new agents. According to the British Society for Rheumatology, over 300,000 patients in England alone received biologic therapy for autoimmune conditions in 2023, with treatment initiation rates increasing by 9% annually since 2020. The NHS’s specialized commissioning model centralizes biologic procurement, achieving cost efficiency while ensuring equitable distribution. The UK also excels in post‑marketing surveillance; as per the Yellow Card Scheme, fewer than two serious adverse events per 10,000 patient‑years were recorded for newer human monoclonal antibodies. Academic centers like Oxford and Cambridge drive translational research, with recent studies validating biomarker‑guided biologic selection in Crohn’s disease. This combination of disciplined evaluation, robust monitoring, and research integration sustains the UK’s strategically influential position.

Italy Autoimmune Monoclonal Antibodies Market Analysis

Italy is projected to account for a notable share of the European market during the forecast period owing to the high prevalence of autoimmune disorders and recent policy reforms, according to the Italian Medicines Agency. Autoimmune diseases affect over 4 million Italians, with rheumatoid arthritis and multiple sclerosis showing above‑average incidence in Southern regions. Historically constrained by regional reimbursement disparities, Italy implemented a national uniform pricing framework for biologics in 2022, reducing access gaps between North and South. As per the Italian Society of Rheumatology, biologic prescriptions rose by 21% between 2021 and 2023, particularly in centers of excellence like Milan and Rome. Italy also participates in the European Reference Network for Rare Immunological Diseases, facilitating cross‑border diagnosis and treatment of complex cases. Patient advocacy groups have successfully lobbied for faster approval of subcutaneous formulations, improving adherence in elderly populations. With over 200 biologic infusion centers upgraded since 2020 and telemedicine integration expanding rural reach, Italy is transitioning from a fragmented to a more cohesive autoimmune care environment.

Spain Autoimmune Monoclonal Antibodies Market Analysis

Spain is expected to grow at a healthy CAGR in theEuropeane autoimmune monoclonal antibodies market during the forecast period. Spain is notable for cost containment strategies that enable sustainable biologic use, according to the Spanish Agency of Medicines and Medical Devices. Biosimilar substitution is promoted as a cornerstone of biologic policy, achieving over 70% biosimilar penetration in TNF inhibitor classes by 2023, as per the Spanish Society of Rheumatology. This approach freed an estimated €200 million annually for reinvestment in novel monoclonal antibodies targeting interleukin pathways. Spain also leads in home‑based subcutaneous administration programs; data from the Ministry of Health shows that 63% of psoriasis patients self‑inject biologics, reducing hospital congestion. Regional health services in Catalonia and Andalusia have implemented digital treatment passports that track adherence and adverse events in real time. Furthermore, Spain’s participation in the EU Joint Action on Rare Diseases has improved early diagnosis of systemic lupus erythematosus, expanding the treatable population. These pragmatic, efficiency‑driven strategies position Spain as a model for balancing innovation and affordability in a resource‑conscious healthcare system.

COMPETITIVE LANDSCAPE

Competition in the European autoimmune monoclonal antibodies market is characterized by intense innovation, strategic lifecycle management, and deep engagement with regional healthcare frameworks. Established pharmaceutical leaders compete not only on clinical efficacy but also on delivery convenience, health economic value, and integration into national treatment guidelines. The entry of biosimilars has intensified price competition, prompting originator companies to differentiate through next-generation molecules, subcutaneous formulations, and digital adherence ecosystems. Regulatory harmonization across the European Union enables broad commercial reach, yet national reimbursement heterogeneity necessitates country-specific market access strategies. Companies increasingly leverage real-world data from pan-European registries to support payer negotiations and label expansions. Academic collaborations and clinical trial localization further strengthen scientific credibility. With multiple pipeline candidates targeting novel immune pathways such as interferon and JAK STAT, the competitive landscape remains dynamic, balancing therapeutic advancement with cost containment imperatives across diverse European health systems.

KEY MARKET PLAYERS

Companies playing a promising role in the europe autoimmune monoclonal antibodies market include

- GlaxoSmithKline plc (U.K.)

- AstraZeneca plc (U.K.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Bristol-Myers Squibb (U.S.)

- Johnson & Johnson (U.S.)

- Innovent Biologics, Inc. (China)

- Takeda Pharmaceutical Company Ltd. (Japan)

- Amgen Inc. (U.S.)

- Biogen Inc. (U.S.)

- UCB Company (Belgium)

TOP LEADING PLAYERS IN THE MARKET

- Roche maintains a significant presence in the European autoimmune monoclonal antibodies market through its pioneering humanized and human monoclonal antibody platforms. The company’s portfolio includes rituximab, widely used off-label and in approved regimens for autoimmune conditions such as rheumatoid arthritis and pemphigus vulgaris. Roche has intensified its focus on subcutaneous formulations to enhance patient convenience and adherence across European healthcare systems. In recent years, the company expanded its clinical development pipeline by initiating phase three trials for novel anti-CD19 antibodies in lupus nephritis across sites in Germany, France, and Sweden. Roche also strengthened real-world evidence generation through partnerships with European rheumatology registries to support long term safety and effectiveness data, reinforcing physician confidence and regulatory acceptance throughout the region.

- Johnson and Johnson contributes prominently to the European autoimmune monoclonal antibodies market via its Janssen Biotech division, which markets ustekinumab and guselkumab for psoriatic disease and Crohn disease. These fully human monoclonal antibodies target interleukin 12 and interleukin 23 pathways, aligning with Europe’s shift toward precision immunomodulation. The company recently secured expanded European Medicines Agency approval for guselkumab in pediatric psoriasis, broadening its eligible patient base. Johnson and Johnson has also invested in digital adherence tools integrated with self-injection devices, rolled out across the United Kingdom and the Netherlands. Additionally, it collaborates with national health technology assessment bodies to demonstratcost-effectivenessss through long-term disability prevention, ensuring favorable reimbursement positioning across diverse European payer environments.

- Novartis plays a strategic role in the European autoimmune monoclonal antibodies market through its development and commercialization of ofatumumab, a fully human anti-CD20 monoclonal antibody approved for multiple sclerosis. Administered via subcutaneous autoinjector, ofatumumab offers a differentiated patient-centric delivery model that has gained rapid adoption in Sweden, Denmark, and Switzerland. Novartis has reinforced its European footprint by establishing dedicated neurology support hubs that provide nurse-led training and adherence monitoring. The company also initiated the PREVAIL study in 2023 across twelve European countries to evaluate real-world outcomes in early multiple sclerosis treatment. Furthermore, Novartis enhanced manufacturing resilience by expanding its biologics production capacity at its Sandoz facility in Austria, ensuring a reliable supply amid rising demand for self-administered autoimmune biologics.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European autoimmune monoclonal antibodies market prioritize therapeutic differentiation through novel target discovery and next-generation engineering to reduce immunogenicity. They actively pursue regulatory acceleration by engaging early with the European Medicines Agency and national health technology assessment bodies. Companies invest heavily in real-world evidence programs by partnering with national disease registries to validate long term safety and economic value. Strategic expansion of subcutaneous and self-administration formats enhances patient adherence and reduces healthcare system burden. Additionally, firms strengthen supply chain security through regionalized biomanufacturing and cold chain innovations. Collaborations with academic centers drive biomarker research for patient stratification. Payer engagement focuses on demonstrating cost offset via reduced hospitalizations and disability. Lifecycle management includes biosimilar defense through indication expansion and device integration. Digital health tools are embedded to support treatment persistence. These multifaceted strategies collectively reinforce market positioning across Europe’s complex and high-standard healthcare landscape.

MARKET SEGMENTATION

This research report on the europe autoimmune monoclonal antibodies market has been segmented and sub-segmented into the following categories.

By Source

- Murine

- Chimeric

- Humanized

- Human

By Application

- Systemic Lupus Erythematosus

- Rheumatoid Arthritis

- Multiple Sclerosis

- Transplant Rejection/Graft Versus Host Disease

By End-User

- Hospitals/Clinics

- Research Institutes

- Diagnostic Laboratories

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe